リチウムイオン電池とPFASフリー電池用添加剤 2026-2036:技術、プレーヤー、予測Additives for Li-ion Batteries & PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts リチウムイオンバインダー、乾式電極プロセス、導電性添加剤、電解質添加剤の20年予測。フッ素系、非フッ素系、PFASフリーの新たな代替品。PVDF、PTFE、カーボンブラック、CNT、グラフェン、LiTFSI、LiFSI、Li... もっと見る

サマリーリチウムイオンバインダー、乾式電極プロセス、導電性添加剤、電解質添加剤の20年予測。フッ素系、非フッ素系、PFASフリーの新たな代替品。PVDF、PTFE、カーボンブラック、CNT、グラフェン、LiTFSI、LiFSI、LiBOB。 IDTechExの調査レポート「リチウムイオン電池とPFASフリー電池用添加剤 2026-2036年:技術、プレーヤー、予測」は、急速に発展するリチウムイオン電池用添加剤市場を詳細に深堀しています。リチウムイオン電池のバインダー、導電性添加剤、電解質添加剤市場に関する重要な洞察を提供し、PFAS規制の脅威、新たな生産プロセス、シリコン負極の台頭などの要因が市場にどのような影響を与えるかを分析しています。10年間の詳細な予測では、添加剤市場が2036年までに180億米ドルを超えるビジネスチャンスに成長することを強調している。

電池添加剤とは何か

電池添加剤とは何かについて標準化された定義はないが、この用語は、特定の性能上の利点を提供するためにセル構成要素に少量添加される材料を説明するために使用される。これには、活物質、電解質溶媒、集電体など、セル内の主要コンポーネントは含まれません。その代わりに、IDTechExの報告書では、添加物をセルの構成要素に重量組成で10%以下添加される材料と定義している。

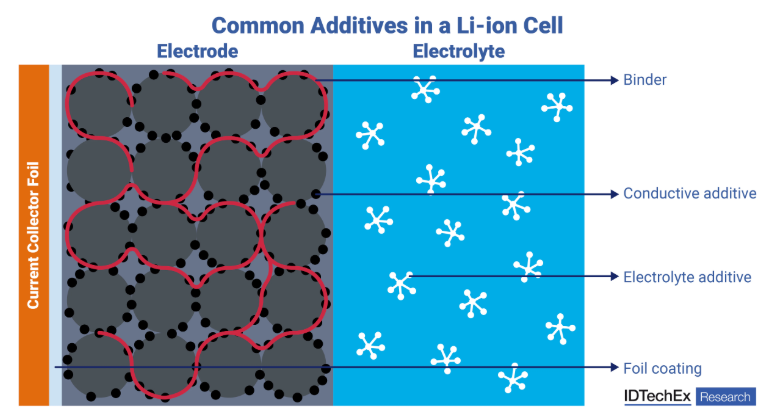

セル内での添加剤の役割とその潜在的な性能上の利点は、実に多様である。バインダーは、集電体、電極活物質、その他の添加剤をつなぎ合わせるポリマーであり、より耐久性があり長持ちする電極を形成する。PVDFは正極用の最も一般的なバインダーであり、CMC/SBRは負極に広く使用されている。カーボンブラックのような導電性添加剤は、電極内に導電性経路を形成し、容量を向上させ、適切な電子伝導性を確保するのに役立ちます。電解質添加剤は、リチウム塩、有機炭酸塩、フッ素、リン、ホウ素などを含む化合物など、その化学構造に驚くほど多様性がある。その用途も同様に多様で、耐食性からSEI形成、難燃性まで多岐にわたる。

IDTechExの「リチウムイオン電池とPFASフリー電池用添加剤2026-2036:技術、プレーヤー、予測」では、上記のすべての種類の電池添加剤を詳細に取り上げている。これら以外の集電体コーティング、分散剤、プレリチウム化添加剤などの添加剤も、リチウムイオン電池の生産と応用において重要な役割を果たしており、IDTechExのレポートでも取り上げられている。

電池添加剤の状況はどのように変化しているか

添加剤市場が急成長しているのは、EV、エネルギー貯蔵アプリケーション、家電製品によるリチウムイオンバッテリー需要の急増が大きく寄与している。世界の電動化が進むにつれて、リチウムイオンバッテリーに対する要求も用途によって異なるようになり、添加剤はこの差別化において重要な役割を果たすことになる。そのため、新しい添加剤材料の開発は、エネルギー密度とコストのニーズを確実に満たしながら、複数のパラメータに沿って電池性能を最適化し差別化する必要性によって推進されている。IDTechExの新レポートは、このレンズを通して添加剤を評価し、進化する電池産業において各添加剤が果たすべき役割を整理している。

添加剤の使用量にもトレードオフがある。添加剤は本質的に不活性な成分であり、セル全体の重量と体積を増加させる。添加剤の添加量は、添加剤がもたらす利点と、添加剤の使用に伴う潜在的なエネルギー密度低下との妥協点となり、メーカーは、望ましい性能レベルを達成するために、できるだけ添加剤を使用しないことを目指している。

本レポート「リチウムイオン電池およびPFASフリー電池用添加剤 2026-2036:技術、プレーヤー、予測」では、より広範な業界動向が電池の添加剤需要にどのような影響を及ぼすかについて掘り下げている。乾式電極プロセス(溶媒やスラリー形成を行わずに電極製造を行う)は、低コストで持続可能な製造手段として支持を集めている。しかし、乾式電極のバインダー需要は従来のプロセスとは全く異なり、PVDFやCMC/SBRがPTFEやその他多数の潜在的バインダーに取って代わられている。

導電性添加剤の分野でも変化が起きており、CNTやグラフェンの価格下落や商業化の進展は、カーボンブラックに取って代わりつつあることを意味する。IDTechExのレポートで強調されているように、シリコンアノードの成長も添加剤に対する独自の需要を生み出しており、シリコンはサイクル中に体積変化が大きいため、バインダー、導電性添加剤、電解質添加剤にわたって進歩が求められている。

PFAS規制は電池添加剤業界をどのように形成しているか

現在使用されている主な正極バインダーであるPVDFとPTFEはPFASポリマーであり、電解質添加剤として使用される他のPFASまたはフッ素系材料も数多くあります。PFASが健康や環境に与える影響に対する監視の目が厳しくなり、規制の脅威が迫っているため、リチウムイオン業界向けの非PFAS添加剤の開発が急増している。本レポート「リチウムイオン電池およびPFASフリー電池用添加剤2026-2036:技術、プレーヤー、予測」において、IDTechExは現在存在する非PFAS代替品について最先端の分析を行い、バインダーや電解質添加剤としての潜在的用途に焦点を当て、主要プレーヤーを強調し、この分野における最新の学術的ブレークスルーに光を当て、それらが添加剤市場をどのように混乱させる可能性があるかを明らかにした。

現代のバッテリー生産におけるPFASの偏在と、クリーンエネルギーへのニーズの加速は、PFASが産業界から容易に浄化されないことを意味する。しかし、新たな代替品、処理の改善、その他の適切な緩和戦略の間には、近い将来、バッテリー業界内でPFASを浄化するための複数の道があります。LeclancheやElyteのような企業が製品からPFASを除去するという最近の進展は、業界初のPFASフリー電池セルの商業化がそう遠くないことを示唆している。

「リチウムイオン電池とPFASフリー電池用添加剤2026-2036:技術、プレーヤー、予測」は、上記の動向とそれ以上をまとめ、リチウムイオン電池と電池添加剤産業の差し迫った変革に焦点を当てている。IDTechExのレポートでは、世界的な分析において主要な業績、経済、規制、その他の市場要因を考察している。主要プレーヤーと材料は、バインダー、導電性添加剤、電解質添加剤の幅広いクラスにわたってベンチマークされている。材料の需要と市場規模に関する10年間のきめ細かな予測を提供し、添加剤別にセグメント化することで、添加剤市場の成長に寄与する主な要因に関する重要な洞察を提供している。

主要な側面

本レポートは、リチウムイオン電池添加剤市場に関する以下のような重要な市場情報を提供します:

添加剤市場の分析

バインダー技術と動向

導電性添加剤市場の進化

電解質添加剤の動向

電池添加剤におけるPFAS浄化

市場予測

目次1.エグゼクティブ・サマリー

1.1.主な調査結果

1.2.添加剤はリチウムイオン電池の性能を最適化する

1.3.成長するリチウムイオン市場が添加剤需要を生み出す

1.4.独自のバインダーを用いた乾式電極処理が新たな選択肢に

1.5.複数の乾式加工法が検討されている

1.6.新しいバインダーは重要な基準を満たす必要がある

1.7.TRL1-9までに開発中の非PFAS正極バインダー

1.8.導電性添加剤はリチウムイオン動作に不可欠

1.9.導電性添加剤の比較

1.10.カーボンブラックは主要な導電性添加剤

1.11.電池におけるカーボンブラック性能の主な指標

1.12.導電性添加剤としてのCNTの台頭

1.13.CNTは価格と生産規模で異なる

1.14.加速するグラフェン導電性添加剤の商業化

1.15.電解質添加剤の重要性と多様性

1.16.電解質からのPFASの排除

1.17.電池添加剤材料の需要(キロトン) 2025-2036 添加剤タイプ別

1.18.電池添加剤市場規模(億米ドル) 2025-2036 添加剤タイプ別

1.19.バインダー材料の需要(キロトン) 2025-2036 材料別

1.20.導電性添加剤材料の需要(キロトン) 2025-2036 材料別

1.21.電解質添加剤材料の需要(キロトン) 2025-2036 タイプ別

1.22.電池添加剤材料の需要(キロトン) 2025-2036 材料別

1.23.IDTechEx サブスクリプションでさらにアクセス

2.リチウムイオン電池と添加剤の紹介

2.1.リチウムイオン電池の概要

2.1.1.リチウムイオン電池とは

2.1.2.リチウム電池の化学物質

2.1.3.なぜリチウムなのか?

2.1.4.主要市場とリチウムイオン電池の用途

2.1.5.EVによるリチウムイオン需要の拡大

2.1.6.リチウムイオン電池添加剤

2.1.7.なぜリチウムイオン電池に添加剤が必要なのか?

2.1.8.添加剤開発はトレードオフが原動力

2.1.9.電池添加剤の種類

2.1.10.IDTechEx 関連レポートの詳細情報

3.バインダー

3.1.スラリーベースの電極処理用バインダー

3.1.1.湿式/スラリーベースの電極加工

3.1.2.バインダーの特性と例

3.1.3.主要バインダーメーカー

3.1.4.カソード用代替バインダー

3.1.5.シリコンアノード用バインダー

3.1.6.特許(1)によるSi-アノードバインダーシステムの例

3.1.7.特許(2)からのSi-アノードバインダーシステムの例

3.1.8.Si-アノードバインダーシステムの例

3.2.乾式電極加工用バインダー

3.2.1.乾式電極加工

3.2.2.乾式電極処理の利点

3.2.3.乾式粉末析出法とバインダーの可能性

3.2.4.乾式電極プロセスの商業化

3.2.5.テスラ高分子フィブリル化の商業化

3.2.6.結果高分子フィブリル化

3.2.7.乾式スプレー蒸着の商業化

3.2.8.LGエネルギー貯蔵:乾式電極の商業化計画&特許分析

3.2.9.LGエネルギー貯蔵乾式電極の特許分析

3.2.10.ブルー・ソリューションズ溶融押出

3.2.11.パワーコ粉末圧縮の商業化

3.2.12.乾式電極プロセスの将来

4.導電性添加剤

4.1.導電性添加剤のベンチマーク

4.1.1.導電性添加剤

4.1.2.アドバンスト・カーボンの概要

4.1.3.導電性添加剤のベンチマーキング

4.1.4.導電性添加剤の主要メーカー

4.2.カーボンブラック

4.2.1.カーボンブラックの概要

4.2.2.カーボンブラックの製造工程

4.2.3.カーボンブラックの世界市場

4.2.4.電池におけるカーボンブラック性能の主な指標

4.2.5.ナノ粒子における無秩序炭素と黒鉛質炭素

4.2.6.Nouryon:ケッチェンブラック

4.2.7.イメリススーパーPとスーパーC65

4.2.8.ケッチェンブラックとスーパーPの比較:細孔径分布

4.2.9.キャボットLITXシリーズ カーボンブラック

4.2.10.ビルラカーボン

4.2.11.カーボンブラックの表面官能基化

4.3.グラファイト

4.3.1.黒鉛の特性と用途

4.3.2.合成黒鉛と天然黒鉛

4.3.3.導電性添加剤としての黒鉛

4.3.4.イメリスLシリーズ黒鉛

4.3.5.SGLカーボン

4.4.カーボンナノファイバー

4.4.1.カーボンナノファイバーの紹介

4.4.2.添加剤としてのカーボンナノファイバー

4.4.3.ナノファイバーの技術経済的評価

4.4.4.レゾナックVGCF

4.5.カーボンナノチューブ(CNT)

4.5.1.CNT入門

4.5.2.CNT:理想と現実

4.5.3.リチウムイオン電池におけるCNT

4.5.4.CNTの価格ポジション:SWCNTs vs. MWCNTs

4.5.5.CNTの世界生産能力

4.5.6.リチウムイオン電池におけるCNTの主な供給関係

4.5.7.結果リチウムイオン電極におけるCNT使用の影響(1)

4.5.8.結果リチウムイオン電極におけるCNT使用の影響(2)

4.5.9.結果SWCNTがLFPのサイクル寿命を改善

4.5.10.結果高 C レートでの性能向上

4.5.11.結果シリコンアノード用CNT

4.5.12.CNT分散の意義

4.5.13.キャボットカーボンナノ構造(CNS)

4.5.14.CNTを用いたハイブリッド導電性カーボン

4.5.15.CNTとカーボンブラックの組み合わせ

4.5.16.カーボンナノチューブ 2025-2035:市場、技術、プレーヤー

4.6.グラフェン

4.6.1.グラフェン入門

4.6.2.電池におけるグラフェンの役割

4.6.3.電池市場におけるグラフェンの主要プレーヤー(1)

4.6.4.電池市場におけるグラフェンの主要プレーヤー(2)

4.6.5.結果グラフェンは低負荷で性能を向上させる

4.6.6.グラフェンと他の導電性添加剤との組み合わせ

4.6.7.結果:グラフェンと他の導電性添加剤との組み合わせ

4.6.8.グラフェン生産の商業化

4.6.9.主要メーカーの製品仕様

4.6.10.電池用ハイドログラフ・グラフェン・スラリー

4.6.11.グラフェン市場&2D材料アセスメント 2024-2034:技術、市場、プレーヤー

5.電解質添加剤

5.1.電解質添加剤の紹介

5.1.1.リチウムイオン電解質の紹介

5.1.2.電解質添加剤の開発

5.1.3.電解質添加剤の台頭

5.1.4.電解質特許の比較-主要電池メーカー

5.1.5.電解質特許の比較-主要電解質メーカー

5.1.6.電解質添加剤の例

5.1.7.電解質バリューチェーン

5.2.電解質添加剤のカテゴリーと例

5.2.1.リチウム塩電解質添加剤

5.2.2.リチウム塩添加剤LiTFSI & LiFSI

5.2.3.リチウム塩添加剤LiTDI, LiTA, & LiBOB

5.2.4.Li塩添加剤:LiDFOBおよびその他のLi塩

5.2.5.有機炭酸塩添加剤

5.2.6.含硫黄・含ケイ素添加剤

5.2.7.フッ素系電解質添加剤

5.2.8.電解質・電解質添加剤の概要

5.3.主要サプライヤー&ケーススタディ

5.3.1.アルケマ

5.3.2.ソルベイ (1)

5.3.3.ソルベイ (2)

5.3.4.ティンチ・マテリアル

5.3.5.トリノヘックス・ウルトラ

5.3.6.電解質添加剤の新興企業:ハロカーボン & エリート イノベーションズ

5.3.7.電解質添加剤の新興企業:サウス8とニュー・ドミニオン

5.3.8.CATL添加剤関連特許(1)

5.3.9.CATL添加剤関連特許(2)

5.3.10.その他の電解質添加剤特許

6.その他の添加剤

6.1.箔コーティング

6.1.1.集電箔とコーティングの必要性

6.1.2.箔コーティングの種類

6.1.3.アルケマインセリオン水性箔コーティング

6.1.4.カーボンベースのコーティングアーマーフィルム&チャルコアルミニウム

6.1.5.LG: サーマル・サプレッション・コーティング

6.2.スラリー添加剤

6.2.1.電極スラリー & 添加剤の重要性

6.2.2.ケーススタディハンツマン

6.2.3.ケーススタディ花王-ルナエース

6.2.4.その他のケーススタディボレガード、カーギル、アルケマ

6.2.5.さらなるケーススタディエボニック&ダウ・ケミカル

6.3.プレリチウム化電極添加剤

6.3.1.プレリチウム化の必要性と主要戦略

6.3.2.正極プレリチウム化添加剤

6.3.3.プレリチウム化と「ゼロ劣化」電池

6.3.4.プレリチウム化添加剤の例:Catl (1)

6.3.5.プレリチウム化添加剤の例:CATL (2)

7.リチウムイオン電池添加剤におけるPFAS浄化

7.1.PFASの紹介

7.1.1.PFASの紹介

7.1.2.PFASの応用

7.1.3.PFASの悪影響をめぐる懸念の高まり

7.1.4.世界におけるPFAS規制

7.1.5.PFASはどこで電池に使われているのか

7.1.6.PFAS代替と管理

7.1.7.PFASに関するIDTechExレポート

7.2.バインダー中のPFAS除去

7.2.1.電池中のPFASバインダーの代替

7.2.2.非PFASポリマーの中から可能性のある結合剤を特定する

7.2.3.学術文献における水性バインダー

7.2.4.非PFAS正極水性バインダーのTRL

7.2.5.水性バインダーシステムの限界

7.2.6.ポリアクリル酸(PAA)

7.2.7.ルクランシェ水性PFASフリー電極

7.2.8.各国政府による非PFASバインダー研究への資金提供

7.2.9.UV硬化とエネルギー硬化バインダー

7.2.10.アテイオス・システムズエネルギー硬化型バインダー

7.2.11.ミルテックUVバインダー

7.2.12.ビヨンド・リチウムイオンリチウムイオン電池用バインダー

7.2.13.オント・テクノロジーリチウムイオン電池用PFASフリーバインダー&リサイクル

7.2.14.ナノラミックハイブリッドバインダー-導電性添加剤としてのナノカーボン

7.2.15.PFAS除去戦略としてのドライ電極

7.2.16.24M:バインダーの完全除去

7.2.17.PFAS管理戦略としてのリサイクル

7.2.18.リチウムイオン電池のリサイクルの種類

7.2.19.リチウムイオンリサイクル方法の結合剤への影響

7.2.20.バインダー回収のための直接電池リサイクル

7.2.21.バインダー回収のためのリチウムイオン電池リサイクル技術まとめ

7.2.22.バインダーリサイクルの商業的実現可能性

7.3.電解液中のPFAS除去

7.3.1.フッ素系電解質添加剤:機能と種類

7.3.2.SEI形成のための非PFASリチウム塩

7.3.3.E-Lyte:PFAS非含有電解質

7.3.4.SEI形成のための非PFAS炭酸塩および有機化合物

7.3.5.非PFAS難燃剤:リン酸塩系材料

7.3.6.非PFAS系難燃剤:より多くの非フッ素系代替品

7.3.7.HCE用非PFAS希釈剤

7.3.8.PFAS非含有電解質添加剤の概要

8.予測

8.1.予測方法

8.2.予測の前提

8.3.材料価格の前提(米ドル/kg)

8.4.電池添加剤材料の需要予測(キロトン) 2025-2036

8.5.電池添加剤の市場規模予測(10億米ドル) 2025-2036

8.6.バインダー材料の需要予測(キロトン) 2025-2036

8.7.バインダー材料の製造工程タイプ別需要予測(キロトン) 2025-2036

8.8.バインダー市場規模の予測(10億米ドル) 2025-2036

8.9.導電性添加剤材料の需要予測(キロトン) 2025-2036

8.10.導電性添加剤市場規模の予測(10億米ドル) 2025-2036

8.11.電解質添加剤材料の需要予測(キロトン) 2025-2036

8.12.電解質添加剤材料の需要予測:フッ素系 vs 非フッ素系 (キロトン) 2025-2036

8.13.リチウム塩電解質添加剤材料の需要予測(キロトン) 2025-2036

8.14.電解質添加剤市場規模の予測(10億米ドル) 2025-2036

8.15.フッ素系と非フッ素系の電解質添加剤市場規模の予測(10億米ドル) 2025-2036

8.16.リチウム塩電解質添加剤の市場規模予測(10億米ドル) 2025-2036

8.17.電池用添加剤の材料別総需要予測(キロトン) 2025-2036

8.18.電池添加剤の材料別総市場規模予測(10億米ドル) 2025-2036

9.企業プロファイル

9.1.IDTechExポータル上の企業プロファイルへのリンク

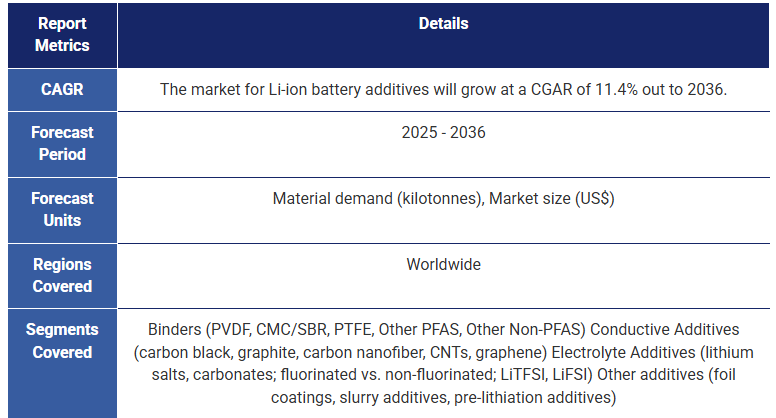

Summary20-year forecasts for Li-ion binders, dry electrode processes, conductive additives, & electrolyte additives. Fluorinated, non-fluorinated, PFAS-free emerging alternatives. PVDF, PTFE, carbon black, CNTs, graphene, LiTFSI, LiFSI, LiBOB. IDTechEx's report "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" provides a detailed deep-dive into the fast-evolving additives for Li-ion batteries market. The report provides crucial insights into the markets for binders, conductive additives, and electrolyte additives in Li-ion cells, analyzing how factors such as the threat of PFAS regulation, emerging production processes, and the rise of silicon anodes will impact the market. Granular 10-year forecasts highlight how the additives market will grow to be an over US$18 billion opportunity by 2036.

What are battery additives?

While there is no standardized definition of what a battery additive is, the term is used to describe materials that are added to cell components in small amounts to provide specific performance advantages. This does not include major components within the cell, such as active materials, electrolyte solvents, or current collectors. Instead, IDTechEx's report defines additives as materials that are added to a component of the cell in weight compositions of no more than 10%.

The role of additives within the cell and their potential performance advantages are immensely varied. Binders are polymers that hold together the current collector, electrode active materials, and other additives, forming an electrode that is more durable and longer-lasting. PVDF is the most common binder for cathodes and CMC/SBR is widely used in anodes. Conductive additives such as carbon black help create conductive pathways within the electrode that can improve its capacity and ensure proper electronic conductivity. Electrolyte additives possess incredible variety in their chemical structure - including materials such as lithium salts, organic carbonates, and compounds containing fluorine, phosphorus, boron, and more. Their applications are equally varied, ranging from corrosion resistance to SEI formation to flame retardance.

IDTechEx's "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" covers all of the above types of battery additives in great detail. Outside of these, other additives such as current collector coatings, dispersants, and pre-lithiation additives play important roles in the production and application of Li-ion cells which are also discussed in IDTechEx's report.

How is the battery additive landscape changing?

The additives market is growing quickly thanks in large part to the rapid increase in demand for Li-ion batteries from EVs, energy storage applications, and consumer electronics. As the world continues to electrify, different applications will exert different demands on their Li-ion cells, with additives set to play an important role in this differentiation. The development of new additive materials is therefore being driven by the need to optimize and differentiate battery performance along multiple parameters while ensuring that energy density and cost needs are still met. IDTechEx's new report evaluates additives through this lens, laying out the role each additive has to play in an evolving battery industry.

There are also tradeoffs to be found in the quantities of additives used. Additives are inherently inactive components that add weight and volume to the overall cell. Their loading quantities will be a compromise between the benefits they can provide and the potential energy density penalty that comes with their use, and manufacturers aim to use as little of an additive as possible to achieve their desired performance level.

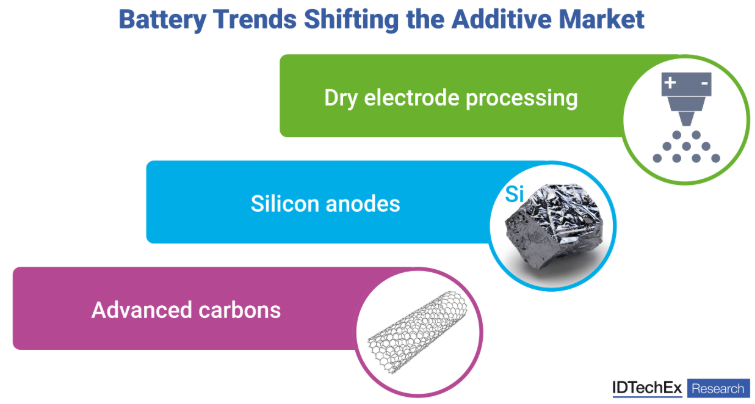

The "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" report dives into how wider industry trends affect additive demands of cells. Dry electrode processes - where electrode production is carried out without solvents or slurry formation - are gaining traction as a lower cost and more sustainable means of manufacturing. However, the binder demands of dry electrodes are wholly different than that of conventional processes, with PVDF and CMC/SBR making way for PTFE and a plethora of other potential binders.

Shifts are also taking place in the conductive additives space, where falling prices and growing commercialization of CNTs and graphene means they are supplanting carbon black. The growth of silicon anodes too creates unique demands for additives, with silicon's high volume change during cycling requiring advancements across binders, conductive additives, and electrolyte additives, as highlighted in the IDTechEx report.

How are PFAS regulations shaping the battery additives industry?

PVDF - the primary cathode binder used today - and PTFE are PFAS polymers, and there are plenty of other PFAS or otherwise fluorinated materials used as electrolyte additives too. With the increasing recent scrutiny around PFAS for its health and environmental impacts, and the looming threat of regulation, there has been a surge in development for non-PFAS additives for the Li-ion industry. In the "Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" report, IDTechEx has conducted state-of-the-art analysis into the non-PFAS alternatives that exist today, highlighting their potential uses as binders or electrolyte additives, emphasizing key players, shedding light on the most recent academic breakthroughs in the space and how they might disrupt the additive market.

The ubiquity of PFAS in modern-day battery production and the accelerating need for clean energy means that PFAS will not be easy to remediate from the industry. But between emerging alternatives, processing improvements, and other suitable mitigation strategies, there are multiple avenues for PFAS remediation within the battery industry in the near-term. Recent developments from players like Leclanche and Elyte in removing PFAS from their products suggest that the industry may not be far away from commercializing the first PFAS-free battery cells!

"Additives for Li-ion Batteries and PFAS-Free Batteries 2026-2036: Technologies, Players, Forecasts" brings together all of the above trends and more, highlighting the impending transformation of the Li-ion battery and battery additive industries. IDTechEx's report considers key performance, economic, regulatory, and other market factors in its global analysis. Key players and materials are benchmarked across a wide range of binder, conductive additive, and electrolyte additive classes. 10-year granular forecasts for material demand and market size are provided and segmented by additive, providing critical insights into the key contributors to the growth of the additive market.

Key Aspects

This report provides critical market intelligence into the market for Li-ion battery additives, including:

Analysis of the additive market landscape

Binder technologies and trends

Evolution of conductive additive markets

Electrolyte additive trends

PFAS remediation in battery additives

Market forecasts

Table of Contents1. EXECUTIVE SUMMARY

1.1. Key Report Findings

1.2. Additives Optimize Performance of Li-ion Batteries

1.3. Growing Li-ion Market Creates Demand for Additives

1.4. Dry Electrode Processing an Emerging Option with Unique Binders

1.5. Multiple Dry Processing Methods Being Explored

1.6. New Binders Must Meet Key Criteria

1.7. Non-PFAS Cathode Binders in Development By TRL 1-9

1.8. Conductive Additives are Critical to Li-ion Operation

1.9. Comparing Conductive Additives

1.10. Carbon Black is The Leading Conductive Additive

1.11. Key Measures of Carbon Black Performance in Batteries

1.12. CNTs On the Rise as Conductive Additives

1.13. CNTs Vary in Price & Production Scale

1.14. Commercialization of Graphene Conductive Additives Accelerating

1.15. Electrolyte Additives More Critical & Varied Than Ever

1.16. Eliminating PFAS From Electrolytes

1.17. Battery Additive Material Demand (kilotonnes) 2025-2036 By Additive Type

1.18. Battery Additive Market Size (US$ Billion) 2025-2036 By Additive Type

1.19. Binder Material Demand (kilotonnes) 2025-2036 By Material

1.20. Conductive Additive Material Demand (kilotonnes) 2025-2036 By Material

1.21. Electrolyte Additive Material Demand (kilotonnes) 2025-2036 By Type

1.22. Battery Additive Material Demand (kilotonnes) 2025-2036 By Material

1.23. Access More With an IDTechEx Subscription

2. INTRODUCTION TO LI-ION BATTERIES AND ADDITIVES

2.1. Li-ion Batteries Overview

2.1.1. What is a Li-ion Battery?

2.1.2. Lithium Battery Chemistries

2.1.3. Why Lithium?

2.1.4. Key Markets & Applications for Li-ion Batteries

2.1.5. EVs Generating Growing Li-ion Demand

2.1.6. Li-ion Battery Additives

2.1.7. Why Do Li-ion Batteries Need Additives?

2.1.8. Additive Development is Driven by Tradeoffs

2.1.9. Types of Battery Additives

2.1.10. More Information in Related IDTechEx Reports

3. BINDERS

3.1. Binders for Slurry-Based Electrode Processing

3.1.1. Wet/Slurry-Based Electrode Processing

3.1.2. Binder Properties & Examples

3.1.3. Key Binder Manufacturers

3.1.4. Alternative Binders for Cathodes

3.1.5. Binders for Silicon Anodes

3.1.6. Example Si-Anode Binder Systems from Patents (1)

3.1.7. Example Si-Anode Binder Systems from Patents (2)

3.1.8. Example Si-Anode Binder Systems

3.2. Binders for Dry Electrode Processing

3.2.1. Dry Electrode Processing

3.2.2. Benefits of Dry Electrode Processing

3.2.3. Dry Powder Deposition Methods & Potential Binders

3.2.4. Commercialization of Dry Electrode Processes

3.2.5. Tesla: Commercialization of Polymer Fibrillation

3.2.6. Results: Polymer Fibrillation

3.2.7. Commercialization of Dry Spraying Deposition

3.2.8. LG Energy Storage: Dry Electrode Commercialization Plans & Patent Analysis

3.2.9. LG Energy Storage: Dry Electrode Patent Analysis

3.2.10. Blue Solutions: Melt Extrusion

3.2.11. PowerCo: Commercializing Powder Compression

3.2.12. The Future of Dry Electrode Processes

4. CONDUCTIVE ADDITIVES

4.1. Conductive Additive Benchmarking

4.1.1. Conductive Additives

4.1.2. Overview of Advanced Carbon

4.1.3. Benchmarking of Conductive Additives

4.1.4. Key Manufacturers of Conductive Additives

4.2. Carbon Black

4.2.1. Carbon Black Overview

4.2.2. Carbon Black Production Processes

4.2.3. Global Carbon Black Market

4.2.4. Key Measures of Carbon Black Performance in Batteries

4.2.5. Disordered vs Graphitic Carbon in Nanoparticles

4.2.6. Nouryon: Ketjen Black

4.2.7. Imerys: Super P and Super C65

4.2.8. Ketjen Black vs. Super P: Pore Size Distribution

4.2.9. Cabot: LITX Series Carbon Blacks

4.2.10. Birla Carbon

4.2.11. Surface Functionalization of Carbon Black

4.3. Graphite

4.3.1. Graphite Properties and Applications

4.3.2. Synthetic vs. Natural Graphite

4.3.3. Graphite as a Conductive Additive

4.3.4. Imerys: L-Series Graphite

4.3.5. SGL Carbon

4.4. Carbon Nanofiber

4.4.1. Introduction to Carbon Nanofiber

4.4.2. Carbon Nanofibers as an Additive

4.4.3. Techno-Economic Evaluation of Nanofibers

4.4.4. Resonac VGCF

4.5. Carbon Nanotubes (CNTs)

4.5.1. Introduction to CNTs

4.5.2. CNTs: Ideal vs Reality

4.5.3. CNTs in Li-ion Batteries

4.5.4. Price Position of CNTs: SWCNTs vs. MWCNTs

4.5.5. Global Production Capacity of CNTs

4.5.6. Key Supply Relationships for CNTs in Li-ion Batteries

4.5.7. Results: Impact of CNT Use in Li-ion Electrodes (1)

4.5.8. Results: Impact of CNT Use in Li-ion Electrodes (2)

4.5.9. Results: SWCNT Improves LFP Cycle Life

4.5.10. Results: Improved Performance at Higher C-Rate

4.5.11. Results: CNTs for Silicon Anodes

4.5.12. Significance of CNT Dispersion

4.5.13. Cabot Carbon Nanostructures (CNS)

4.5.14. Hybrid Conductive Carbons Using CNTs

4.5.15. Combining CNTs with Carbon Black

4.5.16. Carbon Nanotubes 2025-2035: Market, Technology & Players

4.6. Graphene

4.6.1. Introduction to Graphene

4.6.2. The Role of Grpahene in Batteries

4.6.3. Key Graphene Players in Battery Market (1)

4.6.4. Key Graphene Players in Battery Market (2)

4.6.5. Results: Graphene Enhances Performance at Lower Loadings

4.6.6. Combining Graphene with Other Conductive Additives

4.6.7. Results: Graphene in Si-Anodes

4.6.8. Commercialization of Graphene Production

4.6.9. Product Specifications of Key Players

4.6.10. Hydrograph Graphene Slurries for Batteries

4.6.11. Graphene Market & 2D Materials Assessment 2024-2034: Technologies, Markets, Players

5. ELECTROLYTE ADDITIVES

5.1. Introduction to Electrolyte Additives

5.1.1. Introduction to Li-ion Electrolytes

5.1.2. Developments in Formulated Electrolytes

5.1.3. The Rise of Electrolyte Additives

5.1.4. Electrolyte Patent Comparisons - Key Battery Players

5.1.5. Electrolyte Patent Comparisons - Key Electrolyte Players

5.1.6. Electrolyte Additives Examples

5.1.7. Electrolyte Value Chain

5.2. Electrolyte Additive Categories & Examples

5.2.1. Lithium Salt Electrolyte Additives

5.2.2. Li Salt Additives: LiTFSI & LiFSI

5.2.3. Li Salt Additives: LiTDI, LiTA, & LiBOB

5.2.4. Li Salt Additives: LiDFOB and Other Li Salts

5.2.5. Organic Carbonate Additives

5.2.6. Sulfur-Containing & Silicon-Containing Additives

5.2.7. Fluorinated Electrolyte Additives

5.2.8. Electrolyte & Electrolyte Additives Overview

5.3. Key Suppliers & Case Studies

5.3.1. Arkema

5.3.2. Solvay (1)

5.3.3. Solvay (2)

5.3.4. Tinci Materials

5.3.5. Trinohex Ultra

5.3.6. Electrolyte Additive Startups: Halocarbon & Elyte Innovations

5.3.7. Electrolyte Additive Startups: South 8 & New Dominion

5.3.8. CATL Additive-Related Patents (1)

5.3.9. CATL Additive-Related Patents (2)

5.3.10. More Electrolyte Additive Patents

6. OTHER ADDITIVES

6.1. Foil Coatings

6.1.1. Current Collector Foils & The Need for Coatings

6.1.2. Types of Foil Coatings

6.1.3. Arkema: Incellion Aqueous Foil Coating

6.1.4. Carbon-Based Coatings: Armor Films & Chalco Aluminium

6.1.5. LG: Thermal Suppression Coating

6.2. Slurry Additives

6.2.1. Electrode Slurries & The Importance of Additives

6.2.2. Case Studies: Huntsman

6.2.3. Case Studies: Kao - Luna Ace

6.2.4. Further Case Studies: Borregaard, Cargill, and Arkema

6.2.5. Further Case Studies: Evonik & Dow Chemical

6.3. Pre-Lithiation Electrode Additives

6.3.1. The Need for Pre-Lithiation & Key Strategies

6.3.2. Cathode Pre-Lithiation Additives

6.3.3. Pre-Lithiation and 'Zero Degradation' Batteries

6.3.4. Pre-Lithiation Additive Example: CATL (1)

6.3.5. Pre-Lithiation Additive Example: CATL (2)

7. PFAS REMEDIATION IN LI-ION BATTERY ADDITIVES

7.1. Introduction to PFAS

7.1.1. Introduction to PFAS

7.1.2. Applications of PFAS

7.1.3. Growing Concerns Around Negative Impacts of PFAS

7.1.4. PFAS Regulation Around The World

7.1.5. Where is PFAS Used in Batteries?

7.1.6. PFAS Substitution vs Management

7.1.7. IDTechEx Reports on PFAS

7.2. PFAS Removal in Binders

7.2.1. Replacing PFAS Binders in Batteries

7.2.2. Identifying Potential Binders Among Non-PFAS Polymers

7.2.3. Aqueous Binders in Academic Literature

7.2.4. TRL of Non-PFAS Aqueous Cathode Binders

7.2.5. Limitations of Aqueous Binder Systems

7.2.6. Polyacrylic Acid (PAA)

7.2.7. Leclanche: Aqueous PFAS-Free Electrode

7.2.8. Governments Funding Non-PFAS Binder Research

7.2.9. UV-Cured & Energy-Cured Binders

7.2.10. Ateios Systems: Energy-Cured Binders

7.2.11. Miltec: UV Binders

7.2.12. Beyond Li-ion: Seeo & Binders for Li-S Batteries

7.2.13. OnTo Technology: PFAS-Free Binders & Recycling for Li-S

7.2.14. Nanoramic: Nanocarbons as Hybrid Binder-Conductive Additives

7.2.15. Dry Electrodes as a PFAS Removal Strategy

7.2.16. 24M: Removing Binders Entirely

7.2.17. Recycling as a PFAS Management Strategy

7.2.18. Types of Li-ion Battery Recycling

7.2.19. Implication of Li-ion Recycling Methods on Binders

7.2.20. Direct Battery Recycling for Binder Recovery

7.2.21. Li-ion Battery Recycling Technologies for Binder Recovery Summary

7.2.22. Commercial Feasibility of Binder Recycling

7.3. PFAS Removal in Electrolytes

7.3.1. Fluorinated Electrolyte Additives: Function & Types

7.3.2. Non-PFAS Li Salts for SEI Formation

7.3.3. E-Lyte: PFAS-Free Electrolyte

7.3.4. Non-PFAS Carbonates & Organic Compounds for SEI Formation

7.3.5. Non-PFAS Flame Retardants: Phosphate-Based Materials

7.3.6. Non-PFAS Flame Retardants: More Non-Fluorinated Alternatives

7.3.7. Non-PFAS Diluents for HCEs

7.3.8. Overview of PFAS-Free Electrolyte Additives

8. FORECASTS

8.1. Forecast Methodology

8.2. Forecast Assumptions

8.3. Material Price Assumptions (US$/kg)

8.4. Battery Additive Material Demand Forecast (kilotonnes) 2025-2036

8.5. Battery Additive Market Size Forecast (US$ Billion) 2025-2036

8.6. Binders Material Demand Forecast (kilotonnes) 2025-2036

8.7. Binders Material Demand Forecast by Manufacturing Process Type (kilotonnes) 2025-2036

8.8. Binders Market Size Forecast (US$ Billion) 2025-2036

8.9. Conductive Additive Material Demand Forecast (kilotonnes) 2025-2036

8.10. Conductive Additive Market Size Forecast (US$ Billion) 2025-2036

8.11. Electrolyte Additive Material Demand Forecast (kilotonnes) 2025-2036

8.12. Electrolyte Additive Material Demand Forecast: Fluorinated vs Non-Fluorinated (kilotonnes) 2025-2036

8.13. Lithium Salt Electrolyte Additive Material Demand Forecast (kilotonnes) 2025-2036

8.14. Electrolyte Additive Market Size Forecast (US$ Billion) 2025-2036

8.15. Fluorinated vs Non-Fluorinated Electrolyte Additive Market Size Forecast (US$ Billion) 2025-2036

8.16. Lithium Salt Electrolyte Additive Market Size Forecast (US$ Billion) 2025-2036

8.17. Total Battery Additive Material Demand Forecast by Material (kilotonnes) 2025-2036

8.18. Total Battery Additive Market Size Forecast by Material (US$ Billion) 2025-2036

9. COMPANY PROFILES

9.1. Links to company profiles on IDTechEx's portal

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

関連レポート(キーワード「リチウム」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|