レドックスフロー電池市場2026~2036年:予測、市場、技術、プレイヤーRedox Flow Batteries Market 2026-2036: Forecasts, Markets, Technologies and Players この調査レポートは、レドックスフロー電池(RFB)の世界市場を分析し、主要企業、技術ベンチマーク、材料・部品の技術革新、電解質生産、政策、用途、長時間エネルギー貯蔵(LDES)、データセンター、10年間... もっと見る

サマリーこの調査レポートは、レドックスフロー電池(RFB)の世界市場を分析し、主要企業、技術ベンチマーク、材料・部品の技術革新、電解質生産、政策、用途、長時間エネルギー貯蔵(LDES)、データセンター、10年間の市場予測などを掲載しています。 IDTechExの予測によると、レドックスフロー電池(RFB)市場は2036年までに金額ベースで92億米ドルに達する見込みである。電力網における可変再生可能エネルギー(VRE)の普及が進むと、こうした断続的な電源からの供給が発生しない期間が長くなる。このため、6時間以上の長い時間枠で経済的にエネルギーを供給できる長時間エネルギー貯蔵(LDES)技術の需要が生まれる。リチウムイオン電池蓄電システム(BESS)のコストは下がり続けているが、これらの技術はエネルギー容量と出力を切り離すことはできない。RFBは、エネルギー容量については電解液量を、出力についてはセルスタックを独立にスケーリングすることで、これを可能にする。理論的には、より長時間の貯蔵で、リチウムイオンBESSよりも低い設備投資額(米ドル/kWhベース)を達成することができる。このことは、豊富な材料を使用する有機または鉄ベースのRFB、あるいは合成コストの安い電解質など、バナジウム以外の化学的性質と相まって、長期的にはより低コストのRFB技術が有望であることを示唆している。

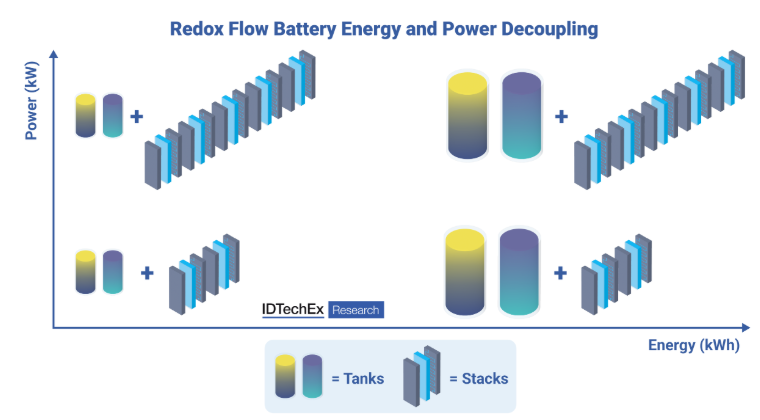

レドックスフロー電池のエネルギーと電力のデカップリング。出典:IDTechEx:IDTechEx.

LDES技術に対する将来の需要以外では、人工知能(AI)ブームの中で、RFBはデータセンターをサポートするためにも使われる可能性がある。IDTechExは、欧米で開発されているRFBを利用したデータセンター・プロジェクトをいくつか観測している。RFBは、持続的な無停電電源装置(UPS)を提供し、不安定な計算負荷を管理し、グリッドから電力をピークカットするためのディーゼル発電機の必要性を代替することで、データセンターの脱炭素化を支援することができる。RFBには不燃性電解液が使用されており、最近の大規模火災の中でリチウムイオン蓄電池の安全性に対する監視の目が高まっていることも、RFB開発者にとって重要な価値提案となっている。電解液のリサイクル可能性や、蓄電期間が長いほど平準化蓄電コスト(LCOS)が低くなるといった他の主要な利点も、中期的にはRFB開発企業によって活用されるであろう。2026~2036年のRFB市場の年平均成長率(CAGR)は27%である。

過去数年間、RFB市場は2023年以前と比べて大きく成長しており、主要プレーヤーであるRongke Powerは複数の100MWhフロー電池プロジェクト、さらにはGWh規模のプロジェクトを担当している。住友電気工業、Invinity Energy Systems、CellCubeといった他の主要プレーヤーも、事業を拡大しサプライチェーン・パートナーシップを形成しながら、バナジウムフローバッテリーを着実に大量導入し続けている。市場全体の資金調達額も大きく、IDTechExはRFBプレーヤーによる累計調達額が10億米ドルを超えることを確認している。これは、既存のリチウムイオンBESSと競合するあらゆるエネルギー貯蔵技術にとって重要な金額である。

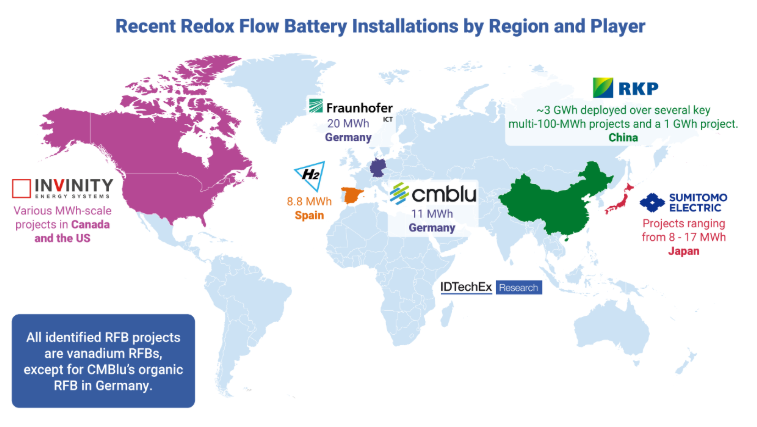

最近設置されたレドックスフロー電池プロジェクト出典IDTechEx.

RFBの成長を促進する政策とプログラム

最近のRFBの成長は著しいが、その量はリチウムイオンBESSのそれに比べればまだ小さい。これは主に、バナジウムRFB(VRFB)技術のコストが高いことに起因している。RFBとLDESの成長を支えるために、米国のOBBBA(One Big Beautiful Bill Act)、英国のキャップ・アンド・フロア制度、カリフォルニア州エネルギー委員会(CEC)が支援する主要プロジェクトなどの主要な政策やプログラムも、成長する西側RFB市場の出現に影響を与えるだろう。このIDTechExレポートでは、これらの政策、プログラム、プロジェクトの影響について論じている。

レドックスフロー電池化学

VRFBは、その十分な性能により、最も広く導入され、理解されているRFB化学である。リチウムイオンBESSと比較すると、この性能はしばしば劣り(エネルギー密度など)、貯蔵期間が短いとコストが高くなる。これは、重要な鉱物であるバナジウムを使用する高価な電解液を使用することに起因する。そのため、バナジウム以外のRFB化学物質への需要が近年高まっている。IDTechExは、全鉄、クロム、亜鉛、バナジウム、および水素を含む可能性のある有機および鉄ベースの化学物質の開発、商業化、および主要プロジェクトの増加を観察している。また、マンガン、CO2、塩水、マイクロエマルジョン製剤など、ニッチなRFB化学物質も開発されている。使用できる酸化還元カップルの種類は膨大である。しかし、競争が激化する世界のエネルギー貯蔵市場でRFB技術が成功するためには、エネルギー密度、エネルギー効率、出力密度、システム寿命にわたる強力な性能と相まって、アクセスしやすいサプライチェーンで豊富で低コストの材料を使用することが必要である。IDTechExの本レポートでは、設備投資、商業状態、主要性能指標にわたって10種類のレドックスフロー電池化学をベンチマークし、それぞれの長所と短所を評価するとともに、今後10年間のRFB化学市場シェアの見通しを示している。

コンポーネント、材料、電解質におけるイノベーション

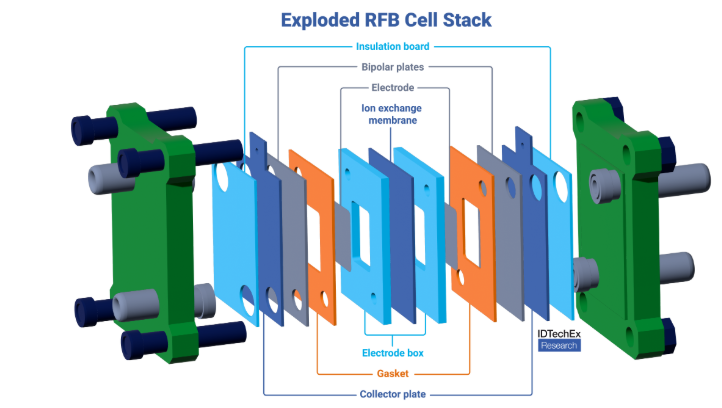

電解質はフロー電池の主要部品のひとつであるが、これらのデバイスは複雑なシステムであり、その構造は燃料電池や電解槽に似ている。全体的な性能は、電解液、セルスタック、プラントバランスなどの構成部品によって決まる。IDTechExは、電極とバイポーラプレート(BPP)を中心に、スタックの出力密度を向上させるためのセルスタック材料とコンポーネントの技術革新を観察してきた。実際、エネルギー貯蔵市場におけるRFB全体の見通しを改善するためには、RFBコンポーネントの性能を向上させる必要がある。バナジウム電解液の製造能力の拡大も観察されており、主要地域の電解液メーカーとRFB開発者の間でサプライチェーン・パートナーシップの構築やリースが行われている。このIDTechExレポートは、バナジウム供給、主要電解質市場の最新情報、セルスタック構成部品の技術革新、主要部品サプライヤー、PFASベースの膜と代替品に関する主要な解説を含むセルスタックの今後の材料動向に関する分析を提供している。

レドックスフロー電池のセルスタックとコンポーネントの分解図。出典IDTechEx.

予測

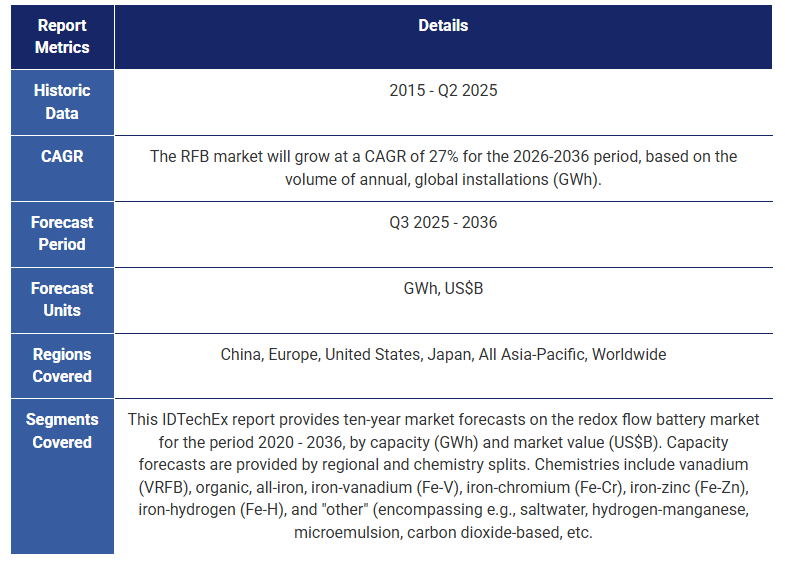

このIDTechExのレポートでは、2020年から2036年までのレドックスフロー電池市場について、地域別(GWh)、化学別(GWh)、化学別金額別(億米ドル)の10年間の市場予測を掲載しています。地域には中国、欧州、米国、日本、その他のアジア、その他の地域が含まれます。化学別予測には、バナジウム(VRFB)、有機、全鉄、鉄-バナジウム(Fe-V)、鉄-クロム(Fe-Cr)、鉄-亜鉛(Fe-Zn)、鉄-水素(Fe-H)、「その他」が含まれる。

企業プロファイル

このIDTechExレポートには、レドックスフロー電池プレーヤー、セルスタック部品・材料サプライヤー、電解質メーカー・サプライヤーを含む45社の企業プロファイルが掲載されています。

主要な側面

本レポートは以下の情報を提供します。

目次1.エグゼクティブサマリー

1.1.世界のレドックスフロー電池市場のヘッドラインと主な解説

1.2.レドックスフロー電池と隣接市場の主な推進要因と機会

1.3.レドックスフロー電池と隣接市場の主要課題

1.4.エネルギー貯蔵技術の分類

1.5.RFB-エネルギーと電力のデカップリング(1)

1.6.RFB - エネルギーと電力の分離(2)

1.7.長期エネルギー貯蔵とは?

1.8.RFB - LDESのエネルギーと電力のデカップリングとリチウムイオンBESSとの比較

1.9.LDES技術の市場タイミングVREによる世界平均発電ミックス

1.10.レドックスフロー電池の用途とタイムラインの概要

1.11.バナジウムレドックスフロー電池とリチウムイオン電池の LCOS(4 時間、6 時間、8 時間、10 時間)

1.12.レドックスフロー電池対リチウムイオン電池蓄電システム - GWh別設置量、市場概要、主な利点

1.13.英国の「キャップ・アンド・フロア制度」の概要とスケジュール

1.14.レドックスフロー電池技術と化学の展望

1.15.RFB 技術のベンチマーク(設備投資、電解液コスト、商業状況、電圧、エネルギー密度、エネルギー効率、電解液の溶解性など)

1.16.化学物質別のRFBの長所、短所、商業状況

1.17.コスト削減と性能向上のための RFB コンポーネントと材料の動向

1.18.RFBスタック部品の概要

1.19.RFB構成材料の概要-既存材料と将来材料

1.20.RFBセルスタック材料マップ

1.21.IEM材料はRFBスタック全体のコストに大きく寄与する

1.22.より高い出力密度でRFBセルのコスト削減を可能にする

1.23.RFB材料・部品サプライヤーとプレーヤーマップ

1.24.バナジウム供給、生産、2025年のV2O5価格、長期トレンドの概要

1.25.レドックスフロー電池市場 - 主要動向、プレーヤーの活動、パートナーシップ、化学、資金調達、導入、用途

1.26.2015-2025年のレドックスフロー電池の地域別展開

1.27.レドックスフロー電池のプレーヤー別累積導入量と市場シェア(MWh)

1.28.化学別のレドックスフロー電池の累積導入量(MWh)

1.29.化学別のRFB技術開発者マップ

1.30.2023-2025 年の RFB プロジェクト(用途別)-C&I 対グリッドスケール(MWh)

1.31.RFB開発者が2023年第3四半期~2025年第2四半期に受け取った資金と投資額(百万米ドル)と累積資金

1.32.2023-2025年のRFBプロジェクトの主な世界導入実績

1.33.主要および特定された将来のRFB世界プロジェクトマップ

1.34.世界のRFBと電解液の生産能力(プレーヤー別、地域別)マップ(MWh/年、化学)

1.35.世界のRFB生産と電解質生産の拡張:プレーヤーと地域マップ

1.36.RFB開発企業と電解質供給取引と合弁事業(JV)マップ

1.37.世界のRFB市場における代替RFB化学メーカーの新規参入とプロジェクト開発者

1.38.主要RFB開発企業の閉鎖と再編

1.39.レドックスフロー電池の地域別予測(GWh) 2020-2036年

1.40.レドックスフロー電池の化学別予測(GWh)2020-2036年

1.41.レドックスフロー電池化学市場シェア予測・分析

1.42.レドックスフロー電池の金額別予測(US$B)2020-2036年

1.43.IDTechEx サブスクリプションでさらにアクセス

2.用途、長期エネルギー貯蔵、政策、プログラム & 蓄電の平準化費用

2.1.概要

2.1.1.レドックスフロー電池の用途とタイムラインの概要

2.2.用途と収益の流れ

2.2.1.BESS市場の3つの中核セグメント

2.2.2アプリケーションと収益の概要

2.2.3.ビジネスモデルと収益の流れの概要

2.2.4.収益の流れの説明

2.2.5.FTM:アンシラリーサービスにおける蓄電池の提供価値

2.2.6.FTM:ユーティリティサービスにおける蓄電池の価値

2.2.7.BTM サマリー:蓄電池が顧客側に提供する価値

2.2.8.マイクログリッドと遠隔地

2.2.9.確立されたRFBの応用例

2.2.10.データセンター用レドックスフロー電池 - 新興アプリケーション(1)

2.2.11.データセンター用レドックスフロー電池 - 新興アプリケーション(2)

2.2.12.データセンター向けレドックスフロー電池 - 新興アプリケーション(3)

2.2.13.データセンター支援用RFB - 主要プロジェクト(1)

2.2.14.データセンター向けRFB-主要プロジェクト(2)

2.2.15.住宅用アプリケーションのRFB?

2.3.長期エネルギー貯蔵の紹介

2.3.1.エネルギー貯蔵技術の分類

2.3.2.エネルギー貯蔵技術の利点と欠点

2.3.3.長期エネルギー貯蔵とは何か?

2.3.4.可変再生可能エネルギー(VRE)の紹介

2.3.5.VREによる発電の世界的見通し

2.3.6.GW、GWh、蓄電期間(時間)とVREによる発電量の比較

2.3.7.LDES技術の市場タイミング:VRE による世界平均発電構成

2.3.8.LDESの早期導入地域

2.3.9.IDTechExによるLDESの収益創出の課題と長期エネルギー貯蔵に関する更なる研究

2.4.RFB と LDES の政策とプログラム

2.4.1.Flow Batteries Europe - 欧州におけるフロー電池の政策立案

2.4.2.DESNZ - LDES とエネルギー貯蔵支援プログラム

2.4.3.DESNZ - 英国「キャップ・アンド・フロア制度」のスケジュール

2.4.4.ファラデー研究所(The Faraday Institution) - LDES の需要と将来の英国市場、超低コスト LDES 技術のプログラムに関する見解

2.4.5.カリフォルニア州エネルギー委員会-カリフォルニア州におけるBESS/LDESの開発(1)

2.4.6.カリフォルニア州エネルギー委員会-カリフォルニア州におけるBESS/LDESの開発(2)

2.4.7.OBBBAFEOC の制限、MACR の閾値、45X 生産クレジットの資格への影響

2.4.8.OBBBA後の第48条投資税額控除(ITC)

2.4.9.ハンガリーエネルギー省 - ハンガリーの電力とESS市場、エネルギー貯蔵の入札に関する見解

2.4.10.オーストリアの再生可能エネルギー発電省 - BESS、RFB、LDESの成長を促進する新しい法律

2.5.RFBビジネスとプロジェクト開発の展望

2.5.1.セルキューブ - オーストリアの LDES と RFB 市場に関する見解

2.5.2.セルキューブ - 新興RFB市場、入札、主要用途

2.5.3.EDP - RFBと主要パイロットプロジェクトに関するエネルギー事業者と投資家の見解

2.5.4.Verbund - RFBプロジェクト開発へのエネルギー事業者の関与と電力市場に関する見解

2.5.5.R.Flo - ウクライナのエネルギーグリッドを再構築するための RFB、ウクライナのビジネ スケースと電力市場

2.5.6.Vanevo - RFBのビジネスケース、LCOE、24時間365日のクリーンPPAに関するRFB部品供給会社の見解

2.5.7.Invinity Energy Systems - RFB プロジェクト開発における利害関係者の協力の重要性

2.6.RFB の LCOS 計算

2.6.1.バナジウムレドックスフロー電池とリチウムイオン電池の LCOS(持続時間 4h、6h、8h、10h)

2.6.2.LCOS 計算:計算式と仮定 (1)

2.6.3.LCOS計算:計算式と仮定 (2)

2.6.4.LCOS 計算:計算式と仮定 (3)

2.6.5.LCOS計算:計算式と仮定 (4)

2.6.6.LCOS 計算:考察と限界 (1)

2.6.7.LCOS 計算:考察と限界 (2)

2.6.8.VRFB の平準化貯蔵コストの結論 (1)

2.6.9.VRFBの平準化蓄電コスト結論(2)

3.レドックスフロー電池の技術と化学物質

3.1.概要レドックスフロー電池技術と化学物質

3.1.1.要旨-レドックスフロー電池技術と化学

3.1.2.RFB 技術のベンチマーク(設備投資、電解質コスト、商業的状況、電圧、エネルギー密度、エネルギー効率、電解質の溶解性など)

3.1.3.化学物質別の RFB の強み、弱み、商業状況

3.1.4.化学物質別RFB技術開発者マップ

3.2.レドックスフロー電池技術の紹介

3.2.1.概要 - コスト削減と性能向上を目指すRFBコンポーネントと材料の動向

3.2.2.定義 - RFBの電気化学

3.2.3.定義 - 効率

3.2.4.RFB - エネルギーと電力のデカップリング(1)

3.2.5.RFB - エネルギーとパワーのデカップリング(2)

3.2.6.RFB - LDESのエネルギーと電力のデカップリングとリチウムイオンBESSとの比較(1)

3.2.7.RFB - LDESのエネルギーと電力のデカップリングとリチウムイオンBESSとの比較(2)

3.2.8.RFB - フィット・アンド・フォーゲットの考え方

3.2.9.RFBと燃料電池の比較

3.2.10.酸化還元活性種と溶媒の選択(1)

3.2.11.酸化還元活性種と溶媒の選択(2)

3.2.12.レドックスフロー電池の分類(1)

3.2.13.レドックスフロー電池の分類(2)

3.2.14.レドックスフロー電池の歴史年表

3.3.レドックスフロー電池のケミストリ

3.3.1.オールバナジウムRFB(VRFB)

3.3.2.VRFBの強みと弱み

3.3.3.全鉄製RFB

3.3.4.全鉄RFBの長所と短所

3.3.5.亜鉛鉄(Zn-Fe)系RFB

3.3.6.アルカリ性亜鉛-フェリシアン化物RFB

3.3.7.Zn-Fe RFBの長所と短所

3.3.8.鉄-クロム(Fe-Cr)系RFB

3.3.9.鉄-クロム系RFBの長所と短所

3.3.10.鉄-バナジウム(Fe-V)系RFB

3.3.11.Fe-V RFBの長所と短所

3.3.12.水素-鉄(H-Fe) RFB

3.3.13.H-Fe系RFBの長所と短所

3.3.14.水素マンガン(H-Mn) RFB

3.3.15.H-Mnの強みと弱み

3.3.16.有機レドックスフロー電池(ORFB)

3.3.17.ORFBの分類

3.3.18.ORFBの活性種

3.3.19.ORFBの長所と短所

3.3.20.水素-臭素(H-Br)RFB

3.3.21. H-Br RFBの長所と短所

3.3.22.亜鉛-臭素(Zn-Br)RFB

3.3.23.Zn-Br RFBの長所と短所

3.3.24.ポリスルフィド-臭素(PSB)RFB

3.3.25.PSBの歴史年表

3.3.26.PSBの主な弱点

3.3.27.バナジウム-臭素(V-Br)系RFB

3.3.28.V-Br RFBの強みと弱み

3.3.29.酸塩基(塩水)「フロー電池」

4.レドックスフロー電池セルスタックの材料とコンポーネント

4.1.材料とコンポーネントの概要

4.1.1.まとめ - コスト削減と性能向上のための RFB コンポーネントと材料の傾向

4.1.2.RFBシステムの紹介

4.1.3.RFBスタック構成部品の概要

4.1.4.RFB コンポーネントの材料概要 - 現存する材料と将来の材料

4.1.5.RFBセルスタック材料マップ

4.1.6.RFBの主な材料選択

4.1.7.IEM材料はRFBスタック全体のコストに大きく寄与する

4.1.8.より高い出力密度で RFB セルのコスト削減を可能にする

4.1.9.RFB材料・部品サプライヤーとプレーヤーマップ

4.1.10.イオン交換膜(IEM)、電極、バイポーラプレート(BPP)、その他のコンポーネントに関するさらなる研究

4.1.11.レドックスフロー電池用膜

4.1.12.RFB用イオン交換膜の概要

4.1.13.レドックスフロー電池のイオン交換膜はじめに

4.1.14.レドックスフロー電池のイオン交換膜概要

4.1.15.RFB セルスタック材料マップ

4.1.16.セパレーターの選択 - イオン交換膜(IEM)と多孔質セパレーターの比較

4.1.17.過フッ素イオン交換膜と炭化水素イオン交換膜

4.1.18.レドックスフロー電池の化学物質とIEM要件の概要

4.1.19.PFAS材料禁止の可能性がRFB市場に与える影響

4.1.20.主要膜メーカー(膜素材別)

4.1.21.PFSA膜サプライヤーと膜特性の比較

4.1.22.市販の炭化水素系AEM材料の例(I)

4.1.23.市販の炭化水素系AEM材料の例(II)

4.1.24.Syensqo - 酸化還元フロー電池膜用炭化水素系アイオノマーと炭化水素膜のコスト

4.1.25.Syensqo - レドックスフロー電池用炭化水素膜の性能

4.1.26.RFBにおけるIEM材料の革新分野(I)

4.1.27.RFBにおけるIEM材料の革新分野(Ⅱ)

4.1.28.RFBにおけるIEM材料の革新領域(III)

4.1.29.強化多層IEMの革新領域

4.2.レドックスフロー電池用電極

4.2.1.レドックスフロー電池用電極の概要 - 機能と特性

4.2.2.レドックスフロー電池用電極の概要-基材と触媒

4.2.3.異なるRFBケミストリーに共通する電極触媒

4.2.4.フローナノ - レドックスフロー電池用ナノ構造電極の開発とプロセス

4.2.5.フローナノ-RFB用ナノ構造電極の性能

4.2.6.フローナノ - RFB電極製造プロセスのスケールアップとカーボンナノイオンの継続開発

4.2.7.フローナノ - レドックスフロー電池のためのナノ構造電極のコストメリット

4.2.8.先端炭素材料 - RFB 用リサイクル活性炭とグラファイトフェルト電極

4.3.レドックスフロー電池用バイポーラプレート

4.3.1.RFBにおけるバイポーラプレートの概要 - 機能と材料

4.3.2.RFBにおけるバイポーラプレートの概要-材料と製造

4.3.3.バイポーラプレートの流れ場

4.3.4.流れ場の比較

4.3.5.RFBバイポーラプレートの主要メーカー

4.3.6.Schmalz - RFBにおける圧力損失とシャント電流を最小化するフローフレーム設計の改良

4.3.7.バイポーラプレート・フローフィールドの今後の方向性

4.4.ガスケット、シール、レドックスフロー電池用セルフレーム

4.4.1.RFB用ガスケット

4.4.2.RFB ガスケットの機能と要求事項

4.4.3.ガスケット設計の考慮点

4.4.4.ガスケット材料の選定(1/2)

4.4.5.ガスケット材料の選定(2/2)

4.4.6.レドックスフロー電池用ガスケット及びシール材サプライヤー

4.4.7.WEVO-CHEMIE - RFB ガスケット、シール剤、接着剤 (1)

4.4.8.WEVO-CHEMIE - RFB ガスケット、シーラント、接着剤(2)

4.4.9.WEVO-CHEMIEのガスケット製造における考慮点、利点、RFB用途への供給

4.4.10.Oリング及び射出成形ガスケット

4.4.11.セルフレーム

4.5.レドックスフロー電池のその他の部品

4.5.1.集電板 - 概要と主要材料

4.5.2.集電板-技術革新と主要サプライヤー

4.5.3.RFB 用エンドプレート/絶縁板

4.5.4.Syensqo - PPSエンドプレート

4.5.5.ピンフロー(Pinflow) - RFB部品の供給とRFB開発者のサポート

4.5.6.BioZen Batteries - RedoxinoTM ミニフローセルテストシステム

5.レドックスフロー電池市場、バナジウム電解質市場、主な最新情報

5.1.レドックスフロー電池市場の概要、最新情報、データ分析

5.1.1.レドックスフロー電池市場のエグゼクティブサマリー - 主要動向、プレイヤーの活動、パートナーシップ、化学、資金調達、導入、用途

5.1.2.2015ー2025年の地域別レドックスフロー電池展開

5.1.3.プレーヤー別のレドックスフロー電池の累積導入量と市場シェア(MWh)

5.1.4.化学別のレドックスフロー電池の累積導入量(MWh)

5.1.5.化学別のRFB技術開発者マップ

5.1.6.アプリケーション別 RFB プロジェクト 2023-2025年 - C&I 対グリッドスケール(MWh)

5.1.7.用途別 RFB プロジェクト 2023-2025年 - グリッド規模プロジェクトの用途分析

5.1.8.アプリケーション別 RFB プロジェクト 2023-2025年 - C&I プロジェクトアプリケーション分析

5.1.9.2023 年第 3 四半期ー2025 年第 2 四半期の RFB 開発企業の資金調達額と投資額(百万米ドル)

5.1.10.RFB開発者の累積資金(百万米ドル)

5.1.11.2023ー2025年の世界の主要RFBプロジェクト導入実績

5.1.12.主要及び特定された将来のRFB世界プロジェクト地図

5.1.13.世界のRFBと電解液の生産能力(プレーヤー別、地域別)マップ(MWh/年、化学)

5.1.14.世界のRFB生産と電解質生産の拡張:プレーヤーと地域マップ

5.1.15.RFB開発企業と電解質供給取引と合弁事業(JV)マップ

5.1.16.主要なRFB開発企業と電解質メーカーの合弁事業とパートナーシップ(1)

5.1.17.主要RFB開発企業と電解質メーカーの合弁事業とパートナーシップ(2)

5.1.18.世界のRFB市場における代替RFB化学メーカーの新規参入とプロジェクト開発業者

5.1.19.主要RFB開発企業の閉鎖と再編

5.1.20.過去の RFB プロジェクトの生データ表 2023-2025年 [技術提供者、パートナー、MW、MWh、貯蔵期間、化学、導入年、国、地域、用途、C&I 対グリッド] (1)

5.1.21.過去のRFBプロジェクトの生データ表 2023-2025年 [技術提供者, パートナー, MW, MWh, 蓄電期間, 化学, 導入年, 国, 地域, 用途, C&I vs グリッド] (2)

5.1.22.過去のRFBプロジェクトの生データ表 2023-2025年 [技術提供者、パートナー、MW、MWh、貯蔵期間、化学、導入年、国、地域、用途、C&I vs グリッド] (3)

5.1.23.将来の RFB プロジェクトの生データ表(2026ー2027年)[技術提供者、パートナー、MW、MWh、貯蔵期間、化学、将来の導入年、国、地域、用途、C&I 対グリッド]

5.1.24.将来の RFB プロジェクトの生データ表(2028ー2029年超)[技術提供者、パートナー、MW、MWh、貯蔵期間、化学、将来の導入年、国、地域、用途、C&I 対グリッド]

5.1.25.RFBの生産能力と拡張:生データ表[MWh/年、所在地]

5.1.26.バナジウム電解液の生産能力と拡張:生データ表[プレーヤー, MWh /年, 所在地, RFBの顧客]

5.2.RFBの主要プレーヤー、VRFB技術、プロジェクトの最新情報 2023-2025年

5.2.1.Rongke Power - 世界をリードするRFBプレーヤーからの最新情報

5.2.2.サウジアラムコ - サウジアラビアでのFe-V RFB開発とスケールアップ、栄科電力との主要パートナーシップ (1)

5.2.3.栄科電力の主要VRFB プロジェクト

5.2.4.サウジアラムコ - サウジアラビアでの Fe-V RFB 開発とスケールアップ、栄科電力との主要パートナーシップ(2)

5.2.5.住友電工 - VRFB とグローバルな活動

5.2.6.住友電工 - 構成、エネルギー密度、技術設備投資、バナジウム市場

5.2.7.インビニティ・エナジー・システムズ - 主要市場の最新情報と考察

5.2.8.インビニティ・エナジー・システムズの概要と貯蔵期間の変化に対する設計

5.2.9.インビニティ・エナジー・システムズ - Endurium VRFB 技術(1)

5.2.10.インビニティ・エナジー・システムズ-エンデュリアムVRFB技術(2)

5.2.11.インビニティ・エナジー・システムズ - 電解液中の金属不純物の許容範囲、電解液添加剤、コスト

5.2.12.セルキューブ - VRFB技術開発と現地視察からの考察

5.2.13.セルキューブ - 現場視察からの洞察、製造工程、品質管理、セルスタックの進化

5.2.14.セルキューブ - バナジウム電解質の不均衡と酸化状態の変化を管理する戦略(1)

5.2.15.セルキューブ - バナジウム電解質の不均衡と酸化状態の変化を管理するための戦略(2)

5.2.16.セルキューブ - バナジウム電解質の不均衡と酸化状態の変化を管理するための戦略(3)

5.2.17.出光興産 - 住友電工とのオーストラリアにおけるVRFBプロジェクト開発と、オーストラリアにおけるLDESの価値提案の欠如に関する見解

5.2.18.フレックスベース-データセンター向けRFBプロジェクトの開発(1)

5.2.19.データセンター向け RFB - 主要プロジェクト(2)

5.2.20.H2, Inc. - スペインにおける主要VRFBプロジェクト、システム・アーキテクチャ、部品輸送ロジスティク スに関する教訓

5.2.21.H2, Inc. - 最新のVRFB技術と性能測定基準

5.2.22.VFlowTech - シンガポールにおける VRFB 実証プロジェクト

5.2.23.フラウンホーファーICT - プロジェクトSMHYLESにおけるVRFBの開発

5.3.バナジウム電解液市場と最新情報

5.3.1.エグゼクティブサマリー - 2025年のバナジウム供給、生産、V2O5価格の概要と長期トレンド

5.3.2.世界の地域別・技術別バナジウム生産量

5.3.3.2022年以前のバナジウム価格動向と需要急増

5.3.4.RFB電解質の原料

5.3.5.バナジウムの概要

5.3.6.バナジウム鉱業と製品(1)

5.3.7.バナジウム鉱業と製品(2)

5.3.8.バナジウム鉱石の加工

5.3.9.バナジウムジュニアマイナーとプロジェクト

5.3.10.バナジウム電解液のリサイクル

5.3.11.バナジウム電解液のリース

5.3.12.電解液漏れの緩和

5.3.13.RFB開発者と電解質供給取引と合弁事業(JV)マップ

5.3.14.主要なRFB開発企業と電解質メーカーの合弁事業とパートナーシップ(1)

5.3.15.主なRFB開発会社と電解質メーカーの合弁事業とパートナーシップ(2)

5.3.16.出光興産 - オーストラリアでの採掘事業とバナジウム電解液生産を支援、米国への拡張計画

5.3.17.R&D Investment Center / Adamant CTC - バナジウム生産(V2O5)とFeV採掘

5.3.18.Storion Energy - 米国での生産を目指すバナジウム電解液メーカーと電解液リースモデル

5.3.19.Storion Energy - VRFBの初期コストに対する電解液リースとセルスタックの影響

5.4.非バナジウムRFBのプレーヤー、技術、プロジェクト(有機、Fe-Cr、Zn-Mn、H-Mn、全鉄、塩水)

5.4.1.レドックス・ワン/タリサ - 鉄クロムRFB開発(1)

5.4.2.レドックス・ワン/タリサ - 鉄-クロムRFB開発(2)

5.4.3.レドックス・ワン/タリサ - 鉄-クロムRFB開発(3)

5.4.4.亜鉛マンガンRFBの性能とコスト

5.4.5.Zn-Mn RFBの安定性を促進する電極

5.4.6.亜鉛-臭素系RFBの性能向上

5.4.7.水素-マンガンRFBの性能と安定性(1)

5.4.8.水素マンガンRFBの性能と安定性(2)

5.4.9.RFC Power - H-Mn RFB技術の開発とプロジェクト

5.4.10.ESS社の概要と全鉄RFB技術

5.4.11.ESS社の全鉄RFB技術の最新情報

5.4.12.ESS社 主要市場の最新情報と考察

5.4.13.TNO / ESS社 - スキポール空港における全鉄RFBプロジェクト

5.4.14.アクアバッテリー - 塩水フロー電池の開発(1)

5.4.15.アクアバッテリー - 塩水フローバッテリーの開発(2)

5.4.16.アクアバッテリー - 塩水フロー電池の開発(3)

5.4.17.キノエナジー - 有機RFB開発概要

5.4.18.Quino Energy - 有機RFBアノライトの開発と合成

5.4.19.キノエナジー-有機RFBプロジェクトと応用(1)

5.4.20.キノエナジー-有機RFBプロジェクトと応用(2)

5.4.21.キノエナジー-有機RFBのコストと実績

5.4.22.Iberian Center for Research in Energy Storage - ORFB 性能向上のための電極親水性向上

5.4.23.Jolt Energy - ピリジニウムを用いた ORFB 技術の開発

5.4.24.ジョルト・エナジー - 非水系有機RFB開発における機械学習AIの利用

5.4.25.Rivus Batteries - 有機RFB開発企業

5.5.レドックスフロー電池市場 2021年第3四半期ー2023年第2四半期の更新スケジュール

5.5.1.2021年第3四半期ー2022年第4四半期のタイムライン

5.5.2.2023年第1四半期ー2023年第2四半期のタイムライン

5.5.3.2021年9月ー2022年2月

5.5.4.2022年2月ー2022年7月

5.5.5.2022年8月ー2022年11月

5.5.6.2022年11月ー2023年2月

5.5.7.2023年2月ー2023年3月

5.5.8.2023年4月ー2023年6月

6.レドックスフロー電池の予測 2020-2036年

6.1.エグゼクティブサマリー - レドックスフロー電池予測 2020-2036年

6.2.2020~2036年レドックスフロー電池予測の前提条件、方法論、主な変更点 (1)

6.3.2020~2036年レドックスフロー電池予測の前提条件、方法論、主な変更点(2)

6.4.レドックスフロー電池の地域別予測(GWh) 2020-2036年

6.5.レドックスフロー電池の地域別予測データ表(MWh) 2020-2036年

6.6.レドックスフロー電池の化学別予測(GWh)2020-2036年

6.7.レドックスフロー電池の化学別予測データ表(MWh)2020-2036年

6.8.レドックスフロー電池の化学別市場シェア予測と分析

6.9.レドックスフロー電池の金額別予測(US$B)2020-2036年

6.10.レドックスフロー電池の金額別予測データ表(US$B)2020-2036年

7.企業プロファイル

7.1.アゴラ・エナジー・テクノロジーズ

7.2.アクアバッテリー

7.3.AvCarb

7.4.バイオゼン・バッテリー

7.5.セルキューブ(2025年)

7.6.セルキューブ(2023年)

7.7.CMBlu Energy (2024年)

7.8.CMBlu Energy (2023年)

7.9.エレストール (2023年)

7.10.エレストール (2023年)

7.11.ESS社(2024年)

7.12.ESS社(2023年)

7.13.フレックスベース

7.14.フローナノ

7.15.フマテック

7.16.グリーンエネルギーストレージ(GES)

7.17.H2社(2025年)

7.18.H2社(2023年)

7.19.ハイプルーフ・テック

7.20.出光興産(バナジウム電解質)

7.21.インビニティ・エナジー・システムズ (2025年)

7.22.インビニティ・エナジー・システムズ (2024年)

7.23.インビニティ・エナジー・システムズ (2023年)

7.24.イオノマー・イノベーションズ

7.25.ジョルト・エナジー

7.26.ケミワット

7.27.コリッド・エナジー/エーブス

7.28.ラルゴ

7.29.ピンフロー

7.30.キノエナジー(2025年)

7.31.キノ・エナジー(2023年)

7.32.RFCパワー(2025年)

7.33.RFCパワー(2023年)

7.34.リバスバッテリー

7.35.栄科電力(2025年)

7.36.栄科電力(2023年)

7.37.シュマルツ

7.38.ストレン・テクノロジーズ

7.39.ストリオンエナジー

7.40.住友電気工業(2025年)

7.41.住友電気工業(2023年)

7.42.VFlowTech

7.43.VRBエナジー

7.44.ワットジュール

7.45.WeView (& ViZn Energy)

SummaryGlobal redox flow battery (RFB) market analysis including key players, technology benchmarking, material & component innovation, electrolyte production, policies, applications, long duration energy storage (LDES), data centers, & 10-year market forecasts. IDTechEx forecasts that the redox flow battery (RFB) market is forecast to reach US$9.2B in value by 2036. The growing penetration of variable renewable energy (VRE) in electricity grids will create longer periods where supply from these intermittent sources is not occurring. This will create demand for long duration energy storage (LDES) technologies which can dispatch energy over these longer, 6+ hour, timeframes economically. While Li-ion battery energy storage system (BESS) costs continue to decrease, these technologies cannot decouple their energy capacity and power output. RFBs are capable of this by independently scaling electrolyte volumes for energy capacity and cell stacks for power output. In theory, they can achieve lower Capex (on a US$/kWh basis) than li-ion BESS at longer durations of storage. This, coupled with non-vanadium chemistries such as organic or iron-based RFBs using abundant materials, or electrolytes which are cheaper to synthesize, suggests promise for lower-cost RFB technologies in the long-term.

Redox flow battery energy and power decoupling. Source: IDTechEx.

Outside of the future demand for LDES technologies, and amid the artificial intelligence (AI) boom, RFBs could also be used to support data centers. IDTechEx has observed several key RFB-data center projects being developed in Europe and the US. RFBs can support data center decarbonization by replacing the need for diesel generators to provide uninterruptible power supply (UPS) over sustained periods, to manage volatile compute loads, and to peak shave electricity from the grid. The use of non-flammable electrolyte in RFBs and increasing scrutiny of Li-ion battery storage safety amid recent large-scale fires provides a key value proposition for RFB developers. Other key advantages such as electrolyte recyclability and a lower levelized cost of storage (LCOS) at longer durations of storage will be leveraged by RFB developers in the medium-term. These factors are but some which will drive the RFB market to grow at a CAGR of 27% for the 2026-2036 period.

Over the past few years, the RFB market has seen significant growth compared to pre-2023, with key player Rongke Power being responsible for several multi-100-MWh flow battery projects, and even a GWh-scale project. Other key players such as Sumitomo Electric Industries, Invinity Energy Systems, and CellCube, have continued to steadily deploy volumes of vanadium flow batteries also, while scaling their businesses and forming supply chain partnerships. Funding across the market is also significant, with IDTechEx identifying over US$1B raised cumulatively by RFB players. This is a significant volume for any energy storage technology competing against the incumbent li-ion BESS.

Recently installed redox flow battery projects. Source: IDTechEx.

Policies and Programs to Drive RFB Growth

While recent RFB growth has been significant, these volumes are still minor compared to those seen by li-ion BESS. This has been driven primarily by the high cost of vanadium RFB (VRFB) technologies. To support RFB and LDES growth, key policies and programs such as the One Big Beautiful Bill Act (OBBBA) in the US, the UK Cap & Floor Scheme, and key projects supported by the California Energy Commission (CEC) will also factor into the emergence of growing western RFB markets. The impact of these policies, programs, and projects are discussed in this IDTechEx report.

Redox Flow Battery Chemistries

VRFBs are the most widely deployed and understood RFB chemistry, thanks to its sufficient performance. Compared to Li-ion BESS, this performance is often worse (e.g., energy density), and at shorter durations of storage, cost is often higher. This is driven by the use expensive electrolyte which uses the critical mineral, vanadium. Therefore, demand for other non-vanadium RFB chemistries has increased in recent years. IDTechEx has observed an uptick in development, commercialization of, and key projects of organic and iron-based chemistries which could include all-iron, chromium, zinc, vanadium, and hydrogen. Other, niche RFB chemistries also see development, for example utilizing manganese, CO2, saltwater, or microemulsion formulations. The variety of redox couples that can be used is vast. However, for an RFB technology to be successful in an increasingly competitive global energy storage market, the use of abundant and low-cost materials in easy-to-access supply chains, coupled with strong performance across energy density, energy efficiency, power density, and system lifetime will be needed. This IDTechEx report benchmarks 10 redox flow battery chemistries across Capex, commercial status, and key performance metrics, assesses their advantages and disadvantages, and provides an outlook for RFB chemistry market share over the next 10 years.

Innovation in Components, Materials and Electrolytes

While the electrolyte is one of the main parts of flow batteries, these devices are complex systems, similar to fuel cells and electrolyzers in their structure. The overall performance is dictated by its constituent components including the electrolyte, cell stack, and balance of plant. IDTechEx has observed innovations in cell stack materials and components to improve the power density of the stack, with focus on the electrodes and bipolar plates (BPP). Indeed, improving the performance of RFB components will be needed to improve overall RFB outlook in the energy storage market. The expansion of vanadium electrolyte manufacturing capacity has also been observed, with the emergence of supply chain partnerships and leasing occurring between electrolyte manufacturers and RFB developers in key regions. This IDTechEx report provides analysis on vanadium supply, key electrolyte market updates, cell stack component innovation, key component suppliers, and future material trends in the cell stack including key commentary on PFAS-based membranes and alternatives.

Exploded redox flow battery cell stack and components. Source: IDTechEx.

Forecasts

This IDTechEx report provides 10-year market forecasts on the redox flow battery market for the 2020-2036 period, by region (GWh), chemistry (GWh) and value by chemistry (US$B). Regions include China, Europe, United States, Japan, Rest of Asia, and Rest of the World. Chemistry forecasts include vanadium (VRFB), organic, all-iron, iron-vanadium (Fe-V), iron-chromium (Fe-Cr), iron-zinc (Fe-Zn), iron-hydrogen (Fe-H), and "other".

Company Profiles

This IDTechEx report includes 45 company profiles, including redox flow battery players, cell stack component and material suppliers, and electrolyte manufacturers and suppliers.

Key Aspects

This report provides the following information

Table of Contents1. EXECUTIVE SUMMARY

1.1. Global redox flow battery market headlines and key commentary

1.2. Key drivers and opportunities for redox flow batteries and adjacent markets

1.3. Key challenges for redox flow batteries and adjacent markets

1.4. Energy storage technology classification

1.5. RFBs - decoupling energy and power (1)

1.6. RFBs - decoupling energy and power (2)

1.7. What is long duration energy storage?

1.8. RFBs - decoupling energy and power for LDES and comparison to Li-ion BESS

1.9. Market timing for LDES technologies: Global average electricity generation mix from VRE

1.10. Redox flow battery applications and timeline overview

1.11. LCOS of vanadium redox flow battery versus Li-ion battery (4h, 6h, 8h, 10h duration)

1.12. Redox flow batteries vs Li-ion battery energy storage systems - installation by GWh, market overview, and key advantages

1.13. UK 'Cap and Floor Scheme' overview and timeline

1.14. Redox flow battery technology and chemistry outlook

1.15. RFB technology benchmarking (Capex, electrolyte cost, commercial status, voltage, energy density, energy efficiency, electrolyte solubility, etc.)

1.16. RFB strengths, weaknesses and commercial status by chemistry

1.17. RFB component and material trends to reduce costs and improve performance

1.18. Overview of RFB stack components

1.19. RFB components material summary - incumbent and future materials

1.20. RFB cell stack materials map

1.21. IEM materials contribute significantly to overall RFB stack cost

1.22. Enabling reduced RFB cell costs with higher power densities

1.23. RFB materials & components supplier and player map

1.24. Overview of vanadium supply, production, V2O5 prices in 2025 and long-term trends

1.25. Redox flow battery market - key trends, player activity, partnerships, chemistries, funding, installations & applications

1.26. Redox flow battery deployments by region 2015 - 2025

1.27. Cumulative redox flow battery deployments and market share by player (MWh)

1.28. Cumulative redox flow batteries installed by chemistry (MWh)

1.29. RFB technology developer map by chemistry

1.30. RFB projects 2023-2025 by application - C&I vs grid-scale by MWh

1.31. RFB developer funding and investments received Q3 2023 - Q2 2025 (US$M) and cumulative funding

1.32. Key global identified RFB project installations 2023-2025

1.33. Key and identified future global RFB projects map

1.34. Global RFB and electrolyte production capacity by player and region map (MWh / annum, chemistry)

1.35. Global RFB production and electrolyte production expansions: Player and region map

1.36. RFB developer and electrolyte supply deals and joint ventures (JV) map

1.37. New alternative RFB chemistry manufacturer entrants and project developers in the global RFB market

1.38. Key RFB developer closures and restructures

1.39. Redox flow battery forecasts by region (GWh) 2020-2036

1.40. Redox flow battery forecasts by chemistry (GWh) 2020-2036

1.41. RFB chemistry market share forecast and analysis

1.42. Redox flow battery forecasts by value (US$B) 2020-2036

1.43. Access more with an IDTechEx subscription

2. APPLICATIONS, LONG DURATION ENERGY STORAGE, POLICY, PROGRAMS & LEVELIZED COST OF STORAGE

2.1. Summary

2.1.1. Redox flow battery applications and timeline overview

2.2. Applications and Revenue Streams

2.2.1. The three core BESS market segments

2.2.2. Applications and revenues overview

2.2.3. Business models and revenue streams overview

2.2.4. Revenue stream descriptions

2.2.5. FTM: Values provided by battery storage in ancillary services

2.2.6. FTM: Values provided by battery storage in utility services

2.2.7. BTM summary: Values provided by battery storage - customer side

2.2.8. Microgrids and remote locations

2.2.9. Established RFB application examples

2.2.10. Redox flow batteries for data centers - emerging application (1)

2.2.11. Redox flow batteries for data centers - emerging application (2)

2.2.12. Redox flow batteries for data centers - emerging application (3)

2.2.13. RFB for data center support - key project (1)

2.2.14. RFB for data center support - key project (2)

2.2.15. RFBs for residential applications?

2.3. Introduction to Long Duration Energy Storage

2.3.1. Energy storage technology classification

2.3.2. Advantages and disadvantages of energy storage technologies

2.3.3. What is long duration energy storage?

2.3.4. Introduction to variable renewable energy (VRE)

2.3.5. Global outlook of electricity generated by VRE

2.3.6. GW, GWh and duration of storage (hours) vs electricity generation % from VRE

2.3.7. Market timing for LDES technologies: Global average electricity generation mix from VRE

2.3.8. The earlier adopting regions of LDES

2.3.9. LDES revenue generation challenges and further research on Long Duration Energy Storage by IDTechEx

2.4. RFB & LDES Policies and Programs

2.4.1. Flow Batteries Europe - policymaking for flow batteries in Europe

2.4.2. DESNZ - LDES and energy storage support programs

2.4.3. DESNZ - UK 'Cap and Floor Scheme' timelines

2.4.4. The Faraday Institution - Views on demand for LDES and future UK market and programmes for ultra-low cost LDES technologies

2.4.5. California Energy Commission - development of BESS / LDES in California (1)

2.4.6. California Energy Commission - development of BESS / LDES in California (2)

2.4.7. OBBBA: FEOC restrictions, MACR thresholds and impact on 45X Production Credit eligibility

2.4.8. Section 48 Investment Tax Credit (ITC) after The OBBBA

2.4.9. Hungary's Ministry of Energy - views on Hungarian electricity and ESS market, and tender for energy storage

2.4.10. Austria's Department for Renewable Energy Generation - new Acts to promote BESS, RFB, and LDES growth

2.5. Perspectives on RFB Business & Project Development

2.5.1. CellCube - views on Austrian market for LDES and RFBs

2.5.2. CellCube - emerging RFB markets, tenders, and key applications

2.5.3. EDP - energy operator and investor's perspective on RFBs and key pilot projects

2.5.4. Verbund - energy utility's involvement in RFB project development and views on electricity markets

2.5.5. R.Flo - RFBs to rebuild Ukraine's energy grid, business cases and electricity markets in Ukraine

2.5.6. Vanevo - RFB component supplier's views on business cases for RFBs, LCOE, and 24/7 clean PPAs

2.5.7. Invinity Energy Systems - importance of stakeholder collaboration in RFB project development

2.6. RFB LCOS Calculations

2.6.1. LCOS of vanadium redox flow battery versus Li-ion battery (4h, 6h, 8h, 10h duration)

2.6.2. LCOS Calculation: Formula and assumptions (1)

2.6.3. LCOS Calculation: Formula and assumptions (2)

2.6.4. LCOS Calculation: Formula and assumptions (3)

2.6.5. LCOS Calculation: Formula and assumptions (4)

2.6.6. LCOS Calculation: Considerations and limitations (1)

2.6.7. LCOS Calculation: Considerations and limitations (2)

2.6.8. VRFB levelized cost of storage conclusions (1)

2.6.9. VRFB levelized cost of storage conclusions (2)

3. REDOX FLOW BATTERY TECHNOLOGIES AND CHEMISTRIES

3.1. Summary: Redox Flow Battery Technologies and Chemistries

3.1.1. Executive summary - RFB technologies and chemistries

3.1.2. RFB technology benchmarking (Capex, electrolyte cost, commercial status, voltage, energy density, energy efficiency, electrolyte solubility, etc.)

3.1.3. RFB strengths, weaknesses and commercial status by chemistry

3.1.4. RFB technology developer map by chemistry

3.2. Introduction to Redox Flow Battery Technologies

3.2.1. Summary - RFB component and material trends to reduce costs and improve performance

3.2.2. Definitions - RFB electrochemistry

3.2.3. Definitions - efficiencies

3.2.4. RFBs - decoupling energy and power (1)

3.2.5. RFBs - decoupling energy and power (2)

3.2.6. RFBs - decoupling energy and power for LDES and comparison to Li-ion BESS (1)

3.2.7. RFBs - decoupling energy and power for LDES and comparison to Li-ion BESS (2)

3.2.8. RFBs - Fit-and-forget philosophy

3.2.9. Comparison of RFBs vs fuel cells

3.2.10. Choice of redox-active species and solvents (1)

3.2.11. Choice of redox-active species and solvents (2)

3.2.12. Redox flow battery classification (1)

3.2.13. Redox flow battery classification (2)

3.2.14. RFB historical timeline

3.3. Redox Flow Battery Chemistries

3.3.1. All vanadium RFB (VRFB)

3.3.2. VRFB strengths and weaknesses

3.3.3. All-iron RFB

3.3.4. All-iron RFB strengths and weaknesses

3.3.5. Zinc-iron (Zn-Fe) RFB

3.3.6. Alkaline Zn-Ferricyanide RFB

3.3.7. Zn-Fe RFB strengths and weaknesses

3.3.8. Iron-chromium (Fe-Cr) RFB

3.3.9. Fe-Cr RFB strengths and weaknesses

3.3.10. Iron-vanadium (Fe-V) RFB

3.3.11. Fe-V RFB strengths and weaknesses

3.3.12. Hydrogen-iron (H-Fe) RFB

3.3.13. H-Fe RFB strengths and weaknesses

3.3.14. Hydrogen-manganese (H-Mn) RFB

3.3.15. H-Mn strengths and weaknesses

3.3.16. Organic redox flow batteries (ORFB)

3.3.17. Classification of ORFBs

3.3.18. Active species for ORFBs

3.3.19. ORFBs strengths and weaknesses

3.3.20. Hydrogen-bromine (H-Br) RFB

3.3.21. H-Br RFB strengths and weaknesses

3.3.22. Zinc-bromine (Zn-Br) RFB

3.3.23. Zn-Br RFB strengths and weaknesses

3.3.24. Polysulfides-bromine (PSB) RFB

3.3.25. PSB historical timeline

3.3.26. PSB key weakness

3.3.27. Vanadium-bromine (V-Br) RFB

3.3.28. V-Br RFB strengths and weaknesses

3.3.29. Acid-base (salt water) 'flow battery'

4. MATERIALS AND COMPONENTS FOR REDOX FLOW BATTERY CELL STACKS

4.1. Materials and Components Summary

4.1.1. Summary - RFB component and material trends to reduce costs and improve performance

4.1.2. Introduction to the RFB system

4.1.3. Overview of RFB stack components

4.1.4. RFB components material summary - incumbent and future materials

4.1.5. RFB cell stack materials map

4.1.6. Key material choices for RFBs

4.1.7. IEM materials contribute significantly to overall RFB stack cost

4.1.8. Enabling reduced RFB cell costs with higher power densities

4.1.9. RFB materials & components supplier and player map

4.1.10. Further research on ion exchange membranes (IEMs), electrodes, bipolar plates (BPP) and other components

4.1.11. Membranes for Redox Flow Batteries

4.1.12. Ion exchange membranes for RFBs summary

4.1.13. Ion exchange membranes in redox flow batteries: Introduction

4.1.14. Ion exchange membranes in redox flow batteries: Overview

4.1.15. RFB cell stack materials map

4.1.16. Choice of separator - ion exchange membranes (IEMs) vs porous separators

4.1.17. Perfluorinated and hydrocarbon ion exchange membranes

4.1.18. Overview of redox flow battery chemistries and IEM requirements

4.1.19. Impact of potential ban on PFAS materials on RFB market

4.1.20. Key membrane manufacturers, by membrane material

4.1.21. Comparison of PFSA membrane supplier and membrane properties

4.1.22. Commercial hydrocarbon AEM material examples (I)

4.1.23. Commercial hydrocarbon AEM material examples (II)

4.1.24. Syensqo - Hydrocarbon-based ionomer for redox flow battery membranes and costs of hydrocarbon membranes

4.1.25. Syensqo - Hydrocarbon membrane performance for redox flow batteries

4.1.26. IEM material innovation areas in RFBs (I)

4.1.27. IEM material innovation areas in RFBs (II)

4.1.28. IEM material innovation areas in RFBs (III)

4.1.29. Innovation areas for reinforced multilayer IEMs

4.2. Electrodes for Redox Flow Batteries

4.2.1. Overview of electrodes for RFBs - function & characteristics

4.2.2. Overview of electrodes for RFBs - substrate materials & catalysts

4.2.3. Common electrode catalysts for different RFB chemistries

4.2.4. Flow-nano - nanostructured electrode development and process for redox flow batteries

4.2.5. Flow-nano - nanostructured electrode performance for RFBs

4.2.6. Flow-nano - scale-up of RFB electrode manufacturing process and continued carbon nano-onion development

4.2.7. Flow-nano - nanostructured electrode cost benefit for redox flow batteries

4.2.8. Advanced Carbon Materials - recycled activated carbon and graphite felt electrodes for RFBs

4.3. Bipolar Plates for Redox Flow Batteries

4.3.1. Overview of bipolar plates in RFBs - functions & materials

4.3.2. Overview of bipolar plates in RFBs - materials & manufacturing

4.3.3. Bipolar plate flow fields

4.3.4. Comparison of flow fields

4.3.5. Key manufacturers for RFB bipolar plates

4.3.6. Schmalz - Improved flow frame design to minimizing pressure loss and shunt currents in RFBs

4.3.7. Future directions for bipolar plate flow fields

4.4. Gaskets, Seals & Cell Frames for Redox Flow Batteries

4.4.1. Gaskets for RFBs

4.4.2. RFB gasket functions & requirements

4.4.3. Gasket design considerations

4.4.4. Gasket material selection (1/2)

4.4.5. Gasket material selection (2/2)

4.4.6. Gasket and sealant suppliers for redox flow batteries

4.4.7. WEVO-CHEMIE - RFB gaskets, sealants and adhesives (1)

4.4.8. WEVO-CHEMIE - RFB gaskets, sealants and adhesives (2)

4.4.9. WEVO-CHEMIE's gasket manufacturing considerations, advantages and supply for RFB applications

4.4.10. O-ring & injection molded gaskets

4.4.11. Cell frames

4.5. Other Components for Redox Flow Batteries

4.5.1. Current collector plates - overview and key materials

4.5.2. Current collector plates - innovations and key suppliers

4.5.3. End plates / insulation boards for RFBs

4.5.4. Syensqo - PPS endplates

4.5.5. Pinflow - RFB component provider and support for RFB developers

4.5.6. BioZen Batteries - RedoxinoTM mini flow cell test system

5. REDOX FLOW BATTERY MARKET, VANADIUM ELECTROLYTE MARKET, AND KEY UPDATES

5.1. Redox Flow Battery Market Summary, Updates & Data Analysis

5.1.1. Redox flow battery market executive summary - key trends, player activity, partnerships, chemistries, funding, installations & applications

5.1.2. Redox flow battery deployments by region 2015-2025

5.1.3. Cumulative redox flow battery deployments and market share by player (MWh)

5.1.4. Cumulative redox flow batteries installed by chemistry (MWh)

5.1.5. RFB technology developer map by chemistry

5.1.6. RFB projects 2023-2025 by application - C&I vs grid-scale by MWh

5.1.7. RFB projects 2023-2025 by application - grid-scale project application analysis

5.1.8. RFB projects 2023-2025 by application - C&I project application analysis

5.1.9. RFB developer funding and investments received Q3 2023 - Q2 2025 (US$M)

5.1.10. Cumulative RFB developer funding (US$M)

5.1.11. Key global identified RFB project installations 2023-2025

5.1.12. Key and identified future global RFB projects map

5.1.13. Global RFB and electrolyte production capacity by player and region map (MWh / annum, chemistry)

5.1.14. Global RFB production and electrolyte production expansions: Player and region map

5.1.15. RFB developer and electrolyte supply deals and joint ventures (JV) map

5.1.16. Key RFB developer and electrolyte producer joint ventures and partnerships (1)

5.1.17. Key RFB developer and electrolyte producer joint ventures and partnerships (2)

5.1.18. New alternative RFB chemistry manufacturer entrants and project developers in the global RFB market

5.1.19. Key RFB developer closures and restructures

5.1.20. Historical RFB projects raw data table 2023-2025 [technology provider, partners, MW, MWh, duration of storage, chemistry, year deployed, country, region, application, C&I vs grid] (1)

5.1.21. Historical RFB projects raw data table 2023-2025 [technology provider, partners, MW, MWh, duration of storage, chemistry, year deployed, country, region, application, C&I vs grid] (2)

5.1.22. Historical RFB projects raw data table 2023-2025 [technology provider, partners, MW, MWh, duration of storage, chemistry, year deployed, country, region, application, C&I vs grid] (3)

5.1.23. Future RFB projects raw data table (2026-2027) [technology provider, partners, MW, MWh, duration of storage, chemistry, future year deployed, country, region, application, C&I vs grid]

5.1.24. Future RFB projects raw data table (2028-2029+) [technology provider, partners, MW, MWh, duration of storage, chemistry, future year deployed, country, region, application, C&I vs grid]

5.1.25. RFB production capacity and expansions: Raw data table [MWh / annum, location]

5.1.26. Vanadium electrolyte production capacity and expansions raw data table [player, MWh / annum, location, RFB customer]

5.2. Key RFB Players, VRFB Technologies, and Project Updates 2023-2025

5.2.1. Rongke Power - Updates from globally leading RFB player

5.2.2. Saudi Aramco - Fe-V RFB development and scale-up in Saudi Arabia and key partnership with Rongke Power (1)

5.2.3. Rongke Power Key VRFB Projects

5.2.4. Saudi Aramco - Fe-V RFB development and scale-up in Saudi Arabia and key partnership with Rongke Power (2)

5.2.5. Sumitomo Electric - VRFBs and global activity

5.2.6. Sumitomo Electric - configuration, energy density, technology CapEx, and vanadium markets

5.2.7. Invinity Energy Systems - key market updates and discussion

5.2.8. Invinity Energy Systems overview and design for changing duration of storage

5.2.9. Invinity Energy Systems - Endurium VRFB technology (1)

5.2.10. Invinity Energy Systems - Endurium VRFB technology (2)

5.2.11. Invinity Energy Systems - tolerance of metal impurities in electrolyte, electrolyte additives, and cost

5.2.12. CellCube - VRFB technology development and insights from site visit

5.2.13. CellCube - Insights from site visit, manufacturing process, quality control, and cell stack evolution

5.2.14. CellCube - strategies to manage vanadium electrolyte imbalance and changes in oxidation state (1)

5.2.15. CellCube - strategies to manage vanadium electrolyte imbalance and changes in oxidation state (2)

5.2.16. CellCube - strategies to manage vanadium electrolyte imbalance and changes in oxidation state (3)

5.2.17. Idemitsu Kosan - VRFB project development in Australia with Sumitomo Electric and views on lack of LDES value proposition in Australia

5.2.18. FlexBase - development of RFB project for data center application (1)

5.2.19. RFB for data center support - key project (2)

5.2.20. H2, Inc. - key VRFB project in Spain, system architecture, and lessons learned with component transportation logistics

5.2.21. H2, Inc. - Latest VRFB technology and performance metrics

5.2.22. VFlowTech - VRFB demonstration project in Singapore

5.2.23. Fraunhofer ICT - Development of VRFB in project SMHYLES

5.3. Vanadium Electrolyte Market & Updates

5.3.1. Executive summary - overview of vanadium supply, production, V2O5 prices in 2025 and long-term trends

5.3.2. Global vanadium production by region and technique

5.3.3. Vanadium price trend and spikes in demand pre-2022

5.3.4. Raw materials for RFB electrolytes

5.3.5. Vanadium overview

5.3.6. Vanadium mining and products (1)

5.3.7. Vanadium mining and products (2)

5.3.8. Vanadium ore processing

5.3.9. Vanadium junior miners and projects

5.3.10. Vanadium electrolyte recycling

5.3.11. Vanadium electrolyte leasing

5.3.12. Electrolyte leakage mitigation

5.3.13. RFB developer and electrolyte supply deals and joint ventures (JV) map

5.3.14. Key RFB developer and electrolyte producer joint ventures and partnerships (1)

5.3.15. Key RFB developer and electrolyte producer joint ventures and partnerships (2)

5.3.16. Idemitsu Kosan - supporting mining operations and vanadium electrolyte production in Australia and expansion plans to the US

5.3.17. R&D Investment Center / Adamant CTC - vanadium production (V2O5) and FeV mining

5.3.18. Storion Energy - vanadium electrolyte manufacturer targeting US production and electrolyte leasing model

5.3.19. Storion Energy - impacts of electrolyte leasing and cell stacks on upfront VRFB costs

5.4. Non-Vanadium RFB Players, Technologies and Projects (organic, Fe-Cr, Zn-Mn, H-Mn, all-iron, saltwater)

5.4.1. Redox One / Tharisa - iron-chromium RFB development (1)

5.4.2. Redox One / Tharisa - iron-chromium RFB development (2)

5.4.3. Redox One / Tharisa - iron-chromium RFB development (3)

5.4.4. Zinc-Manganese RFB performance and cost

5.4.5. Electrodes to promote stability in Zn-Mn RFBs

5.4.6. Improving performance of Zinc-Bromine RFBs

5.4.7. Performance and stability of Hydrogen-Manganese RFB (1)

5.4.8. Performance and stability of Hydrogen-Manganese RFB (2)

5.4.9. RFC Power - development of H-Mn RFB technology and projects

5.4.10. ESS Inc. overview and all-iron RFB technology

5.4.11. ESS Inc. all-iron RFB technology updates

5.4.12. ESS Inc. key market updates and discussion

5.4.13. TNO / ESS Inc. - All-iron RFB project at Schiphol Airport

5.4.14. AquaBattery - development of saltwater flow battery (1)

5.4.15. AquaBattery - development of saltwater flow battery (2)

5.4.16. AquaBattery - development of saltwater flow battery (3)

5.4.17. Quino Energy - organic RFB development overview

5.4.18. Quino Energy - organic RFB anolyte development and synthesis

5.4.19. Quino Energy - organic RFB projects and applications (1)

5.4.20. Quino Energy - organic RFB projects and applications (2)

5.4.21. Quino Energy - organic RFB costs and performance

5.4.22. Iberian Center for Research in Energy Storage - improving electrode hydrophilicity for improved ORFB performance

5.4.23. Jolt Energy - development of ORFB technology with pyridinium

5.4.24. Jolt Energy - use of machine learning AI in non-aqueous organic RFB development

5.4.25. Rivus Batteries - organic RFB developer

5.5. Redox Flow Battery Market Q3 2021 - Q2 2023 updates timeline

5.5.1. Q3 2021 - Q4 2022 timeline

5.5.2. Q1 2023 - Q2 2023 timeline

5.5.3. September 2021 - February 2022

5.5.4. February 2022 - July 2022

5.5.5. August 2022 - November 2022

5.5.6. November 2022 - February 2023

5.5.7. February 2023 - March 2023

5.5.8. April 2023 - June 2023

6. REDOX FLOW BATTERY FORECASTS 2020-2036

6.1. Executive summary - redox flow battery forecasts 2020-2036

6.2. Assumptions, methodology & key changes for redox flow battery forecasts 2020-2036 (1)

6.3. Assumptions, methodology & key changes for redox flow battery forecasts 2020-2036 (2)

6.4. Redox flow battery forecasts by region (GWh) 2020-2036

6.5. Redox flow battery forecasts by region data table (MWh) 2020-2036

6.6. Redox flow battery forecasts by chemistry (GWh) 2020-2036

6.7. Redox flow battery forecasts by chemistry data table (MWh) 2020-2036

6.8. RFB chemistry market share forecast and analysis

6.9. Redox flow battery forecasts by value (US$B) 2020-2036

6.10. Redox flow battery forecasts by value data table (US$B) 2020-2036

7. COMPANY PROFILES

7.1. Agora Energy Technologies

7.2. AquaBattery

7.3. AvCarb

7.4. BioZen Batteries

7.5. CellCube (2025)

7.6. CellCube (2023)

7.7. CMBlu Energy (2024)

7.8. CMBlu Energy (2023)

7.9. Elestor (2023)

7.10. Elestor (2023)

7.11. ESS Inc. (2024)

7.12. ESS Inc. (2023)

7.13. FlexBase

7.14. Flow-nano

7.15. Fumatech

7.16. Green Energy Storage (GES)

7.17. H2, Inc. (2025)

7.18. H2, Inc. (2023)

7.19. Hyproof Tech.

7.20. Idemitsu Kosan (Vanadium Electrolyte)

7.21. Invinity Energy Systems (2025)

7.22. Invinity Energy Systems (2024)

7.23. Invinity Energy Systems (2023)

7.24. Ionomr Innovations

7.25. Jolt Energy

7.26. Kemiwatt

7.27. Korid Energy/AVESS

7.28. Largo

7.29. Pinflow

7.30. Quino Energy (2025)

7.31. Quino Energy (2023)

7.32. RFC Power (2025)

7.33. RFC Power (2023)

7.34. Rivus Batteries

7.35. Rongke Power (2025)

7.36. Rongke Power (2023)

7.37. Schmalz

7.38. Storen Technologies

7.39. Storion Energy

7.40. Sumitomo Electric Industries (2025)

7.41. Sumitomo Electric Industries (2023)

7.42. VFlowTech

7.43. VRB Energy

7.44. WattJoule

7.45. WeView (& ViZn Energy)

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|