リチウムの直接抽出 2026-2036年:技術、プレーヤー、予測Direct Lithium Extraction 2026-2036: Technologies, Players, Forecasts リチウム直接抽出、硬岩採掘、ブライン蒸発、堆積の10年予測。主要プレーヤー、プロジェクト、技術 - 吸着、イオン交換、溶媒抽出、膜、電気化学。米国、欧州、中国、南米をカバー。 IDTechExのレポート... もっと見る

サマリーリチウム直接抽出、硬岩採掘、ブライン蒸発、堆積の10年予測。主要プレーヤー、プロジェクト、技術 - 吸着、イオン交換、溶媒抽出、膜、電気化学。米国、欧州、中国、南米をカバー。 IDTechExのレポート「直接リチウム抽出 2026-2036年:技術、プレーヤー、予測」は世界のリチウム生産と急成長する直接リチウム抽出(DLE)の展望を深堀りしています。DLEの出現により、リチウム市場は2036年までに520億ドル規模に成長すると予測している。

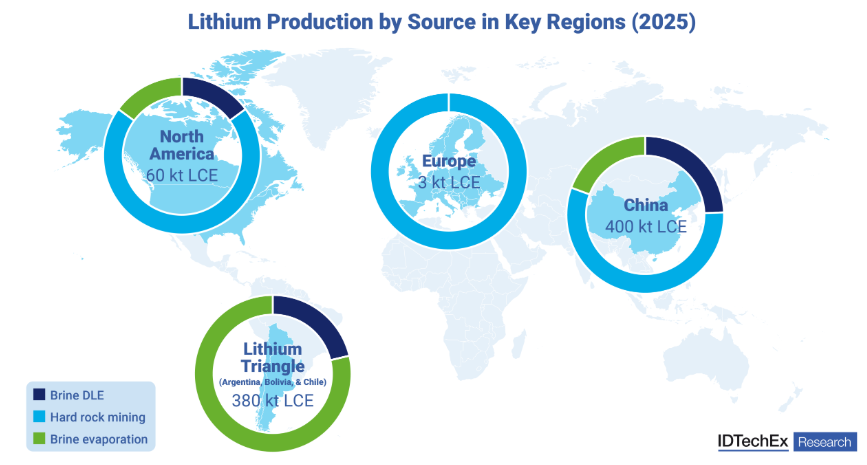

米州、欧州、中国のリチウム生産源:IDTechEx

DLEの成長の原動力は何か?

電気自動車や蓄電システム(BESS)用のリチウムイオン電池市場の急速な拡大が、リチウム需要の急増につながっている。従来のリチウム抽出には、硬い岩石鉱物の採掘か、リチウムを多く含む塩水の蒸発が必要だった。しかし、こうした資源はごく一部の地域(中国とオーストラリアの硬質岩石鉱物、中国とアルゼンチン、ボリビア、チリのリチウム・トライアングルのかん水)に集中しており、どちらの方法にも規模拡大を困難にする欠点がある。

ひとつは、かん水の蒸発プロセスは最終製品に到達するまでに12~24ヵ月を要し、リチウム回収率は40~60%と低い。また、特定の塩水組成や、蒸発池に適した土地と気候も必要となる。一方、硬岩リチウムは自然界にあまり存在せず、採掘には環境への影響が大きい。

蒸発を伴わずにかん水からリチウムをより選択的に抽出できるDLE技術の出現は、世界的な生産に新たな可能性をもたらす。DLE技術は、その選択性により、わずか数時間から数日でかん水からリチウムを抽出することができ、リチウムの供給と需要を密接に一致させるために、市場の柔軟性をはるかに高めることができる。DLEはまた、より持続可能な生産経路でもあり、80%以上のリチウム回収率を達成する一方で、従来の方法に必要な土地と水を回避することができる。電池のサプライチェーン全体で持続可能性がより重要になるにつれ、DLEへの投資がさらに促進されるでしょう。

DLE技術の選択性により、地熱や油田かん水など、リチウム濃度が低かったり汚染物質が多かったりする幅広いかん水の利用が可能になる。抽出に適したかん水が増え、特定の気候条件を必要としないDLEは、より多くの地域でリチウムの国内生産を可能にする。これは、特にリチウムの生産に意味のない地域で、電池のサプライチェーンを地域化し、確保するのに役立つ。DLEはすでにヨーロッパと北米で、それぞれ地熱と油田かん水を利用するために多額の投資を得ている。IDTechExの「直接リチウム抽出2026-2036:技術、プレーヤー、予測」レポートは、2036年までに米国が主要なDLE市場になると予測している。

DLEの主要技術は?

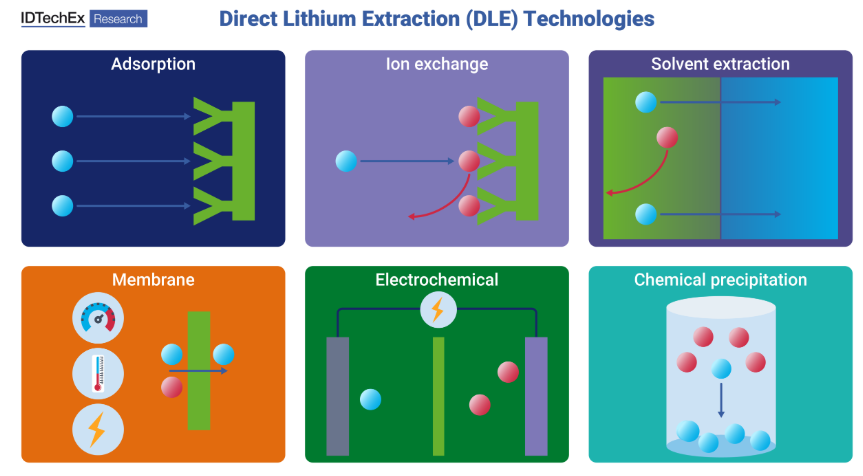

DLEは多様な技術状況を特徴としており、様々な開発段階にある6つの主要技術がある。それぞれに長所と短所があり、特定のブラインのタイプやプロセス条件に適している。2つとして同じブラインはないことから、複数の技術が市場内で地位を確立するだろう。

直接リチウム抽出技術の種類、出典:IDTechEx

吸着DLEは現在、最も成熟し、よく理解されている。これらのプロセスでは、アルミニウムベースの吸着剤を使用して塩水からリチウムを捕獲し、水を使用した脱着によって溶出液に放出する。吸着は、現在のDLE生産の大部分を占めており、リオ・ティントやエラメットなどの企業によって、アルゼンチンと中国で商業プロジェクトがすでに稼動している。

しかし、残りの技術も商業化に向けて急速に進展しており、そのほとんどはすでに実証規模に達しており、今後数年のうちに商業化を計画している。これらの技術の採用は、継続的な成熟に加え、吸着に比べて持続可能性が高く、リチウム選択性が高いことが原動力になるだろう。例えば、イオン交換DLEは吸着と同様の収着メカニズムを使用するが、脱着には酸を使用する。これにより、多くの地熱や油田のかん水がそうであるように、リチウムが100mg/L未満の非常に貧弱なかん水の利用が可能になる。溶媒抽出DLEは、他のプロセスよりも少ない水とエネルギー投入で、低品質のブラインを利用することもできる。

これらのDLE技術の本格的な商業化には、まだ課題が残っている。資源会社から広く賛同を得るためには、成熟した低リスクの技術でなければならない。また、これらの技術は、その性能が吸着剤、溶媒、膜などの特注材料の開発に依存する一方で、高いCAPEXに悩まされることもある。しかし、技術の進歩は加速しており、今後10年間に多くの新しいDLEプロジェクトが発表され、リチウム市場にシフトが起こりつつあることを浮き彫りにしている。

「Direct Lithium Extraction 2026-2036: Technologies, Players, Forecasts(リチウム直接抽出2026-2036:技術、プレーヤー、予測)」は、上記のトレンドとそれ以上のものをまとめている。IDTechExのレポートでは、主要な業績、技術経済、規制、その他の市場要因を考慮して分析している。主要プレーヤーとそのプロジェクトは各技術タイプにわたってベンチマークされている。

世界のリチウム市場について、供給源別の生産量(kt LCE)と市場価値(10億米ドル)の10年間のきめ細かな予測を提供している。供給源には、かん水DLE、かん水蒸発、硬岩採掘、堆積が含まれる。DLE市場については、技術別、ブラインの種類別、場所別の生産量(kt LCE)と市場価値(10億米ドル)の10年予測も示している。技術には、吸着、イオン交換、溶媒抽出、膜、電気化学が含まれる。ブラインのタイプには、大陸性、地熱、油田が含まれる。所在地には、アルゼンチン、ボリビア、チリ、米国、カナダ、英国、フランス、ドイツ、中国が含まれます。

材料供給業者、プロセス開発業者、採掘業者を含む17の企業プロフィールにアクセスすることで、市場への洞察が深まります。

主要な側面

本レポートは以下の重要な情報を提供します:

目次1.要旨

1.1.主な調査結果

1.2. リチウムの用途と需要の伸び

1.3. リチウムの供給源:

リチウム資源と生産の地域的集中

1.5. リチウム抽出規制は世界的に異なる

1.6. DLEの主な推進要因

1.7. DLEの主な課題

1.8. DLEとブライン蒸発の比較

1.9.リチウム塩水の種類とDLEへの影響

1.10. DLE技術

1.11. DLE技術のベンチマーク

1.12. DLE技術の主要開発企業

1.13. リチウム供給源別の主要DLE開発企業

1.14. 技術概要と市場:

1.15.

1.16.

1.17.

1.18.

1.19.

1.20.

1.21. 世界のリチウム市場規模(10億米ドル)2025-2036年(供給源別)

1.22. リチウム生産量対需要(kt LCE)2025-2036年の比較

1.23.DLEリチウム生産量(kt LCE) 2025-2036年技術別

1.24.DLEリチウム生産量(kt LCE) 2025-2036年 ブライン型式別

1.25. DLEリチウム生産量(kt LCE) 2025-2036年 地域別

1.26. Access More With an IDTechEx Subscription

2. リチウム生産と直接リチウム抽出への導入

2.1. リチウムの概要

2.1.1. リチウムとその用途

2.1.2.電池からのリチウム需要の増大

2.1.3. 炭酸リチウムと水酸化リチウムの比較

2.1.4. 重要な電池材料採掘事業への投資が減少

2.1.5. 電池用グレードのリチウム化学物質

2.2. 従来のリチウム抽出方法

2.2.1.

2.3. リチウムかん水鉱床の種類

2.2.4. 蒸発池を利用した大陸かん水リチウム回収

2.2.5. 商業かん水蒸発プロジェクト

2.2.6. 硬岩・堆積物系リチウム回収

2.2.7. スポジュメンのアップグレード

2.2.8. スポジュメン精製

2.2.9. スポジュメン輸送と世界供給網への依存

2.2.10. 商業スポジュメンプロジェクト(2025年)

2.2.11. 底質リチウム回収

2.2.12. 堆積層リチウムプロジェクトの開発

2.2.13. 代表的なリチウム・プロジェクトのスケジュール

2.2.14. 国別のリチウム資源量

2.2.15. 国別のリチウム生産量

2.2.16. 地域別のリチウム生産量

2.2.17.リチウム直接抽出の概要

2.3.1. リチウム直接抽出の動機

2.3.2. DLEの歴史と発展

2.3.3. ブライン蒸発 vs DLE

2.3.4. DLE vs. 従来法:持続可能性

2.3.5. DLE対従来法: リチウム塩水の種類がDLEに及ぼす影響

2.4. 世界のリチウム抽出規制

2.4.1.4.アルゼンチン

2.4.3. オーストラリア

2.4.4. ボリビア

2.4.5. ブラジル

2.4.6. カナダ

2.4.7. チリ

2.4.8. 中国

2.4.9. 欧州連合

2.4.10.メキシコ

2.4.11. 米国

2.4.12. ジンバブエ

3. 直接リチウム抽出のための技術

3.1. 技術の概要

3.1.1. DLE技術の種類

3.1.DLEプロセスの一般的なプロセスフロー図

3.1.3. DLE技術のベンチマーキング

3.2. 吸着

3.2.1. 吸着と吸着剤:吸着とイオン交換の比較

3.2.2. DLE用吸着剤

3.2.3. 吸着DLEの概要

3.2.4. 吸着-脱着プロセス

3.2.5. 吸着に基づくプロセスの設計

3.2.6. 吸着用Al系吸着剤の評価

3.2.7.イオン交換

3.3.1. イオンふるい

3.3.2. イオン交換プロセス

3.3.3. イオン交換用Mn系およびTi系吸着剤の評価

3.3.4. イオン交換SWOT

3.4. 溶媒抽出

3.4.1. 溶媒抽出プロセス

3.4.2. 炭酸による抽出

3.4.4. 溶媒抽出SWOT

3.5. 膜技術

3.5.1. リチウム回収のための膜プロセス

3.5.2. DLEにおける膜の応用

3.5.3. 圧力駆動膜プロセス

3.5.4. 熱駆動膜プロセス

3.5.5. 電気駆動膜プロセス

3.5.6. リチウム回収における膜プロセスの 役割

3.5.7. リチウム抽出のための膜材料

3.5.8. 膜のファウリング

3.5.9. 膜のSWOT

3.6. 電気化学技術

3.6.1. リチウム回収のための電気化学技術

3.6.2. リチウム精製のための電解

3.6.3. 静電容量脱イオン

3.6.4.電池ベースの技術

3.6.5. 膜増強電池ベースの技術

3.6.6. 電気駆動プロセスの比較

3.6.7. 電気化学SWOT

3.7. 化学沈殿法

3.7.1. リチウム回収のための化学沈殿法

3.7.2.化学析出技術の開発

3.7.3. 化学析出SWOT

4. 市場動向と主要プレーヤー

4.1. 市場概要

4.1.1. DLE技術開発者の状況

4.1.2. DLEのビジネスモデルとプレーヤー

4.1.3. 主な投資先と提携先:2021~2024年(1)

4.1.4. 主な投資先と提携先:2021~2024年(2)

4.1.5. 最近の主な投資先と提携先:2024~2025年

4.1.6. DLEのオフテイク契約

4.1.7. DLE用に探索されたリチウムソース

4.2. 吸着

4.2.1. 主な要点: 吸着技術開発企業

4.2.3. 吸着DLEプロジェクトの比較

4.2.4. リオ・ティント: Fenix(Hombre Muerto) project (2)

4.2.6. SunResin

4.2.7. 中国の吸着剤の輸出規制

4.2.8. Eramet

4.2.9. Eramet:Vulcan Energy Resources (1)

4.2.10.

4.2.11. Vulcan Energy Resources (2)

4.2.12. Aquatech

4.2.13. Standard Lithium & Aquatech

4.2.14. International Battery Metals (1)

4.2.15. International Battery Metals (2)

4.2.16. CleanTech Lithium

4.2.17. EnergyX

4.2.18. LightOre

4.2.19. Summit Nanotech

4.3. Ion exchange

4.3.1. Key takeaways: イオン交換技術開発企業

4.3.2.

4.3.3. イオン交換vs吸着vs蒸発の比較

4.3.4. ライラック・ソリューションズ: ライラック・ソリューションズ:カチ・プロジェクト(アルゼンチン)

4.3.5.

4.3.6. ライラック・ソリューションズ:Go2Lithium

4.3.7.

4.3.8.

4.3.9. Go2Lithium:イオン交換技術とプロセスフロー

4.3.10. Go2Lithium: LibertyStream (1)

4.3.11.

4.3.12. LibertyStream (2)

4.3.13. GeoLith

4.4. 溶媒抽出

4.4.1. Key takeaways: 溶媒抽出技術開発企業

4.4.2.

4.4.3. 溶媒抽出と他のDLEプロジェクトの比較

4.4.4. Adionics (1)

4.4.5. Adionics (2)

4.4.6. Ekosolve

4.4.7. Ekosolve:Tenova & Syensqo (1)

4.4.8.

4.4.9. Tenova & Syensqo (2)

4.4.10. Tenova: 市場動向

4.4.11. 新興プレーヤー:LiCAN Resources & Novalith

4.5. 膜技術

4.5.1. Key takeaways: 膜技術開発企業

4.5.2.

4.5.3. 回収ステップ別膜開発企業

4.5.4. HZランラン(1)

4.5.5. HZランラン(2)

4.5.6. Evove:テクノロジー

4.5.7. エヴォーブ: SLB

4.5.8.

4.5.9. Lithium Infinity

4.5.10. ElectraLith

4.5.11. KMXTechnologies

4.6. Electrochemical technologies

4.6.1. Key takeaways: 電気化学技術開発企業

4.6.2.

4.6.3. リチウムインフィニティー:電気化学プロセス

4.6.4. リチウムインフィニティ: Vito

4.6.5.

4.6.6.

4.7. 化学的沈殿技術

4.7.1. 化学的沈殿DLEの解説

5. FORECASTS

5.1. 予測の概要

5.1.1.予測手法と前提条件

5.2.1. 予測手法

5.2.2. 予測手法: 前提条件

5.3. リチウムとDLEの生産予測

5.3.1. 世界の供給源別リチウム生産量(kt LCE) 2025-2036

5.3.2. リチウム生産量対需要量(kt LCE) 2025-2036

5.3.技術別DLEリチウム生産量(kt LCE) 2025-2036

5.3.4. ブライン型別 DLEリチウム生産量(kt LCE) 2025-2036

5.3.5. 地域別 DLEリチウム生産量(kt LCE) 2025-2036

5.3.6. 市場規模の予測

5.4.1. 世界のリチウム市場規模:供給源別(10億米ドル) 2025-2036

5.4.2. DLEのリチウム市場規模:技術別(10億米ドル) 2025-2036

5.4.3. DLEリチウムの地域別市場規模(10億米ドル) 2025-2036

5.4.4.

5.4.5. DLEリチウムの国別市場規模(10億米ドル) 2025-2036

6. 会社プロファイル

6.1. 会社プロファイル

Summary10-year forecasts for direct lithium extraction, hard rock mining, brine evaporation, & sedimentary. Key players, projects & technologies - adsorption, ion exchange, solvent extraction, membranes, electrochemical. Covers US, Europe, China, South America. IDTechEx's report "Direct Lithium Extraction 2026-2036: Technologies, Players, Forecasts" provides a deep-dive into global lithium production and the fast-growing direct lithium extraction (DLE) landscape. This includes critical insights into technologies, key project data, and granular 10-year forecasts which detail how the emergence of DLE will grow the lithium market into one valued at US$52 billion dollars by 2036.

Sources of lithium production across the Americas, Europe, and China, Source: IDTechEx

What is driving the growth of DLE?

The rapid expansion of the li-ion battery market for electric vehicles and battery energy storage systems (BESS) has led to surging lithium demand. Conventional lithium extraction involves either the mining of hard rock minerals or evaporation of lithium-rich brines. However, such resources are concentrated in just a few regions (hard rock minerals in China and Australia; brines in China and the Lithium Triangle of Argentina, Bolivia, & Chile), and both methods have shortcomings that make them difficult to scale.

For one, brine evaporation processes can require 12-24 months to arrive at a final product, and they achieve low lithium recovery rates of 40-60%. They also require specific brine compositions and the right land and climate for evaporation ponds. Meanwhile, hard rock lithium is less prevalent in nature and mining comes with much greater environmental impacts.

The emergence of DLE technology, which allows for more selective lithium extraction from brines without evaporation, opens new opportunities for global production. DLE technologies can extract lithium from brines in just hours or days due to their selectivity, creating far more market flexibility to closely match lithium supply with demand. DLE also represents a more sustainable production pathway, bypassing the land and water requirements of conventional methods while achieving over 80% lithium recovery. As sustainability becomes more crucial across the battery supply chain, this will further drive investment into DLE.

The selectivity of DLE technology enables utilization of wide-ranging brines with lower lithium concentrations or more contaminants, including geothermal and oilfield brines. With more brines now suitable for extraction, and without any specific climate requirements, DLE will allow more regions to produce lithium domestically. This will help localize and secure battery supply chains, especially in areas that do not have meaningful lithium production. DLE has already gained significant investment in Europe and North America to make use of their geothermal and oilfield brines respectively. IDTechEx's "Direct Lithium Extraction 2026-2036: Technologies, Players, Forecasts" report expects the USA to become a leading DLE market by 2036.

What are the key DLE technologies?

DLE features a diverse technological landscape, with six major technology types at various stages of development. Each has its own strengths and weaknesses that make them suited to certain brine types or process conditions. Given that no two brines are identical, multiple technologies will establish a place within the market.

Direct lithium extraction technology types, Source: IDTechEx

Adsorption DLE is currently the most mature and well-understood of them all. These processes use aluminium-based sorbents to capture lithium from brines, which is then released into an eluate by desorption using water. Adsorption makes up the bulk of current DLE production, with commercial projects already running in Argentina and China, operated by players such as Rio Tinto and Eramet.

However, the remaining technologies are quickly progressing to commercialization, with most already at demonstration scale and with commercialization plans in the coming years. Their adoption will be driven by their continuing maturation as well as their greater sustainability and lithium selectivity compared to adsorption. For example, ion exchange DLE uses a similar sorption mechanism to adsorption but where acids are used for desorption. This allows for exploitation of very poor brines with under 100 mg/L lithium, which is the case for many geothermal or oilfield brines. Solvent extraction DLE can also make use of low-quality brines while requiring less water and energy input than other processes.

There remain challenges to the full-scale commercialization of these DLE technologies. They must be mature and low risk in order to gain buy-in from resource companies at large. These technologies can also suffer from high CAPEX, while their performance relies on the development of bespoke materials such as sorbents, solvents, and membranes. However, technological progress is accelerating and many new DLE projects have been announced for the coming decade, highlighting the shift that is coming to the lithium market.

"Direct Lithium Extraction 2026-2036: Technologies, Players, Forecasts" brings together all of the above trends and more. IDTechEx's report considers key performance, technoeconomic, regulatory, and other market factors in its analysis. Key players and their projects are benchmarked across each technology type.

10-year granular forecasts of the global lithium market are provided for production quantities (kt LCE) and market value (US$ billion) by source. Sources include brine DLE, brine evaporation, hard rock mining, and sedimentary. 10-year forecasts are also provided of the DLE market in terms of production quantities (kt LCE) and market value (US$ billion) by technology, brine type, and location. Technologies include adsorption, ion exchange, solvent extraction, membranes, and electrochemical. Brine types include continental, geothermal, and oilfield. Locations include Argentina, Bolivia, Chile, USA, Canada, UK, France, Germany, and China.

Access to 17 company profiles, including material suppliers, process developers, and mining companies, provide greater insight into the market.

Key Aspects

This report provides the following critical information:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Key report findings

1.2. Lithium applications and growing demand

1.3. Lithium sources: Brine, hard rock, & sediment

1.4. Regional concentration of lithium resources and production

1.5. Lithium extraction regulations vary globally

1.6. Key drivers for DLE

1.7. Key challenges for DLE

1.8. Comparing DLE & brine evaporation

1.9. Lithium brine types & impacts on DLE

1.10. DLE technologies

1.11. Benchmarking of DLE technologies

1.12. DLE technology key developers

1.13. Key DLE developers by lithium source

1.14. Technology overview & market: Adsorption

1.15. Technology overview & market: Ion exchange

1.16. Technology overview & market: Solvent extraction

1.17. Technology overview & market: Membranes

1.18. Technology overview & market: Electrochemical

1.19. Technology overview & market: Chemical precipitation

1.20. Global lithium production (kt LCE) 2025-2036 by source

1.21. Global lithium market size (US$ billion) 2025-2036 by source

1.22. Comparing lithium production vs demand (kt LCE) 2025-2036

1.23. DLE lithium production (kt LCE) 2025-2036 by technology

1.24. DLE lithium production (kt LCE) 2025-2036 by brine type

1.25. DLE lithium production (kt LCE) 2025-2036 by region

1.26. DLE lithium production (kt LCE) 2025-2036 by country

1.27. Access More With an IDTechEx Subscription

2. LITHIUM PRODUCTION & INTRODUCTION TO DIRECT LITHIUM EXTRACTION

2.1. Lithium overview

2.1.1. Lithium and its uses

2.1.2. Growing lithium demand from batteries

2.1.3. Lithium carbonate vs lithium hydroxide

2.1.4. Investment in critical battery material mining operations is reducing

2.1.5. Lithium price volatility in the 2020s

2.1.6. Effects of volatility in the lithium market

2.1.7. Battery grade lithium chemicals

2.2. Conventional lithium extraction methods

2.2.1. Geological sources of lithium

2.2.2. Extraction processes for different lithium deposits

2.2.3. Types of lithium brine deposits

2.2.4. Continental brine lithium recovery via evaporation ponds

2.2.5. Commercial brine evaporation projects

2.2.6. Hard rock & sediment-hosted lithium recovery

2.2.7. Spodumene upgrading

2.2.8. Spodumene refining

2.2.9. Spodumene transportation & dependence on global supply networks

2.2.10. Commercial spodumene projects (2025)

2.2.11. Sediment-hosted lithium recovery

2.2.12. Developing sedimentary lithium projects

2.2.13. Typical lithium project timeline

2.2.14. Lithium resources by country

2.2.15. Lithium production by country

2.2.16. Regional lithium production by source

2.2.17. Global lithium production breakdown: 2025 estimates

2.3. Direct lithium extraction overview

2.3.1. Motivations behind direct lithium extraction

2.3.2. History & development of DLE

2.3.3. Brine evaporation vs DLE

2.3.4. DLE vs. conventional methods: Sustainability

2.3.5. DLE vs conventional methods: Cost

2.3.6. Impact of lithium brine types on DLE

2.4. Global lithium extraction regulations

2.4.1. Summary of global lithium extraction regulations

2.4.2. Argentina

2.4.3. Australia

2.4.4. Bolivia

2.4.5. Brazil

2.4.6. Canada

2.4.7. Chile

2.4.8. China

2.4.9. European Union

2.4.10. Mexico

2.4.11. USA

2.4.12. Zimbabwe

3. TECHNOLOGIES FOR DIRECT LITHIUM EXTRACTION

3.1. Technology overview

3.1.1. DLE technology types

3.1.2. General process flow diagram for a DLE process

3.1.3. DLE technology benchmarking

3.2. Adsorption

3.2.1. Sorption & sorbents: Comparing adsorption vs. ion exchange

3.2.2. Sorbents for DLE

3.2.3. Overview of adsorption DLE

3.2.4. Adsorption-desorption process

3.2.5. Design of sorption-based processes

3.2.6. Assessment of Al-based sorbents for adsorption

3.2.7. Adsorption SWOT

3.3. Ion exchange

3.3.1. Ion sieves

3.3.2. Ion exchange process

3.3.3. Assessment of Mn- and Ti-based sorbents for ion exchange

3.3.4. Ion exchange SWOT

3.4. Solvent extraction

3.4.1. Solvent extraction process

3.4.2. Potential extraction systems

3.4.3. Extraction via carbonation

3.4.4. Solvent extraction SWOT

3.5. Membrane technologies

3.5.1. Membrane processes for lithium recovery

3.5.2. Application of membranes in DLE

3.5.3. Pressure-driven membrane processes

3.5.4. Thermally-driven membrane processes

3.5.5. Electrically-driven membrane processes

3.5.6. Roles of membranes processes in lithium recovery

3.5.7. Membrane materials for lithium extraction

3.5.8. Membrane fouling

3.5.9. Supported liquid membranes

3.5.10. Membranes SWOT

3.6. Electrochemical technologies

3.6.1. Electrochemical technologies for lithium recovery

3.6.2. Electrolysis for lithium refining

3.6.3. Capacitive deionization

3.6.4. Battery-based technologies

3.6.5. Membrane-enhanced battery-based technologies

3.6.6. Comparison of electrically-driven processes

3.6.7. Electrochemical SWOT

3.7. Chemical precipitation

3.7.1. Chemical precipitation for lithium recovery

3.7.2. Development of chemical precipitation technology

3.7.3. Chemical precipitation SWOT

4. MARKET DEVELOPMENTS AND KEY PLAYERS

4.1. Market overview

4.1.1. DLE technology developer landscape

4.1.2. DLE business models & players

4.1.3. Major investments & partnerships: 2021-2024 (1)

4.1.4. Major investments & partnerships: 2021-2024 (2)

4.1.5. Recent major investments & partnerships: 2024-2025

4.1.6. DLE offtake agreements

4.1.7. Lithium sources explored for DLE

4.2. Adsorption

4.2.1. Key takeaways: Adsorption DLE market

4.2.2. Adsorption technology developers

4.2.3. Comparing adsorption DLE projects

4.2.4. Rio Tinto: Fenix (Hombre Muerto) project (1)

4.2.5. Fenix (Hombre Muerto) project (2)

4.2.6. SunResin

4.2.7. Export controls on Chinese adsorbents

4.2.8. Eramet

4.2.9. Eramet: Centenario project

4.2.10. Vulcan Energy Resources (1)

4.2.11. Vulcan Energy Resources (2)

4.2.12. Aquatech

4.2.13. Standard Lithium & Aquatech

4.2.14. International Battery Metals (1)

4.2.15. International Battery Metals (2)

4.2.16. CleanTech Lithium

4.2.17. EnergyX

4.2.18. LightOre

4.2.19. Summit Nanotech

4.3. Ion exchange

4.3.1. Key takeaways: Ion exchange DLE market

4.3.2. Ion exchange technology developers

4.3.3. Comparing ion exchange vs adsorption vs evaporation

4.3.4. Lilac Solutions: Core technology

4.3.5. Lilac Solutions: Kachi project (Argentina)

4.3.6. Lilac Solutions: Gen 5 technology innovations in 2025

4.3.7. Lilac Solutions: Great Salt Lake project (USA)

4.3.8. Go2Lithium

4.3.9. Go2Lithium: Ion exchange technology and process flow

4.3.10. Go2Lithium: Example process flow diagram

4.3.11. LibertyStream (1)

4.3.12. LibertyStream (2)

4.3.13. GeoLith

4.4. Solvent extraction

4.4.1. Key takeaways: Solvent extraction DLE market

4.4.2. Solvent extraction technology developers

4.4.3. Comparing solvent extraction vs other DLE projects

4.4.4. Adionics (1)

4.4.5. Adionics (2)

4.4.6. Ekosolve

4.4.7. Ekosolve: Project developments

4.4.8. Tenova & Syensqo (1)

4.4.9. Tenova & Syensqo (2)

4.4.10. Tenova: market developments

4.4.11. Emerging players: LiCAN Resources & Novalith

4.5. Membrane technologies

4.5.1. Key takeaways: Membrane DLE market

4.5.2. Membrane technology developers

4.5.3. Membrane developers by recovery step

4.5.4. HZ Lanran (1)

4.5.5. HZ Lanran (2)

4.5.6. Evove: Technology

4.5.7. Evove: Project developments

4.5.8. SLB

4.5.9. Lithium Infinity

4.5.10. ElectraLith

4.5.11. KMX Technologies

4.6. Electrochemical technologies

4.6.1. Key takeaways: Electrochemical DLE market

4.6.2. Electrochemical technology developers

4.6.3. Lithium Infinity: Electrochemical process

4.6.4. Lithium Infinity: Market activity

4.6.5. Vito

4.7. Chemical precipitation technologies

4.7.1. Commentary on chemical precipitation DLE

5. FORECASTS

5.1. Forecasts summary

5.1.1. Summary: Direct lithium extraction 2025-2036 forecasts

5.2. Forecast methodology & assumptions

5.2.1. Forecast methodology

5.2.2. Forecast methodology: Factors impacting lithium production outlook

5.2.3. Forecast assumptions

5.3. Lithium and DLE production forecasts

5.3.1. Global lithium production by source (kt LCE) 2025-2036

5.3.2. Lithium production vs demand (kt LCE) 2025-2036

5.3.3. DLE lithium production by technology (kt LCE) 2025-2036

5.3.4. DLE lithium production by brine type (kt LCE) 2025-2036

5.3.5. DLE lithium production by region (kt LCE) 2025-2036

5.3.6. DLE lithium production by country (kt LCE) 2025-2036

5.4. Market size forecasts

5.4.1. Global lithium market size by source (US$ billion) 2025-2036

5.4.2. DLE lithium market size by technology (US$ billion) 2025-2036

5.4.3. DLE lithium market size by brine type (US$ billion) 2025-2036

5.4.4. DLE lithium market size by region (US$ billion) 2025-2036

5.4.5. DLE lithium market size by country (US$ billion) 2025-2036

6. COMPANY PROFILES

6.1. Company profiles

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の 先端材料 - Advanced Materials&Crisical Minerals分野 での最新刊レポート

関連レポート(キーワード「リチウム」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|