グリーンスチール2025-2035年:技術、プレーヤー、市場、予測Green Steel 2025-2035: Technologies, Players, Markets, Forecasts 低炭素鉄鋼とグリーンスチール技術:水素DRI、電気化学的製鉄、スクラップEAF、高炉脱炭素化など。主要企業、新興企業、ケーススタディ、グリーン・スチール・プロジェクト、地域別グリーン・スチール予測 &n... もっと見る

サマリー 低炭素鉄鋼とグリーンスチール技術:水素DRI、電気化学的製鉄、スクラップEAF、高炉脱炭素化など。主要企業、新興企業、ケーススタディ、グリーン・スチール・プロジェクト、地域別グリーン・スチール予測 世界の鉄鋼業界は重大な岐路に立たされている。世界のCO2 排出量の7-9%を占める鉄鋼メーカーは、気候変動規制の強化や市場の需要の変化に伴い、変革へのプレッシャーに直面している。IDTechExの本レポートでは、2035年まで鉄鋼業界がどのようにこれらの課題に対応していくかを検証し、既存プロセスの漸進的改善と、水素やクリーン電力を利用した革新的な生産方法の両方を分析している。 鉄鋼の炭素問題とグリーン・スチールへの進化 従来の高炉-基礎酸素炉(BF-BOF)製造ルートは、燃料と還元剤の両方に原料炭を使用するため、炭素集約度が高い。規制の進化と持続可能性に向けた世界的な動きは鉄鋼市場に影響を及ぼし、鉄鋼メーカーに脱炭素化への圧力を強めている。 天然ガスベースの直接還元鉄(NG-DRI)生産は、すでにいくつかの地域で定着している。NG-DRIはこれまで、安価で豊富な天然ガスが存在する地域(中東など)に限定されていたが、現在では排出量削減のための過渡的な技術と見なされている。業界は、高炉の改造やCCUSの統合による既存設備の最適化から新技術の導入まで、複数の脱炭素化経路を同時に追求している。グリーン水素を動力源とする水素ベースDRI(H2-DRI)は、業界の主要目標として浮上しており、すべての大手鉄鋼メーカーがこの技術の採用を検討している。 水素ベースの直接還元技術は、複数のプロセスバリエーションを包含する。MidrexとEnergironは、すでにNG-DRIで広く使用されているシャフト炉技術であるが、新しい流動床とプラズマ還元アプローチも出現している。Voestalpine社、POSCO社などの企業は、生産全体を簡素化しながら、より低品位の鉄鉱石を消費できる、より新しいタイプの技術を開発している。  鉄鋼メーカー、冶金技術開発者、鉱業会社、新興企業はすべて、持続可能な製鉄のためのまったく新しいコンセプトの開発に取り組んでいる。本レポートでは、詳細なケーススタディを通じて、将来の生産を形成する可能性のある主要技術を紹介している。特筆すべきは、ボストンメタルやエレクトラのような新興企業が、アルセロール・ミタルのような既存企業とともに、鉄生産のための新しい電気化学的手法を開発していることである。全体として、グリーン・スチール革新企業は、政府の補助金と並んで、大手企業や金融機関から多額の投資を集めており、有望な可能性を示している。 IDTechExは、採鉱事業における再生可能エネルギーの導入、高炉におけるバイオマスや水素の注入、スクラップをリサイクルするための電気炉(EAF)の能力拡大、電気化学的製鉄、溶融酸化物電解、プラズマベースの還元技術などの新しいアプローチなど、幅広い脱炭素化戦略をカバーしている。 EU 排出権取引制度(ETS)や炭素国境調整メカニズム(CBAM)のような政策的枠組みは、鉄鋼メーカーに低炭素技術の採用を求める経済的圧力を生み出しており、自動車や建設などの分野ではより環境に優しい材料への需要が高まっている。大手鉄鋼メーカーは、技術開発と水素対応生産拠点に数十億ドルを投じており、2030年代半ばまでに世界で1億トン近い水素対応生産能力が発表されている。これらのプロジェクトのほとんどは、天然ガスの使用からスタートし、最終的には低炭素水素への移行を目指している。 大量の鉄埋蔵量と再生可能エネルギーの可能性が組み合わさることで、オーストラリア、ブラジル、アフリカなどの地域に、新たな鉄鋼生産拠点が設立される可能性がある。グリーン水素の開発はグリーン・スチールにとって重要な触媒であるが、プロジェクトの商業運転開始には支援的な法律と財政的インセンティブが必要である。 IDTechExのレポートでは、これらの市場力学について以下のような詳細な分析を行っている:

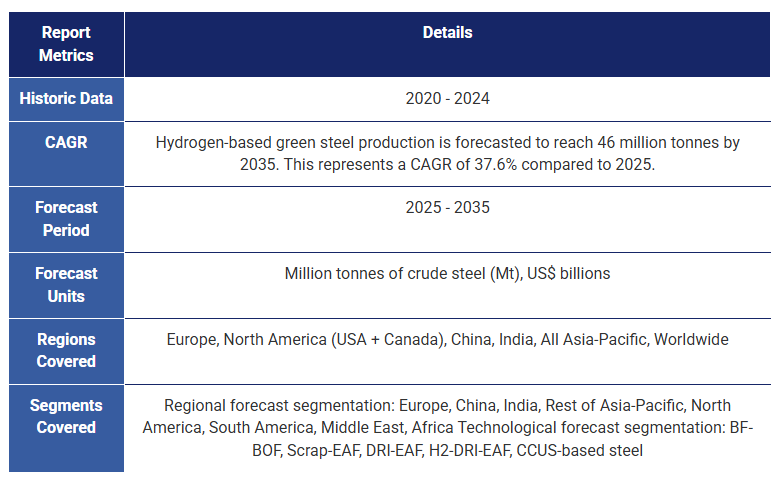

予測、地域動向、世界的見通し IDTechExの10年予測は、世界の鉄鋼生産とグリーン・スチール採用を主要地域と生産ルート別に分類し、市場の進化に関する包括的な見通しを提供しています。予測は、BF-BOF、スクラップ-EAF、NG-DRI-EAF、H₂-DRI-EAF、CCUSベースの鋼を含む主要な生産ルート別にセグメント化されています。これらの世界予測は地域別にも区分されており、欧州、中国、インド、その他のアジア太平洋地域、北米、南米、中東、アフリカをカバーし、各地域の異なる技術の進化に関する見通しを掲載している。 主要な側面 本レポートは、低炭素でグリーンな鉄鋼生産への移行を形成する技術的な道筋、市場力学、競争環境を理解することに関心のある関係者に重要な洞察を提供します。 持続可能な鉄鋼生産技術と市場分析

業界動向と市場ダイナミクス

市場予測と地域分析:

目次

1.要旨

1.1.鉄鋼業の現状 - 主要生産地域

1.2.世界のトップ鉄鋼メーカー

1.3.世界の最終製品における鉄鋼使用量

1.4.鉄鋼生産ルートの概要

1.5.なぜ鉄鋼生産は脱炭素化が難しいのか?

1.6.鉄鋼業の排出量は世界の排出量の10%に迫る

1.7.鉄鋼セクターの脱炭素化技術の概要

1.8.グリーン・スチールとは何か?

1.9.グリーン・スチール規制・政策 - 世界の概要

1.10.鉄鉱石鉱業の概要

1.11.鉄鉱石凝集における脱炭素技術(ペレタイジングと焼結)

1.12.高炉サイトの排出削減戦略の概要

1.13.高炉を石炭ベースの製錬還元代替物に置き換える

1.14.CCUSが鉄鋼セクターの脱炭素化に果たす役割は限定的

1.15.鉄鋼の脱炭素化における水素のケース

1.16.製鉄への水素技術統合の機会

1.17.グリーンH2を用いたH2-DRI-EAF

1.18.注目すべき鉄鋼メーカーと水電解装置のOEM提携

1.19.直接還元シャフト炉技術のプレーヤー

1.20.流動床と固定床の還元プロセス

1.21.電炉でのスクラップ・リサイクルは、すでに鉄鋼の脱炭素化のための重要な経路となっている

1.22.大手鉄鋼メーカーは電気炉(EAF)の能力を増強している

1.23.電気製錬炉(ESF)-EAFと比較した場合の主な利点

1.24.代替製鉄技術開発のケース

1.25.水素ベースの製鉄と電化製鉄

1.26.新しい製鉄技術に関する企業の状況

1.27.TRLの比較

1.28.異なるグリーン・スチール製造ルートのコスト比較

1.29.潜在的CO₂ 削減量とCO₂ 削減コストの比較

1.30.鉄鋼メーカーは新しい低炭素鋼製品ラインを確立している

1.31.自動車はグリーン・スチールの主な用途市場

1.32.グリーン・スチールを採用するその他のセクター

1.33.水素対応DRI生産能力のプロジェクト発表(Mt DRI)

1.34.グリーン・スチール・サプライチェーンの例 - ステグラ

1.35.世界の鉄鋼生産予測(生産ルート別)-考察

1.36.世界の鉄鋼生産予測(地域別)-考察

1.37.低炭素鋼の技術別予測、2025-2035年

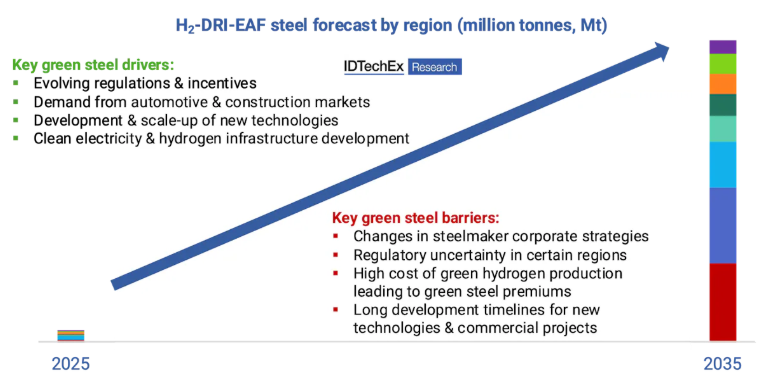

1.38.水素を利用したグリーン・スチール地域別予測 -考察(1)

1.39.水素を利用したグリーン・スチール地域別予測-考察(2)

1.40.LCOSと水素ベースの鉄鋼生産の世界総コスト、2025-2035年

2.はじめに

2.1.世界の鉄鋼業の概要

2.1.1.鉄鋼の紹介

2.1.2.鉄鉱石鉱業の概要-上位生産地域

2.1.3.鉄鉱石鉱業の概要-トップ生産企業

2.1.4.世界の鉄鋼業の歴史的成長

2.1.5.世界の鉄鋼生産能力は西から東へシフト

2.1.6.鉄鋼業の現状-上位生産地域

2.1.7.鉄鋼生産ルートの概要

2.1.8.鉄鋼工場の地域分布

2.1.9.世界の製鉄能力

2.1.10.世界の製鉄能力

2.1.11.世界のトップ鉄鋼メーカー

2.1.12.鉄鋼市場の最近の動向

2.1.13.世界の完成品鉄鋼使用量(1)

2.1.14.世界の完成品鉄鋼使用量(2)

2.1.15.鉄鋼生産上位国の最近の動向(1)

2.1.16.鉄鋼生産上位国の最近の動向(1)

2.1.17.鉄鋼生産上位国の最新動向(1)

2.1.18.鉄鋼セクターにおける主な市場促進要因・障壁

2.2.BF-BOFを用いた従来の鉄鋼生産

2.2.1.鉄鋼業界は急速に新技術を導入しているが、依然として石炭に依存している

2.2.2.高炉-BOF プロセスの概要

2.2.3.高炉操業-概要

2.2.4.高炉操業 - 反応

2.2.5.高炉材料バランス - 投入と排出

2.2.6.高炉のサイズ

2.2.7.高炉ガス管理

2.2.8.下流の製鋼プロセス

2.2.9.鉄鋼に使用される合金元素

2.2.10.製鋼-塩基性酸素炉(BOF)と電気炉(EAF)の比較

2.3.グリーン・スチールの必要性

2.3.1.鉄鋼業界の排出量は、世界の排出量の10%に近づいている

2.3.2.なぜ鉄鋼生産は脱炭素化が難しいのか?

2.3.3.従来のBF-BOFプロセスからのCO₂排出量の内訳

2.3.4.鉄鋼業における主なCO₂ 削減の焦点

2.3.5.鉄鋼セクターの脱炭素化技術の概要

2.3.6.グリーン・スチールとは何か?

2.3.7.グリーン・スチールへの主なルート(1)

2.3.8.グリーン・スチールへの主なルート(2)

2.3.9.グリーン・スチール産業にとっての主な推進要因と障壁

2.4.グリーン・スチール需要の促進:政策と規制

2.4.1.グリーン・スチール規制と政策-グローバルな概観

2.4.2.グリーン・スチール政策の枠組みと脱炭素戦略(1)

2.4.3.鉄鋼グリーン化政策と脱炭素戦略(2)

2.4.4.鉄鋼グリーン化政策フレームワークと脱炭素戦略(3)

2.4.5.鉄鋼グリーン化政策フレームワークと脱炭素戦略(4)

2.4.6.鉄鋼グリーン化政策と脱炭素戦略(5)

2.4.7.カーボンプライシング、炭素市場、排出量取引制度の紹介

2.4.8.世界のコンプライアンス カーボンプライシングメカニズム

2.4.9.EUETS が欧州鉄鋼業に与える影響-過去、現在、未来

2.4.10.EU 炭素国境調整メカニズム(CBAM)

2.4.11.CBAMの主な定義

2.4.12.EU CBAM - 遵守とスケジュール

2.4.13.EUのCBAMに対する鉄鋼業界の批判と改革案

2.4.14.CBAMは鉄鋼市場にどのような影響を与えるか?

2.4.15.自動車用グリーン・スチール使用を促進するEU規制

2.4.16.欧州のESPR規制と鉄鋼への潜在的影響

2.4.17.トランプ大統領による鉄鋼・アルミ部門への関税の潜在的影響

2.4.18.トランプ政権下で不確実性に直面する米国のグリーン・スチール・プロジェクト

3.既存の鉄鋼設備の脱炭素化

3.1.鉄鉱石採掘の脱炭素化

3.1.1.鉄鉱石の種類 - グリーン・スチールにはマグネタイトが好ましい

3.1.2.鉄鉱石の採掘と選鉱

3.1.3.鉱業における再生可能エネルギーの利用

3.1.4.鉱業における再生可能エネルギー利用の機会と課題

3.1.5.鉱山機械の電化の利点と障壁

3.1.6.鉱業車両のCO₂排出貢献

3.1.7.鉱山会社の排出目標

3.1.8.鉱山車両の脱炭素化を奨励するカナダ

3.1.9.鉱業用EVはどこで採用されるか?

3.1.10.電気自動車の生産性メリット

3.1.11.電動化に向けた主要な鉱山車のタイプ

3.1.12.OEMの主な電動化活動

3.1.13.Fortescue社、Liebherr社の鉱山用EVを大々的に導入

3.1.14.欧州で本格的に使用され始めた電動ダンプトラック

3.2.鉄鉱石集積の脱炭素化

3.2.1.サプライチェーンの概要

3.2.2.加工鉄鉱石-塊、焼結鉱、ペレット

3.2.3.鉄鉱石の塊、焼結鉱、ペレットの比較

3.2.4.添加物 - コークス、石灰石、その他

3.2.5.鉄鉱石凝集における脱炭素技術(ペレタイジングと焼結)

3.2.6.凝集における排出削減のための商業的アプローチ(1)

3.2.7.凝集における排出削減への商業的アプローチ(2)

3.2.8.主要な鉄鉱石凝集プロセス技術サプライヤー

3.2.9.焼結組成を調整することでCO₂ 排出量を削減できる

3.2.10.Primetals Technologiesの焼結工場の改善

3.2.11.宝鋼のマイクロ波焼結技術

3.2.12.鉄鉱石ペレット化におけるCO₂排出量

3.2.13.LKAB のペレタイジング作業における燃料切り替え試験

3.2.14.CSIRO の新しいペレタイジングプロセス

3.2.15.Metso Outotec の次世代ペレタイジングプラント

3.2.16.ヴァーレの冷間鉄鉱石ブリケッティング技術

3.3.高炉の脱炭素化と他の石炭ベースの代替

3.3.1.高炉サイトの排出削減戦略の概要

3.3.2.還元剤としてバイオマスを使用する企業

3.3.3.高炉への水素吹き込み - 新日本製鐵

3.3.4.高炉への水素注入を検討しているその他の企業

3.3.5.ポール・ウルト社のケーススタディ-高炉用合成ガス乾式改質

3.3.6.Paul Wurth 社のケーススタディ-プラズマを利用した加熱と合成ガス注入

3.3.7.クイーンズランド大学-少量スラグの原料最適化

3.3.8.クイーンズランド大学 - DRI-BF ハイブリッドプロセス

3.3.9.高炉を石炭ベースの製錬還元代替設備に置き換える

3.3.10.タタ・スチールのHisarnaプロセス

3.3.11.ポスコのファイネックス・プロセス

3.3.12.石炭ベースのロータリーキルンDRI&SL/RNプロセス

3.3.13.回転炉床炉(RHF)

3.4.鉄鋼セクターにおけるCCUS

3.4.1.CCUSが鉄鋼セクターの脱炭素化に果たす役割は限定的

3.4.2.炭素回収・利用・貯留(CCUS)とは何か?

3.4.3.CCUSのバリューチェーン

3.4.4.鉄鋼向けCCUSの概要(1)

3.4.5.鉄鋼向けCCUSの概要(2)

3.4.6.高炉-基礎酸素炉(BF-BOF)プロセスのCCUS

3.4.7.CO₂分圧はコストにどう影響するか?

3.4.8.異なる炭素回収技術をいつ使用すべきか?

3.4.9.BF-BOFプロセスの燃焼後回収技術

3.4.10.アミンベースの燃焼後CO₂ 吸収

3.4.11.製鉄のための燃焼前炭素回収(1)

3.4.12.製鉄のための燃焼前炭素回収(2)

3.4.13.吸着強化型水ガスシフト(SEWGS)

3.4.14.製鉄用ガスリサイクルおよび酸素燃焼

3.4.15.高炉ガスCO₂ 回収技術の比較

3.4.16.天然ガスベースのDRIのための炭素回収

3.4.17.鉄鋼セクター向けCCUSプロジェクト・パイプライン

3.4.18.CCUSビジネスモデルの開発

3.4.19.CO₂貯留の概要

3.4.20.貯蔵タイプのTRLと事業者の状況

3.4.21.CO₂輸送の概要

3.4.22.鉄鋼セクターのCO₂利用

3.4.23.産業部門別の炭素回収コスト

3.4.24.カーボンクレジット、カーボンオフセットとは?

3.4.25.鉄鋼メーカーによる炭素クレジットの購入

3.4.26.鉄鋼セクターにおけるCCUSの課題と機会

3.5.電気炉(EAF)製鉄と再生可能エネルギー利用

3.5.1.電気炉でのスクラップリサイクルは、すでに鉄鋼の脱炭素化のための重要な経路である

3.5.2.鉄スクラップは鉄鋼業の主要原料である

3.5.3.なぜEAFがグリーン製鉄に必要なのか?

3.5.4.大手鉄鋼メーカーは電気炉(EAF)の能力を増強している

3.5.5.電気炉(EAF)の設計

3.5.6.大手EAFサプライヤーのケーススタディ - Tenova

3.5.7.超高出力(UHP)EAF

3.5.8.主要EAFサプライヤー(1)

3.5.9.主なEAFサプライヤー(2)

3.5.10.スクラップEAFプロセスとネットゼロDRI-EAFの必要性

3.5.11.EAF製鋼のための再生可能エネルギー調達 - 主な商業活動

3.5.12.製鉄用原子力発電-採用の理由

3.5.13.原子力発電計画と鉄鋼メーカーからの投資

3.5.14.集光型太陽光発電と製鋼用熱エネルギー貯蔵

4.水素ベースの鉄鋼生産

4.1.製鉄用水素サプライチェーンの概要

4.1.1.鉄鋼の脱炭素化における水素のケース

4.1.2.DRI製造の主要技術プロバイダー

4.1.3.水素の色

4.1.4.水素市場の現状

4.1.5.なぜグリーン水素が必要なのか?

4.1.6.代表的なグリーン水素プラントのレイアウト

4.1.7.典型的なグリーン水素プラントのレイアウト

4.1.8.電解槽セル、スタック、プラントバランス(BOP)

4.1.9.グリーン水素:主な電解槽技術

4.1.10.グリーン水素の商業的進展

4.1.11.水素バリューチェーンの概要

4.1.12.各種水素のLCOH予測(灰色、青色、緑色)

4.1.13.製鉄への水素技術統合の機会

4.1.14.グリーンH2を使ったH2-DRI-EAF

4.1.15.注目すべき鉄鋼メーカーと水電解槽のOEM提携

4.1.16.DRIに固体酸化物電解槽(SOEC)を使用するザルツギッター

4.1.17.鉄鋼プロセスへのメタン熱分解の統合の可能性

4.1.18.鉄鋼圧延に使用される水素 - オバコ

4.1.19.グリーン・スチールにおける低炭素水素利用のためのSWOT分析

4.2.水素を利用した直接還元鉄(DRI)&EAF製鉄

4.2.1.世界の直接還元鉄(DRI)生産の現状

4.2.2.DRI-EAFプロセスの概要

4.2.3.直接還元シャフト炉

4.2.4.直接還元シャフト炉と高炉の比較

4.2.5.H2-DRI-EAFプロセスのインプットとアウトプット

4.2.6.直接還元シャフト炉技術のプレーヤー

4.2.7.Midrexプロセス

4.2.8.Energironプロセス

4.2.9.DRI-EAFにおける天然ガスの水素への置き換え(1)

4.2.10.DRI-EAFにおける天然ガスの水素への置換(2)

4.2.11.流動床と固定床の還元プロセス

4.2.12.POSCO FINEX & HyREX プロセス

4.2.13.サーカード・プロセス

4.2.14.Circoredプロセスの商業化における課題

4.2.15. HYFORプロセス 4.2.16.直接還元鉄(DRI)生産量

4.2.17.DRI生産量の比較

4.2.18.製鉄プロセス

4.2.19.大手製鉄会社は電気炉(EAF)の能力を増強している

4.2.20.製鉄-塩基性酸素炉(BOF)と電気炉(EAF)の比較

4.2.21.EAFのエネルギーと材料消費

4.2.22.ゼロ炭素EAF操業の課題

4.2.23.EAFにおけるコークスと石炭のバイオ炭への置き換え

4.3.電気製錬炉(ESF)

4.3.1.EAFの限界とESFとの比較

4.3.2.電気製錬炉(ESF)-EAFと比較した主な利点

4.3.3.電気製錬炉(ESF)-既存プラントとの統合機会

4.3.4.商業的なESFの設計例と技術サプライヤー

4.3.5.電気製錬炉開発をリードする企業

4.3.6.電気製錬炉開発をリードする企業

5.新規製鉄技術

5.1.新規製鉄技術の概要

5.1.1.代替製鉄技術開発のケース

5.1.2.水素ベースの製鉄と電化製鉄

5.1.3.新たな製鉄技術に関する企業動向

5.2.電解製鉄

5.2.1.サイダーウィン - 電解採取技術 (1)

5.2.2.サイダーウィン-電解採取技術(2)

5.2.3.ArcelorMittal & John Cockerill - Volteron電解採取

5.2.4.エレクトラ-電解採取技術(1)

5.2.5.エレクトラ-電解採取技術(2)

5.2.6.Fortescue の直接電気化学還元(DER)

5.2.7.エレメント・ゼロ - 中温電解

5.2.8.ボストンメタル - 溶融酸化物電解(1)

5.2.9.ボストンメタル - 溶融酸化物電解(2)

5.2.10.メタリシス-固体電解(1)

5.2.11.メタリシス-固体電解(2)

5.3.熱化学と水素プラズマを利用した製鉄

5.3.1.HyIron-ロータリーキルンでのH2を使った直接還元(1)

5.3.2.HyIron-ロータリーキルンでの水素による直接還元(2)

5.3.3.フラッシュ製鉄技術

5.3.4.ヘリオス(Helios)-ナトリウムベースの新規熱プロセス(1)

5.3.5.ヘリオス-新規ナトリウムベース熱プロセス(2)

5.3.6.水素プラズマ製錬還元法(HSPR)(1)

5.3.7.水素プラズマ製錬還元法(HSPR)(2)

5.3.8.HSPRスタートアップ - Hertha Metals & Ferrum Technologies

5.4.製鉄用電熱

5.4.1.カリックスのZESTYプロセス - 電化加熱

5.4.2.マイクロ波による鉄還元への取り組み

5.4.3.Rio Tinto BioIron - マイクロ波とバイオマスによる還元(1)

5.4.4.リオティント・バイオアイアン-マイクロ波とバイオマスによる還元(2)

5.4.5.製鉄用レーザー加熱 - ライムライト・スチール

6.鉄鋼プロセスの技術経済比較

6.1.TRL比較

6.2.異なる製鉄ルートにおける鉄原料の必要量

6.3.異なる製鉄ルートのエネルギー消費量

6.4.平準化鉄鋼コスト(LCOS)の概要

6.5.様々なグリーン・スチール製造ルートのコスト比較

6.6.鉄鋼生産ルート別のCAPEX、OPEX、燃料費

6.7.異なる鉄鋼生産ルートのカーボンフットプリント比較

6.8.CO₂削減可能量とCO₂削減コストの比較

6.9.電力供給源による排出量の変動

6.10.水素ベースの製鉄における LCOS の地域差

6.11.DRI-EAFにおける天然ガスからグリーン水素への代替の影響

7.グリーン・スチール市場分析

7.1.グリーン・スチール・プロジェクトの発表とプレーヤー

7.1.1.鉄鋼メーカーの脱炭素化目標

7.1.2.水素対応DRI生産能力(Mt DRI)のプロジェクト発表

7.1.3.水素対応DRIプロジェクトの発表 - 欧州

7.1.4.水素製造が可能なDRIプロジェクトの発表 - アジア太平洋地域

7.1.5.その他の地域 - 水素対応DRIプロジェクトの発表

7.1.6.グリーンな鉄鋼が新たな生産拠点の機会を世界的に創出

7.1.7.グリーン鉄鋼回廊 - グローバル・サプライ・チェーンを再構築する可能性

7.1.8.HYBRITプロジェクト - SSAB、LKAB、Vattenfall

7.1.9.SSABの低炭素鋼

7.1.10.ステグラ(H2グリーン・スチール)

7.1.11.グリーン・スチール・サプライチェーンの例 - ステグラ

7.1.12.鉄鋼メーカーは新たな低炭素鋼製品ラインを確立している

7.1.13.鉄鋼メーカーのマスバランス配分

7.1.14.新技術への再投資に使用されるグリーン・スチール証書

7.1.15.SSABの低排出鉄鋼使用事例

7.1.16.JFEスチールの低排出鉄鋼使用例

7.1.17.HBISグループの中国における水素DRIプロジェクト

7.1.18.アルセロール・ミッタル社のグリーン水素DRIプロジェクト凍結(1)

7.1.19.アルセロール・ミッタル社の水素DRIプロジェクト凍結(2)

7.1.20.米国のグリーン・スチール・プロジェクトとトランプ政権下の不確実性

7.2.応用分野におけるグリーン・スチール

7.2.1.鉄鋼価格 - 2020年以降の主な動向

7.2.2.2024-2025年の鉄鋼HRC価格

7.2.3.鉄鋼市場動向とグリーン・スチールへの影響

7.2.4.持続可能な鉄鋼バイヤーズ・プラットフォーム

7.2.5.自動車はグリーンスチールの主な用途市場

7.2.6.グリーン・スチールを採用するその他のセクター

7.2.7.鉄鋼はエネルギー転換に不可欠

7.2.8.欧州のESPR規制と鉄鋼への潜在的影響

7.2.9.自動車産業におけるグリーン・スチール・プレミアム

7.2.10.建設分野におけるグリーン・スチール・プレミアム

7.2.11.その他のセクターにおけるグリーン・スチール・プレミアム

7.2.12.グリーン・スチール・サプライチェーンの例 - ステグラ

7.2.13.グリーン・スチール&低炭素鋼の自動車向けオフテーカー(欧州)

7.2.14.グリーン・スチール&低炭素スチールの自動車オフテーカー(米国&アジア)

7.2.15.自動車用低炭素鋼のティア1・2のオフテーカー(欧州)

7.2.16.その他の用途市場におけるグリーンスチールのオフテーカー(設備・機械)

7.2.17.その他の用途市場におけるグリーンス チールのオフテーカー(建設関連)

7.2.18.ハイテク企業のグリーン・スチールへの関心

7.2.19.データセンターにおける鉄鋼の役割

7.3.鉄鋼市場の地域別動向

7.3.1.地域概況と市場動向(1)

7.3.2.地域概況と市場動向(2)

7.3.3.各国の製鉄ルート発展への期待(1)

7.3.4.各国の製鉄発展への期待 (2)

8.市場予測

8.1.世界の鉄鋼市場予測

8.1.1.鉄鋼の地域別予測

8.1.2.予測方法と前提

8.1.3.世界の鉄鋼生産量の生産ルート別予測(2025~2035年)

8.1.4.世界の鉄鋼生産量予測(生産ルート別)-考察

8.1.5.世界の鉄鋼生産量の地域別予測(2025~2035年)

8.1.6.世界の鉄鋼生産量の地域別予測-考察

8.1.7.生産技術の地域別動向(1) 8.1.8.生産技術の地域別動向(2)

8.2.グリーン・スチール市場予測

8.2.1.低炭素鋼の技術別予測(2025~2035年)

8.2.2.化石燃料ベースのDRI-EAF鋼の地域別予測、2025~2035年

8.2.3.水素ベースのグリーンスチール地域別予測、2025~2035年

8.2.4.水素ベースのグリーンスチール地域別予測-考察(1)

8.2.5.地域別水素利用鉄鋼予測-考察(2)

8.2.6.水素ベース鋼の平準化コスト予測、2025~2050年

8.2.7.水素ベース鋼の世界総生産コスト(2025~2035年)

8.2.8.グリーン・スチール向け水素需要予測

8.2.9.鉄鋼用炭素回収予測、2024-2035

9. 企業プロフィール

Summary

Low-carbon steel and green steel technologies: hydrogen-DRI, electrochemical ironmaking, scrap-EAF, blast furnace decarbonization, and more. Key players, startups, case studies, green steel projects, and regional green steel forecasts

The global steel industry stands at a critical crossroads. Responsible for 7-9% of global CO2 emissions, steelmakers face mounting pressure to transform as climate regulations tighten and market demands evolve. This IDTechEx report examines how the industry is responding to these challenges through 2035, analyzing both incremental improvements to existing processes and innovative production methods using hydrogen and clean electricity.

Steel's carbon challenge & evolution to green steel

The traditional blast furnace-basic oxygen furnace (BF-BOF) production route uses coking coal as both fuel and reducing agent, making it highly carbon intensive. Evolving regulations and the global push towards sustainability are influencing the steel market, mounting pressure on steelmakers to decarbonize.

Natural gas-based direct reduced iron (NG-DRI) production is already well-established in several regions. While NG-DRI has previously been limited to areas with cheap and abundant natural gas (e.g., Middle East), it is now seen as a transitional technology for reducing emissions. The industry is pursuing multiple decarbonization pathways simultaneously - from optimizing existing facilities through blast furnace modifications and CCUS integration to deploying new technologies. Hydrogen-based DRI (H2-DRI) powered by green hydrogen is emerging as the primary goal for the industry, with all major steelmakers looking to adopt this technology.

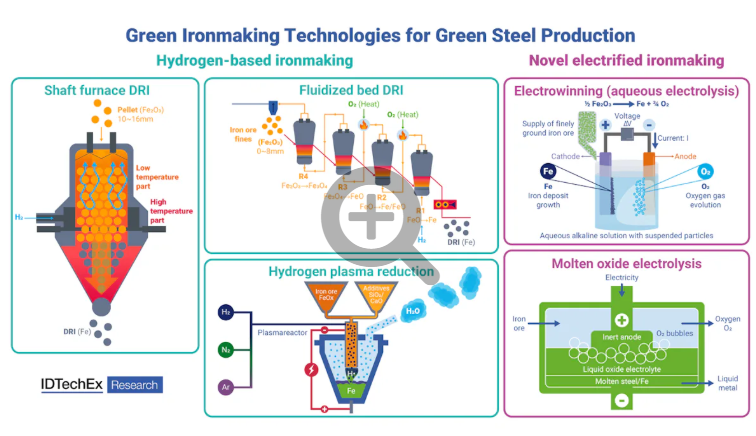

Hydrogen-based direct reduction technologies encompass multiple process variants. Midrex and Energiron are established shaft furnace technologies already widely used in NG-DRI, but newer fluidized bed and plasma reduction approaches are also emerging. Companies like Voestalpine, POSCO, and others are developing newer variants capable of consuming lower grade iron ore while simplifying overall production.

Steelmakers, metallurgical technology developers, mining companies, and startups are all engaged in developing completely new concepts for sustainable ironmaking. The report highlights key technologies that could shape future production through detailed case studies. Notably, startups like Boston Metal and Electra, alongside established players like ArcelorMittal, are developing new electrochemical methods for iron production. Overall, green steel innovators are attracting significant investments from major corporations and financial institutions, alongside government subsidies, indicating promising potential.

IDTechEx covers a wide spectrum of decarbonization strategies, including renewable energy implementation in mining operations, biomass and hydrogen injection in blast furnaces, expansion of electric arc furnace (EAF) capacity for recycling scrap, and novel approaches such as electrochemical ironmaking, molten oxide electrolysis, and plasma-based reduction technologies.

Market drivers & industry transformation

Policy frameworks like the EU Emissions Trading System (ETS) and Carbon Border Adjustment Mechanism (CBAM) are creating economic pressure for steelmakers to adopt low-carbon technologies, while sectors such as automotive and construction increasingly demand greener materials. Major steelmakers are committing billions to technology development and hydrogen-ready production sites, with close to 100 million tonnes of hydrogen-ready production capacity announced globally by the mid-2030s. Most of these projects will start off using natural gas and all aim to eventually transition to low-carbon hydrogen.

The combination of large iron reserves and renewable energy potential could establish new iron and steel production hubs in regions such as Australia, Brazil, and Africa. Green hydrogen development is a key catalyst for green steel, though it will require supportive legislation and financial incentives to bring projects into commercial operation.

IDTechEx's report provides detailed analysis of these market dynamics, including:

Forecasts, regional trends, and global outlook

IDTechEx's 10-year forecasts break down global steel production and green steel adoption by major regions and production routes, offering a comprehensive outlook into market evolution. The forecasts are segmented by major production routes, including BF-BOF, Scrap-EAF, NG-DRI-EAF, H₂-DRI-EAF, and CCUS-based steel. These global forecasts are also segmented regionally, covering Europe, China, India, Rest of Asia-Pacific, North America, South America, Middle East, and Africa, with outlooks on the evolution of different technologies in each region.

Key Aspects

This report offers key insights for stakeholders interested in understanding the technological pathways, market dynamics, and competitive landscape shaping the transition to low-carbon and green steel production.

Sustainable Steel Production Technology and Market Analysis:

Industry Trends and Market Dynamics:

Market Forecasts and Regional Analysis:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Current state of the iron & steel industry - top producing regions

1.2. Top steelmakers globally

1.3. Global steel use in finished products

1.4. Overview of steel production routes

1.5. Why is steel production difficult to decarbonize?

1.6. Steel industry emissions are approaching 10% of global emissions

1.7. Overview of decarbonization technologies for the steel sector

1.8. Green steel - what is it & how is it made?

1.9. Green steel regulation & policies - global overview

1.10. Overview of the iron ore mining industry

1.11. Decarbonization technologies in iron ore agglomeration (pelletizing & sintering)

1.12. Overview of strategies to lower emissions of blast furnace sites

1.13. Replacing blast furnaces with coal-based smelting reduction alternatives

1.14. CCUS will play a limited role in decarbonizing the iron and steel sector

1.15. The case for hydrogen in steel decarbonization

1.16. Opportunities for integration of H2 technologies into steelmaking

1.17. H2-DRI-EAF using green H2

1.18. Notable steelmaker & water electrolyzer OEM partnerships

1.19. Players in direct reduction shaft furnace technologies

1.20. Fluidized bed vs fixed bed reduction processes

1.21. Scrap recycling in EAFs is already a key pathway for steel decarbonization

1.22. Major steelmakers are increasing electric arc furnace (EAF) capacity

1.23. Electric smelting furnaces (ESFs) - key benefits over EAFs

1.24. The case for developing alternative ironmaking technologies

1.25. Hydrogen-based ironmaking vs electrified ironmaking

1.26. Company landscape for novel ironmaking technologies

1.27. TRL comparison

1.28. Cost comparison of different green steel production routes

1.29. Potential CO₂ reductions & cost of CO₂ abatement comparison

1.30. Steelmakers are establishing new low-carbon steel product lines

1.31. Automotive is the main application market for green steel

1.32. Other sectors adopting green steel

1.33. Project announcements for hydrogen-ready DRI capacity (Mt DRI)

1.34. Example of a green steel supply chain - Stegra

1.35. Global steel production forecast by production route - discussion

1.36. Global steel production forecast by region - discussion

1.37. Low-carbon steel forecast by technology, 2025-2035

1.38. Hydrogen-based green steel forecast by region - discussion (1)

1.39. Hydrogen-based green steel forecast by region - discussion (2)

1.40. LCOS & total global cost of hydrogen-based steel production, 2025-2035

2. INTRODUCTION

2.1. Overview of the global iron & steel industry

2.1.1. Introduction to iron & steel

2.1.2. Overview of the iron ore mining industry - top producing regions

2.1.3. Overview of the iron ore mining industry - top producing companies

2.1.4. Historical growth of the global steel industry

2.1.5. Global steelmaking capacity has shifted from the West to East

2.1.6. Current state of the iron & steel industry - top producing regions

2.1.7. Overview of steel production routes

2.1.8. Regional distribution of the iron & steel plants

2.1.9. Global ironmaking capacity

2.1.10. Global steelmaking capacity

2.1.11. Top steelmakers globally

2.1.12. Recent trends in the steel market

2.1.13. Global steel use in finished products (1)

2.1.14. Global steel use in finished products (2)

2.1.15. Recent trends in top steel producing countries (1)

2.1.16. Recent trends in top steel producing countries (1)

2.1.17. Recent trends in top steel producing countries (1)

2.1.18. Major market drivers & barriers in the steel sector

2.2. Conventional iron & steel production using BF-BOF

2.2.1. The steel industry rapidly adopts new technology but still relies on coal

2.2.2. BF-BOF process overview

2.2.3. Blast furnace operation - overview

2.2.4. Blast furnace operation - reactions

2.2.5. Blast furnace material balance - inputs & outputs

2.2.6. Blast furnace sizes

2.2.7. Blast furnace gas management

2.2.8. Downstream steelmaking process

2.2.9. Alloying elements used in steel

2.2.10. Steelmaking - basic oxygen furnace (BOF) vs electric arc furnace (EAF)

2.3. The need for green steel

2.3.1. Steel industry emissions are approaching 10% of global emissions

2.3.2. Why is steel production difficult to decarbonize?

2.3.3. Breakdown of CO₂ emissions from the conventional BF-BOF process

2.3.4. Main CO₂ reduction focuses for the iron and steel industry

2.3.5. Overview of decarbonization technologies for the steel sector

2.3.6. Green steel - what is it & how is it made?

2.3.7. Main routes to green steel (1)

2.3.8. Main routes to green steel (2)

2.3.9. Key drivers & barriers for the green steel industry

2.4. Stimulating demand for green steel: policies & regulation

2.4.1. Green steel regulation & policies - global overview

2.4.2. Green steel policy frameworks & decarbonization strategies (1)

2.4.3. Green steel policy frameworks & decarbonization strategies (2)

2.4.4. Green steel policy frameworks & decarbonization strategies (3)

2.4.5. Green steel policy frameworks & decarbonization strategies (4)

2.4.6. Green steel policy frameworks & decarbonization strategies (5)

2.4.7. Introduction to carbon pricing, carbon markets & emissions trading systems

2.4.8. Compliance carbon pricing mechanisms across the globe

2.4.9. EU ETS impact on the European steel industry - past, present & future

2.4.10. EU Carbon Border Adjustment Mechanism (CBAM)

2.4.11. Key definitions for CBAM

2.4.12. EU CBAM - compliance & timelines

2.4.13. Steel industry criticism of the EU CBAM & proposed reforms

2.4.14. How might CBAM impact the steel market?

2.4.15. EU regulations driving green steel use in automotive

2.4.16. ESPR regulations in Europe & potential impacts on steel

2.4.17. Potential impacts of Trump's tariffs on the steel & aluminum sectors

2.4.18. US green steel projects face uncertainty under Trump's administration

3. DECARBONIZATION OF EXISTING IRON & STEEL FACILITIES

3.1. Iron ore mining decarbonization

3.1.1. Iron ore types - magnetite is preferred for green steel

3.1.2. Iron ore mining & beneficiation

3.1.3. Renewable energy use in mining operations

3.1.4. Opportunities & challenges for renewable energy use in mining

3.1.5. Advantages & barriers to electrification of mining equipment

3.1.6. CO₂ emission contribution of mining vehicles

3.1.7. Emissions targets of mining industry companies

3.1.8. Canada incentivizing decarbonization of mining vehicles

3.1.9. Where might mining EVs be adopted?

3.1.10. Productivity benefits of electric vehicles

3.1.11. Key mining vehicle types for electrification

3.1.12. Major electrification activity of OEMs

3.1.13. Fortescue goes big on Liebherr mining EVs

3.1.14. Electric dump trucks entering full-time use in Europe

3.2. Decarbonizing iron ore agglomeration

3.2.1. Supply chain overview

3.2.2. Processed iron ore - lumps, sinters, pellets

3.2.3. Comparison of iron ore lumps, sinters & pellets

3.2.4. Additive materials - coke, limestone & others

3.2.5. Decarbonization technologies in iron ore agglomeration (pelletizing & sintering)

3.2.6. Commercial approaches to emission reductions in agglomeration (1)

3.2.7. Commercial approaches to emission reductions in agglomeration (2)

3.2.8. Major iron ore agglomeration process technology suppliers

3.2.9. Adjusting sinter composition can reduce CO₂ emissions

3.2.10. Primetals Technologies' sinter plant improvements

3.2.11. Baosteel's microwave sintering technology

3.2.12. CO₂ emissions in iron ore pelletizing

3.2.13. LKAB's fuel switching tests for pelletizing operations

3.2.14. CSIRO's new pelletizing process

3.2.15. Metso Outotec's next-gen pelletizing plants

3.2.16. Vale's cold iron ore briquetting technology

3.3. Blast-furnace decarbonization & other coal-based alternatives

3.3.1. Overview of strategies to lower emissions of blast furnace sites

3.3.2. Companies using biomass as a reducing agent

3.3.3. Hydrogen injection into blast furnaces - Nippon Steel

3.3.4. Other companies considering hydrogen injection into blast furnaces

3.3.5. Paul Wurth case study - syngas dry reforming for blast furnaces

3.3.6. Paul Wurth case study - plasma-based heating & syngas injection

3.3.7. University of Queensland - feedstock optimization for low-volume slag

3.3.8. University of Queensland - DRI-BF hybrid processes

3.3.9. Replacing blast furnaces with coal-based smelting reduction alternatives

3.3.10. Tata Steel's Hisarna process

3.3.11. POSCO's FINEX process

3.3.12. Coal-based rotary kiln DRI & SL/RN process

3.3.13. Rotary hearth furnace (RHF)

3.4. CCUS in the steel sector

3.4.1. CCUS will play a limited role in decarbonizing the iron and steel sector

3.4.2. What is carbon capture, utilization and storage (CCUS)?

3.4.3. The CCUS value chain

3.4.4. Overview of CCUS for iron & steel (1)

3.4.5. Overview of CCUS for iron & steel (2)

3.4.6. CCUS for BF-BOF (blast furnace-basic oxygen furnace) process

3.4.7. How does CO₂ partial pressure influence cost?

3.4.8. When should different carbon capture technologies be used?

3.4.9. Post combustion capture technologies for BF-BOF process

3.4.10. Amine-based post-combustion CO₂ absorption

3.4.11. Pre-combustion carbon capture for ironmaking (1)

3.4.12. Pre-combustion carbon capture for ironmaking (2)

3.4.13. Sorption enhanced water gas shift (SEWGS)

3.4.14. Gas recycling and oxyfuel combustion for ironmaking

3.4.15. Blast furnace gas CO₂ capture technologies comparison

3.4.16. Carbon capture for natural gas-based DRI

3.4.17. CCUS project pipeline for the steel sector

3.4.18. Development of the CCUS business model

3.4.19. Overview of CO₂ storage

3.4.20. Storage-type TRL and operator landscape

3.4.21. Overview of CO₂ transportation

3.4.22. CO₂ utilization for the steel sector

3.4.23. Carbon capture costs by industrial sector

3.4.24. What is a carbon credit and carbon offsetting?

3.4.25. Steelmakers purchasing carbon credits

3.4.26. Challenges and opportunities for CCUS in the steel sector

3.5. Electric arc furnace (EAF) steelmaking & renewable energy use

3.5.1. Scrap recycling in EAFs is already a key pathway for steel decarbonization

3.5.2. Ferrous scrap is a key raw material for the steel industry

3.5.3. Why are EAFs needed for green steelmaking?

3.5.4. Major steelmakers are increasing electric arc furnace (EAF) capacity

3.5.5. Electric arc furnace (EAF) design

3.5.6. Leading EAF supplier case study - Tenova

3.5.7. Ultra-high power (UHP) EAF

3.5.8. Major EAF suppliers (1)

3.5.9. Major EAF suppliers (2)

3.5.10. Scrap-EAF process & the need for net-zero DRI-EAF

3.5.11. Renewable energy procurement for EAF steelmaking - key commercial activities

3.5.12. Nuclear power for steelmaking - reasons for adoption

3.5.13. Nuclear power plans & investments from steelmakers

3.5.14. Concentrated solar power & thermal energy storage for steelmaking

4. HYDROGEN-BASED STEEL PRODUCTION

4.1. Overview of the hydrogen supply chain for steelmaking

4.1.1. The case for hydrogen in steel decarbonization

4.1.2. Key technology providers for DRI production

4.1.3. The colors of hydrogen

4.1.4. State of the hydrogen market today

4.1.5. Why is green hydrogen needed?

4.1.6. Typical green hydrogen plant layout

4.1.7. Typical green hydrogen plant layout

4.1.8. Electrolyzer cells, stacks and balance of plant (BOP)

4.1.9. Green hydrogen: main electrolyzer technologies

4.1.10. Commercial progress of green hydrogen

4.1.11. Hydrogen Value Chain Overview

4.1.12. LCOH forecast for different types of hydrogen (grey, blue & green)

4.1.13. Opportunities for integration of H2 technologies into steelmaking

4.1.14. H2-DRI-EAF using green H2

4.1.15. Notable steelmaker & water electrolyzer OEM partnerships

4.1.16. Salzgitter using solid oxide electrolyzers (SOECs) for DRI

4.1.17. Potential integration of methane pyrolysis into iron & steel processes

4.1.18. Hydrogen used in steel rolling - Ovako

4.1.19. SWOT analysis for low-carbon hydrogen use in green steel

4.2. Hydrogen-based direct reduction of iron (DRI) & EAF steelmaking

4.2.1. Current state of the global direct reduced iron (DRI) production

4.2.2. DRI-EAF process overview

4.2.3. Direct reduction shaft furnaces

4.2.4. DR shaft furnaces vs blast furnaces

4.2.5. H2-DRI-EAF process inputs & outputs

4.2.6. Players in direct reduction shaft furnace technologies

4.2.7. Midrex process

4.2.8. Energiron process

4.2.9. Replacing natural gas with hydrogen in DRI-EAF (1)

4.2.10. Replacing natural gas with hydrogen in DRI-EAF (2)

4.2.11. Fluidized bed vs fixed bed reduction processes

4.2.12. POSCO FINEX & HyREX processes

4.2.13. Circored process

4.2.14. Challenges in commercializing the Circored process

4.2.15. HYFOR process

4.2.16. Direct reduced iron (DRI) output

4.2.17. Comparison of DRI outputs

4.2.18. Steelmaking process

4.2.19. Major steelmakers are increasing electric arc furnace (EAF) capacity

4.2.20. Steelmaking - basic oxygen furnace (BOF) vs electric arc furnace (EAF)

4.2.21. EAF energy & material consumption

4.2.22. Challenges for zero-carbon EAF operation

4.2.23. Replacing coke and coal with biochar in the EAF

4.3. Electric smelting furnaces (ESF)

4.3.1. EAF limitations & comparison to ESF

4.3.2. Electric smelting furnaces (ESFs) - key benefits over EAFs

4.3.3. Electric smelting furnaces (ESFs) - integration opportunity with existing plants

4.3.4. Commercial ESF design examples & technology suppliers

4.3.5. Companies leading electric smelting furnace development

4.3.6. Companies leading electric smelting furnace development

5. NOVEL IRONMAKING TECHNOLOGIES5.1. Overview of novel iron & steel technologies

5.1.1. The case for developing alternative ironmaking technologies

5.1.2. Hydrogen-based ironmaking vs electrified ironmaking

5.1.3. Company landscape for novel ironmaking technologies

5.2. Electrochemical ironmaking

5.2.1. SIDERWIN - electrowinning technology (1)

5.2.2. SIDERWIN - electrowinning technology (2)

5.2.3. ArcelorMittal & John Cockerill - Volteron electrowinning

5.2.4. Electra - electrowinning technology (1)

5.2.5. Electra - electrowinning technology (2)

5.2.6. Fortescue's direct electrochemical reduction (DER)

5.2.7. Element Zero - medium-temperature electrolysis

5.2.8. Boston Metal - molten oxide electrolysis (1)

5.2.9. Boston Metal - molten oxide electrolysis (2)

5.2.10. Metalysis - solid-state electrolysis (1)

5.2.11. Metalysis - solid-state electrolysis (2)

5.3. Thermochemical & hydrogen plasma-based ironmaking

5.3.1. HyIron - direct reduction using H2 in rotary kilns (1)

5.3.2. HyIron - direct reduction using H2 in rotary kilns (2)

5.3.3. Flash ironmaking technology

5.3.4. Helios - novel sodium-based thermal process (1)

5.3.5. Helios - novel sodium-based thermal process (2)

5.3.6. Hydrogen plasma smelting reduction (HSPR) (1)

5.3.7. Hydrogen plasma smelting reduction (HSPR) (2)

5.3.8. HSPR startups - Hertha Metals & Ferrum Technologies

5.4. Electrified heating for ironmaking

5.4.1. Calix's ZESTY process - electrified heating

5.4.2. Microwave-based iron reduction initiatives

5.4.3. Rio Tinto BioIron - reduction with microwaves & biomass (1)

5.4.4. Rio Tinto BioIron - reduction with microwaves & biomass (2)

5.4.5. Laser heating for ironmaking - Limelight Steel

6. TECHNO-ECONOMIC COMPARISON OF STEEL PROCESSES6.1. TRL comparison

6.2. Iron feedstock requirements for different steelmaking routes

6.3. Energy consumption of different steel production routes

6.4. Levelized cost of steel (LCOS) overview

6.5. Cost comparison of different green steel production routes

6.6. CAPEX, OPEX and fuel costs of different steel production routes

6.7. Carbon footprint comparison of different steel production routes

6.8. Potential CO₂ reductions & cost of CO₂ abatement comparison

6.9. Emission variations due to source of electricity

6.10. Regional variations in LCOS for hydrogen-based steelmaking

6.11. Impact of natural gas replacement with green hydrogen in DRI-EAF

7. GREEN STEEL MARKET ANALYSIS7.1. Green steel projects announcements & players

7.1.1. Steelmakers' decarbonization targets

7.1.2. Project announcements for hydrogen-ready DRI capacity (Mt DRI)

7.1.3. Hydrogen-ready DRI project announcements - Europe

7.1.4. Hydrogen-ready DRI project announcements - Asia-Pacific

7.1.5. Hydrogen-ready DRI project announcements - Rest of the World

7.1.6. Green iron & steel create opportunities for new production hubs globally

7.1.7. Green iron & steel corridors - potential to reshape global supply chains

7.1.8. HYBRIT project - SSAB, LKAB & Vattenfall

7.1.9. SSAB's low-carbon steel

7.1.10. Stegra (H2 Green Steel)

7.1.11. Example of a green steel supply chain - Stegra

7.1.12. Steelmakers are establishing new low-carbon steel product lines

7.1.13. Steelmakers using mass balance allocation

7.1.14. Green steel certificates used for reinvestment for new technologies

7.1.15. SSAB's low-emission steel use case example

7.1.16. JFE Steel's low-emission steel use cases

7.1.17. HBIS Group's hydrogen DRI project in China

7.1.18. ArcelorMittal's freeze on green hydrogen DRI projects (1)

7.1.19. ArcelorMittal's freeze on green hydrogen DRI projects (2)

7.1.20. US green steel projects & uncertainty under Trump's administration

7.2. Green steel in application sectors

7.2.1. Steel prices - key trends since 2020

7.2.2. Steel HRC prices in 2024-2025

7.2.3. Steel market trends & effect on green steel

7.2.4. Sustainable Steel Buyers Platform

7.2.5. Automotive is the main application market for green steel

7.2.6. Other sectors adopting green steel

7.2.7. Steel is vital for the energy transition

7.2.8. ESPR regulations in Europe & potential impacts on steel

7.2.9. Green steel premiums in automotive

7.2.10. Green steel premiums in construction

7.2.11. Green steel premiums in other sectors

7.2.12. Example of a green steel supply chain - Stegra

7.2.13. Automotive off-takers for green steel & low-carbon steel (Europe)

7.2.14. Automotive off-takers for green steel & low-carbon steel (USA & Asia)

7.2.15. Tier 1 & 2 automotive off-takers for green steel & low-carbon steel (Europe)

7.2.16. Off-takers in other application markets for green steel (equipment & machinery)

7.2.17. Off-takers in other application markets for green steel (construction-related)

7.2.18. Tech companies' interest in green steel

7.2.19. Role of steel in data centers

7.3. Regional trends in the steel market

7.3.1. Regional overview & market dynamics (1)

7.3.2. Regional overview & market dynamics (2)

7.3.3. Expectations for evolution of steelmaking routes in different countries (1)

7.3.4. Expectations for evolution of steelmaking in different countries (2)

8. MARKET FORECASTS8.1. Global steel market forecasts

8.1.1. Regional segmentation of forecasts for steel

8.1.2. Forecasting methodology & assumptions

8.1.3. Global steel production forecast by production route, 2025-2035

8.1.4. Global steel production forecast by production route - discussion

8.1.5. Global steel production forecast by region, 2025-2035

8.1.6. Global steel production forecast by region - discussion

8.1.7. Regional trends in production technologies (1)

8.1.8. Regional trends in production technologies (2)

8.2. Green steel market forecasts

8.2.1. Low-carbon steel forecast by technology, 2025-2035

8.2.2. Fossil fuel-based DRI-EAF steel forecast by region, 2025-2035

8.2.3. Hydrogen-based green steel forecast by region, 2025-2035

8.2.4. Hydrogen-based green steel forecast by region - discussion (1)

8.2.5. Hydrogen-based green steel forecast by region - discussion (2)

8.2.6. Levelized cost of hydrogen-based steel forecast, 2025-2050

8.2.7. Total global cost of hydrogen-based steel production, 2025-2035

8.2.8. Hydrogen demand forecast for green steel

8.2.9. Carbon capture for steel forecast, 2024-2035

9. COMPANY PROFILES

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(金属材料)の最新刊レポートIDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

本レポートと同じKEY WORD(steel)の最新刊レポートよくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|