自動車における自律走行ソフトウェアとAI 2026-2046年:技術、市場、プレーヤーAutonomous Driving Software and AI in Automotive 2026-2046: Technologies, Markets, Players SAEレベル別(L1、L2、L2+、L3、L4)自律走行コンシューマカー、レベル4ドライバーレスロボットタクシー、商用ロボットタクシーサービス、自律走行ルールと規制、自律走行ソフトウェア、ADASソフトウェア ... もっと見る

サマリー

SAEレベル別(L1、L2、L2+、L3、L4)自律走行コンシューマカー、レベル4ドライバーレスロボットタクシー、商用ロボットタクシーサービス、自律走行ルールと規制、自律走行ソフトウェア、ADASソフトウェア

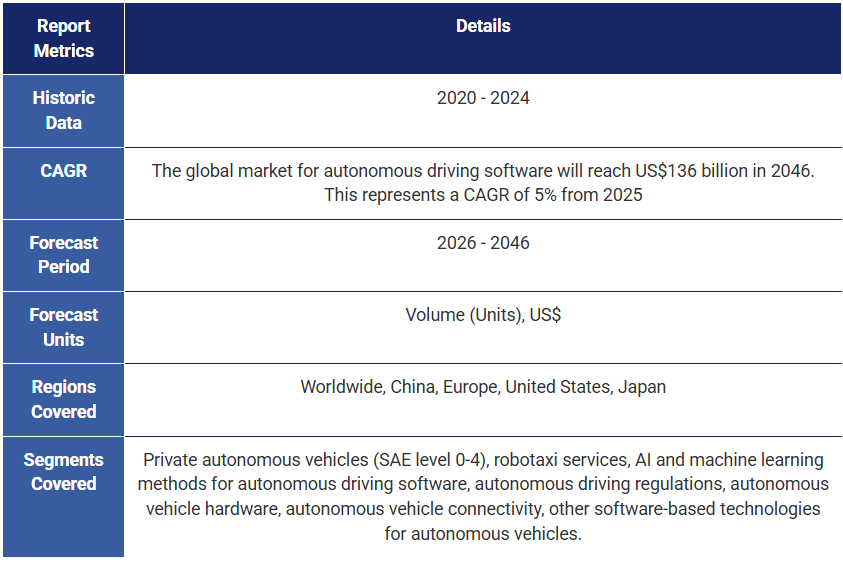

本レポートはADASと自律走行ソフトウェア市場の分析を提供する。トピックカバレッジには、ADASと自律走行市場で発展しているビジネスモデル、ハードウェア、ソフトウェアのパラダイムとトレンドが含まれる。IDTechExは、SAEレベル別の自動車、robotaxisからのソフトウェア収益、地域とSAEレベル別に分割した世界の自動車ADASと自律走行ソフトウェアの20年予測ラインを提供しています。予測は販売台数とUSドルである。

自動車産業は伝統的にハードウェア中心の産業であった。しかし、ソフトウェアで定義された自動車とソフトウェア主導の収益への移行に伴い、自動車OEMとティアワンサプライヤーは競争が激化する市場に供給するための技術開発に注目している。

IDTechExの調査レポート「自動車における自律走行ソフトウェアとAI 2026-2046:技術、市場、プレーヤー」は、ADAS(先進運転支援システム)と自律走行(AD)のソフトウェア市場を分析し、販売台数と年間市場規模の予測を提供している。本レポートでは、これらの機能の主要なソフトウェアスタックに加え、X-by-wire技術、HDマップ、OTA(over-the-air)アップデートのアプリケーションなど、ADASおよびADソフトウェア市場で見られるトレンドについても詳しく解説している。より高度な技術を取り入れることは、自家用車であれロボットタクシーであれ、より高いSAEレベルの自律走行を成功させるために最も重要である。IDTechExは、この分野からのソフトウェア由来の収益が急成長し、2046年までにほぼ10億米ドルの市場となり、年平均成長率はほぼ50%になると予測している。

ADAS ソフトウェアは今後 10 年間の主要市場である

アダプティブ・クルーズ・コントロールは 20 年以上前から自動車に搭載されており、その数年後には自律型緊急ブレーキや車線維持支援といった他の機能も搭載されるようになった。これらは、ハードウェア(前方カメラ、レーダー、超音波センサーなど)とソフトウェアの組み合わせで実現され、車両が進路を維持したり、必要に応じて介入したりできるようになっている。これらの機能は現在、大半の新車に当たり前のように搭載されており、ルールベースのアルゴリズムを使用して、ドライバーが常に調整することなく、車両が必要とする行動を客観的に定義している。

このような機能には、物体認識などのタスクで機械学習手法が使用されていたが、より高度なADAS機能やL2+(TeslaのFSDなど)が自家用車に搭載されるようになり、より高い性能要件と相まって、必要なコンピューティングパワーが上昇し、モデルのトレーニングとアクティブ運転の両方で、ディープラーニングとAIの応用が増加した。IDTechExは、成熟したADASソフトウェア市場(SAEレベル1~2+と定義)が今後10年間、ADASおよびAD市場全体を支配し続けると予測している。

自家用車は最終的に L3 と L4 の車両から大きなソフトウェア収益を得ることになる。

SAEレベル2+からレベル3への移行は重要なものである。多くのレベル2+システムが普及し、大部分は効果的であることが証明されているが、レベル3車両は、状況によっては道路から目を離すことができることを意味する。一般的に、レベル3の作動中に発生した事故の責任は、ドライバーではなくメーカーにあることになる。その結果、ハードウェアとソフトウェアの両方で定義される全体的な信頼性は、はるかに高くなければならない。これは、必要とされる計算能力が大幅に向上し、より多くのセンサーが搭載されるだけでなく、ソフトウェアにも反映される。このようなソフトウェアの性能は、畳み込みニューラルネットワークやトランスフォーマーなどのAIや機械学習手法の助けを借りて向上している。モービルアイなどの大手企業は、自律性のレベルが高くなると、ソフトウェア関連の収益の割合が大幅に増加すると述べている。

IDTechExは、10年後にはレベル3の自動車が、台数面でも運用面でも道路上でより一般的になると予測している。その結果、この移行に伴い、OTA(over-the-air)アップデート、HDマップ、X-by-wire技術などの機能がさらに普及するとIDTechExは予想している。現在、OTAアップデートのほとんどは、インフォテインメント・ソフトウェアのような安全上重要でない機能を対象としている。サイバーセキュリティは、自動車がサイバー攻撃のリスクなしにアップデートを行い、安全に走行できるようにするために最も重要である。IDTechExは、2030年代後半までにはレベル3とレベル4のソフトウェアが自家用車市場の大半を占めるようになると予想している。

ロボットタクシーが台頭し、継続的な収入をもたらす

2025年はこれまでのところ、ロボットタクシーにとって記念すべき年となった。市場をリードするウェイモは現在1,500台以上の車両を保有し、フェニックスやサンフランシスコなどの都市に営業地域を拡大している。バイドゥ・アポロも1,000台以上の車両を保有し、ウェイヴ、テスラ、モービルアイを導入したフォルクスワーゲンなどもテストや実証実験を開始している。自家用車は利用料やオプションから継続的な収益を得ることができるが、ロボットタクシーは毎日の乗車で確実に収益を得ることができる。ただし、IDTechExの知る限りでは、2025年6月現在、まだ黒字化したロボットタクシーサービスはない。

しかし、ロボットタクシーはまだ極めて初期段階にある。企業が数万台から数百万台への規模拡大を目指す中、どんな小さなミスや遅れも非常に危険なものとなる可能性がある。IDTechExが最も多くの企業が高度な自律走行技術を開発すると期待しているのはロボットタクシーであり、ディープラーニングのトレーニング方法、トランスフォーマー、エンドツーエンドのソフトウェアが、これを開発しスケールアップするための重要な推進力となっている。企業がレベル4技術の信頼性を証明できれば、これらの能力は乗用車の低レベルの自律性に転用できる。

IDTechExの調査レポート「自動車における自律走行ソフトウェアとAI 2026-2046:技術、市場、プレーヤー」は、SAEレベル4までの自家用車とロボットタクシーのソフトウェア市場をカバーし、今後20年間の市場を予測している。その中で、エンド・ツー・エンドのソフトウェア、センサー・フュージョン、ステア・バイ・ワイヤのような関連技術の重要性など、主要なトレンドとアプローチを特定している。また、自律走行に関する地域の規制を分析し、その他の自動車用途におけるジェネレーティブAIの応用に関する洞察も提供している。

主要な側面

本レポートでは、自家用車とロボットタクシーの両方の自律走行とADASソフトウェア市場について、以下のような分析を提供しています:

目次1.EXECUTIVE SUMMARY

1.1. 自律走行技術

1.2. SAE 自動化レベル

1.3. 自律走行車が合法とされる地域の概要

1.4. 自律走行に向けた2つの発展経路

1.5. カリフォルニア州、2024年の離脱1マイルあたり

1.6. 自動車用ソフトウェアのさまざまな種類

1.7. エンドツーエンドとモジュラーソフトウェアの比較

1.8. Tesla FSD

1.10. Waymoの運用領域

1.11. ADASのアップデートをOTAで行うOEM

1.12. Steer-by-Wire サプライヤー

1.13. 自動車における複合AIの用途

1.14 複合AIの自動車分野への応用

1.15. ロボットタクシー用ソフトウェアの世界売上高 2025-2046

1.16. SAEレベル別ADASおよびAVソフトウェアの世界市場 2025-2046

1.17.IDTechExサブスクリプションでさらに多くのコンテンツにアクセス

2. はじめに

2.1. 機械学習入門

2.1.1. AI入門:ゴールポストの移動

2.1.2. 人工知能のサブセットとしての機械学習

2.1.3. 機械学習アプローチ

2.1.4. 教師あり学習

2.1.5. 教師なし学習

2.1.6. 強化学習

2.1.7 教師あり学習と教師なし学習における問題クラス

2.1.8. 半教師付き学習と能動学習

2.1.9. ニューラルネットワーク-入門

2.1.10. 学習プロセスにおける人工ニューロン

2.1.11. ニューラルネットワークの種類

2.1.12. 自動車における複合AIの応用

2.1.13. 自動車向けEnd-to-End AIの実装

2.2. 定義

2.2.2. SAE 自動化レベル

2.2.3. 自律走行技術

2.2.4. 法規制と自律走行

2.2.5. 自動運転車の合法化状況の概要

2.2.6 L3級乗用車(試験用および公道走行用)の承認

2.2.7. 欧州におけるレベル3の見通し

2.2.8. 米国の自律走行乗用車ランキング

2.2.9. 2023年にADASの主要機能の採用が再び増加

2.2.10. SAEレベル2の採用が前年比で増加

2.2.11. 高レベルの自律走行は、車両あたりのセンサー数の増加を意味する

2.2.12. ロボタクシーは計測可能なほど安全になってきているが、安全性は十分か

2.2.13. 自動車用ソフトウェアのさまざまなタイプ

2.2.14. AUTOSAR

2.2.15. AUTOSARパートナーと開発者

2.3.自律走行車のハードウェア

2.3.1. 主要3センサーの相補的な特性

2.3.2. レベル1からレベル4までのセンサースイートの進化

2.3.3. 自律走行車におけるカメラの使われ方

2.3.4. 自律走行車のための熱・赤外線センシング

2.3.5. 自律走行車におけるフロントレーダーの使用

2.3.6. サイドレーダーが提供する自律走行機能

2.3.車載用LiDAR

2.3.8. 低性能SoCチップ

2.3.9. 中性能SoCチップ

2.3.10. 高性能SoCチップ

2.3.11. 高性能SoCチップ - SoCチップの性能進化

2.3.12. 自律走行車ハードウェアの詳細情報

2.4. ソフトウェア定義車両

2.4.1. ソフトウェア定義車両とは

2.4.2 SDV 特徴マップ

2.4.3. 自律走行車のコネクテッドな側面

2.4.4. SAE 自動化レベル

2.4.5. Level 2 要件

2.4.6. Level 3 要件

2.4.7. Level 4 (プライベート) 要件

2.4.8. Level 4 (ロボタクシー) 要件

2.4.9. 自律レベル要件の比較

2.4.10. IDTechExのソフトウェア定義車両に関する研究

2.5. 自律走行車のビジネスモデル

2.5.1. MaaSレベル4と個人所有レベル4は異なる

2.5.2. ロボットタクシー & ロボットシャトル

2.5.3. 自律走行に向けた2つの開発パス

2.5.4. 将来のモビリティシナリオ: 定義、利用可能性、法規制が固まりつつあるレベル2+

2.5.5 レベル2+ 定義、利用可能性、および立法における確立

2.5.6. ロボタクシーODDの指数関数的成長

2.5.7. 2024年に自律走行ロボットタクシーサービスを運営する主要プレーヤー

2.5.8. 2025年に自律走行ロボットタクシーサービスを運営する主要プレーヤー

2.5.9. さまざまなレベルでの自律走行機能

2.5.10. 自家用車における自律走行機能のロードマップ

3. 自律走行ソフトウェア

3.1. 自律走行ソフトウェアへのさまざまなアプローチ

3.1.1. グラウンドトゥルース

3.1.2. AVL グラウンドトゥルースシステム

3.1.3. エッジインテリジェンス

3.1.4. 自動運転の4つの柱

3.1.5 バイドゥアポロのモジュラー・ソフトウェア

3.1.6. エンド・ツー・エンド(E2E)アーキテクチャ

3.1.7. エンド・ツー・エンド・アーキテクチャ

3.1.8. ニューラル・ネットワークの分解

3.1.9. エンド・ツー・エンド対モジュラー・ソフトウェア

3.1.10. モジュラーの短所

3.1.11. エンド・ツー・エンドの短所

3.1.12. エンド・ツー・エンド対モジュラー・アプローチを使用するプレイヤーのまとめ

3.1.13. ビジョン・ベース対 LiDAR ベース・システム

3.1.14. テスラ・オキュパンシー・ネットワーク

3.1.15. アーリー・ステージ対レイト・ステージのセンサー・フュージョン

3.1.16. トランスフォーマーの自律走行車への応用

3.2. バイワイヤー技術

3.2.1. ステア・バイ・ワイヤー: ステアバイワイヤ

3.2.3. EUと米国におけるステアバイワイヤ

3.2.4. アジアにおけるステアバイワイヤ

3.2.5. ステアバイワイヤのサプライヤー

3.2.6.バイワイヤ市場

3.3. OTAアップデート

3.3.1. ADAS向け OTAアップデート

3.3.2. ADASアップデートをOTAで提供するOEM

3.4. HDマップ

3.4.1. ローカライズとは?(1)

3.4.2. ローカライズとは?(2)

3.4.3. HDマッピング資産: ADASマップからレベル5自律走行用のフルマップまで

3.4.4 HD Map as a Service

3.4.5. 市民地図: 自動運転のためのHDマップ

3.4.6 自動運転用の高精度地図

3.4.7. HDマップレイヤー

3.4.8. HDマップの自動車への搭載方法

4. 自動運転ソフトウェアプレーヤー

4.1.1. フルスタックおよびソフトウェアのみのプレーヤー

4.2. ADASソフトウェアパッケージ

4.2.1.ADASの追加機能として

4.2.2 アウディ

4.2.3. テスラFSD

4.2.4. シボレー スーパークルーズ

4.2.5. モービルアイ

4.2.6. モービルアイの製品ライン

4.2.7. モービルアイのパートナーシップ

4.2.8. モバイルアイの2025年導入コスト

4.2.9 クアルコム

4.2.10. スナップドラゴン・ライド・プラットフォームの機能

4.3. 自動運転のプレーヤー

4.3.1. プレーヤーの表(1)

4.3.2 プレーヤーの表(2)

4.3.3. 運転シェアリング企業とその自律走行パートナーシップ

4.3.4. 2023年の開発状況

4.3.5. 2024年の開発状況

4.3.6. 2025年の開発状況

4.3.7. VWとMobileye Robotaxi

4.3.8. 応用された直観

4.3.9. バイドゥアポロ

4.3.10. TierIV

4.3.11. TierIVの自律走行アプローチ

4.3.12. オートウェア財団

4.3.13.ウェイモの第6世代

4.3.14. ウェイモのオペレーション領域

4.3.15. ウェイモの基盤モデルとエンド・ツー・エンドの研究

4.3.16. ウェイモのSWOT分析

4.3.18. ウェイブ

4.3.19. ウェイブ

4.3.20. コンマAI

4.3.21. ホロマティック

4.3.22. モーメンタ

4.3.23. モーメンタ・ ロボタクシーとアルゴリズム開発

4.3.24. Qクラフト

4.3.25. Qクラフト ソリューションズ

4.3.26. NuTonomy

4.3.27. Motional

4.3.28. Motionalのソフトウェア開発

4.3.29. Motionalのクローズドループ開発と強化学習

4.3.30. Helm AI

4.3.31. Helm AIのモジュラー・ソフトウェア・アプローチと教師なし学習

4.3.32. Aptiv

4.3.33. AptivのADASおよび自律走行向けソリューション

4.3.34. エヌビディア・エヌダス

4.3.35. 離脱距離(マイル)トレンド 2019-2022

4.3.36. 離脱距離(マイル)2023

4.3.37. 離脱距離(マイル)2024

5. OTHER AI AND SOFTWARE APPLICATIONS IN VEHICLES

5.1. 車両用AIアシスタント

5.1.1. はじめに

5.1.2. Apple CarPlay

5.1.4. Android AutoとGoogle Automotive Services

5.1.5. スマートコックピット向けDeepSeek

5.2. 車載ソフトウェア向けサードパーティマーケットプレイス

5.2.1. 車載ソフトウェア向けサードパーティマーケットプレイス:SDVerse

5.2.2. 自動車ソフトウェア向けサードパーティマーケットプレイスの利点と課題

6. フォーキャスト

6.1.1. フォーキャスト手法

6.2. 自律走行車フォーキャスト

6.2.1. SAEレベル別自家用車 2025-2046

6.3.世界のロボットタクシー用ソフトウェア市場予測

6.3.1. 世界のロボットタクシー用ソフトウェア売上高 2025-2046

6.4. 地域別ソフトウェア市場予測

6.4.1. 世界のSAEレベル別ADAS・AVソフトウェア市場 2025-2046

6.4.2 RoWのADASとAVソフトウェア市場:SAEレベル別 2025-2046

6.4.3. 日本のADASとAVソフトウェア市場:SAEレベル別 2025-2046

6.4.4. 欧州のADASとAVソフトウェア市場:SAEレベル別 2025-2046

6.4.5.米国の ADAS と AV ソフトウェア市場:SAE レベル別 2025-2046

7. COMPANY PROFILES

7.1. IDTechEx ポータルの企業プロファイルへのアクセス

Summary

Autonomous consumer cars by SAE level (L1, L2, L2+, L3, L4), Level 4 driverless robotaxis, commercial robotaxi services, autonomous driving rules and regulations, autonomous driving software, ADAS software

This report provides an analysis of the software market for ADAS and autonomous driving software. Topic coverage includes business models, hardware, and software paradigms and trends developing in the market for ADAS and autonomous driving. IDTechEx provides 20-year forecast lines for cars by SAE level, software revenue from robotaxis, and global vehicle ADAS and autonomous driving software, split by region and SAE level. Forecasts are in unit sales and US$.

The automotive sector has been a traditionally hardware-centric industry. However, with the transition to software-defined vehicles and software-driven revenue, automotive OEMs and tier-one suppliers have looked to develop technologies to supply into an increasingly competitive market.

IDTechEx's report, "Autonomous Driving Software and AI in Automotive 2026-2046: Technologies, Markets, Players", analyzes the software market for ADAS (advanced driver assistance systems) and autonomous driving (AD), providing forecasts of unit sales and yearly market size. Alongside the main software stack for these features, the report also goes into detail on trends seen in the ADAS and AD software market, including the applications of X-by-wire technologies, HD maps, and OTA (over-the-air) updates. The inclusion of more advanced technologies is paramount to the success of higher SAE levels of autonomous driving, whether that is in private vehicles or robotaxis. Robotaxis, by definition, are required to be at least SAE level 4, with IDTechEx forecasting a rapid growth of software-derived revenue from the sector, making it an almost US$1 billion market by 2046, at a CAGR of almost 50%.

ADAS software is the key market for the next ten years

Adaptive cruise control has been in vehicles for over two decades, with other features such as autonomous emergency braking and lane-keeping assistance following on a few years later. These were enabled with a combination of hardware (such as front-facing cameras, radar, and ultrasonic sensors) and software that allowed the vehicle to maintain a path or intervene where necessary. These features are now commonplace in the majority of new cars and use rule-based algorithms to objectively define the actions required by the vehicle without the driver constantly adjusting.

While machine learning methods were used for such features in tasks such as object recognition, the dawn of more advanced ADAS features and L2+ (such as Tesla's FSD) in private vehicles, combined with higher performance requirements, has driven the computing power required up, and increased the applications of deep learning and AI, for both training models and in active driving. IDTechEx forecasts the mature ADAS software market (defined as SAE level 1 to 2+) to continue to dominate the ADAS and AD market as a whole for the next ten years.

Private cars will eventually see major software revenue from L3 and L4 vehicles.

The transition from SAE level 2+ to level 3 is a significant one. While many level 2+ systems have proven popular and, for the most part, effective, level 3 vehicles mean that, in some situations, eyes can be taken off the road. Generally, this would result in the accountability of any accident occurring while level 3 is operational falling onto the manufacturer, not the driver. As a result, the overall reliability, defined by both the hardware and software, has to be much greater. This is reflected in the significantly greater computing power required, the inclusion of more sensors, but also in the software. Performance of such software has increased with the help of AI and machine learning methods such as convolutional neural networks and transformers. It has been stated by major players such as Mobileye that the proportion of software-related revenue increases significantly at higher levels of autonomy.

IDTechEx forecasts that in ten years, level 3 cars will become more commonplace on the roads, both in number and in operational areas. As a result, IDTechEx expects that features such as over-the-air (OTA) updates, HD maps, and X-by-wire technologies will gain further traction to accompany this transition. Currently, most OTA updates are for non-safety-critical functions, such as infotainment software. Cybersecurity will be paramount to making sure that vehicles can update and also drive safely without risk of cyberattack. By the late 2030s, IDTechEx expects level 3 and level 4 software to make up the majority of the market for private vehicles.

Robotaxis are on the rise and provide continuous income

2025 has been a momentous year for robotaxis so far. Market leaders Waymo now have a fleet of over 1,500 vehicles and has expanded its areas of operations to cities such as Phoenix and San Francisco. Baidu Apollo also has an established fleet of over 1,000 cars, while other players such as Wayve, Tesla, and Volkswagen with Mobileye have begun testing and demonstrations. While private vehicles will be able to provide continuous revenue from subscription fees and optional extras, robotaxis are a guaranteed way to gain revenue through daily rides. It should be noted, however, that to IDTechEx's best knowledge, no singular robotaxi service has turned a profit yet, as of June 2025.

However, robotaxis are still in an extremely nascent stage. As companies look to scale up to tens of thousands to potentially millions, any small error or delay could prove extremely dangerous. Robotaxis are where IDTechEx expects most companies to develop advanced autonomous driving technology, with deep learning training methods, transformers, and end-to-end software being key drivers to developing and scaling this. If a company can prove the reliability of its level 4 technology, then these capabilities can be translated to lower levels of autonomy in passenger cars.

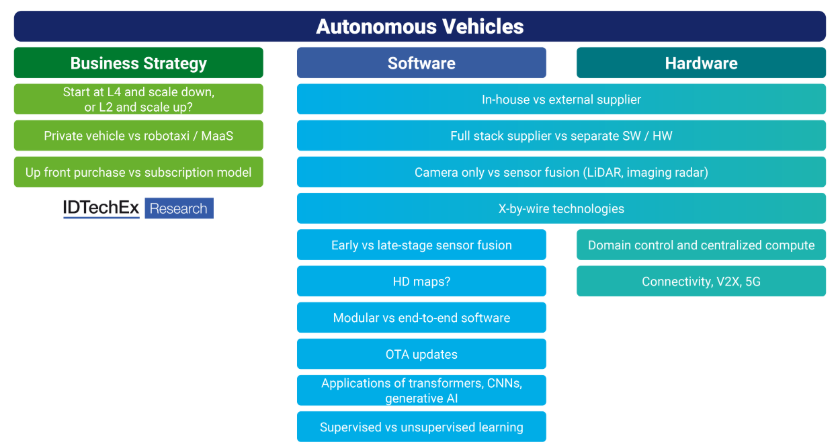

IDTechEx's report, "Autonomous Driving Software and AI in Automotive 2026-2046: Technologies, Markets, Players", provides coverage of both the private car and robotaxi software markets, up to SAE level 4, and forecasts the market for the next twenty years. In its coverage, it has identified key trends and approaches, including end-to-end software, sensor fusion, and the importance of tangential technologies such as steer-by-wire. It analyzes regional regulations for autonomous driving and provides insight into the applications of generative AI in other automotive applications.

Key Aspects

This report provides an analysis of the autonomous driving and ADAS software market for both private cars and robotaxis, including:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Autonomous Driving Technologies

1.2. SAE Levels of Automation

1.3. Overview of Where Autonomous Cars are Legal

1.4. Two Development Paths Towards Autonomous Driving

1.5. California Miles per Disengagement 2024

1.6. Different Types of Automotive Software

1.7. End-to-End vs Modular Software

1.8. Summary of Players Using End-to-End vs Modular Approaches

1.9. Tesla FSD

1.10. Waymo Operational Areas

1.11. OEMs with ADAS Updates OTA

1.12. Steer-by-Wire Suppliers

1.13. How HD Maps fit into a Vehicle

1.14. Applications of Compound AI in Automotive

1.15. Global Robotaxi Software Revenue 2025-2046

1.16. Global ADAS and AV Software Market by SAE Level 2025-2046

1.17. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. Introduction to Machine Learning

2.1.1. An Introduction to AI: Shifting Goalposts

2.1.2. Machine Learning as a Subset of Artificial Intelligence

2.1.3. Machine Learning Approaches

2.1.4. Supervised Learning

2.1.5. Unsupervised Learning

2.1.6. Problem Classes in Supervised and Unsupervised Learning

2.1.7. Reinforcement learning

2.1.8. Semi-supervised and Active Learning

2.1.9. Neural Networks - an Introduction

2.1.10. An Artificial Neuron in the Training Process

2.1.11. Types of Neural Network

2.1.12. Applications of Compound AI in Automotive

2.1.13. Implementations of End-to-End AI for Automotive

2.2. Introduction to Autonomous Vehicles

2.2.1. Definitions

2.2.2. SAE Levels of Automation

2.2.3. Autonomous Driving Technologies

2.2.4. Legislation and Autonomy

2.2.5. Overview of Where Autonomous Cars are Legal

2.2.6. L3-Level Passenger Vehicles Approved for Testing and on road

2.2.7. Level 3 Outlook in Europe

2.2.8. US Autonomous Passenger Vehicle Rankings

2.2.9. Adoption of Key ADAS Features Increased Again in 2023

2.2.10. Year-On-Year Increase in SAE Level 2 Adoption

2.2.11. High Levels of Autonomy Means More Sensors per Vehicle

2.2.12. Robotaxis Are Getting Measurably Safer, Are They Safe Enough

2.2.13. Different Types of Automotive Software

2.2.14. AUTOSAR

2.2.15. AUTOSAR Partners and Developers

2.3. Autonomous Vehicles Hardware

2.3.1. The Complimentary Qualities of Primary Three Sensors

2.3.2. Evolution of Sensor Suites from Level 1 to Level 4

2.3.3. How Cameras are Used in Autonomous Cars

2.3.4. Thermal and Infrared Sensing for Autonomous Cars

2.3.5. Front Radars Use in Autonomous Cars

2.3.6. Autonomous Driving Functions Provided by Side Radar

2.3.7. Automotive LiDAR

2.3.8. Low-performance SoC Chips

2.3.9. Mid-performance SoC Chips

2.3.10. High-performance SoC Chips

2.3.11. High-performance SoC Chips - Performance Evolution of SoC Chips

2.3.12. More Information on Autonomous Vehicles Hardware

2.4. Software Defined Vehicles

2.4.1. What is a Software-Defined Vehicle?

2.4.2. SDV Feature Map

2.4.3. Connected Aspects of Autonomous Vehicles

2.4.4. SAE Levels of Automation

2.4.5. Level 2 Requirements

2.4.6. Level 3 Requirements

2.4.7. Level 4 (Private) Requirements

2.4.8. Level 4 (Robotaxi) Requirements

2.4.9. Autonomy Levels Requirements Compared

2.4.10. IDTechEx Research on Software-Defined Vehicles

2.5. Autonomous Vehicles Business Models

2.5.1. MaaS Level 4 is Different From Privately Owned Level 4

2.5.2. Robotaxis & Robot Shuttles

2.5.3. Two Development Paths Towards Autonomous Driving

2.5.4. Future Mobility Scenarios: Autonomous and Shared

2.5.5. Level 2+ Solidifying in Definition, Availability, and Legislation

2.5.6. Exponential Growth in Robotaxi ODD

2.5.7. The Key Players Operating Autonomous Robotaxi Services in 2024

2.5.8. The Key Players Operating Autonomous Robotaxi Services in 2025

2.5.9. Functions of Autonomous Driving at Different Levels

2.5.10. Roadmap of Autonomous Driving Functions in Private Cars

3. AUTONOMOUS VEHICLES SOFTWARE

3.1. Different Approaches to Autonomous Driving Software

3.1.1. Ground Truth

3.1.2. AVL Ground Truth System

3.1.3. Edge Intelligence

3.1.4. 4 Pillars of Autonomous Driving

3.1.5. Baidu Apollo's Modular Software

3.1.6. End-to-End (E2E) Architecture

3.1.7. End-to-End Architectures

3.1.8. Breaking Down the Neural Network

3.1.9. End-to-End vs Modular Software

3.1.10. Modular Disadvantages

3.1.11. End-to-End Disadvantages

3.1.12. Summary of Players Using End-to-End vs Modular Approaches

3.1.13. Vision Based vs LiDAR Based Systems

3.1.14. Tesla Occupancy Network

3.1.15. Early vs Late Stage Sensor Fusion

3.1.16. Applications of Transformers for Autonomous Vehicles

3.2. By-Wire Technologies

3.2.1. Steer-by-Wire: Introduction

3.2.2. Steer-by-Wire

3.2.3. Steer-by-Wire in the EU and US

3.2.4. Steer-by-Wire in Asia

3.2.5. Steer-by-Wire Suppliers

3.2.6. By-Wire Market

3.3. OTA Updates

3.3.1. OTA Updates for ADAS

3.3.2. OEMs with ADAS Updates OTA

3.4. HD Maps

3.4.1. What is Localization? (1)

3.4.2. What is Localization? (2)

3.4.3. HD Mapping Assets: From ADAS Map to Full Maps for Level-5 Autonomy

3.4.4. HD Map as a Service

3.4.5. Civil Maps: Low-Data rate Maps

3.4.6. HD Maps for Autonomous Driving

3.4.7. HD Map Layers

3.4.8. How HD Maps fit into a Vehicle

4. AUTONOMOUS DRIVING SOFTWARE PLAYERS

4.1.1. Full-Stack and Software Only Players

4.2. ADAS Software Packages

4.2.1. ADAS as an Add-on

4.2.2. Audi

4.2.3. Tesla FSD

4.2.4. Chevrolet Super Cruise

4.2.5. Mobileye

4.2.6. Mobileye Product Line

4.2.7. Mobileye Partnerships

4.2.8. Mobileye Costs to Deploy 2025

4.2.9. Qualcomm

4.2.10. Snapdragon Ride Platform Capabilities

4.3. Autonomous Driving Players

4.3.1. Table of Players (1)

4.3.2. Table of Players (2)

4.3.3. Driving Sharing Companies and Their Autonomous Partnerships

4.3.4. State of Development in 2023

4.3.5. State of Development in 2024

4.3.6. State of Development in 2025

4.3.7. VW and Mobileye Robotaxi

4.3.8. Applied Intuition

4.3.9. Baidu Apollo

4.3.10. Tier IV

4.3.11. Tier IV's Autonomous Driving Approach

4.3.12. The Autoware Foundation

4.3.13. Waymo's Sixth Generation

4.3.14. Waymo Operational Areas

4.3.15. Waymo's Foundational Model and End-to-End Research

4.3.16. Waymo vs Tesla on Robotaxis and Profitability

4.3.17. Waymo SWOT Analysis

4.3.18. Wayve

4.3.19. Wayve

4.3.20. Comma AI

4.3.21. Holomatic

4.3.22. Momenta

4.3.23. Momenta Robotaxi and Algorithm Development

4.3.24. QCraft

4.3.25. QCraft Solutions

4.3.26. NuTonomy

4.3.27. Motional

4.3.28. Motional's Software Development

4.3.29. Motional Closed Loop Development and Reinforcement Learning

4.3.30. Helm AI

4.3.31. Helm AI's Modular Software Approach and Unsupervised Learning

4.3.32. Aptiv

4.3.33. Aptiv's Solutions for ADAS and Autonomous Driving

4.3.34. Nvidia NDAS

4.3.35. Trends in Miles per Disengagement 2019-2022

4.3.36. Miles per Disengagement 2023

4.3.37. Miles per Disengagement 2024

5. OTHER AI AND SOFTWARE APPLICATIONS IN VEHICLES

5.1. Vehicle AI Assistants

5.1.1. Introduction

5.1.2. Automotive Voice Control and the Birth of LLMs

5.1.3. Apple CarPlay

5.1.4. Android Auto and Google Automotive Services

5.1.5. DeepSeek for Smart Cockpits

5.2. Third Party Marketplaces for Automotive Software

5.2.1. Third Party Marketplaces for Automotive Software: SDVerse

5.2.2. Benefits and Challenges of a Third Party Marketplace for Automotive Software

6. FORECASTS

6.1.1. Forecast Methodology

6.2. Autonomous Vehicles Forecast

6.2.1. Private Vehicles by SAE Level 2025-2046

6.3. Robotaxi Software Market Forecast

6.3.1. Global Robotaxi Software Revenue 2025-2046

6.4. Regional Software Market Forecast

6.4.1. Global ADAS and AV Software Market by SAE Level 2025-2046

6.4.2. RoW ADAS and AV Software Market by SAE Level 2025-2046

6.4.3. Japan ADAS and AV Software Market by SAE Level 2025-2046

6.4.4. Europe ADAS and AV Software Market by SAE Level 2025-2046

6.4.5. China ADAS and AV Software Market by SAE Level 2025-2046

6.4.6. US ADAS and AV Software Market by SAE Level 2025-2046

7. COMPANY PROFILES

7.1. Access to company profiles on the IDTechEx portal

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|