二酸化炭素除去(CDR)2025-2035年:技術、プレーヤー、炭素クレジット市場、予測Carbon Dioxide Removal (CDR) 2025-2035: Technologies, Players, Carbon Credit Markets, and Forecasts DACCS(直接大気炭素回収・貯留)、BECCS、バイオ炭、植林・植林、無機化、海洋ベースCDRを含む二酸化炭素除去技術、動向、予測、炭素クレジット市場 2024年、自主的な炭素クレジット市場にお... もっと見る

サマリー

DACCS(直接大気炭素回収・貯留)、BECCS、バイオ炭、植林・植林、無機化、海洋ベースCDRを含む二酸化炭素除去技術、動向、予測、炭素クレジット市場

2024年、自主的な炭素クレジット市場における耐久性のある人工的な二酸化炭素除去(CDR)クレジットの事前購入は、過去最高を記録した。こうした高品質のクレジットに対する企業の需要は供給を上回り続けており、新たな二酸化炭素除去技術のスケールアップを後押ししている。パリ協定6.4条のメカニズムなど、自主的炭素市場とコンプライアンス炭素市場の重複が進む中、CDR技術のビジネスケースは確固たるものとなりつつある。

「二酸化炭素除去(CDR)2025-2035:技術、プレーヤー、炭素クレジット市場、予測」は、新興のCDR産業と炭素クレジット市場の包括的な展望を提供し、この市場を形成している技術的、経済的、規制的、環境的側面の詳細な分析を行っている。この中でIDTechExは、大気からCO₂ を積極的に除去し、炭素吸収源に隔離する技術に焦点を当てている:

1.直接大気炭素回収・貯留(DACCS)は、化学プロセスを活用して大気からCO₂ を直接回収し、地層や耐久性のある製品に貯留する。

2.炭素除去・貯留を伴うバイオマス(BiCRS):バイオマスを利用して大気からCO2を除去し、地下または長寿命製品に貯留する戦略。これには、BECCS(炭素回収・貯留を伴うバイオエネルギー)、バイオ炭、バイオマス埋設、バイオオイル地下注入などのアプローチが含まれる。

3.土壌、森林、その他の陸上生態系における炭素貯留量を増加させるために生物学的プロセスを活用する陸上CDR手法、すなわち植林や再植林、土壌炭素貯留技術

4.岩石風化の促進、鉱物廃棄物の炭酸化、酸化物のループ化を通じて、大気中のCO₂を岩石と永久的に結合させる天然鉱物プロセスを強化する鉱化CDR技術

5.海洋アルカリ性強化、海洋直接捕獲、人工湧昇/湧昇、沿岸ブルーカーボン、藻類養殖/海藻沈降、海洋受精などを通じて、海洋の炭素ポンプを強化する海洋ベースのCDR手法

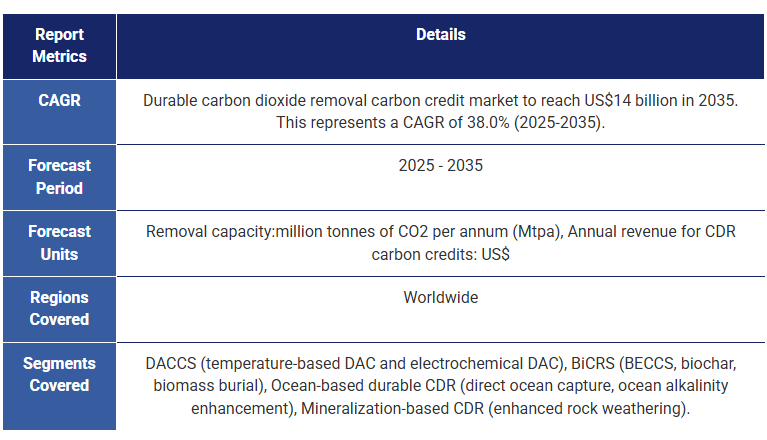

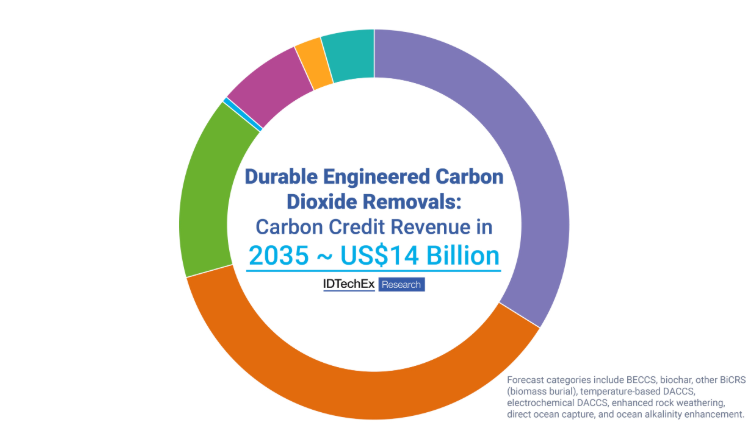

これらのCDR技術は、幅広い技術準備レベルにある。DACCSやBECCSなど、大規模展開の可能性を秘めた耐久性のある工学的CDR技術は、現在、補助金や税額控除(米国の45Q税額控除など)を通じて政府の支援を受けているほか、企業がスコープ3のCO2排出量に対処しようとしているため、自主的な炭素クレジット市場からも収益を得ている。IDTechExの予測によると、これらの技術は2035年に炭素クレジット収入に最も貢献すると予想されている。

2025年、DACCSがメガトン規模に到達

2024年、DACのパイオニアであるクライムワークスが、年間4万トンのCO2を大気中から除去する世界最大の直接空気回収施設を稼働させた。2025年に1PointFiveのストラトス施設が完成すれば、DACCSはメガトン規模に飛躍することになる。大規模施設によるコスト削減が進む一方で、DACCSの分野では現在100社を超える企業が活動しており、捕捉コストを下げるためのさらなる改良を模索している。さまざまな吸着剤、再生方法、装置設計が追求される中、DACCSは公共部門と民間部門から多額の資金を獲得し続けている。本報告書では、経済性とエネルギー需要を考慮し、どのような直接空気回収技術が最も成功しそうかを検討する。

加速する電気化学的二酸化炭素除去法

耐久性に優れ、工学的に設計されたあらゆる形態の二酸化炭素除去技術は、現在、高品質の炭素クレジットの需要が供給を上回っているため、規模が拡大している。興味深い傾向のひとつは、電気化学的二酸化炭素除去技術の成長である。エネルギー需要は、しばしば回収コストの大きな要因となる。近年、いくつかの新興企業が、エネルギー効率の向上と、風力や太陽光のような断続的な再生可能エネルギー源とのより良い互換性を求めて、電気化学的二酸化炭素除去法の開発に着手している。電解と電気透析技術は、海洋での直接回収の分野ではトップランナーであり、同様のpHスイング電気化学的方法は、大気での直接回収への投資関心が高まっている。本レポートでは、電気化学的CDRの実態(経済性、製造とサプライチェーンの発展、技術的課題、主要プレーヤーなど)を分析している。

包括的な分析と市場予測

このIDTechExのレポートは、CDR炭素クレジット市場を詳細に評価し、さまざまな技術、最新の進歩、潜在的な採用促進要因と障壁を評価しています。また、8つのCDRカテゴリー(温度ベースDACCS、電気化学的DACCS、BECCS、バイオ炭、バイオマス埋設、海洋直接回収、海洋アルカリ性強化、強化岩石風化)の展開に関する2035年までの詳細な予測と、独自の分析およびインタビューに基づく企業プロファイルも掲載している。

主要な側面

本レポートは以下の情報を提供します:

技術と市場の分析

直接空気回収を含む、各種二酸化炭素除去ソリューションに関するデータと背景

CDR(二酸化炭素除去)排出権市場における課題と機会の分析

電気化学的アプローチや装置設計のような新技術を含む、直接空気回収の技術革新の現状

CDR技術の詳細な概要:陸上ベース、鉱物化ベース、海洋ベース、DACCS(貯蔵を伴う直接空 気炭素回収)BiCRS(炭素回収・貯蔵を伴うバイオマス)

CDR カーボンオフセットの市場ポテンシャル(ボランタリー及びコンプライアンス)

CDR 技術を拡大するための主要戦略と経済性

CDRの市場導入に必要な要件(インフラ、エネルギー、サプライチェーン等)の評価

主なCDRソリューションの潜在的気候利益

技術成熟度(TRL)、コスト、規模の可能性などの要因に基づくベンチマーキング

CDR 市場に影響を与える主な規制と政策

プレーヤー分析とトレンド

CDR 関連主要企業からの一次情報

CDR関連企業の最新動向、発表されたプロジェクトの観察、資金調達、動向、パートナーシップの分析

市場予測と分析

耐久性のある設計された CDR ソリューションについて、8 つの技術分野に細分化した 2035 年までのきめ細かな市場予測

目次

1. 要旨

1.1. なぜ二酸化炭素除去(CDR)なのか?

1.2. 本レポートで取り上げるCDR技術 (1/2)

1.3. 本レポートで取り上げたCDR技術(2/2)

1.4. 二酸化炭素除去法の規模と技術準備レベル

1.5. CDRビジネスモデルとその課題 炭素クレジット

1.6. 二酸化炭素除去のサプライチェーン 炭素クレジット市場のプレーヤー

1.7. 炭素クレジット市場における耐久性CDRに対する買い手の選好の変化

1.8. 全体像: 2024年の自主的炭素クレジット市場

1.9. 2024年の耐久性のある炭素除去の価格は?

1.10. DACCS: まとめ

1.11. DACCSの現状

1.12. DACCSを支える税額控除の役割: 45QとITC

1.13. 直接空気回収を拡大するための主な課題は何か?

1.14. DACの技術状況: 企業

1.15. 最も成功するDAC技術は?

1.16. DAC技術はどのように発展していくのか?

1.17. 固体吸着剤-半連続運転はエネルギー強度を下げることができる

1.18. 電気化学的DAC:要点

1.19. BECCSを超えるBiCRSの可能性: ベンチマーキング

1.20. 既存のBECCSプロジェクトの大半はエタノール生産である

1.21. BECCSの主流は溶剤回収技術である

1.22. BECCSに対する政府の支援が加速している

1.23. BECCS: 主な要点

1.24. 世界のバイオ炭市場の現状

1.25. バイオ炭CDRの規模拡大

1.26. バイオ炭 主要なポイント

1.27. BiCRSのバリューチェーン

1.28. 植林と森林再生 主な要点

1.29. 要点 土壌の炭素貯留

1.30. 主要なポイント:鉱物化による二酸化炭素除去(CDR)

1.31. 海洋ベースのCDRにおける主要なプレイヤー

1.32. 主要なポイント:海洋ベースのCDR

1.33. 技術別二酸化炭素除去能力の予測(年間百万トンCO2)、2025-2035

1.34. 技術別二酸化炭素除去年間炭素クレジット収入予測(億米ドル)、2025-2035

1.35. 二酸化炭素除去市場予測、2025-2035:議論

1.36. 持続可能なCDR市場の進化

1.37. IDTechExサブスクリプションでさらに詳しく

2. 序論

2.1. 導入と一般分析

2.1.1. 二酸化炭素除去(CDR)とは何か?

2.1.2. 主なCDR手法の解説

2.1.3. なぜ二酸化炭素除去(CDR)なのか?

2.1.4. CDRとCCUSの違いとは?

2.1.5. 高品質な二酸化炭素除去:耐久性、永続性、追加性

2.1.6. 二酸化炭素除去手法の規模と技術成熟度レベル

2.1.7. 二酸化炭素除去技術のベンチマーク

2.1.8. CDR技術の現状と可能性

2.1.9. CDRのモニタリング、報告、検証

2.1.10. CDR:問題を先送りしているのか?

2.1.11. CDR分野のさらなる発展に必要なものは何か?

2.1.12. 2024年のCDR市場動向

2.1.13. Xprize Carbon Removal

2.1.14. 地域要因が最適なCDR戦略を決定する可能性

2.2. 炭素クレジット市場

2.2.1. グローバルな気候行動 - パリ協定

2.2.2. 炭素価格設定と炭素市場

2.2.3. 世界の炭素価格設定メカニズム

2.2.4. グローバルな炭素価格メカニズムにおけるCO2の価格は?

2.2.5. 炭素クレジットとは何か?

2.2.6. 炭素クレジットはどのように認証されるか?

2.2.7. 炭素登録機関のクレジット市場における役割

2.2.8. 炭素クレジットの測定、報告、検証(MRV)

2.2.9. 自発的炭素クレジットはどのように購入されるか?

2.2.10. 炭素除去炭素クレジット市場の参加者

2.2.11. 遵守市場と自発的市場との相互作用(地理的)

2.2.12. 遵守市場と自発的市場との相互作用(部門別)

2.2.13. 政府の炭素クレジットメカニズム

2.2.14. パリ協定第6条第4項:グローバルで統一された炭素クレジット市場

2.2.15. 炭素クレジットの品質

2.2.16. 炭素除去と炭素回避/削減クレジット

2.2.17. 二酸化炭素除去と排出削減

2.2.18. 二酸化炭素除去は$100億のコンプライアンス市場において非常に限定的な役割しか果たさない

2.2.19. 自発的炭素市場におけるCDRの現状

2.2.20. 炭素クレジット市場における持続可能なCDRに対する買い手の好みの変化

2.2.21. 2024年の自主的炭素クレジット市場の全体像

2.2.22. 持続可能なCDRにおける先進的な市場コミットメント

2.2.23. 企業は現在、二酸化炭素除去に投資すべきである

2.2.24. 持続可能な炭素除去の最大の買い手

2.2.25. 事前購入が持続可能なCDR分野を依然として支配している

2.2.26. CDRクレジットの価格

2.2.27. 2024年の持続可能な炭素除去はどれほど高価だったか?

2.2.28. 企業と技術別現在の炭素クレジット価格

2.2.29. 炭素市場規模

2.2.30. 持続可能なCDR技術に十分な買い手は存在するのか?

2.2.31. CDR技術:主要なポイント

3. 直接空気二酸化炭素回収・貯留(DACCS)

3.1. 直接空気回収(DAC)の概要

3.1.1. 直接空気回収(DAC)とは何か?

3.1.2. なぜDACCSがCDRソリューションとして選ばれるのか?

3.1.3. DACCSの現在の状況

3.1.4. DACCSプロジェクトのパイプライン:立地と技術

3.1.5. 動向:地域別のDACに対する政策支援

3.1.6. DACCS支援における税額控除の役割:45QとITC

3.1.7. 米国は20の大規模地域DACハブ設立を計画

3.1.8. 動向:DACへの民間投資

3.1.9. 2024年のDAC資金の調達先は?

3.1.10. DACの土地要件は優位性である

3.1.11. DACと点源二酸化炭素回収の比較

3.1.12. DACの電力要件

3.1.13. 名目容量と実際のネット除去量

3.1.14. クリーンエネルギーの調達困難さ

3.1.15. 運用柔軟性 - 間欠的な再生可能エネルギーでDACを駆動する

3.1.16. 直接空気捕集の拡大における主要な課題は何ですか?

3.2. 主要なDAC技術

3.2.1. DACにおけるCO2捕集/分離メカニズム

3.2.2. 直接空気捕集技術

3.2.3. 固体と液体のDACにおける再生方法

3.2.4. 固体と液体のDACにおける再生方法の比較

3.2.5. 主要なDAC企業

3.2.6. 直接空気捕集の分野:技術と立地別の分析

3.2.7. DAC用の固体吸着剤

3.2.8. Climeworks

3.2.9. S-DACのプロセスフロー図:Climeworks

3.2.10. 固体吸着剤 - 半連続運転はエネルギー強度を低減できる

3.2.11. Heirloom

3.2.12. CaOループングのプロセスフロー図:Heirloom

3.2.13. DAC用の液体溶剤

3.2.14. 液体溶剤ベースのDAC:Carbon Engineering

3.2.15. Carbon Engineering

3.2.16. Stratos:DACを半メガトン規模へ

3.2.17. L-DACのプロセスフロー図:Carbon Engineering

3.2.18. DACプロセス:クライムワークスとカーボン・エンジニアリング

3.2.19. 電力と熱源:クライムワークスとカーボン・エンジニアリング

3.2.20. 年間1メガトンCO2の捕集要件:クライムワークスとカーボン・エンジニアリング

3.2.21. DAC技術動向:企業

3.2.22. どのDAC技術が最も成功するでしょうか?

3.2.23. DAC技術はどのように発展するでしょうか?

3.2.24. DACCSの炭素クレジット販売(企業別)

3.3. エレクトロスイング/電気化学的DAC技術

3.3.1. エレクトロスイング/電気化学的DAC

3.3.2. 電気化学的DACのタイプ(1/2)

3.3.3. 電気化学的DACのタイプ(2/2)

3.3.4. 電気化学セル部品の望ましい特性

3.3.5. 電気化学DAC企業の動向

3.3.6. 電気化学DAC手法のベンチマーク

3.3.7. 電気化学DACの技術的課題

3.3.8. 電気化学DAC:低コストの断続的再生可能電力への柔軟性

3.3.9. 電気化学DACのコストは電力価格に強く依存する

3.3.10. 電気化学的DAC:主要なポイント

3.4. 新規DAC技術

3.4.1. 湿度変動型直接空気捕集(湿度変動)

3.4.2. 湿度変動型DAC用のイオン交換樹脂

3.4.3. 低温直接空気捕集企業

3.4.4. 膜式直接空気捕集

3.4.5. 反応型直接空気捕集 - 捕集と変換の組み合わせ

3.5. DAC用設備 - 設計と製造

3.5.1. DACの製造サプライチェーン

3.5.2. 空気接触器:既存の設計

3.5.3. 商業用空気接触器製造施設

3.5.4. カーボン・エンジニアリングからの教訓:既存の産業設備を適応させてサプライチェーンを確立

3.5.5. グローバル・サーモスタットからの教訓:技術開発にはパートナーシップが不可欠

3.5.6. 受動的空気接触

3.5.7. DACを既存の産業プロセスへの統合:冷却塔、HVAC、および廃熱

3.6. DACの経済性

3.6.1. DACの経済性

3.6.2. DACのCAPEX:サブシステムごとの貢献度

3.6.3. DACのOPEX

3.6.4. DACの全体的な捕集コスト(1/2)

3.6.5. DACの全体的な捕集コスト(2/2)

3.6.6. DACCSにおけるコンポーネントごとの捕集コストの貢献度

3.6.7. DACの資金調達

3.6.8. DACのビジネスモデル

3.6.9. 直接空気捕集の炭素クレジット販売価格

3.7. CO₂貯留

3.7.1. DACは二酸化炭素除去のため永久貯留と組み合わせて実施する必要がある

3.7.2. 超臨界CO₂の地下貯留

3.7.3. 地中CO₂捕集のメカニズム

3.7.4. CO₂漏洩は小さなリスクである

3.7.5. 地質的CO₂貯留の貯留タイプ:塩水含水層

3.7.6. 地質的CO₂貯留の貯留タイプ:枯渇した石油・ガス田

3.7.7. 非伝統的貯留資源:玄武岩と超マフィック岩

3.7.8. 世界のCO₂貯留容量の推定

3.7.9. 国別CO₂貯留ポテンシャル

3.7.10. CO₂貯留の許可と承認

3.7.11. クラスVI許可が米国におけるDACCS開発を遅らせている

3.7.12. DACの貯留事業者例

3.7.13. 主要なポイント:CO₂貯留

3.8. DACの課題

3.8.1. DAC技術に関連する課題

3.8.2. 石油・ガス業界のDACへの参画

3.8.3. DACCSと地熱エネルギーの共立地

3.8.4. DACは風力・太陽光産業のスケールアップから何を学べるか?

3.8.5. 2050年までにギガトン規模の容量を達成するためにDACに必要なものは何か?

3.8.6. DACCSのSWOT分析

3.8.7. DACCS:要約

4. バイオマスと炭素除去・貯蔵(BICRS)

4.1. 序論

4.1.1. バイオマスと炭素除去・貯蔵(BiCRS)

4.1.2. BiCRSの可能な原料

4.1.3. 現在のCDRで利用されているバイオマスの種類は?

4.1.4. BiCRSの潜在的な可能性はBECCSを超えている:ベンチマーク

4.1.5. BiCRSの変換経路

4.2. バイオエネルギーと二酸化炭素回収・貯留(BECCS)

4.2.1. バイオエネルギーと二酸化炭素回収・貯留(BECCS)

4.2.2. ポイントソース回収技術

4.2.3. 既存のBECCSプロジェクトのほとんどはエタノール生産に関連している

4.2.4. 溶剤回収技術がBECCS分野を支配している

4.2.5. アミン溶剤技術がBECCSを支配している

4.2.6. BECCSに対する政府支援が加速している

4.2.7. BECCSのビジネスモデル - Ørstedの事例

4.2.8. BECCSは耐久性のあるエンジニアードCDRクレジットの販売を支配している

4.2.9. 生物由来のCO2は二酸化炭素除去のため永久貯留と組み合わされる必要がある

4.2.10. BECCSプロジェクト - 動向と議論

4.2.11. イギリスのBECCS事例研究

4.2.12. エタノール生産がBECCSプロジェクトパイプラインを支配

4.2.13. BECCSのためのバイオエタノール工場接続ネットワーク

4.2.14. BECCSの機会:熱発電

4.2.15. BECCSの機会:廃棄物からエネルギー

4.2.16. BECCSの課題

4.2.17. BECCSのエネルギー効率と炭素効率

4.2.18. 生物起源の排出量における炭素会計における再生速度の重要性

4.2.19. BECCSは持続可能か?

4.2.20. BECCS:主要なポイント

4.3. バイオチャール

4.3.1. バイオチャールとは何か?

4.3.2. バイオチャールはどのように生産されるか?(1/2)

4.3.3. バイオチャールはどのように生産されるか?(2/2)

4.3.4. バイオチャールの原料

4.3.5. バイオチャールによる炭素除去の永続性

4.3.6. バイオチャールの応用

4.3.7. バイオチャール生産における経済的考慮事項(1)

4.3.8. バイオチャール生産における経済的考慮事項(2)

4.3.9. バイオチャール:市場とビジネスモデル

4.3.10. グローバルなバイオチャール市場の現状

4.3.11. 手工芸品と工業用バイオチャールの比較

4.3.12. バイオチャール炭素クレジットの売却価格

4.3.13. 規模別のバイオチャールCDR主要プレイヤー

4.3.14. バイオチャールビジネスモデル:設備供給業者とプロジェクト開発者

4.3.15. バイオチャールビジネスモデル:議論

4.3.16. バイオチャールに関する法規制と認証

4.3.17. バイオチャールによる二酸化炭素除去の追加性

4.3.18. バイオチャール:主要なポイント

4.4. その他のBiCRS(バイオオイルとバイオマス埋設)

4.4.1. CDRのためのバイオオイル地質貯蔵

4.4.2. CO2除去のためのバイオマス埋設

4.4.3. CO2トンあたり$100未満の捕集コストがバイオマス埋設の普及を後押し

4.4.4. バイオマス埋設の商業的動向

4.4.5. バイオマスの最適な活用法 - バイオチャール、BECCS、または埋設?

4.4.6. BiCRSバリューチェーン

5. 植林/再植林

5.1. 自然に基づく二酸化炭素除去(CDR)アプローチとは何か?

5.2. なぜ土地ベースの二酸化炭素除去なのか?

5.3. 植林と再植林のCDRポテンシャル

5.4. 気候変動緩和における植林/再植林の賛否

5.5. 植林/再植林における技術:リモートセンシング

5.6. 企業動向:植林/再植林におけるロボティクス

5.7. 2024年の植林/再植林炭素クレジット市場状況

5.8. 植林/再植林は既に多くの政府のネットゼロ目標の一部となっている

5.9. 「もっと木を植えるだけ!」-持続可能性とグリーンウォッシングの考慮点

5.10. A/RとBECCSソリューションの比較

5.11. 植林と再植林:主要なポイント

6. 土壌炭素固定

6.1. 土壌炭素固定(SCS)とは何か?

6.2. 土壌炭素固定の潜在力は巨大である

6.3. 土壌炭素固定を改善するための農業管理手法

6.4. 土壌炭素固定のために微生物接種を利用する企業

6.5. 土壌炭素固定のMRVアプローチ

6.6. 土壌炭素の追加性、測定、永続性は疑問視されている

6.7. SCS展開の課題

6.8. 土壌炭素固定のバリューチェーン

6.9. 2024年の土壌炭素固定市場動向

6.10. 2024年の土壌炭素固定炭素クレジット市場状況

6.11. 土壌炭素固定化のメリットとデメリット

6.12. 主要なポイント:土壌炭素固定化

7. BASED CDR

7.1. CO2の鉱物化はCDRの鍵となる

7.2. 外部鉱物化CDR手法

7.3. 外部鉱物化用の原料

7.4. 鉱物廃棄物の外部炭酸化

7.5. CO2由来コンクリートにおける二酸化炭素貯留

7.6. CO2由来コンクリート:商業的動向

7.7. オキシループ:DACにおける鉱物化

7.8. 強化風化

7.9. 強化岩石風化の概要

7.10. 強化岩石風化におけるMRV

7.11. 強化風化の商業的動向

7.12. 強化岩石風化CDR市場

7.13. 強化された岩石風化の現状:スタートアップ企業

7.14. 主要なポイント:鉱物化CDR

8. 海洋ベースの二酸化炭素除去

8.1. 概要

8.1.1. 海洋ポンプは継続的に大気から二酸化炭素を海洋に引き込む

8.1.2. 海洋ベースのCDR手法

8.1.3. 海洋ベースのCDR技術の定義

8.1.4. なぜ海洋ベースのCDRか?

8.1.5. 海洋ベースのCDRの規模と技術成熟度レベル

8.1.6. 海洋ベースのCDR手法のベンチマーク

8.1.7. 海洋ベースのCDRの主要プレイヤー

8.2. 海洋ベースのCDR:非生物的メソッド

8.2.1. 海洋アルカリ度向上(OAE)

8.2.2. 電気化学的海洋アルカリ度向上

8.2.3. 海洋アルカリ度向上の現状:スタートアップ企業

8.2.4. 直接海洋捕集

8.2.5. 直接海洋捕集の現状:スタートアップ企業

8.2.6. 電気化学的直接海洋捕集

8.2.7. 直接海洋捕集のための電気分解:塩素生成の回避

8.2.8. その他の直接海洋捕集技術

8.2.9. 直接海洋捕集の障壁は依然として存在する

8.2.10. 人工的下降流

8.3. 海洋ベースのCDR:生物学的メソッド

8.3.1. 自発的炭素市場における沿岸ブルーカーボンクレジットの現状

8.3.2. 海藻の培養 - 海藻の沈降

8.3.3. 海洋肥沃化

8.3.4. 複数の海洋肥沃化スタートアップが失敗した

8.3.5. 2025年に海洋肥沃化が再興するだろうか?

8.3.6. 人工的な上昇流

8.3.7. 海洋CDRの大規模展開におけるガバナンス課題

8.3.8. 海洋CDRのMRV

8.3.9. 海洋ベースのCDRクレジットの価格

8.3.10. 主要なポイント:海洋ベースのCDR

9. CDR市場予測

9.1. 予測範囲:耐久性のあるエンジニアリングによる除去

9.2. 予測範囲:自然に基づくアプローチ

9.3. 総二酸化炭素除去予測の方法論/範囲

9.4. 技術別二酸化炭素除去容量予測(年間百万トンCO2)、2025-2035

9.5. 技術別二酸化炭素除去容量予測データ表(年間百万トンCO2)、2025-2035

9.6. 技術別二酸化炭素除去カーボンクレジット年間収益予測(億米ドル)、2025-2035

9.7. 技術別二酸化炭素除去カーボンクレジット年間収益予測データ表(百万米ドル)、2025-2035

9.8. 二酸化炭素除去市場予測(2025-2035年):議論

9.9. 持続可能なCDR市場の進化

9.10. 前回のIDTechEx CDR予測からの変更点

9.11. DACCSによる二酸化炭素除去能力予測(技術別、年間百万トンCO2)、2025-2035年

9.12. DACCS技術別炭素クレジット収入予測(百万米ドル)、2025-2035

9.13. DACCS予測手法と議論

9.14. BiCRS予測手法

9.15. BECCS、バイオチャール、バイオマス埋立による二酸化炭素除去容量予測(百万トンCO2/年)、2025-2035

9.16. BECCS、バイオチャール、およびバイオマス埋蔵の炭素クレジット収入予測(百万米ドル)、2025-2035

9.17. BECCS:予測議論

9.18. バイオチャールとバイオマス埋蔵:予測議論

9.19. 強化された岩石風化による炭素除去能力予測(年間百万トンCO2)、2025-2035

9.20. 強化された岩石風化による炭素クレジット収入予測(百万米ドル)、2025-2035

9.21. 鉱物化CDR:強化された岩石風化予測手法と議論

9.22. 海洋ベースのCDR:予測手法

9.23. 海洋ベースの炭素除去能力予測(年間百万トンCO2)、2025-2035

9.24. 海洋ベースの炭素クレジット収入予測(百万米ドル)、2025-2035

9.25. 海洋ベースのCDR:予測議論

10. 付録

10.1. 大規模DACCSプロジェクトデータベース

10.2. 運用中のBECCUSプロジェクト

10.3. 建設中または開発段階のBECCSプロジェクト

10.4. バイオチャール企業(1/2)

10.5. バイオチャール企業(2/2)

11. 企業プロファイル

11.1. 3R-BioPhosphate

11.2. 8 Rivers

11.3. 8 Rivers

11.4. Airex Energy

11.5. Airhive

11.6. BC Biocarbon

11.7. Brineworks

11.8. CapChar

11.9. Captura

11.10. Carbo Culture

11.11. Carbofex

11.12. Carbogenics

11.13. Carbon Asset Solutions

11.14. Carbon Blade

11.15. CarbonBlue

11.16. Climeworks

11.17. クライムワークス

11.18. クライムワークス

11.19. CO2ロック

11.20. DACMA

11.21. エクアティック

11.22. フリーズカーボン

11.23. JCCL(日本カーボンサイクル研究所)

11.24. マイノカーボン

11.25. ネオカーボン

11.26. neustark

11.27. O.C.O Technology

11.28. Paebbl

11.29. Paebbl

11.30. Parallel Carbon

11.31. Phlair

11.32. ピロCCS

11.33. シーウィード・ジェネレーション

11.34. スカイツリー

11.35. タカチャール

11.36. ウンド

11.37. ヴィカーブ

11.38. ウェイストエックス

11.39. ヤマ

Summary

Carbon dioxide removal technologies including DACCS (direct air carbon capture and storage), BECCS, biochar, afforestation/reforestation, mineralization, ocean-based CDR, with trends, forecasts, and carbon credit markets

In 2024, pre-purchases of durable, engineered carbon dioxide removal (CDR) credits in the voluntary carbon credit markets reached a new record high. Corporate demand for these high-quality credits continues to outstrip supply, driving the scale-up of emerging carbon dioxide removal technologies. With the increasing overlap of voluntary and compliance carbon markets - such as mechanisms for Article 6.4 of the Paris Agreement - the business case for CDR technologies is solidifying.

"Carbon Dioxide Removal (CDR) 2025-2035:, Technologies, Players, Carbon Credit Markets, and Forecasts" provides a comprehensive outlook of the emerging CDR industry and carbon credit markets, with an in-depth analysis of the technological, economic, regulatory, and environmental aspects that are shaping this market. In it, IDTechEx focuses on technologies that actively remove CO₂ from the atmosphere and sequester it into carbon sinks, namely:

1. Direct air carbon capture and storage (DACCS), which leverages chemical processes to capture CO₂ directly from the air and sequester it in geologic formations or durable products.

2. Biomass with carbon removal and storage (BiCRS), which involves strategies that use biomass to remove CO2 from the atmosphere and store it underground or in long-lived products. It includes approaches such as BECCS (bioenergy with carbon capture and storage), biochar, biomass burial, and bio-oil underground injection.

3. Land-based CDR methods that leverage biological processes to increase carbon stocks in soils, forests, and other terrestrial ecosystems, i.e. afforestation and reforestation and soil carbon sequestration techniques.

4. Mineralization CDR technologies that enhance natural mineral processes that permanently bind CO₂ from the atmosphere with rocks through enhanced rock weathering, carbonation of mineral wastes, and oxide looping.

5. Ocean-based CDR methods that strengthen the ocean carbon pump through ocean alkalinity enhancement, direct ocean capture, artificial upwelling/downwelling, coastal blue carbon, algae cultivation/marine seaweed sinking, and ocean fertilization.

These CDR technologies are at a wide range of technology readiness levels. Durable, engineered CDR technologies that have potential for vast scale deployment - such as DACCS and BECCS - currently receive government support through subsidies or tax credits (such as the 45Q tax credit in the US) alongside generating revenue from voluntary carbon credit markets as businesses seek to address scope 3 CO2 emissions. These technologies are expected to make the biggest contribution to carbon credit revenue in 2035 according to IDTechEx forecasting.

DACCS reaches the megatonne scale in 2025

In 2024, DAC pioneer Climeworks inaugurated the world's largest direct air capture facility, removing 40,000 tonnes per year of CO2 from the atmosphere. With the completion of 1PointFive's Stratos facility in 2025, DACCS will be catapulted to the megatonne scale. While large-scale facilities are reducing costs, there are now over a hundred companies active in the DACCS space, seeking further improvements that can lower capture costs. With different sorbents, regeneration methods, and equipment designs being pursued, DACCS continues to see significant public sector and private sector funding. By considering economics and energy demand, this report examines which direct air capture technologies are likely to be most successful.

Accelerating electrochemical methods of carbon dioxide removal

All forms of durable, engineered carbon dioxide removal technologies have been scaling up because demand for high quality carbon credits currently outstrips supply. One interesting trend is the growth in electrochemical CDR. Energy demand can often be a significant contributor to capture cost. In recent years, several start-ups have begun to develop electrochemical methods of carbon dioxide removal in search of increased energy efficiency and better compatibility with intermittent renewable energy sources such as wind and solar. Electrolysis and electrodialysis technologies are the frontrunners in the direct ocean capture space, and similar pH-swing electrochemical methods have seen increased investment interest for direct air capture. This report analyses the reality of electrochemical CDR - including economics, manufacturing and supply chain development, technical challenges, and key players.

Comprehensive analysis and market forecasts

This IDTechEx report assesses the CDR carbon credit market in detail, evaluating the different technologies, latest advancements, and potential adoption drivers and barriers. The report also includes a granular forecast until 2035 for the deployment of eight CDR categories (Temperature-based DACCS, electrochemical DACCS, BECCS, biochar, biomass burial, direct ocean capture, ocean alkalinity enhancement, and enhanced rock weathering), alongside exclusive analysis and interview-based company profiles.

Key aspects:

This report provides the following information:

Technology and market analysis:

• Data and context on each type of carbon dioxide removal solution including direct air capture.

• Analysis of the challenges and opportunities in the nascent CDR (carbon dioxide removal) carbon credit markets.

• State of the art and innovation in the field for direct air capture - including emerging technologies such as electrochemical approaches and equipment design.

• Detailed overview of CDR technologies: land-based, mineralization-based, ocean-based, DACCS (direct air carbon capture with storage), and BiCRS (biomass with carbon capture and storage).

• Market potential (both voluntary and compliance) of CDR carbon offsets.

• Key strategies and economies for scaling up CDR technologies.

• Assessment of requirements (infrastructure, energy, supply chain, etc) for CDR market uptake, with a focus on direct air capture.

• Climate benefit potential of main CDR solutions.

• Benchmarking based on factors such as technology readiness level (TRL), cost, and scale potential.

• Key regulations and policies influencing the CDR market.

Player analysis and trends:

• Primary information from key CDR-related companies.

• Analysis of CDR players' latest developments, observing projects announced, funding, trends, and partnerships.

Market forecasts and analysis:

• Granular market forecasts until 2035 for durable, engineered CDR solutions, subdivided in eight technological areas.

Table of Contents1. EXECUTIVE SUMMARY

1.1. Why carbon dioxide removal (CDR)?

1.2. The CDR technologies covered in this report (1/2)

1.3. The CDR technologies covered in this report (2/2)

1.4. Scale and technology readiness level of carbon dioxide removal methods

1.5. The CDR business model and its challenges: Carbon credits

1.6. The carbon removal supply chain: Carbon credit market players

1.7. Shifting buyer preferences for durable CDR in carbon credit markets

1.8. Overall picture: Voluntary carbon credit markets in 2024

1.9. How expensive were durable carbon removals in 2024?

1.10. DACCS: Summary

1.11. Current status of DACCS

1.12. The role of tax credits in supporting DACCS: 45Q and ITC

1.13. What are the major challenges for scaling up direct air capture?

1.14. DAC technology landscape: Companies

1.15. Which DAC technologies will be the most successful?

1.16. How will DAC technologies develop?

1.17. Solid sorbents - semi-continuous operation can lower energy intensity

1.18. Electrochemical DAC: Key takeaways

1.19. The potential for BiCRS goes beyond BECCS: Benchmarking

1.20. Most existing BECCS projects are in ethanol production

1.21. Solvent capture technologies dominate the BECCS space

1.22. Government support for BECCS is accelerating

1.23. BECCS: Key takeaways

1.24. The state of the global biochar market

1.25. Biochar CDR is scaling up

1.26. Biochar: Key takeaways

1.27. BiCRS Value Chain

1.28. Afforestation and reforestation: Key takeaways

1.29. Key takeaways: Soil carbon sequestration

1.30. Key takeaways: Mineralization CDR

1.31. Key players in ocean-based CDR

1.32. Key takeaways: Ocean-based CDR

1.33. Carbon dioxide removal capacity forecast by technology (million metric tons of CO2 per year), 2025-2035

1.34. Carbon dioxide removal annual carbon credit revenue forecast by technology (billion US$), 2025-2035

1.35. Carbon dioxide removal market forecast, 2025-2035: Discussion

1.36. The evolution of the durable CDR market

1.37. Access More With an IDTechEx Subscription

2. INTRODUCTION2.1. Introduction and general analysis

2.1.1. What is carbon dioxide removal (CDR)?

2.1.2. Description of the main CDR methods

2.1.3. Why carbon dioxide removal (CDR)?

2.1.4. What is the difference between CDR and CCUS?

2.1.5. High-quality carbon removals: Durability, permanence, additionality

2.1.6. Scale and technology readiness level of carbon dioxide removal methods

2.1.7. Carbon dioxide removal technology benchmarking

2.1.8. Status and potential of CDR technologies

2.1.9. Monitoring, reporting, and verification of CDR

2.1.10. CDR: Deferring the problem?

2.1.11. What is needed to further develop the CDR sector?

2.1.12. CDR market traction in 2024

2.1.13. The Xprize Carbon Removal

2.1.14. Regional factors could determine the best CDR strategy

2.2. Carbon credit markets

2.2.1. Global climate action - the Paris Agreement

2.2.2. Carbon pricing and carbon markets

2.2.3. Compliance carbon pricing mechanisms across the globe

2.2.4. What is the price of CO2 in global carbon pricing mechanisms?

2.2.5. What is a carbon credit?

2.2.6. How are carbon credits certified?

2.2.7. The role of carbon registries in the credit market

2.2.8. Measurement, Reporting, and Verification (MRV) of Carbon Credits

2.2.9. How are voluntary carbon credits purchased?

2.2.10. The carbon removal carbon credit market players

2.2.11. Interaction between compliance markets and voluntary markets (geographical)

2.2.12. Interaction between compliance markets and voluntary markets (sectoral)

2.2.13. Governmental carbon crediting mechanisms

2.2.14. Article 6.4 of the Paris Agreement: Global, unified carbon credit market

2.2.15. Quality of carbon credits

2.2.16. Carbon removal vs carbon avoidance/reduction credits

2.2.17. Carbon dioxide removal vs emissions reductions

2.2.18. Carbon dioxide removal has a very limited role in $100 billion compliance markets

2.2.19. The state of CDR in the voluntary carbon market

2.2.20. Shifting buyer preferences for durable CDR in carbon credit markets

2.2.21. Overall picture: Voluntary carbon credit markets in 2024

2.2.22. Advanced market commitment in durable CDR

2.2.23. Businesses should be investing in carbon dioxide removal now

2.2.24. Biggest durable carbon removal buyers

2.2.25. Pre-purchases still dominate the durable CDR space

2.2.26. Prices of CDR credits

2.2.27. How expensive were durable carbon removals in 2024?

2.2.28. Current carbon credit prices by company and technology

2.2.29. Carbon market sizes

2.2.30. Are there enough buyers for durable CDR technologies?

2.2.31. CDR technologies: key takeaways

3. DIRECT AIR CARBON CAPTURE AND STORAGE (DACCS)3.1. Introduction to direct air capture (DAC)

3.1.1. What is direct air capture (DAC)?

3.1.2. Why DACCS as a CDR solution?

3.1.3. Current status of DACCS

3.1.4. DACCS project pipeline: Locations and technologies

3.1.5. Momentum: Policy support for DAC by region

3.1.6. The role of tax credits in supporting DACCS: 45Q and ITC

3.1.7. The US has plans to establish 20 large-scale regional DAC Hubs

3.1.8. Momentum: Private investment in DAC

3.1.9. Where did money for DAC come from in 2024?

3.1.10. DAC land requirement is an advantage

3.1.11. DAC vs point-source carbon capture

3.1.12. Power requirements for DAC

3.1.13. Nameplate capacity vs actual net removal

3.1.14. Difficulties sourcing clean energy

3.1.15. Operational flexibility - powering DAC with intermittent renewables

3.1.16. What are the major challenges for scaling up direct air capture?

3.2. Leading DAC technologies

3.2.1. CO2 capture/separation mechanisms in DAC

3.2.2. Direct air capture technologies

3.2.3. Regeneration methods for solid and liquid DAC

3.2.4. Comparing regeneration methods for solid and liquid DAC

3.2.5. Leading DAC companies

3.2.6. Direct air capture space: Technology and location breakdown

3.2.7. Solid sorbents for DAC

3.2.8. Climeworks

3.2.9. Process flow diagram of S-DAC: Climeworks

3.2.10. Solid sorbents - semi-continuous operation can lower energy intensity

3.2.11. Heirloom

3.2.12. Process flow diagram of CaO looping: Heirloom

3.2.13. Liquid solvents for DAC

3.2.14. Liquid solvent-based DAC: Carbon Engineering

3.2.15. Carbon Engineering

3.2.16. Stratos: Bringing DAC to the half megatonne scale

3.2.17. Process flow diagram of L-DAC: Carbon Engineering

3.2.18. DAC process: Climeworks and Carbon Engineering

3.2.19. Electricity and heat sources: Climeworks and Carbon Engineering

3.2.20. Requirements to capture 1 Mt of CO2 per year: Climeworks and Carbon Engineering

3.2.21. DAC technology landscape: Companies

3.2.22. Which DAC technologies will be the most successful?

3.2.23. How will DAC technologies develop?

3.2.24. DACCS carbon credit sales by company

3.3. Electroswing/electrochemical DAC technologies

3.3.1. Electroswing/electrochemical DAC

3.3.2. Types of electrochemical DAC (1/2)

3.3.3. Types of electrochemical DAC (2/2)

3.3.4. Desired characteristics of electrochemical cell components

3.3.5. Electrochemical DAC company landscape

3.3.6. Benchmarking electrochemical DAC methods

3.3.7. Technical challenges in electrochemical DAC

3.3.8. Electrochemical DAC: Flexibility for low-cost intermittent renewable power

3.3.9. Electrochemical DAC costs depend strongly on electricity prices

3.3.10. Electrochemical DAC: Key takeaways

3.4. Novel DAC technologies

3.4.1. Moisture-swing direct air capture (humidity swing)

3.4.2. Ion exchange resins for moisture swing DAC

3.4.3. Cryogenic direct air capture companies

3.4.4. Membrane direct air capture

3.4.5. Reactive direct air capture - combined capture and conversion

3.5. Equipment for DAC - design and manufacturing

3.5.1. Manufacturing supply chains for DAC

3.5.2. Air contactors: Existing designs

3.5.3. Commercial air contactor manufacturing facility

3.5.4. Lessons learned from Carbon Engineering: Adapt existing industrial equipment to establish supply chain

3.5.5. Lessons learned from Global Thermostat: Partnerships essential for technology development

3.5.6. Passive air contacting

3.5.7. Integration DAC into existing industrial processes: Cooling towers, HVAC, and waste heat

3.6. DAC economics

3.6.1. The economics of DAC

3.6.2. The CAPEX of DAC: Sub-system contribution

3.6.3. The OPEX of DAC

3.6.4. Overall capture cost of DAC (1/2)

3.6.5. Overall capture cost of DAC (2/2)

3.6.6. Component specific capture cost contributions for DACCS

3.6.7. Financing DAC

3.6.8. Business models for DAC

3.6.9. Direct air capture carbon credit selling prices

3.7. CO2 storage

3.7.1. DAC must be coupled with permanent storage for carbon dioxide removals

3.7.2. Storing supercritical CO₂ underground

3.7.3. Mechanisms of subsurface CO₂ trapping

3.7.4. CO2 leakage is a small risk

3.7.5. Storage type for geologic CO2 storage: Saline aquifers

3.7.6. Storage type for geologic CO2 storage: Depleted oil and gas fields

3.7.7. Unconventional storage resources: Basalts and ultra-mafic rocks

3.7.8. Estimates of global CO₂ storage space

3.7.9. CO2 storage potential by country

3.7.10. Permitting and authorization of CO2 storage

3.7.11. Class VI permits are delaying DACCS development in US

3.7.12. Examples of storage providers for DAC

3.7.13. Key takeaways: CO2 storage

3.8. DAC Challenges

3.8.1. Challenges associated with DAC technology

3.8.2. Oil and gas sector involvement in DAC

3.8.3. DACCS co-location with geothermal energy

3.8.4. What can DAC learn from the wind and solar industries' scale-up?

3.8.5. What is needed for DAC to achieve the gigatonne capacity by 2050?

3.8.6. DACCS SWOT analysis

3.8.7. DACCS: Summary

4. BIOMASS WITH CARBON REMOVAL AND STORAGE (BICRS)4.1. Introduction

4.1.1. Biomass with carbon removal and storage (BiCRS)

4.1.2. BiCRS possible feedstocks

4.1.3. What type of biomass is currently used for CDR?

4.1.4. The potential for BiCRS goes beyond BECCS: Benchmarking

4.1.5. BiCRS conversion pathways

4.2. Bioenergy with carbon capture and storage (BECCS)

4.2.1. Bioenergy with carbon capture and storage (BECCS)

4.2.2. Point source capture technologies

4.2.3. Most existing BECCS projects are in ethanol production

4.2.4. Solvent capture technologies dominate the BECCS space

4.2.5. Amine-solvent technologies dominate BECCS

4.2.6. Government support for BECCS is accelerating

4.2.7. BECCS business model - Ørsted example

4.2.8. BECCS dominates the sales of durable, engineered CDR credits

4.2.9. Biogenic CO2 must be coupled with permanent storage for carbon dioxide removals

4.2.10. BECCS projects - trends and discussion

4.2.11. UK BECCS case studies

4.2.12. Ethanol production dominates the BECCS project pipeline

4.2.13. Network connecting bioethanol plants for BECCS

4.2.14. Opportunities in BECCS: Heat generation

4.2.15. Opportunities in BECCS: Waste-to-energy

4.2.16. The challenges of BECCS

4.2.17. The energy and carbon efficiency of BECCS

4.2.18. Importance of regrowth rates on carbon accounting for biogenic emissions

4.2.19. Is BECCS sustainable?

4.2.20. BECCS: Key takeaways

4.3. Biochar

4.3.1. What is biochar?

4.3.2. How is biochar produced? (1/2)

4.3.3. How is biochar produced? (2/2)

4.3.4. Biochar feedstocks

4.3.5. Permanence of biochar carbon removal

4.3.6. Biochar applications

4.3.7. Economic considerations in biochar production (1)

4.3.8. Economic considerations in biochar production (2)

4.3.9. Biochar: Market and business model

4.3.10. The state of the global biochar market

4.3.11. Artisanal vs industrial biochar

4.3.12. Biochar carbon credit selling price

4.3.13. Key players in biochar CDR by scale

4.3.14. Biochar business model: Equipment suppliers and project developers

4.3.15. Biochar business model: Discussion

4.3.16. Biochar legislation and certification

4.3.17. Additionality of biochar carbon removal

4.3.18. Biochar: Key takeaways

4.4. Other BiCRS (bio-oil and biomass burial)

4.4.1. Bio-oil geological storage for CDR

4.4.2. Biomass burial for CO2 removal

4.4.3. Capture costs below $100/tonne of CO2 drive popularity of biomass burial

4.4.4. Biomass burial commercial landscape

4.4.5. Best use of biomass - biochar, BECCS, or burial?

4.4.6. BiCRS Value Chain

5. AFFORESTATION/REFORESTATION

5.1. What are nature-based CDR approaches?

5.2. Why land-based carbon dioxide removal?

5.3. The CDR potential of afforestation and reforestation

5.4. The case for and against A/R for climate mitigation

5.5. Technologies in A/R: Remote sensing

5.6. Company landscape: Robotics in afforestation/reforestation

5.7. Afforestation/reforestation carbon credit market status in 2024

5.8. Afforestation/reforestation is already part of many government net-zero targets

5.9. "Just plant more trees!" - sustainability and greenwashing considerations

5.10. Comparing A/R and BECCS solutions

5.11. Afforestation and reforestation: Key takeaways

6. SOIL CARBON SEQUESTRATION

6.1. What is soil carbon sequestration (SCS)?

6.2. The soil carbon sequestration potential is vast

6.3. Agricultural management practices to improve soil carbon sequestration

6.4. Companies using microbial inoculation for soil carbon sequestration

6.5. Approaches to MRV for soil carbon sequestration

6.6. Additionality, measurement, and permanency of soil carbon is in doubt

6.7. Challenges in SCS deployment

6.8. The soil carbon sequestration value chain

6.9. Market trends for soil carbon sequestration in 2024

6.10. Soil carbon sequestration carbon credit market status in 2024

6.11. Soil carbon sequestration pros and cons

6.12. Key takeaways: Soil carbon sequestration

7. BASED CDR

7.1. CO2 mineralization is key for CDR

7.2. Ex situ mineralization CDR methods

7.3. Source materials for ex situ mineralization

7.4. Ex situ carbonation of mineral wastes

7.5. Carbon dioxide storage in CO2-derived concrete

7.6. CO2-derived concrete: Commercial landscape

7.7. Oxide looping: Mineralization in DAC

7.8. Enhanced weathering

7.9. Enhanced rock weathering overview

7.10. MRV in Enhanced Rock Weathering

7.11. Enhanced weathering commercial landscape

7.12. Enhanced rock weathering CDR market

7.13. Enhanced rock weathering status: Startups

7.14. Key takeaways: Mineralization CDR

8. OCEAN-BASED CARBON DIOXIDE REMOVAL8.1. Introduction

8.1.1. Ocean pumps continuously pull CO2 from the atmosphere into the ocean

8.1.2. Ocean-based CDR methods

8.1.3. Definitions of ocean-based CDR technologies

8.1.4. Why ocean-based CDR?

8.1.5. Scale and technology readiness level for ocean-based CDR

8.1.6. Benchmarking of ocean-based CDR methods

8.1.7. Key players in ocean-based CDR

8.2. Ocean-based CDR: Abiotic methods

8.2.1. Ocean alkalinity enhancement (OAE)

8.2.2. Electrochemical ocean alkalinity enhancement

8.2.3. Ocean alkalinity enhancement status: Start-ups

8.2.4. Direct ocean capture

8.2.5. Direct ocean capture status: Start-ups

8.2.6. Electrochemical direct ocean capture

8.2.7. Electrolysis for direct ocean capture: Avoiding chlorine formation

8.2.8. Other direct ocean capture technologies

8.2.9. Barriers remain for direct ocean capture

8.2.10. Artificial downwelling

8.3. Ocean-based CDR: Biotic methods

8.3.1. Status of coastal blue carbon credits in the voluntary carbon markets

8.3.2. Algal cultivation - seaweed sinking

8.3.3. Ocean fertilization

8.3.4. Several ocean fertilization start-ups have failed

8.3.5. Will ocean fertilization resurge in 2025?

8.3.6. Artificial upwelling

8.3.7. The governance challenge in large-scale deployment of ocean CDR

8.3.8. MRV for marine CDR

8.3.9. Price of ocean-based CDR credits

8.3.10. Key takeaways: Ocean-based CDR

9. CDR MARKET FORECASTS

9.1. Forecast scope: Durable, engineered removals

9.2. Forecast scope: Nature-based approaches

9.3. Overall Carbon Dioxide Removal Forecast Methodology/Scope

9.4. Carbon dioxide removal capacity forecast by technology (million metric tons of CO2 per year), 2025-2035

9.5. Data table for carbon dioxide removal capacity forecast by technology (million metric tons of CO2 per year), 2025-2035

9.6. Carbon dioxide removal carbon credit annual revenue forecast by technology (billion US$), 2025-2035

9.7. Data table for carbon dioxide removal carbon credit annual revenue forecast by technology (million US$), 2025-2035

9.8. Carbon dioxide removal market forecast, 2025-2035: discussion

9.9. The evolution of the durable CDR market

9.10. Changes since the previous IDTechEx CDR forecast

9.11. DACCS carbon removal capacity forecast by technology (million metric tons of CO2 per year), 2025-2035

9.12. DACCS carbon credit revenue forecast by technology (million US$), 2025-2035

9.13. DACCS forecast methodology and discussion

9.14. BiCRS forecast methodology

9.15. BECCS, biochar and biomass burial carbon removal capacity forecast (million metric tons of CO2 per year), 2025-2035

9.16. BECCS, biochar, and biomass burial carbon credit revenue forecast (million US$), 2025-2035

9.17. BECCS: Forecast discussion

9.18. Biochar and biomass burial: Forecast discussion

9.19. Enhanced rock weathering carbon removal capacity forecast (million metric tons of CO2 per year), 2025-2035

9.20. Enhanced rock weathering carbon credit revenue forecast (million US$), 2025-2035

9.21. Mineralization CDR: Enhanced rock weathering forecast methodology and discussion

9.22. Ocean-based CDR: Forecast methodology

9.23. Ocean-based carbon removal capacity forecast (million metric tons of CO2 per year), 2025-2035

9.24. Ocean-based carbon credit revenue forecast (million US$), 2025-2035

9.25. Ocean-based CDR: Forecast discussion

10. APPENDIX

10.1. Large-scale DACCS projects database

10.2. Operational BECCUS projects

10.3. BECCS projects under construction or advanced development

10.4. Biochar companies (1/2)

10.5. Biochar companies (2/2)

11. COMPANY PROFILES

11.1. 3R-BioPhosphate

11.2. 8 Rivers

11.3. 8 Rivers

11.4. Airex Energy

11.5. Airhive

11.6. BC Biocarbon

11.7. Brineworks

11.8. CapChar

11.9. Captura

11.10. Carbo Culture

11.11. Carbofex

11.12. Carbogenics

11.13. Carbon Asset Solutions

11.14. Carbon Blade

11.15. CarbonBlue

11.16. Climeworks

11.17. Climeworks

11.18. Climeworks

11.19. CO2 Lock

11.20. DACMA

11.21. Equatic

11.22. Freeze Carbon

11.23. JCCL (Japan Carbon Cycle Labs)

11.24. Myno Carbon

11.25. NeoCarbon

11.26. neustark

11.27. O.C.O Technology

11.28. Paebbl

11.29. Paebbl

11.30. Parallel Carbon

11.31. Phlair

11.32. PyroCCS

11.33. Seaweed Generation

11.34. Skytree

11.35. Takachar

11.36. UNDO

11.37. Vycarb

11.38. WasteX

11.39. Yama

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(環境・エネルギー)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|