リチウムイオン電池市場 2026-2036年:技術、プレーヤー、用途、展望、予測Li-ion Battery Market 2026-2036: Technologies, Players, Applications, Outlooks and Forecasts 電気自動車(EV)、エレクトロニクス、定置型エネルギー貯蔵システム(BESS)を含むアプリケーション市場、LFPやNMCを含むケミストリにセグメント化されたリチウムイオン電池を網羅する市場分析と10年予測 ... もっと見る

サマリー

電気自動車(EV)、エレクトロニクス、定置型エネルギー貯蔵システム(BESS)を含むアプリケーション市場、LFPやNMCを含むケミストリにセグメント化されたリチウムイオン電池を網羅する市場分析と10年予測

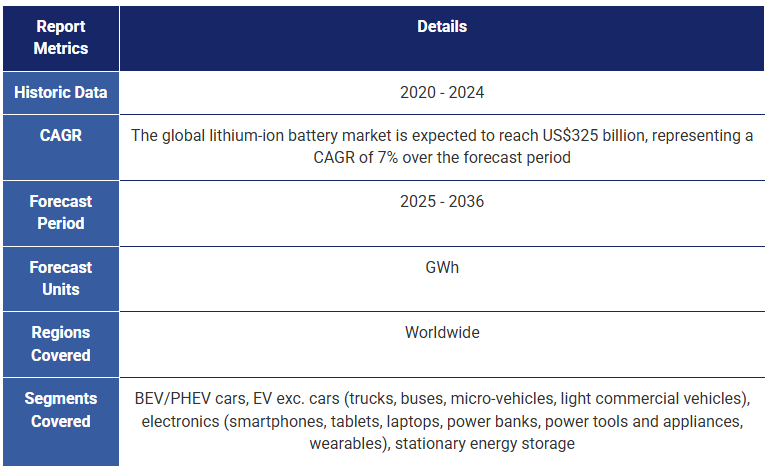

本レポートは、世界のリチウムイオン電池市場に関する洞察とマーケットインテリジェンスを提供し、個々の部品市場と4つの主要分野(電気自動車、その他の電気自動車、エレクトロニクス、定置型エネルギー貯蔵)の需要の両方をカバーします。予測は2026年から2036年までの10年間をカバーし、NMC、LFP、グラファイト負極、シリコン負極など、用途別とリチウムイオン電池のケミストリー別に市場を分類しています。製品例やプレーヤー分析も含まれています。

リチウム電池の種類出典IDTechEx

予測と市場分析

本レポートはリチウムイオン電池の需要動向に関する最新予測を提供し、予測期間中のリチウムイオン電池需要のCAGRを14.2%と予測している。主要市場分野の販売動向のボトムアップ分析、コスト分析、市場浸透動向の応用により作成した。2026年から2036年までの10年間をカバーし、技術、材料、市場占有率の内訳を含む。プレーヤーの分析と考察も含まれている。また、用途別に異なるセル化学の電気化学特性をベンチマークしている。

セル部品

リチウムイオン電池は多くの部品から形成され、それぞれがエネルギー密度や出力密度から重量やコストに至るまで、電池の電気化学的特性や材料特性に大きな役割を果たしている。本レポートでは、各コンポーネントの技術動向と市場動向について論じている。

製造予測

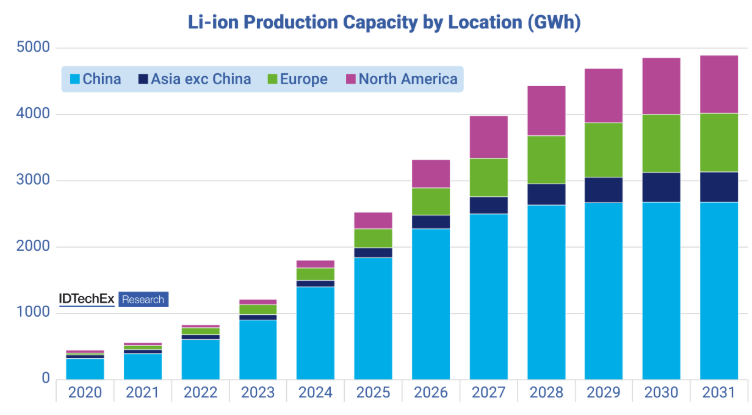

リチウムイオン電池メーカーは、大幅な需要増に備え、市場シェア争いを可能にするため、過剰生産能力の開発に注力してきた。この戦略により、世界の生産量をはるかに上回る製造能力が生み出されました。現在、世界生産の70%以上は中国が占めているが、今後5年間は米国と欧州が世界生産に占める割合が高まるだろう。本レポートでは、2031年までの生産能力の伸びを予測し、なぜ多くのギガファクトリーが遅延やキャンセルに見舞われるのかを解説する。

成長する市場

リチウムイオン電池の開発は、リチウムイオンが高いエネルギー密度を提供することから、当初はエレクトロニクス産業が牽引していた。最近では、電気自動車、特にバッテリー式電気自動車が市場を大きく成長させ、サプライヤーにギガファクトリーの開発と正極、負極、電解質の分野における技術革新を促している。電気自動車が主要地域、特に中国、欧州、米国でさらに採用・普及が進むにつれて、リチウムイオン電池市場は大幅な成長を遂げ、2036年には世界需要が5456TWhに拡大すると予想される。

民生用電子機器がリチウムイオンの開発を推進する当初の要因であったが、今後10年間は、販売の伸びが鈍化するため、民生用電子機器の需要は電気自動車と定置用エネルギー貯蔵の両方に駆逐されるであろう。しかし、リチウムイオンは価格が高いため収益が高く、依然として重要な市場分野である。

定置型エネルギー貯蔵は、今後10年間で大きな成長が見込まれる、もう一つの魅力的な機会である。これは主に再生可能エネルギー源への投資の増加によるもので、通常、エネルギーを貯蔵して電力供給を安定させるためにバッテリーの付随が必要となる。定置用エネルギー市場は、大規模な送電網への導入が主流だが、商業用や家庭用への導入も、データセンター向けなど、今後10年間で成長するだろう。

規制に関する考察

リチウムイオン電池市場は電気自動車と密接に結びついているため、規制は地域的にも世界的にも市場の成長に重要な役割を果たしている。中国では、電気自動車に対する長年にわたる税額控除、バッテリー開発業者に対する多額の補助金、政府による資金援助プロジェクトが大規模な逆風となり、バッテリー式電気自動車が広く採用されるようになった。こうした政策の結果、2024年には中国は世界の電気自動車市場の58%を占めるようになった。

欧州と米国では、規制は普及を支援する役割を果たしたものの、その成果は限定的であった。しかし、米国では2025年9月に電気自動車税額控除が停止され、電気自動車に対する一般的な政治的無関心もあって、短中期的には北米の電気自動車市場に大きな影響を与える可能性がある。ギガファクトリー計画も欧州と北米の両方で延期または中止されているが、これは間違いなく政府からの支援が限られているためである。これについては、本レポートで詳述する。

主要な側面

本レポートは、世界のリチウムイオン電池市場を概観し、4つの主要市場分野(バッテリー電気自動車、電気自動車、エレクトロニクス、定置型エネルギー貯蔵)と、すべての主要セルコンポーネントをカバーしている。

これには、

また、ギガファクトリーのスケジュールや拡張計画、用途別の販売動向、パックや化学物質別の材料コスト分析など、より広範な市場動向についても論じている。

また、今後10年間で需要やセルコストがどのように変化するかを、アプリケーション分野別、負極や正極の種類を含む化学分野別に区分して予測している。

目次1.要旨

1.1.リチウムイオン市場の動向

1.2.リチウムイオン市場の動向

1.3.リチウムイオン電池市場 - 地域別概要

1.4.リチウムイオン電池市場 - 地域別概要

1.5.リチウムイオン電池市場における地域政策

1.6.リチウムイオン電池市場における地域別の取り組みと政策

1.7.リチウムイオン電池市場における地域別の取り組みと政策

1.8.リチウムイオン電池市場における地域別の取り組みと政策

1.9.リチウムイオン電池市場における地域別の取り組みと政策

1.10.リチウムイオン電池のバリューチェーン

1.11.リチウムイオン電池市場のプレーヤー

1.12.世界の場所別セル容量拡大見通し

1.13.世界のギガファクトリー拡張の見通し

1.14.合成黒鉛と天然黒鉛の分割

1.15.リチウムイオン黒鉛負極のプレイヤー別市場

1.16.正極材の世界シェア推移

1.17.正極材化学物質別生産量見通し(kt)

1.18.正極メーカーシェア

1.19.2024年正極メーカーシェア

1.20.CAM価格動向

1.21.主要技術開発

1.22.主要技術開発

1.23.電池技術の新興企業

1.24.電池技術の新興企業 - 地域別の動き

1.25.主要技術の動向

1.26.リチウムイオンの性能と技術年表

1.27.リチウムイオンに代わるものはあるか?

1.28.リチウムイオン電池の用途別予測、GWh

1.29.リチウムイオン電池の用途別予測(億ドル)

1.30.正極別リチウムイオン市場、GWh

1.31.リチウムイオン電池正極の展望

1.32.負極別リチウムイオン電池市場、GWh

2.はじめに

2.1.リチウムイオンの重要性

2.2.リチウムイオン電池とは?

2.3.リチウム電池の化学物質

2.4.リチウム電池の種類

2.5.なぜリチウムなのか?

2.6.リチウム一次電池

2.7.ラゴンプロット

2.8.種類以上のリチウムイオン電池

2.9.市販の負極 - グラファイト

2.10.電池のトリレンマ

2.11.バッテリー・ウィッシュリスト

2.12.なぜ急速充電ができないのか?

2.13.材料レベルでのレート制限要因

2.14.急速充電の設計階層

2.15.はじめに - 主要な電池性能指標

2.16.市販セル化学物質の比較

2.17.ターンキー・バッテリー・パックに求められるトレードオフ

2.18.電気化学の定義 1

2.19.電気化学の定義 2

2.20.性能比較に役立つチャート

3.負極

3.1.負極によるリチウム電池の種類

3.2.負極材料の比較

3.3.負極材料の考察

3.4.負極材料の考察

3.5.リチウムイオン負極材料の比較

3.6.負極材料

3.7.黒鉛

3.8.黒鉛の紹介

3.9.LIB用天然黒鉛

3.10.被覆球状高純度黒鉛(CSPG)

3.11.合成/人造黒鉛製造

3.12.天然黒鉛負極と合成黒鉛負極の比較

3.13.天然黒鉛と人造黒鉛の比較

3.14.黒鉛価格引き下げの影響

3.15.合成黒鉛と天然黒鉛の性能

3.16.合成黒鉛と天然黒鉛の性能

3.17.合成黒鉛と天然黒鉛の性能

3.18.合成黒鉛と天然黒鉛の比較

3.19.合成黒鉛と天然黒鉛の結論

3.20.黒鉛の展望

3.21.黒鉛市場

3.22.リチウムイオン黒鉛負極材サプライヤー

3.23.プレーヤー別リチウムイオン黒鉛負極材市場

3.24.黒鉛負極材のプレーヤーシェア

3.25.黒鉛負極材市場の集中度

3.26.黒鉛負極材の地域別販売量

3.27.黒鉛生産能力

3.28.黒鉛生産の拡張

3.29.黒鉛負極材の新規参入

3.30.リチウムイオン黒鉛負極材価格

3.31.合成黒鉛と天然黒鉛の分割

3.32.シリコン負極材

3.33.シリコンの将来性

3.34.シリコン負極材の価値提案

3.35.シリコン負極材の課題

3.36.合金負極材

3.37.シリコンの比較-ハイレベルの概要

3.38.シリコン封入のソリューション

3.39.シリコン負極材のソリューション

3.40.主なシリコン負極材ソリューション

3.41.シリコン負極の特許譲渡先トップ3

3.42.特許譲渡先トップ3のシリコン負極技術比較

3.43.セルエネルギー密度はシリコン含有量と共に増加する

3.44.シリコン負極には大きな利点があるが、課題もある

3.45.シリコン負極の性能

3.46.シリコン負極の耐用年数

3.47.シリコン負極のコストメリット

3.48.シリコン負極のセルコスト対黒鉛

3.49.シリコン負極の環境面での利点

3.50.シリコン負極の性能に関する結論

3.51.現在のシリコン使用

3.52.シリコンとLFP

3.53.民生機器におけるシリコン

3.54.商業化のスケジュールに関する議論

3.55.シリコン負極の新興企業に対する戦略的パートナーシップと契約

3.56.シリコンEV電池技術の注目すべきプレーヤー

3.57.シリコン負極への既存企業の関与

3.58.商用シリコン負極の仕様

3.59.テジュSiO仕様

3.60.シリコン負極材 - ユミコア

3.61.シリコン負極材 - Wacker Chemie

3.62.商用シリコン負極市場

4.正極

4.1.正極の紹介

4.2.リチウムイオン正極の概要

4.3.リチウムイオン正極技術

4.4.正極の総括

4.5.正極材料 - LCOとLFP

4.6.正極材料 - NMC、NCA、LMO

4.7.正極の性能比較

4.8.正極比較

4.9.正極の比較

4.10.正極によるエネルギー密度

4.11.市販セル化学物質の比較

4.12.層状酸化物正極の理解

4.13.民生機器用正極材料

4.14.正極粉末合成(NMC)

4.15.正極化学の複雑さ

4.16.NMCの開発-111から811へ

4.17.正極材料 - NCA

4.18.高ニッケル及び超高ニッケルNMCの利点

4.19.高ニッケル/ニッケルリッチのサイクル寿命と安定性の問題

4.20.高ニッケル層状酸化物の主要課題

4.21.高ニッケルカソード安定化への道

4.22.高ニッケルカソードへの道

4.23.高ニッケルカソードへの道

4.24.高ニッケルカソードへの道

4.25.高ニッケルカソードへの道

4.26.単結晶NCAカソード

4.27.超高ニッケルカソードのタイムライン

4.28.高ニッケルの展望-解説

4.29.LFP IP

4.30.電気自動車へのLFP採用

4.31.LFPとNMCの比較

4.32.正極メーカーのロードマップ

4.33.先進正極技術とプレーヤー

4.34.先進カソード技術とプレーヤー

4.35.正極の適合性

4.36.リチウムイオン正極の技術開発

4.37.リチウムイオン正極の技術開発

4.38.先進・次世代リチウムイオン正極の詳細は...

4.39.正極市場

4.40.正極市場の概要

4.41.正極メーカーの生産能力

4.42.正極メーカーの生産能力

4.43.正極メーカー-販売量

4.44.正極メーカーシェア

4.45.正極メーカーシェア

4.46.2024年正極メーカーシェア

4.47.2024 LFP正極メーカー

4.48.LFP正極メーカー別販売量

4.49.LFP用正極メーカー:生産能力別

4.50.LFP正極メーカーシェア

4.51.2023 NMC/NCA正極メーカー

4.52.2024 NMC/NCA正極メーカー

4.53.NMC/NCA正極メーカー:販売数量別

4.54.NMC/NCA正極メーカー:生産能力別

4.55.NMC/NCA正極メーカーシェア

4.56.2024年正極市場:地域別

4.57.2024年の正極市場:化学・地域別

4.58.2023年正極市場:化学・地域別

4.59.正極の地域別市場

4.60.正極の生産:地域別

4.61.正極の化学別生産量

4.62.正極合剤生産の広がり

4.63.化学別の生産能力増

4.64.正極の化学組成別生産量見通し(kt)

4.65.正極の化学組成別生産量見通し(GWh)

4.66.中国以外のLFP正極生産量

4.67.中国以外のLFP正極生産量

4.68.生産能力増の見通し

4.69.地域別生産能力の将来見通し

4.70.地域別生産能力の将来見通し

4.71.世界の電気自動車用正極の化学的性質

4.72.欧州のBEV車用正極シェア

4.73.米国のBEV車用正極シェア

4.74.中国のBEV車用正極シェア

4.75.地域別BEV車用正極シェア

4.76.世界の正極シェア推移

4.77.正極活物質(CAM)新規参入企業

4.78.正極コスト分析

4.79.正極材料の集約度

4.80.正極化学がリチウム消費に与える影響

4.81.原料価格動向

4.82.リチウム価格の下落傾向

4.83.リチウム価格の変動

4.84.CAM価格の動向

4.85.正極活物質市場価格

4.86.CAM価格のセル材料コストへの影響

4.87.リチウムイオン電池材料コストの動向

4.88.金属価格のNMC 811 $/kWhセル材料コストへの影響

4.89.金属価格の$/kWh LFPセル材料コストへの影響

4.90.NMC 811 と LFP の感度分析

4.91.新しい化学物質は、重要材料への依存度を低減する

4.92.新しい化学物質は、重要物質への依存度を低減する

5.バインダーと添加剤

5.1.なぜリチウムイオン電池には添加剤が必要なのか?

5.2.添加剤開発はトレードオフが原動力

5.3.電池添加剤の種類

5.4.バインダー

5.5.湿式/スラリーベースの電極処理

5.6.バインダーの特性と例

5.7.主なバインダーメーカー

5.8.導電性添加剤

5.9.アドバンスト・カーボンの概要

5.10.導電性添加剤のベンチマーク

5.11.導電性添加剤の主要メーカー

5.12.CNTの世界生産能力

5.13.リチウムイオン電池におけるCNTの主な供給関係

6.電解質

6.1.リチウムイオン電解質の開発

6.2.リチウムイオン電解質の紹介

6.3.電解質の分解

6.4.電解質添加剤 1

6.5.電解質添加剤 2

6.6.電解質添加剤 3

6.7.100万マイル」電池の開発

6.8.CATL添加剤関連特許

6.9.CATLの電解質添加剤特許例

6.10.電解質特許トピックの比較-主要電池メーカー

6.11.電解質特許トピックの比較-主要電解質プレーヤー

6.12.電解質技術の概要

6.13.電解液バリューチェーン

6.14.電解質メーカー

6.15.電解質サプライヤーの市場シェア

6.16.電解液市場

6.17.世界の電解液生産能力

6.18.電解液の地域別市場

6.19.電解質サプライヤー

6.20.固体電解質と固体電池の概要

6.21.固体電池の紹介

6.22.固体電解質の分類

6.23.固体電解質システムの比較

6.24.固体電解質技術のアプローチ

6.25.固体電解質の特徴の分析

6.26.固体電解質技術のまとめ

6.27.現在の電解質の課題と解決策

6.28.固体電解質材料の比較

6.29.SSB社の商業計画

6.30.SSB各社の商業計画

6.31.各社の技術概要

6.32.SSBの開発

7.セパレーター

7.1.セパレーターの紹介

7.2.セパレーター製造

7.3.ポリオレフィン・セパレーター

7.4.乾式・湿式セパレーターと仕様

7.5.製品仕様例

7.6.セパレーターのコーティング

7.7.セパレーターの革新

7.8.セパレーターの革新

7.9.主要セパレーター・プレーヤー

7.10.リチウムイオンセパレータープレーヤーの市場シェア

7.11.地域別セパレーター市場

8.集電体

8.1.リチウムイオン電池セル内の集電体はどこにあるのか?

8.2.集電体材料

8.3.銅箔の製造

8.4.集電体

8.5.穴あき箔

8.6.プラスチックおよび複合集電体

8.7.銅集電体の厚さ

8.8.銅箔厚さの動向

8.9.リチウムイオン銅箔集電体プレーヤー

8.10.銅集電体市場

8.11.集電体市場

8.12.銅集電体の動向

9.セルの設計と製造

9.1.リチウムイオン電池セル製造プロセス

9.2.LIB製造の電力需要

9.3.リチウムイオン電池製造のエネルギー消費量

9.4.ドライルームの必要性

9.5.電極スラリーの混合

9.6.セル製造

9.7.乾式電極処理

9.8.乾式電極処理の利点

9.9.乾式粉末析出法と潜在的バインダー

9.10.乾式電極プロセスの商業化

9.11.形成サイクル

9.12.セル設計の最適化

9.13.新しいセルメーカーはどのように競争するか

9.14.セル製造における主要開発

9.15.主要電池メーカーの技術動向

9.16.主要メーカーの技術動向

9.17.エネルギー密度向上のための選択肢

9.18.負極材料は高エネルギー密度化への重要なルートである

9.19.セル設計もエネルギー密度に最適化できる

9.20.電極の厚さは設計上の重要なレバーである

9.21.エネルギー密度は1200Wh/l、400Wh/kgを超えることができる

9.22.急速充電能力を向上させるオプション

9.23.急速充電能力の重要性が増している

9.24.複合電極設計の最適化はレート能力を改善できる

9.25.急速充電電池の開発

9.26.サイクル寿命向上の選択肢

9.27.サイクル寿命改善への様々なルート

9.28.サイクル寿命改善への様々なルート

9.29.サイクル寿命は高エネルギー化学物質にとって特に重要

9.30.CATLの劣化ゼロTENER電池

9.31.ナラダパワーのゼロ劣化バッテリー

9.32.CATLの劣化ゼロESS電池を支えるもの

9.33.劣化ゼロ」の主張で重要な役割を果たすと思われるプレリチウム化

9.34.正極のプレリチウム化添加剤

9.35.ゼロ劣化を主張する可能性を示すデータ

9.36.CATLプレリチウム化添加剤の特許例

9.37.CATLプレリチウム化添加剤の特許例

9.38."劣化ゼロ "バッテリーは複数の設計レバーを強調する

9.39.安全性向上のための選択肢

9.40.安全性を確保するために必要な全体設計アプローチ

9.41.安全のためのセル設計

9.42.固体電池は安全性を改善できる(保証はしない)

9.43.パック設計はリチウムイオン電池の安全性に寄与する

9.44.セルコストはどこまで下げられるか?

9.45.まとめ

9.46.リチウムイオン電池メーカー

9.47.セル生産は大手が独占

9.48.セルメーカーの市場シェア

9.49.電気自動車用電池メーカーの地域別シェア

9.50.リチウムイオン電池生産の見通し

9.51.ギガファクトリーの建設期間は?

9.52.ギガファクトリー建設費用は?

9.53.ギガファクトリーの拡張計画

9.54.電池生産の見通し - 欧州

9.55.セル容量の拡大 - 欧州

9.56.電池生産の見通し - 北米

9.57.セル容量の拡大 - 北米

9.58.電池生産の見通し - アジア

9.59.電池容量拡大 - アジア

9.60.世界の場所別電池容量拡大見通し

9.61.世界のギガファクトリー拡張の見通し

9.62.場所別ギガファクトリー生産能力

9.63.リチウムイオン電池生産需給見通し

9.64.リチウムイオン電池生産需給見通し

9.65.セル容量拡大データ

9.66.リチウムイオン電池生産需給解説

10.コスト分析と予測

10.1.リチウムイオンのバリューチェーン

10.2.正極化学別のコスト

10.3.原材料価格の動向

10.4.リチウム価格の下落傾向

10.5.リチウム価格の変動

10.6.CAM価格の動向

10.7.リチウムイオン黒鉛負極価格

10.8.CAM価格のセル材料コストへの影響

10.9.金属価格のNMC 811 $/kWhセル材料コストへの影響

10.10.金属価格の$/kWh LFPセル材料コストへの影響

10.11.NMC 811とLFPの感度分析

10.12.リチウムイオン電池材料コストのトレンド

10.13.NMC 811のコスト内訳トレンド

10.14.LFPコストの内訳動向

10.15.過去のリチウムイオン電池価格

10.16.高ニッケルNMC材料コスト

10.17.リチウムイオン電池価格見通し

10.18.BEV車用バッテリー価格予測

11.電池パックとモジュール

11.1.リチウムイオン電池:セルからパックへ

11.2.セルとパック設計の変化

11.3.EV用電池のKPI

11.4.モジュール・パック設計

11.5.セル・ツー・パックとは?

11.6.セル・トゥ・パックの推進要因と課題

11.7.セル・ツー・シャーシ/ボディとは?

11.8.BYD Bladeバッテリー

11.9.CATL セル・ツー・パック

11.10.セル・トゥ・パックとセル・トゥ・ボディ設計のまとめ

11.11.重量エネルギー密度とセル・パック比

11.12.体積エネルギー密度とセル・パック比

11.13.セル・トゥ・パックかモジュールか?

11.14.セル・ツー・パックとセル・ツー・ボディ設計の展望

11.15.モジュールとパックの製造工程

11.16.セグメントによるパック設計の違い

11.17.電池パックの比較

11.18.バッテリーモジュール/パックの比較

11.19.ターンキーEVパックにおけるケミストリーの選択

11.20.電池パックメーカーの役割

11.21.電池パックメーカーの今後の役割

11.22.バッテリー管理システムの動向

11.23.BMSの中核機能

11.24.BMSの機能

11.25.BMSコアハードウェア

11.26.一般的なBMSブロック図

11.27.BMSトポロジー

11.28.BMSプレーヤー

11.29.BMSの革新

11.30.先進的なBMS活動

11.31.BEVの電圧上昇

11.32.800Vプラットフォームの推進要因

11.33.新たな800VプラットフォームとSiCインバータ

11.34.IDTechEx リチウムイオン電池タイムライン

12.電池市場と用途 .12.1 電気電子機器の電力範囲

12.2.アプリケーション電池の優先順位

12.3.アプリケーション電池の優先順位に関する議論

12.4.バッテリー電気自動車

12.5.地域別電気自動車販売台数 2015-2024

12.6.中国の購入補助金延長

12.7.EUの排出量と目標

12.8.米国の排出基準

12.9.セル形式市場シェア

12.10.その他の自動車カテゴリー

12.11.電気バス - グローバルな展望

12.12.2045年までに地域的に多様化すると予測される電気バス販売

12.13.バスのバッテリー容量の増加

12.14.電気バスに使用される化学物質

12.15.中国市場はLFP有利、欧州市場は混在

12.16.バッテリーサプライヤーとOEMの関係

12.17.電動LCV:推進要因と障壁

12.18.欧州の電動LCVの歴史的販売台数

12.19.中国の過去の電動LCV販売台数

12.20.LCVの航続距離要件

12.21.商用電気自動車のサイクル寿命要件

12.22.eLCVのIDTechEx見通し

12.23.コロナウイルスからの回復対応可能なトラック市場 2019-2022

12.24.世界の主要Eトラックメーカー販売台数 2021年~2023年上半期

12.25.BEVとFCEVのM&HDトラック:重量とバッテリー容量

12.26.EトラックOEMのバッテリー化学の選択

12.27.トラック用バッテリー化学の例

12.28.電動中型・大型トラック

12.29.地域別トラック市場

12.30.マイクロEVの紹介

12.31.主要な電動二輪車市場のあるアジア

12.32.インド電動二輪・三輪車市場の成長

12.33.中国電動二輪車市場の歴史

12.34.中国とインド:主要な三輪車市場

12.35.マイクロカー:都市型EVのゴルディロックス

12.36.マイクロEVの特徴

12.37.マイクロカーの平均バッテリー容量

12.38.マリン市場のまとめ

12.39.電気・ハイブリッド船舶の市場促進要因のまとめ

12.40.舶用電池市場の歴史 2019~2025年:サブセクター別:フェリー、クルーズ、RORO、貨物、OSV、タグ、その他

12.41.舶用バッテリーがユニークな理由

12.42.電子機器と電動工具

12.43.民生用電子機器 - バッテリーと機器の価格比

13.予測

13.1.リチウムイオン電池の用途別予測、GWh

13.2.リチウムイオン電池の用途別予測、データ

13.3.リチウムイオン電池の用途別予測, $B

13.4.リチウムイオン電池の用途別予測, $B

13.5.リチウムイオン電池需要シェア

13.6.リチウムイオン予測, GWh

13.7.リチウムイオンEV予測、GWh

13.8.リチウムイオンエレクトロニクス予測、GWh

13.9.リチウムイオンBEV自動車市場:正極別、GWh

13.10.リチウムイオン電池正極別市場:GWh

13.11.リチウムイオン電池正極の展望

13.12.負極別リチウムイオン電池市場 (GWh)

Summary

Market analysis and ten-year forecast covering lithium-ion batteries, segmented into application markets including electric vehicles (EVs), electronics and stationary energy storage systems (BESS), and chemistries, including LFP and NMC

This report provides insight and market intelligence into the global lithium-ion battery market, covering both individual component markets and demand across four major sectors (electric car, other electric vehicle, electronics and stationary energy storage). The forecast covers a ten-year period from 2026-2036, breaking down the market by both application and lithium-ion battery chemistry, including NMC, LFP, graphite-anode, silicon-anode and more. Example products and player analysis are also included.

Types of lithium battery. Source: IDTechEx

Forecasts and market analysis

This report provides an up-to-date forecast of lithium-ion battery demand trends, and predicts a CAGR of 14.2% for lithium-ion demand over the forecast period. It was produced through bottom-up analysis of sales trends in major market sectors and application of cost analysis and market penetration trends. It covers a ten-year period between 2026 and 2036 and includes a breakdown of technologies, materials and market uptake. Player analysis and discussion is also included. The report also benchmarks the electrochemical properties of different cell chemistries for different applications.

Cell components

A lithium-ion cell is formed from many components, each of which plays a major role in the cell's electrochemical and material properties, from energy density and power density to weight and cost. This report discusses technological and market trends for each component, including

Manufacturing forecast

Lithium-ion battery players have focused on developing overcapacity, to prepare for significant increases in demand, and to enable competition for market share. This strategy has resulted in manufacturing capacity far in excess of global production. More than 70% of global manufacturing is currently based in China, however the US and Europe will gain increasing shares of global production over the next five years. This report forecasts growth in production capacity until 2031, and breaks down why so many gigafactories see delays and cancellations.

A growing market

Development of lithium-ion batteries was driven initially by the electronics industry, due to lithium-ion offering high energy density. More recently, electric vehicles, especially battery electric cars, have led to significant growth in the market, driving suppliers to develop gigafactories and innovate in the cathode, anode and electrolyte spaces. As electric vehicles see further adoption and rollout across major regions, especially China, Europe and the US, the lithium-ion battery market will see significant growth, with global demand expected to grow to 5.456 TWh by 2036.

While consumer electronics was the initial factor driving development of lithium-ion, demand for consumer electronics will be eclipsed by both electric vehicles and stationary energy storage over the next decade, due to slower sales increases. However, it remains a significant market sector due to higher prices and therefore higher revenue.

Stationary energy storage is another compelling opportunity, expected to see significant growth over the next decade. This is driven primarily by increasing investment in renewable energy sources, which usually require battery accompaniment in order to store energy and stabilize power supply. The stationary energy market is dominated by large-scale grid deployments, but commercial and residential deployments will also grow over the next decade, e.g. for data centers.

A discussion of regulation

As the lithium-ion battery market is closely tied to electric vehicles, regulation plays a significant role in the market's growth, both regionally and globally. In China, years of tax credits for electric vehicles, significant subsidies for battery developers and government funding projects saw a massive headwind and wide adoption of battery electric cars. In 2024, China accounted for 58% of the global electric vehicle market as a result of these policies.

Regulation has seen more limited success in Europe and in the US, though it has played a role in assisting with rollout. However, the suspension of the electric vehicle tax credit in the US in September 2025, as well as general political apathy towards electric vehicles may have significant effects on the North American electric vehicle market in the short-medium term. Gigafactory plans have also been delayed or cancelled in both Europe and North America, arguably due to limited support from government. This is discussed in more detail in the report.

Key Aspects

This report provides an overview of the global lithium-ion battery market, covering four major market sectors (battery electric car, electric vehicle, electronics and stationary energy storage), and all major cell components.

This includes material and cost analysis and market trends for

The report also discusses wider market trends, including gigafactory timelines and expansion plans, sales trends in different applications and material cost analysis for different packs and chemistries.

A forecast is also provided, discussing how demand and cell costs will change over the course of the next decade, segmented by application area and by chemistry, including anode and cathode type.

Table of Contents1. EXECUTIVE SUMMARY

1.1. Trends in the Li-ion market

1.2. Trends in the Li-ion market

1.3. Li-ion market - regional overview

1.4. Li-ion market - regional overview

1.5. Regional policies in the Li-ion battery market

1.6. Regional efforts and policies in the Li-ion battery market

1.7. Regional efforts and policies in the Li-ion battery market

1.8. Regional efforts and policies in the Li-ion battery market

1.9. Regional efforts and policies in the Li-ion battery market

1.10. Li-ion value chain

1.11. Li-ion market players

1.12. Global cell capacity expansions outlook by location

1.13. Global gigafactory expansions outlook

1.14. Synthetic and natural graphite split

1.15. Li-ion graphite anode market by player

1.16. Global cathode market share trend

1.17. Cathode production outlook by chemistry, kt

1.18. Cathode manufacturer market share

1.19. Cathode market by manufacturer share 2024

1.20. CAM price trend

1.21. Key technology developments

1.22. Key technology developments

1.23. Battery technologies - start-up activity

1.24. Battery technology start-ups - regional activity

1.25. Key technology developments

1.26. Li-ion performance and technology timeline

1.27. Are there alternatives to Li-ion?

1.28. Li-ion battery forecast by application, GWh

1.29. Li-ion battery forecast by application, $B

1.30. Li-ion market by cathode, GWh

1.31. Li-ion battery cathode outlook

1.32. Li-ion market by anode, GWh

2. INTRODUCTION

2.1. Importance of Li-ion

2.2. What is a Li-ion battery?

2.3. Lithium battery chemistries

2.4. Types of lithium battery

2.5. Why lithium?

2.6. Primary lithium batteries

2.7. Ragone plots

2.8. More than one type of Li-ion battery

2.9. Commercial anodes - graphite

2.10. The battery trilemma

2.11. Battery wish list

2.12. Why can't you just fast charge?

2.13. Rate limiting factors at the material level

2.14. Fast charge design hierarchy

2.15. Introduction - key battery performance metrics

2.16. Comparing commercial cell chemistries

2.17. Turnkey battery packs highlight trade-offs required

2.18. Electrochemistry definitions 1

2.19. Electrochemistry definitions 2

2.20. Useful charts for performance comparison

3. ANODES

3.1. Types of lithium battery by anode

3.2. Anode materials comparison

3.3. Anode materials discussion

3.4. Anode materials discussion

3.5. Li-ion anode materials compared

3.6. Anode materials

3.7. Graphite

3.8. Introduction to graphite

3.9. Natural graphite for LIBs

3.10. Coated spherical purified graphite (CSPG)

3.11. Synthetic/artificial graphite production

3.12. Comparing natural and synthetic graphite anodes

3.13. Comparing natural and synthetic graphite

3.14. Impact of graphite price reduction

3.15. Performance of synthetic and natural graphite

3.16. Performance of synthetic and natural graphite

3.17. Performance of synthetic and natural graphite

3.18. Synthetic vs natural graphite overview

3.19. Synthetic vs natural graphite conclusions

3.20. Graphite outlook

3.21. Graphite market

3.22. Li-ion graphite anode suppliers

3.23. Li-ion graphite anode market by player

3.24. Graphite anode player shares

3.25. Graphite anode market concentration

3.26. Graphite anode sales volume by region

3.27. Graphite production capacity

3.28. Expansions in graphite production

3.29. New entrants in graphite anodes

3.30. Li-ion graphite anode prices

3.31. Synthetic and natural graphite split

3.32. Silicon anodes

3.33. The promise of silicon

3.34. Value proposition of silicon anodes

3.35. The challenges of silicon anode material

3.36. Alloy anode materials

3.37. Comparing silicon - a high-level overview

3.38. Solutions for silicon incorporation

3.39. Solutions for silicon incorporation

3.40. Key silicon anode material solutions

3.41. Top Si-anode patent assignee topics

3.42. Top 3 patent assignee Si-anode technology comparison

3.43. Cell energy density increases with silicon content

3.44. Silicon anodes offer significant benefits but also challenges

3.45. Silicon anode performance

3.46. Silicon anode calendar life

3.47. Silicon anode cost benefits

3.48. Silicon anode cell cost vs graphite

3.49. Silicon anode environmental benefits

3.50. Concluding remarks on Si-anode performance

3.51. Current silicon use

3.52. Silicon and LFP

3.53. Silicon in consumer devices

3.54. Discussion on commercialisation timelines

3.55. Strategic partnerships and agreements developing for silicon anode start-ups

3.56. Notable players for silicon EV battery technology

3.57. Established company involvement in silicon anodes

3.58. Commercial silicon anode specification

3.59. Daejoo SiO specifications

3.60. Silicon anode material - Umicore

3.61. Silicon anode material - Wacker Chemie

3.62. Commercial silicon anode market

4. CATHODES

4.1. Cathode introduction

4.2. Overview of Li-ion cathodes

4.3. Li-ion cathode technologies

4.4. Cathode recap

4.5. Cathode materials - LCO and LFP

4.6. Cathode materials - NMC, NCA and LMO

4.7. Cathode performance comparison

4.8. Cathode comparisons

4.9. Cathode comparisons

4.10. Energy density by cathode

4.11. Comparing commercial cell chemistries

4.12. Understanding layered oxide cathodes

4.13. Cathode materials for consumer devices

4.14. Cathode powder synthesis (NMC)

4.15. Complexity of cathode chemistry

4.16. NMC development - from 111 to 811

4.17. Cathode materials - NCA

4.18. Benefits of high and ultra-high nickel NMC

4.19. High-Ni / Ni-rich cycle life and stability issues

4.20. Key issues with high-nickel layered oxides

4.21. Routes to high nickel cathode stabilisation

4.22. Routes to high-nickel cathodes

4.23. Routes to high-nickel cathodes

4.24. Routes to high-nickel cathodes

4.25. Routes to high-nickel cathodes

4.26. Single crystal NCA cathode

4.27. Ultra-high nickel cathode timelines

4.28. Outlook on high-Ni - commentary

4.29. LFP IP

4.30. LFP adoption in electric vehicles

4.31. LFP vs NMC

4.32. Cathode player roadmaps

4.33. Advanced cathode technologies and players

4.34. Advanced cathode technologies and players

4.35. Cathode suitability

4.36. Li-ion cathode technology developments

4.37. Li-ion cathode technology developments

4.38. For more info on advanced and next-generation Li-ion cathodes...

4.39. Cathode market

4.40. Cathode market overview

4.41. Cathode player manufacturing capacities

4.42. Cathode manufacturers - production capacity

4.43. Cathode manufacturers by sales volume

4.44. Cathode manufacturer market share

4.45. Cathode manufacturer market share

4.46. Cathode market by manufacturer share 2024

4.47. 2024 LFP cathode manufacturers

4.48. LFP cathode manufacturers by sales volume

4.49. LFP cathode manufacturers by production capacity

4.50. LFP cathode manufacturer market share

4.51. 2023 NMC/NCA cathode manufacturers

4.52. 2024 NMC/NCA cathode manufacturers

4.53. NMC/NCA cathode manufacturers by sales volume

4.54. NMC/NCA cathode manufacturers by Production capacity

4.55. NMC/NCA cathode manufacturer market share

4.56. 2024 cathode market by region

4.57. 2024 cathode market by chemistry and region

4.58. 2023 cathode market by chemistry and region

4.59. Cathode market by region

4.60. Cathode production by region

4.61. Cathode production by chemistry

4.62. Cathode chemistry production spread

4.63. Capacity additions by chemistry

4.64. Cathode production outlook by chemistry, kt

4.65. Cathode production outlook by chemistry, GWh

4.66. LFP cathode production outside China

4.67. LFP cathode production outside China

4.68. Production capacity growth outlook

4.69. Future production capacity outlook by region

4.70. Future production capacity outlook by region

4.71. Global battery electric car cathode chemistry split

4.72. Europe BEV car cathode share

4.73. US BEV car cathode share

4.74. China BEV car cathode share

4.75. BEV cathode share by region

4.76. Global cathode market share trend

4.77. New cathode active material (CAM) entrants

4.78. Cathode cost analysis

4.79. Cathode material intensities

4.80. Cathode chemistry impact on lithium consumption

4.81. Raw material price trends

4.82. Lithium prices trending down

4.83. Lithium price volatility

4.84. CAM price trend

4.85. Cathode active material market prices

4.86. Impact of CAM prices on cell material costs

4.87. Li-ion cell material cost trends

4.88. Impact of metal prices on NMC 811 $/kWh cell material costs

4.89. Impact of metal prices on $/kWh LFP cell material costs

4.90. NMC 811 and LFP sensitivity analyses

4.91. New chemistries offer reduced reliance on critical materials

4.92. New chemistries offer reduced reliance on critical materials

5. BINDERS AND ADDITIVES

5.1. Why Do Li-ion Batteries Need Additives?

5.2. Additive Development is Driven by Tradeoffs

5.3. Types of Battery Additives

5.4. Binders

5.5. Wet/Slurry-Based Electrode Processing

5.6. Binder Properties & Examples

5.7. Key Binder Manufacturers

5.8. Conductive Additives

5.9. Overview of Advanced Carbon

5.10. Benchmarking of Conductive Additives

5.11. Key Manufacturers of Conductive Additives

5.12. Global Production Capacity of CNTs

5.13. Key Supply Relationships for CNTs in Li-ion Batteries

6. ELECTROLYTES

6.1. Developments in Li-ion electrolytes

6.2. Introduction to Li-ion electrolytes

6.3. Electrolyte decomposition

6.4. Electrolyte additives 1

6.5. Electrolyte additives 2

6.6. Electrolyte additives 3

6.7. Developments for the "million mile" battery

6.8. CATLs additive related patent

6.9. CATL electrolyte additive patent example

6.10. Electrolyte patent topic comparisons - key battery players

6.11. Electrolyte patent topic comparisons - key electrolyte players

6.12. Electrolyte technology overview

6.13. Electrolyte value chain

6.14. Electrolyte manufacturers

6.15. Electrolyte supplier market shares

6.16. Electrolyte market

6.17. Global electrolyte production capacity

6.18. Electrolyte market by region

6.19. Electrolyte suppliers

6.20. Overview of solid electrolytes and solid-state batteries

6.21. Introduction to solid-state batteries

6.22. Classifications of solid-state electrolyte

6.23. Comparison of solid-state electrolyte systems

6.24. Solid-state electrolyte technology approach

6.25. Analysis of SSB features

6.26. Summary of solid-state electrolyte technology

6.27. Current electrolyte challenges and solutions

6.28. Solid electrolyte material comparison

6.29. SSB company commercial plans

6.30. SSB company commercial plans

6.31. Technology summary of various companies

6.32. SSB developments

7. SEPARATORS

7.1. Introduction to Separators

7.2. Separator manufacturing

7.3. Polyolefin separators

7.4. Dry and wet separators and specifications

7.5. Product specification examples

7.6. Separator coatings

7.7. Innovation in separators

7.8. Innovation in separators

7.9. Key separator players

7.10. Li-ion separator player market shares

7.11. Separator market by region

8. CURRENT COLLECTORS

8.1. Where are the current collectors in a Li-ion battery cell?

8.2. Current collector materials

8.3. Copper foil production

8.4. Current collectors

8.5. Perforated foils

8.6. Plastic and composite current collectors

8.7. Copper current collector thickness

8.8. Trends in copper foil thickness

8.9. Li-ion copper foil current collector players

8.10. Copper current collector market

8.11. Current collector market

8.12. Trends in copper current collectors

9. CELL DESIGN AND MANUFACTURING

9.1. Li-ion battery cell manufacturing process

9.2. Power demand of LIB production

9.3. Energy consumption of Li-ion cell production

9.4. The need for a dry room

9.5. Electrode slurry mixing

9.6. Cell production

9.7. Dry Electrode Processing

9.8. Benefits of Dry Electrode Processing

9.9. Dry Powder Deposition Methods & Potential Binders

9.10. Commercialization of Dry Electrode Processes

9.11. Formation cycling

9.12. Cell design optimisations

9.13. How will new cell manufacturers compete

9.14. Key developments in cell manufacturing

9.15. Technology trends of major battery manufacturers

9.16. Technology trends of major manufacturers

9.17. Options for improving energy density

9.18. Anode materials are a key route to higher energy density

9.19. Cell design can also be optimised for energy density

9.20. Electrode thickness an important design lever

9.21. Energy density can exceed 1200 Wh/l and 400 Wh/kg

9.22. Options for improving fast-charge capability

9.23. Fast charge capability increasingly important

9.24. Composite electrode design optimisation can improve rate capability

9.25. Fast-charging battery developments

9.26. Options for improving cycle life

9.27. Various routes to improving cycle life

9.28. Various routes to improving cycle life

9.29. Cycle life particularly important for high energy chemistries

9.30. CATL's zero degradation TENER battery

9.31. Narada Power's zero-degradation battery

9.32. What underpins CATL's zero degradation ESS battery

9.33. Pre-lithiation likely to play key role in 'zero-degradation' claim

9.34. Cathode pre-lithiation additives

9.35. Data highlights the possibility for claiming zero-degradation

9.36. CATL pre-lithiation additive patent example

9.37. CATL pre-lithiation additive patent example

9.38. "Zero-degradation" battery highlights multiple design levers

9.39. Options for improving safety

9.40. Holistic design approach needed to ensure safety

9.41. Cell design for safety

9.42. Solid-state batteries can improve (but don't guarantee) safety

9.43. Pack design contributes to Li-ion battery safety

9.44. How low can cell costs go?

9.45. Concluding remarks

9.46. Li-ion cell manufacturers

9.47. Large players dominate cell production

9.48. Cell manufacturer market shares

9.49. Electric car battery manufacturer share by region

9.50. Li-ion battery production outlook

9.51. How long to build a Gigafactory?

9.52. How much to build a Gigafactory?

9.53. Gigafactory expansion plans

9.54. Battery production outlook - Europe

9.55. Cell capacity expansions - Europe

9.56. Battery production outlook - North America

9.57. Cell capacity expansion - North America

9.58. Battery production outlook - Asia

9.59. Cell capacity expansion - Asia

9.60. Global cell capacity expansions outlook by location

9.61. Global gigafactory expansions outlook

9.62. Gigafactory capacity by location

9.63. Li-ion battery production supply and demand outlook

9.64. Li-ion battery production supply and demand outlook

9.65. Cell capacity expansions data

9.66. Li-ion battery production supply and demand commentary

10. COST ANALYSES AND FORECASTS

10.1. Li-ion value chain

10.2. Cost by cathode chemistry

10.3. Raw material price trends

10.4. Lithium prices trending down

10.5. Lithium price volatility

10.6. CAM price trend

10.7. Li-ion graphite anode prices

10.8. Impact of CAM prices on cell material costs

10.9. Impact of metal prices on NMC 811 $/kWh cell material costs

10.10. Impact of metal prices on $/kWh LFP cell material costs

10.11. NMC 811 and LFP sensitivity analyses

10.12. Li-ion cell material cost trends

10.13. NMC 811 cost breakdown trend

10.14. LFP cost breakdown trend

10.15. Historic Li-ion cell prices

10.16. High nickel NMC material cost

10.17. Li-ion cell price forecast

10.18. BEV car battery price forecast

11. BATTERY PACKS AND MODULES

11.1. Li-ion Batteries: From Cell to Pack

11.2. Shifts in Cell and Pack Design

11.3. Battery KPIs for EVs

11.4. Modular pack designs

11.5. What is Cell-to-pack?

11.6. Drivers and Challenges for Cell-to-pack

11.7. What is Cell-to-chassis/body?

11.8. BYD Blade battery

11.9. CATL Cell to Pack

11.10. Cell-to-pack and Cell-to-body Designs Summary

11.11. Gravimetric Energy Density and Cell-to-pack Ratio

11.12. Volumetric Energy Density and Cell-to-pack Ratio

11.13. Cell-to-pack or modular?

11.14. Outlook for Cell-to-pack & Cell-to-body Designs

11.15. Module and pack manufacturing process

11.16. Differences in pack design by segment

11.17. Battery pack comparison

11.18. Battery module/pack comparison

11.19. Chemistry Choices in Turnkey EV Packs

11.20. Role of battery pack manufacturers

11.21. Future role for battery pack manufacturers

11.22. Trends in battery management systems

11.23. BMS core functionality

11.24. Functions of a BMS

11.25. BMS core hardware

11.26. Generic BMS block diagram

11.27. BMS topologies

11.28. BMS players

11.29. Innovations in BMS

11.30. Advanced BMS activity

11.31. Increasing BEV voltage

11.32. Drivers for 800V Platforms

11.33. Emerging 800V Platforms & SiC Inverters

11.34. IDTechEx Li-ion Battery Timeline

12. BATTERY MARKETS AND APPLICATIONS

12.1. Power range of electrical and electronic devices

12.2. Application battery priorities

12.3. Application battery priorities discussion

12.4. Battery electric cars

12.5. Regional Electric Car Sales 2015-2024

12.6. China Purchase Subsidies Extended

12.7. EU Emissions and Targets

12.8. US Emissions Standards

12.9. Cell Format Market Share

12.10. Other Vehicle Categories

12.11. Electric Buses - a Global Outlook

12.12. Electric Bus Sales Forecast to Regionally Diversify by 2045

12.13. Battery Capacity in Buses Increasing

12.14. Chemistries Used in Electric Buses

12.15. Chinese Market Favours LFP, European Market More Mixed

12.16. Battery Suppliers and OEM Relationships

12.17. Electric LCVs: Drivers and Barriers

12.18. Historic Electric LCV Sales in Europe

12.19. Historic Electric LCV Sales in China

12.20. LCV Range Requirement

12.21. Cycle life requirements for commercial electric vehicles

12.22. IDTechEx Outlook for eLCVs

12.23. Recovery from Coronavirus: Addressable Truck Market 2019-2022

12.24. Leading Global E-Truck Manufacturer Sales 2021- H1 2023

12.25. BEV and FCEV M&HD Trucks: Weight vs Battery Capacity

12.26. E-Truck OEM Battery Chemistry Choice

12.27. Truck Battery Chemistry Examples

12.28. Electric medium and heavy duty trucks

12.29. Regional Truck markets

12.30. Introduction to Micro EVs

12.31. Asia Home to Major Electric Two-wheeler Markets

12.32. India Electric Two- and Three- wheeler Market Growth

12.33. China Electric Two-wheeler Market History

12.34. China and India: Major Three-wheeler Markets

12.35. Microcars: The Goldilocks of Urban EVs

12.36. Micro EV Characteristics

12.37. Average Battery Capacities of Microcars

12.38. Summary of Marine Markets

12.39. Summary of Market Drivers for Electric & Hybrid Marine

12.40. Marine Battery Market History 2019-2025 by Subsector: ferry, cruise, ro-ro, cargo, OSV, tug, other

12.41. Why Marine Batteries are Unique

12.42. Electronic devices and power tools

12.43. Consumer electronics - battery to device price ratios

13. FORECASTS

13.1. Li-ion battery forecast by application, GWh

13.2. Li-ion battery forecast by application, data

13.3. Li-ion battery forecast by application, $B

13.4. Li-ion battery forecast by application, $B

13.5. Li-ion battery demand share

13.6. Li-ion forecast, GWh

13.7. Li-ion EV forecast, GWh

13.8. Li-ion electronics forecast, GWh

13.9. Li-ion BEV car market by cathode, GWh

13.10. Li-ion market by cathode, GWh

13.11. Li-ion battery cathode outlook

13.12. Li-ion market by anode, GWh

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

関連レポート(キーワード「リチウム」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|