持続可能なバイオ燃料とE-Fuels(電子燃料)市場 2026-2036年:技術、プレーヤー、予測Sustainable Biofuels & E-Fuels Market 2026-2036: Technologies, Players, Forecasts 再生可能ディーゼル、持続可能航空燃料(SAF)、先進バイオ燃料をカバーする再生可能メタノール、e-fuel(電子燃料)製造技術に関する市場展望、10年間の市場予測、企業プロファイル、政策状況、経済性、技術... もっと見る

サマリー再生可能ディーゼル、持続可能航空燃料(SAF)、先進バイオ燃料をカバーする再生可能メタノール、e-fuel(電子燃料)製造技術に関する市場展望、10年間の市場予測、企業プロファイル、政策状況、経済性、技術評価

世界のCO2排出量のうち、輸送が占める割合は20%程度である。電気自動車は、道路を走る自動車にとって長期的に持続可能な解決策を提供するかもしれないが、既存の大量のICE(内燃機関)車には対処できない。また、電気自動車は、エネルギー密度の制約から、航空や海運に実行可能な解決策を提供することはできない。したがって、世界のネットゼロ目標を達成するためには、低炭素燃料が大量に必要となる。このような持続可能な燃料の多くは、ドロップインで代替可能であり、世界のインフラに最小限の変更しか必要としない。

この「持続可能なバイオ燃料とe-fuel(電子燃料)市場 2026-2036:技術、プレーヤー、予測」レポートで、IDTechExは先進バイオ燃料(第二世代以降)とe-fuel(電子燃料)の詳細な分析を提供しています。この分析は、生産プロセス、関連政策、主要技術革新、技術プロバイダー、プロジェクト開発者を網羅しています。また、この分野における技術経済的な課題と機会についても調査している。本レポートは、再生可能ディーゼル、持続可能航空燃料(SAF)、再生可能メタノールなどの主要燃料に焦点を当てている。

新たなSAF需要の出現

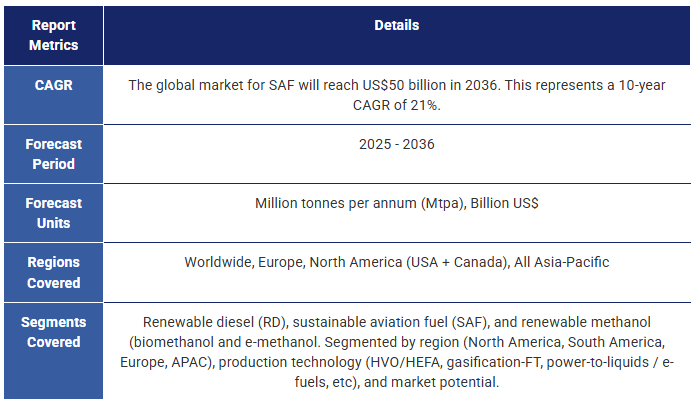

間違いなく、2025年は持続可能な燃料にとって画期的な年となった。英国でもEUでも、ReFuelEU Aviationのような規制がSAF(持続可能な航空燃料)の拘束力のある混合目標を意味し、SAFの前例のない大規模な強制需要を生み出した。世界的な新規プロジェクトの発表は、再生可能ディーゼルよりもむしろSAFに集中している。これは、SAF市場が航空機の脱炭素化の主要な手段として長期的にはより有利になるという業界の考えを反映している。その後、このIDTechExレポートにはSAF市場の潜在性に関する予測が含まれており、世界のSAF市場は2036年に500億米ドルに達すると予測されている。

しかし、SAFを取り巻く規制の不確実性はまだ大きい。例えば、米国では、SAFのための計画されたプロジェクト・パイプラインは非常に大規模であるが、現在利用可能なSAFに対する政府の支援は、航空会社からの自発的な需要以外では、ほとんどの施設において再生可能ディーゼル生産よりもSAFに経済的なインセンティブを与えることはないだろう。短期的には、予想される規制需要よりも早く施設がオープンするため、SAFの大幅な生産能力過剰につながる可能性がある。

IDTechExの本レポートは、再生可能ディーゼルとSAF市場の包括的な分析を提供し、市場を牽引する政策情勢、生産プロセス、注目すべき技術革新、主要プレーヤー、プロジェクト事例、経済性に焦点を当てている。また、再生可能ディーゼルおよびSAFの様々な生産技術や生産ルートに注目し、新たな道筋を探るとともに、各分野における独自の課題や機会についての洞察も提供しています。

HEFA転換点を超える再生可能ディーゼルとSAF

HEFA/HVO経路は、初期のSAF成長に大きく寄与している。HEFA/HVO経路は、SAFの初期成長に大きく寄与している。これは、SAFの最も低コストな生産経路であり、販売価格は従来のジェット燃料とさほど変わらない。しかし、HEFA原料(使用済み食用油、油脂、グリース)には限りがあり、2030年以降のある時点で、世界のSAF市場は「HEFA転換点」に直面しなければならなくなる。

このため、アルコール・ツー・ジェット、ガス化/フィッシャー・トロプシュ、e-SAFといった新たなSAF経路に軸足を移さざるを得なくなる。これらの技術は規模を拡大しつつある。例えば、最初の商業用ATJ施設(2025年に稼働したランザジェットのフリーダム・パインズ・フューエルズ)は、年間900万ガロンのSAFと100万ガロンの再生可能ディーゼルを生産している。しかし、コスト高が依然として大きな障壁となっており、技術開発と規制がこれに対処する必要がある。

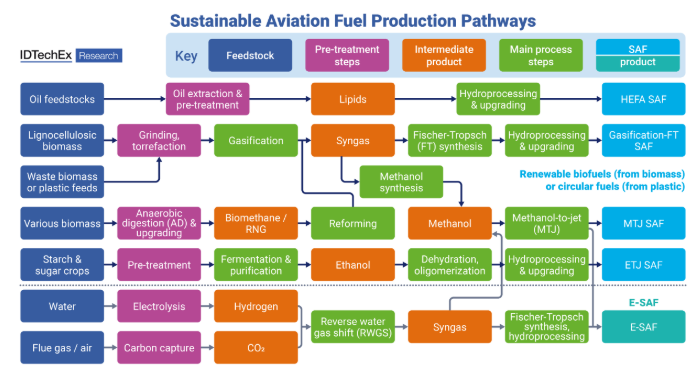

本レポートでは、セルロース系エタノール生産、熱分解、ガス化、フィッシャー・トロプシュ(FT)合成、水熱液化(HTL)、アルコール-ジェット/ガソリンといった第二世代バイオ燃料技術について、主要な技術革新、プロジェクト事例、技術サプライヤーとともに包括的に分析している。また、生産経路、主要プレーヤー、合成ガス生成の進歩に焦点を当て、急速に進化するこのセクターに関する貴重な洞察を提供することで、e-fuelの状況も幅広くカバーしている。

本レポートで分析したSAF製造プロセス出典IDTechEx

低炭素メタノール

再生可能なメタノール生産も急速に増加しており、すでに年産10万トン規模の施設がいくつか建設中である。中国は、既存のメタノール市場で圧倒的な地位を占めており、CAPEXが低く、豊富なバイオマス資源と、バイオマスガス化技術やeメタノール技術のためのグリーン水素資源を有していることから、近い将来、主要地域となることが予想される。低炭素メタノールの需要は、クリーンな海洋燃料、化学セクターの脱炭素化、SAF(メタノール-ジェット経路経由)の原料としての需要に牽引されている。IDTechExの本レポートは、再生可能メタノール市場の詳細な分析を提供し、技術サプライヤー、主要プロジェクト開発者、発表されたプロジェクト容量を網羅し、再生可能メタノールの将来についての詳細な展望を提供します。

市場予測と展望

IDTechExの予測によると、世界の再生可能ディーゼル及びSAF生産能力は2036年までに年間6,700万トンを超え、2026年から2036年までのCAGRは8.1%で成長すると予測されており、持続可能燃料市場は今後数年間で大きく成長する態勢にある。この目覚しい成長軌道は、世界のエネルギーミックスにおける持続可能な燃料の重要性が高まっていることを強調している。

この成長の主な原動力は、EUと英国におけるSAF燃料の義務付けや米国の45Z税額控除などの政策展開や、自動車運行会社や航空会社による二酸化炭素排出量削減の推進である。また、持続可能な燃料生産プロジェクトにおいて、幅広い生産技術が登場し、商業的に利用されるようになったことも大きな推進力となっている。しかし、このセクターは、全体的なエネルギー効率(特に道路輸送用のEVとe燃料を比較した場合)、原料の入手可能性、プロジェクト開発の問題(長い開発期間と多額の資金が必要)、従来の化石燃料とのコスト・パリティの達成に関連する大きな課題にも直面している。これらの推進要因と課題が一体となって、急速に発展するこの市場を形成している。

本レポートでは、再生可能メタノール、再生可能ディーゼル、SAFなど、様々な持続可能燃料の詳細な市場予測を提供している。再生可能ディーゼル、再生可能SAF、再生可能メタノールについて、生産地域(欧州、北米、南米、APAC)および技術経路(HEFA/HVO、ガス化-FT、power-to-liquids/e-fuelsなど)ごとに細分化した詳細な市場予測を提供する。詳細な技術分析から市場予測、プロジェクトケーススタディまで、本レポートはサステイナブル燃料市場を理解し、ナビゲートするために必要な洞察を提供します。

主要な側面

持続可能燃料市場の紹介

従来型(第一世代)バイオ燃料市場の概要

第二世代のバイオ燃料生産技術。IDTechEx は、以下の各項目について、生産技術、主要イノベーション、プロジェクト・ケーススタディ、技術供給者、 課題、機会を分析した

第3・第4世代バイオ燃料技術

e-fuel(電子燃料)生産の展望。IDTechEx は以下の各項目について、生産技術、主要イノベーション、プロジェクト事例、技術サプライヤー、課題、機会を分析した

先進バイオ燃料とe燃料市場

市場予測

目次

1.エグゼクティブサマリー

1.1.なぜ輸送の脱炭素化が必要なのか?

1.2.運輸部門における持続可能な燃料の役割

1.3.バイオ燃料の世代(1/2)

1.4.従来型(第1世代)バイオ燃料の概要

1.5.従来型バイオ燃料の歴史的優位性 - バイオエタノールとバイオディーゼル

1.6.なぜ従来型バイオ燃料から脱却するのか?

1.7.第一世代バイオ燃料からの転換

1.8.HVO/HEFAプロセス - 再生可能ディーゼル&SAFの主流ルート

1.9.第2世代バイオ燃料製造経路

1.10.セルロース系エタノール:概要

1.11.技術別バイオメタノール生産:2026-2036年

1.12.再生可能ディーゼルの生産経路

1.13.SAFの生産経路

1.14.石油精製におけるバイオマス原料の共処理

1.15.再生可能ディーゼル、SAF、ガソリンの原料の概要

1.16.アルコールからジェットへ(ATJ)のプロセスステップ

1.17.e-fuel(電子燃料)の概要

1.18.2025年時点のe燃料の規模

1.19.藻類バイオ燃料:第3/4世代バイオ燃料の道のりはまだ長い

1.20.持続可能な燃料技術開発者のビジネスモデル

1.21.e-fuel(電子燃料)の最終製品別技術・プロセス開発企業

1.22.e-fuel(電子燃料)の最終製品別プロジェクト開発者

1.23.先進バイオ燃料とe-fuel(電子燃料)の生産技術プロバイダー

1.24.先進バイオ燃料とe-fuel(電子燃料)の生産技術プロバイダー

1.25.プロジェクト開発者と燃料製造者のためのビジネスモデルと考慮事項

1.26.生産技術別のRD&SAFプロジェクト開発者

1.27.SAFの価格 - 普及を阻む重要な問題

1.28.SAFに関する主な要点と展望

1.29.米国における再生可能ディーゼル燃料生産の経済性

1.30.再生可能ディーゼルの要点と見通し

1.31.地域別SAF生産能力:2026-2036年

1.32.地域別SAF生産量考察

1.33.技術別SAF生産能力:2026-2036年

1.34.SAF市場:2026-2036年(10億米ドル)

1.35.技術別の再生可能ディーゼル生産:2026-2036年

1.36.技術別再生可能ディーゼル生産量考察

1.37.e-fuel(電子燃料)の複合予測:2026-2036年

2.バイオ燃料と政策の展望

2.1.気温上昇をもたらす世界の排出量

2.2.幅広い脱炭素化ソリューションが必要

2.3.世界の輸送排出量と持続可能な燃料の役割

2.4.運輸部門における持続可能な燃料の役割

2.5.輸送の脱炭素化におけるバイオ燃料の役割

2.6.バイオ燃料サプライチェーンの概要と温室効果ガス排出量

2.7.バイオ燃料の世代(1/2)

2.8.バイオ燃料の世代(2/2)

2.9.バイオ燃料生産/導入の推進要因と障壁

3.従来のバイオ燃料:バイオエタノールとバイオディーゼル

3.1.バイオエタノールとバイオディーゼルの生産

3.1.1.従来型バイオ燃料の歴史的優位性 - バイオエタノールとバイオディーゼル

3.1.2.バイオエタノールの重要性とその応用

3.1.3.第1世代バイオエタノール生産の概要

3.1.4.第一世代バイオエタノール製造プロセスの概要

3.1.5.代表的なバイオエタノール製造プロセス - 穀物を使った乾式製粉プロセス

3.1.6.代表的なバイオエタノール製造プロセス - サトウキビエタノールプロセス

3.1.7.従来のバイオディーゼル(FAME)と石油ディーゼルの比較

3.1.8.従来のバイオディーゼルとその用途

3.1.9.世界のバイオディーゼル、再生可能ディーゼルの生産と消費

3.1.10.代表的なバイオディーゼル生産プロセス

3.1.11.バイオディーゼル生産におけるその他の考慮事項

3.2.バイオ燃料をめぐる持続可能性への懸念

3.2.1.バイオ燃料の複雑な持続可能性

3.2.2.バイオ燃料サプライチェーンと温室効果ガス排出の概要

3.2.3.バイオ燃料による炭素排出の概要 - トウモロコシエタノールの例

3.2.4.土地利用の変化:直接(LUC)& 間接(ILUC)

3.2.5.バイオ燃料の持続可能性と土地利用変化

3.2.6.バイオ燃料の LCA 比較

3.2.7.バイオ燃料のライフサイクル排出量と土地利用変化(LUC)

3.2.8.バイオ燃料の世代別土地利用排出量

3.2.9.土地利用変化による排出の地域差

3.2.10.MJ 当たりの燃料炭素原単位の比較

3.2.11.km当たりの燃料炭素原単位の比較

3.2.12.電気自動車からの炭素排出量

3.2.13.各種自動車のライフサイクル排出量の比較

3.2.14.第一世代バイオ燃料からの転換

4.第二世代バイオ燃料技術

4.1.先進バイオ燃料の紹介

4.1.1.石油製品の種類と持続可能な代替燃料

4.1.2.先進バイオ燃料の略語と定義

4.1.3.バイオディーゼルと再生可能ディーゼル:特性とエンジン適合性

4.1.4.化石ディーゼル、バイオディーゼル、再生可能ディーゼルの比較

4.1.5.ジェット燃料の組成と種類

4.1.6.ジェットA-1のドロップイン代替燃料としてのSAF

4.1.7.第2世代バイオ燃料製造経路

4.1.8.バイオ燃料技術の概要

4.1.9.バイオ燃料技術の概要

4.1.10.バイオ燃料技術の概要

4.1.11.バイオ燃料製造経路の製造コストの SAF との比較

4.2.セルロース系エタノール生産

4.2.1.リグノセルロース系バイオマス原料

4.2.2.セルロース系エタノール生産の概要

4.2.3.リグノセルロース系バイオマスの分解における課題

4.2.4.バイオ燃料生産における酵素の利用

4.2.5.セルロース系エタノール企業の状況

4.2.6.セルロース系エタノール企業のケーススタディ

4.2.7.セルロース系エタノール企業のケーススタディ

4.2.8.セルロース系エタノールは大きな課題に直面している

4.2.9.セルロース系エタノール生産者が直面する共通の課題

4.2.10.セルロース系エタノール生産は死んだのか?

4.2.11.活発で進行中のセルロース系エタノールプロジェクト

4.2.12.セルロース系エタノール生産者にとってSAF生産は新たな機会である

4.2.13.SAFをターゲットとする主なセルロース系エタノール企業

4.3.熱分解技術

4.3.1.バイオマス&プラスチック廃棄物熱分解の紹介

4.3.2.熱分解製品と市場応用

4.3.3.熱分解プロセスの設計に影響を与える主な技術的要因

4.3.4.熱分解リアクターの設計

4.3.5.バイオマス・プラスチック熱分解における分解方法の概要

4.3.6.熱分解プラント設計における考慮事項:加熱方法

4.3.7.熱分解リアクターのサイズ制限

4.3.8.バイオオイル及びプラスチック熱分解オイルの組成

4.3.9.油の品質に影響する因子と燃料への下流処理

4.3.10.熱分解技術の比較

4.3.11.油中の水素不足と追加水素の必要性

4.3.12.持続可能な燃料生産に携わる熱分解企業

4.3.13.熱分解バイオクリュード企業のケーススタディ - Alder Renewables

4.4.ガス化技術

4.4.1.バイオマス・廃棄物ガス化の概要

4.4.2.廃棄物の熱分解とガス化プロセスの比較

4.4.3.ガス化&フィッシャー・トロプシュバイオマス・ツー・リキッド(BtL)経路

4.4.4.バイオマスとプラスチックのガス化のための前処理方法

4.4.5.ガス化炉のタイプ

4.4.6.バイオマスガス化炉の性能比較

4.4.7.異なるガス化炉タイプの長所と短所

4.4.8.ガス化技術開発者

4.4.9.バイオマスガス化のためのガス化炉のタイプ

4.4.10.バイオマスガス化の新しい技術(1/2)

4.4.11.バイオマスガス化技術の革新(2/2)

4.4.12.コンコード・ブルー - 新規ガス化・改質コンセプト

4.4.13.ガス化技術サプライヤー

4.4.14.ガス化触媒

4.4.15.バイオマスのガス化+FTプロジェクト - 運転中および計画中

4.4.16.ガス化-FT バイオ SAF プロジェクトのケーススタディ - Altalto Immingham

4.4.17.フルクラム・バイオエナジー-失敗したSAF生産者

4.4.18.バイオマスガス化による水素製造

4.4.19.バイオマスガス化によるメタノール製造

4.5.水熱液化(HTL)技術

4.5.1.水熱液化(HTL)の概要

4.5.2.水熱液化における水の役割

4.5.3.水熱液化原料-バイオマス

4.5.4.水熱液化原料-プラスチック

4.5.5.プラスチック廃棄物の水熱液化-リセラのケーススタディ

4.5.6.水熱液化原料 - バイオマス対プラスチック

4.5.7.主要な高温ガス炉設計の概要

4.5.8.水熱液化技術開発者-プロセス規模と原料

4.6.フィッシャー・トロプシュ(FT)合成

4.6.1.フィッシャー・トロプシュ合成:合成ガスから炭化水素

4.6.2.フィッシャー・トロプシュ(FT)合成の概要

4.6.3.既存のFT触媒の概要

4.6.4.FT反応器設計の概要

4.6.5.FT反応器の概要

4.6.6.FT リアクターの設計比較

4.6.7.FT リアクターの革新 - マイクロチャンネル反応器

4.6.8.FT反応器の革新-マイクロ構造反応器

4.6.9.e-fuel(電子燃料)用フィッシャー・トロプシュ触媒

4.6.10.反応器タイプ別フィッシャー・トロプシュ(FT)技術サプライヤー

4.7.バイオ原油の精製・アップグレード技術

4.7.1.バイオリファイナリーで使用される精製・アップグレーディングプロセス

4.7.2.水素化分解プロセス

4.7.3.水素化分解プロセス

4.7.4.異性化工程

4.7.5.脱ロウ工程

4.7.6.分別蒸留工程概要

4.7.7.分別蒸留工程:詳細な考察

4.7.8.アップグレードプロセスによる水素消費量

4.7.9.アップグレーディングプロセスにおける高い水素消費量の意味

4.7.10.アップグレーディングプロセスにおける主な課題とプロセスの考慮事項

4.7.11.水素化分解、水素化分解、異性化技術サプライヤー

4.7.12.水素化分解、水素化分解、異性化技術のサプライヤー

4.8.バイオメタノール生産

4.8.1.メタノール生産の概要と色

4.8.2.従来のメタノール生産

4.8.3.バイオメタノール生産の主な経路

4.8.4.バイオガス改質からのバイオメタノール

4.8.5.メタンの水蒸気改質

4.8.6.バイオガスと新しい改質技術を使ったバイオメタノールプロジェクト

4.8.7.バイオマスガス化からのバイオメタノール

4.8.8.水熱ガス化からのバイオメタノール

4.8.9.メタノール合成技術の主要企業

4.9.アルコール-ジェット(ATJ)&アルコール-ガソリン(ATG):メタノール & エタノール

4.9.1.エタノール原料

4.9.2.CO2からエタノールへのルートLanzaTech

4.9.3.メタノール原料

4.9.4.メタノール-ガソリン(MTG)プロセスの概要

4.9.5.従来の固定床MTGプロセス

4.9.6.新しい流動床 MTG プロセス

4.9.7.アルコール-ジェット(ATJ)プロセスのステップ

4.9.8.エタノール&メタノール製造

4.9.9.アルコール脱水&オリゴマー化

4.9.10.水素化、異性化、分別蒸留からジェット

4.9.11.MTGとMTJプロセスの比較

4.9.12.アルコール・トゥ・ジェット(ATJ)と競合するSAFルートとの長所と短所

4.9.13.ランザジェット:世界初の商業規模のエタノール・ツー・ジェット・プラント

4.9.14.メタノール-ガソリン(MTG)技術プロバイダー

4.9.15.アルコールジェット(ATJ)技術プロバイダー

4.9.16.アルコールジェット(ATJ)技術プロバイダー

4.9.17.アルコールジェット(ATJ)技術プロバイダー

5.第三・第四世代バイオ燃料技術

5.1.第三・第四世代バイオ燃料の紹介

5.2.巨大藻類、微細藻類、シアノバクテリア

5.3.藻類は複数の市場に応用できる

5.4.第3世代バイオ燃料生産:原料

5.5.大型藻類を用いたバイオ燃料生産プロセス

5.6.微細藻類/シアノバクテリアを用いたバイオ燃料生産プロセス

5.7.藻類バイオ燃料生産-プロセス例

5.8.微細藻類培養における代謝経路

5.9.微細藻類培養における主要成長基準

5.10.微細藻類培養のための開放容器

5.11.微細藻類培養用の密閉容器

5.12.微細藻類培養システムの開放型と閉鎖型

5.13.微細藻類培養システムサプライヤー光バイオリアクター(PBR)&池

5.14.ケーススタディ:持続可能な航空燃料(SAF)生産に藻類を使用

5.15.藻類バイオ燃料開発は歴史的な課題に直面してきた

5.16.藻類バイオ燃料企業は、焦点を移すか倒産した

5.17.藻類・微生物バイオ燃料プロセス&プロジェクトの主要プレーヤー

5.18.藻類・微生物バイオ燃料プロセスの主要プレーヤーとプロジェクト

5.19.藻類・微生物バイオ燃料プロセスの主要企業&プロジェクト

5.20.微細藻類の利用を計画しているSAFプロジェクト

5.21.微細藻類の利用を計画しているSAFプロジェクト

5.22.第3・4世代バイオ燃料生産のSWOT分析

5.23.第3世代および第4世代バイオ燃料の展望

6.e-fuel(電子燃料)生産

6.1.e燃料の概要

6.1.1.e燃料とは何か?

6.1.2.なぜe燃料が必要なのか?

6.1.3.e燃料と化石燃料およびバイオ燃料との比較

6.1.4.合成燃料の主要原料としてのCO2

6.1.5.e-fuel(電子燃料)生産におけるエネルギーと炭素の流れの概要

6.1.6.e-fuel(電子燃料)の生産効率

6.1.7.e-fuel(電子燃料)を取り巻くエネルギー効率の課題

6.1.8.e-fuel(電子燃料)は特定の状況で使用されなければならない

6.1.9.e-燃料のSWOT分析

6.1.10. e-燃料に特有の義務化

6.1.11.e-燃料の課題と機会

6.1.12.e-fuel(電子燃料)製造におけるグリーン水素の役割

6.1.13.電解槽セル、スタック、バランス・オブ・プラント(BOP)

6.1.14.電解槽技術の概要

6.1.15.電解槽の性能特性の比較

6.1.16.世界の主要電解槽OEMの概要

6.1.17.4つの主要電解槽技術の長所と短所

6.1.18.回収されたCO2の供給源が重要

6.1.19.EUの再生可能エネルギー指令におけるe-fuel(電子燃料)製造のためのCO2源

6.1.20.ほとんどのe-fuel(電子燃料)プロジェクトは、生物起源CO2を供給源としている

6.1.21.どの炭素回収技術が最も成熟しているか?

6.1.22.ポイントソースの炭素回収技術プロバイダー

6.1.23. e-fuel(電子燃料)の製造コストは地域によって異なる

6.1.24.2025年時点でのe燃料の規模

6.2.e-燃料用の合成ガス製造

6.2.1.CO2を合成ガスに変換する逆水ガスシフト

6.2.2.逆水ガスシフト用触媒

6.2.3.RWGS 触媒イノベーション・ケーススタディ

6.2.4.逆水ガスシフト用リアクター

6.2.5.RWGSリアクターの革新ケーススタディ

6.2.6.CO2-合成ガスプロセス:代替技術

6.2.7.代替CO2削減技術の検討

6.2.8.RWGS & SOEC 共電分解ルートの比較

6.2.9.固体酸化物電解槽(SOEC)の概要

6.3.メタンの分類 & 発電からガスへの変換(P2G)

6.3.2.メタン化の概要

6.3.3.熱触媒と生体触媒のメタン化

6.3.4.稼働中のe-メタンプロジェクト

6.3.5.熱触媒メタン化技術プロバイダー

6.3.6.熱触媒メタン化リアクターの比較

6.3.7.プロセスフロー図:熱触媒メタン化技術

6.3.8.生物学的メタン化技術プロバイダー

6.3.9.ex-situとin-situの生物学的メタン化

6.3.10.生物電気化学的メタン化

6.3.11. 欧州におけるe-メタン生産

6.3.12.生物学的e-メタン技術における最近の進歩

6.3.13.e-メタン生産の経済性

6.3.14.メタン化技術のSWOT

6.3.15.世界の発電メタン化プロジェクト - 現在進行中と発表済み

6.3.16. 2025年のe-メタン生産

6.4. e-メタノール生産

6.4.1.メタノール生産の概要と色彩

6.4.2.トップソーのCO2-メタノール変換触媒

6.4.4.クラリアントのCO2-メタノール触媒

6.4.5.CO2-メタノール化用チューブ冷却リアクター

6.4.6.東洋エンジニアリングの小規模メタノール反応器

6.4.7.メタノール合成の主要プレーヤー

6.4.8.メタノール合成の主要企業

6.4.9.新規メタノール合成コンセプトを持つ新興企業

6.4.10.新規メタノール合成コンセプトを持つ新興企業

6.4.11.2025年のeメタノール生産

6.5. e-ケロシン、e-SAF、e-ガソリン、e-ディーゼル、e-ワックス

6.5.1.液体炭化水素e燃料への経路の概要

6.5.2.e-SAFにおけるフィッシャー・トロプシュとメタノール・ツー・ジェットの比較

6.5.3.フィッシャー・トロプシュとメタノール・ツー・ジェットの経済性

6.5.4.e-fuel(電子燃料)用フィッシャー・トロプシュ触媒

6.5.5.大規模な工業規模のe-fuel(電子燃料)プラントのコンセプト

6.5.6.MTGe-fuel(電子燃料)プラントのケーススタディ

6.5.7.モジュール式e-fuel(電子燃料)プラントのコンセプト

6.5.8.RWGS-FT燃料プラントのケーススタディ

6.5.9.既存の液化ガス(GTL)設備のe-fuel(電子燃料)への転換

6.5.10.e-SAF用フィッシャー・トロプシュからの製品スレート

6.5.11.大規模e-fuel(電子燃料)プロジェクト:稼働中と建設中

6.5.12.大規模e-fuel(電子燃料)プラントの主要サプライヤー

6.5.13.e-fuel(電子燃料)の最終製品別技術・プロセス開発企業

6.5.14.2025年のe-ケロシン、e-ガソリン、e-ディーゼル、e-ワックスの生産

7.先進バイオ燃料・e-燃料市場

7.1.再生可能メタノール市場

7.1.1.メタノール市場の現状

7.1.2.地域別メタノール市場の現状

7.1.3.将来のメタノール用途

7.1.4.低炭素メタノールの主な成長ドライバー

7.1.5.メタノールは主要な低炭素輸送用燃料

7.1.6.メタノール生産の概要と色

7.1.7.グリーンメタノールの製造コスト

7.1.8.EUにおける再生可能メタノールの最高販売価格

7.1.9.バイオメタノール生産の主な経路

7.1.10.バイオメタノールプロジェクト開発者 - 企業一覧

7.1.11.バイオガスを利用したバイオメタノールプラント

7.1.12.ガス化を利用したバイオメタノールプラント

7.1.13. 現在開発中のe-メタノールプロジェクト(事業化後)

7.1.14. 現在開発中のe-メタノールプロジェクト(事業化後)

7.1.15.低炭素メタノールの地域別市場:欧州と中国

7.2.再生可能ディーゼル&SAF-一般的市場シナリオ

7.2.1.再生可能ディーゼル、SAF、ガソリンの原料の概要

7.2.2.再生可能ディーゼル・SAF 製造における典型的な製品分割

7.2.3.石油精製におけるバイオマス原料の共処理

7.2.4.将来の総合バイオリファイナリー

7.2.5.持続可能な燃料技術開発業者のビジネスモデル

7.2.6.先進バイオ燃料とe-fuel(電子燃料)の生産技術プロバイダー

7.2.7.先進バイオ燃料及びe-fuel(電子燃料)の生産技術プロバイダー

7.2.8.持続可能な燃料プロジェクトに影響を与える主な技術経済的要因

7.2.9.プロジェクト開発者と燃料生産者のためのビジネスモデルと考慮事項

7.2.10.生産技術別の研究開発及び SAF プロジェクト開発者

7.2.11.バイオ燃料プロジェクトにおける主要課題

7.2.12.e-fuel(電子燃料)(液化発電)プロジェクトにおける主な課題

7.2.13.再生可能ディーゼル&SAFのライフサイクル排出量

7.2.14.HEFA再生可能ディーゼル&SAFの生産コストに影響を与える要因

7.2.15.再生可能ディーゼルの生産コスト

7.3.再生可能ディーゼル市場

7.3.1.再生可能ディーゼルとその最終用途市場

7.3.2.バイオディーゼルと再生可能ディーゼル原料と生産プロセス

7.3.3.世界の再生可能ディーゼル生産量

7.3.4.米国における再生可能ディーゼルの現状

7.3.5.米国における再生可能ディーゼル生産の推進要因

7.3.6.米国における再生可能ディーゼル生産の経済性

7.3.7.再生可能ディーゼル2025の市場データ

7.3.8.再生可能ディーゼルかSAFか?

7.3.9.再生可能ディーゼルの生産経路

7.3.10.再生可能ディーゼルの要点と展望

7.4.持続可能な航空燃料(SAF)市場

7.4.1.航空機の脱炭素化におけるSAFの重要性

7.4.2.SAFの政府目標と義務化

7.4.3.SAFの政府目標と義務化-EUと英国を中心に

7.4.4.SAF生産者に対する政府のインセンティブ

7.4.5.CORSIA:世界の航空業界の脱炭素化

7.4.6.旅客航空会社および貨物航空会社によるSAFへの取り組みの概要

7.4.7.主な旅客航空会社のSAFへの取り組みと活動

7.4.8.SAFのビジネスモデル

7.4.9.SAFの主要市場ドライバーの概要

7.4.10.SAFの主な生産経路

7.4.11.バイオSAFとe-SAF - SAFへの2つの主要経路

7.4.12.ASTM認可の製造経路

7.4.13.HEFA-SPK生産者のケーススタディ - Neste

7.4.14.ガス化-FTバイオSAFプロジェクトのケーススタディ - Altalto Immingham

7.4.15.ATJプロジェクト・ケーススタディ - フリーダムパインズ

7.4.16. e-SAFプロジェクト・ケーススタディ - ERA ONE

7.4.17.フルクラム・バイオエナジー-失敗したSAF生産者

7.4.18.その他の中止されたSAFプロジェクトと失敗の理由

7.4.19.SAFの価格 - 導入を阻む重要な問題

7.4.20.誰がSAFのグリーンプレミアムを支払うのか?

7.4.21.SAFコスト削減の主な推進要因と課題

7.4.22.SAFの生産能力と市場見通し

7.4.23.SAFに関する主な要点と展望

8.市場予測

8.1.持続可能燃料市場の予測方法と前提条件

8.2.持続可能燃料の組み合わせ予測:2026-2036年

8.3.e燃料の組み合わせ予測:2026-2036年

8.4.地域別バイオメタノール生産能力:2026-2036年

8.5.地域別バイオメタノール生産量考察

8.6.技術別バイオメタノール生産能力:2026-2036年

8.7. 地域別eメタノール生産能力:2026-2036年

8.8. 地域別eメタノール生産能力:2026-2036年

8.9.議論

8.9.技術別の再生可能ディーゼル生産:2026-2036年

8.10.技術別再生可能ディーゼル生産量考察

8.11.地域別SAF生産能力:2026-2036年

8.12.地域別SAF生産量考察

8.13.技術別のSAF生産能力:2026-2036年

8.14.SAF市場:2026年-2036年(10億米ドル)

9.企業プロフィール

9.1.アビオックス

9.2.Brineworks

9.3.カーボンニュートラル燃料

9.4.カーボン・リサイクル・インターナショナル

9.5.カーボンブリッジ

9.6.サークリア・ノルディック

9.7.コンコード・ブルー・エンジニアリング

9.8.シアノキャプチャー

9.9.ディメンショナル・エナジー

9.10.エクソンモービルメタノール-ガソリン(MTG)

9.12.GIG カラセックECO2CELL

9.13.HIFグローバル(Highly Innovative Fuels)

9.14.日立造船株式会社PEMEL & メタン化技術

9.15.HYCO1

9.16.株式会社IHIメタン化システム

9.17.INERATEC

9.18.インフィニウム

9.19.KEWテクノロジー

9.20.ランザジェット

9.21.ランザテック

9.22.OXCCU

9.23.キューパワー

9.24.積水化学工業CO₂ 利用のための化学ループ

9.25.Shell Catalysts & Technologies:SGPガス化炉

9.26.シンヘリオン

9.27.Syzygy Plasmonics

9.28.TES (Tree Energy Solutions): e-NG

9.29.ベロシス

SummaryMarket outlook, ten-year market forecasts, company profiles, policy landscape, economics, technology assessment of renewable diesel, sustainable aviation fuel (SAF), renewable methanol covering advanced biofuels, and e-fuel production technologies

Transportation accounts for ~20% of all global CO2 emissions. While electric vehicles may provide the long-term sustainable solution for road vehicles, they do not address the large amounts of existing ICE (internal combustion engine) vehicles. They also cannot provide a feasible solution for aviation and shipping due to energy density constraints. Therefore, low-carbon fuels will be needed in large amounts to reach global net-zero targets. Many of these sustainable fuels can be drop-in replacements, requiring minimal changes in global infrastructure.

In this "Sustainable Biofuels & E-Fuels Market 2026-2036: Technologies, Players, Forecasts" report, IDTechEx provides detailed analysis of advanced biofuels (second generation and beyond) and e-fuels. This analysis encompasses production processes, relevant policies, key technological innovations, technology providers, and project developers. It also explores the techno-economic challenges and opportunities in the sector. The report focuses on key fuels such as renewable diesel, sustainable aviation fuel (SAF), and renewable methanol, amongst others.

New SAF demand emerging

Undoubtedly, 2025 was a landmark year for sustainable fuels. In both the UK and EU, regulation such as ReFuelEU Aviation means binding blending targets for SAF (sustainable aviation fuel) came into effect, creating unprecedented large-scale mandatory demand for SAF. New project announcements worldwide have focused on SAF rather than renewable diesel. This reflects the industry belief that SAF markets will be more lucrative long-term as the leading tool for aviation decarbonization. Subsequently, this IDTechEx report contains forecasting for SAF market potential, with the global SAF market projected to reach US$50 billion in 2036.

However, there is still a large amount of regulatory uncertainty surrounding SAF. For example, in the US, the planned project pipeline for SAF is very large, but current available government support for SAF would not economically incentivize SAF over renewable diesel production at most facilities outside of voluntary demand from airlines. In the short term, this may lead to significant SAF overcapacity as facilities open ahead of expected regulatory demand.

This IDTechEx report provides a comprehensive analysis of the renewable diesel and SAF markets, focusing on policy landscapes driving the market, production processes, notable technological innovations, key players, project case studies, and economics. It highlights the different production technologies and routes for renewable diesel and SAF production, exploring emerging pathways, as well as providing insights into the unique challenges and opportunities within each sector.

Renewable diesel and SAF beyond the "HEFA tipping point"

The HEFA/HVO pathway is a major contributor to early SAF growth. This is the lowest cost production pathway for SAF, with a selling price not too far from conventional jet fuel. However, HEFA feedstocks (used cooking oils, fats, and greases) are limited, and at some point beyond 2030, the global SAF market will have to start contending with the "HEFA tipping point" - when HEFA SAF supply will become insufficient to meet the rapidly growing demand for SAF spurred by increased decarbonization regulation.

This will force a pivot to emerging SAF pathways such as alcohol-to-jet, gasification/Fischer Tropsch, and e-SAF. These technologies are scaling up. For example, the first commercial ATJ facility (LanzaJet's Freedom Pines Fuels that came online in 2025) produces 9 million gallons of SAF and 1 million gallons of renewable diesel per year. However, high cost remains a significant barrier that technology development and regulation need to address.

This report provides a comprehensive analysis of second-generation biofuel technologies, such as cellulosic ethanol production, pyrolysis, gasification, Fischer-Tropsch (FT) synthesis, hydrothermal liquefaction (HTL) and alcohol-to-jet/gasoline, along with key innovations, project case studies, and technology suppliers. It also extensively covers the e-fuel landscape, focusing on production pathways, key players, and advancements in syngas generation, offering valuable insights into this rapidly evolving sector.

SAF production processes analyzed in this report. Source: IDTechEx

Low-carbon methanol

Renewable methanol production is also rapidly increasing, with several ~100,000 tonnes per annum facilities already under construction. China will soon emerge as the leading region given its dominant position in existing methanol markets, its low CAPEX construction, and its plentiful biomass and green hydrogen resources for emerging biomass gasification and e-methanol technologies. Demand for low-carbon methanol is being driven by demand for clean marine fuels, decarbonization of the chemical sector, and as a feedstock for the SAF (via the methanol-to-jet pathway). IDTechEx's report offers an in-depth analysis of the renewable methanol market, covering technology suppliers, key project developers, and announced project capacities, providing a detailed outlook on the future of renewable methanol.

Market forecasts & outlook

The sustainable fuel market is poised for significant growth in the coming years with IDTechEx forecasting the global renewable diesel and SAF production capacity is forecast to exceed 67 million tonnes annually by 2036, growing at a CAGR of 8.1% between 2026 and 2036. This impressive growth trajectory underscores the increasing importance of sustainable fuels in the global energy mix.

The major drivers for this growth are policy developments, such as SAF fuel mandates in the EU and UK or the US' 45Z tax credit, as well as a push from vehicle fleet operators and airlines to reduce carbon emissions. Another major driver is the emergence of a wide range of production technologies and their commercial uptake in sustainable fuel production projects. However, the sector also faces significant challenges associated with overall energy efficiency (especially when comparing e-fuels to EVs for road transport), feedstock availability, project development issues (long development timelines and significant funding needed) and achieving cost parity with conventional fossil fuels. Together, these drivers and challenges are shaping this rapidly developing market.

This report provides detailed market forecasts for various sustainable fuel types, including renewable methanol, renewable diesel, and SAF. Detailed market forecasts are provided, that may be broken down by production regions (Europe, North America, South America, and APAC) and technological pathways (e.g., HEFA/HVO, gasification-FT, and power-to-liquids/e-fuels) for renewable diesel, SAF, and renewable methanol. From detailed technology analyses to market forecasts and project case studies, this report provides the insights needed to understand and navigate the sustainable fuel landscape.

Key aspects

Introduction to the sustainable fuel market

Overview of the conventional (first generation) biofuel market

Second generation biofuel production technologies. For each of the below, IDTechEx analyzed the production technologies, key innovations, project case studies, technology suppliers, challenges & opportunities

Third & fourth generation biofuel technologies

E-fuel production landscape. For each of the below, IDTechEx analyzed the production technologies, key innovations, project case studies, technology suppliers, challenges & opportunities

Advanced biofuel & e-fuel markets

Market forecasts

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Why do we need to decarbonize transportation?

1.2. Role of sustainable fuels in transport sectors

1.3. Biofuel generations (1/2)

1.4. Overview of conventional (1st generation) biofuels

1.5. Historical dominance of conventional biofuels - bioethanol & biodiesel

1.6. Why move away from conventional biofuels?

1.7. The shift away from first generation biofuels

1.8. HVO/HEFA process - the dominant route for renewable diesel & SAF

1.9. 2nd generation biofuel production pathways

1.10. Cellulosic ethanol: Overview

1.11. Biomethanol production by technology: 2026-2036

1.12. Renewable diesel production pathways

1.13. SAF production pathways

1.14. Co-processing of biomass feedstocks in petroleum refineries

1.15. Overview of feedstocks for renewable diesel, SAF & gasoline

1.16. Alcohol-to-jet (ATJ) process steps

1.17. Overview of e-fuels

1.18. Scale of e-fuels as of 2025

1.19. Algae biofuels: 3rd/4th generation biofuels still have a long way to go

1.20. Business models for sustainable fuel technology developers

1.21. Technology & process developers in e-fuels by end-product

1.22. Project developers in e-fuels by end-product

1.23. Production technology providers for advanced biofuels & e-fuels

1.24. Production technology providers for advanced biofuels & e-fuels

1.25. Business models & considerations for project developers & fuel producers

1.26. RD & SAF project developers by production technology

1.27. SAF prices - a key issue holding back adoption

1.28. Key takeaways and outlook on SAF

1.29. Economics of renewable diesel production in the US

1.30. Key takeaways & outlook on renewable diesel

1.31. SAF production capacity by region: 2026-2036

1.32. SAF production by region: Discussion

1.33. SAF production capacity by technology: 2026-2036

1.34. SAF market: 2026-2036 (US$ billion)

1.35. Renewable diesel production by technology: 2026-2036

1.36. Renewable diesel production by technology: Discussion

1.37. Combined forecast for e-fuels: 2026-2036

1.38. Access More With an IDTechEx Subscription

2. INTRODUCTION TO BIOFUELS & POLICY LANDSCAPE

2.1. Global emissions driving temperature increase

2.2. Wide range of decarbonization solutions needed

2.3. Global transport emissions & role of sustainable fuels

2.4. Role of sustainable fuels in transport sectors

2.5. Role of biofuels in decarbonization of transportation

2.6. Overview of the biofuel supply chain & greenhouse gas emissions

2.7. Biofuel generations (1/2)

2.8. Biofuel generations (2/2)

2.9. Drivers & barriers for biofuel production/adoption

3. CONVENTIONAL BIOFUELS: BIOETHANOL & BIODIESEL

3.1. Bioethanol & biodiesel production

3.1.1. Historical dominance of conventional biofuels - bioethanol & biodiesel

3.1.2. Importance of bioethanol & its applications

3.1.3. Overview of 1st generation bioethanol production

3.1.4. Overview of 1st generation bioethanol production processes

3.1.5. Typical bioethanol production process - dry milling process using grains

3.1.6. Typical bioethanol production process - sugarcane ethanol process

3.1.7. Conventional biodiesel (FAME) vs petroleum diesel

3.1.8. Conventional biodiesel & its applications

3.1.9. Global biodiesel & renewable diesel production & consumption

3.1.10. Typical biodiesel production process

3.1.11. Further considerations in biodiesel production

3.2. Sustainability concerns around biofuels

3.2.1. The complex sustainability case for biofuels

3.2.2. Overview of the biofuel supply chain & greenhouse gas emissions

3.2.3. Overview of biofuel carbon emissions - corn ethanol example

3.2.4. Land use change: Direct (LUC) & indirect (ILUC)

3.2.5. Sustainability of biofuels & land use change

3.2.6. LCA comparison for biofuels

3.2.7. Lifecycle emissions of biofuels & land use change (LUC)

3.2.8. Land use emissions from biofuel generations

3.2.9. Regional variations in emissions from land use change

3.2.10. Fuel carbon intensity comparison per MJ

3.2.11. Fuel carbon intensity comparisons per km

3.2.12. Carbon emissions from electric vehicles

3.2.13. Comparison of lifecycle emissions from various vehicles

3.2.14. The shift away from first generation biofuels

4. SECOND GENERATION BIOFUEL TECHNOLOGIES

4.1. Introduction to advanced biofuels

4.1.1. Petroleum product ranges & sustainable fuel alternatives

4.1.2. Acronyms & definitions for advanced biofuels

4.1.3. Biodiesel vs renewable diesel: Properties & engine compatibility

4.1.4. Comparison of fossil diesel, biodiesel & renewable diesel

4.1.5. Jet fuel composition & types

4.1.6. SAF as a drop-in replacement for Jet A-1

4.1.7. 2nd generation biofuel production pathways

4.1.8. Biofuel technology overview

4.1.9. Biofuel technology overview

4.1.10. Biofuel technology overview

4.1.11. Comparing production costs for biofuel routes to SAF

4.2. Cellulosic ethanol production

4.2.1. Lignocellulosic biomass feedstocks

4.2.2. Cellulosic ethanol production overview

4.2.3. Challenges in breaking down lignocellulosic biomass

4.2.4. Enzyme uses in biofuel production

4.2.5. Cellulosic ethanol company landscape

4.2.6. Cellulosic ethanol company case study

4.2.7. Cellulosic ethanol company case study

4.2.8. Cellulosic ethanol have faced significant challenges

4.2.9. Common challenges faced by cellulosic ethanol producers

4.2.10. Is cellulosic ethanol production dead?

4.2.11. Active and ongoing cellulosic ethanol projects

4.2.12. SAF production is a new opportunity for cellulosic ethanol producers

4.2.13. Key cellulosic ethanol companies targeting SAF

4.3. Pyrolysis technologies

4.3.1. Introduction to biomass & plastic waste pyrolysis

4.3.2. Pyrolysis products & market applications

4.3.3. Key technical factors that impact the design of the pyrolysis process

4.3.4. Pyrolysis reactor designs

4.3.5. Overview of decomposition methods in biomass & plastic pyrolysis

4.3.6. Considerations in pyrolysis plant design: Heating methods

4.3.7. Size limitations of pyrolysis reactors

4.3.8. Composition of bio-oil & plastic pyrolysis oil

4.3.9. Factors influencing oil quality & downstream processing into fuels

4.3.10. Comparison of pyrolysis technologies

4.3.11. Hydrogen deficiency in oils & need for additional hydrogen

4.3.12. Pyrolysis companies involved in sustainable fuel production

4.3.13. Pyrolysis biocrude company case study - Alder Renewables

4.4. Gasification technologies

4.4.1. Biomass & waste gasification overview

4.4.2. Comparison of pyrolysis and gasification processes for waste

4.4.3. Gasification & Fischer-Tropsch biomass-to-liquid (BtL) pathway

4.4.4. Pre-treatment methods for gasification of biomass and plastics

4.4.5. Gasifier types

4.4.6. Biomass gasifier performance comparison

4.4.7. Pros & cons of different gasifier types

4.4.8. Gasification technology developers

4.4.9. Gasifier types for biomass gasification

4.4.10. Novel technologies for biomass gasification (1/2)

4.4.11. Innovations in biomass gasification technology (2/2)

4.4.12. Concord Blue - novel gasification & reforming concept

4.4.13. Gasification technology suppliers

4.4.14. Gasification catalysts

4.4.15. Biomass gasification + FT projects - operational and planned

4.4.16. Gasification-FT bio-SAF project case study - Altalto Immingham

4.4.17. Fulcrum BioEnergy - a failed SAF producer

4.4.18. Biomass gasification for hydrogen production

4.4.19. Biomass gasification for methanol production

4.5. Hydrothermal liquefaction (HTL) technologies

4.5.1. Overview of hydrothermal liquefaction (HTL)

4.5.2. Role of water in hydrothermal liquefaction

4.5.3. Hydrothermal liquefaction feedstocks - biomass

4.5.4. Hydrothermal liquefaction feedstocks - plastics

4.5.5. Hydrothermal liquefaction of plastic waste - Licella case study

4.5.6. Hydrothermal liquefaction feedstocks - biomass vs plastics

4.5.7. Overview of key HTL reactor designs

4.5.8. Hydrothermal liquefaction technology developers - process scale & feedstock

4.6. Fischer-Tropsch (FT) synthesis

4.6.1. Fischer-Tropsch synthesis: Syngas to hydrocarbons

4.6.2. Fischer-Tropsch (FT) synthesis overview

4.6.3. Overview of incumbent FT catalysts

4.6.4. Overview of FT reactor designs

4.6.5. Overview of FT reactors

4.6.6. FT reactor design comparison

4.6.7. FT reactor innovation - microchannel reactors

4.6.8. FT reactor innovation - microstructured reactor

4.6.9. Fischer Tropsch catalysts for e-fuels

4.6.10. Fischer-Tropsch (FT) technology suppliers by reactor type

4.7. Biocrude oil refining & upgrading technologies

4.7.1. Refining & upgrading processes used in biorefineries

4.7.2. Hydrotreating processes

4.7.3. Hydrocracking process

4.7.4. Isomerization process

4.7.5. Dewaxing process

4.7.6. Fractional distillation process: Overview

4.7.7. Fractional distillation process: Detailed considerations

4.7.8. Hydrogen consumption by upgrading processes

4.7.9. Implications of high hydrogen consumption in upgrading processes

4.7.10. Key challenges & process considerations in upgrading processes

4.7.11. Hydrotreating, hydrocracking and isomerization technology suppliers

4.7.12. Hydrotreating, hydrocracking and isomerization technology suppliers

4.8. Biomethanol production

4.8.1. Overview of methanol production & colors

4.8.2. Traditional methanol production

4.8.3. Main pathways to biomethanol production

4.8.4. Biomethanol from biogas reforming

4.8.5. Steam methane reforming

4.8.6. Biomethanol project using biogas & new reforming technology

4.8.7. Biomethanol from biomass gasification

4.8.8. Biomethanol from hydrothermal gasification

4.8.9. Key players in methanol synthesis technology

4.9. Alcohol-to-jet (ATJ) & alcohol-to-gasoline (ATG): Methanol & ethanol

4.9.1. Ethanol feedstocks

4.9.2. CO2-to-ethanol route: LanzaTech

4.9.3. Methanol feedstocks

4.9.4. Methanol-to-gasoline (MTG) process overview

4.9.5. Conventional fixed bed MTG process

4.9.6. New fluidized bed MTG process

4.9.7. Alcohol-to-jet (ATJ) process steps

4.9.8. Ethanol & methanol production

4.9.9. Alcohol dehydration & oligomerization

4.9.10. Hydrogenation, isomerization & fractional distillation to jet

4.9.11. MTG vs MTJ process comparison

4.9.12. Pros & cons of alcohol-to-jet (ATJ) versus competing SAF routes

4.9.13. LanzaJet: World's first commercial-scale ethanol-to-jet plant

4.9.14. Methanol-to-gasoline (MTG) technology providers

4.9.15. Alcohol-to-jet (ATJ) technology providers

4.9.16. Alcohol-to-jet (ATJ) technology providers

4.9.17. Alcohol-to-jet (ATJ) technology providers

5. THIRD & FOURTH GENERATION BIOFUEL TECHNOLOGIES

5.1. Introduction to third & fourth generation biofuels

5.2. Macroalgae, microalgae and cyanobacteria

5.3. Algae has multiple market applications

5.4. 3rd generation biofuel production: Feedstocks

5.5. Biofuel production process using macroalgae

5.6. Biofuel production process using microalgae/cyanobacteria

5.7. Algal biofuel production - process example

5.8. Metabolic pathways in microalgae cultivation

5.9. Key growth criteria in microalgae cultivation

5.10. Open vessels for microalgae cultivation

5.11. Closed vessels for microalgae cultivation

5.12. Open vs closed algae cultivation systems

5.13. Microalgae cultivation system suppliers: Photobioreactors (PBRs) & ponds

5.14. Case study - algae used for sustainable aviation fuel (SAF) production

5.15. Algal biofuel development has faced historical challenges

5.16. Algal biofuel companies shifted focus or went bust

5.17. Key players in algal and microbial biofuel processes & projects

5.18. Key players in algal and microbial biofuel processes & projects

5.19. Key players in algal and microbial biofuel processes & projects

5.20. SAF projects planning to use microalgae

5.21. SAF projects planning to use microalgae

5.22. SWOT analysis for 3rd and 4th generation biofuel production

5.23. Outlook for 3rd and 4th generation biofuels

6. E-FUEL PRODUCTION

6.1. Overview of e-fuels

6.1.1. What is an e-fuel?

6.1.2. Why do we need e-fuels?

6.1.3. Comparison of e-fuels to fossil and biofuels

6.1.4. CO2 as a key raw material for synthetic fuels

6.1.5. Overview of energy & carbon flows in e-fuel production

6.1.6. E-fuel production efficiencies

6.1.7. Energy efficiency challenges surrounding e-fuels

6.1.8. E-fuels must be used in specific contexts

6.1.9. SWOT analysis for e-fuels

6.1.10. e-Fuel specific mandates

6.1.11. Challenges and opportunities for e-fuels

6.1.12. Role of green hydrogen in e-fuel production

6.1.13. Electrolyzer cells, stacks and balance of plant (BOP)

6.1.14. Overview of electrolyzer technologies

6.1.15. Comparison of electrolyzer performance characteristics

6.1.16. Overview of leading electrolyzer OEMs globally

6.1.17. Pros & cons of the four main electrolyzer technologies

6.1.18. The source of captured CO2 matters

6.1.19. CO2 source for e-fuel production under the EU's Renewable Energy Directive

6.1.20. Most e-fuel projects source biogenic CO2

6.1.21. Which carbon capture technologies are most mature?

6.1.22. Point-source carbon capture technology providers

6.1.23. e-Fuel production costs vary by region

6.1.24. Scale of e-fuels as of 2025

6.2. Syngas production for e-fuels

6.2.1. Reverse water gas shift converts CO2 into syngas

6.2.2. Catalysts for reverse water gas shift

6.2.3. RWGS catalyst innovation case study

6.2.4. Reactors for reverse water gas shift

6.2.5. RWGS reactor innovation case study

6.2.6. CO2-to-syngas processes: Alternatives

6.2.7. Alternative CO2 reduction technologies considerations

6.2.8. Comparison of RWGS & SOEC co-electrolysis routes

6.2.9. Solid oxide electrolyzer (SOEC) overview

6.3. e-Methane production

6.3.1. Methane classifications & power-to-gas (P2G)

6.3.2. Methanation overview

6.3.3. Thermocatalytic vs biocatalytic methanation

6.3.4. Operational e-methane projects

6.3.5. Thermocatalytic methanation technology providers

6.3.6. Comparison of thermocatalytic methanation reactors

6.3.7. Process flow diagrams: Thermocatalytic methanation technologies

6.3.8. Biological methanation technology providers

6.3.9. Ex-situ vs in-situ biological methanation

6.3.10. Bio-electrochemical methanation

6.3.11. e-Methane production in Europe

6.3.12. Recent advances in biological e-methane technologies

6.3.13. Economics of e-methane production

6.3.14. SWOT for methanation technology

6.3.15. Power-to-methane projects worldwide - current and announced

6.3.16. e-Methane production in 2025

6.4. e-Methanol production

6.4.1. Overview of methanol production & colors

6.4.2. e-Methanol production

6.4.3. Topsoe's CO2-to-methanol catalysts

6.4.4. Clariant's CO2-to-methanol catalysts

6.4.5. Tube cooled reactors for CO2-to-methanol

6.4.6. Toyo Engineering's small-scale methanol reactor

6.4.7. Key players in methanol synthesis

6.4.8. Key players in methanol synthesis

6.4.9. Start-ups with novel methanol synthesis concepts

6.4.10. Start-ups with novel methanol synthesis concepts

6.4.11. Project developers and technology/process developers in e-methanol

6.4.12. e-Methanol production in 2025

6.5. e-Kerosene, e-SAF, e-Gasoline, e-Diesel, and e-Waxes

6.5.1. Overview of pathways to liquid hydrocarbon e-fuels

6.5.2. Fischer-Tropsch vs Methanol-to-jet for e-SAF

6.5.3. Fischer-Tropsch vs Methanol-to-jet pathway economics

6.5.4. Fischer Tropsch catalysts for e-fuels

6.5.5. Large industrial-scale e-fuel plant concepts

6.5.6. MTG e-fuel plant case study

6.5.7. Modular e-fuel plant concepts

6.5.8. RWGS-FT e-fuel plant case study

6.5.9. Conversion of existing gas-to-liquid (GTL) facilities to e-fuels

6.5.10. Products slate from Fischer Tropsch for e-SAF

6.5.11. Large-scale e-fuel projects: Operational and under construction

6.5.12. Key suppliers for large-scale e-fuel plants

6.5.13. Technology & process developers in e-fuels by end-product

6.5.14. Project developers in e-fuels by end-product

6.5.15. e-Kerosene, e-gasoline, e-diesel, and e-waxes production in 2025

7. ADVANCED BIOFUEL & E-FUEL MARKETS

7.1. Renewable methanol market

7.1.1. Current state of the methanol market

7.1.2. Current state of the methanol market by region

7.1.3. Future methanol applications

7.1.4. Main growth drivers for low-carbon methanol

7.1.5. Methanol is a leading low-carbon shipping fuel

7.1.6. Overview of methanol production & colors

7.1.7. Production costs for green methanol routes

7.1.8. Maximum selling prices for renewable methanol in the EU

7.1.9. Main pathways to biomethanol production

7.1.10. Biomethanol project developers - company landscape

7.1.11. Biomethanol plants using biogas

7.1.12. Biomethanol plants using gasification

7.1.13. e-Methanol projects under active development (post-feasibility)

7.1.14. e-Methanol projects under active development (post-feasibility)

7.1.15. e-Methanol project developers - company landscape

7.1.16. Low carbon methanol market by region: Europe and China

7.2. Renewable diesel & SAF - general market narratives

7.2.1. Overview of feedstocks for renewable diesel, SAF & gasoline

7.2.2. Typical product splits in renewable diesel & SAF production

7.2.3. Co-processing of biomass feedstocks in petroleum refineries

7.2.4. Future integrated biorefineries

7.2.5. Business models for sustainable fuel technology developers

7.2.6. Production technology providers for advanced biofuels & e-fuels

7.2.7. Production technology providers for advanced biofuels & e-fuels

7.2.8. Key techno-economic factors influencing sustainable fuel projects

7.2.9. Business models & considerations for project developers & fuel producers

7.2.10. RD & SAF project developers by production technology

7.2.11. Key challenges in biofuel projects

7.2.12. Key challenges in e-fuel (power-to-liquids) projects

7.2.13. Renewable diesel & SAF lifecycle emissions

7.2.14. Factors influencing HEFA renewable diesel & SAF production costs

7.2.15. Renewable diesel production costs

7.3. Renewable diesel market

7.3.1. Renewable diesel & its end-use markets

7.3.2. Biodiesel vs renewable diesel: Feedstocks & production process

7.3.3. Global renewable diesel production

7.3.4. Current state of renewable diesel in the US

7.3.5. Drivers of renewable diesel production in the US

7.3.6. Economics of renewable diesel production in the US

7.3.7. Market data for Renewable Diesel 2025

7.3.8. Renewable diesel or SAF?

7.3.9. Renewable diesel production pathways

7.3.10. Key takeaways & outlook on renewable diesel

7.4. Sustainable aviation fuel (SAF) market

7.4.1. The critical importance of SAF in decarbonizing aviation

7.4.2. Government targets & mandates for SAF

7.4.3. Government targets & mandates for SAF - focus on EU & UK

7.4.4. Government incentives for SAF producers

7.4.5. CORSIA: Decarbonizing global aviation

7.4.6. Overview of SAF commitments by passenger & cargo airlines

7.4.7. Major passenger airline commitments & activities in SAF

7.4.8. Book and claim SAF business model

7.4.9. Summary of key market drivers for SAF

7.4.10. Main SAF production pathways

7.4.11. Bio-SAF vs e-SAF - the two main pathways to SAF

7.4.12. ASTM-approved production pathways

7.4.13. HEFA-SPK producer case study - Neste

7.4.14. Gasification-FT bio-SAF project case study - Altalto Immingham

7.4.15. ATJ project case study - Freedom Pines

7.4.16. e-SAF project case study - ERA ONE

7.4.17. Fulcrum BioEnergy - a failed SAF producer

7.4.18. Other cancelled SAF projects & reasons for failure

7.4.19. SAF prices - a key issue holding back adoption

7.4.20. Who will pay for the green premium of SAF?

7.4.21. Key drivers and challenges for SAF cost reduction

7.4.22. SAF production capacities and market outlook

7.4.23. Key takeaways and outlook on SAF

8. MARKET FORECASTS

8.1. Sustainable fuel market forecasting methodology & assumptions

8.2. Combined forecast for sustainable fuels: 2026-2036

8.3. Combined forecast for e-fuels: 2026-2036

8.4. Biomethanol production capacity by region: 2026-2036

8.5. Biomethanol production by region: Discussion

8.6. Biomethanol production capacity by technology: 2026-2036

8.7. e-Methanol production capacity by region: 2026-2036

8.8. e-Methanol production by region: Discussion

8.9. Renewable diesel production by technology: 2026-2036

8.10. Renewable diesel production by technology: Discussion

8.11. SAF production capacity by region: 2026-2036

8.12. SAF production by region: Discussion

8.13. SAF production capacity by technology: 2026-2036

8.14. SAF market: 2026-2036 (US$ billion)

9. COMPANY PROFILES

9.1. Avioxx

9.2. Brineworks

9.3. Carbon Neutral Fuels

9.4. Carbon Recycling International

9.5. CarbonBridge

9.6. Circlia Nordic

9.7. Concord Blue Engineering

9.8. CyanoCapture

9.9. Dimensional Energy

9.10. eChemicles

9.11. ExxonMobil: Methanol-to-Gasoline (MTG)

9.12. GIG Karasek: ECO2CELL

9.13. HIF Global (Highly Innovative Fuels)

9.14. Hitachi Zosen Corporation: PEMEL & Methanation Technologies

9.15. HYCO1

9.16. IHI Corporation: Methanation System

9.17. INERATEC

9.18. Infinium

9.19. KEW Technology

9.20. LanzaJet

9.21. LanzaTech

9.22. OXCCU

9.23. Q Power

9.24. Sekisui Chemical: Chemical Looping for CO₂ Utilization

9.25. Shell Catalysts & Technologies: SGP Gasifier

9.26. Synhelion

9.27. Syzygy Plasmonics

9.28. TES (Tree Energy Solutions): e-NG

9.29. Velocys

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野の最新刊レポート

IDTechEx社の 持続可能性 - Sustainability分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|