PEM燃料電池用材料 2026-2036年:技術、市場、プレーヤーMaterials for PEM Fuel Cells 2026-2036: Technologies, Markets, Players 輸送産業で使用されるPEM燃料電池の材料需要について、OEM、材料サプライヤー、主要部品メーカーの広範な調査に基づき、10年間の詳細な市場予測を実施:BPP、GDL、アイオノマー膜、CCMs 燃料電池(FCEV... もっと見る

サマリー輸送産業で使用されるPEM燃料電池の材料需要について、OEM、材料サプライヤー、主要部品メーカーの広範な調査に基づき、10年間の詳細な市場予測を実施:BPP、GDL、アイオノマー膜、CCMs 燃料電池(FCEV)市場の拡大に伴い、固体高分子形燃料電池(PEM)の材料需要も拡大すると予想される。本レポートでは、バイポーラプレート(BPP)、ガス拡散層(GDL)、触媒コートメンブレン(CCM)、メンブレン電極アセンブリ(MEA)、アイオノマー、白金触媒など、PEM燃料電池のコンポーネントの主要情報について詳述する。

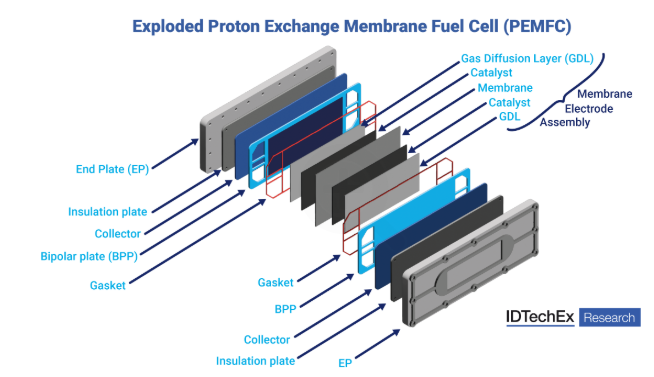

固体高分子形燃料電池(PEMFC)の分解模式図。個々の燃料電池部品と膜電極接合体(MEA)を示す。出典:IDTechExIDTechEx

PEM燃料電池は様々な構成要素の相乗的相互作用によって作動する。BPPは燃料電池全体に燃料を供給し、GDLは反応物と生成物をそれぞれ触媒層へ/触媒層から輸送する。触媒は膜(CCM)上にコーティングされ、膜自体はプロトンを燃料電池の一方から他方へ輸送する。CCMとGDLを総称してMEAと呼ぶ。PEM燃料電池用材料市場は、2026年から2036年にかけて年平均成長率24%で成長すると予想されているが、燃料電池に使用される部品に関しては重要な疑問がある。既存材料と新興材料の動向は?需要の増加に対応するため、これらの部品の製造方法はどのように変化するのか?拡大する燃料電池部品市場の主要プレーヤーは?

PEM燃料電池コンポーネントの技術動向

本レポートでは、燃料電池内の主要コンポーネントの内訳を示し、それぞれの事例で使用されている既存の材料と技術を詳述しています。サプライチェーンや業界内の主要プレーヤーを分析することで、市場全体の概要を構築している。しかし、既存の材料であっても、材料の選択によって技術にバリエーションが生まれる可能性はある。BPPを例にとると、典型的な材料選択には、金属(チタン、ステンレス鋼など)またはグラファイト製のプレートが含まれる。本レポートでは、金属プレートとグラファイトプレートのベンチマークを示し、各素材が最も適している特定の車種(乗用車、バン、トラック、バス、船舶、列車)に焦点を当てている。

アイオノマー膜のナフィオンのような有力な既存材料にもかかわらず、破壊的技術が出現し始めており、早期に有望な兆しを見せている一方、PFAS材料を制限する潜在的規制が市場に大きな影響を与える可能性がある。新素材、コーティング、製造技術は学術的な段階にあり、早期に商業的な利用も始まっている。代替高分子交換膜の包括的な分析が実施され、燃料電池の最適性能を確保するために最も重要なパラメータについて、既存のナフィオンに対するベンチマークが示されている。

IDTechEx は、BEV がゼロ・エミッション車市場を支配すると予測しているが、ゼロ・エミッション車への推進に伴い、 FCEV が自動車セクター全体のシェアを拡大すると予測している。特に、FCEV は、トラック、船舶、列車などの大型車セクターで有望であり、サプライチェーンのハブツーハブコネクターと して機能するため、多様な水素燃料インフラの必要性が軽減される。このような市場シェアの拡大により、PEM燃料電池を構成するすべての部品に対する材料需要が増加し、その主な結果として、規模の経済が定着するにつれて部品のコストが削減されることになる。

本報告書では、既存技術の最適化から新素材や自動製造システムまで、構成部品のコスト削減の道筋をいくつか概説している。BPP材料の場合、多様なメーカー、現在実用化されている様々な材料と製造技術、そして提案されている技術について詳細な概要が示されており、燃料電池を動力とする輸送手段がより広範囲に普及するにつれて、プレート1枚当たりの価格がどのように上昇するかについても論じられている。

市場を牽引するもの

政府が、特に都市環境におけるゼロエミッション車の導入を支援する政策を制定しようとしている中、いくつかの政府機関は、BEVや従来の内燃エンジン車との競争を可能にするために燃料電池技術のコストを下げるという全体的な目標を掲げ、メーカーや材料サプライヤーが取り組むべき目標を設定している。本レポートでは、これらの目標が燃料電池用材料市場に与える影響について取り上げている。例えば、米国エネルギー省(DOE)による燃料電池の触媒質量目標が、材料のR&D分野にどのような影響を与えているかなどである。

R&Dを推進するその他の要因には、材料の経済的価値や燃料電池スタックの効率などがある。新興材料が燃料電池の白金に取って代わり、触媒(およびCCM)のコストを削減する方法については、本レポートで取り上げている。一方、コンポーネントのフォームファクターを小さくすることでスタックの出力密度を高めたいという要望は、より薄いBPPの開発に最も明確に表れている。本レポートでは、これらのプレートを製造するための新しいコーティング技術や製造方法を取り上げている。

包括的な分析と市場予測

IDTechExは電気自動車産業を包括的にカバーしており、BEVとFCEVを船舶と鉄道とともに詳述している。FCEVの調査は乗用車、小型商用車(バン)、大型トラック、市バスで区分している。定置用燃料電池市場については、PEMを含む様々なタイプの燃料電池をカバーしています。技術および市場動向に関する専門知識は、世界規模の主要企業へのインタビューや複数の会議への出席を通じて構築しています。

本レポートでは、FCEV業界におけるIDTechExの予測に基づき、輸送用途におけるPEMFCの材料需要について、主要燃料電池部品(BPP、GDL、CCM、MEA、アイオノマーなど)を輸送手段別、車両タイプ別に分類し、きめ細かな10年間の市場予測を提供している。各構成部品に関連する価値を詳述しながら、構成部品の材料需要について単位と数量の両方で予測を行っている。

主要側面

本レポートは以下の情報を提供する

技術動向

バリューチェーン分析

市場予測&分析

目次1.要旨と結論

1.1.PEMFCの概要

1.2.PEMFCの主要部品

1.3.燃料電池の用途と主要プレーヤー

1.4.BPP:目的とフォームファクター

1.5.BPPの材料:グラファイトと金属の比較

1.6.BPPメーカーのフローチャート

1.7.GDL:目的とフォームファクター

1.8.FCEV スタック用 GDL サプライチェーン

1.9.膜:目的とフォームファクター

1.10.主要な最新PFSA膜 - 主なプレーヤーと特性

1.11.イオン交換膜材料のベンチマーク - PEM燃料電池

1.12.PFAS規制に対する継続的な懸念

1.13.触媒:触媒:目的とフォームファクター

1.14.燃料電池用触媒の動向

1.15.燃料電池用触媒の主要サプライヤー

1.16.PEM燃料電池のプラントバランス

1.17.市場予測の概要

1.18.PEM燃料電池市場価値(百万米ドル)2026-2036年

1.19.IDTechEx サブスクリプションでさらにアクセス

2.市場予測

2.1.1.予測方法と前提条件

2.1.2.PEM燃料電池の用途別需要(MW) 2023-2036年

2.1.3.PEM燃料電池市場金額(百万米ドル) 2023-2036年

2.1.4.市場予測バイポーラプレート

2.1.5.用途別BPP需要(百万ユニット) 2023-2036年

2.1.6.BPPの需要(百万ユニット):材料別 2023-2036年

2.1.7.BPPの金額(百万米ドル):材料別 2023-2036年

2.1.8.市場予測ガス拡散層

2.1.9.用途別GDL需要(単位:万m2) 2023-2036年

2.1.10.用途別GDL価値(百万米ドル) 2023-2036年

2.1.11.GDL材料需要(トン) 2023-2036年

2.2.市場予測膜、触媒、CCM

2.2.1.用途別PEM需要(千平方メートル) 2023-2036年

2.2.2.用途別PEM価値(百万米ドル) 2023-2036年

2.2.3.用途別触媒/PGM需要(kg) 2023-2036年

2.2.4.用途別 CCM 価値(百万米ドル) 2023-2036年

3.序論

3.1.1.燃料電池の紹介

3.1.2.燃料電池とは何か?

3.1.3.PEMFCの概要

3.1.4.PEMFCの動作原理

3.1.5.水-ガスシフト(WGS)&サワーシフト反応器

3.1.6.PEM電解槽とPEM燃料電池の比較

3.1.7.PEMFCの主要コンポーネント

3.1.8.燃料電池技術の概要

3.1.9.燃料電池技術の比較

3.1.10.高温PEMFC(1)

3.1.11.高温PEMFC(2)

3.1.12.燃料電池自動車とは?

3.1.13.燃料電池自動車の魅力

3.1.14.燃料電池のモビリティ用途

3.1.15.PEMFC市場のプレーヤー

3.1.16.中国のPEMFC市場プレーヤー

3.2.水素経済

3.2.1.水素市場の現状

3.2.2.水素製造・普及の主な推進要因

3.2.3.水素開発を促進する主な法律と資金調達メカニズム

3.2.4.欧州の水素市場 - 主な進展

3.2.5.欧州の水素市場 - 主な挫折と課題

3.2.6.米国の水素市場の促進要因 - 2025年以前

3.2.7.米国の水素市場の課題 - 2024年と2025年

3.2.8.米国の低炭素水素産業の展望

3.2.9.世界の低炭素水素産業の展望

4.燃料電池車市場

4.1.燃料電池自動車とは?

4.2.水素経済における燃料電池自動車

4.3.燃料電池車プロトタイプの30年

4.4.BEVとFCEVのシステム効率

4.5.燃料電池車のモデル

4.6.燃料電池乗用車の成長、停滞、凋落

4.7.トヨタ・モビリティ・ロードマップ

4.8.トヨタMIRAI第2世代

4.9.トヨタFCEVの2024年以降の目標

4.10.ヒュンダイ 燃料電池乗用車の歴史

4.11.ヒュンダイNEXO SUV

4.12.2021年からの韓国補助金インセンティブ:FCEVを後押しするも、BEVははるかに先

4.13.ホンダ、FC-クラリティを廃止:需要低迷

4.14.ホンダ、FCEV市場に再参入

4.15.BMWがFCEVを生産

4.16.中国のFCEV車

4.17.燃料電池乗用車の展望

4.18.小型商用車の定義

4.19.燃料電池LCV

4.20.燃料電池LCVに関するIDTechExの見通し

4.21.トラック重量の定義

4.22.バッテリートラックと燃料電池トラックの比較航続距離

4.23.燃料電池トラックにおける燃料電池メーカーの協力

4.24.燃料電池トラックの展望

4.25.燃料電池バス - 新市場が販売台数を押し上げる可能性

4.26.燃料電池バスの主な利点/欠点

4.27.燃料電池バスの展望

4.28.2045 年の FCEV 対 BEV 市場シェア

5.FCトレイン市場

5.1.列車タイプの概要

5.2.ゼロ・エミッション鉄道の推進要因

5.3.燃料電池列車の概要

5.4.燃料電池列車の航続距離の優位性

5.5.鉄道用燃料電池技術のベンチマーク

5.6.鉄道用燃料電池サプライヤー

5.7.FCマルチプルユニットの概要

5.8.FC機関車の概要

5.9.燃料電池・電気機関車の展望

6.FC船舶市場

6.1.船舶用燃料電池の紹介

6.2.船舶用燃料電池技術

6.3.燃料電池サプライヤー:リーダーとチャレンジャー

6.4.燃料電池サプライヤー市場シェア 2019-2024年

6.5.船舶タイプ別燃料電池納入量 2019-2024年

6.6.舶用燃料電池の政策推進要因

6.7.舶用PEM燃料電池の展望

7. 固定FC市場

7.1.1.定置用燃料電池アプリケーション

7.1.2.定置用燃料電池アプリケーション市場の概要

7.1.3.PEMFC産業用ケーススタディ

7.1.4.PEMFC商業用ケーススタディ

7.1.5.PEMFCユーティリティ発電のケーススタディ

7.1.6.PEMFC通信ケーススタディ

7.1.7.定置用燃料電池市場の展望

7.2.定置用PEMFCプレーヤー

7.2.1.定置用PEMFC市場の概要

7.2.2.主要プレーヤーによる買収

7.2.3.バラード・パワー・システムズの概要

7.2.4.バラード社の技術

7.2.5.バラード・パワー社の定置用燃料電池技術

7.2.6.バラード・パワーのグローバル製造能力と主要パートナー

7.2.7.プラグパワーの概要

7.2.8.プラグ・パワー社の技術概要

7.2.9.プラグ・パワーの定置電力技術と燃料供給

7.2.10.プラグパワーの顧客

7.2.11.パワーセルグループの概要

7.2.12.パワーセルグループの技術

7.2.13.PowerCell グループのパートナーシップと契約

7.2.14.インテリジェント・エナジーの概要

7.2.15.インテリジェント・エナジーの定置電力技術

7.2.16.インテリジェントエナジーのパートナーシップ

7.2.17.東芝の概要

7.2.18.東芝の燃料電池技術

7.2.19.カミンズの概要

7.2.20.カミンズの燃料電池技術によるアクセラ

7.2.21.SFCエネルギーの概要

7.2.22.SFCエナジーのPEMFC技術

8.バイポーラプレート

8.1.1.バイポーラ・プレートの目的

8.1.2.BPPフォームファクター

8.1.3.BPPフォームファクターの効果

8.1.4.バイポーラプレート組み立て(BPA)

8.2.BPPの材料

8.2.1.BPPで考慮すべき重要な材料パラメーター

8.2.2.BPP材料としてのグラファイト

8.2.3.BPP材料としての金属

8.2.4.BPAのコスト上昇

8.2.5.金属BPPにはコーティングが必要

8.2.6.金属BPPのコーティングの選択

8.2.7.BPPの製造方法

8.2.8.BPP製造業者のフローチャート

8.3.BPPメーカー

8.3.1.BPPサプライヤーの概要(非網羅的リスト)

8.3.2.ケーススタディ(NCチタン):神戸製鋼所

8.3.3.ケーススタディ(デュアルサプライ):ダナ

8.3.4.ケーススタディ(グラファイト):SGLカーボン

8.3.5.ケーススタディ(黒鉛複合材):FJコンポジット

8.3.6.ケーススタディ(システムサプライヤー):シューラー

8.3.7.ケーススタディ(レーザーエッチング)SITEC

8.3.8.マイクロプレシジョン - ケミカルエッチング

8.3.9.スイッツァー - ケミカルエッチング

8.3.10.Yiangteng

8.3.11.Hongfeng - グラファイト

8.3.12.グラファイト BPP サプライヤーの比較

8.3.13.グラファイトBPPのランク比較

8.4.BPPコーティング専門メーカー

8.4.1.インパクト・コーティングス

8.4.2.Precors

8.5.BPPの最新動向と研究

8.5.1.バイポーラプレートフローフィールドの今後の方向性

8.5.2.プリント基板のBPP - Bramble Energy

8.5.3.BPPの最新動向

8.5.4.ループ・エネルギー

8.5.5.CoBiPプロジェクト

8.5.6.BPPへの共同アプローチ

8.5.7.BPPの初期段階の商業的開発

8.5.8.BPPに関する最近の学術研究

8.5.9.燃料電池用織物メッシュ

8.5.10.NBCメッシュテック

8.5.11.Haver & Boecker

8.5.12.新たな製造方法

8.5.13.BPPへの共同アプローチ

9.ガス拡散層

9.1.1.多孔質輸送層(PTL)&ガス拡散層(GDL)の概要

9.1.2.PTL/GDLの特性と材料

9.1.3.代表的なGDL構造

9.1.4.カソードGDL:疎水処理

9.1.5.ウェット対ドライGDL性能

9.1.6.GDL製造プロセス

9.1.7.セルロース繊維GDL:MPL不要

9.1.8.GDLと触媒層の相互作用

9.1.9.GDLの技術革新動向

9.1.10.疎水性と親水性の二重挙動への注目

9.2.GDL サプライチェーンとプレーヤー

9.2.1.FCEV スタック用 GDL サプライチェーン

9.2.2.GDL プレーヤーSGL カーボン

9.2.3.GDLプレーヤー東レ

9.2.4.GDL プレーヤーフロイデンベルグ

9.2.5.AvCarb - 燃料電池用GDL設計の進歩

9.2.6.主要GDLサプライヤー

10.膜

10.1.1.膜の目的

10.1.2.膜のフォームファクター

10.1.3.燃料電池における水管理

10.1.4.プロトン交換膜の歴史、機能、材料

10.1.5.PFSAアイオノマーの構造と特性を規定する主要パラメーター

10.1.6.膜について考慮すべき重要な材料パラメーター

10.1.7.PEM膜の劣化を引き起こす要因の概要

10.1.8.膜メーカーの歴史的展望と主要特性

10.1.9.ナフィオン-市場をリードする膜

10.1.10.ケムール社のナフィオンの特性とグレード

10.1.11.ナフィオンとPFSA膜の長所と短所

10.1.12.プロトン交換膜市場の展望

10.1.13.最新のPFSA膜の主要プレーヤーと特性

10.1.14.PFSA膜特性の比較

10.1.15.イオン交換膜材料のベンチマーク - PEM燃料電池

10.1.16.プロトン交換膜のサプライチェーン例 - ゴア

10.1.17.高温プロトン交換膜

10.1.18.PEMFC膜の革新はPEMELに影響を与えるかもしれない(1)

10.1.19.PEMFC膜の技術革新がPEMELに影響を与える可能性(2)

10.1.20.PFASに関する継続的な懸念

10.1.21.PEM燃料電池膜としての炭化水素

10.1.22.代替PEM材料:炭化水素IEM

10.1.23.炭化水素膜の評価

10.1.24.既存のPFAS膜に対するIonomr膜のベンチマーク

10.1.25.代替電解質膜材料:グラフェン複合材料

10.2.PFAS膜の製造

10.2.1.ポリマーピラミッドにおけるフッ素樹脂

10.2.2.PFSAアイオノマーの設計

10.2.3.PFSA膜の押出キャスティングプロセス

10.2.4.PFSA膜溶液キャスティングプロセス

10.2.5.PFSA 溶液キャスティングプロセス用特殊剥離膜

10.2.6.PFSA膜分散キャスティングプロセス

10.2.7.メルトブローPEM製造プロセス - カナダNRC

10.2.8.PFSA膜の改良

10.2.9.膜性能の最適化におけるトレードオフ

10.2.10.同時延伸による寸法および機械的安定性の改善

10.2.11.強化PFAS膜:多層膜と織膜の比較

10.2.12.ケムール社の強化ナフィオン膜

10.2.13.ゴア強化SELECT膜

10.2.14.多層共押出しによるイオン交換膜の補強

10.2.15.補強多層IEMの革新分野

10.2.16.PFSA複合材料

10.2.17.グラフェン複合材料

10.3.イオン交換膜におけるPFASの代替物質

10.3.1.PEM燃料電池および電解槽に影響するPFAS規制

10.3.2.ナフィオンの責任ある製造に注力するケムール社

10.3.3.PFAS膜の代替に必要な主要パラメータ

10.3.4.新たな代替膜

10.3.5.炭化水素膜はPFAS含有膜の主要な競争相手

10.3.6.イオン交換膜の代替ポリマー材料

10.3.7.ホウ素含有炭化水素膜

10.3.8.その他の非PBI含有イオン溶解膜

10.3.9.膜の剛性を向上させるガラス充填架橋PEEK

10.3.10.セルロースをベースとしたバイオベースのPFSA非含有膜

10.3.11.無機および無機-有機ハイブリッドイオン交換膜

10.3.12.無機膜:メンブリオン

10.3.13.有機金属骨格(MOF)-概要

10.3.14.イオン交換膜におけるMOFの応用

10.3.15.MOFベースのイオン交換膜は商業化の準備が整っていない

10.3.16.イオン交換膜におけるPFAS代替物質の商業的成熟度

11.触媒

11.1.1.重要な白金族金属:はじめに

11.1.2.重要な白金族金属:サプライチェーンに関する考察

11.1.3.世界の白金族金属の需要と用途区分

11.1.4.重要な白金族金属:用途とリサイクル率

11.1.5.触媒としての白金

11.1.6.カーボンブラック担体がPt/Cに及ぼす影響

11.1.7.触媒コーティング膜(CCM)

11.1.8.CCM製造技術

11.1.9.CCM製造技術

11.1.10.コーティングプロセスの比較

11.1.11.ロールtoロールCCM製造プロセス(1/2)

11.1.12.ロールtoロールCCM製造プロセス(2/2)

11.1.13.RWTH Aachen & LaufenbergのCCM製造に関する研究

11.1.14.触媒インクの調合-重要な考慮点

11.1.15.典型的な触媒コーティング膜(CCM)

11.1.16.燃料電池における触媒材料の負荷低減目標

11.1.17.触媒のリサイクル

11.1.18.触媒の劣化メカニズム

11.1.19.触媒のトレンドの概要

11.1.20.触媒活性の向上 - 代替金属

11.1.21.触媒活性の向上 - フォームファクター

11.1.22.SonoTek - 超音波蒸着

11.1.23.Mebius - 触媒コア上の白金スキン

11.1.24.触媒被毒の低減

11.1.25.触媒コストの低減

11.1.26.触媒の今後の方向性

11.2.触媒の主要サプライヤー

11.2.1.キャタラーコーポレーション

11.2.2.ユミコア

11.2.3.ジョンソン・マッセイ(ハネウェル)

11.2.4.タナカ、ヘレウス、BASF

11.2.5.新規開発触媒

12.企業プロフィール

12.1.アレイマ燃料電池 BPP & インターコネクトマテリアルズ

12.2.エイムズ・ゴールドスミス・セイミグPEMEL/FC電極触媒

12.3.AvCarb

12.4.バラード・モティブ・ソリューションズ

12.5.バラード・パワー・システムズ

12.6.バラード・パワー・システムズ

12.7.ブランブル・エナジー

12.8.セルモ

12.9.カミンズ/ハイドロジェニックス水素燃料電池

12.10.ダナ(バイポーラプレート)

12.11.EKPO燃料電池テクノロジー

12.12.FJコンポジット

12.13.ヘレウス水素経済用触媒

12.14.Hongfeng Carbon Solutions

12.15. Hydrogenics

12.16.インパクトコーティング

12.17.イオノマー・イノベーションズ

12.18.江蘇燕騰

12.19.ジョンソン・マッセイブルーハイドロジェン・ソリューションズ

12.20.ニットメッシュ・テクノロジーズ電解槽電極&PTL/GDL

12.21.コベルコ(バイポーラプレート)

12.22.プラグパワー

12.23.プラグパワー社

12.24.プレシジョン・マイクロ

12.25.シュンク

SummaryGranular ten-year market forecasts for the material demand for PEM fuel cells used in the transportation industry based on extensive research of OEMs, material suppliers, manufacturers of key components: BPPs, GDLs, ionomer membranes, CCMs Materials demand for proton exchange membrane (PEM) fuel cells is set to grow in line with an expanding fuel cell electric vehicle (FCEV) market, while stationary applications are also promising, as the hydrogen economy continues to gain traction. This report details the key information for components in PEM fuel cells such as bipolar plates (BPP), gas diffusion layers (GDL), catalyst coated membrane (CCM), membrane electrode assemblies (MEA), ionomers, platinum catalysts and more.

Schematic of an exploded proton exchange membrane fuel cell (PEMFC), showing individual fuel cell components and membrane electrode assembly (MEA). Source: IDTechEx

A PEM fuel cell operates via the synergistic interaction of the various components. The BPP distributes fuel throughout the fuel cell, before the GDL transports reactants and products to/from the catalyst layer, respectively. The catalyst is coated on the membrane (CCM), while the membrane itself transports protons from one side of the fuel cell to the other. Collectively, the CCM and GDL are known as an MEA. The materials for PEM fuel cells market is set to grow at a CAGR of 24% between 2026 and 2036, but there are key questions to be answered with respect to the components used in fuel cells. What are the trends seen for incumbent and emerging materials? How will manufacturing methods for these components change to meet increased demand? Who are the main players within the expanding fuel cell components market?

Technology trends for PEM fuel cell components

This report gives a breakdown of the key components within a fuel cell, detailing the incumbent materials and technologies used in each instance. Analysis of supply chains and major players within the industry builds an overview of the market as a whole. However, even for the incumbent materials, there is still scope for variations to the technology based on materials selection. Taking the example of BPPs, typical material choice includes plates made from either metal (e.g. titanium, stainless steel) or graphite. This report provides benchmarking of metal and graphite plates, highlighting the particular vehicle types (passenger cars, vans, trucks and buses alongside ships and trains) for which each material is most well suited.

Despite dominant incumbent materials, such as Nafion for ionomer membranes, disruptive technologies are beginning to emerge, showing signs of early promise, while potential regulations restricting PFAS materials could heavily impact the market. Novel materials, coatings and manufacturing techniques are seen at academic stage, with some early commercial uptake, and analysis of these disruptions to the incumbent are included in this report. A comprehensive analysis of alternative polymer exchange membranes was carried out and these are benchmarked against the incumbent, Nafion, for the most important parameters to ensure optimal performance of the fuel cell.

Economy of scale to reduce cost of components

FCEVs are yet to achieve similar market penetration seen for battery electric vehicles (BEV), and while IDTechEx expects BEVs to dominate the zero-emission vehicles market, the drive towards zero-emission vehicles is expected to see FCEVs capture a growing share of the overall vehicles sector. In particular, FCEVs show promise for the heavy-duty sector, powering trucks, ships and trains that can operate as hub-to-hub connectors for the supply chain, mitigating the need for a diverse hydrogen fuel infrastructure. This increasing market share will see higher material demand for all of the components within PEM fuel cells, and a major outcome of this will be a reduction in cost of components as the economy of scale takes hold.

This report outlines several paths by which the cost of components will reduce, from optimisation of incumbent technology to emerging materials and automated manufacturing systems. For the case of BPP materials, a detailed overview is given of the diverse range of manufacturers and the various materials and manufacturing techniques currently implemented, and those that are proposed, with a discussion of the related price progression per plate as wider-scale uptake of fuel cell powered transportation occurs.

Market drivers: Catalysts for research and development

As governments seek to enact policy to assist the implementation of zero emission vehicles, specifically in urban environments, several government agencies have set targets for manufacturers and material suppliers to work towards, with the overall goal of reducing the cost of fuel cell technology to enable competition with BEVs and traditional internal combustion engine vehicles, while fuel cells will also compete for zero-emission stationary power applications. This report covers the manner in which these targets impact the materials market for fuel cells, such as how US Department of Energy's (DOE) targets for the mass of catalyst in fuel cells is influencing the areas of material R&D.

Other factors driving R&D include the economic value of materials and efficiency of the fuel cell stack. The manner in which emerging materials can replace platinum in the fuel cell and reduce the cost of the catalyst (and CCM) is covered in the report, while the desire to increase the power density of the stack by reducing the form factor of components is most clearly evident in the development of thinner BPPs. The report covers novel coating techniques and manufacturing methods for producing these plates.

Comprehensive analysis and market forecasts

IDTechEx covers the electric vehicle industry comprehensively, detailing BEVs and FCEVs, alongside ships and trains; with the FCEV research segmented by passenger car, light commercial vehicle (van), heavy duty trucks and city buses. Coverage of the stationary fuel cell market covers a range of fuel cell types, including PEMs. Expertise on technical and market developments is built through interviewing major players on the global scale and attending several conferences.

This report offers granular 10-year market forecasts, derived from IDTechEx forecasts in the FCEV industry, for the materials demand for PEMFCs in transportation applications for key fuel cell components (BPP, GDL, CCM, MEA, ionomer, etc) segmented by mode of transport and vehicle type. Forecasts are given for materials demand for components by both units and volume, while detailing the value associated with each of these components.

Key Aspects

This report provides the following information

Technology trends

Value chain analysis

Market Forecasts & Analysis

Table of Contents1. EXECUTIVE SUMMARY AND CONCLUSIONS

1.1. Overview of PEMFCs

1.2. Major components for PEMFCs

1.3. Applications for fuel cells and major players

1.4. BPP: Purpose and form factor

1.5. Materials for BPPs: Graphite vs metal

1.6. BPP manufacturers flow chart

1.7. GDL: Purpose and form factor

1.8. GDL supply chain for FCEV stacks

1.9. Membrane: Purpose and form factor

1.10. Leading modern PFSA membranes - key players & properties

1.11. Ion exchange membrane material benchmarking - PEM fuel cells

1.12. Ongoing concerns with PFAS regulations

1.13. Catalyst: Purpose and form factor

1.14. Trends for fuel cell catalysts

1.15. Key suppliers of catalysts for fuel cells

1.16. Balance of plant for PEM fuel cells

1.17. Overview of market forecasts

1.18. PEM Fuel Cell Market Value (US$ millions) 2026-2036

1.19. Access more with an IDTechEx subscription

2. MARKET FORECASTS

2.1.1. Forecast methodology and assumptions

2.1.2. PEM Fuel Cell Demand by Application (MW) 2023-2036

2.1.3. PEM Fuel Cell Market Value (US$ millions) 2023-2036

2.1.4. Market Forecasts: Bipolar Plates

2.1.5. BPP Demand (millions of units) by Application 2023-2036

2.1.6. BPP Demand (millions of units) by Material 2023-2036

2.1.7. BPP Value (US$ millions) by Material 2023-2036

2.1.8. Market Forecasts: Gas Diffusion Layer

2.1.9. GDL Demand (000s m2) by Application 2023-2036

2.1.10. GDL Value (US$ millions) by Application 2023-2036

2.1.11. GDL Material Demand (metric tonne) 2023-2036

2.2. Market Forecasts: Membrane, Catalyst & CCM

2.2.1. PEM Demand (000s m2) by Application 2023-2036

2.2.2. PEM Value (US$ millions) by Application 2023-2036

2.2.3. Catalyst/PGM Demand (kg) by Application 2023-2036

2.2.4. CCM Value (US$ millions) by Application 2023-2036

3. INTRODUCTION

3.1.1. Introduction to fuel cells

3.1.2. What is a fuel cell?

3.1.3. Overview of PEMFCs

3.1.4. PEMFCs operating principle

3.1.5. Water-gas shift (WGS) & sour shift reactors

3.1.6. PEM electrolyzer vs PEM fuel cell

3.1.7. Major components for PEMFCs

3.1.8. Fuel cell technologies - overview

3.1.9. Comparison of fuel cell technologies

3.1.10. High temperature PEMFC (1)

3.1.11. High temperature PEMFC (2)

3.1.12. What is a Fuel Cell Vehicle?

3.1.13. Attraction of fuel cell vehicles

3.1.14. Mobility applications for fuel cells

3.1.15. PEMFC market players

3.1.16. Chinese PEMFC market players

3.2. Hydrogen Economy

3.2.1. State of the hydrogen market today

3.2.2. Major drivers for hydrogen production & adoption

3.2.3. Key legislation & funding mechanisms driving hydrogen development

3.2.4. European hydrogen market - major developments

3.2.5. European hydrogen market - major setbacks & challenges

3.2.6. US hydrogen market drivers - pre-2025

3.2.7. US hydrogen market challenges - 2024 and 2025

3.2.8. Outlook on the low-carbon hydrogen industry in the US

3.2.9. Outlook on the low-carbon hydrogen industry globally

4. FCEV MARKETS

4.1. What is a Fuel Cell Vehicle?

4.2. Fuel Cell Vehicles as a Part of the Hydrogen Economy

4.3. 30 Years of Fuel Cell Vehicle Prototypes

4.4. System Efficiency Between BEVs and FCEVs

4.5. Fuel Cell Car Models

4.6. Growth, Stagnation, and Fall of Fuel Cell Passenger Cars

4.7. Toyota Mobility Roadmap

4.8. Toyota Mirai 2nd Generation

4.9. Toyota FCEV Goals 2024 and Beyond

4.10. Hyundai Fuel Cell Passenger Car History

4.11. Hyundai NEXO SUV

4.12. Korea Subsidy Incentives from 2021: FCEV push but BEV far ahead

4.13. Honda Discontinue FC-Clarity: Weak Demand

4.14. Honda to Re-enter FCEV Market

4.15. BMW to Produce FCEVs

4.16. Chinese FCEV Cars

4.17. Outlook for Fuel Cell Passenger Cars

4.18. Light Commercial Vehicles Definition

4.19. Fuel Cell LCVs

4.20. IDTechEx's Outlook on Fuel Cell LCVs

4.21. Truck Weight Definitions

4.22. Battery vs Fuel Cell Trucks: Driving Range

4.23. Fuel Cell Manufacturers Collaboration on FC-Trucks

4.24. Fuel Cells Trucks Outlook

4.25. Fuel Cell Buses - New Markets May Boost Low Sales

4.26. Main Advantages / Disadvantages of Fuel Cell Buses

4.27. Outlook for Fuel Cell Buses

4.28. FCEV vs BEV Market Share in 2045

5. FC TRAIN MARKETS

5.1. Overview of Train Types

5.2. Drivers for Zero-emission Rail

5.3. Fuel Cell Train Overview

5.4. Range Advantage for Fuel Cell Trains

5.5. Fuel Cell Technology Benchmarking for Rail

5.6. Rail Fuel Cell Suppliers

5.7. FC Multiple Unit Overview

5.8. FC Locomotives Overview

5.9. Outlook for Fuel Cell & Electric Trains

6. FC SHIP MARKETS

6.1. Marine Fuel Cells Introduction

6.2. Fuel Cells Technologies for Ships

6.3. Fuel Cell Suppliers: Leaders & Challengers

6.4. Fuel Cell Supplier Market Share 2019-2024

6.5. Fuel Cell Deliveries by Vessel Type 2019-2024

6.6. Policy Drivers for Maritime Fuel Cells

6.7. Outlook for Marine PEM Fuel Cells

7. STATIONARY FC MARKETS

7.1.1. Stationary fuel cell applications

7.1.2. Overview of the stationary fuel cell application market

7.1.3. PEMFC industrial case studies

7.1.4. PEMFC commercial case studies

7.1.5. PEMFC utilities generation case studies

7.1.6. PEMFC telecommunications case studies

7.1.7. Outlook of the stationary fuel cell market

7.2. Stationary PEMFC Players

7.2.1. Overview of the stationary PEMFC market

7.2.2. Acquisitions by major players

7.2.3. Ballard Power Systems Overview

7.2.4. Ballard technologies

7.2.5. Ballard Power stationary fuel cell technology

7.2.6. Ballard Power global manufacturing capabilities and key partners

7.2.7. Plug Power overview

7.2.8. Plug Power technology overview

7.2.9. Plug Power stationary power technology and fuelling

7.2.10. Plug Power customers

7.2.11. PowerCell Group overview

7.2.12. PowerCell Group technologies

7.2.13. PowerCell Group partnerships and agreements

7.2.14. Intelligent Energy overview

7.2.15. Intelligent Energy stationary power technology

7.2.16. Intelligent Energy partnerships

7.2.17. Toshiba overview

7.2.18. Toshiba fuel cell technology

7.2.19. Cummins overview

7.2.20. Accelera by Cummins fuel cell technology

7.2.21. SFC Energy overview

7.2.22. SFC Energy PEMFC technology

8. BIPOLAR PLATES

8.1.1. Purpose of bipolar plate

8.1.2. BPP form factor

8.1.3. Effect of BPP form factor

8.1.4. Bipolar plate assembly (BPA)

8.2. Materials for BPPs

8.2.1. Important material parameters to consider for BPPs

8.2.2. Graphite as a BPP material

8.2.3. Metal as a BPP material

8.2.4. Cost progression of BPAs

8.2.5. Coatings are required for metal BPPs

8.2.6. Coating choices for metal BPPs

8.2.7. Manufacturing methods for BPPs

8.2.8. BPP manufacturers flow chart

8.3. BPP manufacturers

8.3.1. Overview of BPP Suppliers (non-exhaustive list)

8.3.2. Case Study (NC Titanium): Kobe Steel

8.3.3. Case Study (Dual Supply): Dana

8.3.4. Case Study (Graphite): SGL Carbon

8.3.5. Case Study (Graphite Composite): FJ Composite

8.3.6. Case Study (System Supplier): Schuler

8.3.7. Case Study (Laser Etch): SITEC

8.3.8. Micro Precision - Chemical Etching

8.3.9. Switzer - Chemical Etching

8.3.10. Yiangteng

8.3.11. Hongfeng - Graphite

8.3.12. Comparison of graphite BPP suppliers

8.3.13. Ranked comparison of graphite BPPs

8.4. BPP coating specialists

8.4.1. Impact Coatings

8.4.2. Precors

8.5. Latest trends and research for BPPs

8.5.1. Future directions for bipolar plate flow fields

8.5.2. Printed Circuit Board BPPs - Bramble Energy

8.5.3. Latest trends for BPPs

8.5.4. Loop Energy

8.5.5. CoBiP project

8.5.6. Collaborative Approaches to BPP

8.5.7. Early-stage commercial developments for BPPs

8.5.8. Recent academic research for BPPs

8.5.9. Woven mesh for fuel cells

8.5.10. NBC Meshtec

8.5.11. Haver & Boecker

8.5.12. Emerging manufacturing methods

8.5.13. Collaborative Approaches to BPP

9. GAS DIFFUSION LAYERS

9.1.1. Porous transport layer (PTL) & gas diffusion layer (GDL) summary

9.1.2. PTL/GDL characteristics & materials

9.1.3. Typical GDL structure

9.1.4. Cathode GDL: Hydrophobic treatment

9.1.5. Wet vs dry GDL performance

9.1.6. GDL manufacturing process

9.1.7. Cellulosic fiber GDL: No MPL required

9.1.8. Interactions between GDL & catalyst layer

9.1.9. GDL innovation trends

9.1.10. Focus on dual hydrophobic and hydrophilic behaviour

9.2. GDL Supply Chain & Players

9.2.1. GDL supply chain for FCEV stacks

9.2.2. GDL player: SGL Carbon

9.2.3. GDL player: Toray

9.2.4. GDL player: Freudenberg

9.2.5. AvCarb - advancements in GDL designs for fuel cells

9.2.6. Key GDL suppliers

10. MEMBRANES

10.1.1. Purpose of the membrane

10.1.2. Form factor of the membrane

10.1.3. Water management in the fuel cell

10.1.4. Proton exchange membranes - brief history, functions & materials

10.1.5. Key parameters defining PFSA ionomer structure & properties

10.1.6. Important material parameters to consider for the membrane

10.1.7. Overview of factors causing PEM membrane degradation

10.1.8. Historical perspective on membrane manufacturers & key properties

10.1.9. Nafion - the market leading membrane

10.1.10. Chemours' Nafion properties & grades

10.1.11. Pros & cons of Nafion & PFSA membranes

10.1.12. Proton exchange membrane market landscape

10.1.13. Leading modern PFSA membranes - key players & properties

10.1.14. Comparison of PFSA membrane properties

10.1.15. Ion exchange membrane material benchmarking - PEM fuel cells

10.1.16. Example supply chain for proton exchange membranes - Gore

10.1.17. High-temperature proton exchange membranes

10.1.18. Innovations in PEMFC membranes may influence PEMEL (1)

10.1.19. Innovations in PEMFC membranes may influence PEMEL (2)

10.1.20. Ongoing concerns with PFAS

10.1.21. Hydrocarbons as PEM fuel cell membranes

10.1.22. Alternative PEM materials: Hydrocarbon IEMs

10.1.23. Assessment of hydrocarbon membranes

10.1.24. Benchmarking of Ionomr membrane against incumbent PFAS membrane

10.1.25. Alternative PEM materials: graphene composites

10.2. Production of PFAS membranes

10.2.1. Fluoropolymers in the polymer pyramid

10.2.2. PFSA ionomer design

10.2.3. PFSA membrane extrusion casting process

10.2.4. PFSA membrane solution casting process

10.2.5. Special release membrane for PFSA solution casting process

10.2.6. PFSA membrane dispersion casting process

10.2.7. Melt-blowing PEM manufacturing process - NRC Canada

10.2.8. Improvements to PFSA membranes

10.2.9. Trade-offs in optimizing membrane performance

10.2.10. Improving dimensional and mechanical stability using simultaneous stretching

10.2.11. Reinforced PFAS membranes: Multilayer vs woven membranes

10.2.12. Chemours reinforced Nafion membranes

10.2.13. Gore reinforced SELECT membranes

10.2.14. Reinforcing ion exchange membranes using multilayer co-extrusion

10.2.15. Innovation areas for reinforced multilayer IEMs

10.2.16. PFSA composite materials

10.2.17. Graphene composites

10.3. Alternatives to PFAS in ion exchange membranes

10.3.1. PFAS Regulations Affecting PEM Fuel Cells & Electrolyzers

10.3.2. Chemours' focus on responsible manufacturing of Nafion

10.3.3. Key Parameters Required to Replace PFAS Membranes

10.3.4. Emerging Alternative Membranes

10.3.5. Hydrocarbon membranes are leading competitors to PFAS-containing membranes

10.3.6. Alternative polymer materials for ion exchange membranes

10.3.7. Boron-containing hydrocarbon membranes

10.3.8. Other non-PBI containing ion solvating membranes

10.3.9. Glass-filled cross-linked PEEK for improved membrane stiffness

10.3.10. Bio-based PFSA-free membranes based on cellulose

10.3.11. Inorganic and inorganic-organic hybrid ion exchange membranes

10.3.12. Inorganic membranes: Membrion

10.3.13. Metal-organic frameworks (MOFs) - overview

10.3.14. MOF applications in ion exchange membranes

10.3.15. MOF-based ion exchange membranes are not ready for commercialization

10.3.16. Commercial maturity of PFAS alternatives in ion exchange membranes

11. CATALYSTS

11.1.1. Critical platinum group metals: Introduction

11.1.2. Critical platinum group metals: Supply chain considerations

11.1.3. Global PGM demand and application segmentation

11.1.4. Critical platinum group metals: Applications and recycling rates

11.1.5. Platinum as a catalyst

11.1.6. Influence of carbon black support on Pt/C

11.1.7. Catalyst coated membrane (CCM)

11.1.8. CCM production technologies

11.1.9. CCM production technologies

11.1.10. Comparison of coating processes

11.1.11. Roll-to-roll CCM production processes (1/2)

11.1.12. Roll-to-roll CCM production processes (2/2)

11.1.13. RWTH Aachen & Laufenberg's research into CCM production

11.1.14. Catalyst ink formulation - key considerations

11.1.15. Typical catalyst coated membrane (CCM)

11.1.16. Targets for reducing loading of catalytic materials in fuel cells

11.1.17. Recycling of the catalyst

11.1.18. Catalyst degradation mechanisms

11.1.19. Overview of trends for catalysts

11.1.20. Increasing catalytic activity - alternative metals

11.1.21. Increasing catalytic activity - form factor

11.1.22. SonoTek - Ultrasonic Deposition

11.1.23. Mebius - Pt Skin over Catalyst Core

11.1.24. Reduction of catalyst poisoning

11.1.25. Reduction of cost of catalyst

11.1.26. Future directions for catalysts

11.2. Key Suppliers of Catalysts

11.2.1. Cataler Corporation

11.2.2. Umicore

11.2.3. Johnson Matthey (Honeywell)

11.2.4. Tanaka, Heraeus and BASF

11.2.5. Newly developed catalysts

12. COMPANY PROFILES

12.1. Alleima: Fuel Cell BPP & Interconnect Materials

12.2. Ames Goldsmith Ceimig: PEMEL/FC Electrocatalysts

12.3. AvCarb

12.4. Ballard Motive Solutions

12.5. Ballard Power Systems

12.6. Ballard Power Systems

12.7. Bramble Energy

12.8. CellMo

12.9. Cummins/Hydrogenics: Hydrogen Fuel Cells

12.10. Dana (Bipolar Plates)

12.11. EKPO Fuel Cell Technologies

12.12. FJ Composite

12.13. Heraeus: Catalysts for the Hydrogen Economy

12.14. Hongfeng Carbon Solutions

12.15. Hydrogenics

12.16. Impact Coatings

12.17. Ionomr Innovations

12.18. Jiangsu Yiangteng

12.19. Johnson Matthey: Blue Hydrogen Solutions

12.20. KnitMesh Technologies: Electrolyzer Electrodes & PTL/GDLs

12.21. Kobelco (Bipolar Plates)

12.22. Plug Power

12.23. Plug Power Inc

12.24. Precision Micro

12.25. Schunk

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|