ソフトウェア定義自動車、コネクテッド・カー、自動車におけるAI 2026-2036年Software-Defined Vehicles, Connected Cars, and AI in Cars 2026-2036 SDVs、コネクテッドカー(CAVs)、車載AIアシスタント、V2X、Autonomy as a Service、コネクテッドカー、E/Eアーキテクチャ、高度道路交通システム(ITS-G5)、DSRC、C-V2X、Features as a Service、ADAS ... もっと見る

サマリー

SDVs、コネクテッドカー(CAVs)、車載AIアシスタント、V2X、Autonomy as a Service、コネクテッドカー、E/Eアーキテクチャ、高度道路交通システム(ITS-G5)、DSRC、C-V2X、Features as a Service、ADAS

自動車業界は、機能性、価値、ユーザーエクスペリエンスがハードウェアではなくソフトウェアによってますます支配される、ソフトウェア定義車両(SDVs)への基盤的なシフトを進めている。IDTechExのレポート「自動車におけるソフトウェア定義自動車、コネクテッドカー、AI 2026-2036:市場、動向、予測」は、車載電気/電子(E/E)アーキテクチャの進化、コネクティビティプラットフォーム、機能収益化モデル、長期市場予測を網羅し、この変革の包括的な分析を提供している。IDTechEx の予測によると、セントラルコンピュートプラットフォームと準ゾーン SDV プラットフォームは、2029 年までに約 7,550 億米ドルのハードウェア売上を創出し、OEM にとって価値向上の主要な源泉となる。SDV 機能関連の収益は、接続性と自律性に基づくサービスの収益化が原動力となり、2035 年まで年平均成長率 30~34%で成長すると予想される。

ECUから中央演算へ:SDV アーキテクチャの台頭

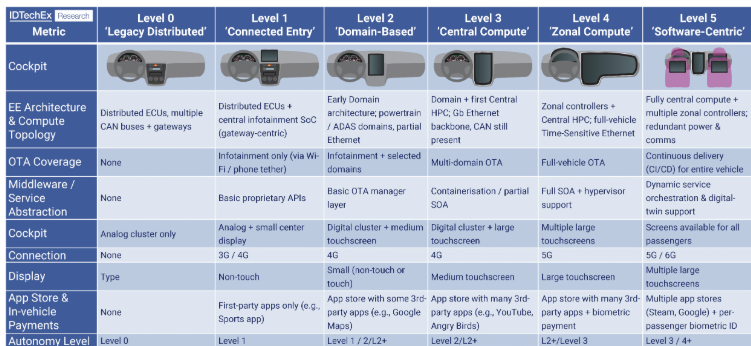

最新の SDV は、集中型コンピューティングプラットフォームと無線(OTA)アップデート機能によってサポートされる、ハードウェアとソフトウェアを切り離す能力によって定義されます。このレポートでは、SDV をゲートウェイ中心、ドメインベースのシステムから完全なソフトウェア中心の車両まで、5 つのレベルに分類し、ハイパフォーマンスコンピューティング(HPC)、ゾーンコントローラ、サービス指向ミドルウェアなどの主要な実現コンポーネントの詳細な内訳を示します。

このレポートでは、BMW の Neue Klasse、Tesla の FSD 対応モデル、BYD、NIO、Li Auto などの中国の新興 SDV などの主要プラットフォームを分析している。また、これらの車両がTSNイーサネット、AI対応SoC、ソリッドステート配電などの技術をどのように利用し、EEランドスケープを再構築するかについても解説しています。

SDV時代の収益化:フィーチャー・アズ・ア・サービスと車載コマース

SDVは技術的なアップグレードであるだけでなく、ビジネスモデルの転換を意味する。自動車メーカーは、先進運転支援システム(ADAS)からインフォテインメント、パーソナライゼーション、さらには暖房機能まで、収益化可能な機能を車両に組み込む傾向を強めている。

本レポートでは、BMW、フォード、メルセデス・ベンツのようなOEMメーカーが、FaaS(features-as-a-service)やOTAアップデートをどのように活用し、継続的な収益を上げているかについて概説している。また、サブスクリプションモデル、地域別の価格戦略、SDV 機能が顧客維持やブランド差別化に与える影響についても調査しています。

ケーススタディでは、BMW の Neue Klasse、Mastercard と JPMorgan Mobility Payments による車載決済プラットフォームなど、実際の導入事例を紹介しています。

V2Xコネクティビティとインフラの準備

自動車の自律性とコネクティビティが高まるにつれ、V2X(Vehicle-to-Everything)テクノロジーは、安全性、協調性、ユーザーエクスペリエンスの向上を確保する上で不可欠な役割を果たします。本レポートでは、C-V2X、DSRC、5Gベースの通信を深く掘り下げ、その性能、コスト、地理的な採用を評価しています。

IDTechExは、中国、EU、米国、日本、韓国を含む主要地域の周波数割り当てと政策動向をマッピングしている。また、主要なV2Xハードウェアプロバイダのプロフィールを紹介し、車載ユニット(OBU)、路側ユニット(RSU)、チップセットがSDVプラットフォームにどのように統合されているかを解説している。

ジェネレーティブAIとインテリジェントキャビン

本レポートでは、SDVにおけるジェネレーティブAIの統合、特に車載アシスタント、パーソナライズされたインフォテイメント、予測診断についても調査しています。クアルコム、Nvidia、Unityなどの企業がデバイス上でのAI推論を可能にすることで、OEMが適応的で没入感のあるデジタル体験を提供する新たな機会が生まれつつある。

音声制御だけでなく、SDVのコックピットはデジタルプラットフォームになりつつある。フルワイドのスクリーン、AIアバター、カスタマイズ可能なソフトウェアスキンは、ブランドロイヤルティとユーザーエンゲージメントの新たな戦場を作り出している。

2036年までの予測:SDVの採用と収益見通し

この調査レポートは、2026年から2036年までのSDV市場について、数量と市場金額の両方で10年間の市場予測を掲載しています。予測には以下が含まれる:

2029 年までに準ゾーン SDV プラットフォームのハードウェア収益は 7,550 億米ドルに達すると予測され、機能ベースの収益化は 30~34% の CAGR で成長し、2035 年までに累積収益が数千億ドルに達すると予測される。

主要な側面1.エグゼクティブサマリー

自動車業界におけるハードウェア定義からソフトウェア定義のパラダイムへの移行を概観し、主要な業界動向、技術的イネーブラー、マネタイズ戦略を明らかにする。

2.ソフトウェア定義車両

2025 年頃に予想される次世代 SDV アーキテクチャを網羅:

3.V2X とコネクテッド・ビークル技術

コネクテッド・ビークルを実現する技術とインフラの評価:

4.自律走行コネクティビティ

自律走行能力におけるコネクティビティの役割の評価:

5.予測(2025~2036年)

SDVの普及とV2Xの普及に関する定量的予測:

目次1.エグゼクティブサマリー

1.1.ソフトウェア定義車両とは何か

1.2.SDVに必要なもの

1.3.ソフトウェア定義車両のレベルガイド

1.4.SDVレベルチャート:主要OEMの比較

1.5.SDVレベルガイドの説明

1.6.SDVのフィーチャーレイヤー

1.7.主要OEMと代表的なモデル/プラットフォーム

1.8.SDV E/E アーキテクチャ - マイコンユニット

1.9.SDV E/E アーキテクチャのプレーヤー

1.10.SDV 結論と主な要点 (1)

1.11.SDV の結論と重要なポイント(2)

1.12.無線アップデートと診断

1.13.ソフトウェア定義車両の予測(台数)

1.14.SDV予測(ハードウェア収益)

1.15.コネクテッド・ビークルとは?

1.16.コネクテッド・ビークルの主要用語

1.17.無線アクセス技術の比較

1.18.コネクテッドカーのサプライチェーン

1.19.V2Xチップセット - 比較

1.20.無線アクセス技術の比較

1.21.無線アクセス技術の比較

1.22.V2V/V2Iユースケースの例

1.23.V2X地域の規制状況

1.24.V2V/V2Iの普及予測

1.25.V2V/V2I無線アクセス技術の予測

1.26.オートノミーにとって5Gが重要な理由

1.27.企業プロファイル

1.28.IDTechEx サブスクリプションでさらにアクセス

2.ソフトウェア定義車両

2.1.1.ソフトウェア定義車両とは何か

2.1.2.なぜこのような宣伝があるのか(1)

2.1.3.なぜこのような誇大広告があるのか(2)

2.1.4.SDVレベルガイド

2.1.5.SDVレベルチャート:主要OEMの比較

2.2.SDV サービスとアプリケーション

2.2.1.サービスとしてのコネクティビティ

2.2.2.保険向けSDV(Allianz)

2.2.3.車載決済

2.2.4.インフォテインメント・ハードウェア

2.2.5.インフォテインメント(1)

2.2.6.インフォテインメント(2)

2.2.7.サービスとしてのハードウェア(HaaS)

2.2.8.無線アップデート

2.2.9.無線診断

2.2.10.サービスとしてのオートノミー(AaaS)

2.2.11.パーソナライゼーション

2.3.SDV サービスとアプリケーション ハードウェア

2.3.1.SDV ハードウェア要件

2.3.2.通信

2.3.3.コンピューティング

2.3.4.接続機能を容易にするための画面(1)

2.3.5.接続機能を容易にする画面(2)

2.3.6.車載用透明アンテナ

2.3.7.欧州で中国製SDVを販売 - BYD

2.4.SDVサービスソフトウェアのケーススタディ

2.4.1.フォード

2.4.2.mg(SAIC)

2.4.3.フォルクスワーゲン

2.4.4.BMW (1) - コネクテッド・ドライブ・ポータル

2.4.5.BMW (2) - SDVマネタイズ

2.4.6.BMW (3) - コネクテッド・パッケージ

2.4.7.BMW (4) - 国際戦略

2.4.8.SDV E/Eアーキテクチャー紹介

2.4.9.スマート・コックピット・ソフトウェア・アーキテクチャ

2.4.10.車両制御ソフトウェア・アーキテクチャ

2.5.SDV E/E アーキテクチャ

2.5.1.自動車 E/E アーキテクチャのパラダイムシフト

2.5.2.SDV E/E アーキテクチャのプレーヤー

2.5.3.従来のイーサネットの後継として光ファイバーが登場

2.5.4.インテル

2.5.5.クアルコム

2.5.6.黒ゴマ(1)

2.5.7.黒ゴマ(2)

2.5.8.ユニティ

2.6.ゾーン制御による集中コンピューティング

2.6.1.SDV E/E アーキテクチャ - OEMレベルのゾーン制御アーキテクチャ(1)

2.6.2.SDV E/E アーキテクチャ - OEMレベルのゾーン制御アーキテクチャ(2)

2.6.3.SDV E/E アーキテクチャ - ティア1レベルのゾーン制御アーキテクチャ(1)

2.6.4.SDV E/E アーキテクチャ - ティア1レベルのゾーン制御アーキテクチャ(2)

2.6.5.SDV E/Eアーキテクチャ - ティア1レベルのゾーン制御アーキテクチャ(3)

2.7.ゾーンアーキテクチャのMCU

2.7.1.SDV E/E アーキテクチャ - マイクロコントローラ・ユニット

2.7.2.インフィニオン - AURIX TC4x

2.7.3.Infineon - Flexモジュールゾーン

2.7.4.NXPS32 CoreRideプラットフォーム

2.7.5.ルネサスRH850/U2x および Zone-ECU 仮想化プラットフォーム

2.7.6.STマイクロエレクトロニクス:Stellar および STM32A

2.7.7.インテルACU U310

2.8.OEM の社内 SDV E/E アーキテクチャ

2.8.1.主要 OEM と代表的なモデル/プラットフォーム

2.8.2.BMW --- ノイエクラッセ (1)

2.8.3.BMW --- ノイエ・クラッセ (2)

2.8.4.BMW --- 中国におけるノイエクラッセ SDVプラットフォーム (1)

2.8.5.BMW --- 中国におけるノイエクラッセ SDV プラットフォーム (2)

2.8.6.テスラ

2.8.7.VW.OS EEA

2.8.8.OPPO フォルクスワーゲン

2.8.9.Rivian フォルクスワーゲン

2.8.10.Toyota Arene OS

2.8.11.ステランティス

2.8.12.AWS SDV

2.8.13.Xpeng

2.8.14.メルセデス

2.9.SDVのためのジェネレーティブAI

2.9.1.ジェネレーティブAIとは

2.10.車載ジェネレーティブAI

2.10.1.スマート・コックピット

2.10.2.パーソナルアシスタントのスパイク(AWS & BMW)

2.10.3.パーソナライズされたデジタルアシスタント(AWS)

2.11.自動車メーカーのためのジェネレーティブAI

2.11.1.自動車デザインのためのジェネレーティブAI

2.11.2.Vizcom (powered by Nvidia)

2.11.3.マイクロソフト - 自動車向けAI

2.11.4.マイクロソフト - M365コパイロット

2.11.5.デジタル・ツインズとシミュレーテッド・オートノミー

2.11.6.Nvidia デジタル・ツインとシミュレーテッド・オートノミー

2.11.7.SDV関連規制

2.12.結論

2.12.1.SDVの結論と要点 (1)

2.12.2.SDV の結論と要点(2)

3. V2X とコネクテッドビークル技術

3.1.1.V2Xの略語

3.1.2.コネクテッド・ビークルとは

3.1.3.なぜV2Xなのか

3.1.4.無線アクセス技術の比較(1)

3.1.5.コネクテッド・ビークルの主要用語

3.1.6.無線アクセス技術の比較(2)

3.1.7.無線アクセス技術の比較

3.1.8.無線アクセス技術の比較

3.1.9.3GPP 5Gの解釈

3.1.10.ポリシーの解釈中国における自動車・道路・クラウドの統合開発

3.1.11. 3GPP自動車ロードマップ

3.1.12.規制状況:DSRC vs C-V2X (1)

3.1.13.規制状況:DSRCとC-V2Xの比較(2)

3.1.14.規制状況:DSRCとC-V2Xの比較(3)

3.1.15.V2X 低遅延(PC5)のユースケース

3.1.16.V2X High Data Rate(Uu)のユースケース

3.1.17.コネクテッドカーのサイバーセキュリティ

3.1.18.C-V2Xロードマップ(第3版)

3.2.安全と持続可能性のためのV2VとV2Iのユースケース

3.2.1.V2VとV2Iとは何か?

3.2.2.1日目/2日目/3日目

3.2.3.V2VとV2Iの仕組み

3.2.4.V2Xアプリケーションの立ち上げ時期と基準

3.3.現在の「Day 1」V2V/V2Iに依存するユースケース

3.3.1.V2V/V2Iに依存するユースケース (1)

3.3.2.V2V/V2Iに依存するユースケース(2)

3.3.3.V2V/V2I必須のユースケース(3)

3.3.4.V2V/V2Iが必要なユースケース(4)

3.4.V2V/V2Iの恩恵を受ける現在のユースケース

3.4.1.V2V/V2Iの恩恵を受けるユースケース

3.4.2.V2V/V2Iが有益なユースケース

3.4.3.V2V/V2Iユースケースの例

3.5.ケーススタディと 5GAA

3.5.1.ZTE 5G と C-V2X のユースケース

3.5.2.自律走行車向け5G:5GAA

3.5.3.5GAA C-V2Xの概要

3.5.4.5G自動車協会(5GAA)理事とのQ&A(1)

3.5.5.5G自動車協会(5GAA)理事との Q&A (2)

3.5.6.5G 自動車協会(5GAA)理事との質疑応答(3)

3.5.7.C-V2X:5Gネットワークにおける自動バレーパーキング(1)

3.5.8.C-V2X:5Gネットワークにおける自動バレーパーキング(2)

3.6.V2X ITS ハードウェア

3.6.1.V2Xハードウェア:V2Xモジュールの中身

3.6.2.V2Xハードウェア:主要用語の説明

3.6.3.テレマティクス制御ユニット

3.6.4.コネクテッドカーのサプライチェーン

3.6.5.V2V/V2Iサプライチェーン

3.6.6.V2Xチップセット - 比較

3.6.7.V2Xチップセット:クアルコム

3.6.8.V2XチップセットNXP & Huawei

3.6.9.V2Xチップセットオートトークス

3.6.10.V2Xチップセットマーベルとモーニングコア

3.6.11.V2Xモジュールの比較

3.6.12.V2Xモジュール - 比較(2)

3.6.13.V2Xモジュール - 比較(3)

3.6.14.LG Innotekモジュール

3.6.15.アルプスアルパインモジュール

3.6.16.Rolling Wirelessモジュール

3.6.17.V2XハードウェアRSU

3.6.18.村田製作所製モジュール

3.6.19.Quectelモジュール

3.6.20.Cohda Wireless モジュール、OBU、および RSU

3.6.21.Commsignia モジュール、OBU、および RSU

3.6.22.V2Xハードウェア:RSU および OBU

3.6.23.ブラックセサミ RSU

3.6.24.ブラックセサミ RSU

3.6.25.シーメンス RSU

3.6.26.Huawei RSU

3.6.27.将来のモビリティのためのAI強化型路側ユニット(RSU)(2)

3.6.28.C-V2X サイドリンク位置決め用インテリジェント RSU

3.6.29.V2Xソフトウェア

3.6.30.V2Xマイクロモビリティ・ソリューション

3.6.31.コネクテッド・ビークル まとめと考察

4.自律走行コネクティビティ

4.1.1.なぜ自動車を自動化するのか

4.1.2.自動化レベルの詳細

4.1.3.レベル別の自律走行機能

4.1.4.自家用車における自律走行機能のロードマップ

4.1.5.自律走行車の典型的なセンサースイート

4.1.6.レベル1からレベル4までのセンサースイートの進化

4.1.7.自律走行技術

4.1.8.AVにとってセルラー接続が重要な理由

4.1.9.自律走行車のコネクテッドな側面

4.1.10.4Gと5Gの比較

4.1.11.4Gと5Gの比較

4.1.12.自律走行にとって5Gが重要な理由

4.1.13.オートノミーにとってV2Xサイドリンクが重要な理由(1)

4.1.14.オートノミーにとってV2Xサイドリンクが重要な理由(2)

4.1.15.レベル2要件

4.1.16.レベル3の要件

4.1.17.レベル4(プライベート)の要件

4.1.18.レベル4(ロボットタクシー)の要件

4.1.19.比較される自律性レベルの要件

4.2.マッピングとローカライゼーション

4.2.1.ローカリゼーションとは

4.2.2.ローカライゼーション:絶対的か相対的か

4.2.3.レーンモデル:用途と欠点

4.2.4.HDマッピング資産:ADASマップからレベル5自動運転用フルマップへ

4.2.5.自律走行用HDマップの多くのレイヤー

4.2.6.サービスとしてのHD地図

4.2.7.プレイヤーは誰か?

4.2.8.地図のビジネスモデル

4.2.9.垂直統合型マッパー

4.2.10.カメラ付きHDマッピング

4.2.11.カメラ付きHDマッピング

4.2.12.ディープマップ

4.2.13.シビルマップ

4.2.14.データから地図へのプロセスの半自動化または完全自動化

4.2.15.レーダーマッピング

4.2.16.レーダー測位:ナブテック

4.2.17.レーダー測位ウェーブセンス

4.3.遠隔操作

4.3.1.自律型MaaSの実現

4.3.2.遠隔操作の3つのレベル

4.3.3.遠隔操作の仕組み - Zoox

4.3.4.リモートアシスタンス

4.3.5.遠隔操作

4.3.6.遠隔操作は現在どこで使われているのか?

4.3.7.プレーヤー

4.3.8.MaaSと独立系ソリューション・プロバイダー

4.3.9.オットピアの高度遠隔操作(1)

4.3.10.オットピアの先進的遠隔操作(2)

4.3.11.AVのバックアップとしてのファントムオートの遠隔操作

4.3.12.ロジスティクスで勢いを増すファントムオート

4.3.13.ヘイロー-自律性を破壊する

5. 予測

5.1.予測内容

5.2.予測手法

5.3.ソフトウェア定義車両レベルガイド

5.4.SDV予測手法

5.5.SDV 世界の車両総販売台数予測(台)

5.6.SDV世界総販売台数予測(台)

5.7.SDV予測手法

5.8.SDV世界車両販売台数予測(ハードウェア収入)

5.9.SDVの予測(ハードウェア収入)

5.10.SDVフィーチャー収入予測手法

5.11.SDV 機能関連収入の予測手法

5.12.SDVフィーチャー関連の収入予測(グローバル収入)

5.13.SDVフィーチャー関連の収益予測(グローバル収益)

5.14.V2V/V2I普及予測

5.15.V2V/V2I無線アクセス技術の予測

5.16.V2V/V2I車両販売台数予測

5.17.V2V/V2I 販売台数予測

6.企業プロファイル

6.1.ADASTEC

6.2.AiDEN: Enabling Services on Connected Cars

6.3.AUO

6.4.オートクリプト

6.5.ブラックセサミ

6.6.コンチネンタル

6.7.クルーズ

6.8.エテルノビア車載イーサネット

6.9.イノベイトUK

6.10.JPMorgan モビリティ決済ソリューション:車載決済

6.11.モービルアイ

6.12.Monumo:モーター開発のための人工知能

6.13.NXPセミコンダクターズ

6.14.PIXムービング

6.15.プレアクト・テクノロジーズソフトウェア定義センサー

6.16.クアルコムセンスID

6.17.レコグニ-二ューラルネットワーク加速自律走行車コンピューティング

6.18.TCLテクノロジー

6.19.ヴィジョノックス

6.20.ウェイモ自律走行トラック

6.21.ゼロステック

Summary

SDVs, Connected and Autonomous Vehicles (CAVs), In-Car AI Assistants, V2X, Autonomy as a Service, Connected Vehicles, E/E Architecture, Intelligent Transportation Systems (ITS-G5), DSRC, C-V2X, Features as a Service, ADAS

The automotive industry is undergoing a foundational shift toward software-defined vehicles (SDVs), where functionality, value, and user experience are increasingly governed by software rather than hardware. IDTechEx's report, "Software-Defined Vehicles, Connected Cars, and AI in Cars 2026-2036: Markets, Trends, and Forecasts", offers a comprehensive analysis of this transformation, covering the evolution of in-vehicle electrical/electronic (E/E) architecture, connectivity platforms, feature monetization models, and long-term market forecasts. According to IDTechEx forecasts, Central Compute and quasi-zonal SDV platforms are set to generate around US$755 billion in hardware revenue by 2029, becoming the key source of value uplift for OEMs. SDV feature-related revenue is expected to grow at a 30-34% CAGR through 2035, driven by connectivity and autonomy-based service monetization.

From ECUs to Central Compute: The Rise of SDV Architectures

Modern SDVs are defined by their ability to decouple hardware from software, supported by centralized computing platforms and over-the-air (OTA) update capabilities. This report classifies SDVs across five levels, from gateway-centric and domain-based systems to fully software-centric vehicles and provides a detailed breakdown of the key enabling components, including high-performance compute (HPC), zonal controllers, and service-oriented middleware.

The report analyzes flagship platforms such as BMW's Neue Klasse, Tesla's FSD-capable models, and emerging Chinese SDVs from BYD, NIO, and Li Auto. It also explains how these vehicles use technologies like TSN Ethernet, AI-enabled SoCs, and solid-state power distribution to reshape the EE landscape.

Monetization in the SDV Era: Features-as-a-Service and In-Vehicle Commerce

SDVs are not only a technical upgrade, they represent a shift in the business model. Automakers are increasingly embedding monetizable features in the vehicle, ranging from advanced driver assistance systems (ADAS) to infotainment, personalization, and even heating functions.

The report outlines how OEMs like BMW, Ford, and Mercedes-Benz are leveraging features-as-a-service (FaaS) and OTA updates to generate recurring revenue. It investigates subscription models, regional pricing strategies, and the impact of SDV features on customer retention and brand differentiation.

Case studies highlight real-world deployments, including BMW's Neue Klasse, and in-car payment platforms powered by Mastercard and JPMorgan Mobility Payments.

V2X Connectivity and Infrastructure Readiness

As vehicles become more autonomous and connected, V2X (Vehicle-to-Everything) technologies play an essential role in ensuring safety, coordination, and enhanced user experience. This report provides a deep dive into C-V2X, DSRC, and 5G-based communications, evaluating their performance, cost, and geographic adoption.

IDTechEx maps spectrum allocations and policy developments across key regions including China, the EU, the US, Japan, and South Korea. The report also profiles major V2X hardware providers and explains how onboard units (OBUs), roadside units (RSUs), and chipsets are integrated into SDV platforms.

Generative AI and the Intelligent Cabin

The report also explores the integration of generative AI in SDVs, particularly in in-car assistants, personalized infotainment, and predictive diagnostics. With companies like Qualcomm, Nvidia, and Unity enabling on-device AI inference, new opportunities are emerging for OEMs to offer adaptive and immersive digital experiences.

Beyond voice control, the SDV cockpit is becoming a digital platform. Full-width screens, AI avatars, and customizable software skins are creating a new battleground for brand loyalty and user engagement.

Forecasts to 2036: SDV Adoption and Revenue Outlook

This IDTechEx report provides 10-year market forecasts on the SDV market for the period 2026-2036, in both volume and market value. Forecasts include:

By 2029, quasi-zonal SDV platforms are forecast to reach US$755 billion in hardware revenue, while feature-based monetization could grow at a 30-34% CAGR, reaching hundreds of billions in cumulative revenue by 2035.

Key Aspects

1. Executive Summary

An overview of the shift from hardware-defined to software-defined paradigms in the automotive industry, highlighting key industry trends, technical enablers, and monetization strategies.

2. Software-Defined Vehicles

Coverage of next-generation SDV architectures expected around 2025, including:

3. V2X and Connected Vehicle Technology

Evaluation of the technologies and infrastructure that enable connected vehicles:

4. Autonomous Vehicle Connectivity

Assessment of the role of connectivity in autonomous driving capability:

5. Forecasts (2025-2036)

Quantitative forecasts for SDV penetration and V2X uptake:

Table of Contents1. EXECUTIVE SUMMARY

1.1. What is a software-defined vehicle?

1.2. What's required for an SDV

1.3. Software-Defined Vehicle Level Guide

1.4. SDV Level Chart: Major OEMs compared

1.5. SDV Level Guide Explained

1.6. SDV feature layer

1.7. Mainstream OEMs and Representative Models/Platforms

1.8. SDV E/E Architecture - Microcontroller Unit

1.9. SDV E/E Architecture players

1.10. SDV Conclusions and Key Takeaways (1)

1.11. SDV Conclusions and Key Takeaways (2)

1.12. Over-the-Air updates and diagnostics

1.13. Software-Defined Vehicle Forecast (Units)

1.14. SDV Forecast (Hardware Revenue)

1.15. What is a Connected Vehicle?

1.16. Connected Vehicles Key Terminology

1.17. Radio Access Technologies Compared

1.18. The Connected Vehicle Supply Chain

1.19. V2X Chipsets - Comparison

1.20. Radio Access Technologies Compared

1.21. Radio Access Technologies Compared

1.22. Example V2V/V2I use cases summarised

1.23. V2X Regional Regulatory Status

1.24. V2V/V2I Uptake Forecasting

1.25. V2V/V2I Radio Access Technology Forecast

1.26. Why 5G Matters for Autonomy

1.27. Company Profiles

1.28. Access More With an IDTechEx Subscription

2. SOFTWARE-DEFINED VEHICLES

2.1.1. What is a software-defined vehicle?

2.1.2. Why is there this hype? (1)

2.1.3. Why is there this hype? (2)

2.1.4. Software-Defined Vehicle Level Guide

2.1.5. SDV Level Chart: Major OEMs compared

2.2. SDV Service and Applications

2.2.1. Connectivity as a Service

2.2.2. SDV for Insurance (Allianz)

2.2.3. In-vehicle payments

2.2.4. Infotainment hardware

2.2.5. Infotainment (1)

2.2.6. Infotainment (2)

2.2.7. Hardware as a Service (HaaS)

2.2.8. Over-the-Air updates

2.2.9. Over-the-Air diagnostics

2.2.10. Autonomy as a Service (AaaS)

2.2.11. Personalization

2.3. SDV Service and Applications Hardware

2.3.1. SDV Hardware Requirements

2.3.2. Communication

2.3.3. Compute

2.3.4. Screens to facilitate connected features (1)

2.3.5. Screens to facilitate connected features (2)

2.3.6. Automotive transparent antennas

2.3.7. Selling a Chinese SDV in Europe - BYD

2.4. SDV Service Software Case Study

2.4.1. Ford

2.4.2. MG (SAIC)

2.4.3. Volkswagen

2.4.4. BMW (1) - Connected Drive Portal

2.4.5. BMW (2) - SDV Monetization

2.4.6. BMW (3) - Connected Package

2.4.7. BMW (4) - International Strategy

2.4.8. SDV E/E Architecture Introduction

2.4.9. Smart Cockpit Software Architecture

2.4.10. Vehicle Control Software Architecture

2.5. SDV E/E Architecture

2.5.1. Paradigm Shift in Automotive E/E Architectures

2.5.2. SDV E/E Architecture players

2.5.3. Optical Fiber Emerges as a Successor to Traditional Ethernet

2.5.4. Intel

2.5.5. Qualcomm

2.5.6. Black sesame (1)

2.5.7. Black sesame (2)

2.5.8. Unity

2.6. Centralized Computing with Zonal Control

2.6.1. SDV E/E Architecture - OEM Level Zonal Control Architecture (1)

2.6.2. SDV E/E Architecture - OEM Level Zonal Control Architecture (2)

2.6.3. SDV E/E Architecture - Tier 1 Level Zonal Control Architecture (1)

2.6.4. SDV E/E Architecture - Tier 1 Level Zonal Control Architecture (2)

2.6.5. SDV E/E Architecture - Tier 1 Level Zonal Control Architecture (3)

2.7. MCU in Zonal Architecture

2.7.1. SDV E/E Architecture - Microcontroller Unit

2.7.2. Infineon - AURIX TC4x

2.7.3. Infineon - Flex Modular Zone

2.7.4. NXP: S32 CoreRide Platform

2.7.5. Renesas: RH850/U2x and Zone-ECU Virtualization Platform

2.7.6. STMicroelectronics: Stellar and STM32A

2.7.7. Intel: ACU U310

2.8. OEMs' in-house SDV E/E Architecture

2.8.1. Mainstream OEMs and Representative Models/Platforms

2.8.2. BMW --- Neue Klasse (1)

2.8.3. BMW --- Neue Klasse (2)

2.8.4. BMW --- Neue Klasse SDV platform in China (1)

2.8.5. BMW --- Neue Klasse SDV platform in China (2)

2.8.6. Tesla

2.8.7. VW.OS EEA

2.8.8. OPPO Volkswagen

2.8.9. Rivian Volkswagen

2.8.10. Toyota Arene OS

2.8.11. Stellantis

2.8.12. AWS SDV

2.8.13. Xpeng

2.8.14. Mercedes

2.9. Generative AI for SDVs

2.9.1. What is a Generative AI?

2.10. In-vehicle generative AI

2.10.1. Smart Cockpit

2.10.2. Spike the personal assistant (AWS & BMW)

2.10.3. A personalized digital assistant (AWS)

2.11. Generative AI for automakers

2.11.1. Generative AI for Automotive Design

2.11.2. Vizcom (powered by Nvidia)

2.11.3. Microsoft - AI for automotive

2.11.4. Microsoft - M365 Copilot

2.11.5. Digital Twins and Simulated Autonomy

2.11.6. Nvidia Digital Twins and Simulated Autonomy

2.11.7. SDV-related Regulations

2.12. Conclusion

2.12.1. SDV Conclusions and Key Takeaways (1)

2.12.2. SDV Conclusions and Key Takeaways (2)

3. V2X AND CONNECTED VEHICLE TECHNOLOGY

3.1.1. V2X Acronyms

3.1.2. What is a Connected Vehicle?

3.1.3. Why V2X

3.1.4. Radio Access Technologies Compared (1)

3.1.5. Connected Vehicles Key Terminology

3.1.6. Radio Access Technologies Compared (2)

3.1.7. Radio Access Technologies Compared

3.1.8. Radio Access Technologies Compared

3.1.9. 3GPP 5G Interpretation

3.1.10. Policy Interpretation: Integrated Vehicle-Road-Cloud Development in China

3.1.11. 3GPP Automotive Roadmap

3.1.12. Regulatory Status: DSRC vs C-V2X (1)

3.1.13. Regulatory Status: DSRC vs C-V2X (2)

3.1.14. Regulatory Status: DSRC vs C-V2X (3)

3.1.15. V2X Low Latency (PC5) use cases

3.1.16. V2X High Data Rate (Uu) use cases

3.1.17. Connected Vehicle Cybersecurity

3.1.18. C-V2X roadmap (third edition)

3.2. V2V and V2I Use Cases for Safety and Sustainability

3.2.1. What is V2V and V2I?

3.2.2. Day 1/Day 2/Day 3

3.2.3. How V2V and V2I works:

3.2.4. V2X applications Launch Timeline and Standard

3.3. Current 'Day 1' V2V/V2I dependent use cases

3.3.1. V2V/V2I-required use cases (1)

3.3.2. V2V/V2I-required use cases (2)

3.3.3. V2V/V2I-required use cases (3)

3.3.4. V2V/V2I-required use cases (4)

3.4. Current use cases that benefit from V2V/V2I

3.4.1. V2V/V2I-beneficial use cases

3.4.2. V2V/V2I-beneficial use cases

3.4.3. Example V2V/V2I use cases summarised

3.5. Case Studies and the 5GAA

3.5.1. ZTE 5G and C-V2X use cases

3.5.2. 5G for Autonomous Vehicles: 5GAA

3.5.3. 5GAA C-V2X overview

3.5.4. Q&A with 5G Automotive Association (5GAA) director (1)

3.5.5. Q&A with 5G Automotive Association (5GAA) director (2)

3.5.6. Q&A with 5G Automotive Association (5GAA) director (3)

3.5.7. C-V2X: Automated valet parking in a 5G network (1)

3.5.8. C-V2X: Automated valet parking in a 5G network (2)

3.6. V2X ITS Hardware

3.6.1. V2X Hardware: What's in a V2X module

3.6.2. V2X Hardware: Key terms explained

3.6.3. Telematics Control Unit

3.6.4. The Connected Vehicle Supply Chain

3.6.5. V2V/V2I Supply Chain

3.6.6. V2X Chipsets - Comparison

3.6.7. V2X Chipsets: Qualcomm

3.6.8. V2X Chipsets: NXP & Huawei

3.6.9. V2X Chipsets: Autotalks

3.6.10. V2X Chipsets: Marvell and Morningcore

3.6.11. V2X Modules - Comparison

3.6.12. V2X Modules - Comparison (2)

3.6.13. V2X Modules - Comparison (3)

3.6.14. LG Innotek Modules

3.6.15. Alps Alpine Modules

3.6.16. Rolling Wireless Modules

3.6.17. V2X Hardware: RSUs

3.6.18. Murata Modules

3.6.19. Quectel Modules

3.6.20. Cohda Wireless Modules, OBUs, & RSUs

3.6.21. Commsignia Modules, OBUs, & RSUs

3.6.22. V2X Hardware: RSUs and OBUs

3.6.23. Black Sesame RSUs

3.6.24. Black Sesame RSUs

3.6.25. Siemens RSUs

3.6.26. Huawei RSUs

3.6.27. AI-enhanced roadside unit (RSU) for future mobility (2)

3.6.28. Intelligent RSU for C-V2X side link positioning

3.6.29. V2X Software

3.6.30. V2X micromobility solutions

3.6.31. Connected Vehicle Conclusion and Thoughts

4. AUTONOMOUS VEHICLE CONNECTIVITY

4.1.1. Why Automate Cars?

4.1.2. The Automation Levels in Detail

4.1.3. Functions of Autonomous Driving at Different Levels

4.1.4. Roadmap of Autonomous Driving Functions in Private Cars

4.1.5. Typical Sensor Suite for Autonomous Cars

4.1.6. Evolution of Sensor Suites from Level 1 to Level 4

4.1.7. Autonomous driving technologies

4.1.8. Why is cellular connectivity important for AVs

4.1.9. Connected aspects of Autonomous Vehicles

4.1.10. 4G compared to 5G

4.1.11. 4G compared to 5G visualized

4.1.12. Why 5G Matters for Autonomy

4.1.13. Why V2X Sidelink Matters for Autonomy (1)

4.1.14. Why V2X Sidelink Matters for Autonomy (2)

4.1.15. Level 2 Requirements

4.1.16. Level 3 Requirements

4.1.17. Level 4 (Private) Requirements

4.1.18. Level 4 (Robotaxi) Requirements

4.1.19. Autonomy Levels Requirements compared

4.2. Mapping and Localization

4.2.1. What is Localization?

4.2.2. Localization: Absolute vs Relative

4.2.3. Lane Models: Uses and Shortcomings

4.2.4. HD Mapping Assets: From ADAS Map to Full Maps for Level-5 Autonomy

4.2.5. Many Layers of an HD Map for Autonomous Driving

4.2.6. HD Map as a Service

4.2.7. Who are the Players?

4.2.8. Mapping Business Models

4.2.9. Vertically Integrated Mappers

4.2.10. HD Mapping with Cameras

4.2.11. HD Mapping with Cameras

4.2.12. DeepMap

4.2.13. Civil Maps

4.2.14. Semi- or Fully Automating the Data-to-Map Process

4.2.15. Radar Mapping

4.2.16. Radar Localization: Navtech

4.2.17. Radar Localization: WaveSense

4.3. Teleoperation

4.3.1. Enabling Autonomous MaaS

4.3.2. Three Levels of Teleoperation

4.3.3. How remote assistance works - Zoox

4.3.4. Remote assistance

4.3.5. Remote Control

4.3.6. Where is teleoperation currently used?

4.3.7. Players

4.3.8. MaaS vs Independent solution providers

4.3.9. Ottopia's Advanced Teleoperation (1)

4.3.10. Ottopia's Advanced Teleoperation (2)

4.3.11. Phantom Auto's Teleoperation as Back-Up for AVs

4.3.12. Phantom Auto Gaining Momentum in Logistics

4.3.13. Halo - Subverting Autonomy

5. FORECASTS

5.1. Forecasting Content

5.2. Forecasting Methodology

5.3. Software-Defined Vehicle Level Guide

5.4. SDV Forecast Methodology

5.5. SDV Global Total Vehicle Sales Forecast (Units)

5.6. SDV Global Total Vehicle Sales Forecast (Units)

5.7. SDV Forecast Methodology

5.8. SDV Global Vehicle Revenue Forecast (Hardware Revenue)

5.9. SDV Forecast (Hardware Revenue)

5.10. SDV Feature Revenue Forecast Methodology

5.11. SDV Feature Revenue Forecast Methodology

5.12. SDV Feature-related Revenue Forecast (Global Revenue)

5.13. SDV Feature Forecast (Global Revenue)

5.14. V2V/V2I Uptake Forecasting

5.15. V2V/V2I Radio Access Technology Forecast

5.16. V2V/V2I Vehicle Unit Sales Forecasting

5.17. V2V/V2I Unit Sales Forecasting

6. COMPANY PROFILES

6.1. ADASTEC

6.2. AiDEN: Enabling Services on Connected Cars

6.3. AUO

6.4. Autocrypt

6.5. Black Sesame

6.6. Continental

6.7. Cruise

6.8. Ethernovia: Automotive Ethernet

6.9. Innovate UK

6.10. JPMorgan Mobility Payments Solutions: In-Vehicle Payments

6.11. Mobileye

6.12. Monumo: Artificial Intelligence for Motor Development

6.13. NXP Semiconductors

6.14. PIX Moving

6.15. PreAct Technologies: Software-Defined Sensors

6.16. Qualcomm: Sense ID

6.17. Recogni ? Neural Network Accelerated Autonomous Car Computing

6.18. TCL Technology

6.19. Visionox

6.20. Waymo: Autonomous Trucking

6.21.Zelostech

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|