乗用車ADAS市場 2025-2045年:技術、市場分析、予測Passenger Car ADAS Market 2025-2045: Technology, Market Analysis, and Forecasts ここ数年、先進運転支援システム(ADAS)は乗用車市場の中核的な競争要因となっている。特に「レベル2+」は、ハイウェイ・ナビゲート・オン・パイロットやシティ・ナビゲート・オン・パイロットのような、より... もっと見る

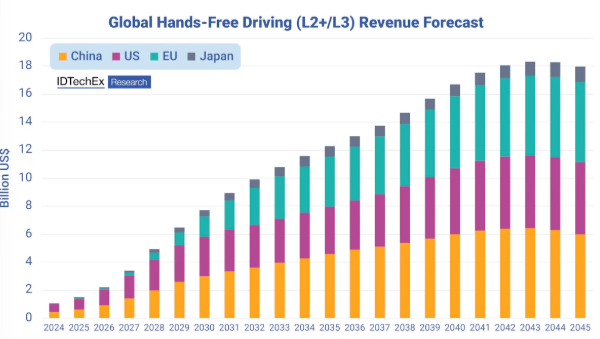

サマリーここ数年、先進運転支援システム(ADAS)は乗用車市場の中核的な競争要因となっている。特に「レベル2+」は、ハイウェイ・ナビゲート・オン・パイロットやシティ・ナビゲート・オン・パイロットのような、より洗練された機能を持つ先進レベル2ADASを表す言葉として登場した。IDTechEx は、L2+ 機能の世界市場は、プレミアム市場と大衆市場の両方の採用とハンズフリー運転機能の台頭によって、2045 年までに 179 億 8,000 万米ドルに達する可能性があると予測している。

レベル2+の台頭長年にわたり、「レベル2+」は従来のレベル2を超える、より洗練された運転支援を表してきた。この "プラス "は、ドライバーが道路から目を離さずに(アイズオン)、ハンドルから手を短時間離すことができることを示している。典型的な高速道路のシナリオにとどまらず、L2+のオペレーショナル・デザイン・ドメイン(ODD)は現在、高速道路のNOA(Navigate on Autopilot)や都市部のNOAにまで拡大しており、レベル3の自律性に向けた重要な足がかりとなっている。

自家用車市場では近年、ハンズフリー運転の採用が急増している。ゼネラルモーターズ(GM)は2017年に初期のスーパークルーズ・システムを導入し、ハンズオフADASの基盤を確立した。2024年までに、GMは20車種以上にスーパークルーズを搭載し、マッピングされた道路を75万マイルまで拡張する。フォードもまた、BlueCruise(L2+)を欧州に導入し、ハンズフリー運転機能で同地域をカバーする最初のOEMとなることで、注目すべきマイルストーンに到達した。一方、中国市場では2023年以降、大手EVメーカーがNOA機能を大規模に展開している。Li Auto、Huawei、XPeng、NIOは、中国の規制がまだ正式に真のハンズフリー運転を認めていないにもかかわらず、それぞれ独自のL2+ NOA機能を展開した。2024年までに、Li Autoは年間50万台以上のL2+車両販売を達成し、ユーザーによるL2+走行距離は29.3億kmに達し、中国の地図なし自動運転システム(ADS)による都市部のNOAカバー率は90%を超えた。

レベル3の苦闘

レベル2+とレベル3の主な違いは、アイズオンがアイズオフになることである。これは事実上、車両がレベル3で作動していると報告している間に起こったことについては、OEMが責任を負うことを意味する。これまでのところ、これを喜んで受け入れているOEMはメルセデスとBMWだけで、メルセデスはドイツ、カリフォルニア、ネバダでレベル3走行を認証しており、BMWはドイツでのみ技術を持っている。

レベル3は2021年から公道での走行が認められており、日本ではホンダがごく小規模ながら導入している。その後、メルセデスが2022年にドイツで、2023年に米国でシステムを認証した。その後、BMWがドイツで認証を取得し、メルセデスは最高運転速度を時速60kmから時速95kmに引き上げる意向を表明した。IDTechExは、2024年末までに、より多くの地域でレベル3認証が取得され、GMとフォードを中心に、より多くの企業が自社の技術を認証すると予想していた。進捗は当初考えられていたよりもはるかに遅れており、このことはIDTechExの予測にも反映されている。IDTechExは現在、レベル2+がより重要な発展の道であり、レベル3は数年後に回復すると見ている。

IDTechExは、レベル3車両のスタートが遅かったことから、その展開と普及は当初の予測よりもはるかに遅れると予想している。これらの自動車で利用可能な技術、レベル3展開を取り巻くすべてのルール、レベル3技術がどのように普及するかについてのIDTechExの予測については、レポート全文を参照。

中国のサプライチェーンとソフトウェア・ハードウェアの相乗効果

中国が迅速にL2+を採用した大きな理由のひとつは、OEM、ソフトウェア・ソリューション・プロバイダー、ハードウェア・サプライヤーにまたがる強固なサプライチェーンの統合である。Momenta、Apollo、WeRideのような企業は、迅速なOEM統合のためにADソフトウェア・スタックを提供している。Huawei社、Mobileye社、Bosch社、Horizon Robotics社、Black Sesame社は、ハードウェアとソフトウェアを組み合わせたソリューションを提供し、従来の自動車メーカーの市場投入までの時間をさらに短縮している。また、社内のクラウドコンピューティングセンター、エンドツーエンドのアルゴリズム設計、社内のLiDAR、レーダー、またはドメインコントローラーの開発によってサポートされる、社内のADSアーキテクチャを採用するOEMもある。IDTechExは、R&Dチームのコスト、クラウドコンピューティング費用、異なるモデルにおけるL2+普及率を考慮した、中国の主要OEMの販売台数と損益分岐点に関するケーススタディを実施した。これは、先進的なADASへの大規模な投資がどの程度で採算に乗るかについての洞察を提供するものである。

加速する ADAS 機能とセンサーの普及

世界的な安全義務化の高まりにより、AEB(自動緊急ブレーキ)などのアクティブ・セーフティ機能が急成長し、カメラ、レーダー、LiDAR、ドメイン・コントローラーの導入が増加している。AEBは当初、前方カメラに依存するかもしれないが、多くの場合、前方レーダーと融合させることで精度が向上する。レーンチェンジアシストにはサイドレーダーや超音波センサーが必要になるかもしれないが、360°サラウンドビューにはパノラマ画像をつなぎ合わせるために少なくとも4台のカメラが必要になる。IDTechEx は、乗用車における 14 の主要な L1-L2+/L3 ADAS 機能を特定し、地域別(米国、欧州、中国、日本)に 20 年間の採用予測を示している。センサーコスト、SoC価格、ソフトウェアライセンス料を分析することで、本レポートは各ADAS機能の収益予測を行い、SAE L0-L2+を取り巻く市場発展への洞察を提供している。

本レポートは、基本的なL0~L1の安全ADAS機能、L2のラグジュアリー機能、レベル2+(ハンズオフ、アイズオン)の展開における自動車メーカーの進捗状況を、カバーされた道路の総走行距離や各地域で遭遇した規制上の課題も含めて包括的に概観している。また、純粋なビジョンからLiDAR依存のフュージョン・アルゴリズムまで、L2+ソリューションに採用されているセンサー・アレイの範囲を検証し、異なるコスト構造が異なる車両セグメントにどのように整合するかを説明している。さらに、現在入手可能なL2+モデルのリスト、センサー構成、価格、市場分析も含まれている。

主な内容

乗用車のADAS車両をSAEレベルでカバー

ADAS機能とセンサーの自家用車への採用率、2020年から2023年に販売された車両からの採用率

L2+ADAS 乗用車の性能

ADAS車両販売台数の20年予測、機能別販売台数

目次

1.はじめに

1.1. レポートの要約と主な要点

1.2. 自動運転レベル(L0~L5)の概要

1.3. 個人所有の自律走行車の概要

1.4. レベル2+の定義、利用可能性、法規制が固まる

1.5. 最大の障壁はL3またはL4への移行 - 責任

1.6. レベル2+は長期的な中間地点となる可能性

1.7. 自律走行車が合法な地域の概要

1.8. ADASの主要機能の採用は2023年に再び増加

1.9. SAE Level 2の採用が前年比で増加

1.10. 高レベルの自律走行は、1台当たりのセンサーの増加を意味する

1.11. LiDARはレベル3と中国市場向け

1.12. 自律走行は自動車サプライチェーンを変える

1.13. L2+ 乗用車市場のサプライチェーン概要

1.14. 中国都市部の L2+ 市場の急成長が ADAS サプライヤーの売上急増を牽引

1.15. 中国 L2+ / NOA ソリューション・プロバイダー/サプライヤー

1.16. エンド・ツー・エンド(E2E)アーキテクチャ

1.17. EU市場概要:L2が優勢、L2+とL3は模索段階 - 消費者の選択への影響は限定的

1.19. 中国市場概要:L2+が主要な購入促進要因として台頭、サプライチェーンの優位性が競争力を高める

1.20. 米国市場サマリー:強固なL2 ADAS基盤、L2+/L3成長の高い可能性

1.21. 米国における2022-2045年の自律走行車普及

1.22. 中国における2022-2044年の自律走行車普及

1.23. 日本における自律走行車の普及 2022-2044

1.25. L2+/L3機能の地域別普及予測

1.26. 世界のSAEレベル別自動車販売台数とピークカー 2022-2045

1.27. 駐車支援機能の採用予測

2. はじめに

2.1. レベル2、レベル2+、レベル3

2.2. L3レベルの乗用車が公道使用を承認

2.3. 自動化レベルの詳細

2.4. L2およびL2+の自律走行システムとブランド

2.6. L3レベルの乗用車が試験および路上使用を承認

2.7. IDTechExのADAS機能データベース

3. はじめに

3.1.1. 自動化レベル(L0~L5)の概要

3.1.2. 民間所有の自律走行車の概要

3.1.3. 定義、利用可能性、法規制が固まりつつあるレベル2+

3.1.4. 最大の障壁はL3またはL4への移行 - 責任

3.1.5. レベル2+は長期的な中間地点となる可能性がある

3.2. ADASの特徴

3.2.1. L0~L2乗用車における安全性および高級ADAS機能の概要

3.2.2. 安全 ADAS 機能-AEB

3.2.4. 高級 ADAS 機能-CC/ACC

3.2.5. ADAS 機能-LDW/LKA/LCA

3.2.6. 安全 ADAS 機能-BSM/BSD

3.2.7. 安全 ADAS 機能-信号認識

3.2.8. ラグジュアリー ADAS 機能 - オートパーキング

4. ADAS AUTOMATION TRENDS AND REGULATIONS

4.1. 法規制と自律性

4.2. 米国

4.3. レベル 3、法規制、米国

4.4. 英国

4.5. EU

4.6. 欧州におけるレベル3の展望

4.8. アジア太平洋(中国) - 試験規模が拡大、規制の枠組みが深化

4.9. 北京、上海、深圳でL3、L4自律走行の展開が加速

4.10. 世界の法規制における責任の種類と前提の明確化

4.12. より包括的な規制の枠組みが世界的に構築されつつある

5. ADAS自動車市場の分析

5.1.1. 乗用車ADAS自動車市場の準備

5.1.2. 米国におけるADAS機能の展開

5.1.3. 中国におけるADAS機能の展開

5.1.4. EUにおけるADAS機能の展開

5.1.5. 日本におけるADAS機能の展開

5.1.6. 中国ADASエコシステム: 中国 L2+ / NOA ソリューション・プロバイダー/サプライヤー

5.1.8. 中国 OEM - L2+ / NOA 開発タイムライン

5.1.9. 中国 OEM - L2+ / NOA 開発

5.1.10. 主要OEM - L2+/NOA開発

5.1.12. マルチセンサーとピュアビジョンソリューションの比較

5.1.13. 中国OEM - NOA用センサー構成の分析

5.1.14. 自動車におけるエンド・ツー・エンド・モデルの展開

5.1.16. 中国のトップ 4 LiDAR メーカーが 2024 年市場を独占

5.1.17. ADAS ティア 1 サプライヤーは前例のない課題に直面している

5.1.18. 2025 年の ADAS ティア 1 製品リスト

5.2. ADAS ソリューション・プロバイダー

5.2.1.Horizon Robotics

5.2.4. DJI Automotive (Zhuoyu)

5.2.5. BOSCH

5.2.6. Huawei

5.2.7. Mobileye

5.2.8. Qcraft

5.3.Socメーカー

5.3.1. ADS SoCチップの競争環境

5.3.2. ADS SoCチップの競争環境 - ケーススタディ

5.3.3. 三大SoCメーカー - Nvidia

5.3.4. 三大SoCメーカー - Mobileye

5.3.5.三大SoCメーカー - Horizon Robotics

5.3.6. 低性能SoCチップ

5.3.7. 中性能SoCチップ

5.3.8. 高性能SoCチップ

5.3.9. 高性能SoCチップ - SoCチップの性能進化

5.3.10. 代表的なモデルの特徴 Urban NOA / L2+ Functionality

5.4. ADAS 車向けセンサースイート

5.4.1. センサースイートの免責事項

5.4.2. センサースイートの進化 Level 1 から Level 4 へ

5.4.3. センサとその目的

5.4.4.レベル1からレベル4までのセンサースイートの進化

5.4.5. ADAS乗用車の代表的なセンサースイート - カメラとレーダー

5.4.6. 一体型フロントビューカメラ

5.4.7. 一体型フロントビューカメラ:

5.4.8.ロントビュー一体型カメラサプライヤー一覧:

5.4.9. フロントビュー一体型カメラサプライヤー一覧: L2+の能力を満たすために徐々に改善する性能 (1)

5.4.10:フロントレーダーの用途

5.4.11. サイドレーダーの役割

5.4.12. 1台あたりのフロントレーダーとサイドレーダー

5.4.13. SAEレベル別の1台あたりのレーダー総数

5.4.自律走行用外部カメラ

5.4.15. LiDARの展開

5.4.16. テクノロジー別自動車用ライダーのプレーヤー

5.5. L2、L2+、L2++ Navigation on Autopilot (NOA) レースの主要OEM

5.5.1. 日産

5.5.2. 日産Propilot 2.1

5.5.3. ホンダ

5.5.4. ホンダセンシング 360+ センサスイート

5.5.5. ステランティス

5.5.6. メルセデス S クラスおよび EQS

5.5.7. メルセデス S クラス - センサスイート

5.5.8.Daimler/Bosch Atonomous Parking

5.5.9. BMW level 3 and level 2+

5.5.10. BMW 7 Series and 5 Series Sensors

5.5.11. Tesla

5.5.12. Tesla's Hardware 4.0

5.5.13. Algorithm Side: GMのスーパークルーズ

5.5.15. GMのスーパークルーズ搭載車

5.5.16. フォードのブルークルーズ

5.5.17. トヨタとレクサス

5.5.18. 中国OEM - AITO(ファーウェイ)

5.5.19. 中国OEM - Xpeng

5.5.20. 中国 OEM - Avata(ファーウェイ ADS)

5.5.22. 中国 OEM - Arcfox(ファーウェイ ADS)

5.5.23. 中国 OEM - Lotus

5.5.24. 中国 OEM - Xiaomi

5.5.25. 中国 OEM - Li Auto

5.5.26. 中国 OEM - Zeekr

5.6.コスト構造とビジネスモデルの分析

5.6.1. 主要メーカーのコスト構造

5.6.2. リーダー企業

5.6.3. 主要メーカーのコスト構造 - 中国OEMのケーススタディ

5.6.4. 主要メーカーのコスト構造

5.6.5. ADAS 機能販売モデル

5.6.7. 販売台数と損益分岐点のケーススタディ

5.6.8. 販売台数と損益分岐点の算出

5.6.9. ADAS 機能販売モデル

6. ENABLING ECHNOLOGIES:LIDAR, RADAR, CAMERAS, INFRARED, HD MAPPING, TELEOPERATION, 5G AND V2X

6.1. はじめに

6.1.1. コネクテッドカー

6.1.2. ローカリゼーション

6.1.3. AIとトレーニング

6.1.4. 遠隔操作

6.1.5. サイバーセキュリティ

6.2. 自律走行センサー

6.2.1. 主な3つのセンサー - カメラ、レーダー、LiDAR

6.2.3. センサーの性能と傾向

6.2.4. 悪天候に対する堅牢性

6.2.5. センサー・スイートの進化 レベル1からレベル4まで

6.2.6. センサー・フュージョンとは何か?

6.2.7. 自動運転には異なる検証システムが必要

6.2.8. アプリケーションのためのセンサーフュージョン技術動向

6.2.9. センサーフュージョンのためのハイブリッドAI

6.2.10. 自動運転と電気自動車

6.2.11. EVの航続距離短縮

6.2.12. 都市交通における交通弱者の課題

6.2.歩行者の危険検知

6.2.14. SAE レベル 2 からレベル 4 & Robotaxi に推奨されるセンサースイート

6.2.15. カメラ

6.2.16. 赤外線カメラ

6.2.17. レーダー

6.2.18. LiDAR

6.2.19. マッピングとローカリゼーション

6.3. コネクテッドカー

6.3.1. コネクテッドカーとは何か?

6.3.2.ぜ V2X なのか

6.3.3. コネクテッド・カー:テクノロジー

6.3.4. コネクテッドカー:ユースケースとケーススタディ

7. フォーキャスト:ADAS 市場の動向と成長予測

7.1. 予測手法: L2+/L3機能の地域別導入予測

7.3. ADAS 機能の地域別導入予測 - 米国

7.4. ADAS 機能の地域別導入予測 - 中国

7.5. ADAS 機能の地域別導入予測 - EU

7.6. ADAS 機能の地域別導入予測 - 日本

7.7.米国における自律走行車の導入 2022-2045

7.9. ADAS機能の地域別販売台数-米国

7.10. 中国における自律走行車の導入 2022-2044

7.11. ADAS機能の地域別販売台数-中国

7.12.地域別ADASフィーチャー売上高 - EU + UK + EFTA

7.14. 日本における自律走行車の普及 2022-2044

7.15. 地域別ADASフィーチャー売上高 - 日本

7.16. 高水準ADASフィーチャー予測 - 米国

7.17. ADAS 機能別地域別売上高-中国

7.19. ADAS 機能別地域別売上高-EU + UK + EFTA

7.20. ADAS 機能別地域別売上高-日本

7.21. 駐車支援機能の採用予測

8. COMPANY PROFILES

SummaryOver the past few years, Advanced Driver Assistance Systems (ADAS) have become a core competitive factor in the passenger vehicles market. In particular, "Level 2+" has emerged as a term describing advanced Level 2 ADAS with more sophisticated capabilities, such as Highway navigate on Pilot and City navigate on Pilot. IDTechEx projects that the global market for L2+ functionalities could reach US$17.98 billion by 2045, driven by both premium and mass-market adoption and the rise of hands-free driving features.

The rise of Level 2+ availability

For many years, "Level 2+" has described well-refined driving assistance that goes beyond conventional Level 2. The "plus" indicates that drivers can briefly remove their hands from the wheel while keeping their eyes on the road (eyes-on). Beyond typical highway scenarios, the Operational Design Domain (ODD) for L2+ is now expanding to highway NOA (Navigate on Autopilot) and urban NOA, serving as a vital steppingstone toward Level 3 autonomy.

The private car market has seen a major surge in hands-free driving adoption in recent years. General Motors (GM) introduced early Super Cruise systems in 2017, establishing a foundation for hands-off ADAS. By 2024, GM have over 20 models equipped with Super Cruise and extended mapped roads to 750,000 miles. Ford has also reached a notable milestone by bringing BlueCruise (L2+) to Europe, making it the first OEM to cover the region with hands-free driving capabilities. Meanwhile, the Chinese market has witnessed leading EV makers roll out NOA features at scale since 2023. Li Auto, Huawei, XPeng, and NIO have each deployed their own L2+ NOA features, despite regulations in China that have not yet formally allowed true hands-free driving. By 2024, Li Auto achieved annual L2+ vehicle sales of over 500,000 units and accumulated 2.93 billion km in L2+ driving mileage by users, claiming more than 90% coverage of urban NOA cities through mapless Automated Driving System (ADS) in China.

Level 3 struggling

The key difference between level 2+ and level 3 is that eyes-on becomes eyes-off. This effectively means that the OEM becomes liable for anything that happens while the vehicle is reporting that it is operating at level 3. So far, the only OEMs happy to accept this have been Mercedes and BMW, the forming having certified level 3 driving in Germany, California, and Nevada, and the latter only having the technology in Germany.

Level 3 has been allowed on the roads since 2021, with a very small deployment from Honda in Japan. Following that Mercedes certified its system in Germany in 2022, then in the US in 2023. Since then BMW has certified in Germany and Mercedes has announced intentions to raise its maximum operating speed from 60kph (~40mph) to 95kph (~60mph). By the end of 2024, IDTechEx had expected to see more regions getting level 3 certification and more companies, especially GM and Ford, certifying their technologies. Progress has been much slower than initially thought, something that is reflected in IDTechEx's forecasts. IDTechEx now sees level 2+ as a more significant avenue of development, with level 3 likely to pick up in a few years' time.

Given the slow start that level 3 vehicles have had, IDTechEx now anticipates their deployment and adoption will be much slower than initially predicted. See the full report for the technologies available on these vehicles, all the rules surrounding level 3 deployment, and IDTechEx's forecasts for how level 3 technologies will spread.

China's supply chain and software-hardware synergy

One of the major reasons behind China's swift L2+ adoption is its robust supply chain integration across OEMs, software solution providers, and hardware suppliers. Companies like Momenta, Apollo, and WeRide deliver AD software stacks for rapid OEM integration. Huawei, Mobileye, Bosch, Horizon Robotics, and Black Sesame offer combined hardware-software solutions that further shorten the time to market for traditional automakers. Some OEMs also adopt in-house ADS architecture, supported by in-house cloud computing centers, end-to-end algorithm design, and in-house LiDAR, radar, or domain controller development. IDTechEx conducted a case study on leading Chinese OEMs' Sales Volume and Break-even Point, factoring in R&D team costs, cloud computing expenses, and L2+ penetration rates in different models. This provides insight into how quickly large investments in advanced ADAS might turn profitable.

Accelerating ADAS features and sensor proliferation

Rising global safety mandates have led to rapid growth of active safety functions such as AEB (Automatic Emergency Braking), which in turn drives increased deployment of cameras, radars, LiDARs, and domain controllers. AEB may initially rely on a forward camera, but accuracy often improves when fused with forward-facing radar. Lane Change Assist might call for side radars or ultrasonic sensors, while 360° surround view requires at least four cameras to stitch together a panoramic image. IDTechEx has identified 14 major L1-L2+/L3 ADAS features in passenger vehicles and provides a 20-year forecast of their adoption by region (the US, Europe, China, Japan). By analyzing sensor costs, SoC prices, and software license fees, this report provides revenue projections for each ADAS feature, offering insights into the market development surrounding SAE L0-L2+.

This report offers a comprehensive overview of automakers' progress in basic L0-L1 safety ADAS features, L2 luxury functionality, and Level 2+ (hands-off, eyes-on) deployments, including the total miles of roads covered and the regulatory challenges encountered in different regions. It also examines the range of sensor arrays employed in L2+ solutions, from pure vision to LiDAR-dependent fusion algorithms, explaining how different cost structures align with distinct vehicle segments. Additionally, it includes a list of currently available L2+ models, their sensor configurations, prices, and market analyses.

Key aspects

Coverage of passenger ADAS vehicles at SAE levels

Uptake of ADAS features and sensors on private cars, adoption percentages from vehicles sold in 2020 to 2023 for

L2+ADAS Passenger Vehicle Performance, Sale and Sensor Suites Analysis

Enabling technologies and key developments therein

20-year forecast of private ADAS vehicle sales, and Features sales in:

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Report Summary and Key Takeaways

1.2. Automation Levels (L0 to L5) Overview

1.3. Summary of Privately Owned Autonomous Vehicles

1.4. Level 2+ Solidifying in Definition, Availability, and Legislation

1.5. Biggest Barriers move onto L3 or L4 - Liability

1.6. Level 2+ could be a long-term middle-ground

1.7. Overview of where autonomous cars are legal

1.8. Adoption of Key ADAS Features Increased Again in 2023

1.9. Year-On-Year Increase in SAE Level 2 Adoption

1.10. High Levels of Autonomy Means More Sensors per Vehicle

1.11. LiDAR is for Level 3 and the Chinese Market

1.12. Autonomy is Changing the Automotive Supply Chain

1.13. L2+ Passenger vehicle market supply chain overview

1.14. Rapid Growth in China's Urban L2+ Market Drives ADAS Supplier Sales Surge

1.15. China L2+ / NOA Solution Providers/Suppliers

1.16. End-to-End (E2E) Architecture

1.17. Deployment of End-to-End Models in Vehicles

1.18. EU Market Summary: L2 Dominates, L2+ and L3 in Exploration Phase - Limited Impact on Consumer Choice

1.19. China Market Summary: L2+ Emerges as Key Purchase Driver, Supply Chain Advantages Drive Competitive Edge

1.20. US Market Summary: Strong L2 ADAS Foundation, High Potential for L2+/L3 Growth

1.21. Autonomous Vehicle Adoption in US 2022-2045

1.22. Autonomous Vehicle Adoption in China 2022-2044

1.23. Autonomous Vehicle Adoption in EU + UK + EFTA 2022-2044

1.24. Autonomous Vehicle Adoption in Japan 2022-2044

1.25. L2+/L3 Feature Adoption Forecast by Region

1.26. Global Vehicle Sales and Peak Car by SAE Level 2022-2045

1.27. Parking Assist Features Adoption Forecast

2. INTRODUCTION

2.1. Level 2, Level 2+, and Level 3

2.2. L3-Level Passenger Vehicles Approved for Road Use

2.3. The Automation Levels in Detail

2.4. Roadmap of Autonomous Driving Functions in Private Cars

2.5. L2 and L2+ Autonomous Driving Systems and Brands

2.6. L3-Level Passenger Vehicles Approved for Testing and on road

2.7. IDTechEx's ADAS Feature Database

3. SUMMARY OF ADAS TECHNOLOGIES

3.1. Introduction

3.1.1. Automation Levels (L0 to L5) Overview

3.1.2. Summary of Privately Owned Autonomous Vehicles

3.1.3. Level 2+ Solidifying in Definition, Availability, and Legislation

3.1.4. Biggest Barriers move onto L3 or L4 - Liability

3.1.5. Level 2+ could be a long-term middle-ground

3.2. ADAS Features

3.2.1. Overview of Safety and Luxury ADAS Features in L0-L2 Passenger Vehicles

3.2.2. Overview of ADAS Features in L0-L3 Passenger Vehicles

3.2.3. Safety ADAS Features - AEB

3.2.4. Luxury ADAS Features-CC/ACC

3.2.5. ADAS Features-LDW/LKA/LCA

3.2.6. Safety ADAS Features- BSM/BSD

3.2.7. Safety ADAS Features- Signal Recognition

3.2.8. Safety ADAS Features- Rear/360 Parking

3.2.9. Luxury ADAS Features - Auto Parking

4. ADAS AUTOMATION TRENDS AND REGULATIONS

4.1. Legislation and Autonomy

4.2. US

4.3. Level 3, Legislation, US

4.4. UK

4.5. EU

4.6. Level 2+ starting to grow in Europe

4.7. Level 3 outlook in Europe

4.8. Asia-Pacific (China) - Testing Scale Expands, Regulatory Framework Deepens

4.9. Beijing, Shanghai, and Shenzhen Accelerate Deployment of L3 and L4 Autonomous Driving

4.10. Asia-Pacific (Japan)

4.11. Clarifying Responsibility Types and Assumption in Global Legislation

4.12. More Comprehensive Regulatory Frameworks are Being Established Globally

5. ADAS CARS MARKET ANALYSIS

5.1. Passenger ADAS Vehicle Market readiness

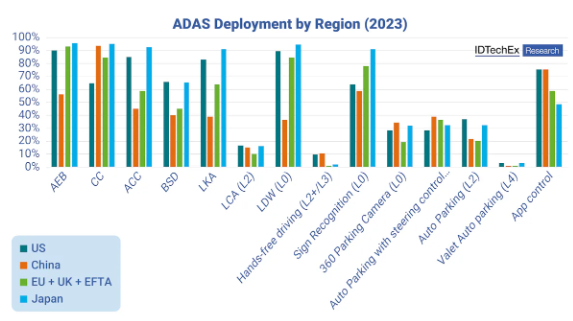

5.1.1. ADAS Adoption by Region in 2023

5.1.2. ADAS Feature Deployment in US

5.1.3. ADAS Feature Deployment in China

5.1.4. ADAS Feature Deployment in EU

5.1.5. ADAS Feature Deployment in Japan

5.1.6. China ADAS Ecosystem: SoC Manufacturers and Solution Providers

5.1.7. China L2+ / NOA Solution Providers/Suppliers

5.1.8. Chinese OEMs - L2+ / NOA development timeline

5.1.9. Chinese OEMs - L2+ / NOA development

5.1.10. US Autonomous Passenger Vehicle Rankings

5.1.11. Main OEMs - L2+ / NOA development

5.1.12. Comparison of Multi-Sensor and Pure Vision Solutions

5.1.13. Chinese OEMs - Analysis of Sensor Configurations for NOA

5.1.14. End-to-End (E2E) Architecture

5.1.15. Deployment of End-to-End Models in Vehicles

5.1.16. China's Top 4 LiDAR Manufacturers Dominate its 2024 Market

5.1.17. ADAS Tier 1 suppliers are facing unprecedented challenges

5.1.18. ADAS Tier 1 Product List 2025

5.2. ADAS Solution Providers

5.2.1. Baidu Apollo

5.2.2. Momenta

5.2.3. Horizon Robotics

5.2.4. DJI Automotive (Zhuoyu)

5.2.5. BOSCH

5.2.6. Huawei

5.2.7. Mobileye

5.2.8. Qcraft

5.3. Soc Manufactures

5.3.1. Competitive Landscape of ADS SoC Chips

5.3.2. Competitive Landscape of ADS SoC Chips - Case study

5.3.3. Three major SoC manufacturers - Nvidia

5.3.4. Three major SoC manufacturers - Mobileye

5.3.5. Three major SoC manufacturers - Horizon Robotics

5.3.6. Low-performance Soc Chips

5.3.7. Mid-performance Soc Chips

5.3.8. High-performance Soc Chips

5.3.9. High-performance Soc Chips - Performance Evolution of SoC Chips

5.3.10. Typical Models features Urban NOA / L2+ Functionality

5.4. Sensor Suite for ADAS Cars

5.4.1. Sensor Suite Disclaimer

5.4.2. Evolution of Sensor Suite From Level 1 to Level 4

5.4.3. Sensors and their Purpose

5.4.4. Evolution of Sensor Suites from Level 1 to Level 4

5.4.5. Typical Sensor Suite for ADAS Passenger Cars - Camera and Radar

5.4.6. Integrated Front-view Cameras

5.4.7. Integrated Front-view Cameras: Regulations are accelerating

5.4.8. List of Integrated Front-view Camera Suppliers: Performance Gradually Improving to Meet L2+ Capabilities (1)

5.4.9. List of Integrated Front-view Camera Suppliers: Performance Gradually Improving to Meet L2+ Capabilities (2)

5.4.10. Front Radar Applications

5.4.11. The Role of Side Radars

5.4.12. Front and Side Radars per Car

5.4.13. Total Radars per Car for Different SAE levels

5.4.14. External Cameras for Autonomous Driving

5.4.15. LiDAR Deployment

5.4.16. Automotive lidar players by technology

5.5. Key OEMs in the L2, L2+,L2++ Navigation on Autopilot (NOA) race

5.5.1. Nissan

5.5.2. Nissan Propilot 2.1

5.5.3. Honda

5.5.4. Honda Sensing 360+ sensor suite

5.5.5. Stellantis

5.5.6. Mercedes S-Class and EQS

5.5.7. Mercedes S-class - Sensor Suite

5.5.8. Daimler/Bosch Autonomous Parking

5.5.9. BMW level 3 and level 2+

5.5.10. BMW 7 Series and 5 Series Sensors

5.5.11. Tesla

5.5.12. Tesla's Hardware 4.0

5.5.13. Algorithm Side: Tesla Adopts End-to-End Large Model

5.5.14. GM's Super Cruise

5.5.15. Vehicles with GM Super Cruise

5.5.16. Ford BlueCruise

5.5.17. Toyota and Lexus

5.5.18. Chinese OEMs - AITO (Huawei)

5.5.19. Chinese OEMs - Xpeng

5.5.20. Chinese OEMs - NIO

5.5.21. Chinese OEMs - Avata (Huawei ADS)

5.5.22. Chinese OEMs - Arcfox (Huawei ADS)

5.5.23. Chinese OEMs - Lotus

5.5.24. Chinese OEMs - Xiaomi

5.5.25. Chinese OEMs - Li Auto

5.5.26. Chinese OEMs - Zeekr

5.6. Cost Structure and Business Model Analysis

5.6.1. Cost Structure for Major Manufacturers

5.6.2. Leaders

5.6.3. Cost Structure for Major Manufacturers - Case Study on Chinese OEMs

5.6.4. Cost Structure for Major Manufacturers

5.6.5. Comparative Analysis of Cloud Computational Power

5.6.6. ADAS Feature Sales Model

5.6.7. Sales Volume and Break-even Point Case Study

5.6.8. Sales Volume and Break-even Point Calculation

5.6.9. ADAS Feature Sales Model

6. ENABLING TECHNOLOGIES: LIDAR, RADAR, CAMERAS, INFRARED, HD MAPPING, TELEOPERATION, 5G AND V2X

6.1. Introduction

6.1.1. Connected vehicles

6.1.2. Localization

6.1.3. AI and Training

6.1.4. Teleoperation

6.1.5. Cyber security

6.2. Autonomous Vehicle Sensors

6.2.1. Autonomous driving technologies

6.2.2. The Primary Three Sensors - Cameras, Radar, and LiDAR

6.2.3. Sensor Performance and Trends

6.2.4. Robustness to Adverse Weather

6.2.5. Evolution of Sensor Suite From Level 1 to Level 4

6.2.6. What is Sensor Fusion?

6.2.7. Autonomous Driving Requires Different Validation System

6.2.8. Sensor Fusion Technology Trends for Applications

6.2.9. Hybrid AI for Sensor Fusion

6.2.10. Autonomy and Electric Vehicles

6.2.11. EV Range Reduction

6.2.12. The Vulnerable Road User Challenge in City Traffic

6.2.13. Pedestrian Risk Detection

6.2.14. Recommended Sensor Suites For SAE Level 2 to Level 4 & Robotaxi

6.2.15. Cameras

6.2.16. IR Cameras

6.2.17. Radar

6.2.18. LiDAR

6.2.19. Mapping and Localization

6.3. Connected Cars

6.3.1. What is a Connected Vehicle?

6.3.2. Why V2X

6.3.3. Connected Cars: Technologies

6.3.4. Connected Cars: Use Cases and Case Studies

7. FORECASTS: ADAS MARKET TRENDS AND GROWTH PROJECTIONS

7.1. Forecasting Methodology: Private Cars Feature Adoption

7.2. L2+/L3 Feature Adoption Forecast by Region

7.3. ADAS Feature Adoption Forecast by Region - US

7.4. ADAS Feature Adoption Forecast by Region - China

7.5. ADAS Feature Adoption Forecast by Region - EU

7.6. ADAS Feature Adoption Forecast by Region - Japan

7.7. Global Vehicle Sales and Peak Car by SAE Level 2022-2045

7.8. Autonomous Vehicle Adoption in US 2022-2045

7.9. ADAS Feature Sales by Region- US

7.10. Autonomous Vehicle Adoption in China 2022-2044

7.11. ADAS Feature Sales by Region- China

7.12. Autonomous Vehicle Adoption in EU + UK + EFTA 2022-2044

7.13. ADAS Feature Sales by Region - EU + UK + EFTA

7.14. Autonomous Vehicle Adoption in Japan 2022-2044

7.15. ADAS Feature Sales by Region- Japan

7.16. High level ADAS Feature Forecast - US

7.17. ADAS Feature Sales Revenue by Region- US

7.18. ADAS Feature Sales Revenue by Region - China

7.19. ADAS Feature Sales Revenue by Region- EU + UK + EFTA

7.20. ADAS Feature Sales Revenue by Region- Japan

7.21. Parking Assist Features Adoption Forecast

8. COMPANY PROFILES

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|