マテリアルズ・インフォマティクス 2025-2035市場、戦略、プレーヤーMaterials Informatics 2025-2035: Markets, Strategies, Players 材料科学における設計と発見のためのデータ中心アプローチ。データインフラ、機械学習、AIにおける注目すべき進歩。プレーヤーのプロフィール、技術の進歩、市場の展望、戦略的アプローチ。 マ... もっと見る

サマリー

材料科学における設計と発見のためのデータ中心アプローチ。データインフラ、機械学習、AIにおける注目すべき進歩。プレーヤーのプロフィール、技術の進歩、市場の展望、戦略的アプローチ。

マテリアルズ・インフォマティクス(MI)には、機械学習を含むマテリアルサイエンスのR&Dのためのデータ中心アプローチの適用が含まれる。複数の戦略的アプローチと多くの注目すべき成功事例があり、採用は加速しており、この移行を逃すと大きな代償を払うことになる。

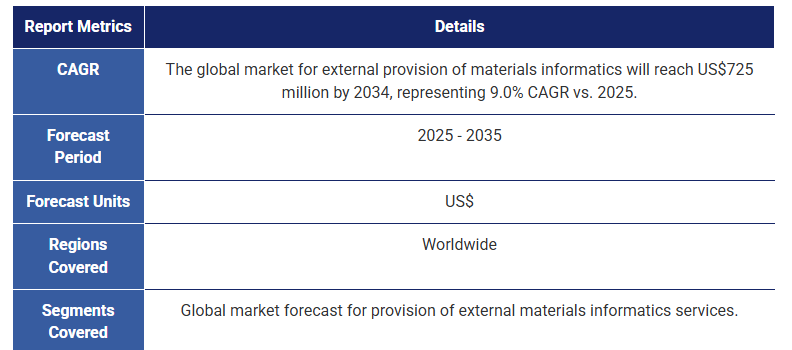

本レポートは、この新興分野における重要な洞察と商業的展望を提供する。この分野の企業25社への一次インタビューに基づいており、読者はこの業界のプレーヤー、ビジネスモデル、テクノロジー、戦略を詳細に理解することができる。MIサービスを提供する企業の収益は2035年まで予測され、それまでの年平均成長率は9.0%と予想される。現在進行中のAIブームの影響も考慮し、材料科学全般にわたる多数の関連プロジェクトを取り上げている。基礎技術の分析により、R&Dにおけるデジタル変革の急成長分野を解明する。

材料インフォマティクスとは?

マテリアルズ・インフォマティクスとは、マテリアルサイエンスの進歩のためにデータ中心のアプローチを用いることである。これは様々な形をとり、R&Dのあらゆる部分(仮説-データ処理・取得-データ分析-知識抽出)に影響を与える。

主に、MIはデータインフラを利用し、新材料の設計、用途に応じた材料の発見、加工方法の最適化のための機械学習ソリューションを活用することに基づいている。

MIは技術革新の "前進 "方向(入力材料に対して特性が実現される)を加速させることができるが、理想的な解決策は "後退 "方向(所望の特性を与えられた材料が設計される)を可能にすることである。

これは一筋縄ではいかず、現在のAI産業革命の規模にもかかわらず、まだ黎明期を脱したばかりである。多くの場合、データ基盤は包括的ではなく、MIアルゴリズムは与えられた実験データに対して未熟すぎることが多い。課題は、他のAI主導の分野(自律走行車やソーシャルメディアなど)と同じではなく、プレーヤーは多くの場合、疎な、高次元の、偏った、ノイズの多いデータを扱っている。

一部の人が信じていることとは逆に、これは研究科学者を置き換えるものではない。正しく統合されれば、MIは、科学者のR&Dプロセスを加速させるとともに、彼らの専門知識を活用する一連のテクノロジーとなるだろう。多くの人にとって、夢の最終ゴールは、人間が自律的な自動運転研究室を監督することである。まだ初期段階であるが、重要な改良がなされ、スピンアウト企業が設立され、サクセスストーリーのすべてがMIの開発によって促進されている。

なぜ今なのか?

これは新しいアプローチではない。多くの分野で何十年もの間、同様の設計アプローチが採用されてきた。しかし、この革新的な技術が今まさに材料科学の分野に影響を与えている主な理由は3つある:

IDTechExは、R&Dプロセスに高度な機械学習技術を採用することで得られる3つの利点を挙げている。それは、候補物質のスクリーニング強化や研究分野の絞り込み、新素材開発のための実験回数の削減(ひいては市場投入までの時間の短縮)、新素材や関係の発見である。トレーニングデータは、社内の実験、計算シミュレーション、および/または社外のデータリポジトリに基づくことができる。強化されたラボのインフォマティクスとハイスループット実験または計算は、多くのプロジェクトに不可欠である。

本レポートでは、MIにおける機械学習の主要な進展、成功事例、そしてエンドユーザーがどのように機械学習に積極的に取り組んでいるかについて考察する。

戦略的アプローチとは?

このR&Dの変遷を無視することは、材料を設計したり、材料を使って設計したりする企業にとって大きな見落としである。これは、競争力のある製品を市場に投入する場合、サプライチェーンにおける汎用性を開発する場合、次世代の機会を見つける場合、事業部門や材料ポートフォリオを多様化する能力を生み出す場合などが考えられる。

すでに多くの企業が、完全に自社で運営する、外部企業と協力する、コンソーシアムの一員として力を合わせるという3つの中核的アプローチで、この採用を開始している。これらの各アプローチは、報告書の中で詳細に評価されている。MIの採用を開始することを選択することは重要であり、正しい道を選択することが不可欠である。

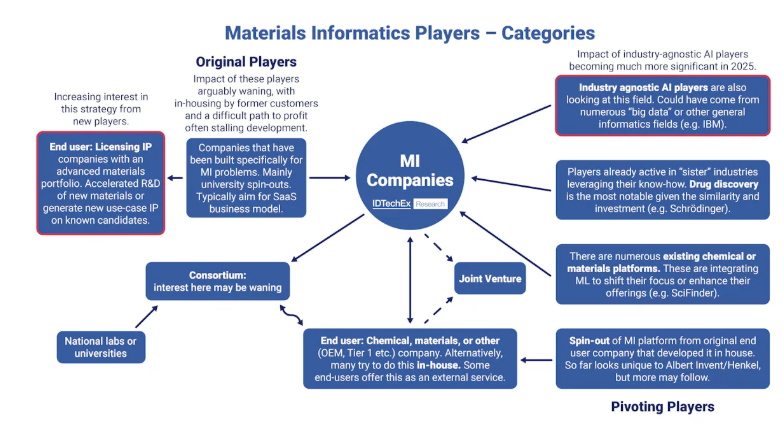

外部のMIプレーヤーは、下図に概略を示すように、多くの出発点から来ることができる。MIプレーヤーには、強力な先端材料ポートフォリオを持つライセンシング企業になるという選択肢もあり、またエンドユーザーがサービスとしてMIを提供するという選択肢もある。地理的には、この技術を採用しているエンドユーザーの多くは日本企業であり、新興の外部企業の多くは米国企業である。

このIDTechExレポートには、多くの主要企業のインタビューベースのプロフィールが含まれている。

主要な側面

本レポートは以下の情報を提供している

技術動向:

企業分析:

アプリケーションと市場展望

目次

1. エグゼクティブサマリー

1.1. マテリアル・インフォマティクスとは?

1.2. マテリアル・インフォマティクス: 2025年の業界の現状

1.3. 材料設計と開発の各段階でのAIの機会

1.4. 材料科学データの問題点

1.5. 探索的な機械学習ワークフロー

1.6. MIアルゴリズムの種類 - 教師あり学習 vs 教師なし学習

1.7. 基盤モデルとマテリアル・インフォマティクス

1.8. 科学におけるLLM(大規模言語モデル)の能力

1.9. MIにおけるアルゴリズムアプローチの多様性

1.10. マテリアル・インフォマティクスのプレイヤー - カテゴリ

1.11. 戦略的アプローチに対する結論と展望: エンドユーザー向けアプローチ(I)

1.12. 戦略的アプローチに対する結論と展望: エンドユーザー向けアプローチ(II)

1.13. MIエンドユーザーにとって、万能のアプローチは存在しない

1.14. 特定の外部プロバイダーの重要なパートナーと顧客

1.15. 民間企業による資金調達(I): 内部開発による高い資本需要

1.16. 民間企業による資金調達(II): SaaSビジネスモデルへの信頼は薄れているのか?

1.17. Lila Sciences: 現時点での最大の資金調達

1.18. 主要な業界プレイヤー(I): 設立されたリーダー

1.19. 主要な業界プレイヤー(II): 有望な挑戦者

1.20. 主要なMIプレイヤー: 利益化への道を歩んでいるか?

1.21. 外部MI企業の市場展望

1.22. 注目すべきMIコンソーシアム

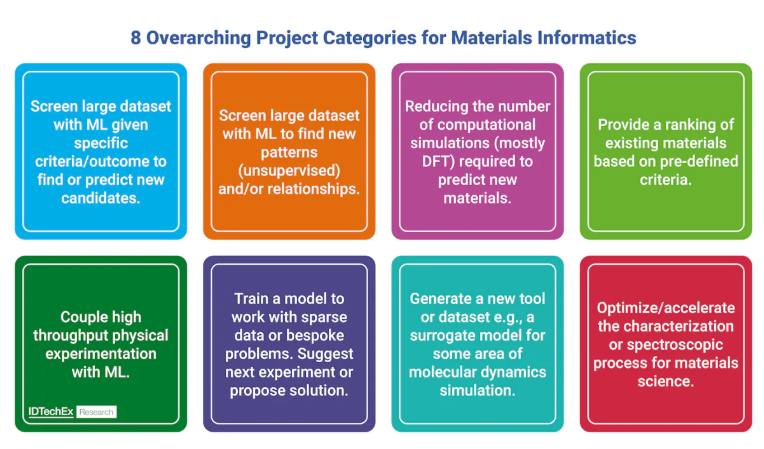

1.23. MIにおけるプロジェクトカテゴリ

1.24. 応用の進展

1.25. マテリアル・インフォマティクスのロードマップ

1.26. 市場予測: 外部マテリアル・インフォマティクス企業

2. はじめに

2.1. マテリアル・インフォマティクスとは?

2.2. マテリアル・インフォマティクス - なぜ今なのか?

2.3. マテリアル・インフォマティクス - カテゴリの定義

2.4. 科学と工学における広範なインフォマティクス領域

2.5. マテリアル・インフォマティクスにおける主要な課題

2.6. 従来の合成アプローチのループを閉じる

2.7. 高スループット仮想スクリーニング(HTVS)

2.8. 化学および材料科学におけるMLの利点 - 加速

2.9. 化学および材料科学におけるMLの利点 - スコーピングとスクリーニング

2.10. 化学および材料科学におけるMLの利点 - スコーピングとスクリーニング(2)

2.11. 化学および材料科学におけるMLの利点 - 新しい種と関係

2.12. 化学および材料科学のデータインフラ

2.13. ELN/LIMSソフトウェアとマテリアル・インフォマティクス

2.14. マテリアル・インフォマティクスの価値の証明

3. 技術評価

3.1. はじめに

3.1.1. マテリアル・インフォマティクスアルゴリズムの入力と出力

3.1.2. マテリアル・インフォマティクスに必要なもの

3.1.3. 技術アプローチの概要

3.1.4. 実験データの不確実性が分析を妨げる

3.1.5. QSARおよびQSPR: 構造と性質の関連付け

3.2. MIアルゴリズム

3.2.1. MIアルゴリズムの概要

3.2.2. 材料科学データの問題点

3.2.3. 探索的機械学習ワークフロー

3.2.4. 記述子とモデルの学習

3.2.5. コンピュータに材料を記述する(I)

3.2.6. コンピュータに材料を記述する(II)

3.2.7. MIアルゴリズムの種類 - 教師あり学習 vs 教師なし学習

3.2.8. 教師あり学習と教師なし学習の問題クラス

3.2.9. 強化学習: 試行錯誤による学習

3.2.10. 自動特徴選択

3.2.11. 利用か探求か: 既知の情報を活用するか、それとも新しい領域を探索するか?

3.2.12. 純粋な探索とε-greedyポリシー

3.2.13. アクティブラーニングとMI: 改善を最大化する実験の選択

3.2.14. 教師あり学習モデル: 「より高度」であることが常に良いわけではない

3.2.15. ベイズ最適化: 機械学習の多目的ツール

3.2.16. 遺伝的アルゴリズム: 自然選択の模倣

3.2.17. 教師なし学習事例研究 - フェーズのマッピング

3.2.18. 深層学習: 脳の模倣

3.2.19. 深層学習: ニューラルネットワークの種類

3.2.20. ニューラルネットワークの特徴付けと計算

3.2.21. 生成的アルゴリズム vs 判別的アルゴリズム - 説明 vs ラベリング

3.2.22. 「生成的AI」と生成的アルゴリズムの違い

3.2.23. マテリアル・インフォマティクスにおける生成的アルゴリズムの事例研究

3.2.24. 深層学習: MIの事例

3.2.25. 物理インフォームド・ニューラルネットワーク(PINNs)による材料開発

3.2.26. マテリアル・インフォマティクスにおけるPINNの応用

3.2.27. 無機化合物の生成的モデル(I)

3.2.28. 無機化合物の生成的モデル(II):生成的敵対ネットワーク

3.2.29. トランスフォーマーモデルはAIブームの中心

3.2.30. 基盤モデルとマテリアル・インフォマティクス

3.2.31. マテリアル・インフォマティクスにおける基盤モデル: 実験データ

3.2.32. データの可用性と計算費用が基盤モデルの導入を妨げる

3.2.33. 大規模言語モデル(LLMs)と材料研究開発

3.2.34. 科学におけるLLMの能力

3.2.35. 材料科学におけるタスクベースの機械学習の難しさ

3.2.36. 小さな材料データセットとどのように協力するか

3.2.37. 小さな材料データセットによる深層学習: 事例(I)

3.2.38. 小さな材料データセットによる深層学習: 事例(II)

3.2.39. AutoML: 機械学習の民主化

3.2.40. マルチモデルアンサンブル: 複数の予測手法を組み合わせる

3.2.41. 概要: MIにおけるアルゴリズムアプローチは多様である

3.3. データインフラの確立

3.3.1. データインフラはMIにとって重要である

3.3.2. 化学および材料科学に特化した開発

3.3.3. ELN/LIMS、マテリアル・インフォマティクス、およびR&Dプロセスの管理

3.4. 外部データベース

3.4.1. データリポジトリ - 組織

3.4.2. データリポジトリの活用

3.4.3. ChemDataExtractor V1.0: 出版物と特許のデータマイニング

3.4.4. ChemDataExtractor V2.0: 関連データのマイニング

3.4.5. 重要な情報の注釈と抽出: 商業スペース

3.4.6. LLMsがマテリアルデータマイニングの能力を拡張する

3.5. 計算材料科学とMI

3.5.1. 化学および材料科学R&Dのためのシミュレーション

3.5.2. 密度汎関数理論(DFT) - CAMDのための量子力学的モデリング

3.5.3. 代理モデルが原子スケールのシミュレーションの計算コストを削減する

3.5.4. 長さスケールの連続体を超えた物質のシミュレーション: マルチスケールモデリング

3.5.5. ICMEと機械学習の役割

3.5.6. ICME: なぜ重要なのか?

3.5.7. QuesTek InnovationsとICME: サービスからSaaSへ

3.5.8. Thermo-CalcとCompuTherm: ICMEソフトウェア提供とQuesTekの協力

3.5.9. クラウドベースのシミュレーションを活用した探索的設計

3.5.10. 量子コンピュータの活用の可能性

3.5.11. 材料発見のための計算自律性

3.5.12. ビッグテック、計算材料科学、そしてマテリアル・インフォマティクス

3.5.13. 概要: シミュレーションデータはMIプロセスへの重要な入力である

3.6. 物理実験および特性評価によるMI

3.6.1. 高い量の物理実験データの取得

3.6.2. 高い量の物理実験データの取得(2)

3.6.3. イン・シチュスペクトロスコピーの進展

3.6.4. 材料の高スループットスクリーニングが他の科学分野より難しい理由

3.7. 自律型ラボ

3.7.1. 未来 - 完全自律型ラボ

3.7.2. 未来 - 「Chemputer」

3.7.3. DeepMatterと「Chemputer」

3.7.4. ラボ自動化のためのワークフロー管理

3.7.5. 自律型高スループット実験

3.7.6. 商業化された自動運転ラボ

3.7.7. Gearu: モバイル自律型ロボティックサイエンティストの商業化を目指す

3.7.8. 逆合成からロボット実行まで

3.7.9. 化学自律性のための技術的柱

4. 業界分析

4.1. マテリアル・インフォマティクス:2025年の業界の状況

4.2. マテリアル・インフォマティクスへの戦略的アプローチ

4.2.1. マテリアル・インフォマティクスのプレーヤー - カテゴリー

4.2.2. 戦略的アプローチの結論と展望:エンドユーザー向けアプローチ(I)

4.2.3. 戦略的アプローチの結論と展望:エンドユーザー向けアプローチ(II)

4.2.4. 戦略的アプローチの結論と展望:外部マテリアル・インフォマティクス企業向けアプローチ(I)

4.2.5. 戦略的アプローチの結論と展望:外部マテリアル・インフォマティクス企業向けアプローチ(II)

4.3. プレーヤー分析

4.3.1. マテリアル・インフォマティクスのプレーヤー - 概要

4.3.2. 選定された外部提供者の主要パートナーおよび顧客

4.3.3. エンジニアリングシミュレーションソフトウェアとの提携

4.3.4. 民間企業が調達した資金(I):社内開発は高い資本要求を伴う

4.3.5. 民間企業が調達した資金(II):SaaSビジネスモデルへの信頼は薄れつつあるのか?

4.3.6. Lila Sciences:これまでで最大の資金調達

4.3.7. NobleAI:MI、Microsoft、AIブーム、クラウドマーケットプレイス

4.3.8. 主な業界プレーヤー(I):確立されたリーダー

4.3.9. 主な業界プレーヤー(II):有望な挑戦者

4.3.10. 主要なMIプレーヤー:利益を上げる道を歩んでいるか

4.3.11. MI SaaSプラットフォームの価格設定

4.3.12. MIにおけるSaaSビジネスモデルのリスク

4.3.13. MI SaaSプレーヤーの利益への障壁は何か

4.3.14. MicrosoftのAzure Quantum Elements:小規模MIプレーヤーにとっての厳しい競争

4.3.15. Azure Quantum Elementsの応用

4.3.16. マテリアル・インフォマティクスの社内導入

4.3.17. 社内オペレーションをサービスとして提供

4.3.18. オペレーションを社内に取り入れるためには最初に何を行う必要があるか?

4.3.19. Enthought:科学/エンジニアリングR&Dのデジタルトランスフォーメーション

4.3.20. Resonac/昭和電工 - 外部の関与から社内MI戦略へ?

4.3.21. 逆合成予測:「この化合物は作れるか?」

4.3.22. 商業的な逆合成予測ツール

4.3.23. 注目すべきMIコンソーシアム(1) - NIMSおよびMaterials Open Platforms

4.3.24. 注目すべきMIコンソーシアム(2) - AIST Data-Driven Consortium

4.3.25. 注目すべきMIコンソーシアム(3) - トヨタ研究所および大学とのコラボレーション

4.3.26. 注目すべきMIコンソーシアム(4) - The Global Acceleration Network

4.3.27. 過去の注目すべきMIコンソーシアム(1) - IBMとのコラボレーション

4.3.28. 過去の注目すべきMIコンソーシアム(2) - CHiMaDおよびCMDネットワーク

4.3.29. 公共と民間の共同協力

4.3.30. Open Catalyst Project:MIのクラウドソーシング

4.3.31. Materials Genome Initiative(MGI)

4.3.32. Materials Genome Engineering(MGE)またはNational Materials Genome Project(中国)

4.3.33. 世界中のその他の主要イニシアティブおよび研究センター(1)

4.3.34. 世界中のその他の主要イニシアティブおよび研究センター(2)

4.3.35. 結論:MIのエンドユーザーにとって、ワンサイズ・フィット・オールのアプローチはない

4.4. マテリアル・インフォマティクスの応用

4.4.1. マテリアル・インフォマティクスのプロジェクトカテゴリー

4.4.2. 応用の進展

4.4.3. マテリアル・インフォマティクスのロードマップ

4.5. 市場予測と展望

4.5.1. 市場予測:外部マテリアル・インフォマティクスプレーヤー

4.5.2. 予測データと市場展望

4.6. MI業界のプレーヤーデータ

4.6.1. MIプレーヤーのリスト

4.6.2. 完全なプレーヤーリスト - 商業企業(運営確認済み)(1)

4.6.3. 完全なプレーヤーリスト - 商業企業(運営確認済み)(2)

4.6.4. 完全なプレーヤーリスト - 商業企業(運営確認済み)(3)

4.6.5. 完全なプレーヤーリスト - 商業企業(運営確認済み)(4)

4.6.6. 完全なプレーヤーリスト - 商業企業(運営確認済み)(5)

4.6.7. 完全なプレーヤーリスト - 商業企業(運営確認済み)(6)

4.6.8. 完全なプレーヤーリスト - 商業企業(運営確認済み)(7)

4.6.9. 完全なプレーヤーリスト - 業界離脱者(可能性ありおよび確認済み)

4.6.10. プレーヤーリスト - 公的組織(I)

4.6.11. プレーヤーリスト - 公的組織(II)

5. 企業プロフィール

5.1. アルバート・インベント(Albert Invent)

5.2. アルケミー・クラウド(Alchemy Cloud)

5.3. アンツァッツAI(Ansatz AI)

5.4. シトリナ・インフォマティクス(Citrine Informatics)

5.5. シトリナ・インフォマティクス(Citrine Informatics)

5.6. シトリナ・インフォマティクス:アップデート(Citrine Informatics: Update)

5.7. コペルニック・カタリスツ(Copernic Catalysts)

5.8. シノラ(Cynora)

5.9. ドゥニア・イノベーションズ(Dunia Innovations)

5.10. エリックス株式会社(Elix, Inc.)

5.11. エクソマター(ExoMatter)

5.12. エクスポネンシャル・テクノロジーズ(Exponential Technologies)

5.13. フェルマン・マテリアルズX(FEHRMANN MaterialsX)

5.14. フルエンス・アナリティクス(Fluence Analytics)

5.15. インテリジェンス(Intellegens)

5.16. ケボティクス(Kebotix)

5.17. ケボティクス(Kebotix)

5.18. キュルックス(Kyulux)

5.19. LG AIリサーチ(LG AI Research)

5.20. マテリアルズ・ゾーン(Materials Zone)

5.21. マテリアルズ・ゾーン(Materials Zone)

5.22. マテリアルズイン(materialsIn)

5.23. マテリアルズゾーン(MaterialsZone)

5.24. マットメライズ(Matmerize)

5.25. メタマテリアル・テクノロジーズ(Metamaterial Technologies)

5.26. ノーブルAI(NobleAI)

5.27. OTIルミオニクス(OTI Lumionics)

5.28. フェーズシフト・テクノロジーズ(Phaseshift Technologies)

5.29. ポリマライズ(Polymerize)

5.30. プレフェアード・コンピュータショナル・ケミストリー(PFCC)/マットランティス(Matlantis)

5.31. プレフェアード・コンピュータショナル・ケミストリー(PFCC)/マットランティス(MATLANTIS):2025年初更新(Early 2025 Update)

5.32. クエステック・イノベーションズ(QuesTek Innovations LLC)

5.33. シュレーディンガー(Schrödinger)

5.34. ストイケイア(Stoicheia)

5.35. アンカウンタブル(Uncountable)

5.36. アンカウンタブル(Uncountable)

5.37. エクシンテラ(Xinterra)

Summary

Data-centric approaches for design and discovery within materials science. Notable advancements in data infrastructures, machine learning, and AI. Player profiles, technology progression, market outlook, strategic approaches.

Materials informatics (MI) involves applying data-centric approaches for materials science R&D, including machine learning. There are multiple strategic approaches and many notable success stories; adoption is accelerating and missing this transition will be costly.

This report provides key insights and commercial outlooks for this emerging field. Built upon primary interviews with 25 companies in the field, readers will get a detailed understanding of the players, business models, technology, and strategies in this industry. The revenue of firms offering MI services is forecast to 2035, with 9.0% CAGR expected until then. The impact of the ongoing AI boom is considered and numerous relevant projects across materials science are covered. Analysis of the underlying technologies demystifies this fast-growing area of digital transformation in R&D.

What is materials informatics?

Materials informatics is the use of data-centric approaches for the advancement of materials science. This can take numerous forms and influence all parts of R&D (hypothesis - data handling & acquisition - data analysis - knowledge extraction).

Primarily, MI is based on using data infrastructures and leveraging machine learning solutions for the design of new materials, discovery of materials for a given application, and optimization of how they are processed.

MI can accelerate the "forward" direction of innovation (properties are realized for an input material) but the idealized solution is to enable the "inverse" direction (materials are designed given desired properties).

This is not straightforward and, despite the scale of the current AI industrial revolution, is still emerging from its nascent stage. In many cases, the data infrastructure is not comprehensive and MI algorithms are often too immature for the given experimental data. The challenge is not the same as in other AI-led areas (such as autonomous cars or social media), the players are often dealing with sparse, high-dimensional, biased, and noisy data; leveraging domain knowledge is an essential part of most approaches.

Contrary to what some may believe, this is not something that will displace research scientists. If integrated correctly, MI will become a set of enabling technologies accelerating scientists' R&D processes whilst making use of their domain expertise. For many, the dream end-goal is for humans to oversee an autonomous self-driving laboratory; although still at an early-stage there have been key improvements, spin-out companies formed, and success stories all facilitated by MI developments.

Why now?

This is not a new approach; many sectors have adopted similar design approaches for decades. But there are three main reasons why this transformative technology is impacting the materials science space right now:

IDTechEx has identified three repeated advantages to employing advanced machine learning techniques into your R&D process: enhanced screening of candidates & scoping research areas, reducing the number of experiments to develop a new material (and therefore time to market), and finding new materials or relationships. The training data can be based on internal experimental, computational simulation and/or from external data repositories; enhanced laboratory informatics and high throughput experimentation or computation can be integral to many projects.

This report looks at the key progressions in machine learning for MI, the success stories, and how end-users are actively engaging with this.

What are the strategic approaches?

Ignoring this R&D transition is a major oversight for any company that designs materials or designs with materials: awareness of the potential significant missed opportunities in the mid- to long-term is growing rapidly. This could be when bringing competitive products to market, developing versatility in the supply chain, finding next-generation opportunities, or generating the ability to diversify a business unit or material portfolio.

Numerous players have already begun this adoption with three core approaches: operate fully in-house, work with an external company, or join forces as part of a consortium. Each of these approaches is appraised in detail in the report; choosing to start the adoption of MI is important, choosing the right path is essential.

The external MI players can come from numerous starting points, as outlined in the figure below. There is also the option for MI players to become a licensing company with a strong advanced material portfolio and also for end-users to offer MI as a service. Geographically, many of the end-users embracing this technology are Japanese companies, many of the emerging external companies are from USA, and the most notable consortia and academic labs are split across Japan and the USA.

Interview based profiles of many key companies are included within this IDTechEx report.

Key Aspects

This report provides the following information

Technology Trends:

Company Analysis:

Applications and Market Outlook

Table of Contents1. EXECUTIVE SUMMARY

1.1. What is materials informatics?

1.2. Materials Informatics: the state of the industry in 2025

1.3. AI opportunities at every stage of materials design and development

1.4. Problems with materials science data

1.5. Exploratory machine learning workflow

1.6. Types of MI algorithms - Supervised vs unsupervised

1.7. Foundation models and materials informatics

1.8. Capabilities of LLMs in science

1.9. Algorithmic approaches in MI are diverse

1.10. Materials informatics players - categories

1.11. Conclusions and outlook for strategic approaches: approaches for end-users (I)

1.12. Conclusions and outlook for strategic approaches: approaches for end-users (II)

1.13. For MI end-users, there is no one-size-fits-all approach

1.14. Key Partners and Customers of Selected External Providers

1.15. Funding raised by private companies (I): in-house development leads to high capital requirements

1.16. Funding raised by private companies (II): is faith in SaaS business models waning?

1.17. Lila Sciences: the largest funding raise in MI to date

1.18. Main industry players (I): Established leaders

1.19. Main industry players (II): Promising challengers

1.20. Major MI players: on a path to profitability?

1.21. Market outlook for external MI companies

1.22. Notable MI consortia

1.23. Project categories in MI

1.24. Application Progression

1.25. Materials informatics roadmap

1.26. Market forecast: external materials informatics players

2. INTRODUCTION

2.1. What is materials informatics?

2.2. Materials informatics - Why now?

2.3. Materials Informatics - Category definitions

2.4. The broader informatics space in science and engineering

2.5. Key challenges for MI across the full materials spectrum

2.6. Closing the loop on traditional synthetic approaches

2.7. High Throughput Virtual Screening (HTVS)

2.8. Advantages of ML for chemistry and materials science - Acceleration

2.9. Advantages of ML for chemistry and materials science - Scoping and screening

2.10. Advantages of ML for chemistry and materials science - Scoping and screening (2)

2.11. Advantages of ML for chemistry and materials science - New species and relationships

2.12. Data infrastructures for chemistry and materials science

2.13. ELN/LIMS Software and Materials Informatics

2.14. Proving the value of materials informatics

3. TECHNOLOGY ASSESSMENT

3.1. Introduction

3.1.1. Inputs and outputs of materials informatics algorithms

3.1.2. What is needed for materials informatics?

3.1.3. Summary of technology approaches

3.1.4. Uncertainty in experimental data undermines analysis

3.1.5. QSAR and QSPR: relating structure to properties

3.2. MI algorithms

3.2.1. Overview of MI algorithms

3.2.2. Problems with materials science data

3.2.3. Exploratory machine learning workflow

3.2.4. Descriptors and training a model

3.2.5. Describing materials to a computer (I)

3.2.6. Describing materials to a computer (II)

3.2.7. Types of MI algorithms - Supervised vs unsupervised

3.2.8. Problem classes in supervised and unsupervised learning

3.2.9. Reinforcement learning: Learning by trial and error

3.2.10. Automated feature selection

3.2.11. Exploitation vs exploration: Use what you know or look into new areas?

3.2.12. Pure exploitation vs epsilon-greedy policies in materials informatics

3.2.13. Active learning and MI: Choosing experiments to maximize improvement

3.2.14. Supervised learning models: "More sophisticated" is not always better

3.2.15. Bayesian optimization: A versatile tool in machine learning

3.2.16. Genetic algorithms: Mimicking natural selection

3.2.17. Unsupervised learning case study - Mapping phases

3.2.18. Deep learning: Imitating the brain

3.2.19. Deep learning: Types of neural network

3.2.20. Characterizing and computing neural networks

3.2.21. Generative vs discriminative algorithms - Explaining vs labelling

3.2.22. "Generative AI" is distinct from generative algorithms

3.2.23. Generative algorithms in materials informatics: case study

3.2.24. Deep learning: An example in MI

3.2.25. Physics-Informed Neural Networks (PINNs) in material development

3.2.26. PINN applications in materials informatics

3.2.27. Generative models for inorganic compounds (I)

3.2.28. Generative models for inorganic compounds (II): Generative adversarial networks

3.2.29. Transformer models are at the core of the AI boom

3.2.30. Foundation models and materials informatics

3.2.31. Foundation models in materials informatics: experimental data

3.2.32. Data availability and computational expense hold back foundation model deployment

3.2.33. Large Language Models (LLMs) and Materials R&D

3.2.34. Capabilities of LLMs in science

3.2.35. Task-based machine learning is harder to avoid in materials science than many areas of machine learning interest

3.2.36. How to work with small material datasets

3.2.37. Deep learning with small material datasets: examples (I)

3.2.38. Deep learning with small material datasets: examples (II)

3.2.39. AutoML: democratizing machine learning

3.2.40. Multi-model ensembles: combining multiple predictive methodologies

3.2.41. Summary: Algorithmic approaches in MI are diverse

3.3. Establishing a data infrastructure

3.3.1. A data infrastructure is critical for MI

3.3.2. Developments targeted for chemical and materials science

3.3.3. ELN/LIMS, materials informatics and managing R&D processes

3.4. External databases

3.4.1. Data repositories - Organizations

3.4.2. Leveraging data repositories

3.4.3. ChemDataExtractor V1.0: Data mining publications and patents

3.4.4. ChemDataExtractor V2.0: Mining relational data

3.4.5. Annotating and extracting the relevant information: The commercial space

3.4.6. LLMs expand material data mining capabilities

3.5. MI with computational materials science

3.5.1. Simulations for chemistry and materials science R&D

3.5.2. Density functional theory (DFT) - Quantum mechanical modelling for CAMD

3.5.3. Surrogate models reduce the computational expense of atomistic simulation

3.5.4. Simulating matter across the length scale continuum: multiscale modelling

3.5.5. ICME and the role of machine learning

3.5.6. ICME: Why is it important?

3.5.7. QuesTek Innovations and ICME: from service to SaaS

3.5.8. Thermo-Calc and CompuTherm: ICME software provision and QuesTek collaboration

3.5.9. Explorative design utilizing cloud-based simulation

3.5.10. The potential in leveraging quantum computing

3.5.11. Computation autonomy for materials discovery

3.5.12. Big Tech, computational materials science and materials informatics

3.5.13. Summary: simulation data is an important input to MI processes

3.6. MI with physical experiments and characterization

3.6.1. Achieving high-volumes of physical experimental data

3.6.2. Achieving high-volumes of physical experimental data (2)

3.6.3. In-situ spectroscopy developments

3.6.4. Why is high throughput screening in materials tougher than other areas of science?

3.7. Autonomous labs

3.7.1. The future - fully autonomous labs

3.7.2. The future - "Chemputer"

3.7.3. DeepMatter and the Chemputer

3.7.4. Workflow management for laboratory automation

3.7.5. Autonomous high throughput experimentation

3.7.6. Commercial self-driving-laboratories

3.7.7. Gearu: attempting to commercialize mobile autonomous robotic scientists

3.7.8. Retrosynthesis through to robot execution

3.7.9. Technology pillars for chemical autonomy

4. INDUSTRY ANALYSIS

4.1. Materials Informatics: the state of the industry in 2025

4.2. Strategic approaches to MI

4.2.1. Materials informatics players - categories

4.2.2. Conclusions and outlook for strategic approaches: approaches for end-users (I)

4.2.3. Conclusions and outlook for strategic approaches: approaches for end-users (II)

4.2.4. Conclusions and outlook for strategic approaches; approaches for external materials informatics companies (I)

4.2.5. Conclusions and outlook for strategic approaches; approaches for external materials informatics companies (II)

4.3. Player analysis

4.3.1. Materials informatics players - overview

4.3.2. Key Partners and Customers of Selected External Providers

4.3.3. Partnerships with engineering simulation software

4.3.4. Funding raised by private companies (I): in-house development leads to high capital requirements

4.3.5. Funding raised by private companies (II): is faith in SaaS business models waning?

4.3.6. Lila Sciences: the largest funding raise in MI to date

4.3.7. NobleAI: MI, Microsoft, the AI boom and cloud marketplaces

4.3.8. Main industry players (I): Established leaders

4.3.9. Main industry players (II): Promising challengers

4.3.10. Major MI players: on a path to profitability?

4.3.11. Pricing MI SaaS platforms

4.3.12. Risks for SaaS business models in MI

4.3.13. What are the barriers to profitability for MI SaaS players?

4.3.14. Microsoft's Azure Quantum Elements: stiff competition for smaller MI players

4.3.15. Applications of Azure Quantum Elements

4.3.16. Taking materials informatics in-house

4.3.17. Offering in-housed operations as a service

4.3.18. Taking the operation in-house: What needs to happen first?

4.3.19. Enthought: Digital transformation in scientific/engineering R&D

4.3.20. Resonac/Showa Denko - from external engagements to in-housed MI strategy?

4.3.21. Retrosynthesis prediction: "Can I make this compound?"

4.3.22. Commercial retrosynthesis predictors

4.3.23. Notable MI consortia (1) - NIMS and Materials Open Platforms

4.3.24. Notable MI consortia (2) - AIST Data-Driven Consortium

4.3.25. Notable MI consortia (3) - Toyota Research Institute and university collaboration

4.3.26. Notable MI consortia (4) - The Global Acceleration Network

4.3.27. Notable past MI consortia (1) - IBM collaborations

4.3.28. Notable past MI consortia (2): CHiMaD and the CMD Network

4.3.29. Public-private collaborations

4.3.30. The Open Catalyst Project: Crowdsourcing MI

4.3.31. Materials Genome Initiative (MGI)

4.3.32. Materials Genome Engineering (MGE) or National Materials Genome Project (China)

4.3.33. Additional key initiatives and research centers around the world (1)

4.3.34. Additional key initiatives and research centers around the world (2)

4.3.35. Conclusion: for MI end-users, there is no one-size-fits-all approach

4.4. Applications of materials informatics

4.4.1. Project categories in MI

4.4.2. Application Progression

4.4.3. Materials informatics roadmap

4.5. Market forecast and outlook

4.5.1. Market forecast: external materials informatics players

4.5.2. Forecast data and market outlook

4.6. MI industry player data

4.6.1. Lists of MI players

4.6.2. Full player list - Commercial companies (confirmed operational) (1)

4.6.3. Full player list - Commercial companies (confirmed operational) (2)

4.6.4. Full player list - Commercial companies (confirmed operational) (3)

4.6.5. Full player list - Commercial companies (confirmed operational) (4)

4.6.6. Full player list - Commercial companies (confirmed operational) (5)

4.6.7. Full player list - Commercial companies (confirmed operational) (6)

4.6.8. Full player list - Commercial companies (confirmed operational) (7)

4.6.9. Full player list - Industry leavers (likely and confirmed)

4.6.10. Player list - Public organizations (I)

4.6.11. Player list - Public organizations (II)

5. COMPANY PROFILES

5.1. Albert Invent

5.2. Alchemy Cloud

5.3. Ansatz AI

5.4. Citrine Informatics

5.5. Citrine Informatics

5.6. Citrine Informatics: Update

5.7. Copernic Catalysts

5.8. Cynora

5.9. Dunia Innovations

5.10. Elix, Inc.

5.11. ExoMatter

5.12. Exponential Technologies

5.13. FEHRMANN MaterialsX

5.14. Fluence Analytics

5.15. Intellegens

5.16. Kebotix

5.17. Kebotix

5.18. Kyulux

5.19. LG AI Research

5.20. Materials Zone

5.21. Materials Zone

5.22. materialsIn

5.23. MaterialsZone

5.24. Matmerize

5.25. Metamaterial Technologies

5.26. NobleAI

5.27. OTI Lumionics

5.28. Phaseshift Technologies

5.29. Polymerize

5.30. Preferred Computational Chemistry (PFCC)/Matlantis

5.31. Preferred Computational Chemistry (PFCC)/MATLANTIS: Early 2025 Update

5.32. QuesTek Innovations LLC

5.33. Schrödinger

5.34. Stoicheia

5.35. Uncountable

5.36. Uncountable

5.37. Xinterra

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(半導体)の最新刊レポート

IDTechEx社の 半導体、コンピュータ、AI - Semiconductors, Computing & AI分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|