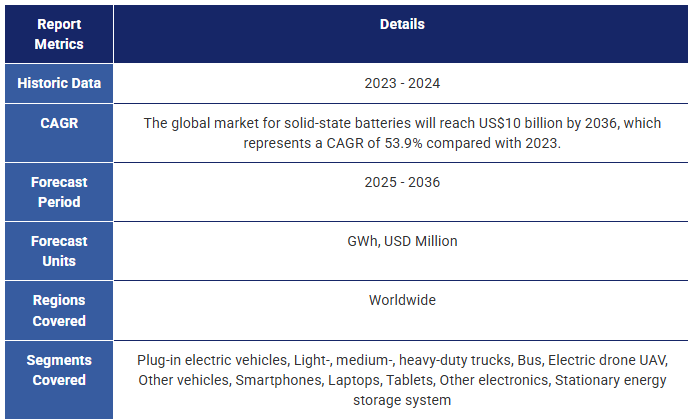

全固体電池 2026-2036年:技術、予測、プレーヤーSolid-State Batteries 2026-2036: Technology, Forecasts, Players 全固体&半固体ハイブリッドセル、硫化物/酸化物/ポリマー電解質、リチウムメタル、高Si&無負極アノード、EV統合、製造スケールアップ、コストロードマップ、性能、サプライチェーン、プレーヤー&パート... もっと見る

サマリー

全固体&半固体ハイブリッドセル、硫化物/酸化物/ポリマー電解質、リチウムメタル、高Si&無負極アノード、EV統合、製造スケールアップ、コストロードマップ、性能、サプライチェーン、プレーヤー&パートナーシップ

全固体電池(SSB)業界は、先進技術とアプリケーション全般にわたる需要の高まりに牽引され、変貌を遂げつつある。安全性とエネルギー密度に画期的な進歩をもたらす SSB は、2036 年までに 100 億米ドル市場に達する可能性がある。IDTechExの2026-2036年レポートは、このダイナミックな業界を包括的に分析し、最先端技術、市場動向、製造上の課題、固体電池を取り巻く世界的なエコシステムの相互関係を探っています。

全固体電池:技術的飛躍

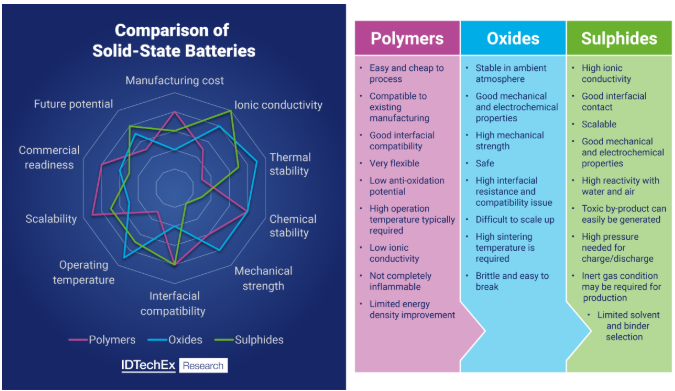

全固体電池は、液体電解質を固体材料に置き換え、熱暴走のリスクを低減することで安全性を高め、リチウム金属またはシリコンの負極によってエネルギー密度を高めます。この転換により、より軽量でコンパクトな設計が可能になる。硫化物は高いイオン伝導性を持つが、毒性と製造上の課題がある。ポリマーはスケーラブルだが、より高い温度を必要とし、安定性に問題がある。各技術は、性能、コスト、拡張性においてトレードオフの関係にあり、報告書ではそれぞれの長所と限界について詳述している。

固体電池の比較。出典:IDTechExIDTechEx

市場ダイナミクス:

EVの急成長が電池技術革新の主な原動力となっている。1991年の商業化以来、リチウムイオン電池が市場を支配してきたが、可燃性のリスク、資源の制約、環境への懸念など、その限界が、固体電池のような代替品への関心を高めている。

固体電池採用の主な推進要因:

全固体電池はリチウムイオン技術に取って代わる可能性があると見なされることが多いが、商業化への準備については議論が続いている。現在の高コストと製造上の課題から、過大評価されているとの見方もある。また、既存の電池技術における重大な限界を克服するカギを握っているという見方もある。

グローバル・エコシステムと地域動向

全固体電池の開発は、研究機関、材料サプライヤー、電池メーカー、自動車OEM、投資家が関与するグローバルな共同作業であり、地域的な力学が業界を大きく形成している。日本、韓国、中国に代表される東アジアは、電池の技術革新と生産能力において引き続き優位を占めており、北米と欧州は東アジアへの依存度を下げるために現地生産に多額の投資を行っている。一方、新興市場は材料やシステムに対する革新的なアプローチを提供し、サプライチェーンをさらに再編成している。このシフトは、コスト効率を維持しながら新素材やコンポーネントを統合できる、適応力のある製造プロセスの必要性を浮き彫りにしており、業界の進化を促進する広範なトレンドを反映している。

課題と機会

SSBは、従来のリチウムイオン・バッテリーに比べて安全性が向上し、エネルギー密度が高く、設計が簡素化されているため、エネルギー貯蔵における革新的な進歩である。可燃性の液体電解質を固体材料に置き換えることで、SSBは火災リスクを大幅に低減し、高温での安全な運用を可能にする。リチウム金属アノードを使用することでエネルギー密度が向上し、EVの航続距離の延長とコンパクトな設計が可能になる。SSBはまた、充電の高速化と長寿命化を約束し、EVや再生可能エネルギー貯蔵システムに理想的である。

しかし、広く商業化するには大きなハードルがある。製造工程が複雑で、まだ拡張性がないため、コストが高くなっている。高品質で製造が容易な部品を開発し、シームレスな統合を実現するには精密工学が必要である。リチウムのデンドライト形成などの安全性の課題はショートを引き起こす可能性があり、低温での性能限界や急速充電下でのサイクル寿命の低下にはさらなる改善が必要である。さらに、使用されている材料が特殊であるため、リサイクルや使用済み製品の管理も未解決のままである。

こうした課題にもかかわらず、パイロット生産ラインやギガファクトリーで進行中の進歩は、コスト削減と性能向上のための研究とともに、SSBを持続可能なエネルギー貯蔵と輸送のための重要な技術として位置づけている。

最近の重点分野

電池技術における実験室規模の開発から商業規模の生産への移行は、個々のセル開発からシステムレベルの統合へと焦点を移している。これには、個々のセルの性能を最適化するだけでなく、バッテリーパックやシステムにシームレスに組み込むことも含まれる。バッテリー管理システム(BMS)の設計や機能、機械的な最適化を保証する構造設計など、システムレベルでの考慮は、現在、全体的な安全性、効率性、信頼性を高めるために不可欠です。システムレベルの最適化を優先することで、メーカーは電気自動車やグリッド・ストレージのような大規模アプリケーションの複雑な要求を満たすソリューションを提供することを目指しています。

もうひとつの重点分野は、生産拡大に伴うコスト削減と拡張性の課題への対応である。製造工程を合理化し、コストを削減しながら性能を維持するスケーラブルな設計を開発する努力がなされている。

さらに、電池の寿命と安全性に直接影響するセル圧管理などの要素にも注目が集まっている。これらの進歩は、先進的なバッテリー技術の普及を可能にしながら、技術的・経済的障壁を克服するという業界のコミットメントを反映している。

IDTechExの包括的な洞察

IDTechExのレポートは2026年から2036年までの固体電池市場を詳細に分析しています。

主な特徴は以下の通り

固体電池を取り巻く「誇大広告」と、それらが直面する現実的な課題の両方を取り上げることで、本レポートはその潜在的な影響についてバランスの取れた視点を提供しています。

主な内容

固体電池入門

電解質イノベーション

性能の特徴

市場予測&分析

地域別の動きと動向

最近の注目分野

企業プロファイル

目次1.要旨

1.1.固体電解質の分類

1.2.液体電池と固体電池

1.3.薄膜電池とバルク固体電池

1.4.SSB企業の商業計画

1.5.自動車OEMによる固体電池の共同開発/投資

1.6.SSBの自動車搭載に関する自動車メーカーのスケジュール計画

1.7.SSBに関する自動車メーカーの計画と進捗状況

1.8.既存のEVモデルと今後のEVモデル

1.9.技術の現状と今後の動向

1.10.サプライチェーンの現状と今後の動向

1.11.市場・事業の現状と今後の動向

1.12.製造/製品の状況と今後の動向

1.13.資源への配慮

1.14.固体電池に対する否定的意見

1.15.固体電池のさまざまな特徴の分析

1.16.固体電池の開発段階

1.17.固体電池開発における主な課題と不確実性

1.18.固体電池セルの改良戦略

1.19.主要固体電池企業の所在地

1.20.固体電解質技術の概要

1.21.固体電解質システムの比較 1

1.22.固体電解質システムの比較 2

1.23.現在の電解質の課題と可能な解決策

1.24.各社の技術概要

1.25.固体電池のバリューチェーン

1.26.アプリケーション分析

1.27.市場予測方法

1.28.固体電池の市場予測の前提条件と分析

1.29.様々な用途における固体電池の価格予測

1.30.ソリッドステート電池のアドレス可能な市場規模

1.31.固体電池の用途別予測 2025-2035年 (GWh)

1.32.固体電池の用途別2025~2035年予測(市場価値)

1.33.固体電池の技術別2025~2035年予測(GWh)

1.34.固体電池の2025~2035年予測:技術別(GWh)

1.35.2024年と2030年の市場規模区分

1.36.自動車プラグイン用固体電池の予測 2023-2035年

2.固体電池入門

2.1.固体電池とは何か?

2.2.固体電池とは?

2.3.確かな未来?

2.4.固体電池の歴史

2.5.固体電池開発のマイルストーン

2.6.多機能固体電解質への要求

2.7.固体電池セルの構成

2.8.一般的な固体電池セルの選択

2.9.リチウム金属負極

2.10.リチウムはどこにある?

2.11.リチウムの製造方法

2.12.水酸化リチウムと炭酸リチウム

2.13.リチウム金属製造の高コスト

2.14.電気化学的不可逆性への挑戦

2.15.電気分解による従来のリチウム金属製造

2.16.リチウム金属電池のアプローチ

2.17.金属リチウム負極の失敗談

2.18.リチウム金属への挑戦

2.19.デンドライト形成:電流密度

2.20.デンドライト形成:圧力と温度

2.21.負極を使用しないリチウム金属電池のサイクル特性

2.22.リチウム金属負極を持つ固体電池

2.23.固体電池中のリチウム

2.24.リチウム金属箔

2.25.リチウム金属に関する考察

2.26.リチウム金属の減速要因

2.27.シリコン負極

2.28.シリコン負極の紹介

2.29.シリコン負極の価値提案

2.30.グラファイトとシリコンの比較

2.31.シリコン導入の解決策

2.32.固体電解質用シリコン負極

2.33.サイクル特性向上のための初期高圧コンディショニングの重要性

2.34.シリコン負極と固体電池

3.固体電解質

3.1.固体電解液のランドスケープ

3.2.固体電解質

3.3.固体高分子電解質

3.4.LiPo電池、ポリマー系電池、ポリマー電池

3.5.ポリマー電解質の種類

3.6.電解ポリマーの選択肢

3.7.ポリマー電解質の利点と問題点

3.8.固体高分子電解質のPEO

3.9.ポリマー固体電池に取り組む企業

3.10.固体酸化物無機電解質

3.11.酸化物電解質

3.12.ガーネット

3.13.LLZOベースのSSBの推定コスト予測

3.14.酸化物固体電解質の代表的な厚さ範囲

3.15.NASICONタイプ

3.16.ペロブスカイト型

3.17.LiPON

3.18.LiPON:構造

3.19.リポンをベースとする電池に取り組んできた、また取り組んでいるプレーヤー

3.20.LiPON系電池の正極材料の選択肢

3.21.LiPON系電池の負極

3.22.LiPON系電池の基板オプション

3.23.各社の薄膜電池の材料とプロセスの動向

3.24.LiPON:容量増加

3.25.無機酸化物固体電解質の比較

3.26.リチウム金属を含む酸化物電解質の熱安定性

3.27.酸化物固体電池に取り組む企業

3.28.硫化物系無機固体電解質

3.29.LISICONタイプ1

3.30.リシコンタイプ2

3.31.アルジロダイト

3.32.硫化物電解質のコスト構造

3.33.硫化物固体電池に取り組む企業

3.34.その他の電解質

3.35.リチウム水素化物

3.36.リチウムハライド

3.37.複合電解質

3.38.両方の長所?

3.39.理想的な複合固体電解質へのアプローチ

3.40.一般的なハイブリッド電解質コンセプト

3.41.電解質の分析と比較

3.42.技術評価

3.43.技術評価(続き)

3.44.リチウムイオン用固体無機電解質の種類

3.45.無機電解質の利点と課題 1

3.46.無機電解質の利点と課題 2

3.47.無機電解質の利点と課題 3

4.固体電池の特徴

4.1.固体電池の価値提案

4.2.安全性

4.3.安全性への配慮

4.4.液体電解質リチウムイオン電池の安全性

4.5.現代のホラー映画は、携帯電話の電池切れに恐怖を見出している

4.6.サムスンのファイヤーゲート

4.7.リチウムイオン電池の温度と予想される結果

4.8.リチウムイオン電池の安全性

4.9.固体電池はより安全か?

4.10.固体電池の安全性の結論

4.11.エネルギー密度

4.12.SSBはエネルギー密度にどのように役立つのか

4.13.エネルギー密度の向上

4.14.固体電池が必ずしもエネルギー密度の向上につながるとは限らない

4.15.異なる電解質の比エネルギー比較

4.16.高エネルギー密度には代替負極が必要

4.17.固体電池のエネルギー密度の結論

4.18.急速充電

4.19.各段階での急速充電

4.20.従来のリチウムイオン電池における急速充電の難しさ

4.21.急速充電における電池特性の重要性

4.22.固体電池の急速充電

5.固体電池に関する関心と活動

5.1.エネルギー貯蔵の進化

5.2.米国での活動

5.3.政策と規制

5.4.米国での活動とイニシアティブ

5.5.USABC

5.6.固体電池に関するIRAのメリット

5.7.韓国での活動

5.8.韓国における主な活動と政策

5.9.電池ベンダーの取り組み - サムスンSDI

5.10.サムスンの商業的取り組み

5.11.LGの貢献

5.12.日本での取り組み

5.13.日本における主な活動と進展

5.14.中国での活動

5.15.政策支援

5.16.中国における関心

5.17.中国企業25社の進展

5.18.中国の自動車メーカー11社の固体電池に関する活動

5.19.その他の地域での活動

5.20.地域での取り組み英国

5.21.各地域での取り組みドイツ

5.22.地域的な取り組みフランス

5.23.地域的な取り組みオーストラリア

5.24.自動車メーカーへの取り組み

5.25.自動車メーカーの取り組み - BMW

5.26.BMWの固体電池研究

5.27.ラボからプロトタイプへのBMWのスケーリングコンピタンス

5.28.メルセデス・ベンツの自社セル開発

5.29.自動車メーカーの取り組み - フォルクスワーゲン

5.30.フォルクスワーゲンの電気自動車用バッテリーへの投資

5.31.自動車メーカーの取り組み - 現代自動車

5.32.現代自動車の固体電池技術の特徴

5.33.エノベイト・モーターズ

5.34.その他の自動車メーカー

6.固体電池の最新動向

6.1.固体電池の代表的な宣伝文句

6.2.固体電池の要件

6.3.2025年の固体電池開発の焦点

6.4.固体電池の温度性能

6.5.固体電池の圧力効果

6.6.圧力はエネルギー密度を低下させる

6.7.固体電池開発におけるAIの統合

6.8.固体電池のデンドライト成長防止

6.9.デンドライト防止

7.固体電池のセル設計からシステム設計まで

7.1.固体電池のセル設計

7.2.市販電池のフォームファクター 1

7.3.市販電池のフォームファクター 2

7.4.電池の構成 1

7.5.電池構成 2

7.6.セルのスタッキングオプション

7.7.バイポーラセル

7.8.プロロジウムのバイポーラ設計

7.9.「無負極電池

7.10.無負極電池の課題

7.11.密着スタッキング

7.12.固体電池が提供する柔軟性とカスタマイズ

7.13.セルサイズのトレンド

7.14.セル設計のアイデア

7.15.セルからパックへ

7.16.パック・パラメーターはセル以上の意味を持つ

7.17.パックシステムの重要性

7.18.CTP設計の影響

7.19.BYDのブレードバッテリー概要

7.20.BYD のブレード電池:構造と構成

7.21.BYD のブレード電池設計

7.22.BYD ブレード電池パックレイアウト

7.23.BYD のブレード電池エネルギー密度の向上

7.24.BYD のブレード電池熱安全性

7.25.BYD のブレード電池:構造安全性

7.26.コストと性能

7.27.BYD のブレード電池CTPが示すもの

7.28.CATLのCTP設計

7.29.CATLのCTP電池の進化

7.30.CATLの麒麟電池

7.31.従来型リチウムイオンのセルからパックへ

7.32.固体電池:セルからパックへ

7.33.バイポーラ対応CTP

7.34.従来設計とバイポーラセル設計

7.35.EVバッテリーパックの組み立て

7.36.プロロジウム「MAB」EVバッテリーパック組立

7.37.組立稼働率を高めるMABのアイデア

7.38.固体電池:パックレベルでの競争

7.39.電池・自動車メーカー間のビジネスモデル

7.40.固体電池のバッテリー管理システム

7.41.バッテリー管理システムの重要性

7.42.BMSの機能

7.43.BMSサブシステム

7.44.セル制御

7.45.冷却技術の比較

7.46.異なる形状のBMS設計

7.47.麒麟電池の熱管理システム

7.48.セルの熱伝導率

7.49.セルの接続

7.50.パックレベルへの圧力の影響

7.51.高圧がバッテリーパックのエネルギー密度に与える影響

7.52.SSB 用 BMS 設計の考慮点

8.固体電池の製造

8.1.大量生産のタイムライン

8.2.技術準備レベルの規模

8.3.従来のリチウムイオン電池セル製造プロセス

8.4.硫化物系セルの製造コスト

8.5.酸化物系セルの製造コスト

8.6.現在のプロセス:ラミネーション

8.7.従来のリチウムイオン電池の製造条件

8.8.従来のリチウムイオン電池とSSBの一般的な製造上の違い

8.9.固体電解質製造のプロセスチェーン

8.10.負極製造プロセスチェーン

8.11.正極製造のプロセスチェーン

8.12.セル組立のプロセスチェーン

8.13.例示的な製造工程

8.14.固体電池部品製造の可能な加工ルート

8.15.大量生産は可能か?

8.16.パウチセル

8.17.アルミラミネートシートの製造技術

8.18.パウチ電池1の包装手順

8.19.パウチセル2の包装手順

8.20.酸化物電解質の厚さと処理温度

8.21.固体電池の製造工程

8.22.固体電池の製造装置

8.23.リチウム金属ポリマー電池の工業規模製造

8.24.薄膜電解質は実現可能か?

8.25.薄膜電池の主な製造技術のまとめ

8.26.リチウム酸化物薄膜の湿式・真空成膜法

8.27.リチウム酸化物薄膜材料の大量製造のための現在の処理方法と課題

8.28.薄膜電池用PVDプロセス 1

8.29.薄膜電池用PVDプロセス 2

8.30.薄膜電池用PVDプロセス 3

8.31.イリカのPVDアプローチ

8.32.製造への道

8.33.トヨタのアプローチ1

8.34.トヨタのアプローチ 2

8.35.日立造船のアプローチ

8.36.Sakti3のPVDアプローチ

8.37.プラナーエナジーのアプローチ

8.38.全固体電池の代表的な製造方法(SMDタイプ)

8.39.プロロジウムのLCB製造工程

8.40.プロロジウムの製造工程

8.41.ソリッドパワー正極と電解質の製造

8.42.ソリッドパワーのセル製造

8.43.ソリッドパワーのパイロット生産施設

8.44.青島の製造プロセス

8.45.宜春1GWh施設の設備と容量

8.46.乾式電極製造の紹介

8.47.乾式と従来の製造の比較

8.48.乾電池電極の製造

8.49.乾式電極バインダー

8.50.湿式スラリーと乾式電極プロセスの比較

9.リサイクル

9.1.リチウムイオン電池のリサイクルに関する世界の政策概要

9.2.リサイクルのための電池形状

9.3.パックの標準化の欠如

9.4.LIBリサイクルアプローチの概要

9.5.リサイクルカテゴリー

9.6.SSBのリサイクル 1

9.7.SSB のリサイクル 2

9.8.SEクラスの概要とリサイクル可能性の評価

9.9.プロロジム1のリサイクル計画

9.10.プロロジウム2のリサイクル計画

9.11.ブルー・ソリューションズによる革新的なリチウム金属リサイクル

9.12.ブルー・ソリューションズが提案するリサイクル

9.13.リチウムメタルリサイクル

10.自動車用途の規格/政策/規制

10.1.標準化と法的枠組み

10.2.グローバルな標準化と規制

10.3.国際機関

10.4.関連する国内組織

10.5.国連 38.3

10.6.IEC - 61960

10.7.IEC 61960 - 3 & 4

10.8.SAE J2464

10.9.UL 1642

10.10.UL 1642 - 追加情報:試験範囲

10.11.EUCAR と危険レベル

10.12.共通安全検証

11.会社概要

11.1.24M Technologies, Inc.

11.2.アンプセラ

11.3.北京WeLion新能源科技

11.4.ブルーカレント

11.5.ブルー・ソリューションズボロレ・バッテリー開発企業の最新事情

11.6.ブライトボルト社

11.7.CALB

11.8.CEA-Leti社

11.9.中国科学アカデミー

11.10.コンテンポラリー・アンペレックス・テクノロジー Co.リミテッド(CATL)

11.11.コスライト・インターナショナル・グループ

11.12.シンベット・コーポレーション

11.13.Ensurge Micropower ASA

11.14.エクセラトロン・ソリッド・ステート LLC

11.15.ファクトリアルエナジー

11.16.FDK株式会社

11.17.フィスカー

11.18.フラウンホーファー

11.19.フロントエッジ・テクノロジー

11.20.甘峰リチウム

11.21.ハイドロ・ケベック

11.22.ハイツァー・エナジー

11.23.イリカ

11.24.インフィニット・パワー・ソリューションズ

11.25.イオン貯蔵システム

11.26.イオンマテリアル

11.27.Jiawei Renewable Energy

11.28.ジョンソン・エナジー・ストレージ

11.29.カナデビアコーポレーション

11.30.ナトリオン

11.31.大原鉄工所

11.32.ポリプラス・バッテリー・カンパニー

11.33.プリエト・バッテリー

11.34.プライムプラネットエナジー&ソリューションズ

11.35.プロロジウム・テクノロジー

11.36.青島エネルギー開発

11.37.クォンタムスケープ

11.38.リマック・テクノロジー

11.39.ショットAG

11.40.シーオ社

11.41.SES AI

11.42.ソリッドパワー

11.43.ソリソール

11.44.ソルベイ

11.45.STマイクロエレクトロニクス

11.46.太陽誘電

11.47.TDK

11.48.東芝

11.49.トヨタ自動車

Summary

All-solid-state & semi-solid hybrid cells; sulfide/oxide/polymer electrolytes; li-metal, high-Si & anode-free anodes; EV integration; manufacturing scale-up, cost roadmaps, performance, supply chain, players & partnerships

The solid-state battery (SSB) industry is transforming, driven by advanced technologies and rising demand across applications. Offering breakthroughs in safety and energy density, SSBs could reach a US$10 billion market by 2036. The IDTechEx report for 2026-2036 provides a comprehensive analysis of this dynamic industry, exploring the interplay between cutting-edge technologies, market trends, manufacturing challenges, and the global ecosystem surrounding solid-state batteries.

Solid-State Batteries: A Technological Leap

SSBs replace liquid electrolytes with solid materials, enhancing safety by reducing thermal runaway risks and increasing energy density through lithium metal or silicon anodes. This shift enables lighter, more compact designs. SSB development focuses on three electrolyte types: sulfides offer high ionic conductivity but face toxicity and manufacturing challenges; polymers are scalable but require higher temperatures and have stability issues; and oxides provide excellent stability for lithium metal anodes but suffer from high interface resistance and costs. Each technology involves trade-offs in performance, cost, and scalability, with the report detailing their strengths and limitations.

Comparison of solid-state batteries. Source: IDTechEx

Market Dynamics: Pushing Boundaries

The rapid growth of EVs has been a key driver of battery innovation. While lithium-ion batteries have dominated the market since their commercialization in 1991, their limitations -- such as flammability risks, resource constraints, and environmental concerns -- have spurred interest in alternatives like solid-state batteries.

Key Drivers of Solid-State Battery Adoption:

While solid-state batteries are often viewed as a potential replacement for lithium-ion technology, debates persist about their readiness for commercialization. Some see them as overhyped due to their current high costs and manufacturing challenges. Others believe they hold the key to overcoming critical limitations in existing battery technologies.

Global Ecosystem and Regional Trends

The development of solid-state batteries is a collaborative global effort involving research institutes, material suppliers, battery manufacturers, automotive OEMs, and investors, with regional dynamics significantly shaping the industry. East Asia, led by Japan, South Korea, and China, continues to dominate in battery innovation and production capacity, while North America and Europe are heavily investing in localized manufacturing to reduce dependence on East Asia. Meanwhile, emerging markets are contributing innovative approaches to materials and systems, further reshuffling the supply chain. This shift highlights the need for adaptable manufacturing processes that can integrate new materials and components while maintaining cost efficiency, reflecting broader trends driving the industry's evolution.

Challenges & Opportunities

SSBs represent a transformative advancement in energy storage, offering improved safety, higher energy density, and simplified designs compared to traditional lithium-ion batteries. By replacing flammable liquid electrolytes with solid materials, SSBs significantly reduce fire risks and enable safer operation at higher temperatures. Their use of lithium-metal anodes allows for greater energy density, enabling longer EV ranges and more compact designs. SSBs also promise faster charging and longer lifespans, making them ideal for EVs and renewable energy storage systems.

However, widespread commercialization faces significant hurdles. Manufacturing processes are complex and not yet scalable, leading to high costs. Precision engineering is required to develop high-quality, easily manufactured components and ensure seamless integration. Safety challenges, such as lithium dendrite formation, can cause short circuits, while performance limitations at low temperatures and reduced cycle life under fast charging require further improvement. Additionally, recycling and end-of-life management remain unresolved due to the unique materials used.

Despite these challenges, ongoing progress in pilot production lines and gigafactories, alongside research to reduce costs and enhance performance, positions SSBs as a key technology for sustainable energy storage and transportation.

Recent Focus Areas

The transition from laboratory-scale development to commercial-scale production in battery technology has shifted the focus from individual cell development to system-level integration. This includes optimizing not just the performance of individual cells but also ensuring their seamless incorporation into battery packs and systems. System-level considerations, such as the design and functionality of Battery Management Systems (BMS), structure design to ensure mechanical optimization, are now critical to enhancing overall safety, efficiency, and reliability. By prioritizing system-level optimization, manufacturers aim to deliver solutions that meet the complex demands of large-scale applications like electric vehicles and grid storage.

Another key focus area is addressing the challenges of cost reduction and scalability as production expands. Efforts are being made to streamline manufacturing processes and develop scalable designs that maintain performance while reducing costs.

Additionally, factors such as cell pressure management, which directly impacts battery longevity and safety, are receiving increased attention. These advancements reflect the industry's commitment to overcoming technical and economic barriers while enabling the widespread adoption of advanced battery technologies.

Comprehensive Insights from IDTechEx

The IDTechEx report provides an in-depth analysis of the solid-state battery market from 2026 to 2036. Key features include:

By addressing both the "hype" surrounding solid-state batteries and the practical challenges they face, this report offers a balanced perspective on their potential impact.

Key Aspects

Introduction to Solid-State Batteries

Electrolyte Innovations

Performance Features

Market Forecasts & Analysis:

Regional Activities and Trends

Recent Focus Areas

Company Profiles

Table of Contents1. EXECUTIVE SUMMARY

1.1. Classifications of solid-state electrolytes

1.2. Liquid vs solid-state batteries

1.3. Thin film vs bulk solid-state batteries

1.4. SSB company commercial plans

1.5. Solid state battery collaborations /investment by automotive OEMs

1.6. Automakers' timeline plans for installing SSB in vehicles

1.7. Automotive maker plans and progress on SSBs

1.8. Existing and upcoming EV models

1.9. Technological status and future trends

1.10. Supply chain status and future trends

1.11. Market / business status and future trends

1.12. Manufacturing / product status and future trends

1.13. Resources considerations

1.14. Negative opinions on solid-state batteries

1.15. Analysis of different features of SSBs

1.16. Solid-state battery development stage

1.17. Key challenges and uncertainties in solid-state battery development

1.18. Solid-state battery cell improvement strategies

1.19. Location overview of major solid-state battery companies

1.20. Summary of solid-state electrolyte technology

1.21. Comparison of solid-state electrolyte systems 1

1.22. Comparison of solid-state electrolyte systems 2

1.23. Current electrolyte challenges and possible solution

1.24. Technology summary of various companies

1.25. Solid-state battery value chain

1.26. Application analysis

1.27. Market forecast methodology

1.28. Assumptions and analysis of market forecast of SSB

1.29. Price forecast of solid-state battery for various applications

1.30. Solid-state battery addressable market size

1.31. Solid-state battery forecast 2025-2035 by application (GWh)

1.32. Solid-state battery forecast 2025-2035 by application (market value)

1.33. Solid-state battery forecast 2025-2035 by technology (GWh)

1.34. Solid-state battery forecast 2025-2035 by technology (GWh)

1.35. Market size segmentation in 2024 and 2030

1.36. Solid-state battery forecast 2023-2035 for car plug in

2. INTRODUCTION TO SOLID-STATE BATTERIES

2.1. What is a Solid-State Battery?

2.2. What is a solid-state battery?

2.3. A solid future?

2.4. History of solid-state batteries

2.5. Milestone of solid-state battery development

2.6. Requirements for solid-state electrolyte with multifunctions

2.7. Solid-State Cell Composition

2.8. Popular solid-state battery cell choices

2.9. Lithium metal anodes

2.10. Where is lithium?

2.11. How to produce lithium

2.12. Lithium hydroxide vs lithium carbonate

2.13. High cost of lithium metal production

2.14. Challenge of electrochemical irreversibility

2.15. Conventional lithium metal production via electrolysis

2.16. Lithium-metal battery approaches

2.17. Failure story about metallic lithium anode

2.18. Lithium metal challenge

2.19. Dendrite formation: Current density

2.20. Dendrite formation: Pressure and temperature

2.21. Cycling preference for anode-free lithium metal cells

2.22. Solid-state battery with lithium metal anode

2.23. Lithium in solid-state batteries

2.24. Lithium metal foils

2.25. Lithium metal considerations

2.26. Lithium-metal slowing down factors

2.27. Silicon anode

2.28. Introduction to silicon anode

2.29. Value proposition of silicon anodes

2.30. Comparison between graphite and silicon

2.31. Solutions for silicon incorporation

2.32. Silicon anode for solid-state electrolyte

2.33. Importance of initial high-pressure conditioning for enhanced cyclability

2.34. Silicon anodes and solid-state batteries

3. SOLID-STATE ELECTROLYTE

3.1. Solid-state electrolyte landscape

3.2. Solid-state electrolytes

3.3. Solid Polymer Electrolyte

3.4. LiPo batteries, polymer-based batteries, polymeric batteries

3.5. Types of polymer electrolytes

3.6. Electrolytic polymer options

3.7. Advantages and issues of polymer electrolytes

3.8. PEO for solid polymer electrolyte

3.9. Companies working on polymer solid state batteries

3.10. Solid Oxide Inorganic Electrolytes

3.11. Oxide electrolyte

3.12. Garnet

3.13. Estimated cost projection for LLZO-based SSB

3.14. Typical thickness ranges of oxide solid-state electrolytes

3.15. NASICON-type

3.16. Perovskite

3.17. LiPON

3.18. LiPON: Construction

3.19. Players that have worked and are working on LIPON-based batteries

3.20. Cathode material options for LiPON-based batteries

3.21. Anodes for LiPON-based batteries

3.22. Substrate options for LiPON-based batteries

3.23. Trend of materials and processes of thin-film battery in different companies

3.24. LiPON: Capacity increase

3.25. Comparison of inorganic oxide solid-state electrolyte

3.26. Thermal stability of oxide electrolyte with lithium metal

3.27. Companies working on oxide solid state batteries

3.28. Solid Sulfide Inorganic Electrolytes

3.29. LISICON-type 1

3.30. LISICON-type 2

3.31. Argyrodite

3.32. Sulfide electrolyte cost structure

3.33. Companies working on sulphide solid state batteries

3.34. Other Electrolytes

3.35. Li-hydrides

3.36. Li-halides

3.37. Composite Electrolytes

3.38. The best of both worlds?

3.39. Approaches to an ideal composite solid-state electrolyte

3.40. Common hybrid electrolyte concept

3.41. Electrolyte analysis and comparison

3.42. Technology evaluation

3.43. Technology evaluation (continued)

3.44. Types of solid inorganic electrolytes for Li-ion

3.45. Advantages and issues with inorganic electrolytes 1

3.46. Advantages and issues with inorganic electrolytes 2

3.47. Advantages and issues with inorganic electrolytes 3

4. SOLID-STATE BATTERY FEATURES

4.1. Value propositions of solid-state batteries

4.2. Safety

4.3. Safety consideration

4.4. Safety of liquid-electrolyte lithium-ion batteries

4.5. Modern horror films are finding their scares in dead phone batteries

4.6. Samsung's Firegate

4.7. LIB cell temperature and likely outcome

4.8. Safety aspects of Li-ion batteries

4.9. Are solid-state battery safer?

4.10. Conclusions of SSB safety

4.11. Energy Density

4.12. How do SSBs help with energy density

4.13. Energy density improvement

4.14. Solid state battery does not always lead to higher energy density

4.15. Specific energy comparison of different electrolytes

4.16. Alternative anode is required for high energy density

4.17. Conclusions of solid-state battery energy density

4.18. Fast Charging

4.19. Fast charging at each stage

4.20. Difficulties of fast charging in conventional Li-ion batteries

4.21. The importance of battery feature for fast charging

4.22. Fast charging for solid-state batteries

5. INTERESTS AND ACTIVITIES ON SOLID-STATE BATTERIES

5.1. Energy storage evolvement

5.2. Activities in the US

5.3. Policies and regulations

5.4. Activities and initiatives in the U.S.

5.5. USABC

5.6. IRA benefits on solid-state batteries

5.7. Activities in South Korea

5.8. Key activities and policies in South Korea

5.9. Battery vendors' efforts - Samsung SDI

5.10. Samsung's commercial efforts

5.11. LG's contributions

5.12. Activities in Japan

5.13. Key activities and developments in Japan

5.14. Activities in China

5.15. Policy support

5.16. Interests in China

5.17. 25 Chinese corporate progresses

5.18. 11 Chinese car player activities on solid-state batteries

5.19. Activities in Other Regions

5.20. Regional efforts: UK

5.21. Regional efforts: Germany

5.22. Regional efforts: France

5.23. Regional efforts: Australia

5.24. Activities on Automotive OEMs

5.25. Automakers' efforts - BMW

5.26. BMW's solid-state battery research

5.27. BMW's scaling competences from lab to prototype

5.28. Mercedes-Benz's inhouse cell development

5.29. Automakers' efforts - Volkswagen

5.30. Volkswagen's investment in electric vehicle batteries

5.31. Automakers' efforts - Hyundai

5.32. Hyundai's solid-state battery technology features

5.33. Enovate Motors

5.34. Other automotive OEMs

6. SOLID-STATE BATTERY RECENT FOCUSES

6.1. Typical hypes of solid-state batteries

6.2. Solid-state battery requirement

6.3. Solid-state battery development focuses in 2025

6.4. Temperature performance in solid-state batteries

6.5. Pressure effects on solid-state batteries

6.6. Pressure can lower energy density

6.7. AI integration in solid-state battery development

6.8. Preventing dendrite growth in solid-state batteries

6.9. Dendrites prevention

7. FROM CELLS DESIGN TO SYSTEM DESIGN FOR SOLID-STATE BATTERIES

7.1. Solid-State Battery Cell Design

7.2. Commercial battery form factors 1

7.3. Commercial battery form factors 2

7.4. Battery configurations 1

7.5. Battery configurations 2

7.6. Cell stacking options

7.7. Bipolar cells

7.8. ProLogium's bipolar design

7.9. "Anode-free" batteries

7.10. Challenges of anode free batteries

7.11. Close stacking

7.12. Flexibility and customisation provided by solid-state batteries

7.13. Cell size trend

7.14. Cell design ideas

7.15. From Cell to Pack

7.16. Pack parameters mean more than cells

7.17. The importance of a pack system

7.18. Influence of the CTP design

7.19. BYD's blade battery: Overview

7.20. BYD's blade battery: Structure and composition

7.21. BYD's blade battery: Design

7.22. BYD's blade battery: Pack layout

7.23. BYD's blade battery: Energy density improvement

7.24. BYD's blade battery: Thermal safety

7.25. BYD's blade battery: Structural safety

7.26. Cost and performance

7.27. BYD's blade battery: What CTP indicates

7.28. CATL's CTP design

7.29. CATL's CTP battery evolution

7.30. CATL's Qilin Battery

7.31. From cell to pack for conventional Li-ions

7.32. Solid-state batteries: From cell to pack

7.33. Bipolar-enabled CTP

7.34. Conventional design vs bipolar cell design

7.35. EV battery pack assembly

7.36. ProLogium: "MAB" EV battery pack assembly

7.37. MAB idea to increase assembly utilization

7.38. Solid-state battery: Competing at pack level

7.39. Business models between battery-auto companies

7.40. Battery Management System for Solid-State Batteries

7.41. The importance of a battery management system

7.42. Functions of a BMS

7.43. BMS subsystems

7.44. Cell control

7.45. Cooling technology comparison

7.46. BMS designs with different geometries

7.47. Qilin Battery's thermal management system

7.48. Thermal conductivity of the cells

7.49. Cell connection

7.50. Implications of pressure on pack level

7.51. Impact of high pressure on energy density in battery packs

7.52. BMS design considerations for SSBs

8. SOLID-STATE BATTERY MANUFACTURING

8.1. Timeline for mass production

8.2. Technology readiness level scale

8.3. Conventional Li-ion battery cell production process

8.4. Manufacturing cost for sulfide-based cells

8.5. Manufacturing cost for oxide-based cells

8.6. The incumbent process: Lamination

8.7. Conventional Li-ion battery manufacturing conditions

8.8. General manufacturing differences between conventional Li-ion and SSBs

8.9. Process chains for solid electrolyte fabrication

8.10. Process chains for anode fabrication

8.11. Process chains for cathode fabrication

8.12. Process chains for cell assembly

8.13. Exemplary manufacturing processes

8.14. Possible processing routes of solid-state battery components fabrication

8.15. Is mass production coming?

8.16. Pouch cells

8.17. Techniques to fabricate aluminium laminated sheets

8.18. Packaging procedures for pouch cells 1

8.19. Packaging procedures for pouch cells 2

8.20. Oxide electrolyte thickness and processing temperatures

8.21. Solid battery fabrication process

8.22. Manufacturing equipment for solid-state batteries

8.23. Industrial-scale fabrication of Li metal polymer batteries

8.24. Are thin film electrolytes viable?

8.25. Summary of main fabrication technique for thin film batteries

8.26. Wet-chemical & vacuum-based deposition methods for Li-oxide thin films

8.27. Current processing methods and challenges for mass manufacturing of Li-oxide thin-film materials

8.28. PVD processes for thin-film batteries 1

8.29. PVD processes for thin-film batteries 2

8.30. PVD processes for thin-film batteries 3

8.31. Ilika's PVD approach

8.32. Avenues for manufacturing

8.33. Toyota's approach 1

8.34. Toyota's approach 2

8.35. Hitachi Zosen's approach

8.36. Sakti3's PVD approach

8.37. Planar Energy's approach

8.38. Typical manufacturing method of the all-solid-state battery (SMD type)

8.39. ProLogium's LCB manufacturing processes

8.40. ProLogium's manufacturing processes

8.41. Solid Power: Fabrication of cathode and electrolyte

8.42. Solid Power cell production

8.43. Pilot production facility of Solid Power

8.44. Qingtao's manufacturing processes

8.45. Yichun 1GWh facility equipment and capacity

8.46. Introduction to dry electrode manufacturing

8.47. Comparison of dry vs conventional manufacturing

8.48. Dry battery electrode fabrication

8.49. Dry electrode binders

8.50. Comparison between wet slurry and dry electrode processes

9. RECYCLING

9.1. Global policy summary on Li-ion battery recycling

9.2. Battery geometry for recycling

9.3. Lack of pack standardisation

9.4. LIB recycling approaches overview

9.5. Recycling categories

9.6. Recycling of SSBs 1

9.7. Recycling of SSBs 2

9.8. Overview of SE classes and assessment of recyclability

9.9. Recycling plan of ProLogium 1

9.10. Recycling plan of ProLogium 2

9.11. Innovative lithium-metal recycling by Blue Solutions

9.12. Recycling proposed by Blue Solutions

9.13. Lithium metal recycling

10. STANDARDS/POLICIES/ REGULATIONS FOR AUTOMOTIVE APPLICATIONS

10.1. Standardisation and legislative framework

10.2. Global Standardization and Regulation

10.3. International Organizations

10.4. Relevant National Organizations

10.5. UN 38.3

10.6. IEC - 61960

10.7. IEC 61960 - 3 & 4

10.8. SAE J2464

10.9. UL 1642

10.10. UL 1642 - Further information: Scope of the Test

10.11. EUCAR and the Hazard Level

10.12. Common safety verification

11. COMPANY PROFILES

11.1. 24M Technologies, Inc.

11.2. Ampcera

11.3. Beijing WeLion New Energy Technology

11.4. Blue Current

11.5. Blue Solutions: The Latest From the Bolloré Battery Developer

11.6. BrightVolt, Inc

11.7. CALB

11.8. CEA-Leti

11.9. Chinese Academy of Sciences

11.10. Contemporary Amperex Technology Co. Limited (CATL)

11.11. Coslight International Group

11.12. Cymbet Corporation

11.13. Ensurge Micropower ASA

11.14. Excellatron Solid State LLC

11.15. Factorial Energy

11.16. FDK Corporation

11.17. Fisker Inc.

11.18. Fraunhofer

11.19. Front Edge Technology

11.20. Ganfeng Lithium

11.21. Hydro-Québec

11.22. Hytzer Energy

11.23. Ilika

11.24. Infinite Power Solutions

11.25. Ion Storage Systems

11.26. Ionic Materials

11.27. Jiawei Renewable Energy

11.28. Johnson Energy Storage

11.29. Kanadevia Corporation

11.30. Natrion

11.31. Ohara Corporation

11.32. PolyPlus Battery Company

11.33. Prieto Battery Inc

11.34. Prime Planet Energy & Solutions

11.35. Prologium Technology Co Ltd

11.36. Qingtao Energy Development

11.37. QuantumScape

11.38. Rimac Technology

11.39. Schott AG

11.40. Seeo, Inc

11.41. SES AI

11.42. Solid Power

11.43. SOLiTHOR

11.44. Solvay

11.45. STMicroelectronics

11.46. Taiyo Yuden

11.47. TDK

11.48. Toshiba

11.49. Toyota

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

関連レポート(キーワード「固体電池」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|