電気自動車用パワーエレクトロニクス 2026-2036年:技術、市場、予測Power Electronics for Electric Vehicles 2026-2036: Technologies, Markets, and Forecasts インバータ、車載充電器、DC-DCコンバータを含む、2026-2036年のパワーエレクトロニクス予測をUS$とGWでカバー。Si IGBTとSiC MOSFETのサプライチェーン分析。自動車用 GaN 企業と統合パワーエレクトロニクス... もっと見る

サマリー

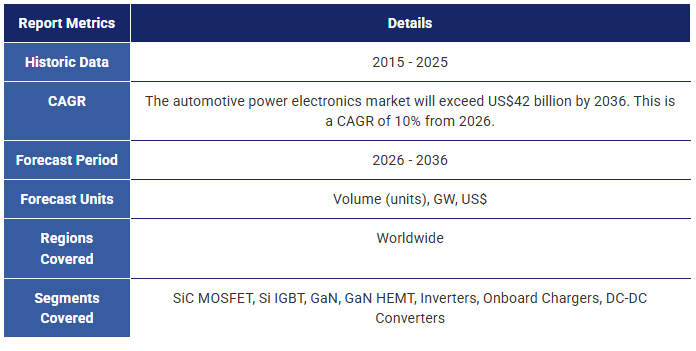

インバータ、車載充電器、DC-DCコンバータを含む、2026-2036年のパワーエレクトロニクス予測をUS$とGWでカバー。Si IGBTとSiC MOSFETのサプライチェーン分析。自動車用 GaN 企業と統合パワーエレクトロニクス。

電気自動車(EV)の需要は今後10年間で急速に伸び、EV用パワーエレクトロニクス市場はさらに急成長する。内燃機関と比較してバッテリー電気自動車(BEV)に対する消費者の懸念に対処するため、自動車OEMは航続距離を延ばし、充電を高速化する方法を模索している。バッテリーやモーター技術とは別に、ワイドバンドギャップ(WBG)半導体、炭化ケイ素(SiC)、窒化ガリウム(GaN)は、800Vアーキテクチャと大幅な効率向上により、既存のシリコン(Si)IGBTやMOSFETに取って代わり、EVパワートレインに革命をもたらす可能性を秘めている。

IDTechExのレポート「電気自動車向けパワーエレクトロニクス 2026-2036」は、SiC MOSFETの急速な微細化から、EVパワーエレクトロニクス市場で確固たる地位を築くGaNの可能性まで、WBG技術の成長の可能性と将来動向を分析している。インバータ、車載充電器(OBC)、DC-DCコンバータを電圧別(600V、1200V)、半導体技術別(Si、SiC、GaN)に区分し、販売台数、電力(GW)、市場規模(US$)を詳細に予測しています。

SiCのサプライチェーン

SiCは、原材料からウェハー、加工技術、デバイス・パッケージに至るまで、確立されたサプライチェーンを持っている。しかし、これはSiCサプライチェーンに発展の余地がないことを意味するものではない。SiCウェハーの供給は、以前は米国企業が独占していた分野であり、OEMは供給とコストを保証するためにSiCのマルチソース化を模索している。昨年、多くの中国企業がSiCウェハー市場に参入し、200mmウェハーの生産を拡大している。150mmから200mmへのSiCウェーハの移行は、自動車産業にとって不可欠な生産能力を大幅に向上させる。さらに、SiCサプライチェーンのグローバル化も推進されており、欧州やアジアの企業がウェハー事業の規模を拡大している。

SiC MOSFETは、過去5年間で価格が大幅に低下したにもかかわらず、Si IGBTよりも高価なままである。これは、インフラ要件、SiCウェーハの価格がはるかに高いこと、エネルギー集約的な処理工程によるものである。IDTechExのレポートでは、EVにSiC MOSFETを実装するためのコスト分析を行い、デバイスレベルと車両レベルの両方における影響を検証している。大手半導体メーカーやTier-1サプライヤー、BYDやメルセデスなどの自動車OEMは、サプライチェーン管理(原材料、インゴット、ウェーハ加工、パッケージング、システム設計)を強化するために垂直統合を開始している。OEMはパワートレインを最大限に活用するため、自動車用半導体サプライヤーと協力している。

EV市場におけるSiC MOSFETの採用

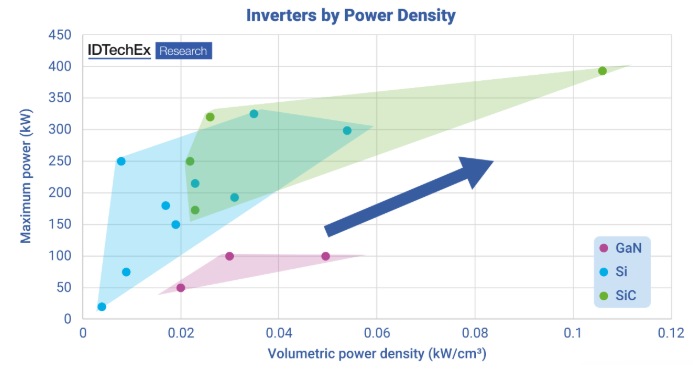

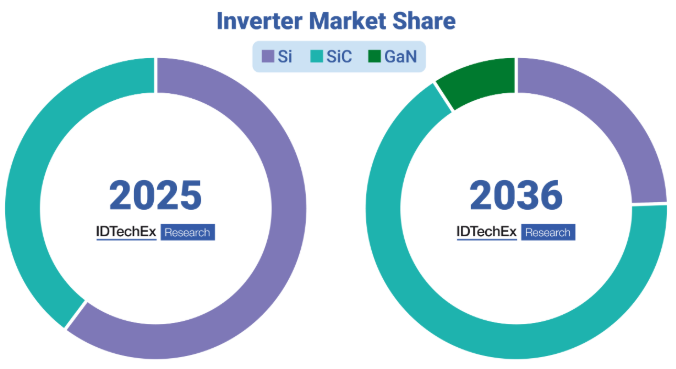

Si IGBTは20年来、トラクション・インバータの唯一の選択肢であり、車載充電器とDC-DCコンバータにはSi MOSFETとダイオードが用いられてきた。しかし、現世代のEVはSiC MOSFETに移行しつつあり、市場シェアは拡大し続け、2035年にはSiC MOSFETがEVインバータ市場の大半を占めるとIDTechExは予測している。SiC MOSFETは、Si IGBTと比較して、高温動作、より高い熱伝導性、EVの航続距離を7%向上させる可能性のある5倍のスイッチング速度、重量と体積を節約するための20%小型のダイと小型の一般的なフォームファクターなど、いくつかの望ましい特徴を提供する。パッケージングからトレンチ技術に至るまで、SiC MOSFET技術の開発は、サプライチェーン、熱管理、信頼性に対する懸念に取り組むため、過去10年間で大幅に改善された。SiC MOSFETとサプライチェーン分析の詳細については、「電気自動車用パワーエレクトロニクス 2026-2036」を参照されたい。

OBCとDC-DCコンバータは、インバータよりも1桁低い電力で動作するが、SiC MOSFETの利点は変わらない:高い電力密度、損失の低減、車両航続距離のわずかな増加。さらに、OBCのSiCはより高速な充電を可能にし、DC-DCコンバーターでは低電圧バッテリーにより効率的に電力を伝達するため、EVの補助電力を必要とする機器(インフォテインメント、パワーステアリング、ヘッドライト)の無駄を省くことができる。このため、OBC や DC-DC コンバータに SiC MOSFET が採用されることになり、要求される電力が低いことから、IDTechEx では、GaN がインバータよりも早くこの市場に参入すると予測している。

車載用 GaN 技術

GaN HEMT と FET は車載用半導体市場で役割を担っている。この役割の程度は、SiCよりも効率的に電力を変換できる材料の可能性を最大限に引き出すために必要な特定の開発次第である。現在、市場に出回っているほとんどのGaNデバイスは650Vに制限されており、構造も横並びである。車載用GaNの可能性を最大化するためには、特に800Vアーキテクチャが主流のEV分野でシェアを拡大するにつれて、より高い電圧で実現可能にするための措置を講じる必要がある。IDTechExは、エンジニアリング技術の改善を通じてであれ、デバイスレベルでの改善であれ、GaNが自動車産業でその可能性を実現する方法を分析している。GaN-on-Siデバイスの代替品についても調査し、企業についても分析している。IDTechExの調査「電気自動車向けパワーエレクトロニクス 2026-2036」には、EV向けパワーエレクトロニクスにおけるGaNの10年予測が含まれており、OBCとDC-DCコンバータで大きな前進が期待され、インバータはその後に続く。

パワーエレクトロニクスの革新

デバイスレベルでの継続的な改良が続く一方で、OEMとティアワン・サプライヤーはEVの性能向上にも注力している。主な目標は、受動部品の配線サイズとコストの削減、および最も効果的な冷却方法の理解である。パワートレイン内のパワーエレクトロニクスの統合は、EVにとって重要な成長分野であり、コストを最小限に抑えながら性能を最大化することを目指している。IDTechExでは、この分野で利用可能な市場ソリューションと能動部品を調査している。統合の程度は、機械的統合から電子的統合まで幅広く、すべてのパワーエレクトロニクスを単一ユニットに統合する可能性もある。その他の技術革新としては、ハイブリッドスイッチインバーター、シングルステージオンボードチャージャー、高電圧バッテリーに直接統合されたパワーエレクトロニクスの採用などがある。

主要な側面

本レポートは以下の主要情報を提供する:

目次1.エグゼクティブ・サマリー

1.1.レポートの紹介

1.2.電気自動車のパワーエレクトロニクス

1.3.シリコン、シリコンカーバイド、窒化ガリウム半導体のベンチマーク

1.4.インバータにおける GaN 対 SiC の可能性

1.5.Si、SiC、GaNのIDTechExインバータ・ベンチマーク

1.6.成長する車載用GaNデバイス・サプライヤー

1.7.GaNのさまざまなアプリケーションの進展

1.8.200mm SiCウェハーの世界生産

1.9.垂直統合:買収と提携

1.10.SiCのインバータコストへの影響

1.11.Si IGBTとSiC MOSFETの価格比較

1.12.自動車OEMとサプライヤーのSiC MOSFET - 主要OEM (1)

1.13.主要OEMのSi IGBTサプライヤー (1)

1.14.SiCドライブ800Vプラットフォーム

1.15.400V DC充電の互換性を確保する方法

1.16.800V充電速度

1.17.800VプラットフォームSiCおよびSi IGBTインバータ

1.18.800VプラットフォームSiC/Si IGBTインバータ(2)

1.19.パワーエレクトロニクスの統合

1.20.DC-DCコンバータ内蔵OBC

1.21.トラクション統合型車載充電器

1.22.片面冷却と両面冷却の比較

1.23.インバータ市場シェア 2023-2036年:GaN 600V、Si IGBT 600V、SiC MOSFET 600V、1200V

1.24.インバーター予測 2023-2036年 (GW):GaN 600V、Si IGBT 600V、SiC MOSFET 600V、1200V

1.25.OBC予測:Si、SiC、GaN 2023-2036年 (GW)

1.26.DC-DCコンバーターの予測:Si、SiC、GaN 2023-2036年 (GW)

1.27.インバーター、OBC、DC-DCコンバータの予測 2023-2036年 (GW)

1.28.インバータ、OBC、DC-DCコンバータの予測 2023-2036年 (US$ billion)

2.電気自動車市場:地域動向と将来の成長

2.1.電気自動車の定義

2.2.電気自動車:代表的な仕様

2.3.地域別電気自動車市場の指数関数的成長

2.4.地域別動向:米国2024年

2.5.地域別動向:中国 2024年

2.6.地域別動向欧州 2024年

2.7.欧州の規制 - 概要

2.8.EUの排出量と目標

2.9.ハイブリッド車販売のピーク

2.10.パワートレインのテールパイプ排出量の比較

2.11.自動車-総所有コスト

2.12.チップ不足 - 2020年から2023年

2.13.チップ不足 - 自動車メーカーの反応

2.14.チップ不足 - 電気自動車

3.電気自動車用パワーエレクトロニクスとWBG半導体の概要

3.1.導入とベンチマーク Si、SiC、GaN

3.1.1.パワーエレクトロニクスとは?

3.1.2.電気自動車におけるパワーエレクトロニクス

3.1.3.トランジスタの歴史とMOSFETの概要

3.1.4.ワイドバンドギャップ(WBG)半導体の利点と欠点

3.1.5.シリコン、シリコンカーバイド、窒化ガリウム半導体のベンチマーク

3.1.6.スイッチング損失:Si vs SiC vs GaN

3.1.7.インバータ、OBC、DC-DC コンバータ

3.1.8.SiC材料の利点

3.1.9.Si IGBT と SiC MOSFET の価格比較

3.1.10.SiCとGaNデバイスのコスト比較

3.1.11.SiC パワー・デバイスの限界

3.1.12.高電圧へのGaNの可能性

3.1.13.Qromisが設計したGaNパワー用基板:QST

3.1.14.SiCとGaNには大きな改善の余地がある

3.1.15.GaNは望ましいOBC技術となる

3.1.16.OBCへのGaNの実装方法

3.1.17.GaN システムの車載充電器

3.1.18.GaNデバイスの課題

3.1.19.SiCパワー・ロードマップ

3.1.20.WBGデバイスのアプリケーション・サマリー

3.2.GaN企業

3.2.1.成長する車載用GaNデバイスサプライヤー

3.2.2.GaNの様々なアプリケーションの進展

3.2.3.GaNはどの基板で普及するか?

3.2.4.エンハンスメントモードとデプレッションモード

3.2.5.GaNシステム

3.2.6.テキサス・インスツルメンツとSTマイクロエレクトロニクス

3.2.7.ルネサス(トランスフォーム)

3.2.8.VisIC Technologies

3.2.9.エフィシェント・パワー・コンバージョン

3.2.10.ネクスペリア

3.2.11.インバータにおける GaN 対 SiC の可能性

3.2.12.リカルド:自動車市場におけるGaN

3.2.13.イノサイエンス

3.2.14.パワーインテグレーションズ

3.2.15.イノバンス・オートモーティブGaN

3.2.16.UAES CharCON HyperGaN

3.2.17.GaN OBCのコスト削減と体積削減

3.2.18.PCIM 2025:車載充電器の動向

3.2.19.その他の GaN 企業:Qromis、QPT、BelGaN、Cambridge GaN Devices、Odyssey Semiconductor

3.2.20.NXP インバーター予測

3.2.21.シングルステージOBC

3.2.22.OBC の現状

3.2.23.OBCにおけるGaN:予測を上回る

3.2.24.インバーターの現状

3.2.25.上海電気駆動:GaN インバーター

3.3.インバータ、OBC、コンバータ設計と Si、SiC、GaN の展望

3.3.1.インバータ、OBC、コンバータ設計と Si、SiC、GaN の展望

3.3.2.インバータの概要

3.3.3.パルス幅変調

3.3.4.従来のEVインバータ

3.3.5.ディスクリート&モジュール

3.3.6.インバータ・プリント基板

3.3.7.インバータ部品とコスト

3.3.8.電気自動車インバータ・ベンチマーク

3.3.9.電気自動車インバータ・ベンチマーク 2

3.3.10.インバータ・パッケージへのSiCの影響

3.3.11.IDTechEx インバーターベンチマーキング

3.3.12.インバーター予測 2023-2036年 (GW):GaN 600V、Si IGBT 600V、SiC MOSFET 600V、1200V

3.3.13.OBC の予測:Si、SiC、GaN 2023-2036年 (GW)

3.3.14.DC-DC コンバータの予測:Si、SiC、GaN 2023-2036年 (GW)

3.3.15.車載充電器の回路部品

3.3.16.テスラ車載充電器/DC-DCコンバータ

3.3.17.レベル別 OBC:4kW、6~11.5kW、16~22kW 2020-2036年

4.ワイドバンドギャップ半導体製造チェーン

4.1.SiC製造

4.1.1.はじめに

4.1.2.Si IGBT 製造:原材料から EV まで

4.1.3.SiC MOSFET製造:原材料からEVまで

4.1.4.SiC専用装置

4.1.5.150mmから200mmへ:潜在的なコスト優位性

4.1.6.200mm ウェハーのダイカウントの優位性

4.1.7.200mmウェハーの世界生産

4.1.8.2025:8インチSiCウェハーへの移行は続く

4.1.9.垂直統合:買収と提携

4.1.10.デンソーSiC結晶成長の高速化に向けた研究開発

4.1.11.シルテクトラ:冷間分割技術

4.1.12.SOITECのSmartSiC技術

4.1.13.SmartSiCの優位性のまとめ

4.1.14.住友金属鉱山SiCkrest

4.1.15.住友金属鉱山SiCkrest (2)

4.2.GaN 製造

4.2.1.GaNはどの基板が主流か?

4.2.2.TSMC、GaNファウンドリー事業から撤退

4.2.3.GaN vs Si:ダイから車載レベルまで

4.2.4.プロセスのエネルギー需要:Si vs GaN

5.パワーエレクトロニクスに影響を与えるトレンド

5.1.はじめに

5.1.1.パワーエレクトロニクスの効率改善

5.1.2.効率と熱利得、800V

5.1.3.自動車産業における SiC の例

5.2.SiCと800V

5.2.1.SiCドライブ800Vプラットフォーム

5.2.2.800Vの充電速度

5.2.3.GMCハマー800Vアーキテクチャを使用しない800V充電

5.2.4.その他のスプリット・バッテリー・パック車:テスラ、ポルシェ、フォード

5.2.5.テスラ・サイバートラック800V アーキテクチャーによる分割バッテリー

5.2.6.ポルシェ・テイカンブースト・コンバーター

5.2.7.Preh - 800V EV向け充電技術

5.2.8.400V SiCプラットフォーム

5.2.9.800V プラットフォーム SiC および Si IGBT インバータ

5.2.10.800VプラットフォームSiCおよびSi IGBTインバータ(2)

5.2.11.800V 2023年

5.2.12.800V 2024-2025年

5.2.13.中国における800Vモデルの発表(2022~2025年)

5.2.14.800Vの賛否

5.2.15.DCFCのリチウムイオンセルへの影響

5.2.16.急速充電セルの設計階層-引くべきレバー

5.2.17.DC急速充電レベル

5.2.18.800Vプラットフォームの議論と展望

5.2.19.ハイブリッド・スイッチ・インバータ

5.2.20.ハイブリッド・スイッチ・インバータ

5.2.21.GaNを解き放つ3レベル・インバータ

5.3.パワーエレクトロニクスの統合

5.3.1.さまざまなレベルの統合

5.3.2.サプライチェーンが鍵

5.3.3.ビテスコとルノー:高電圧ボックスとワンボックス

5.3.4.DC-DCコンバーター付き統合OBC

5.3.5.プレ・コンボ・ユニット

5.3.6.ルノー ゾーイ43kW AC充電

5.3.7.トラクション車載一体型充電器

5.3.8.トラクションiOBCサプライヤー

5.3.9.現代 E-GMP:800V、SiC、パワーエレクトロニクスの統合

5.3.10.ボルグワーナーインバータと DC-DC コンバータの統合

5.3.11.NXP インバータ予測

5.4.Si IGBT と SiC MOSFET の混載

5.4.1.インバータコストへのSiCの影響

5.4.2.SiC MOSFETとSi IGBTの比較:車両全体のコスト

5.4.3.Si IGBTとSiC MOSFETの価格比較

5.4.4.SiCダイオード車載充電器

5.4.5.SiCダイオードインバーター

5.4.6.その他のハイブリッドSiCサプライヤー

5.4.7.NXPインバータ予測

5.5.その他の動向

5.5.1.パワーエレクトロニクスの動向:デュアル・インバータ

5.5.2.デュアル・インバータとパワーモジュールの熱管理

5.5.3.パワーエレクトロニクスとしてのバッテリー

5.5.4.ポルシェ

6.パワー半導体材料、デバイス、OEM のサプライチェーン

6.1.SiC MOSFET と Si IGBT のサプライヤー

6.1.1.供給動向:インフィニオン

6.1.2.供給動向STマイクロエレクトロニクス

6.1.3.供給動向:ウルフスピード

6.1.4.供給動向:ローム

6.1.5.供給動向:オンセミ

6.1.6.自動車OEMおよびサプライヤーのSiC MOSFET - 主要OEM (1)

6.1.7.自動車OEMとサプライヤーのSiC MOSFET - 新興OEM

6.1.8.大手OEM向けSi IGBTサプライヤー

6.1.9.新興OEM向けSi IGBTサプライヤー

6.1.10.新しい SiC 製造センター

6.2.デバイス・サプライヤー

6.2.1.インフィニオンのCoolSiC効率向上

6.2.2.インフィニオン、主要OEMパートナーシップを確立

6.2.3.インフィニオンの設計勝利

6.2.4.ローム半導体、SiC生産能力を拡大

6.2.5.ローム:OEMおよびティアオンとのSiCパートナーシップ

6.2.6.STMicroelectronics、ACEPACKをリリース 市場リーダーとしての競争へ

6.2.7.EVパワーエレクトロニクス向けSTマイクロのポートフォリオ

6.2.8.ウルフスピード:SiCへの大規模投資とOEMパートナーシップ

6.2.9.オンセミ EliteSiC

6.2.10.ナビタスGeneSiC

6.2.11.GeneSiCとそのトレンチアシストプレーナーコンフィギュレーションのベンチマーク

6.2.12.Qorvo

6.2.13.Qorvo SiC FETとSiC MOSFETの比較

6.2.14.トレンチ対プレーナー

6.3.ティア1サプライヤー

6.3.1.デルファイ・テクノロジーズ、高級自動車メーカーにViper SiCモジュールを供給

6.3.2.ボルグワーナー

6.3.3.ボルグワーナー、フォード向け統合ドライブモジュール

6.3.4.ボルグワーナーの設計が勝利

6.3.5.ダナ

6.3.6.バイテスコ

6.3.7.ビテスコパワーエレクトロニクス製品

6.3.8.ビテスコ・シェフラー合併

6.3.9.エキップメイク

6.3.10.LGマグナ

6.3.11.日立の両面IGBTが大手OEMに

6.3.12.コンチネンタル/ジャガー・ランドローバー

6.3.13.ヘリックスCTI-4:ロータス・エビア

6.3.14.モーション・アプライド(旧マクラーレン・アプライド) IPG5-x

6.4.自動車 OEM

6.4.1.現代自動車、ベストセラー800V E-GMPプラットフォーム向けにSiC供給を多様化

6.4.2.GM ボルト&ボルトからウルティウムへ

6.4.3.ボルボの大型SiCインバータ

6.4.4.メルセデス 自社開発

7.パワーエレクトロニクスパッケージ:EVの使用例

7.1.トヨタ・プリウス 2004-2010年

7.2.2008 レクサス

7.3.ホンダ・アコード 2014年

7.4.トヨタ・プリウス 2010-2015年

7.5.日産リーフ 2012年

7.6.ホンダ フィット(by 三菱)

7.7.トヨタ プリウス 2016年以降

7.8.キャデラック 2016(日立製)

7.9.シボレー・ボルト2016年(デルファイ社製)

7.10.BMW i3 (by Infineon)

7.11.JAC iEV4

7.12.中国NEV、インフィニオンを採用

7.13.華晨新利

7.14.テスラ・モデルX:SiCの前にインフィニオンのIGBT

7.15.800V Si IGBT IGBTの選択

7.16.ポルシェ・テイカン

7.17.日産アリヤ2021

7.18.ジャガーI-PACE

7.19.ジャガーI-PACEパワーモジュールと冷却

7.20.武陵紅光ミニEV

7.21.ダンフォス

7.22.リビアンR1T

7.23.レクサスRZ

7.24.フォード F-150 ライトニング

7.25.BYD Atto 3(2022年):8-in-1パワートレイン

7.26.BMW iX3

7.27.テスラ・サイバートラック

7.28.STMicro

8.EV パワーエレクトロニクスの熱管理

8.1.はじめに

8.1.1.パワーエレクトロニクスにおける熱管理戦略 (1)

8.1.2.パワーエレクトロニクスにおける熱管理戦略 (2)

8.1.3.トランジスタの歴史とMOSFETの概要-熱管理への影響

8.1.4.冷却アプローチのまとめ - (1)

8.1.5.冷却アプローチのまとめ - (2)

8.2.パワーエレクトリックにおけるTIM1とTIM2

8.2.1.EV パワーエレクトロニクスのどこで TIM が使用されているか

8.2.2.フリップチップパッケージにおける TIM1

8.2.3.TIM1としてのはんだ

8.2.4.はんだオプションとダイ・アタッチ電流

8.2.5.ダイ・アタッチ・ソリューション-熱伝導率の比較

8.2.6.焼結化の傾向

8.2.7.銀焼結ペースト

8.2.8.金属焼結ペーストのサプライヤー

8.2.9.はんだ合金と焼結ペーストの特性と性能

8.2.10.TIM2 - IDTechExの有望なTIM2に関する分析

8.2.11.TIM の年間市場規模予測(百万米ドル):2024-2034

8.3.液冷 - シングルサイドとダブルサイド

8.3.1.片面、両面、インダイレクト、ダイレクト冷却

8.3.2.片面冷却の主な概要

8.3.3.片面冷却の利点と欠点

8.3.4.TIM2 面積は片面冷却でもほぼ同じ

8.3.5. onsemi - EliteSiC パワーモジュール

8.3.6.ST マイクロエレクトロニクス - Tesla Model 3

8.3.7.両面冷却(DSC)の主なまとめ

8.3.8.両面冷却の紹介

8.3.9.両面冷却の例

8.3.10.パワーモジュールにおける両面冷却の必要性

8.3.11.インフィニオンのHybridPACK DSC

8.3.12.HybridPACK DSC の内部構造

8.3.13. onsemi - VE-Trac ファミリー・モジュール

8.3.14.CRRC

8.3.15.日立インバータ - 両面冷却

8.3.16.BYD 1500V SiC - 両面 Ag 焼結

8.3.17.車載用両面冷却の動向

8.3.18.両面液冷への移行

8.3.19.片面冷却と両面冷却の市場シェア:2024-2034

9.大型車用パワーエレクトロニクス

9.1.1.トラックは資本財である

9.1.2.乗用車用パワーエレクトロニクスと大型車用パワーエレクトロニクスの違い

9.1.3.大型BEVのトルクとピークパワーの比較

9.1.4.PowerizeD

9.1.5.大型トラック用高電圧パワートレイン

9.1.6.DC400V 充電の互換性を確保する方法

9.1.7.MCSの仕様と比較

9.1.8.800Vは大型トラックにとってより理にかなっている

9.1.9.低電力用途の電力変換

9.1.10.電気トラック用車載充電器

9.1.11.大型車用インバーター

9.2.大型 BEV サプライヤー

9.2.1.日立ロードパック

9.2.2.BAE システムズ

9.2.3.BAE and Eaton Commercial Demonstrator 2024

9.2.4.カミンズのアクセラ

9.2.5.Accelera (Cummins)

10.予測

10.1.地域EV市場の指数関数的成長

10.2.方法論

10.3.2022~2036年の1台当たりインバーター予測

10.4.地域別 10.5:地域別

10.5.1台当たりの複数モーター/インバーター

10.6.インバーター予測 2023-2036年 (GW):GaN 600V、Si IGBT 600V、SiC MOSFET 600V、1200V

10.7.インバータ市場シェア 2023-2036年:GaN 600V、Si IGBT 600V、SiC MOSFET 600V、1200V

10.8.インバーター液冷戦略予測(単位):2015-2036年

10.9.インバーター用ディスクリート対パワーモジュールの予測 2023-2036 年

10.10.OBC の予測:Si、SiC、GaN 2023-2036年 (GW)

10.11.DC-DC コンバータの予測:Si、SiC、GaN 2023-2036年 (GW)

10.12.インバーター、OBC、DC-DCコンバーターの予測 2023-2036年 (GW)

10.13.インバーター、OBC、DC-DCコンバーターの販売台数予測 2023-2036年

10.14.インバータ、OBC、DC-DCコンバータの予測 2023-2036年 (US$ billion)

10.15.レベル別OBC:4kW, 6-11.5kW, 16-22kW 2020-2036年

10.16.インバータ、OBC & コンバータ、Si、SiC、GaN コスト想定(kW あたり米ドル)

11.プロファイル

11.1.アドバンスト・エレクトリック・マシーンズ社

11.2.Arteco: EV 専用水-グリコール冷却剤

11.3.BMW

11.4.BYD オート

11.5.ダイヤモンドファウンドリー電気自動車用インバーター

11.6.ダイネックス・セミコンダクター(CRRC):EV パワーエレクトロニクス

11.7.効率的な電力変換:GaN FET

11.8.効率的な電力変換:車載用GaN

11.9.エラフェ駆動サイクル効率を高めるインホイールモーター

11.10.Equipmake:電気モーターとパワーエレクトロニクス

11.11.GaNシステム

11.12.ゼネラルモーターズ(2020年)

11.13.ヘレウスEVパワーエレクトロニクス用ソリューション

11.14.ヒュンダイE-GMP 800Vプラットフォームの成功

11.15.インフィニオン: 車載充電器用750V SiC MOSFET

11.16.インフィニオン車載パワーエレクトロニクス

11.17.インフィニオンSiC OEM パートナーシップの拡大

11.18.インテグラルeドライブ

11.19.ロータス

11.20.ルーシッド・モーターズ

11.21.マグナ・インターナショナル

11.22.マクラーレン・オートモーティブ

11.23.ネクスペリアEVパワーエレクトロニクス用GaN

11.24.NXPセミコンダクターズ

11.25.QPT:MHzスイッチング、アクティブ冷却GaN

11.26.Rivian: 電気乗用車

11.27.ローム半導体ルーシッドモーターへの供給

11.28.STマイクロエレクトロニクスSiCの優位性とサプライチェーン

11.29.テスラ(2019年最新情報)

11.30.トランスフォーム

11.31.ヴァレオ(48Vパワートレイン)

11.32.ウルフスピード

11.33.ウルフスピード:主なSiC供給案件

Summary

Covering Power Electronics forecasts in US$ and GW for 2026-2036, including the inverter, onboard charger, and DC-DC converter. Supply chain analysis of Si IGBTs and SiC MOSFETs. Automotive GaN companies and integrated Power Electronics.

The demand for electric vehicles (EVs) will grow rapidly over the next decade, and the EV power electronics market will grow even faster. To tackle consumer concerns about battery electric vehicles (BEVs) compared to internal combustion engines, automotive OEMs are looking for ways to increase range and speed up charging. Aside from battery and motor technologies, wide bandgap (WBG) semiconductors, silicon carbide (SiC), and gallium nitride (GaN), have the potential to revolutionize EV powertrains in displacing the incumbent silicon (Si) IGBTs and MOSFETs with 800V architectures and significant efficiency gains.

IDTechEx's report "Power Electronics for Electric Vehicles 2026-2036" analyzes the growth potential and future trends in WBG technologies, from the rapid scaling of SiC MOSFETs to the potential of GaN to consolidate itself in the EV power electronics market. The report includes granular forecasts detailing unit sales, power (GW), and market size (US$) demand segmented by inverters, onboard chargers (OBC), and DC-DC converters by voltage (600V, 1200V) and semiconductor technology (Si, SiC, GaN).

SiC supply chain

SiC has an established supply chain from raw materials to wafers, to processing technologies to device packaging. This, however, doesn't mean that there isn't room for development in the SiC supply chain. SiC wafer supply is an area previously dominated by US companies, and OEMs are looking to multisource their SiC to guarantee supply and cost. A number of Chinese players have entered the SiC wafer market in the past year and are scaling up 200mm wafer production. The transition from 150mm to 200mm SiC wafers will significantly increase production capacity, which is vital for the automotive industry. Furthermore, there is a push to globalize the SiC supply chain, with companies in Europe and Asia scaling up wafer operations.

SiC MOSFETs will continue to be more expensive than Si IGBTs, despite significant reductions in prices over the past 5 years. This is due to infrastructure requirements, the much higher price of SiC wafers, and energy-intensive processing steps. IDTechEx's report carries out a cost analysis of implementing SiC MOSFETs in EVs, examining the impact at both the device and vehicle levels. Leading semiconductor and tier-1 suppliers, as well as automotive OEMs, such as BYD and Mercedes, have started vertical integration to strengthen their supply chain control (raw materials, ingot, wafer processing, packaging, and system design). OEMs are collaborating with automotive semiconductor suppliers to get the most out of their powertrains.

SiC MOSFET adoption in the EV market

Si IGBTs have been the singular option for the traction inverter for 20 years, accompanied by Si MOSFETs and diodes for the onboard charger and DC-DC converter. They have proven to be reliable at the medium-high power levels for the inverter, yet current generation EVs are transitioning to SiC MOSFETs, and ramping in market share will continue to grow, with IDTechEx predicting that SiC MOSFETs will be the majority of the EV inverter market by 2035. Compared with Si IGBTs, SiC MOSFETs offer several desirable features, including high-temperature operation, higher thermal conductivity, 5 times faster switching speeds potentially increasing EV ranges by 7%, and a 20% smaller die and smaller general form factor for weight and volume savings. Development in SiC MOSFET technology, from packaging to trench technologies has improved massively over the past 10 years, to tackle concerns over the supply chain, thermal management, and reliability. More information on the SiC MOSFETs and supply chain analysis can be found in "Power Electronics for Electric Vehicles 2026-2036".

OBCs and DC-DC converters operate at powers an order of magnitude lower than inverters, yet the advantages of SiC MOSFET persist: higher power density, a reduction in losses, and a slight increase in vehicle range. Moreover, SiC in the OBC allows for faster charging, and in the DC-DC converter, transfers power more efficiently to the low voltage battery, making the auxiliary power-hungry devices in an EV (infotainment, power steering, headlights) less wasteful. This drives SiC MOSFET adoption in the OBC and DC-DC converters, and the lower power requirements mean that IDTechEx predicts GaN to enter this market earlier than for inverters.

GaN Technologies for Automotive

GaN HEMTs and FETs have a role in the automotive semiconductor market. The extent of this role depends on certain developments needed to maximize the potential of a material that can convert power more efficiently than SiC. Currently, most GaN devices on the market are limited to 650V and are lateral in construction. To maximize the potential of automotive GaN, steps need to be taken to make it feasible at higher voltages, especially as 800V architectures gain market share in the mainstream EV sector. Whether through improvements in engineering technology or at the device level, IDTechEx analyzes ways that GaN can realize its potential in the automotive industry. Alternatives to GaN-on-Si devices are investigated, and companies analyzed. IDTechEx's research "Power Electronics for Electric Vehicles 2026-2036" includes a 10-year forecast of GaN in power electronics for EVs, expecting significant headway for OBCs and DC-DC converters, with inverters to follow later.

Power Electronics Innovations

While ongoing improvements at the device level continue, OEMs and tier-one suppliers also focus on enhancing EV performance. Key goals include reductions in wiring size and costs of the passive components, as well as understanding the most effective cooling methods. The integration of power electronics within the powertrain represents a key growth area for EVs, aiming to maximize performance while minimizing cost. IDTechEx examines available market solutions and active components in this space. The degree of integration varies widely, ranging from mechanical integration to electronic integration, with the potential to consolidate all power electronics into a single unit. Other innovations include the adoption of hybrid switch inverters, single-stage onboard chargers, and power electronics integrated directly into the high voltage battery.

Key Aspects

This report provides the following key information:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Report Introduction

1.2. Power Electronics in Electric Vehicles

1.3. Benchmarking Silicon, Silicon Carbide & Gallium Nitride Semiconductors

1.4. GaN vs SiC Potential in the Inverter

1.5. IDTechEx Inverter Benchmarking For Si, SiC, and GaN

1.6. Automotive GaN Device Suppliers are Growing

1.7. Progress of Different Applications of GaN

1.8. 200mm SiC Wafer Production Worldwide

1.9. Vertical Integration: Acquisitions and Collaborations

1.10. SiC Impact on the Inverter Cost

1.11. Si IGBT and SiC MOSFET Price Comparison

1.12. SiC MOSFET by Automotive OEMs and Suppliers - Leading OEMs (1)

1.13. Si IGBT Suppliers to Leading OEMs (1)

1.14. SiC Drives 800V Platforms

1.15. Ways to have 400V DC Charging Compatibility

1.16. 800V Charging Speeds

1.17. 800V Platforms SiC and Si IGBT Inverters

1.18. 800V Platforms SiC and Si IGBT Inverters (2)

1.19. Integration of Power Electronics

1.20. Integrated OBC with DC-DC converter

1.21. Traction Integrated Onboard Charger

1.22. Comparison of Single-Sided Cooling and Double-Sided Cooling

1.23. Inverter Market Share 2023-2036: GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V

1.24. Inverter Forecast 2023-2036 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V

1.25. OBC Forecast: Si, SiC, GaN 2023-2036 (GW)

1.26. DC-DC Converter Forecast: Si, SiC, GaN 2023-2036 (GW)

1.27. Inverter, OBC, DC-DC Converter Forecast 2023-2036 (GW)

1.28. Inverter, OBC, DC-DC Converter Forecast 2023-2036 (US$ billion)

2. ELECTRIC VEHICLE MARKETS: REGIONAL TRENDS AND FUTURE GROWTH

2.1. Electric Vehicle Definitions

2.2. Electric Vehicles: Typical Specs

2.3. Exponential Growth in Regional EV Markets

2.4. Regional Trends: US 2024

2.5. Regional Trends: China 2024

2.6. Regional Trends: Europe 2024

2.7. Europe Regulations - Overview

2.8. EU Emissions and Targets

2.9. Hybrid Car Sales Peak

2.10. Powertrain Tailpipe Emissions Comparison

2.11. Cars - Total Cost of Ownership

2.12. Chip Shortages - 2020 to 2023

2.13. Chip Shortages - Automaker Reactions

2.14. Chip Shortages - Electric Vehicles

3. OVERVIEW OF EV POWER ELECTRONICS AND WBG SEMICONDUCTORS

3.1. Introduction and Benchmarking Si, SiC and GaN

3.1.1. What is Power Electronics?

3.1.2. Power Electronics Use in Electric Vehicles

3.1.3. Transistor History & MOSFET Overview

3.1.4. Wide Bandgap (WBG) Semiconductor Advantages & Disadvantages

3.1.5. Benchmarking Silicon, Silicon Carbide & Gallium Nitride Semiconductors

3.1.6. Switching Losses: Si vs SiC vs GaN

3.1.7. Inverter, OBC, DC-DC converter

3.1.8. Advantages of SiC Material

3.1.9. Si IGBT and SiC MOSFET Price Comparison

3.1.10. SiC and GaN Device Cost Comparison

3.1.11. Limitations of SiC Power Devices

3.1.12. GaN's Potential to Reach High Voltage

3.1.13. Qromis Engineered Substrate for GaN Power: QST

3.1.14. SiC & GaN have Substantial Room for Improvement

3.1.15. GaN to Become Preferred OBC Technology

3.1.16. How GaN is implemented into an OBC

3.1.17. GaN Systems' Onboard Charger

3.1.18. Challenges for GaN Devices

3.1.19. SiC Power Roadmap

3.1.20. Applications Summary for WBG Devices

3.2. GaN Companies

3.2.1. Automotive GaN Device Suppliers are Growing

3.2.2. Progress of Different Applications of GaN

3.2.3. Which Substrate will Prevail for GaN?

3.2.4. Enhancement Mode vs Depletion Mode

3.2.5. GaN Systems

3.2.6. Texas Instruments and STMicroelectronics

3.2.7. Renesas (Transphorm)

3.2.8. VisIC Technologies

3.2.9. Efficient Power Conversion

3.2.10. Nexperia

3.2.11. GaN vs SiC potential in the Inverter

3.2.12. Ricardo: GaN in the Automotive Market

3.2.13. Innoscience

3.2.14. Power Integrations

3.2.15. Inovance Automotive: GaN

3.2.16. UAES CharCON HyperGaN

3.2.17. Cost and Volume Reductions of a GaN OBC

3.2.18. PCIM 2025: Onboard Charger Trends

3.2.19. Other GaN Companies: Qromis, QPT, BelGaN, Cambridge GaN Devices, Odyssey Semiconductor

3.2.20. NXP Inverter Predictions

3.2.21. Single Stage OBCs

3.2.22. Current Landscape for OBCs

3.2.23. GaN in OBCs: Ahead of Forecasts

3.2.24. Current Inverter Landscape

3.2.25. Shanghai Electric Drive: GaN Inverter

3.3. Inverter, OBC, Converter Design & Si, SiC, GaN Outlook

3.3.1. Inverter, OBC, Converter Design & Si, SiC, GaN Outlook

3.3.2. Inverter Overview

3.3.3. Pulse Width Modulation

3.3.4. Traditional EV Inverter

3.3.5. Discretes & Modules

3.3.6. Inverter Printed Circuit Boards

3.3.7. Inverter Components and Cost

3.3.8. Electric Vehicle Inverter Benchmarking

3.3.9. Electric Vehicle Inverter Benchmarking 2

3.3.10. SiC Impact on the Inverter Package

3.3.11. IDTechEx Inverter Benchmarking

3.3.12. Inverter Forecast 2023-2036 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V

3.3.13. OBC Forecast: Si, SiC, GaN 2023-2036 (GW)

3.3.14. DC-DC Converter Forecast: Si, SiC, GaN 2023-2036 (GW)

3.3.15. Onboard Charger Circuit Components

3.3.16. Tesla Onboard Charger / DC-DC Converter

3.3.17. OBC by Level: 4kW, 6-11.5kW, 16-22kW 2020-2036

4. WIDE BANDGAP SEMICONDUCTOR MANUFACTURING CHAIN

4.1. SiC Manufacturing

4.1.1. Introduction

4.1.2. Si IGBT Production: Raw Material to EV

4.1.3. SiC MOSFET Production: Raw Material to EV

4.1.4. SiC-Specific Equipment

4.1.5. From 150mm to 200mm: Potential Cost Advantages

4.1.6. 200mm Wafer Die Count Advantage

4.1.7. 200mm SiC Wafer Production Worldwide

4.1.8. 2025: The Transition to 8-inch SiC Wafers Continue

4.1.9. Vertical Integration: Acquisitions and Collaborations

4.1.10. Denso: Research and Development for Faster SiC Crystal Growth

4.1.11. Siltectra: Cold Split Technology

4.1.12. SmartSiC Technology from SOITEC

4.1.13. Summary of SmartSiC Advantages

4.1.14. Sumitomo Metal Mining: SiCkrest

4.1.15. Sumitomo Metal Mining: SiCkrest (2)

4.2. GaN Manufacturing

4.2.1. Which Substrate will Prevail for GaN?

4.2.2. TSMC To Exit GaN Foundry Business

4.2.3. GaN vs Si: Die to Vehicle Level

4.2.4. Energy Demand of Processes: Si vs GaN

5. TRENDS IMPACTING POWER ELECTRONICS

5.1. Introduction

5.1.1. Improving The Efficiency of Power Electronics

5.1.2. Efficiency and Thermal gains, 800V

5.1.3. Examples of SiC in the automotive industry

5.2. SiC and 800V

5.2.1. SiC Drives 800V Platforms

5.2.2. 800V Charging Speeds

5.2.3. GMC Hummer: 800V charging without 800V architecture

5.2.4. Other Split Battery Pack Vehicles: Tesla, Porsche, Ford

5.2.5. Tesla Cybertruck: Split Battery with 800V Architecture

5.2.6. Porsche Taycan: Boost Converter

5.2.7. Preh - Charging Technology for 800V EVs

5.2.8. 400V SiC Platforms

5.2.9. 800V Platforms SiC and Si IGBT Inverters

5.2.10. 800V Platforms SiC and Si IGBT Inverters (2)

5.2.11. 800V Adoption 2023

5.2.12. 800V Adoption 2024-2025

5.2.13. 800V Model Announcements in China (2022-2025)

5.2.14. 800V For & Against

5.2.15. DCFC Impact on Li-ion Cells

5.2.16. Fast Charge Cell Design Hierarchy - Levers to Pull

5.2.17. DC Fast Charging levels

5.2.18. 800V Platform Discussion & Outlook

5.2.19. Hybrid Switch Inverters

5.2.20. Hybrid Switch Inverters

5.2.21. 3-Level Inverters to Unlock GaN

5.3. Integration of Power Electronics

5.3.1. Different Levels of Integration

5.3.2. Owning the Supply Chain is Key

5.3.3. Vitesco and Renault: High Voltage Box and One Box

5.3.4. Integrated OBC with DC-DC converter

5.3.5. Preh Combo Units

5.3.6. Renault Zoe: 43kW AC Charging

5.3.7. Traction Integrated Onboard charger

5.3.8. Traction iOBC suppliers

5.3.9. Hyundai E-GMP: 800V, SiC and power electronics integration

5.3.10. BorgWarner: Combined Inverter and DC-DC Converter

5.3.11. NXP Inverter Predictions

5.4. Mixing Si IGBTs and SiC MOSFETs

5.4.1. SiC Impact on the Inverter Cost

5.4.2. SiC MOSFET vs Si IGBT: Overall Vehicle Cost

5.4.3. Si IGBT and SiC MOSFET Price Comparison

5.4.4. SiC Diodes: Onboard Charger

5.4.5. SiC Diodes: Inverter

5.4.6. Other Hybrid SiC Suppliers

5.4.7. NXP Inverter Predictions

5.5. Other Trends

5.5.1. Trends in Power Electronics: Dual Inverters

5.5.2. Thermal Management of the Dual Inverter and Power Modules

5.5.3. The Battery as Power Electronics

5.5.4. Porsche

6. SUPPLY CHAIN FOR POWER SEMICONDUCTOR MATERIALS, DEVICES & OEMS

6.1. SiC MOSFET and Si IGBT Suppliers

6.1.1. Supply Developments: Infineon

6.1.2. Supply Developments: STMicroelectronics

6.1.3. Supply Developments: Wolfspeed

6.1.4. Supply Developments: ROHM

6.1.5. Supply Developments: Onsemi

6.1.6. SiC MOSFET by Automotive OEMs and Suppliers - Leading OEMs (1)

6.1.7. SiC MOSFET by Automotive OEMs and Suppliers - Emerging OEMs

6.1.8. Si IGBT Suppliers to Leading OEMs

6.1.9. Si IGBT Suppliers to Emerging OEMs

6.1.10. New SiC Fabrication Centres

6.2. Device Suppliers

6.2.1. Infineon CoolSiC Efficiency Gains

6.2.2. Infineon Establishing Major OEM Partnerships

6.2.3. Infineon Design Wins

6.2.4. ROHM Semiconductor Expands SiC Production Capacity

6.2.5. ROHM: SiC Partnerships with OEMs and Tier Ones

6.2.6. STMicroelectronics Releases ACEPACK in Race for Market Leadership

6.2.7. STMicro Portfolio for EV Power Electronics

6.2.8. Wolfspeed: Major Investment & OEM Partnerships for SiC

6.2.9. Onsemi EliteSiC

6.2.10. Navitas GeneSiC

6.2.11. Benchmarking GeneSiC and its Trench Assisted Planar Configurations

6.2.12. Qorvo

6.2.13. Qorvo SiC FET vs SiC MOSFET

6.2.14. Trench vs Planar

6.3. Tier-1 Suppliers

6.3.1. Delphi Technologies Supply Luxury Automakers with Viper SiC Module

6.3.2. BorgWarner

6.3.3. BorgWarner Integrated Drive Module for Ford

6.3.4. BorgWarner Design Wins

6.3.5. Dana

6.3.6. Vitesco

6.3.7. Vitesco Power Electronics Products

6.3.8. Vitesco Schaeffler Merger

6.3.9. Equipmake

6.3.10. LG-Magna

6.3.11. Hitachi Double Sided IGBTs to Major OEM

6.3.12. Continental / Jaguar Land Rover

6.3.13. Helix CTI-4: Lotus Evija

6.3.14. Motion Applied (Formerly McLaren Applied) IPG5-x

6.4. Automotive OEMs

6.4.1. Hyundai Diversifies SiC Supply for Best-Selling 800V E-GMP Platform

6.4.2. GM From Bolt & Volt to Ultium

6.4.3. Volvo Heavy Duty SiC Inverter

6.4.4. Mercedes In House Development

7. POWER ELECTRONICS PACKAGES: EV USE-CASES

7.1. Toyota Prius 2004-2010

7.2. 2008 Lexus

7.3. Honda Accord 2014

7.4. Toyota Prius 2010-2015

7.5. Nissan Leaf 2012

7.6. Honda Fit (by Mitsubishi)

7.7. Toyota Prius 2016 Onwards

7.8. Cadillac 2016 (by Hitachi)

7.9. Chevrolet Volt 2016 (by Delphi)

7.10. BMW i3 (by Infineon)

7.11. JAC iEV4

7.12. Chinese NEV Uses Infineon

7.13. Huachen Xinri

7.14. Tesla Model X: Infineon IGBTs before SiC

7.15. 800V Si IGBT IGBT Choices

7.16. Porsche Taycan

7.17. Nissan Ariya 2021

7.18. Jaguar I-PACE

7.19. Jaguar I-PACE Power Module and Cooling

7.20. Wuling Hongguang Mini EV

7.21. Danfoss

7.22. Rivian R1T

7.23. Lexus RZ

7.24. Ford F-150 Lightning

7.25. BYD Atto 3 (2022): 8-in-1 Powertrain

7.26. BMW iX3

7.27. Tesla Cybertruck

7.28. STMicro

8. THERMAL MANAGEMENT FOR EV POWER ELECTRONICS

8.1. Introduction

8.1.1. Thermal Management Strategies in Power Electronics (1)

8.1.2. Thermal Management Strategies in Power Electronics (2)

8.1.3. Transistor History & MOSFET Overview - How Does it Affect Thermal Management

8.1.4. Summary of Cooling Approaches - (1)

8.1.5. Summary of Cooling Approaches - (2)

8.2. TIM1 and TIM2 in power electrics

8.2.1. Where are TIMs used in EV Power Electronics

8.2.2. TIM1 in Flip Chip Packaging

8.2.3. Solders as TIM1

8.2.4. Solder Options and Current Die Attach

8.2.5. Die-Attach Solution - Thermal Conductivity Comparison

8.2.6. Trend Towards Sintering

8.2.7. Silver Sintering Paste

8.2.8. Suppliers of metal sintering pastes

8.2.9. Properties and performance of solder alloys and sintered pastes

8.2.10. TIM2 - IDTechEx's Analysis on Promising TIM2

8.2.11. Yearly Market Size of TIMs Forecast (US$ Millions): 2024-2034

8.3. Liquid cooling - single and double sided

8.3.1. Single side, dual side, in-direct, and direct cooling

8.3.2. Key Summary of Single-Sided Cooling

8.3.3. Benefits and Drawbacks of Single-Sided Cooling

8.3.4. TIM2 Area Largely Similar for Single-Sided Cooling

8.3.5. onsemi - EliteSiC Power Module

8.3.6. ST Microelectronics - Tesla Model 3

8.3.7. Key Summary of Double-Sided Cooling (DSC)

8.3.8. Double-Sided Cooling Introduction

8.3.9. Double-Sided cooling examples

8.3.10. The Need for Double-Sided Cooling in Power Modules

8.3.11. Infineon's HybridPACK DSC

8.3.12. Inner Structure of HybridPACK DSC

8.3.13. onsemi - VE-Trac Family modules

8.3.14. CRRC

8.3.15. Hitachi Inverter - Double-Sided Cooling

8.3.16. BYD 1500V SiC - Double-Sided Ag Sintering

8.3.17. Trend Towards Double-Sided Cooling for Automotive Applications

8.3.18. Transition to Double-Sided Liquid Cooling

8.3.19. Market Share of Single and Double-Sided Cooling: 2024-2034

9. POWER ELECTRONICS FOR HEAVY DUTY VEHICLES

9.1.1. Trucks are Capital Goods

9.1.2. Differences Between Power Electronics for Passenger Vehicles and Heavy-Duty Vehicles

9.1.3. Torque vs Peak Power for Heavy-Duty BEVs

9.1.4. PowerizeD

9.1.5. High Voltage Powertrains for Heavy Duty Trucks

9.1.6. Ways to have 400V DC Charging Compatibility

9.1.7. MCS Specifications and Comparison

9.1.8. 800V Makes More Sense for Heavy Duty Trucks

9.1.9. Power Conversion for Low Power Applications

9.1.10. Onboard Chargers for Electric Trucks

9.1.11. Inverters for Heavy-Duty Vehicles

9.2. Heavy-Duty BEV Suppliers

9.2.1. Hitachi Roadpak

9.2.2. BAE Systems

9.2.3. BAE and Eaton Commercial Demonstrator 2024

9.2.4. Accelera by Cummins

9.2.5. Accelera (Cummins)

10. FORECASTS

10.1. Exponential Growth in Regional EV Markets

10.2. Methodology

10.3. Inverters per Car Forecast 2022-2036

10.4. Inverters per Car: Regional

10.5. Multiple Motors / Inverters per Vehicle

10.6. Inverter Forecast 2023-2036 (GW): GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V

10.7. Inverter Market Share 2023-2036: GaN 600V, Si IGBT 600V, SiC MOSFET 600V, 1200V

10.8. Inverter Liquid Cooling Strategy Forecast (units): 2015-2036

10.9. Discretes vs Power Modules Forecast for Inverters 2023-2036

10.10. OBC Forecast: Si, SiC, GaN 2023-2036 (GW)

10.11. DC-DC Converter Forecast: Si, SiC, GaN 2023-2036 (GW)

10.12. Inverter, OBC, DC-DC Converter Forecast 2023-2036 (GW)

10.13. Inverter, OBC, DC-DC Converter Unit Sales Forecast 2023-2036

10.14. Inverter, OBC, DC-DC Converter Forecast 2023-2036 (US$ billion)

10.15. OBC by Level: 4kW, 6-11.5kW, 16-22kW 2020-2036

10.16. Inverter, OBC & Converter, Si, SiC, GaN Cost Assumptions (US$ per kW)

11. PROFILES

11.1. Advanced Electric Machines Ltd

11.2. Arteco: EV-Specific Water-Glycol Coolants

11.3. BMW

11.4. BYD Auto

11.5. Diamond Foundry: Electric Vehicle Inverters

11.6. Dynex Semiconductor (CRRC): EV Power Electronics

11.7. Efficient Power Conversion: GaN FETs

11.8. Efficient Power Conversion: GaN in Automotive

11.9. Elaphe: In-wheel Motors to Increase Drive Cycle Efficiency

11.10. Equipmake: Electric Motors and Power Electronics

11.11. GaN Systems

11.12. General Motors (2020)

11.13. Heraeus: Solutions for EV Power Electronics

11.14. Hyundai: E-GMP 800V Platform Success

11.15. Infineon: 750V SiC MOSFETs for Onboard Chargers

11.16. Infineon: Automotive Power Electronics

11.17. Infineon: Expanding SiC OEM Partnerships

11.18. Integral e-Drive

11.19. Lotus

11.20. Lucid Motors

11.21. Magna International

11.22. McLaren Automotive

11.23. Nexperia: GaN for EV Power Electronics

11.24. NXP Semiconductors

11.25. QPT: MHz Switching, Active Cooling GaN

11.26. Rivian: Electric Passenger Trucks

11.27. ROHM Semiconductor: Supplying Lucid Motors

11.28. STMicroelectronics: SiC Advantages and Supply Chain

11.29. Tesla (2019 Update)

11.30. Transphorm

11.31. Valeo (48V Powertrain)

11.32. Wolfspeed

11.33. Wolfspeed: Major SiC Supply Deals

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|