電気自動車用電動モーター 2026-2036年:技術、材料、市場、予測Electric Motors for Electric Vehicles 2026-2036: Technologies, Materials, Markets, and Forecasts 電気自動車用モーターの世界市場。モーター技術、材料、レアアース削減、軸方向磁束、インホイール、熱管理、ベンチマーク、サプライヤー。詳細な地域別予測。自動車、マイクロEV、バス、バン、トラック。 ... もっと見る

サマリー

電気自動車用モーターの世界市場。モーター技術、材料、レアアース削減、軸方向磁束、インホイール、熱管理、ベンチマーク、サプライヤー。詳細な地域別予測。自動車、マイクロEV、バス、バン、トラック。

電気モーターはまさに電気自動車(EV)の原動力です。バッテリーとパワーエレクトロニクスに加えて、電気モーターはドライブトレインの重要なコンポーネントです。電気モーターはもともと1800年代に開発されたにもかかわらず、新しい設計、パワーとトルク密度の向上、使用材料に関するより多くの配慮によって、市場は今日でも進化し続けています。これらは単なる漸進的な改善ではなく、軸流モーターやさまざまなOEMがレアアースを完全に排除するなどの開発が行われています。

IDTechExの「電気自動車用モーター 2026-2036年」レポートは、電気自動車用モーター市場におけるOEMの戦略、動向、新興技術について詳述しています。2015年から2024年の間に複数の地域で販売された700以上のEVモデルバリエーションの広範なモデルデータベースは、モーターのタイプ、性能、熱管理、市場シェアのきめ細かな市場分析に役立ちます。自動車、二輪車、三輪車、マイクロカー、小型商用車(バン)、トラック、バスについて、主要OEMの技術と戦略を、いくつかのユースケースと複数のモーターユニットのベンチマークとともに考察しています。また、軸流モータやインホイールモータなど、2036年までの市場予測とともに新技術も取り上げている。モーター要件とユースケースは、性能特性が要求される初期段階の市場として、eVTOL(電動垂直離着陸)航空機とeCTOL(電動従来型離着陸)航空機について詳述しています。

IDTechExは、BEVと新たな代替品におけるモーターの主要パラメータを分析している。出典"Electric Motors for Electric Vehicles 2026-2036"

材料とレアアース

EVモーター市場にとって重要な検討事項は磁性材料である。2015年から2024年にかけて、電気自動車市場における永久磁石(PM)モーターのシェアは、一貫して75%以上を維持しています。レアアース磁石は、そのサプライチェーンが中国に制約されていることと、歴史的な価格変動のため、2025年も引き続き懸念材料となっています。こうした懸念を回避するため、ルノーとBMWが巻線ローター・モーターを採用し、アウディが誘導モーターを採用するなど、欧州の複数のOEMが磁石を使用しない設計を選択している。2023年、テスラは次世代モーターをレアアース不使用のPMマシンにすると発表し、フェライト磁石などの代替磁性材料とそれが大量採用にもたらす課題への注目がさらに高まった。磁石価格は、2021年/2022年のピークを経て2023年に落ち着き、レアアース不使用の設計はやや遠ざかりましたが、輸出規制と地政学的緊張の継続により、2025年まで変動が続き、レアアースの使用は主要なトピックであり続けました。

本レポートでは、IDTechExがマグネットフリーのモーター設計、レアアース削減のルート、代替磁性材料のオプションについて分析しています。IDTechExは、PMモーターがモーターの支配的な形態であり続ける(特にEV市場における中国の優位性)と予測していますが、モーターあたりのレアアースはさらに削減され、代替磁性材料は市場でさらに進歩するでしょう。

自動車市場の大半は永久磁石モーターを使用している。出典「電気自動車用電動モーター 2026-2036"

新たな選択肢としての軸流磁束モーターとインホイールモーター

従来のEVに搭載されるラジアル磁束モーターに加え、多くの関心を集めながらも市場導入の初期段階にある2つの新たな選択肢、すなわち軸流磁束モーターとインホイールモーターがある。

軸流モータは磁束が回転軸に平行である(ラジアル磁束モータは垂直)。軸流モーターの利点には、出力とトルク密度の向上、さまざまなシナリオに組み込むのに理想的なパンケーキ型フォームファクターなどがある。以前は採用が進まなかったにもかかわらず、この技術は市場統合へと発展した。ダイムラーは主要プレーヤーであるYASAを買収し、同社のモーターを次期AMG電動プラットフォームに採用し、ルノーはWHYLOTと提携し、同社のハイブリッド車に軸流モータを採用している。中国勢もVoyahがアキシャルフラックスドライブユニットを展示するなど、アキシャルフラックスの発展を示している。

インホイールモーターは、数量限定のロードスタウントラックなど、一部のオンロード車に採用された。しかし、これまでのところ、インホイールモーターを使用すると表明されたほとんどの自動車プロジェクトは財政難に陥っている。にもかかわらず、重要な進展があったのはProteanで、東風は2023年にProteanDrive(インホイールモーター・プラットフォーム)を搭載した初のホモロゲーション乗用車を実証し、これに続いてフリートテストを実施している。

IDTechExは、特定の車両カテゴリーでは軸流モーターとインホイールモーターの需要が大幅に増加すると予測しているが、近い将来、従来の車載用ラジアルフラックスモーターに取って代わるとは予測していない。本レポートでは、新興モーター技術の性能と市場分析を行い、プレーヤー、採用、10年間の市場予測を掲載しています。

主な内容

自動車、二輪車、三輪車、マイクロカー、小型商用車(バン)、トラック、バス、eVTOL、eCTOL の BEV、PHEV、HEV における電気モーター市場の分析。

10年市場予測と分析

目次1.要旨

1.1.トラクション・モーターの種類の概要

1.2.主要自動車メーカーによるPMモーターへの収束

1.3.モータータイプの市場シェア予測 2015-2036年

1.4.自動車用電動トラクションモーターの動向解説

1.5.自動車用電動モーターの予測 2015-2036年 (台数、地域別)

1.6.自動車用電動モーターの予測 2015-2036年(台数、ドライブトレイン)

1.7.自動車用電動モーターの予測 2015-2036年(台数、モータータイプ)

1.8.マイクロEVのタイプ

1.9.電動3輪車とマイクロカーに搭載されるモーター

1.10.マイクロEVのモーターの種類

1.11.ハブモーターとミッドドライブモーター

1.12.マイクロEV用モーターの予測 2023-2036年 (台数、車種)

1.13.IDTechEx LCVセグメンテーション

1.14. ICEの性能に匹敵するeLCVモーター

1.15.PMモーターが世界的に優勢

1.16.2021~2036年のLCV電動モーター予測(台数、ドライブトレイン)

1.17.BEVとFCEVのM&HDトラック:重量対モーター出力

1.18.中型トラックモデルのモーター出力

1.19.大型トラックモデルのモーター出力

1.20.トラック用モーターの市場シェアと出力要件

1.21.トラック用電動モーターの予測 2021-2036年 (台数、ドライブトレイン&カテゴリー)

1.22.バスのカテゴリーと電動化

1.23.モーター取り付け - 中央または車軸取り付け

1.24.バスの電動モーター予測 2021-2036年(台数、ドライブトレイン)

1.25. 商用車用eAxleのベンチマーク:トルクとGAWR

1.26. eVTOLモータのサイジング

1.27.航空機タイプのエネルギーおよび電力要件の概要

1.28.出力密度の比較:航空用モーター

1.29.軸流モーターの出力とトルク密度のプレイヤーベンチマーク

1.30.自動車用軸流モーターの予測 2021-2036年 (台)

1.31.インホイールモーターの生産台数予測 2021-2036年 (台)

1.32.モータータイプの出力密度ベンチマーク

1.33.モータータイプ別出力・トルク密度の平均と範囲

1.34.最高速度と出力密度

1.35.OEM & Tier 1のレアアース排除への取り組み

1.36.モーター巻線の進化

1.37.ヘアピン巻線の地域市場シェア

1.38.BEVモーター固定子の銅含有量ベンチマーク

1.39.電動モーターの材料予測 2021-2036年 (kg)

1.40.モーター冷却戦略の予測 2015-2036年 (単位)

1.41.OEMとティア1の供給関係 (1)

1.42.OEMとティア1の供給関係 (2)

1.43.商用車OEMとTier1供給の関係(1)

1.44.商用車OEMとTier1供給の関係 (2)

1.45.2021-2036年年の自動車・ドライブトレイン別モーター総予測(単位)

1.46.IDTechEx サブスクリプションでさらにアクセス

2.序論

2.1.電気自動車:基本原理

2.2.電気自動車の定義

2.3.ドライブトレインの仕様

2.4.パラレル・ハイブリッドとシリーズ・ハイブリッド説明

2.5.電気モーター

3.電気トラクション・モーターの種類とベンチマーク

3.1.1.電気トラクションモーターの種類

3.1.2.トラクション・モーターの種類の概要

3.1.3.電気トラクションモーターのベンチマーク

3.1.4.ピーク特性と連続特性

3.1.5. 101 モータのピーク性能と連続性能のベンチマーク

3.1.6 出力

3.1.6.65 モータのピーク性能と連続性能の比較

3.1.7 トルク

3.1.7.効率

3.1.8.ブラシレスDCモーター(BLDC):動作原理

3.1.9.BLDCモーター:利点、欠点

3.1.10.BLDCモーター:ベンチマークスコア

3.1.11.永久磁石同期モータ(PMSM):動作原理

3.1.12.PMSM:利点、欠点

3.1.13.PMSM:ベンチマークスコア

3.1.14.PMSMとBLDCの違い

3.1.15.巻線型ローター同期モーター(WRSM):動作原理

3.1.16.ルノーのマグネットフリーモータ

3.1.17.ローターの電力伝達:ブラシ対ワイヤレス

3.1.18.WRSMモーターベンチマークスコア

3.1.19.WRSM:利点、欠点

3.1.20.AC インダクションモーター (ACIM):動作原理

3.1.21.AC インダクションモーター (ACIM)

3.1.22.AC インダクションモーター:ベンチマークスコア

3.1.23.AC インダクションモーター:利点、欠点

3.1.24.リラクタンスモーター

3.1.25.リラクタンスモーター:動作原理

3.1.26.スイッチドリラクタンスモーター(SRM)

3.1.27.スイッチドリラクタンスモーターベンチマークスコア

3.1.28.永久磁石アシスト型リラクタンス(PMAR)

3.1.29.PMARモーターベンチマークスコア

3.1.30.リラクタンスと相互作用トルクの寄与

3.1.31.再生

3.2.電気牽引モーター:まとめとベンチマーク結果

3.2.1.トラクション・モーターの構造とメリットの比較

3.2.2.モーター効率の比較

3.2.3.電動トラクション・モーターのベンチマーク

3.2.4.複数のモーター

4.電気自動車のモーター市場

4.1.BEVとPHEVモータータイプの地域別市場シェア 2015-2024年

4.2.主要自動車メーカーによる PM モータへの収束

4.3.モータータイプ市場シェア予測 2015-2036年

4.4.自動車用電動トラクションモーターの動向解説

4.5.自動車用電動モータの予測 2015-2036年 (台数、地域別)

4.6.自動車用電動モーターの予測 2015-2036年(台数、ドライブトレイン)

4.7.自動車用電動モーターの予測 2015-2036年(台数、モータータイプ)

4.8.自動車用電動モータの出力予測 2015-2036年 (kW、地域別)

4.9.自動車用電動モータの出力予測 2015-2036年 (kW、ドライブトレイン)

4.10.自動車用電動モーターの価値予測 2021-2036年 (米ドル、ドライブトレイン)

5.マイクロモビリティ

5.1.マイクロEVの紹介

5.2.マイクロEVのタイプ

5.3.マイクロEVセグメントの比較

5.4.三輪車の本場としてのアジア

5.5.電動二輪車の分類

5.6.電動二輪車:パワークラス

5.7.二輪車のモーター技術

5.8.インドの電動二輪車OEM

5.9.電動二輪車の地域別動力

5.10.電動二輪車のモーター出力

5.11.三輪車の役割

5.12.三輪車の分類

5.13.中国とインド:主な三輪車市場

5.14.インドE3Wのモデル例

5.15.中国のE3Wモデル

5.16.中国とインド以外の三輪車

5.17. 三輪車用eアクスル

5.18.マイクロカー都市型EVのゴルディロックス

5.19.地域別マイクロカーの例

5.20.電動3輪車とマイクロカーのモーター

5.21.マイクロEVのモーターの種類

5.22.ハブモーターとミッドドライブモーター

5.23.マイクロモビリティのモーターメーカー

5.24.マイクロEVモータの予測 2023-2036年 (台数、車種)

5.25.マイクロモビリティ研究

6.電気小型商用車(ELCV)

6.1.電気式LCVの紹介

6.2.小型商用車(LCV)

6.3.IDTechEx LCVセグメンテーション

6.4.地域別LCV販売台数

6.5.電動LCV:推進要因と障壁

6.6.欧州で普及している電動LCVの仕様

6.7.中国で人気のある電動LCVの仕様

6.8.電動LCVに使用されるモーター

6.9.モーター出力の進化

6.10. ICEの性能に匹敵するeLCVモーター

6.11.PMモーターが世界的に優勢

6.12.eLCVのティア1との既知の関係

6.13.OEMはモーター開発を内製化

6.14.LCV 電動モータの予測 2021-2036年 (台数、ドライブトレイン)

6.15.小型商用車リサーチ

7.電気トラック

7.1.トラックは資本財

7.2.ゼロエミッショントラック:推進要因と障壁

7.3.2021-2024 年の地域別モデル供給状況

7.4.BEV と FCEV M&HD トラック:重量対モーター出力

7.5.中型トラックモデルのモーター出力

7.6.大型トラックモデルのモーター出力

7.7.トラック・モーター・タイプの市場シェアと出力要件

7.8.一体型e-Axleスペースの優位性

7.9.AVL

7.10.アリソン・トランスミッションのeGenパワーeアクスル

7.11.ボルグワーナー

7.12.Dana E-Axles

7.13.ダナTM4

7.14.ダンフォス・エディトロン

7.15.デトロイトEアクスル

7.16.FPT トラックモーターズ

7.17.Accelera eAxles

7.18.リナマーコーポレーション eAxles

7.19.メリトール 14Xe 電動ドライブトレイン

7.20.ボルボ・ドライブライン

7.21.ZF セントラルドライブ

7.22.トラック用電動モーター予測 2021-2036年 (台数、ドライブトレイン&カテゴリー)

7.23.電気トラック調査

8.電気バス

8.1.バスのカテゴリーと電動化

8.2.バスの種類の概要と電動化の具体的課題

8.3.排出削減バスの選択肢

8.4.電気バス-グローバルな展望

8.5.モーターの取り付け - 中央取り付けか車軸取り付けか

8.6.電気バスのモータータイプ

8.7.バスのモーターベンチマークと測定基準

8.8.電気バス用トラクションモータ

8.9.モーターサプライヤー - 概要

8.10.PMの収束

8.11.モーターOEM供給関係

8.12.Dana TM4

8.13.Equipmake - 改造用モーター

8.14.Siemens/Cummins ACCELERA

8.15.Traktionssysteme Austria (TSA)

8.16.ヴォイス

8.17.ヴォイス - セントラルモーターズのみ

8.18.ZF Group - AxTraxとCeTrax

8.19.ZF Group - 新型 AxTrax と CeTrax の PM モーターへの移行

8.20.ボルボ電動バス

8.21.バス用電動モーターの予測 2021-2036年 (台数、ドライブトレイン)

8.22.電気バス研究

9.HEV駆動技術

9.1.HEV自動車メーカー

9.2.ハイブリッドシナジードライブ/トヨタハイブリッドシステム

9.3.ハイブリッドシナジードライブ/トヨタハイブリッドシステム

9.4.ホンダ

9.5.ホンダの2モーターハイブリッドシステム

9.6.日産ノートe-POWER

9.7.ヒュンダイ・ソナタ・ハイブリッド

9.8.トヨタ プリウス ドライブモーター:2004-2010年

9.9.トヨタ・プリウス・ドライブモーター:2004-2017年

9.10.ハイブリッド MG の比較

9.11.世界のHEV車用モーター/ジェネレーター動向

9.12.HEV 車の MG の動向と前提条件

9.13.世界の HEV 車用 MG 需要予測 2015-2036年 (台数, kW)

9.14.高電圧ハイブリッド電気自動車リサーチ

10.電動航空機

10.1. eVTOL モータ要件

10.1.1. eVTOL モータ/パワートレイン要件

10.1.2. eVTOL 航空機モータの出力サイジング

10.1.3. eVTOL 電力要件:kW 見積もり

10.1.4.電気モーターと分散型電気推進

10.1.7. eVTOL 電気モーターの数

10.1.8.モータサイジング

10.2. eCTOL モータ要件

10.2.1. eCTOL モータ/パワートレイン要件

10.2.2.航空機タイプのエネルギーおよび電力要件の概要

10.2.3.代表的な航空機エンジン

10.2.4.航空機エンジンの出力と重量

10.2.5.ターボファン出力の推定

10.2.6.電気モーターと分散型電気推進

10.2.7.100MW電気推進ユニット構築の課題

10.3.航空用電気モーター:プレーヤー

10.3.1.上昇

10.3.2.エアバスと東芝:超電導エンジン

10.3.3.コリンズ - モーター製品に取り組む航空宇宙サプライヤー

10.3.4.ダクシオンはターボファンに代わるモーターを再発明している

10.3.5.EMRAX

10.3.6. ePropelled

10.3.7.エボリート

10.3.8.H3X

10.3.9.MAGicALL

10.3.10. MagniX

10.3.11.mgmコンプロ

10.3.12.日本電産エアロスペース

10.3.13.ロールス・ロイス/シーメンス

10.3.14.ロールス・ロイス/シーメンス

10.3.15.サフラン

10.3.16.ライト・エレクトリックの高出力重量モーター

10.3.17.ゼロアビア

10.3.18.その他の選手の例

10.3.19.出力密度の比較:航空用モーター

10.3.20.トルク密度の比較:航空用モーター

10.3.21. eCTOLとeVTOL研究

11.新興モーター技術

11.1.軸流モータ

11.1.1.ラジアル磁束モーター

11.1.2.軸流モータ

11.1.3.ラジアル磁束モーターと軸流磁束モーター

11.1.4.ヨーク付き軸流とヨークレス軸流

11.1.5.軸流熱管理の課題

11.1.6.軸流モーターのプレーヤー一覧

11.1.7.ビヨンド・モーターズ

11.1.8.AVIDはTurntideに買収された

11.1.9.EMRAX

11.1.10.エレメンタル・モーターズ

11.1.11.エミル・モーターズ

11.1.12.インフィニタム・エレクトリックプリント基板ステーター

11.1.13.ランボルギーニ

11.1.14.ケーニグセグ:ラキシャルフラックス

11.1.15.マグナックス

11.1.16.トラキシアル(マグナックス社)

11.1.17.マジェレック・プロパルジョン

11.1.18.Saietta

11.1.19.トレサ・モーターズ

11.1.20.ウィロット

11.1.21.ホワイロットとルノー

11.1.22.YASA軸流モーター

11.1.23.YASAとケーニグセグ

11.1.24.YASAとフェラーリ

11.1.25.ランボルギーニ634-アキシャル・フラックスとV8

11.1.26.ダイムラー、YASAを買収

11.1.27.メルセデス・ビジョン・ワン・イレブン・コンセプト

11.1.28.成長する中国のアキシャルフラックス

11.1.29.商用軸流モーターの出力とトルク密度のベンチマーク

11.1.30.軸流モーターの出力とトルク密度のプレーヤー・ベンチマーク

11.1.31.自動車用軸流モーターの予測 2021-2036年 (台)

11.2.インホイールモーター

11.2.1.インホイールモーター

11.2.2.インホイールモーターのリスクと機会

11.2.3.インホイールモーターのリスクと機会

11.2.4.インホイールモーターのリスクと機会

11.2.5.コニファー

11.2.6.ディープドライブ

11.2.7.ドーナツラボ

11.2.8.エラフェ

11.2.9.フェラーリ

11.2.10.ジェムモーターズ

11.2.11.日立

11.2.12.現代モービス

11.2.13.日本電産

11.2.14.オルビス電気

11.2.15.プロテアンエレクトリック

11.2.16.REEオートモーティブ

11.2.17.ルノーとアルピーヌ、インホイールモーターを採用

11.2.18.VWがインホイールモーターを検討中?

11.2.19.シェフラー

11.2.20.インホイールモーター搭載車の例

11.3.インホイールモーターの軸流

11.3.1.インホイールモーター生産予測 2021-2036 (台)

11.3.2.軸流束とインホイールモーターの BEV モーターに対するベンチマーク

11.3.3.モータータイプの出力密度ベンチマーク

11.3.4.モータ・タイプのトルク密度ベンチマーク

11.3.5.モータータイプ別出力とトルク密度の平均と範囲

11.3.6.最高速度と出力密度

11.4.スイッチドリラクタンスモータの問題の克服

11.4.1.スイッチドリラクタンスモータ(SRM)

11.4.2.SRMには永久磁石がない

11.4.3.先進電気機械(AEM):商用車

11.4.4.AEMとベントレー

11.4.5.エネディム

11.4.6.RETORQ Motors

11.4.7.パンチ・パワートレイン

11.4.8.ターンタイド・テクノロジーズ

11.4.9.EV用スイッチドリラクタンスプレーヤ

11.5.その他の製造開発

11.5.1.モーター製造の将来技術

11.5.2.セグメント化されたステータ

11.5.3.モーターラミネートのスクリーン印刷

11.5.4.銅巻線へのグラフェンの添加

12.電気モーターの材料

12.1.1.電気モーターに必要な材料とは?

12.2.永久磁石の材料

12.2.1.ローターの磁性材料分布

12.2.2.ID4対リーフ対モデル3ローター

12.2.3.モーター用磁石の組成

12.2.4.レアアースの採掘

12.2.5.レアアースの採掘、加工、金属化、磁石生産の地域市場シェア

12.2.6.歴史的な価格変動と最近の技術および材料の輸出規制がレアアース供給の不確実性を煽る

12.2.7.レアアース磁石のサプライチェーンと市場

12.2.8.EVモーター材料の変動性

12.2.9.レアアース排除に向けた市場の動き

12.2.10.高性能モーター用軟磁性材料

12.3.レアアースの削減と排除

12.3.1.欧州のマグネットフリー設計への動き

12.3.2.希土類フリー磁石の主要磁気特性と課題

12.3.3.希土類磁石はほとんどの指標で競合技術を上回る

12.3.4.テスラの次世代モーター

12.3.5.テスラがレアアースを排除する方法(1)

12.3.6.テスラがレアアースを排除する方法(2)

12.3.7.テスラによるレアアース削減の可能性 (3)

12.3.8.日本におけるレアアース削減の進展

12.3.9.レアアース削減のためのモーター設計

12.3.10.レアアースから移行するインド

12.3.11.代替磁性材料

12.3.12.代替磁性材料

12.3.13.トヨタのネオジム還元磁石

12.3.14.ナイロン・マグネティクス

12.3.15.ナイロンの資金調達とパートナーシップ

12.3.16.パッセンジャー希土類フリー磁石

12.3.17.モーターにおけるフェライトの性能とネオジムの比較

12.3.18.フェライトの性能とネオジムの比較

12.3.19.レアアースのリサイクル

12.3.20.レアアースを排除するOEM & Tier 1のアプローチ

12.4.ローターとステーター巻線

12.4.1.ローターのアルミニウムと銅の比較

12.4.2.ステーターの丸線対銅のヘアピン

12.4.3.丸線対ヘアピン対連続巻線

12.4.4.モーター巻線の進化

12.4.5.正方形巻線の多くの種類

12.4.6.波巻き

12.4.7.MGモーターズ(上海汽車)

12.4.8.VWのMEB

12.4.9.テスラ

12.4.10.ラウンド巻とヘアピン巻:OEM

12.4.11.BEVモーター固定子の銅含有量ベンチマーク

12.4.12.ヘアピン巻線の地域シェア

12.4.13.新しい巻線フォーマット?

12.4.14.アルミ巻線と銅巻線の比較

12.4.15.圧縮アルミニウム巻線

12.4.16.アルミ巻線:プレーヤー

12.5.モーター材料の環境影響と予測

12.5.1.環境負荷の紹介

12.5.2.材料の環境負荷

12.5.3.BEV モーターの材料集約度

12.5.4.複数のBEVモーターの環境影響

12.5.5.レアアースモーター用磁石の材料 2021~2036年予測 (kg)

12.5.6.レアアースとレアアースフリーの磁石材料の予測 2021-2036 (kg)

12.5.7.電気モーターの2021~2036年予測(kg)

13.電気モーターの熱管理

13.1.1.電気モーターの冷却

13.2.モーターの冷却戦略

13.2.1.空冷

13.2.2.水-グリコール冷却

13.2.3.油冷却

13.2.4.電気モーターの熱管理の概要

13.2.5.出力別のモーター冷却戦略

13.2.6.モータータイプ別冷却戦略

13.2.7.冷却技術:OEM戦略

13.2.8.地域別モーター冷却戦略 (2015-2024)

13.2.9.モーター冷却戦略の市場シェア(2015-2024年)

13.2.10.モーター冷却戦略の予測 2015-2036 (台)

13.2.11.代替冷却構造

13.2.12.巻線を通しての冷却

13.2.13.冷媒冷却

13.2.14.電動機における二相冷却(1)

13.2.15.電動モーターにおける二相冷却(2)

13.2.16.浸漬冷却

13.2.17.相変化材料

13.2.18.熱管理による重希土類の削減

13.3.モーターの絶縁とカプセル化

13.3.1.含浸とカプセル化

13.3.2.ポッティングおよび封止:プレーヤー

13.3.3.800Vモーター絶縁の課題

13.3.4.PEEK代替としてのPPSU

13.3.5.PEEKとPAEKの利点

13.3.6.アクサルタ-モーター絶縁

13.3.7.イートン - ナノコンポジットPEEK絶縁

13.3.8.Elantas - 800V モーター用絶縁システム

13.3.9.SABIC - 800V モーター絶縁

13.3.10.ソルベイ - PEEK絶縁

13.3.11.絶縁ヘアピン巻線

13.4.PEEKモーター絶縁

13.4.1.PEEKとPAEKの利点

13.4.2.ベカルト-PEEK絶縁

13.4.3.イートン - ナノコンポジットPEEK断熱材

13.4.4.ソルベイ - PEEK断熱材

13.4.5.Syensqo PEEKモーター絶縁

13.4.6.ビクトレックス - PEEKモーター絶縁

13.4.7.PEEKはいつ使用すべきか?

14.EVモーター:OEMの使用例と供給パートナーシップ

14.1.1.OEMとティア1サプライの関係(1)

14.1.2.OEMとティア1サプライの関係(2)

14.1.3.自社でのモーター開発に移行するOEM

14.2.モーター事例

14.2.1.アストンマーティン・ヴァルハラ(1)

14.2.2.アストンマーティン・ヴァルハラ(2)

14.2.3.アウディe-トロン

14.2.4.アウディe-トロン

14.2.5.アウディQ4 e-tron

14.2.6.アウディ・プレミアムプラットフォーム・エレクトリック(PPE)

14.2.7.BMW i3 2016

14.2.8.BMW 第5世代ドライブ(ジャガー)

14.2.9.BMW 第6世代

14.2.10.BYD e-Platform 3.0

14.2.11.BYD >30,000rpmモーター

14.2.12.Chara Technologies

14.2.13.シボレー・ボルト以降(LG)

14.2.14.エキップメイク

14.2.15.フォード・マスタング・マッハE(ボルグワーナー、マグナ)

14.2.16.GAC

14.2.17.GM ウルティウムドライブ

14.2.18.ファーウェイ

14.2.19.現代 E-GMP(ボルグワーナー)

14.2.20.IAV:電動モーターにおける二相冷却(1)

14.2.21.IAV:電動モーターにおける二相冷却(2)

14.2.22.インフィモーション

14.2.23.ジャガーI-PACE(AAM)

14.2.24.ロードスタウン・モーターズ(エラフェ)

14.2.25.ルーシッド・エア

14.2.26.IRPシステムズ

14.2.27.マグナの最新eドライブ

14.2.28.メルセデスEQ

14.2.29.メルセデスCLA

14.2.30.日本電産・第2世代ドライブ

14.2.31.日産アリヤ

14.2.32.日産リーフ

14.2.33.ポルシェ・テイカン

14.2.34.リカルド・レアアース・フリードライブユニット

14.2.35.リマック・テクノロジー・ドライブユニット

14.2.36.リビアン

14.2.37.リビアン自社製モーター

14.2.38.SAIC - 油冷システム

14.2.39.ステランティス・シェアード・プラットフォーム(Npe)

14.2.40.テスラ誘導モーター

14.2.41.テスラPMモーター

14.2.42.テスラのカーボン巻きモーター

14.2.43.テスラ・サイバートラック

14.2.44.トヨタ・プリウス2004~2010

14.2.45.UAES(ボッシュ)

14.2.46.ボルボのモーター開発

14.2.47.VW ID3/ID4

14.2.48.VW APP550

14.2.49.ゼロ・ゼロフォース・パワートレイン

14.2.50.ZF

14.2.51.ZFセレクト・プラットフォーム(1)

14.2.52.ZF SELECTプラットフォーム(2)

14.3.ティア 1 巻線ローター同期モーター/外部励磁同期モーター

14.3.1.ボルグワーナーのEESM開発

14.3.2.マーレ

14.3.3.シェフラーの巻線ローター設計

14.3.4.ヴィテスコ

14.3.5.ZF

14.4.供給関係

14.4.1.商用車OEMとティア1の供給関係(1)

14.4.2.商用車 OEM および Tier1 サプライ関係(2)

14.4.3.アリソン・トランスミッション - Anadolu Isuzu

14.4.4.アイシン精機、デンソー、トヨタ自動車がBluE Nexusを設立

14.4.5.ボルグワーナーの提携と買収(1)

14.4.6.ボルグワーナーの提携と買収(2)

14.4.7.ボッシュ

14.4.8.コンチネンタル

14.4.9.Dana 供給関係と発表

14.4.10.GKNオートモーティブ

14.4.11.ルーシッド供給パートナーシップ

14.4.12.日立

14.4.13.ホースパワートレイン

14.4.14.LGエレクトロニクスとマグナ

14.4.15.マグナとメルセデス

14.4.16.日本電産

14.4.17.マベル

14.4.18.シェフラー

14.4.19.ヴァレオ

14.4.20.ビテスコ・テクノロジーズ

14.4.21.ヴィテスコとシェフラーの合併

14.4.22.ヤマハ - ハイパーカー用電動モーター

14.4.23.ZF

15.EV モーター:OEMベンチマーク

15.1.自動車

15.1.1.BEV パワー密度ベンチマーク

15.1.2.BEV トルク密度ベンチマーク

15.1.3.BEVパワー・トルク密度ベンチマーク

15.1.4.EV ドライブユニット仕様の概要

15.2.商用車

15.2.1.商用車モーター出力密度ベンチマーク

15.2.2.商用車モータのトルク密度ベンチマーク

15.2.3.商用車モーター出力トルク密度ベンチマーク

15.2.4.商用車モータの仕様概要

15.3.軽負荷

15.3.1.小型車両用モーター出力密度ベンチマーク

15.3.2.小型商用車モータのトルク密度ベンチマーク

15.3.3.商用車用 eAxle

15.4.1. 商用車用 eAxle のベンチマーク:商用車用 eAxle のベンチマーク:トルクと GAWR

15.4.2:eAxle Specification Summary

16.予測と前提条件

16.1.予測方法と前提条件

16.2.モーター価格の見通しと前提条件

16.3.2024 年の車両カテゴリー別平均モーター出力(kW)

16.4.1台当たりモーターと1台当たりkWの前提

16.5.自動車用電動モーターの予測 2015-2036年 (台数、地域別)

16.6.自動車用電動モーターの予測 2015-2036年 (台数、ドライブトレイン)

16.7.自動車用電動モーターの予測 2015-2036年(台数、モータータイプ)

16.8.自動車用電動モータの出力予測 2015-2036年 (kW、地域別)

16.9.自動車用電動モータの出力予測 2015-2036年 (kW、ドライブトレイン)

16.10.自動車用電動モータの価値予測 2021-2036年 (米ドル、ドライブトレイン)

16.11.マイクロEVモータの予測 2023-2036 (台数、車両タイプ)

16.12.LCV用電動モータの予測 2021-2036年 (台数、ドライブトレイン)

16.13.トラック用電動モータの予測 2021-2036年 (台数、ドライブトレイン&カテゴリー)

16.14.バス用電動モータの予測 2021-2036年 (台数、ドライブトレイン)

16.15.HEV車用MGの世界需要予測 2015-2036年年 (台, kW)

16.16.自動車用軸流モーターの予測 2021-2036年 (台)

16.17.インホイールモーターの生産台数予測 2021-2036年 (台)

16.18.レアアースモーター用磁石の素材 2021-2036年年予測 (kg)

16.19.レアアース対レアアースフリー磁石材料の予測 2021-2036年 (kg)

16.20.電気モーターの材料 2021~2036年予測(kg)

16.21.自動車モーターの冷却戦略予測 2015-2036年 (台)

16.22.自動車・ドライブトレイン別モーター総出力の予測 2021-2036年 (台)

16.23.自動車・ドライブトレイン別モーター総出力の予測 2021-2036年 (kW)

16.24.2021~2036年の自動車・ドライブトレイン別モーター総市場規模予測(10億米ドル)

17.企業プロファイル

17.1.先進電気機械:レアアース不要モーター

17.2.アリソン・トランスミッション:商用車用eアクスル

17.3.AVIDテクノロジー

17.4.アクサルタ・コーティング・システムズ電気モーター絶縁

17.5.ビヨンド・モーターズ軸流モータ

17.6.カーペンター電化:モーター用軟磁性材料

17.7.DELO:自動車部品用接着剤

17.8.イートン研究所電気モーター絶縁

17.9.エラフェ(2021年)

17.10.ダイナミックトルクスイッチング電動モーター

17.11.エキップメイク電動モーターとパワーエレクトロニクス

17.12.EVRモーター

17.13.インフィニタム・エレクトリックプリント固定子付き軸流モータ

17.14.インフィニタム・エレクトリックプリント基板固定子軸流モータ

17.15.マグナックス

17.16.モーダルモーター

17.17.Monumo:AIモーター設計

17.18.Monumo:モーター開発のための人工知能

17.19.ニーロン・マグネティクスレアアース・フリー永久磁石

17.20.プロテアン電機

17.21.RETORQモーター

17.22.サイエッタ・エレクトリック・ドライブ:軸流モータ

17.23.シェフラーマグネットフリーモーター

17.24.Traxial (a Magnax Company)

17.25.究極のトランスミッションテスラがレアアースマグネットを避ける方法

17.26.究極のトランスミッション電気モーターの熱管理

17.27.ビクトレックス

Summary

Global markets for electric vehicle motors. Motor technology, materials, rare-earth reduction, axial flux, in-wheel, thermal management, benchmarking, and suppliers. Granular regional forecasts. Cars, micro-EVs, buses, vans, and trucks.

Electric motors truly are the driving force behind electric vehicles (EVs). In addition to the batteries and power electronics, the electric motor is a critical component within the drivetrain. Despite electric traction motors originally being developed in the 1800s, the market is still evolving today with new designs, improving power and torque density and more considerations around the materials used. These aren't just incremental improvements either, with developments such as axial flux motors and various OEMs eliminating rare-earths altogether.

This report from IDTechEx on Electric Vehicle Motors 2026-2036 details OEM strategies, trends, and emerging technologies within the motor market for EVs. An extensive model database of over 700 EV model variants sold between 2015-2024 in several geographic regions aids in a granular market analysis of motor type, performance, thermal management, and market shares. Technologies and strategies of major OEMs are considered for cars, two-wheelers, three-wheelers, microcars, light commercial vehicles (vans), trucks, and buses along with several use-cases and benchmarking of several motor units. Emerging technologies are also addressed with market forecasts through to 2036 such as axial flux and in-wheel motors. Motor requirements and use cases are detailed for eVTOL (electric vertical take-off and landing) and eCTOL (electric conventional take-off and landing) aircraft as a much earlier stage market, with demanding performance characteristics.

IDTechEx analyses key parameters of motors in BEVs and emerging alternatives. Source: "Electric Motors for Electric Vehicles 2026-2036"

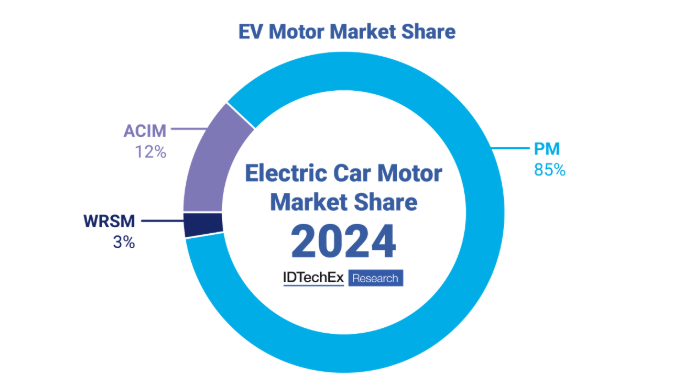

Materials and Rare-earths

A key consideration for the EV motor market is that of magnetic materials. From 2015-2024 the share of permanent magnet (PM) motors in the electric car market remained consistently above 75%. Rare-earth magnets continue to be a concern in 2025 due to their supply chain being constrained to China and the historic price volatility. To avoid these concerns, several European OEMs have opted for magnet free designs including Renault and BMWs adoption of wound rotor motors and Audi's use of induction motors. In 2023, Tesla announced its next generation motor would be a PM machine without rare-earths, further bringing the focus to alternative magnetic materials such as ferrite magnets and the challenges they pose to mass adoption. Magnet prices settled in 2023 after a peak in 2021/2022 pushing rare earth free designs somewhat away from the fore, but the volatility continued into 2025 with export restrictions and continued geopolitical tensions meaning the use of rare earths continues to be a primary topic.

In this report, IDTechEx provides an analysis of magnet free motor designs, routes to rare-earth reduction, and options for alternative magnetic materials. IDTechEx predicts that PM motors will remain the dominant form of motor (especially with China's dominance in the EV market), but there will be further reductions in rare-earths per motor and alternative magnetic materials making greater progress in the market.

The vast majority of the car market is using permanent magnet motors. Source: "Electric Motors for Electric Vehicles 2026-2036"

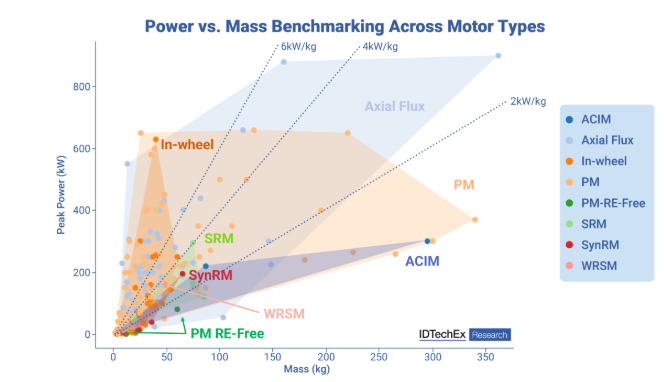

Axial Flux and In-wheel Motors as Emerging Options

In addition to the traditional on-board radial flux motors in EVs, there are two emerging alternatives that have gained a lot of interest but are at early stages of market adoption, namely axial flux and in-wheel motors.

In axial flux motors the magnetic flux is parallel to the axis of rotation (compared to perpendicular in radial flux machines). The benefits of axial flux motors include increased power and torque density and a pancake form factor ideal for integration in various scenarios. Despite the previous lack of adoption, the technology has evolved to market integration. Daimler acquired key player YASA to use its motors in the upcoming AMG electric platform and Renault has partnered with WHYLOT to use axial flux motors in its hybrids. Chinese players are also showing developments in axial flux with Voyah showcasing an axial flux drive unit.

In-wheel motors made it into some on-road vehicles such as a limited quantity of Lordstown trucks. However, most automotive projects stated to use in-wheel motors so far have run into financial troubles. Despite this, key progress was made by Protean where Dongfeng demonstrated the first homologated passenger car with ProteanDrive (in-wheel motor platform) in 2023 and is following this with fleet testing.

IDTechEx expects a large increase in demand for axial flux and in-wheel motors for certain vehicle categories, but does not predict they will displace the traditional on-board radial flux machines in the near future. This report carries out performance and market analysis of emerging motor technologies with players, adoption, and 10 year market forecasts.

Key Aspects

Analysis of the electric motor markets in BEVs, PHEVs and HEVs across cars, two-wheelers, three-wheelers, microcars, light commercial vehicles (vans), trucks, buses, eVTOL, and eCTOL including

10 Year Market Forecasts & Analysis

Table of Contents1. EXECUTIVE SUMMARY

1.1. Summary of Traction Motor Types

1.2. Convergence on PM Motors by Major Automakers

1.3. Motor Type Market Share Forecast 2015-2036

1.4. Commentary on Electric Traction Motor Trends in Cars

1.5. Automotive Electric Motor Forecast 2015-2036 (units, regional)

1.6. Automotive Electric Motor Forecast 2015-2036 (units, drivetrain)

1.7. Automotive Electric Motor Forecast 2015-2036 (units, motor type)

1.8. Micro EV Types

1.9. Motors in Electric Three-Wheelers and Microcars

1.10. Types of Motors in Micro EVs

1.11. Hub Motors vs. Mid-Drive Motors

1.12. Micro-EV Motor Forecast 2023-2036 (units, vehicle type)

1.13. IDTechEx LCV Segmentation

1.14. eLCV Motors Match ICE Performance

1.15. PM Motors Are Dominant Worldwide

1.16. LCV Electric Motor Forecast 2021-2036 (units, drivetrain)

1.17. BEV and FCEV M&HD Trucks: Weight vs Motor Power

1.18. Medium Duty Truck Models Motor Power

1.19. Heavy Duty Truck Models Motor Power

1.20. Truck Motor Type Market Share and Power Output Requirements

1.21. Truck Electric Motor Forecast 2021-2036 (units, drivetrain & category)

1.22. Bus Categories and Electrification

1.23. Motor Mounting - Central or Axle Mounted

1.24. Bus Electric Motor Forecast 2021-2036 (units, drivetrain)

1.25. eAxle for Commercial Vehicle Benchmarking: Torque and GAWR

1.26. eVTOL Motor Sizing

1.27. Overview of Plane Types Energy and Power Requirements

1.28. Power Density Comparison: Motors for Aviation

1.29. Player Benchmark of Axial Flux Motors Power and Torque Density

1.30. Automotive Axial Flux Motor Forecast 2021-2036 (units)

1.31. In-wheel Motors Production Forecast 2021-2036 (units)

1.32. Motor Type Power Density Benchmark

1.33. Average and Range of Power and Torque Density by Motor Type

1.34. Max Speed and Power Density

1.35. OEM & Tier 1 Approaches to Eliminate Rare Earths

1.36. Evolution of Motor Windings

1.37. Hairpin Winding Regional Market Shares

1.38. BEV Motor Stator Copper Content Benchmarking

1.39. Materials in Electric Motors Forecast 2021-2036 (kg)

1.40. Motor Cooling Strategy Forecast 2015-2036 (units)

1.41. OEM and Tier 1 Supply Relationships (1)

1.42. OEM and Tier 1 Supply Relationships (2)

1.43. Commercial Vehicle OEM and Tier 1 Supply Relationships (1)

1.44. Commercial Vehicle OEM and Tier 1 Supply Relationships (2)

1.45. Total Motors Forecast by Vehicle and Drivetrain 2021-2036 (units)

1.46. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. Electric Vehicles: Basic Principle

2.2. Electric Vehicle Definitions

2.3. Drivetrain Specifications

2.4. Parallel and Series Hybrids: Explained

2.5. Electric Motors

3. TYPES OF ELECTRIC TRACTION MOTOR AND BENCHMARKING

3.1.1. Electric Traction Motor Types

3.1.2. Summary of Traction Motor Types

3.1.3. Benchmarking Electric Traction Motors

3.1.4. Peak vs Continuous Properties

3.1.5. Peak vs Continuous Performance Benchmarking of 101 Motors: Power

3.1.6. Peak vs Continuous Performance Benchmarking of 65 Motors: Torque

3.1.7. Efficiency

3.1.8. Brushless DC Motors (BLDC): Working Principle

3.1.9. BLDC Motors: Advantages, Disadvantages

3.1.10. BLDC Motors: Benchmarking Scores

3.1.11. Permanent Magnet Synchronous Motors (PMSM): Working Principle

3.1.12. PMSM: Advantages, Disadvantages

3.1.13. PMSM: Benchmarking Scores

3.1.14. Differences Between PMSM and BLDC

3.1.15. Wound Rotor Synchronous Motor (WRSM): Working Principle

3.1.16. Renault's Magnet Free Motor

3.1.17. Rotor Power Transfer: Brushes vs Wireless

3.1.18. WRSM Motors: Benchmarking Scores

3.1.19. WRSM: Advantages, Disadvantages

3.1.20. AC Induction Motors (ACIM): Working Principle

3.1.21. AC Induction Motor (ACIM)

3.1.22. AC Induction Motors: Benchmarking Scores

3.1.23. AC Induction Motor: Advantages, Disadvantages

3.1.24. Reluctance Motors

3.1.25. Reluctance Motor: Working Principle

3.1.26. Switched Reluctance Motor (SRM)

3.1.27. Switched Reluctance Motors: Benchmarking Scores

3.1.28. Permanent Magnet Assisted Reluctance (PMAR)

3.1.29. PMAR Motors: Benchmarking Scores

3.1.30. Contributions from Reluctance and Interaction Torque

3.1.31. Regeneration

3.2. Electric Traction Motors: Summary and Benchmarking Results

3.2.1. Comparison of Traction Motor Construction and Merits

3.2.2. Motor Efficiency Comparison

3.2.3. Benchmarking Electric Traction Motors

3.2.4. Multiple Motors: Explained

4. MOTOR MARKET IN ELECTRIC CARS

4.1. BEV and PHEV Motor Type Market Share by Region 2015-2024

4.2. Convergence on PM Motors by Major Automakers

4.3. Motor Type Market Share Forecast 2015-2036

4.4. Commentary on Electric Traction Motor Trends in Cars

4.5. Automotive Electric Motor Forecast 2015-2036 (units, regional)

4.6. Automotive Electric Motor Forecast 2015-2036 (units, drivetrain)

4.7. Automotive Electric Motor Forecast 2015-2036 (units, motor type)

4.8. Automotive Electric Motor Power Forecast 2015-2036 (kW, regional)

4.9. Automotive Electric Motor Power Forecast 2015-2036 (kW, drivetrain)

4.10. Automotive Electric Motor Value Forecast 2021-2036 (US$, drivetrain)

5. MICROMOBILITY

5.1. Introduction to Micro EVs

5.2. Micro EV Types

5.3. Comparison of Micro EV Segments

5.4. Asia as the Home of the Three-Wheeler

5.5. Electric Two-wheeler Classification

5.6. Electric Two-wheelers: Power Classes

5.7. Motor Technologies in Two-wheelers

5.8. Indian Electric Two-wheeler OEMs

5.9. Electric Two-Wheelers Power by Region

5.10. Electric Two-Wheelers Motor Power

5.11. The Role of Three-Wheelers

5.12. Three-Wheeler Classification

5.13. China and India: Major Three-wheeler Markets

5.14. India E3W Example Models

5.15. Chinese E3W Example Models

5.16. Three-Wheelers Outside China & India

5.17. eAxles for 3 Wheelers

5.18. Microcars: The Goldilocks of Urban EVs

5.19. Examples of Microcars by Region

5.20. Motors in Electric Three-Wheelers and Microcars

5.21. Types of Motors in Micro EVs

5.22. Hub Motors vs. Mid-Drive Motors

5.23. Micromobility Motor Manufacturers

5.24. Micro-EV Motor Forecast 2023-2036 (units, vehicle type)

5.25. Micromobility Research

6. ELECTRIC LIGHT COMMERCIAL VEHICLES (ELCV)

6.1. Introduction to Electric LCVs

6.2. Light Commercial Vehicles (LCVs)

6.3. IDTechEx LCV Segmentation

6.4. Regional LCV Sales

6.5. Electric LCVs: Drivers and Barriers

6.6. Specifications of Popular Electric LCVs in Europe

6.7. Specifications of Popular Electric LCVs in China

6.8. Motors Used in eLCVs

6.9. Evolution of Motor Power

6.10. eLCV Motors Match ICE Performance

6.11. PM Motors Are Dominant Worldwide

6.12. Known Tier 1 Relationships for eLCVs

6.13. OEMs Moving Motor Development In-House

6.14. LCV Electric Motor Forecast 2021-2036 (units, drivetrain)

6.15. Light Commercial Vehicle Research

7. ELECTRIC TRUCKS

7.1. Trucks are Capital Goods

7.2. Zero Emission Trucks: Drivers and Barriers

7.3. Regional Model Availability 2021-2024

7.4. BEV and FCEV M&HD Trucks: Weight vs Motor Power

7.5. Medium Duty Truck Models Motor Power

7.6. Heavy Duty Truck Models Motor Power

7.7. Truck Motor Type Market Share and Power Output Requirements

7.8. Integrated e-Axle Space Advantage

7.9. AVL

7.10. Allison Transmission eGen Power e-Axles

7.11. BorgWarner

7.12. Dana E-Axles

7.13. Dana TM4

7.14. Danfoss Editron

7.15. Detroit eAxles

7.16. FPT Truck Motors

7.17. Accelera eAxles

7.18. Linamar Corporation eAxles

7.19. Meritor 14Xe Electric Drivetrain

7.20. Volvo Driveline

7.21. ZF Central Drive

7.22. Truck Electric Motor Forecast 2021-2036 (units, drivetrain & category)

7.23. Electric Truck Research

8. ELECTRIC BUSES

8.1. Bus Categories and Electrification

8.2. Overview of Bus Types and Specific Challenges to Electrification

8.3. Options for Reduced Emissions Buses

8.4. Electric Buses - a Global Outlook

8.5. Motor Mounting - Central or Axle Mounted

8.6. Electric Bus Motor Types

8.7. Motor Benchmarking and Metrics for Buses

8.8. Traction Motors of Choice for Electric Buses

8.9. Motor Suppliers - Overview

8.10. Convergence on PM

8.11. Motor OEM Supply Relationships

8.12. Dana TM4

8.13. Equipmake - Motors for Retrofitting

8.14. Siemens/Cummins ACCELERA

8.15. Traktionssysteme Austria (TSA)

8.16. Voith

8.17. Voith - Central Motors Only

8.18. ZF Group - AxTrax and CeTrax

8.19. ZF Group - New AxTrax and CeTrax Shift to PM Motors

8.20. Volvo Electric Buses

8.21. Bus Electric Motor Forecast 2021-2036 (units, drivetrain)

8.22. Electric Bus Research

9. HEV DRIVE TECHNOLOGY

9.1. HEV Car Manufacturers

9.2. Hybrid Synergy Drive/ Toyota Hybrid System

9.3. Hybrid Synergy Drive/ Toyota Hybrid System

9.4. Honda

9.5. Honda's 2 Motor Hybrid System

9.6. Nissan Note e-POWER

9.7. Hyundai Sonata Hybrid

9.8. Toyota Prius Drive Motor: 2004-2010

9.9. Toyota Prius Drive Motor: 2004-2017

9.10. Comparison of Hybrid MGs

9.11. Global HEV Car Motor/Generator Trends

9.12. HEV Car MGs Trends and Assumptions

9.13. Global HEV Car MG Demand Forecast 2015-2036 (units, kW)

9.14. High Voltage Hybrid Electric Vehicle Research

10. ELECTRIC AVIATION

10.1. eVTOL Motor Requirements

10.1.1. eVTOL Motor / Powertrain Requirements

10.1.2. eVTOL Aircraft Motor Power Sizing

10.1.3. eVTOL Power Requirement: kW Estimate

10.1.4. eVTOL Power Requirement

10.1.5. eVTOL Power Requirement: kW Estimate

10.1.6. Electric Motors and Distributed Electric Propulsion

10.1.7. eVTOL Number of Electric Motors

10.1.8. Motor Sizing

10.2. eCTOL Motor Requirements

10.2.1. eCTOL Motor / Powertrain Requirements

10.2.2. Overview of Plane Types Energy and Power Requirements

10.2.3. Typical Airplane Engines

10.2.4. Airplane Engines Power and Weight

10.2.5. Turbofan Power Estimations

10.2.6. Electric Motors and Distributed Electric Propulsion

10.2.7. Challenges in Building a 100MW Electric Propulsion Unit

10.3. Electric Motors for Aviation: Players

10.3.1. Ascendance

10.3.2. Airbus and Toshiba: superconducting engine

10.3.3. Collins - Aerospace Suppliers Working on Motor Products

10.3.4. Duxion is Reinventing the Motor to Replace Turbofans

10.3.5. EMRAX

10.3.6. ePropelled

10.3.7. Evolito

10.3.8. H3X

10.3.9. MAGicALL

10.3.10. magniX

10.3.11. MGM COMPRO

10.3.12. Nidec Aerospace

10.3.13. Rolls-Royce / Siemens

10.3.14. Rolls-Royce / Siemens

10.3.15. SAFRAN

10.3.16. Wright Electric's High Power-to-Weight Motor

10.3.17. ZeroAvia

10.3.18. Other Player Examples

10.3.19. Power Density Comparison: Motors for Aviation

10.3.20. Torque Density Comparison: Motors for Aviation

10.3.21. eCTOL and eVTOL Research

11. EMERGING MOTOR TECHNOLOGIES

11.1. Axial Flux Motors

11.1.1. Radial Flux Motors

11.1.2. Axial Flux Motors

11.1.3. Radial Flux vs Axial Flux Motors

11.1.4. Yoked vs Yokeless Axial Flux

11.1.5. Challenges with Axial Flux Thermal Management

11.1.6. List of Axial Flux Motor Players

11.1.7. Beyond Motors

11.1.8. AVID Acquired by Turntide

11.1.9. EMRAX

11.1.10. Elemental Motors

11.1.11. Emil Motors

11.1.12. Infinitum Electric: Printed PCB Stator

11.1.13. Lamborghini

11.1.14. Koenigsegg - raxial flux

11.1.15. Magnax

11.1.16. Traxial (a Magnax company)

11.1.17. Magelec Propulsion

11.1.18. Saietta

11.1.19. Tresa Motors

11.1.20. WHYLOT

11.1.21. WHYLOT and Renault

11.1.22. YASA Axial Flux Motors

11.1.23. YASA and Koenigsegg

11.1.24. YASA and Ferrari

11.1.25. Lamborghini 634 - V8 with Axial Flux

11.1.26. Daimler Acquires YASA

11.1.27. Mercedes Vision One Eleven Concept

11.1.28. China's Growing Axial Flux Presence

11.1.29. Commercial Axial Flux Motors Power and Torque Density Benchmark

11.1.30. Player Benchmark of Axial Flux Motors Power and Torque Density

11.1.31. Automotive Axial Flux Motor Forecast 2021-2036 (units)

11.2. In-wheel Motors

11.2.1. In-wheel Motors

11.2.2. Risks and Opportunities for In-wheel Motors

11.2.3. Risks and Opportunities for In-wheel Motors

11.2.4. Risks and Opportunities for In-wheel Motors

11.2.5. Conifer

11.2.6. DeepDrive

11.2.7. Donut Lab

11.2.8. Elaphe

11.2.9. Ferrari

11.2.10. Gem Motors

11.2.11. Hitachi

11.2.12. Hyundai Mobis

11.2.13. Nidec

11.2.14. Orbis Electric

11.2.15. Protean Electric

11.2.16. REE Automotive

11.2.17. Renault and Alpine Using In-wheel Motors

11.2.18. VW Considering In-wheel?

11.2.19. Schaeffler

11.2.20. Examples of Vehicles with In-wheel Motors

11.3. Axial Flux for In-wheel Motors

11.3.1. In-wheel Motors Production Forecast 2021-2036 (units)

11.3.2. Axial Flux and In-wheel Motors Benchmarking Against BEV Motors

11.3.3. Motor Type Power Density Benchmark

11.3.4. Motor Type Torque Density Benchmark

11.3.5. Average and Range of Power and Torque Density by Motor Type

11.3.6. Max Speed and Power Density

11.4. Overcoming Issues with Switched Reluctance Motors

11.4.1. Switched Reluctance Motor (SRM)

11.4.2. No Permanent Magnets for SRMs

11.4.3. Advanced Electric Machines (AEM): Commercial Vehicles

11.4.4. AEM and Bentley

11.4.5. Enedym

11.4.6. RETORQ Motors

11.4.7. Punch Powertrain

11.4.8. Turntide Technologies

11.4.9. Switched Reluctance Players for EVs

11.5. Other Manufacturing Developments

11.5.1. Future Technologies for Motor Production

11.5.2. Segmented Stators

11.5.3. Screen Printing Motor Laminations

11.5.4. Adding Graphene to Copper Windings

12. MATERIALS FOR ELECTRIC MOTORS

12.1.1. Which Materials are Required for Electric Motors?

12.2. Materials for Permanent Magnets

12.2.1. Magnetic Material Distribution in Rotors

12.2.2. ID4 vs Leaf vs Model 3 Rotors

12.2.3. Magnet Composition for Motors

12.2.4. Mining of Rare-Earth Metals

12.2.5. Regional market share of rare earth mining, processing, metallization, and magnet production

12.2.6. Historical price volatility and recent technology and material export restrictions fuel rare earth supply uncertainty

12.2.7. Rare Earth Magnets Supply Chain and Market

12.2.8. Volatility of EV Motor Materials

12.2.9. The Market Drive to Eliminate Rare Earths

12.2.10. Soft Magnetic Materials for High Performance Motors

12.3. Rare Earth Reduction and Elimination

12.3.1. Europe's Move to Magnet Free Designs

12.3.2. Key Magnetic Properties and Challenges with Rare Earth Free Magnets

12.3.3. Rare earth magnets outperform competing technologies on most metrics

12.3.4. Tesla's Next Generation Motor

12.3.5. How Tesla Could Eliminate Rare-earths (1)

12.3.6. How Tesla Could Eliminate Rare-earths (2)

12.3.7. How Tesla Could Eliminate Rare-earths (3)

12.3.8. Rare Earth Reduction Progress in Japan

12.3.9. Motor Design to Reduce Rare Earths

12.3.10. India Moving from Rare Earths

12.3.11. Alternative Magnetic Materials

12.3.12. Alternative Magnetic Materials

12.3.13. Toyota's Neodymium Reduced Magnet

12.3.14. Niron Magnetics

12.3.15. Niron Funding and Partnerships

12.3.16. PASSENGER Rare Earth Free Magnets

12.3.17. Ferrite Performance vs Neodymium in Motors

12.3.18. Ferrite Performance vs Neodymium

12.3.19. Recycling Rare Earths

12.3.20. OEM & Tier 1 Approaches to Eliminate Rare Earths

12.4. Rotor and Stator Windings

12.4.1. Aluminium vs Copper in Rotors

12.4.2. Round Wire vs Hairpins for Copper in Stators

12.4.3. Round Wire vs Hairpin vs Continuous Winding

12.4.4. Evolution of Motor Windings

12.4.5. The Many Types of Square Winding

12.4.6. Wave Winding

12.4.7. MG Motors (SAIC)

12.4.8. VW's MEB

12.4.9. Tesla

12.4.10. Round vs Hairpin Windings: OEMs

12.4.11. BEV Motor Stator Copper Content Benchmarking

12.4.12. Hairpin Winding Regional Market Shares

12.4.13. A New Winding Format?

12.4.14. Aluminum vs Copper Windings

12.4.15. Compressed Aluminum Windings

12.4.16. Aluminum Windings: Players

12.5. Motor Materials Environmental Impact and Forecasts

12.5.1. Environmental Impact Introduction

12.5.2. Environmental Impact of Materials

12.5.3. Material Intensity for BEV Motors

12.5.4. Environmental Impact of Several BEV Motors

12.5.5. Materials in Rare Earth Motor Magnets Forecast 2021-2036 (kg)

12.5.6. Rare Earth vs Rare Earth Free Magnet Material Forecast 2021-2036 (kg)

12.5.7. Materials in Electric Motors Forecast 2021-2036 (kg)

13. THERMAL MANAGEMENT OF ELECTRIC MOTORS

13.1.1. Cooling Electric Motors

13.2. Motor Cooling Strategies

13.2.1. Air Cooling

13.2.2. Water-glycol Cooling

13.2.3. Oil Cooling

13.2.4. Electric Motor Thermal Management Overview

13.2.5. Motor Cooling Strategy by Power

13.2.6. Cooling Strategy by Motor Type

13.2.7. Cooling Technology: OEM strategies

13.2.8. Motor Cooling Strategy by Region (2015-2024)

13.2.9. Motor Cooling Strategy Market Share (2015-2024)

13.2.10. Motor Cooling Strategy Forecast 2015-2036 (units)

13.2.11. Alternate Cooling Structures

13.2.12. Cooling Through the Windings

13.2.13. Refrigerant Cooling

13.2.14. Two-phase Cooling in an Electric Motor (1)

13.2.15. Two-phase Cooling in an Electric Motor (2)

13.2.16. Immersion Cooling

13.2.17. Phase Change Materials

13.2.18. Reducing Heavy Rare Earths Through Thermal Management

13.3. Motor Insulation and Encapsulation

13.3.1. Impregnation and Encapsulation

13.3.2. Potting and Encapsulation: Players

13.3.3. Challenges Insulating 800V Motors

13.3.4. PPSU as a PEEK Alternative

13.3.5. Benefits of PEEK and PAEK

13.3.6. Axalta - Motor Insulation

13.3.7. Eaton - Nanocomposite PEEK Insulation

13.3.8. Elantas - Insulation Systems for 800V Motors

13.3.9. SABIC - 800V Motor Insulation

13.3.10. Solvay - PEEK Insulation

13.3.11. Insulating Hairpin Windings

13.4. PEEK Motor Insulation

13.4.1. Benefits of PEEK and PAEK

13.4.2. Bekaert - PEEK Insulation

13.4.3. Eaton - Nanocomposite PEEK Insulation

13.4.4. Solvay - PEEK Insulation

13.4.5. Syensqo PEEK Motor Insulation

13.4.6. Victrex - PEEK Motor Insulation

13.4.7. When Should PEEK be Used?

14. EV MOTORS: OEM USE-CASES AND SUPPLY PARTNERSHIPS

14.1.1. OEM and Tier 1 Supply Relationships (1)

14.1.2. OEM and Tier 1 Supply Relationships (2)

14.1.3. OEMs Moving to In-house Motor Development

14.2. Motor Examples

14.2.1. Aston Martin Valhalla (1)

14.2.2. Aston Martin Valhalla (2)

14.2.3. Audi e-tron

14.2.4. Audi e-tron

14.2.5. Audi Q4 e-tron

14.2.6. Audi Premium Platform Electric (PPE)

14.2.7. BMW i3 2016

14.2.8. BMW 5th Gen Drive (Jaguar)

14.2.9. BMW 6th Gen

14.2.10. BYD e-Platform 3.0

14.2.11. BYD >30,000rpm motor

14.2.12. Chara Technologies

14.2.13. Chevrolet Bolt Onwards (LG)

14.2.14. Equipmake

14.2.15. Ford Mustang Mach-E (BorgWarner and Magna)

14.2.16. GAC

14.2.17. GM Ultium Drive

14.2.18. Huawei

14.2.19. Hyundai E-GMP (BorgWarner)

14.2.20. IAV: Two-phase Cooling in an Electric Motor (1)

14.2.21. IAV: Two-phase Cooling in an Electric Motor (2)

14.2.22. InfiMotion

14.2.23. Jaguar I-PACE (AAM)

14.2.24. Lordstown Motors (Elaphe)

14.2.25. Lucid Air

14.2.26. IRP Systems

14.2.27. Magna's Latest eDrive

14.2.28. Mercedes EQ

14.2.29. Mercedes CLA

14.2.30. Nidec - Gen.2 drive

14.2.31. Nissan Ariya

14.2.32. Nissan Leaf

14.2.33. Porsche Taycan

14.2.34. Ricardo Rare Earth Free Drive Unit

14.2.35. Rimac Technology Drive Units

14.2.36. Rivian

14.2.37. Rivian In-house Motors

14.2.38. SAIC - Oil cooling system

14.2.39. Stellantis Shared Platform (Npe)

14.2.40. Tesla Induction Motor

14.2.41. Tesla PM Motor

14.2.42. Tesla's Carbon Wrapped Motor

14.2.43. Tesla Cybertruck

14.2.44. Toyota Prius 2004 to 2010

14.2.45. UAES (Bosch)

14.2.46. Volvo's Motor Development

14.2.47. VW ID3/ID4

14.2.48. VW APP550

14.2.49. Zero Z-Force Powertrain

14.2.50. ZF

14.2.51. ZF SELECT Platform (1)

14.2.52. ZF SELECT Platform (2)

14.3. Tier 1 Wound Rotor Synchronous Motors/Externally Excited Synchronous Motors

14.3.1. BorgWarner's EESM Development

14.3.2. MAHLE

14.3.3. Schaeffler Wound Rotor Design

14.3.4. Vitesco

14.3.5. ZF

14.4. Supply Relationships

14.4.1. Commercial Vehicle OEM and Tier 1 Supply Relationships (1)

14.4.2. Commercial Vehicle OEM and Tier 1 Supply Relationships (2)

14.4.3. Allison Transmission - Anadolu Isuzu

14.4.4. Aisin Seiki, DENSO and Toyota Motor form BluE Nexus

14.4.5. BorgWarner Partnerships and Acquisitions (1)

14.4.6. BorgWarner Partnerships and Acquisitions (2)

14.4.7. Bosch

14.4.8. Continental

14.4.9. Dana Supply Relationships and Announcements

14.4.10. GKN Automotive

14.4.11. Lucid Supply Partnerships

14.4.12. Hitachi

14.4.13. Horse Powertrain

14.4.14. LG Electronics and Magna

14.4.15. Magna and Mercedes

14.4.16. Nidec

14.4.17. Mavel

14.4.18. Schaeffler

14.4.19. Valeo

14.4.20. Vitesco Technologies

14.4.21. Vitesco and Schaeffler Merger

14.4.22. Yamaha - Hypercar Electric Motor

14.4.23. ZF

15. EV MOTORS: OEM BENCHMARKING

15.1. Automotive

15.1.1. BEV Power Density Benchmarking

15.1.2. BEV Torque Density Benchmarking

15.1.3. BEV Power and Torque Density Benchmark

15.1.4. EV Drive Unit Specification Summary

15.2. Commercial Vehicles

15.2.1. Commercial Vehicle Motors Power Density Benchmarking

15.2.2. Commercial Vehicle Motors Torque Density Benchmarking

15.2.3. Commercial Vehicle Motors Power and Torque Density Benchmark

15.2.4. Commercial Vehicle Motor Specification Summary

15.3. Light Duty

15.3.1. Light Duty Vehicle Motors Power Density Benchmarking

15.3.2. Light Duty Vehicle Motors Torque Density Benchmarking

15.3.3. Light Duty Vehicle Motor Specification Summary

15.4. eAxles for Commercial Vehicles

15.4.1. eAxle for Commercial Vehicle Benchmarking: Torque and GAWR

15.4.2. eAxle for Commercial Vehicle Benchmarking: Power and Torque

15.4.3. eAxle Specification Summary

16. FORECASTS AND ASSUMPTIONS

16.1. Forecast Methodology & Assumptions

16.2. Motor Price Forecast and Assumptions

16.3. Average Motor Power 2024 by Vehicle Category (kW)

16.4. Motor per Vehicle and kW per Vehicle Assumptions

16.5. Automotive Electric Motor Forecast 2015-2036 (units, regional)

16.6. Automotive Electric Motor Forecast 2015-2036 (units, drivetrain)

16.7. Automotive Electric Motor Forecast 2015-2036 (units, motor type)

16.8. Automotive Electric Motor Power Forecast 2015-2036 (kW, regional)

16.9. Automotive Electric Motor Power Forecast 2015-2036 (kW, drivetrain)

16.10. Automotive Electric Motor Value Forecast 2021-2036 (US$, drivetrain)

16.11. Micro-EV Motor Forecast 2023-2036 (units, vehicle type)

16.12. LCV Electric Motor Forecast 2021-2036 (units, drivetrain)

16.13. Truck Electric Motor Forecast 2021-2036 (units, drivetrain & category)

16.14. Bus Electric Motor Forecast 2021-2036 (units, drivetrain)

16.15. Global HEV Car MG Demand Forecast 2015-2036 (units, kW)

16.16. Automotive Axial Flux Motor Forecast 2021-2036 (units)

16.17. In-wheel Motors Production Forecast 2021-2036 (units)

16.18. Materials in Rare Earth Motor Magnets Forecast 2021-2036 (kg)

16.19. Rare Earth vs Rare Earth Free Magnet Material Forecast 2021-2036 (kg)

16.20. Materials in Electric Motors Forecast 2021-2036 (kg)

16.21. Automotive Motor Cooling Strategy Forecast 2015-2036 (units)

16.22. Total Motors Forecast by Vehicle and Drivetrain 2021-2036 (units)

16.23. Total Motor Power Forecast by Vehicle and Drivetrain 2021-2036 (kW)

16.24. Total Motor Market Size Forecast by Vehicle and Drivetrain 2021-2036 (US$ billions)

17. COMPANY PROFILES

17.1. Advanced Electric Machines: Rare Earth Free Motors

17.2. Allison Transmission: eAxles for Commercial Vehicles

17.3. AVID Technology

17.4. Axalta Coating Systems: Electric Motor Insulation

17.5. Beyond Motors: Axial Flux Motors

17.6. Carpenter Electrification: Soft Magnetic Materials for Motors

17.7. DELO: Adhesives for Automotive Components

17.8. Eaton Research Laboratories: Electric Motor Insulation

17.9. Elaphe (2021)

17.10. ePropelled: Dynamic Torque-switching Electric Motor

17.11. Equipmake: Electric Motors and Power Electronics

17.12. EVR Motors

17.13. Infinitum Electric: Axial Flux Motor with Printed Stator

17.14. Infinitum Electric: PCB Stator Axial Flux Motor

17.15. Magnax

17.16. Modal Motors

17.17. Monumo: AI Motor Design

17.18. Monumo: Artificial Intelligence for Motor Development

17.19. Niron Magnetics: Rare Earth Free Permanent Magnets

17.20. Protean Electric

17.21. RETORQ Motors

17.22. Saietta Electric Drive: axial flux motors

17.23. Schaeffler: Magnet Free Motors

17.24. Traxial (a Magnax Company)

17.25. Ultimate Transmissions: How Tesla Could Avoid Rare-Earth Magnets

17.26. Ultimate Transmissions: Thermal Management of Electric Motors

17.27. Victrex

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|