炭素回収・利用・貯留(CCUS)市場2026-2036:技術、市場予測、参入企業Carbon Capture, Utilization, and Storage (CCUS) Markets 2026-2036: Technologies, Market Forecasts, and Players CCUS市場の見通し、10年間の詳細予測、企業プロファイル、主要セクターのポイントソース炭素回収、直接空気回収(DAC)、CO2輸送・貯留(T&S)、CO2利用技術評価 炭素回収・利用・貯留(CCU... もっと見る

サマリー

CCUS市場の見通し、10年間の詳細予測、企業プロファイル、主要セクターのポイントソース炭素回収、直接空気回収(DAC)、CO2輸送・貯留(T&S)、CO2利用技術評価

炭素回収・利用・貯留(CCUS)技術は、排ガスから、あるいは大気から直接CO2を回収する。この回収された二酸化炭素は、恒久的に貯蔵されるか、収益を生み出すために利用される。各国政府は、CCUSが産業の脱炭素化と廃棄物CO2の価値化に果たす役割を認識し、カーボンプライシング、税額控除、補助金などを通じて、CCUSに有利な政策環境を作り続けている。石油・ガス会社がCO2輸送・貯蔵サービスの提供に軸足を移し、データセンターのハイパースケーラーが直接大気回収(DAC)や生物起源CCUS(BECCS)から得られる炭素クレジットの市場を創出するなど、民間セクターの重要な役割が明らかになりつつある。

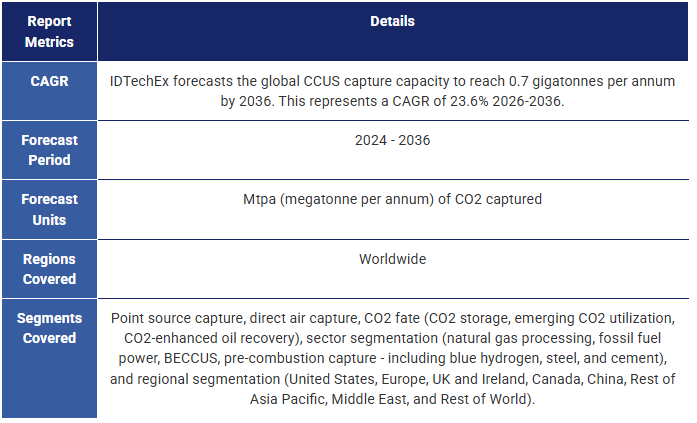

「炭素回収・利用・貯留(CCUS)市場2026-2036:技術、市場予測、プレーヤー」は、新興CCUS産業と炭素市場の包括的な展望を提供し、今後10年間のCCUS産業を形成する技術的、経済的、規制的、環境的側面を詳細に分析する。炭素回収、炭素利用、炭素貯蔵技術を評価し、各分野における最新の進歩、主要プレーヤー、機会と障壁について論じている。また、CCUSの炭素回収能力に関する2036年までの10年間のきめ細かな予測(CO2エンドポイント、ポイントソース対DAC、産業部門、地域別にセグメント化)を、独占分析、60のインタビューに基づく企業プロフィール、350社以上の企業取材とともに掲載している。

CCUS市場の加速は2025年に入っても続いており、ノーザンライツT&SやストラトスDACなど、注目すべき世界初のプロジェクトが始動している。CCUSプロジェクトのパイプラインは膨らみ続けており、2025年時点で5,000万トンの新規生産能力が建設中である。このIDTechExレポートは、CCUSのビジネスモデル、経済性、主要/新興の捕捉技術の概要を提供している。

ビジネスモデル

新規の大規模CCUS 設備を稼動させるには、通常、税額控除や政府補助金が必要である。主な例としては、米国の45Q税額控除(最近、トランプ政権の「ビッグ・ビューティフル・ビル」で二酸化炭素の利用が促進された)や、英国政府が産業用CCUSクラスターに200億ポンドの資金拠出を発表したことなどが挙げられる。コンプライアンス炭素市場メカニズムが、最終的にCCUSを長期的に可能にすると期待されている。2025年時点では、世界のCO2排出量の28%が何らかの炭素価格設定によってカバーされており、2026年には欧州連合(EU)のCBAM(炭素国境調整メカニズム)が登場し、新たな炭素市場開発の動機付けとなる。

さらに、新しい部分的チェーンCCUSハブ、クラスター、ネットワークは、規模の経済を解き放ち、CCUS開発をデボトルネックにする。CO2輸送とCO2貯蔵インフラを共有することで、この新しいCCUSビジネスモデルはCCUSプロジェクト開発を合理化する。

点源捕捉技術の開発

点源炭素捕捉のためのアミン系溶剤は技術的に成熟しているが、脱混合溶剤や水溶性溶剤のような革新的な溶剤の商業化が続いている。このIDTechExのレポートには、吸収塔/ストリッパーカラムにおける物質移動を改善するための進歩を含む、アミン溶剤による炭素回収のプラントバランスに関する考察も含まれている。

アミン系溶媒以外にも、炭素回収の分野では新興企業が溶融ホウ酸塩、促進輸送膜、溶融炭酸塩燃料電池、極低温アプローチなど幅広い技術を追求している。これらの技術は最終的に、回収に必要なエネルギー需要の削減を目指している。本レポートでは、IDTechExが主要な炭素回収プレーヤーを特定し、回収技術をベンチマークしている。

地域別CCUS市場予測

米国は、45Q税額控除支援とCO2-EOR(石油増進回収法)の強力な歴史により、CCUSの世界的リーダーである。欧州、中国、カナダ、英国を含む他の地域も、CCUSの世界的なスケールアップに貢献するだろう。例えば、EUの最近のネット・ゼロ産業法は、2030年までに少なくとも5,000万トンの年間CO2永久貯蔵容量を義務付けている。このIDTechExレポートには、CCUS市場の地域別予測が含まれており、地域によるCCUS成長の違いを示している。

本レポートで扱う主な質問

主要な側面

本レポートは以下の情報を提供する

技術と市場分析

プレーヤー分析と動向

市場予測と分析

目次1.要旨

1.1.炭素回収・利用・貯留(CCUS)とは何か?

1.2.なぜCCUSなのか、なぜ今なのか?

1.3.CCUSビジネスモデルの概要CO2からの価値

1.4.CCSビジネスモデルの開発

1.5.CCUSのビジネスモデル:ネットワークとハブモデル

1.6.CCUSビジネスモデルパーシャルチェーン

1.7.稼働中及び建設中の大規模専用CO2貯留サイトの世界地図

1.8.二酸化炭素貯留タイプの成熟度とオペレーターの状況

1.9.CO2増進回収油市場

1.10.カーボンプライシングと炭素市場

1.11.世界のコンプライアンス・カーボンプライシングメカニズム

1.12.米国におけるカーボンプライシングの代替案:45Q税額控除

1.13.CO₂エンドポイント別CCUS予測-貯留と増進回収

1.14.なぜCO2利用なのか?

1.15.CO2U製品の現在の規模

1.16.主なCO2回収システム

1.17.最も成熟している炭素回収技術は?

1.18.どのような場合に異なる炭素回収技術を使用すべきか?

1.19.ポイントソースの炭素回収技術プロバイダー

1.20.高濃度CO2発生源は低空飛行の果実である

1.21.CO2発生源セクター別のポイントソースCCUS回収能力予測(Mtpa of CO2)

1.22.主要DAC企業

1.23.直接空気回収を拡大するための主な課題は何か?

1.24.CCUSの機運が高まっている

1.25.地域別CCUS回収能力-北米

1.26.CO2輸送の概要

1.27.IDTechEx サブスクリプションでさらにアクセス

2.序論

2.1.炭素回収・利用・貯留(CCUS)とは何か?

2.2.CCUSのバリューチェーン

2.3.なぜCCUSなのか、なぜ今なのか?

2.4.炭素回収

2.5.回収コスト削減への道

2.6.CO2貯蔵

2.7.CCSビジネスモデルの開発

2.8.なぜCO2利用なのか?

2.9.CO2輸送

2.10.CCUSのコストは?

2.11.CCUSはいつネットゼロと言えるのか?

2.12.CCUS市場の課題

2.13.大規模なCCUSの実現

3.CCUSのビジネスモデル

3.1.はじめに

3.1.1.CCUSビジネスモデルの概要CO2からの価値

3.1.2.CCSビジネスモデルの発展

3.1.3.CCSに対する政府の資金支援メカニズム

3.1.4.CCSプロジェクトの政府所有権は国によって異なる

3.1.5.CCUSのビジネスモデル:フルチェーン

3.1.6.CCUSのビジネスモデル:ネットワークとハブモデル

3.1.7.CCUSビジネスモデル:パーシャルチェーン

3.1.8.二酸化炭素利用ビジネスモデル

3.2.炭素価格と炭素市場

3.2.1.炭素価格と炭素市場

3.2.2.世界のコンプライアンス・カーボンプライシングメカニズム

3.2.3.世界のカーボンプライシングメカニズムにおけるCO2価格とは?

3.2.4.欧州連合排出量取引制度(EU ETS)

3.2.5.EU ETSは影響を与えたか?

3.2.6.EU ETSがCCUSをサポートするためには、どのような変更が必要か?

3.2.7.EUカーボン・ボーダー調整メカニズム(CBAM)

3.2.8.EUのCBAMは国際的に最初のものとなる

3.2.9.米国におけるカーボンプライシングの代替案:45Q税額控除

3.2.10.CCUSを支える自主的炭素市場の役割

3.2.11.CCSを支援するためには、どれくらいの炭素価格設定が必要か?

4.CCS産業の現状

4.1.CCUSの機運は高まっている

4.2.2024/2025年におけるCCUSのマイルストーン

4.3.建設・発表された炭素回収施設の世界的パイプライン

4.4.CCUS開発の分析

4.5.CO2発生源:歴史的にどのセクターからCO2が回収されてきたか?

4.6.CCUSが最も成長するセクターは?

4.7.CO2の運命:回収されたCO2はどこへ行くのか?

4.8.CCUSプロジェクトの地域分析

4.9.CCUSの主要プレーヤー

4.10.CCUSプロジェクトの実績-天然ガス処理

4.11.CCUSプロジェクトの実績-天然ガス処理

4.12.CCUSプロジェクトの実績-発電

4.13.CCUSプロジェクトの実績 - 重要なポイント

4.14.バウンダリー・ダム - 捕捉技術問題との戦い

4.15.ペトラ・ノヴァの長期操業停止:業界の教訓?

4.16.CCUSのコストは?

4.17.大規模CCUSプロジェクトのコストと資金調達

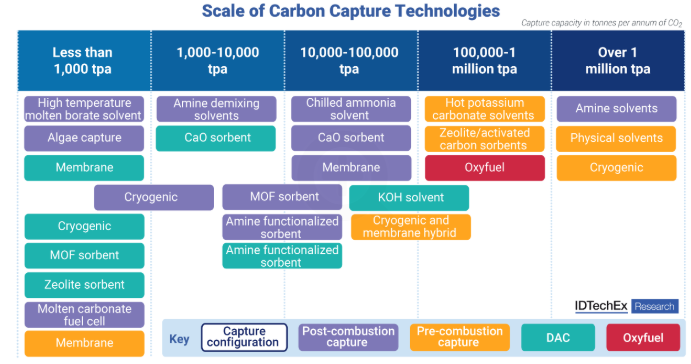

5. 炭素回収技術

5.1.はじめに

5.11.1.CCUSのバリューチェーン

5.11.2.主なCO2回収システム

5.11.3.点源炭素回収の現状

5.11.4.天然ガスのスイートニング

5.11.5.燃焼後CO2回収

5.11.6.燃焼前CO2回収

5.11.7.酸素燃焼によるCO2回収

5.11.8.主なCO2回収技術

5.11.9.CO2回収技術の比較

5.11.10.炭素回収技術の成熟度-概要

5.11.11.最も成熟している炭素回収技術は?

5.11.12.異なる炭素回収技術をいつ使うべきか?

5.11.13.様々な回収技術の典型的な条件と性能

5.11.14.CO₂濃度と分圧は排出源によって異なる

5.11.15.CO₂分圧はコストにどのように影響するか?

5.11.16.高濃度CO2排出源は低空飛行の果実である

5.11.17.単一の炭素回収技術が全ての用途で最良となることはない

5.11.18.既存の大規模プロジェクトにおける炭素回収技術プロバイダー

5.11.19.90%を超える回収率が現在の業界標準

5.11.20.CO2回収率とは何か?

5.11.21.90%以下のCO2回収率についてのケース作り

5.11.22.CO2回収コストへの貢献

5.11.23.CO2回収剤の指標

5.11.24.最先端技術:回収率

5.11.25.最新技術:エネルギー消費量

5.11.26.炭素回収技術の技術的準備状況(1/2)

5.11.27.炭素回収技術の技術的準備状況(2/2)

5.11.28.技術別のポイントソース炭素回収技術プロバイダー

5.2.炭素回収のための溶剤

5.12.1.溶剤ベースのCO₂回収

5.12.2.化学吸収溶剤

5.12.3.アミン系燃焼後CO₂吸収

5.12.4.炭素回収のためのアミン系溶剤の開発

5.12.5.アミン系溶剤の革新

5.12.6.アミン系溶剤はCCUSの主流だが課題は残る

5.12.7.燃焼後回収のためのアミン溶剤炭素回収技術プロバイダー (1/2)

5.12.8.燃焼後回収のためのアミン溶剤炭素回収技術プロバイダー(2/2)

5.12.9.ホット炭酸カリウム(HPC)プロセス

5.12.10.炭素回収のためのHPC炭素回収技術プロバイダー

5.12.11.現在稼働中のCCUS点源プロジェクトで使用されている化学吸収溶剤 (1/2)

5.12.12.現在稼働中のCCUS点源プロジェクトで使用されている化学吸収溶剤(2/2)

5.12.13.化学溶剤による燃焼後回収のコスト内訳

5.12.14.物理吸収溶剤

5.12.15.主な物理吸収溶剤の比較

5.12.16.現在稼働中のCCUS点源プロジェクトで使われている物理溶剤

5.12.17.どのような場合に溶剤ベースの炭素回収を行うべきではないか?

5.3.アミン系溶剤による炭素回収のプラントバランス

5.3.1.アミン系溶剤による燃焼後炭素回収の紹介

5.3.2.炭素回収のプラントバランス(BoP)構成要素のまとめ

5.3.3.燃焼後炭素回収のための排ガス前処理/前処理

5.3.4.バブコック&ウィルコックス排ガス前処理ポートフォリオ

5.3.5.アミン溶剤ベースの炭素回収用吸収塔

5.3.6.アミン溶剤ベースの炭素捕捉用吸収塔構造パッキン

5.3.7.吸収塔用構造化充填剤の材料革新

5.3.8.炭素回収プラントにおける水の使用

5.3.9.吸収塔/ストリッパーの革新:回転充填床

5.3.10.ハイブリッドプロセス:膜コンタクター

5.3.11.主な熱交換器リーン/リッチアミン熱交換器

5.3.12.補助熱交換器

5.3.13.炭素回収用熱交換器の技術提供者

5.3.14.リボイラー負荷低減の革新

5.3.15.大規模 CO2 圧縮技術

5.3.16.CO2 圧縮コスト

5.3.17.BOPケーススタディ:イオンクリーンエナジー

5.3.18.地域別BOP技術のサプライチェーン

5.3.19.中国のCCUS向け設備と技術プロバイダー

5.3.20.燃焼後溶剤ベースの炭素回収における主要成分の高価値マトリックス

5.4.炭素回収のための新しい溶剤

5.4.1.企業展望:炭素回収用の新興溶剤

5.4.2.チルドアンモニアプロセス(CAP)

5.4.3.溶融ホウ酸塩

5.4.4.ポスト燃焼用途の化学吸着炭素回収溶剤の適用性

5.5.炭素回収のための吸着剤

5.5.1.固体吸着剤ベースのCO₂分離

5.5.2.圧力スイング吸着における吸着剤水素分離

5.5.3.圧力スイング吸着における吸着剤

5.5.4:炭素分離

5.5.4.炭素回収のために研究されている固体吸着剤の概要

5.5.5.ゼオライト系吸着剤

5.5.6.炭素系吸着剤

5.5.7.有機金属骨格(MOF)吸着剤

5.5.8.固体アミン系吸着剤

5.5.9.運用中のCCUS点源プロジェクトで使用されている固体吸着剤プロセス

5.5.10.炭素回収のための固体吸着材の概要

5.5.11.吸着強化型水ガスシフト(SEWGS)

5.6.膜ベースの炭素回収

5.6.1.脱炭素のためのガス分離膜の紹介

5.6.2.新しい膜材料の開発:主な動向

5.6.3.ガス分離膜材料の比較

5.6.4.ガス分離用複合膜概要

5.6.5.燃焼後CO2回収のための膜

5.6.6.溶媒を用いた炭素回収の代替案はどのような場合に使用すべきか?

5.6.7.膜を利用した燃焼後CO2回収の主要企業

5.6.8.燃焼後回収用高分子膜の経済性

5.6.9.高分子膜のCO2回収率の向上:MTRの例

5.6.10.燃焼後炭素回収のための促進輸送膜(FTM)

5.6.11.燃焼後炭素回収のための促進輸送膜材料

5.6.12.燃焼後炭素回収における膜の課題とイノベーション

5.6.13.2024/2025年の業界ニュース:燃焼後回収のための膜

5.6.14.燃焼後炭素回収用のグラフェン膜:新素材

5.6.15.燃焼後炭素回収用MOF膜:新素材

5.6.16.直接空気回収用膜

5.6.17.青色水素製造におけるガス分離膜(燃焼前捕捉)

5.7.極低温CO₂回収

5.7.1.極低温CO₂回収:新たな選択肢

5.7.2.極低温CO₂回収はどのような場合に使用されるべきか?

5.7.3.極低温CO2回収技術の現状

5.7.4.極低温直接空気回収企業

5.7.5.青水素中の極低温CO₂回収:Cryocap™

5.8.酸素燃焼によるCO₂回収

5.8.1.酸素燃焼によるCO2回収

5.8.2.酸素燃焼のための酸素分離技術

5.8.3.セメント分野での酸素燃焼

5.8.4.発電用酸素燃焼

5.8.5.新しい酸素燃焼:ケミカル・ルーピング燃焼

5.8.6.ブルー水素のための酸素燃焼

5.8.7.

5.9 新規炭素回収技術

5.8.8.カルシウム・ルーピング

5.8.9.レイラックプロセス:セメント工場での直接CO2回収

5.8.10.溶融炭酸塩燃料電池(MCFC)によるCO2回収

5.8.11.藻類によるCO2回収

6.主要産業のための炭素回収

6.1.はじめに

6.11.1.CO2発生源:歴史的にどのセクターからCO2が回収されてきたか?

6.11.2.CCUSが最も成長するのはどのセクターか?

6.11.3.回収コストはセクターによって異なる

6.2.セメント

6.12.1.CCUSは2050年までに最も重要なセメント脱炭素技術になる

6.12.2.どのセメント脱炭素化技術が最も大きな影響を持つか?

6.12.3.セメント産業における炭素回収の現状

6.12.4.セメント業界初の大規模CCUSプロジェクト

6.12.5.セメントセクターの主なCCUSプロジェクト

6.12.6.燃焼後の溶媒回収はクリンカ製造の中断が少ない

6.12.7.セメントセクターにおける炭素回収技術のベンチマーク

6.12.8.セメントセクターにおける炭素回収:主な要点

6.3.鉄鋼

6.3.1.CCUSが鉄鋼セクターの脱炭素化に果たす役割は限定的

6.3.2.鉄鋼向けCCUSの概要 (1)

6.3.3.鉄鋼向けCCUSの概要(2)

6.3.4.高炉-基礎酸素炉(BF-BOF)プロセスの CCUS

6.3.5.高炉-基礎酸素炉プロセスの燃焼後炭素回収技術

6.3.6.製鉄のための燃焼前炭素回収(1)

6.3.7.製鉄のための燃焼前炭素回収(2)

6.3.8.吸着強化型水ガスシフト(SEWGS)

6.3.9.製鉄のためのガスリサイクルと酸素燃焼

6.3.10.高炉ガスCO2 回収技術の比較

6.3.11.天然ガスベースのDRIのための炭素回収

6.3.12.鉄鋼セクターのCCUSプロジェクトパイプライン

6.3.13.鉄鋼セクターの CO2 利用

6.3.14.鉄鋼セクターにおけるCCUSの課題と機会

6.4.発電

6.4.1.CCUSを導入した発電所は発電量が少ない

6.4.2.石炭発電からのCO2回収

6.4.3.ガス発電からのCO2回収

6.4.4.炭素回収とガス発電

6.4.5.データセンター向けガス発電CCS

6.4.6.電力CCSにおける主なコスト削減機会

6.5.ブルー水素、ブルーアンモニア、化学品

6.5.1.水素製造・導入の主な推進要因

6.5.2.水素バリューチェーンの概要

6.5.3.水素市場の現状

6.5.4.グリーン水素製造の課題

6.5.5.各種水素のコスト比較

6.5.6.ブルー水素製造のケース

6.5.7.ブルー、ターコイズ、バイオマス・ベースの水素製造方法の概要

6.5.8.ブルー水素:主な合成ガス製造技術

6.5.9.ブルー水素の主要技術プレーヤー

6.5.10.ブルー水素の燃焼前CO2回収と燃焼後CO2回収

6.5.11.CCUS ブルー水素プロジェクトの概要

6.5.12.CCUSによるブルー水素製造 - SMR

6.5.13.ATR&POXからのCO2回収はより簡単

6.5.14.ブルー水素製造のためのCO2回収改造オプション

6.5.15.CO2回収のための改造オプション - Honeywell UOPの例

6.5.16.コスト比較:ブルーH2用の商業的CO2回収システム

6.5.17.実際のデータ:ブルー水素用CO2回収システム

6.5.18.将来のブルー水素プロジェクトのための技術

6.5.19.ブルー水素の主な革新分野

6.5.20.米国の水素産業への影響 - 多くのプロジェクト中止

6.5.21.結果 - 中期的にはグリーン水素市場は縮小

6.5.22.EUの水素政策メカニズムの概要

6.5.23.化学物質のための炭素回収

6.6.海事

6.6.1.船上での炭素回収に残された課題

6.6.2.海運セクターにおける船上炭素回収の最近の進展

6.6.3.船上での炭素回収:アミン系溶剤

6.6.4.船上での炭素回収CaOルーピング

6.6.5.船上での炭素回収その他の技術

6.6.6.車載炭素回収・貯留の経済性

7.二酸化炭素除去のための炭素回収(CDR)

7.1.CDRの紹介

7.11.1.CDRとCCUSの違いは何か?

7.11.2.二酸化炭素除去の重要性

7.11.3.CDRのビジネスモデルとその課題炭素クレジット

7.11.4.質の高い炭素除去:耐久性、永続性、付加性

7.11.5.二酸化炭素除去方法の規模と技術準備レベル

7.11.6.炭素クレジット市場における耐久性のある CDR に対する買い手の選好の変化

7.11.7.全体像:2024年の自主的炭素クレジット市場

7.11.8.CDRのために自主的炭素市場とコンプライアンス炭素市場の統合が必要な理由

7.2.直接空気回収(DAC)の導入

7.12.1.直接空気回収(DAC)とは何か?

7.12.2.DACCSの現状

7.12.3.DACCSプロジェクトのパイプライン:場所と技術

7.12.4.勢い:地域別のDACに対する政策支援

7.12.5.DACCS支援における税額控除の役割:45Q と ITC

7.12.6.米国は20の大規模な地域DACハブを設立する計画を持っている

7.12.7.勢い:DACへの民間投資

7.12.8.2024年、DACへの資金はどこから?

7.12.9.DACに必要な電力

7.12.10.銘板容量と実際の純除去量

7.12.11.クリーンエネルギー調達の難しさ

7.12.12.運転の柔軟性-断続的な自然エネルギーによる DAC への電力供給

7.12.13.直接空気回収を拡大するための主な課題は何か?

7.3.主要なDAC技術

7.3.1.DACにおけるCO2回収/分離メカニズム

7.3.2.直接空気回収技術

7.3.3.固体および液体DACの再生方法

7.3.4.固体DACと液体DACの再生方法の比較

7.3.5.主要DAC企業

7.3.6.直接空気捕獲スペース:技術と場所の内訳

7.3.7.DAC用固体吸着剤

7.3.8.クライムワークス

7.3.9.S-DACのプロセスフロー図:クライムワークス

7.3.10.固体吸着剤-半連続運転はエネルギー強度を下げることができる

7.3.11.Heirloom

7.3.12.CaOループ化のプロセスフロー図:ハイルーム

7.3.13.DAC用液体溶媒

7.3.14.液体溶媒ベースのDAC:カーボンエンジニアリング

7.3.15.カーボン・エンジニアリング

7.3.16.ストラトスDACをハーフ・メガトン・スケールへ

7.3.17.L-DACのプロセスフロー図:カーボン・エンジニアリング

7.3.18.どのDAC技術が最も成功するか?

7.3.19.DAC技術はどのように発展するのか?

7.4.エレクトロスウィング/電気化学DAC技術

7.4.1.電気スイング/電気化学DAC

7.4.2.電気化学DACの種類(1/2)

7.4.3.電気化学DACの種類(2/2)

7.4.4.電気化学セル構成部品に望まれる特性

7.4.5.電気化学DACの企業動向

7.4.6.電気化学DAC法のベンチマーク

7.4.7.電気化学的DACにおける技術的課題

7.4.8.電気化学的DAC:低コストの断続的再生可能電力への柔軟性

7.4.9.電気化学DACのコストは電力価格に強く依存する

7.4.10.電気化学DAC:主要な要点

7.4.11. 7.5つの新しいDAC技術

7.4.12.湿度スイング直接空気捕捉(湿度スイング)

7.4.13.湿度スイングDAC用イオン交換樹脂

7.4.14.反応型直接空気捕集-捕集と変換の組み合わせ

7.5.DACの経済性

7.5.1.DACのビジネスモデル

7.5.2.DACのための貯蔵プロバイダーの例

7.5.3.直接回収炭素クレジットの販売価格

7.5.4.DACCSの構成要素別回収コスト貢献

7.5.5.CO2捕捉コスト100ドル/トンの達成

7.6.BECCS (Bioenergy with Carbon Capture and Storage)

7.6.1.BECCSの紹介

7.6.2.既存のBECCSプロジェクトのほとんどはエタノール生産である

7.6.3.バイオマス発電のBECCSはアミン系溶剤が主流

7.6.4.BECCSに対する政府の支援は加速している

7.6.5.BECCSのビジネスモデル - Ørsted社の例

7.6.6.BECCSは耐久性のある設計されたCDRクレジットの販売を支配している

7.6.7.BECCSプロジェクト - 傾向と考察

7.6.8.エタノール生産がBECCSプロジェクトのパイプラインを支配している

7.6.9.BECCS:廃棄物発電

7.6.10.BECCS:バイオガスのアップグレード

7.6.11.BECCSのためのバイオエタノール工場を結ぶネットワーク

7.6.12.BECCS:キーポイント

7.7.DOC(直接海洋回収)

7.7.1.直接海洋捕獲

7.7.2.直接海洋捕獲の現状:スタートアップ企業

7.7.3.電気化学的海洋直接回収

7.7.4.海洋直接捕獲のための電解:塩素生成の回避

7.7.5.その他の海洋直接回収技術

7.7.6.海洋直接回収に残る障壁

8.新たな二酸化炭素利用

8.1.はじめに

8.11.1.なぜ二酸化炭素利用なのか?

8.11.2.二酸化炭素利用とは何か?

8.11.3.成熟市場と新興市場の比較

8.11.4.CO2利用を見過ごせない理由

8.11.5.CO2Uのコストは?

8.11.6.CO2利用経路

8.11.7.いくつかのCO2Uアプリケーションはすでに収益性が証明されている

8.11.8.CO2U市場成長のための主な考察

8.11.9.CO2利用による気候への影響は?

8.11.10.CO2U製品の現在の規模

8.11.11.2045年におけるCO2Uの市場ポテンシャル

8.11.12.新たなCO2利用プレーヤー

8.2.CO2由来コンクリート

8.12.1.高い成長ポテンシャルを持つCO2由来コンクリート

8.12.2.基礎化学CO2の無機化

8.12.3.セメントとコンクリートのサプライチェーンにおけるCO2利用

8.12.4.CO2由来コンクリートの応用分野

8.12.5.CO2由来コンクリート炭素クレジット

8.12.6.原位置無機化リアクターのタイプ

8.12.7.CO2由来コンクリートの主な動向

8.3.CO2由来の化学物質と燃料

8.3.1.メタノール、メタン、ガソリン、灯油、ディーゼルへの CO2 変換経路

8.3.2.脱炭素化規制は、持続可能な燃料が化石燃料との価格格差を達成する必要がなくなったことを意味する

8.3.3.持続可能な航空燃料(SAF)-CO2由来燃料の役割

8.3.4.フィッシャー・トロプシュ合成:合成ガスから炭化水素へ

8.3.5.FT反応器の設計比較

8.3.6.フィッシャー・トロプシュ反応器の革新-マイクロチャンネル反応器

8.3.7.プラント規模別のフィッシャー・トロプシュ(FT)技術サプライヤー

8.3.8.CO2 から CO への経路(合成ガス生産)とプレーヤー

8.3.9.電子燃料用逆水性ガスシフト(RWGS)の主要プレーヤー

8.3.10.電子燃料用 RWGS のスタートアップ企業

8.3.11.RWGS-FT 電子燃料プラントのケーススタディ

8.3.12.直接フィッシャー・トロプシュ合成:CO2 から炭化水素

8.3.13.CO2由来の電子燃料:フィッシャー・トロプシュ対メタノール・ガソリン

8.3.14.MTG電子燃料プラントのケーススタディ

8.3.15.合成ガスの製造:ドライメタンの改質

8.3.16.CO2由来メタノール

8.3.17.メタン化の概要

8.3.18.バイオ触媒によるメタン化のケーススタディ

8.3.19.生物学的変換

8.3.20.電気化学的変換

8.3.21.2024/2025年におけるCO2由来燃料の主要マイルストーン

8.3.22.CO2の部分利用 - CO2由来のポリマーとポリオール

8.3.23.CO2 由来ポリマーの触媒

9.二酸化炭素貯蔵

9.1.はじめに

9.11.1.二酸化炭素の貯留または隔離のケース

9.11.2.超臨界二酸化炭素の地下貯留

9.11.3.地下CO₂トラップのメカニズム

9.11.4.CO₂漏洩は小さなリスク

9.11.5.地震とCO2リーク

9.11.6.地中CO2貯留のための貯留タイプ:塩水帯水層

9.11.7.CO2 地中貯留のための貯留タイプ:塩水帯水層

9.1.7:枯渇油田・ガス田

9.11.8.非在来型貯留資源:石炭層及び頁岩

9.11.9.非在来型貯留資源:玄武岩と超苦鉄質岩

9.11.10.世界のCO₂貯留空間の推定

9.11.11.国別のCO₂貯留ポテンシャル

9.11.12.CO2 貯留の許可と認可

9.11.13.米国におけるCO2貯留:クラス VI 注入許可

9.11.14.米国におけるクラスVI圧入井許可

9.1.14:コストとスケジュール

9.11.15.EU における CO2 貯留:ネットゼロ産業法

9.11.16.CO₂貯留におけるモニタリング、報告、検証(MRV)

9.11.17.CO₂貯留におけるMRV技術とコスト

9.2.CO₂貯留プロジェクトの状況

9.12.1.CO₂貯留の技術状況

9.12.2.稼働中および建設中の大規模なCO₂貯留専用サイトの世界地図

9.12.3.利用可能なCO2貯留量は、まもなくCO2回収量を上回る

9.12.4.専用の地中貯留はすぐにCO2-EORを上回る

9.12.5.CO₂貯留は収益化できるか?

9.12.6.北海のパートチェーン貯留プロジェクト:ロングシップ・プロジェクト

9.12.7.北海における部分連鎖式CO₂貯留プロジェクト:The Longship Project

9.2.7:ポルトス・プロジェクト

9.12.8.炭素隔離のコスト (1/2)

9.12.9.炭素貯留のコスト(2/2)

9.12.10.二酸化炭素貯留タイプの成熟度とオペレーターの状況

9.12.11.二酸化炭素貯留:主要な要点

9.12.12.二酸化炭素貯留と地熱エネルギー

9.3.CO2-EOR

9.3.1.CO2-EOR とは?

9.3.2.注入されたCO2はどうなるのか?

9.3.3.CO2-EOR設計の種類

9.3.4.CO2増進回収法市場

9.3.5.米国におけるCO2-EOR

9.3.6.米国におけるCO2の大部分は、現在も自然由来のもの

9.3.7.米国のCO2-EOR主要プレーヤー

9.3.8.世界の大規模CO2回収とCO2-EOR施設

9.3.9.世界のCO2-EORポテンシャル

9.3.10.中国におけるCO2-EOR

9.3.11.CO2-EORによるCO2貯留促進の経済性

9.3.12.原油価格がCO2-EORの実現可能性に与える影響

9.3.13.CO2-EOR における気候への配慮

9.3.14.CO2-EOR: 進歩的か「グリーンウォッシング」か

9.3.15.CO2-EOR における将来の進歩

9.3.16.CO2-EOR と CO2 貯留の経済性

9.3.17.主要な要点市場

9.3.18.要点:市場環境

9.3.19.増進ガス回収

10.二酸化炭素輸送

10.1.二酸化炭素輸送の概要

10.2.CO2輸送のフェーズ

10.3.CO2輸送方法の概要と条件

10.4.CCSプロジェクトにおけるCO2輸送方法の現状

10.5.パイプラインによるCO2輸送

10.6.米国におけるCO2パイプラインインフラ開発

10.7.CO2パイプライン:技術的課題

10.8.船舶によるCO2輸送

10.9.船舶によるCO2輸送:船舶設計の革新

10.10.鉄道とトラックによるCO2輸送

10.11.CO2輸送に求められる純度

10.12.CO2輸送方法の一般的コスト比較

10.13.CAPEXとOPEXの貢献

10.14.CO₂輸送におけるコスト考慮事項

10.15.CO2輸送のための越境ネットワーク:欧州

10.16.欧州におけるCO2パイプライン開発

10.17.最初の国境を越えたCO2 T&Sプロジェクト:オーロラ・ロングシップ・プロジェクト

10.18.利用可能なCO2輸送量は、まもなくCO2回収量を上回る

10.19.CO2輸送事業者

10.20.サービスとしてのCO2輸送・貯蔵ビジネスモデル

10.21.CO2輸送:主な要点

11.CCUS市場予測

11.1.CCUS予測方法

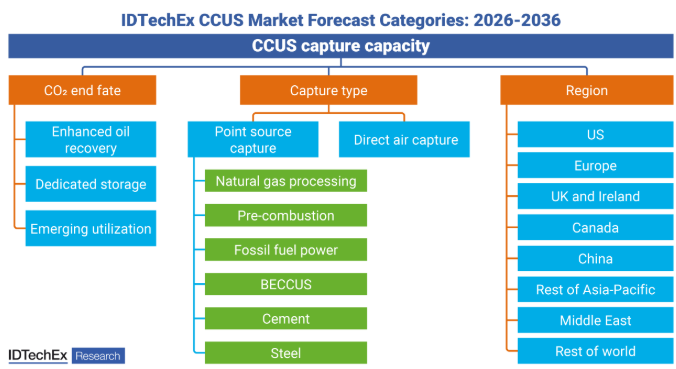

11.2.CCUS予測の内訳

11.3.CCUS市場予測-総論

11.4.CO₂エンドポイント別CCUS回収能力予測、Mtpa of CO2

11.5.CO₂エンドポイント別CCUS予測-貯蔵と増進回収

11.6.CO₂エンドポイント別CCUS予測-新興利用

11.7.回収タイプ別CCUS容量予測、CO₂ Mtpa

11.8.回収タイプ別 CCUS 容量予測-直接空気回収(DAC)容量予測

11.9.CO2発生源セクター別ポイントソース捕捉能力予測、CO₂ Mtpa

11.10.CO2発生源別ポイントソース炭素回収予測

11.11.CO2発生源別ポイントソース炭素回収予測 - 発電

11.12.CO2発生源別ポイントソース炭素回収予測-セメントと鉄鋼

11.13.地域別CCUS回収能力(Mtpa of CO2)

11.14.地域別CCUS回収能力 - 北米

11.15.地域別CCUS回収能力-ヨーロッパとイギリス

11.16.地域別CCUS回収能力-アジア太平洋、中東、その他の地域

11.17.炭素回収・利用・貯留(CCUS)市場 2025-2045 IDTechEx予測

12.企業プロファイル

12.1.8 リバーズ

12.2.エアハイブ

12.3.エアレーンCCUS

12.4.アーデント

12.5.アトコ

12.6.アクセンスDMX

12.7.ベーカーヒューズカーボン・キャプチャー

12.8.ブレントウッド・インダストリーズ構造化パッキング

12.9.ブラインワークス

12.10.カプソ

12.11.カプソル・テクノロジーズ

12.12.キャプチュラ

12.13.カーボンブレード

12.14.カーボンニュートラル燃料

12.15.カーボンビット・テクノロジーズ

12.16.カーボンブリッジ

12.17.チャート・インダストリーズCCUS

12.18.クレアリティ・テック

12.19.クライムワークス

12.20.CO2ロック

12.21.コンクリート4チェンジ

12.22.シアノキャプチャー

12.23.DACMA

12.24. イー・ケミクル

12.25.エコスプレー

12.26.エクアティック

12.27.エステック

12.28.エクソンモービルメタノール-ガソリン(MTG)

12.29.フッ素炭素回収

12.30.燃料電池エネルギー

12.31.家宝

12.32.ホロセン

12.33.Honeywell UOP: CO₂ Solutions

12.34.HYCO1

12.35.ineratec

12.36.インフィニウム

12.37.イオンクリーンエナジー

12.38.JCCL(Japan Carbon Cycle Labs)

12.39.川崎汽船 12.40:CCUS

12.40.マンテル

12.41.ミッション・ゼロ・テクノロジーズ

12.42.三菱重工業KM CDRプロセス

12.43.MTR(膜技術研究)

12.44.日本化学工業R&D分野

12.45.ヌアダMOFベースの炭素捕捉

12.46.OXCCU

12.47.Paebbl

12.48.パラレルカーボン

12.49.Phlair

12.50.Qパワー

12.51.サイペムブルーエンザイム

12.52.シェル&テクニップ・エナジー・アライアンスCANSOLV炭素回収技術

12.53.スカイツリー

12.54.SLB Capturi

12.55.住友重機械FW:炭素回収

12.56.スバンテ

12.57.シクレア

12.58.ユニシーブ

12.59.ベロシス

12.60.ヤマ

Summary

CCUS market outlook, ten-year granular forecasts, company profiles, and technology assessment of point-source carbon capture for key sectors, direct air capture (DAC), CO2 transport and storage (T&S), and CO2 utilization

Carbon capture, utilization, and storage (CCUS) technologies capture CO2 from flue gases or directly from the atmosphere. This captured carbon dioxide is then permanently stored or utilized to generate revenue. Governments have recognized the role CCUS can play in decarbonizing industry and valorizing waste CO2, and are continuing to create favourable CCUS policy environments through carbon pricing, tax credits, and subsidies. The essential role of the private sector is crystallizing, with examples including oil and gas companies pivoting into providing CO2 transportation and storage services and data center hyperscalers creating markets for carbon credits from direct air capture (DAC) and biogenic CCUS (BECCS).

"Carbon Capture, Utilization, and Storage (CCUS) Markets 2026-2036: Technologies, Market Forecasts, and Players" provides a comprehensive outlook of the emerging CCUS industry and carbon markets, with an in-depth analysis of the technological, economic, regulatory, and environmental aspects that are set to shape the CCUS industry over the next 10 years. Carbon capture, carbon utilization, and carbon storage technologies are evaluated, discussing latest advancements, key players, and opportunities and barriers within each area. The report also includes a 10-year granular forecast until 2036 for CCUS carbon capture capacity (segmented by CO2 end-point, point-source vs DAC, industrial sector, and region) alongside exclusive analysis, 60 interview-based company profiles, and coverage of 350+ companies.

The acceleration of CCUS markets has continued into 2025, with noteworthy first-of-a-kind projects coming online including Northern Lights T&S and Stratos DAC. As the CCUS project pipeline continues to swell, with 50 million tonnes of new capacity under construction as of 2025, this IDTechEx report provides an overview of CCUS business models, economics, and leading/emerging capture technologies.

Business model

Tax credits and/or government subsidies are still typically needed to bring new large-scale CCUS capacity online. Key examples include the US 45Q tax credit (recently boosted for carbon dioxide utilization in the Trump administration's Big Beautiful Bill) and the UK government announcing £20 billion in funding for industrial CCUS clusters. Compliance carbon market mechanisms are expected to ultimately enable CCUS long-term. As of 2025, 28% of global CO2 emissions are covered by some form of carbon pricing, with the arrival of the European Union CBAM (carbon border adjustment mechanism) in 2026 motivating new carbon market developments.

Additionally, new partial chain CCUS hubs, clusters, and networks are set to unlock economies of scale and debottleneck CCUS development. By providing shared CO2 transportation and CO2 storage infrastructure, this new CCUS business model will streamline CCUS project development.

Point-source capture technology developments

Amine solvents for point-source carbon capture are technologically mature, but innovations continue to be commercialized such as demixing solvents and water-lean solvents. This IDTechEx report also includes balance of plant considerations for amine solvent carbon capture, including advances to improve mass transfer in absorber/stripper columns.

Beyond amine solvents, emerging start-ups in the carbon capture space are pursuing a broad range of technologies including molten borate salts, facilitated transport membranes, molten carbonate fuel cells, and cryogenic approaches. These technologies ultimately aim to reduce the energy demand of capture. In this report, IDTechEx identifies key carbon capture players and benchmarks capture technologies.

Regional CCUS market forecasts

The US is the world leader for CCUS, due its 45Q tax credit support and strong history of CO2-EOR (enhanced oil recovery). Other regions including Europe, China, Canada, and the UK will also be instrumental for the global scale-up of CCUS. For example, the EU's recent Net-Zero Industry Act mandates an annual CO2 permanent storage capacity of at least 50 million tonnes by 2030. This IDTechEx report includes regional forecasting of CCUS markets, illustrating differences in CCUS growth by geography.

Key questions answered in this report

Key Aspects

This report provides the following information

Technology and market analysis

Player analysis and trends

Market forecasts and analysis

Table of Contents1. EXECUTIVE SUMMARY

1.1. What is Carbon Capture, Utilization and Storage (CCUS)?

1.2. Why CCUS and why now?

1.3. CCUS business model overview: Value from CO2

1.4. Development of the CCS business model

1.5. CCUS business model: Networks and hub model

1.6. CCUS business model: Partial-chain

1.7. World map of operational and under construction large-scale dedicated CO2 storage sites

1.8. Carbon dioxide storage-type maturity and operator landscape

1.9. CO2-Enhanced oil recovery market

1.10. Carbon pricing and carbon markets

1.11. Compliance carbon pricing mechanisms across the globe

1.12. Alternative to carbon pricing in the US: 45Q tax credits

1.13. CCUS forecast by CO₂ end point - Storage and enhanced oil recovery

1.14. Why CO2 utilization?

1.15. Current scale for CO2U products

1.16. Main CO2 capture systems

1.17. Which carbon capture technologies are most mature?

1.18. When should different carbon capture technologies be used?

1.19. Point-source carbon capture technology providers

1.20. High-concentration CO2 sources are the low-hanging fruits

1.21. Point-source CCUS capture capacity forecast by CO2 source sector, Mtpa of CO2

1.22. Leading DAC companies

1.23. What are the major challenges for scaling up direct air capture?

1.24. The momentum behind CCUS is building up

1.25. CCUS capture capacity by region - North America

1.26. CO2 transportation overview

1.27. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. What is Carbon Capture, Utilization and Storage (CCUS)?

2.2. The CCUS value chain

2.3. Why CCUS and why now?

2.4. Carbon capture

2.5. Pathways to lower capture costs

2.6. CO2 storage

2.7. Development of the CCS business model

2.8. Why CO2 utilization?

2.9. CO2 transportation

2.10. How much does CCUS cost?

2.11. When can CCUS be considered net-zero?

2.12. CCUS Market Challenges

2.13. Enabling large-scale CCUS

3. BUSINESS MODELS FOR CCUS

3.1. Introduction

3.1.1. CCUS business model overview: Value from CO2

3.1.2. Development of the CCS business model

3.1.3. Government funding support mechanisms for CCS

3.1.4. Government ownership of CCS projects varies across countries

3.1.5. CCUS business model: Full chain

3.1.6. CCUS business model: Networks and hub model

3.1.7. CCUS business model: Partial-chain

3.1.8. Carbon dioxide utilization business model

3.2. Carbon Pricing and Carbon Markets

3.2.1. Carbon pricing and carbon markets

3.2.2. Compliance carbon pricing mechanisms across the globe

3.2.3. What is the price of CO2 in global carbon pricing mechanisms?

3.2.4. The European Union Emission Trading Scheme (EU ETS)

3.2.5. Has the EU ETS had an impact?

3.2.6. What changes are needed for the EU ETS to support CCUS?

3.2.7. EU Carbon Border Adjustment Mechanism (CBAM)

3.2.8. EU CBAM will be the first of many internationally

3.2.9. Alternative to carbon pricing in the US: 45Q tax credits

3.2.10. The role of voluntary carbon markets in supporting CCUS

3.2.11. How high does carbon pricing need to be to support CCS?

4. STATUS OF THE CCUS INDUSTRY

4.1. The momentum behind CCUS is building up

4.2. CCUS milestones in 2024/2025

4.3. Global pipeline of carbon capture facilities built and announced

4.4. Analysis of CCUS development

4.5. CO2 source: From which sectors has CO2 been captured historically?

4.6. Which sectors will see the biggest growth in CCUS?

4.7. CO2 fate: Where does/will the captured CO2 go?

4.8. Regional analysis of CCUS Projects

4.9. Major CCUS players

4.10. CCUS project performance - natural gas processing

4.11. CCUS project performance - natural gas processing commentary

4.12. CCUS project performance - power generation

4.13. CCUS project performance - key takeaways

4.14. Boundary Dam - battling capture technical issues

4.15. Petra Nova's long shutdown: Lessons for the industry?

4.16. How much does CCUS cost?

4.17. Costs and financing of large-scale CCUS projects

5. CARBON CAPTURE TECHNOLOGIES

5.1. Introduction

5.1.1. The CCUS value chain

5.1.2. Main CO2 capture systems

5.1.3. Status of point source carbon capture

5.1.4. Natural gas sweetening

5.1.5. Post-combustion CO2 capture

5.1.6. Pre-combustion CO2 capture

5.1.7. Oxy-fuel combustion CO2 capture

5.1.8. Main CO2 capture technologies

5.1.9. Comparison of CO2 capture technologies

5.1.10. Maturity of carbon capture technologies - overview

5.1.11. Which carbon capture technologies are most mature?

5.1.12. When should different carbon capture technologies be used?

5.1.13. Typical conditions and performance for different capture technologies

5.1.14. CO2 concentration and partial pressure varies with emission source

5.1.15. How does CO₂ partial pressure influence cost?

5.1.16. High-concentration CO2 sources are the low-hanging fruits

5.1.17. No single carbon capture technology will be the best across all applications

5.1.18. Carbon capture technology providers for existing large-scale projects

5.1.19. Capture percentage exceeding 90% are the current industry standard

5.1.20. What is meant by CO2 capture rate?

5.1.21. Making the case for CO2 capture percentages below 90%

5.1.22. Contributions to carbon capture cost

5.1.23. Metrics for CO2 capture agents

5.1.24. State-of-the-art: Capture percentages

5.1.25. State-of-the-art: Energy consumption

5.1.26. Technology readiness of carbon capture technologies (1/2)

5.1.27. Technology readiness of carbon capture technologies (2/2)

5.1.28. Point-source carbon capture technology providers by technology

5.2. Solvents for Carbon Capture

5.2.1. Solvent-based CO₂ capture

5.2.2. Chemical absorption solvents

5.2.3. Amine-based post-combustion CO₂ absorption

5.2.4. The development of amine solvents for carbon capture

5.2.5. Innovations in amine solvents

5.2.6. Amine-solvents dominate CCUS but challenges remain

5.2.7. Amine solvent carbon capture technology providers for post-combustion capture (1/2)

5.2.8. Amine solvent carbon capture technology providers for post-combustion capture (2/2)

5.2.9. Hot Potassium Carbonate (HPC) process

5.2.10. HPC carbon capture technology providers for carbon capture

5.2.11. Chemical absorption solvents used in current operational CCUS point-source projects (1/2)

5.2.12. Chemical absorption solvents used in current operational CCUS point-source projects (2/2)

5.2.13. Cost breakdown of chemical solvent post-combustion capture

5.2.14. Physical absorption solvents

5.2.15. Comparison of key physical absorption solvents

5.2.16. Physical solvents used in current operational CCUS point-source projects

5.2.17. When should solvent-based carbon capture not be used?

5.3. Balance of Plant for Amine Solvent Carbon Capture

5.3.1. Introduction to amine solvent post-combustion carbon capture

5.3.2. Summary of carbon capture balance of plant (BoP) components

5.3.3. Flue gas preconditioning/pretreatment for post-combustion capture

5.3.4. Babcock & Wilcox flue gas pretreatment portfolio

5.3.5. Absorber columns for amine solvent based carbon capture

5.3.6. Absorber column structured packing for amine solvent based carbon capture

5.3.7. Material innovation in structured packing for absorber columns

5.3.8. Water use in carbon capture plants

5.3.9. Absorber/stripper innovation: Rotating packed beds

5.3.10. Hybrid process - membrane contactors

5.3.11. Main heat exchanger: Lean/rich amine cross exchanger

5.3.12. Auxiliary heat exchangers

5.3.13. Technology providers of heat exchangers for carbon capture

5.3.14. Innovations in reducing reboiler duty

5.3.15. Large-scale CO2 compression technologies

5.3.16. CO2 compression costs

5.3.17. BoP case study: ION Clean Energy

5.3.18. Supply chain considerations of BoP technologies by region

5.3.19. Equipment and Technology Providers for CCUS in China

5.3.20. High value matrix for key components in post-combustion solvent-based carbon capture

5.4. Emerging Solvents for Carbon Capture

5.4.1. Company landscape: Emerging solvents for carbon capture

5.4.2. Chilled ammonia process (CAP)

5.4.3. Molten borates

5.4.4. Applicability of chemical absorption solvents capture solvents for post-combustion applications

5.5. Sorbents for Carbon Capture

5.5.1. Solid sorbent-based CO₂ separation

5.5.2. Adsorbents in pressure swing adsorption: Hydrogen separation

5.5.3. Adsorbents in pressure swing adsorption: Carbon capture

5.5.4. Overview of solid sorbents explored for carbon capture

5.5.5. Zeolite-based adsorbents

5.5.6. Carbon-based adsorbents

5.5.7. Metal organic framework (MOF) adsorbents

5.5.8. Solid amine-based adsorbents

5.5.9. Solid sorbent processes used in operational CCUS point-source projects

5.5.10. Solid sorbent materials for carbon capture overview

5.5.11. Sorption enhanced water gas shift (SEWGS)

5.6. Membrane-based Carbon Capture

5.6.1. Introduction to gas separation membranes for decarbonization

5.6.2. Developing new membrane materials: Key trends

5.6.3. Comparing gas separation membrane materials

5.6.4. Composite membranes for gas separation: Overview

5.6.5. Membranes for post-combustion CO2 capture

5.6.6. When should alternatives to solvent-based carbon capture be used?

5.6.7. Leading players in membrane-based post-combustion capture

5.6.8. Economics of polymer membranes for post-combustion capture

5.6.9. Increasing CO2 recovery rates for polymer membranes: MTR example

5.6.10. Facilitated transport membranes (FTM) for post-combustion carbon capture

5.6.11. Facilitated transport membrane materials for post-combustion carbon capture

5.6.12. Challenges and innovations for membranes in post-combustion capture

5.6.13. 2024/2025 Industry News: Membranes for post-combustion capture

5.6.14. Graphene membranes for post-combustion carbon capture: emerging material

5.6.15. MOF membranes for post-combustion carbon capture: Emerging material

5.6.16. Membranes for direct air capture

5.6.17. Gas separation membranes in blue hydrogen production (pre-combustion capture)

5.7. Cryogenic CO2 Capture

5.7.1. Cryogenic CO₂ capture: An emerging alternative

5.7.2. When should cryogenic carbon capture be used?

5.7.3. Status of cryogenic CO2 capture technologies

5.7.4. Cryogenic direct air capture companies

5.7.5. Cryogenic CO₂ capture in blue hydrogen: Cryocap™

5.8. Oxyfuel Combustion Capture

5.8.1. Oxy-fuel combustion CO2 capture

5.8.2. Oxygen separation technologies for oxy-fuel combustion

5.8.3. Oxyfuel combustion in the cement sector

5.8.4. Oxyfuel combustion for power generation

5.8.5. Novel oxyfuel: Chemical looping combustion

5.8.6. Oxyfuel combustion for blue hydrogen

5.8.7. 5.9 Novel Carbon Capture Technologies

5.8.8. Calcium looping

5.8.9. Leilac process: Direct CO2 capture in cement plants

5.8.10. CO2 capture with Molten Carbonate Fuel Cells (MCFCs)

5.8.11. Algae CO2 capture

6. CARBON CAPTURE FOR KEY INDUSTRIES

6.1. Introduction

6.1.1. CO2 source: From which sectors has CO2 been captured historically?

6.1.2. Which sectors will see the biggest growth in CCUS?

6.1.3. Capture costs vary by sector

6.2. Cement

6.2.1. CCUS will be the most important cement decarbonization technology by 2050

6.2.2. Which cement decarbonization technology will have the biggest impact?

6.2.3. Status of carbon capture in the cement industry

6.2.4. First large-scale cement sector CCUS project

6.2.5. Major CCUS projects in the cement sector

6.2.6. Post-combustion solvent capture is less disruptive to clinker manufacturing

6.2.7. Benchmarking carbon capture technologies in the cement sector

6.2.8. Carbon capture in the cement sector: Key takeaways

6.3. Steel

6.3.1. CCUS will play a limited role in decarbonizing the iron and steel sector

6.3.2. Overview of CCUS for iron & steel (1)

6.3.3. Overview of CCUS for iron & steel (2)

6.3.4. CCUS for BF-BOF (blast furnace-basic oxygen furnace) process

6.3.5. Post combustion capture technologies for BF-BOF process

6.3.6. Pre-combustion carbon capture for ironmaking (1)

6.3.7. Pre-combustion carbon capture for ironmaking (2)

6.3.8. Sorption enhanced water gas shift (SEWGS)

6.3.9. Gas recycling and oxyfuel combustion for ironmaking

6.3.10. Blast furnace gas CO2 capture technologies comparison

6.3.11. Carbon capture for natural gas-based DRI

6.3.12. CCUS project pipeline for the steel sector

6.3.13. CO2 utilization for the steel sector

6.3.14. Challenges and opportunities for CCUS in the steel sector

6.4. Power Generation

6.4.1. Power plants with CCUS generate less energy

6.4.2. CO2 capture from coal power generation

6.4.3. CO2 capture from gas power generation

6.4.4. Carbon capture and gas power

6.4.5. Gas power CCS for data centers

6.4.6. Key cost reduction opportunities in power CCS

6.5. Blue Hydrogen, Blue Ammonia, and Chemicals

6.5.1. Major drivers for hydrogen production & adoption

6.5.2. Hydrogen value chain overview

6.5.3. State of the hydrogen market today

6.5.4. Challenges in green hydrogen production

6.5.5. Cost comparison of different types of hydrogen

6.5.6. The case for blue hydrogen production

6.5.7. Overview of blue, turquoise & biomass-based H2 production methods

6.5.8. Blue hydrogen: Main syngas production technologies

6.5.9. Key technology players in blue hydrogen

6.5.10. Pre- vs post-combustion CO2 capture for blue hydrogen

6.5.11. Overview of CCUS blue hydrogen projects

6.5.12. Blue hydrogen production - SMR with CCUS

6.5.13. Capturing CO2 from ATR & POX is easier

6.5.14. CO2 capture retrofit options for blue H2 production

6.5.15. CO2 capture retrofit options - Honeywell UOP example

6.5.16. Cost comparison: Commercial CO2 capture systems for blue H2

6.5.17. Real world data: CO2 capture systems for blue hydrogen

6.5.18. Technologies for future blue hydrogen projects

6.5.19. Key innovation areas in blue hydrogen

6.5.20. Impact on the US hydrogen industry - many project cancellations

6.5.21. Outcome - a smaller green hydrogen market in the medium term

6.5.22. Overview of EU hydrogen policy mechanisms

6.5.23. Carbon capture for chemicals

6.6. Maritime

6.6.1. Remaining challenges for onboard carbon capture

6.6.2. Recent developments in onboard carbon capture for the maritime sector

6.6.3. Onboard carbon capture: Amine solvents

6.6.4. Onboard carbon capture: CaO looping

6.6.5. Onboard carbon capture: Other technologies

6.6.6. Economics of onboard carbon capture and storage

7. CARBON CAPTURE FOR CARBON DIOXIDE REMOVAL (CDR)

7.1. CDR Introduction

7.1.1. What is the difference between CDR and CCUS?

7.1.2. The importance of carbon dioxide removals

7.1.3. The CDR business model and its challenges: Carbon credits

7.1.4. High-quality carbon removals: Durability, permanence, additionality

7.1.5. Scale and technology readiness level of carbon dioxide removal methods

7.1.6. Shifting buyer preferences for durable CDR in carbon credit markets

7.1.7. Overall picture: voluntary carbon credit markets in 2024

7.1.8. Why voluntary and compliance carbon markets need to merge for CDR

7.2. Direct Air Capture (DAC) Introduction

7.2.1. What is direct air capture (DAC)?

7.2.2. Current status of DACCS

7.2.3. DACCS project pipeline: Locations and technologies

7.2.4. Momentum: Policy support for DAC by region

7.2.5. The role of tax credits in supporting DACCS: 45Q and ITC

7.2.6. The US has plans to establish 20 large-scale regional DAC Hubs

7.2.7. Momentum: Private investment in DAC

7.2.8. Where did money for DAC come from in 2024?

7.2.9. Power requirements for DAC

7.2.10. Nameplate capacity vs actual net removal

7.2.11. Difficulties sourcing clean energy

7.2.12. Operational flexibility - powering DAC with intermittent renewables

7.2.13. What are the major challenges for scaling up direct air capture?

7.3. Leading DAC Technologies

7.3.1. CO2 capture/separation mechanisms in DAC

7.3.2. Direct air capture technologies

7.3.3. Regeneration methods for solid and liquid DAC

7.3.4. Comparing regeneration methods for solid and liquid DAC

7.3.5. Leading DAC companies

7.3.6. Direct air capture space: Technology and location breakdown

7.3.7. Solid sorbents for DAC

7.3.8. Climeworks

7.3.9. Process flow diagram of S-DAC: Climeworks

7.3.10. Solid sorbents - semi-continuous operation can lower energy intensity

7.3.11. Heirloom

7.3.12. Process flow diagram of CaO looping: Heirloom

7.3.13. Liquid solvents for DAC

7.3.14. Liquid solvent-based DAC: Carbon Engineering

7.3.15. Carbon Engineering

7.3.16. Stratos: Bringing DAC to the half megatonne scale

7.3.17. Process flow diagram of L-DAC: Carbon Engineering

7.3.18. Which DAC technologies will be the most successful?

7.3.19. How will DAC technologies develop?

7.4. Electroswing/Electrochemical DAC Technologies

7.4.1. Electroswing/electrochemical DAC

7.4.2. Types of electrochemical DAC (1/2)

7.4.3. Types of electrochemical DAC (2/2)

7.4.4. Desired characteristics of electrochemical cell components

7.4.5. Electrochemical DAC company landscape

7.4.6. Benchmarking electrochemical DAC methods

7.4.7. Technical challenges in electrochemical DAC

7.4.8. Electrochemical DAC: Flexibility for low-cost intermittent renewable power

7.4.9. Electrochemical DAC costs depend strongly on electricity prices

7.4.10. Electrochemical DAC: Key takeaways

7.4.11. 7.5 Novel DAC Technologies

7.4.12. Moisture-swing direct air capture (humidity swing)

7.4.13. Ion exchange resins for moisture swing DAC

7.4.14. Reactive direct air capture - combined capture and conversion

7.5. DAC Economics

7.5.1. Business models for DAC

7.5.2. Examples of storage providers for DAC

7.5.3. Direct air capture carbon credit selling prices

7.5.4. Component specific capture cost contributions for DACCS

7.5.5. Reaching a capture cost of $100/tonne of CO2

7.6. BECCS (Bioenergy with Carbon Capture and Storage)

7.6.1. Introduction to BECCS

7.6.2. Most existing BECCS projects are in ethanol production

7.6.3. Amine solvents dominate BECCS for biomass power

7.6.4. Government support for BECCS is accelerating

7.6.5. BECCS business model - Ørsted example

7.6.6. BECCS dominates the sales of durable, engineered CDR credits

7.6.7. BECCS projects - trends and discussion

7.6.8. Ethanol production dominates the BECCS project pipeline

7.6.9. BECCS: Waste-to-energy

7.6.10. BECCS: Biogas upgrading

7.6.11. Network connecting bioethanol plants for BECCS

7.6.12. BECCS: Key takeaways

7.7. DOC (Direct Ocean Capture)

7.7.1. Direct ocean capture

7.7.2. Direct ocean capture status: Start-ups

7.7.3. Electrochemical direct ocean capture

7.7.4. Electrolysis for direct ocean capture: Avoiding chlorine formation

7.7.5. Other direct ocean capture technologies

7.7.6. Barriers remain for direct ocean capture

8. EMERGING CARBON DIOXIDE UTILIZATION

8.1. Introduction

8.1.1. Why CO2 utilization?

8.1.2. What is CO2 utilization?

8.1.3. Mature vs emerging carbon dioxide utilization market sizes

8.1.4. Why CO2 utilization should not be overlooked

8.1.5. How much does CO2U cost?

8.1.6. CO2 utilization pathways

8.1.7. Some CO2U applications have already proven profitable

8.1.8. Key Considerations for CO2U Market Growth

8.1.9. What is the Climate Impact of CO2 Utilization?

8.1.10. Current scale for CO2U products

8.1.11. Market potential for CO2U in 2045

8.1.12. Emerging CO2 utilization players

8.2. CO2-derived Concrete

8.2.1. CO2-Derived Concrete has High Growth Potential

8.2.2. The Basic Chemistry: CO2 Mineralization

8.2.3. CO2 use in the cement and concrete supply chain

8.2.4. CO2-Derived concrete application areas

8.2.5. CO2 derived concrete: Carbon credits

8.2.6. Ex-situ mineralization reactor types

8.2.7. Key trends in CO2-derived concrete

8.3. CO2-derived Chemicals and Fuels

8.3.1. CO2 conversion pathways to methanol, methane, gasoline, kerosene, and diesel

8.3.2. Decarbonization regulation mean sustainable fuels no longer need to achieve price-parity with fossil fuels

8.3.3. Sustainable aviation fuels (SAF) - role of CO2-derived fuels

8.3.4. Fischer-Tropsch synthesis: Syngas to hydrocarbons

8.3.5. FT reactor design comparison

8.3.6. FT reactor innovation - microchannel reactors

8.3.7. Fischer-Tropsch (FT) technology suppliers by plant scale

8.3.8. CO2 to CO pathways (syngas production) and players

8.3.9. Key players in reverse water gas shift (RWGS) for e-fuels

8.3.10. Start-ups in reverse water gas shift (RWGS) for e-fuels

8.3.11. RWGS-FT e-fuel plant case study

8.3.12. Direct Fischer-Tropsch synthesis: CO2 to hydrocarbons

8.3.13. CO2 derived e-fuels: Fischer-Tropsch vs Methanol-to-gasoline

8.3.14. MTG e-fuel plant case study

8.3.15. Syngas production: Dry methane reforming

8.3.16. CO2-derived methanol

8.3.17. Methanation overview

8.3.18. Biocatalytic methanation case study

8.3.19. Biological conversion

8.3.20. Electrochemical conversion

8.3.21. Key milestones for CO2-derived fuels in 2024/2025

8.3.22. Partial CO2 utilization - CO2-derived polymers and polyols

8.3.23. Catalysts for CO2-derived polymers

9. CARBON DIOXIDE STORAGE

9.1. Introduction

9.1.1. The case for carbon dioxide storage or sequestration

9.1.2. Storing supercritical CO2 underground

9.1.3. Mechanisms of subsurface CO₂ trapping

9.1.4. CO2 leakage is a small risk

9.1.5. Earthquakes and CO2 leakage

9.1.6. Storage type for geologic CO2 storage: Saline aquifers

9.1.7. Storage type for geologic CO2 storage: Depleted oil and gas fields

9.1.8. Unconventional storage resources: Coal seams and shale

9.1.9. Unconventional storage resources: Basalts and ultra-mafic rocks

9.1.10. Estimates of global CO₂ storage space

9.1.11. CO2 storage potential by country

9.1.12. Permitting and authorization of CO2 storage

9.1.13. CO2 storage in the US: Class VI injection permits

9.1.14. Class VI injection well permits in the US: Costs and timeline

9.1.15. CO2 storage in the EU: Net-Zero Industry Act

9.1.16. Monitoring, reporting, and verification (MRV) in CO₂ storage

9.1.17. MRV Technologies and Costs in CO2 Storage

9.2. Status of CO2 Storage Projects

9.2.1. Technology status of CO₂ storage

9.2.2. World map of operational and under construction large-scale dedicated CO2 storage sites

9.2.3. Available CO2 storage will soon outstrip CO2 captured

9.2.4. Dedicated geological storage will soon outpace CO2-EOR

9.2.5. Can CO₂ storage be monetized?

9.2.6. Part-chain storage project in the North Sea: The Longship Project

9.2.7. Part-chain storage project in the North Sea: The Porthos Project

9.2.8. The cost of carbon sequestration (1/2)

9.2.9. The cost of carbon sequestration (2/2)

9.2.10. Carbon dioxide storage-type maturity and operator landscape

9.2.11. CO2 storage: Key takeaways

9.2.12. CO2 storage and geothermal energy

9.3. CO2-EOR

9.3.1. What is CO2-EOR?

9.3.2. What happens to the injected CO2?

9.3.3. Types of CO2-EOR designs

9.3.4. CO2-Enhanced oil recovery market

9.3.5. CO2-EOR in the US

9.3.6. Most CO2 in the U.S. is still naturally sourced

9.3.7. CO2-EOR main players in the U.S.

9.3.8. World's large-scale CO2 capture with CO2-EOR facilities

9.3.9. Worldwide CO2-EOR Potential

9.3.10. CO2-EOR in China

9.3.11. The economics of promoting CO2 storage through CO2-EOR

9.3.12. The impact of oil prices on CO2-EOR feasibility

9.3.13. Climate considerations in CO2-EOR

9.3.14. CO2-EOR: Progressive or "Greenwashing"

9.3.15. Future advancements in CO2-EOR

9.3.16. Economics of CO2-EOR vs CO2 storage

9.3.17. Key takeaways: Market

9.3.18. Key takeaways: Environmental

9.3.19. Enhanced gas recovery

10. CARBON DIOXIDE TRANSPORTATION

10.1. Introduction to CO2 transportation

10.2. Phases of CO2 for transportation

10.3. Overview of CO2 transportation methods and conditions

10.4. Status of CO2 transportation methods in CCS projects

10.5. CO2 transportation by pipeline

10.6. CO2 pipeline infrastructure development in the US

10.7. CO2 pipelines: Technical challenges

10.8. CO2 transportation by ship

10.9. CO2 transportation by ship: Innovations in ship design

10.10. CO2 transportation by rail and truck

10.11. Purity requirements of CO2 transportation

10.12. General cost comparison of CO2 transportation methods

10.13. CAPEX and OPEX contributions

10.14. Cost considerations in CO₂ transport

10.15. Transboundary networks for CO2 transport: Europe

10.16. CO2 pipeline development in Europe

10.17. First cross-border CO2 T&S project: Northern Lights Longship project

10.18. Available CO2 transportation will soon outstrip CO2 captured

10.19. CO2 transport operators

10.20. CO2 transport and/or storage as a service business model

10.21. CO2 transportation: Key takeaways

11. CCUS MARKET FORECASTS

11.1. CCUS forecast methodology

11.2. CCUS forecast breakdown

11.3. CCUS market forecast - Overall discussion

11.4. CCUS capture capacity forecast by CO2 end point, Mtpa of CO2

11.5. CCUS forecast by CO₂ end point - Storage and enhanced oil recovery

11.6. CCUS forecast by CO₂ end point - Emerging utilization

11.7. CCUS capacity forecast by capture type, Mtpa of CO₂

11.8. CCUS forecast by capture type - Direct Air Capture (DAC) capacity forecast

11.9. Point-source capture capacity forecast by CO2 source sector, Mtpa of CO2

11.10. Point-source carbon capture forecast by CO2 source

11.11. Point-source carbon capture forecast by CO2 source - power generation

11.12. Point-source carbon capture forecast by CO2 source - cement and steel

11.13. CCUS capture capacity by region, Mtpa of CO2

11.14. CCUS capture capacity by region - North America

11.15. CCUS capture capacity by region - Europe and UK

11.16. CCUS capture capacity by region - Asia Pacific, Middle East, and Rest of World

11.17. Changes since the Carbon Capture, Utilization, and Storage (CCUS) Markets 2025-2045 IDTechEx forecasts

12. COMPANY PROFILES

12.1. 8 Rivers

12.2. Airhive

12.3. Airrane: CCUS

12.4. Ardent

12.5. Atoco

12.6. Axens: DMX

12.7. Baker Hughes: Carbon Capture

12.8. Brentwood Industries: Structured Packing

12.9. Brineworks

12.10. Capso

12.11. Capsol Technologies

12.12. Captura

12.13. Carbon Blade

12.14. Carbon Neutral Fuels

12.15. Carbonbit Technologies

12.16. CarbonBridge

12.17. Chart Industries: CCUS

12.18. Clairity Tech

12.19. Climeworks

12.20. CO2 Lock

12.21. Concrete4Change

12.22. CyanoCapture

12.23. DACMA

12.24. eChemicles

12.25. Ecospray

12.26. Equatic

12.27. ESTECH

12.28. ExxonMobil: Methanol-to-Gasoline (MTG)

12.29. Fluor: Carbon Capture

12.30. FuelCell Energy

12.31. Heirloom

12.32. Holocene

12.33. Honeywell UOP: CO₂ Solutions

12.34. HYCO1

12.35. INERATEC

12.36. Infinium

12.37. ION Clean Energy

12.38. JCCL (Japan Carbon Cycle Labs)

12.39. Kawasaki Kisen Kaisha ("K" Line): CCUS

12.40. Mantel

12.41. Mission Zero Technologies

12.42. Mitsubishi Heavy Industries: KM CDR Process

12.43. MTR (Membrane Technology and Research)

12.44. Nippon Chemical Industrial: R&D areas

12.45. Nuada: MOF-Based Carbon Capture

12.46. OXCCU

12.47. Paebbl

12.48. Parallel Carbon

12.49. Phlair

12.50. Q Power

12.51. Saipem: Bluenzyme

12.52. Shell & Technip Energies Alliance: CANSOLV Carbon Capture Technology

12.53. Skytree

12.54. SLB Capturi

12.55. Sumitomo SHI FW: Carbon Capture

12.56. Svante

12.57. Syklea

12.58. UniSieve

12.59. Velocys

12.60. Yama

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|