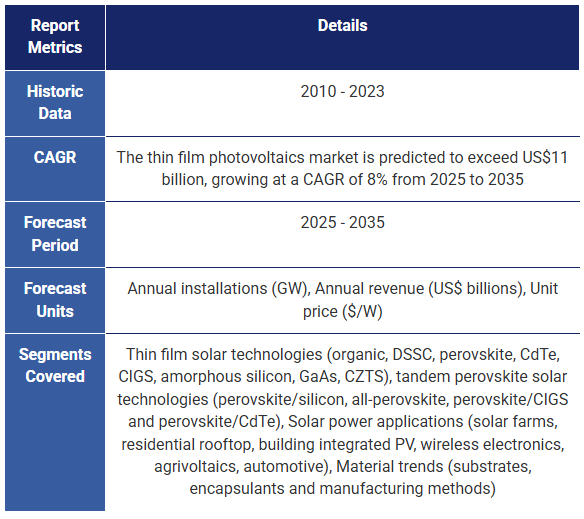

薄膜太陽電池市場2025-2035年:技術、プレーヤー、動向Thin Film Photovoltaics Market 2025-2035: Technologies, Players, and Trends 10年間の薄膜太陽電池市場予測を、太陽光発電技術別、応用分野別に細分化し、コスト分析、主要プレイヤーの詳細評価、データ駆動型ベンチマークとともに掲載 再生可能エネルギー分野は急速に拡大しており... もっと見る

サマリー10年間の薄膜太陽電池市場予測を、太陽光発電技術別、応用分野別に細分化し、コスト分析、主要プレイヤーの詳細評価、データ駆動型ベンチマークとともに掲載 再生可能エネルギー分野は急速に拡大しており、中でも太陽光発電は急成長している技術のひとつです。2023年には、世界の太陽光発電への年間投資額が、世界の石油投資を含め、初めて他のすべての発電技術を追い抜いた。投資の伸びは2024年に入っても続き、IEAは、年末までにこの分野が世界の資金調達で最大のシェアを占めると予測している。シリコン太陽光発電(PV)が引き続き市場を支配している一方で、さまざまな既存技術や新興技術がこの分野の進化に貢献してきたし、これからも貢献していくだろう。そのなかでも薄膜太陽電池は、長らくシリコン太陽電池と同規模での競争に苦戦してきた。しかし、エネルギー需要の増加、脱炭素化への意欲的な目標、エネルギー安全保障への懸念の高まりにより、薄膜PVの普及が進む可能性はあるのだろうか。

IDTechExの最新レポート「薄膜太陽電池市場 2025-2035年」:技術、テクノロジー、プレーヤーと動向」は薄膜PV市場全体を包括的にカバーしている。染料増感太陽電池(DSSC)、有機太陽電池(OPV)、ペロブスカイト太陽電池、テルル化カドミウム(CdTe)、セレン化銅インジウムガリウム(CIGS)、ヒ化ガリウム(GaAs)、アモルファスシリコン(a-Si)、硫化銅亜鉛スズ(CZTS)太陽電池など、既存および新興の薄膜PV技術をデータに基づいてベンチマークし、40以上の主要市場参入企業のプロファイルとともに、薄膜PV分野全体の概要を明らかにしています。ソーラーファーム、住宅用屋上、建物一体型太陽光発電、農業用太陽光発電、ワイヤレスエレクトロニクスを含む主要および新興アプリケーション分野の批判的分析は、太陽電池市場全体のきめ細かな10年予測策定に役立つ。IDTechExは、薄膜太陽電池市場が2035年までに110億米ドルを超えると予測している。

薄膜太陽電池は太陽電池のサブクラスで、ガラス、プラスチック、金属などの基板上に光起電力材料の1つ以上の薄膜を蒸着して製造される。電極を除けば、薄膜太陽電池内の各機能層の厚さは一般的に5~500nmであり、一般的に数nm~数ミクロンの厚さの極めて薄い発電デバイスを可能にする。そのため、薄膜太陽電池モジュールは非常に軽量で、(基板の選択にもよるが)フレキシブルであるため、低重量アプリケーションや曲面への設置が可能である。

薄膜PV市場のシェアは歴史的に低く、2024年時点では全太陽光発電市場の約2.5%にまで低下している。薄膜太陽電池技術は、その性能指標の低さ、原材料の問題、製造コストの問題から、シリコン太陽電池と同程度の競争には苦戦してきた。しかし、技術的状況の変化と応用範囲の拡大は、今後10年間で薄膜市場全体に大きな変化をもたらすだろう。

市場普及の原動力となる新たな用途

薄膜太陽電池は、従来の太陽電池用途だけでなく、シリコン太陽電池技術が適さない用途にも利用できる。こうした用途には、パネルを建物の側面に取り付け、既存のインフラに組み込む建物一体型太陽光発電(BIPV)などがある。薄膜モジュールは、シリコンモジュールよりも最大90%軽量化できるため、大幅な構造変更が必要なく、建物の垂直統合に非常に適している。屋上スペースに比べて垂直スペースの利用可能面積が十分に大きいことから、この用途は再生可能エネルギーへの取り組みに大きく貢献する可能性がある。また、薄膜太陽電池の種類によっては、透明度を調整することができるため、美観上邪魔にならず窓に最適である。

その他の新たな用途としては、小型の自己発電型電子機器やモノのインターネット(IoT)分野がある。これらの小型電子機器は通常、電池に依存しており高い材料費と人件費を負担して数年ごとに交換する必要がある。バッテリーよりも長寿命で低コストの小型PVモジュールを使ってこれらの機器に電力を供給することは、非常に有望なアプリケーションである。

薄膜市場を牽引するペロブスカイト太陽電池技術の登場

ペロブスカイト太陽電池は、その軽量で柔軟な性質、高い製造拡張性、既存の太陽電池技術と比べた大幅な低コストにより、学術的にも業界的にも大きな注目を集めている。ペロブスカイト太陽電池にはペロブスカイト活性層が含まれており、溶液ベースのシート・トゥ・シートまたはロール・トゥ・ロール対応のプロセスを用いて薄膜として成膜できるため、処理の拡張や自動化が容易で、財務的な観点からも非常に魅力的である。これに加え、ペロブスカイトの合成には比較的豊富で安価な原料が使用されるため、IDTechExはペロブスカイト太陽電池がシリコンだけでなく他の薄膜太陽電池技術よりも大幅に安価であると判断している。

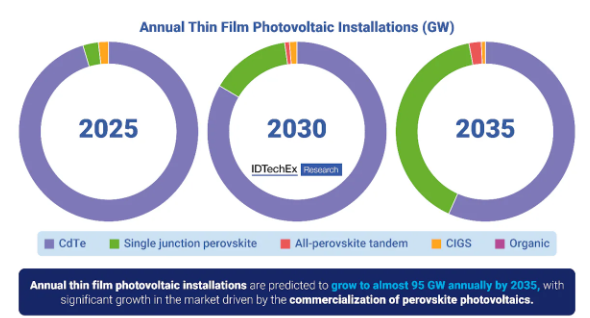

単接合ペロブスカイト太陽電池の製造だけでなく、この技術はタンデム型太陽電池構造への応用も検討されている。確立されたシリコンや薄膜太陽電池を含むすべての単接合技術は、効率プラトーに近づくだろう。単接合デバイスの理論的な最大効率限界は30%であるため、このプラトーは予想される。その代わりに研究者たちははるかに高い電力変換効率を達成するために、ペロブスカイトと他の太陽電池技術との統合を模索している。これらの多接合セルは、約43%というはるかに高い理論効率の限界を持っている。商業的に大きく注目されている技術は、ペロブスカイト/シリコン、オールペロブスカイト、ペロブスカイト/CIGSタンデムPVであり、各デバイスはそれぞれ個別の技術的利点を有している。

ペロブスカイト太陽電池は商業化の初期段階に入り、多くの業界関係者がこの技術を「次の主要な太陽電池技術」と喧伝している。ペロブスカイト太陽電池市場の大きな技術革新の機会、商業的注目の高まり、それに伴う成長予測は、薄膜太陽電池の復活を後押しする大きな要因となっている。IDTechExによる現在の予測では、ペロブスカイト太陽電池は2035年までに薄膜ソーラー設備全体の40%以上を占めると見られている。

本レポートでは、IDTechExが薄膜太陽電池市場の成長促進要因をさらに探るとともに、薄膜PV採用の潜在的な落とし穴についても分析している。これまでのところ市場の成長は限定的であるものの、クリーンで再生可能なエネルギーへの需要が伸び続けていることから、10年後までには大幅な拡大が見込まれている。

重要な側面

色素増感太陽電池(DSSC)、有機太陽電池(OPV)、ペロブスカイト太陽電池、テルル化カドミウム(CdTe)、セレン化銅インジウムガリウム(CIGS)、ガリウムヒ素(GaAs)など、あらゆる薄膜太陽電池技術の詳細分析とデータによるベンチマーク

薄膜太陽電池技術の主要材料動向の詳細分析

新興タンデム型太陽電池市場の評価

全体を通しての市場分析

目次

1.エグゼクティブ・サマリー

1.1.報告書の紹介

1.2.太陽電池とは何か?

1.3.太陽光発電市場の成長

1.4.世界の再生可能エネルギーと太陽エネルギーの目標

1.5.薄膜太陽電池とは?

1.6.本レポートで扱う薄膜太陽電池技術

1.7.薄膜太陽電池技術のベンチマーク(i)

1.8.薄膜太陽電池技術のベンチマーク(ii)

1.9.ソーラー技術の開発状況(TRL)

1.10.薄膜系太陽電池の技術タイプ別企業動向

1.11.色素増感太陽電池の概要

1.12.有機太陽電池の概要

1.13.ペロブスカイト太陽電池 - 薄膜太陽電池市場を復活させる新技術

1.14.CdTe 太陽電池 - 圧倒的な薄膜技術だが、原材料に懸念

1.15.CIGS PV - 市場が脅威にさらされる可能性

1.16.GaAs PVの将来は未知数

1.17.アモルファスシリコンPVは大幅な市場縮小

1.18.わずかな追加コストで効率を高めるタンデムPV技術

1.19.薄膜PVの製造はスケーラブルで低コスト

1.20.太陽光発電技術のコスト

1.21.薄膜太陽電池の用途

1.22.伝統的な太陽光発電の用途 - 屋上と太陽光発電所

1.23.薄膜太陽電池の代替用途 - ビルディング・インテグレーションとワイヤレス・エレクトロニクス

1.24.薄膜太陽電池の市場シェアは伸びるか?

1.25.タイプ別ソーラー年間設置量

1.26.薄膜太陽電池の年間売上高

1.27.薄膜太陽電池市場の展望

1.28.IDTechEx サブスクリプションでさらにアクセス

2.薄膜太陽電池市場の予測

2.1.予測方法

2.2.太陽光発電の年間総設備容量

2.3.薄膜太陽電池の年間総設置容量

2.4.薄膜太陽電池の年間売上高

2.5.アプリケーション分野別の年間薄膜設置量

2.6.ソーラーファームの年間設置量

2.7.ソーラーファームの年間売上高

2.8.住宅用屋上設置量

2.9.住宅用屋上の年間売上高

2.10.ワイヤレスエレクトロニクスの年間生産能力

2.11.太陽電池モジュールのコスト

3.はじめに

3.1.太陽電池とは?

3.2.太陽光発電市場の成長

3.3.世界の太陽光発電投資

3.4.地域別にみた現在の太陽光発電設備

3.5.世界の再生可能エネルギーと太陽エネルギーの目標

3.6.中国が固定価格買取制度を撤廃

3.7.太陽光発電技術の研究進展

3.8.薄膜太陽電池とは?

3.9.薄膜太陽電池の動機

3.10.太陽電池の主な性能指標

3.11.本レポートで扱う薄膜太陽電池技術(i)

3.12.本レポートで扱う薄膜太陽電池技術(ii)

3.13.現在の薄膜太陽電池市場

3.14.薄膜太陽電池市場シェアは伸びるか?

3.15.太陽電池技術のベンチマーク

3.16.主要薄膜技術の比較

3.17.ソーラー技術の開発状況

3.18.薄膜太陽電池企業の状況

3.19.PV技術のコスト

3.20.垂直統合の進展による薄膜太陽電池のメリット

4.薄膜太陽電池の新技術

4.1.1.新興薄膜太陽電池の紹介

4.1.2.新興薄膜太陽電池技術の開発状況

4.2.色素増感太陽電池

4.2.1.色素増感太陽電池の概要

4.2.2.DSSCへの関心

4.2.3.DSSCの仕組み

4.2.4.DSSC光増感剤の特性

4.2.5.DSSC電解液

4.2.6.代替DSSC電解質溶液

4.2.7.DSSC対向電極

4.2.8.DSSCの安定性

4.2.9.DSSCのカプセル化とエッジシール

4.2.10.DSSCの開発機会

4.2.11.色素増感太陽電池のSWOT

4.2.12.DSSC技術の概要

4.2.13.企業の概況

4.2.14.エクセガーの概要

4.2.15.エクセガー社のパワーフォイル技術応用

4.2.16.エクセガー社の商業パートナーシップ

4.2.17.エクセガー社の商業パートナーシップ

4.2.18.Solaronixの概要

4.2.19.GCell by G24 Power 概要

4.3.有機太陽電池

4.3.1.有機太陽電池の概要

4.3.2.有機太陽電池の仕組み

4.3.3.有機太陽電池の基本動作

4.3.4.有機太陽電池の長所と短所

4.3.5.有機太陽電池の活性層

4.3.6.有機活性層:低分子とポリマー

4.3.7.非フラーレン系アクセプターの長所と短所

4.3.8.OPVのチューナビリティ

4.3.9.世界記録となる大面積OPVモジュールに使用されたブリリアント・マターの材料

4.3.10.高効率大面積モジュール実現に向けた現在の課題

4.3.11.OPV材料の可能性

4.3.12.有機PVのSWOT

4.3.13.有機PVのまとめ

4.3.14.有機PV企業の展望

4.3.15.Brilliant Matters - 材料サプライヤー

4.3.16.Brilliant Mattersの有機PV製品

4.3.17.Raynergy Tek - 材料サプライヤー

4.3.18.レイナジーのOPV製品

4.3.19.アスカの概要

4.3.20.アスカのケーススタディ

4.3.21.アスカ、ヘリンググループに買収される

4.3.22.エピシャインの概要

4.3.23.エピシャインの顧客とパートナーシップ

4.3.24.ドラキュラ・テクノロジーズの概要

4.3.25.ドラキュラ・テクノロジーズ - LAYER OPV技術

4.3.26.ヘリアテックの概要

4.3.27.ヘリアテックの設備

4.3.28.リベステックの概要

4.3.29.Sunewの概要

4.3.30.有機PV企業のベンチマーク

4.3.31.有機PV企業の概要

4.4.ペロブスカイト太陽電池

4.4.1.ペロブスカイト太陽電池とは?

4.4.2. n-i-p構成とp-i-n構成

4.4.3.ペロブスカイト太陽電池に使われる足場 - メソポーラス・ペロブスカイト太陽電池

4.4.4.ペロブスカイト太陽電池の製造

4.4.5.ペロブスカイト安定性の概要

4.4.6.外部劣化

4.4.7.本質的劣化メカニズム

4.4.8.材料工学

4.4.9.添加物工学

4.4.10.鉛の懸念は正当化されるか?

4.4.11.鉛に関する一般的認識と現実

4.4.12.ペロブスカイトの材料組成は光学に影響を与える

4.4.13.正孔輸送材料(HTM)

4.4.14.無機輸送材料

4.4.15.薄膜ペロブスカイト太陽電池の最近の動向

4.4.16.薄膜ペロブスカイト太陽電池のSWOT分析

4.4.17.まとめ - 薄膜ペロブスカイト太陽電池

4.4.18.薄膜ペロブスカイト太陽電池市場の概要

4.4.19.薄膜ペロブスカイト太陽電池プレーヤーの概要

4.4.20.薄膜ペロブスカイト太陽電池メーカー各社の概況

4.4.21.ザウル・テクノロジーズ 概要

4.4.22.Microquanta 概要

4.4.23.GCL 概要

4.4.24.レンシャイン・ソーラーの概要

4.4.25.ペロブスカイト薄膜太陽電池の主要メーカーまとめ

4.4.26.ペロブスカイト薄膜太陽電池の主要メーカーまとめ

4.5.新興薄膜太陽電池の用途

4.5.1.新興薄膜太陽電池のアプリケーション紹介

4.5.2.現在の応用開発段階

4.5.3.薄膜ペロブスカイトはシリコンPVの問題点をどのように克服できるのか?

4.5.4.屋内エネルギーハーベスティングと新興IoTアプリケーション

4.5.5.IoTとワイヤレス・エレクトロニクス市場を狙う企業

4.5.6.ペロブスカイト太陽電池は無線エネルギーハーベスティングの費用対効果に優れた選択肢となりうる

4.5.7.薄膜太陽電池は自動車用途に使えるか?

4.5.8.ビル用薄膜太陽電池

4.5.9.BIPVは実現可能な応用分野か?

4.5.10.建築用途の薄膜太陽電池

4.5.11.ペロブスカイト太陽電池は従来の太陽光発電所にとって有効な選択肢か?

4.5.12.新興薄膜太陽電池の用途まとめ

5. 無機薄膜太陽電池

5.1.1.無機薄膜技術 - シリコンPVの代替技術

5.1.2.無機薄膜太陽電池の開発状況

5.2.カドミウムテルル(CdTe)太陽電池

5.2.1.CdTe太陽電池の紹介

5.2.2.CdTeセルの機能

5.2.3.CdTe PVの代替構造

5.2.4.CdTe PV バッファー層の開発

5.2.5.CdTe PVの劣化とドーピング

5.2.6.CdTe 太陽電池の製造

5.2.7.CdTe PVの市場シェア

5.2.8.CdTe PVの毒性に関する懸念

5.2.9.テルル原料への懸念

5.2.10.CdTe 太陽電池のリサイクル

5.2.11.CdTeモジュールのリサイクル手順

5.2.12.CdTeとシリコンPVの比較

5.2.13.CdTeに代わる吸収体材料

5.2.14.CdTe PVの材料開発機会

5.2.15.CdTe PVのSWOT

5.2.16.CdTe PV技術の概要

5.2.17.CdTe PV市場の概要

5.2.18.First Solarの概要

5.2.19.ファースト・ソーラーの技術と製品

5.2.20.ファースト・ソーラーの財務状況

5.2.21.First Solar、ペロブスカイト太陽電池市場に参入

5.2.22.ポリソーラーの概要

5.2.23.CTF Solarの概要

5.2.24.Toledo Solar - 新興プレーヤーが市場から撤退

5.2.25.カリクソ - 倒産の歴史

5.3.銅インジウムガリウムセレン化物(CIGS)太陽電池

5.3.1.CIGS太陽電池の紹介

5.3.2.CIGS太陽電池の仕組み

5.3.3.CIGS太陽電池の効率向上

5.3.4.CIGS PVの長所と短所

5.3.5.CIGS太陽電池とシリコン太陽電池の比較

5.3.6.フレキシブルCIGS太陽電池

5.3.7.CIGS PVモジュールの製造

5.3.8.CIGS PVのシンプルで低コストな成膜の追求

5.3.9.CIGS PV技術の可能性

5.3.10.CIGS PVのSWOT

5.3.11.CIGS PV技術の概要

5.3.12.CIGS PV市場プレーヤーの概要

5.3.13.ミッドサマーの概要

5.3.14.ミッドサマーのパートナーシップ

5.3.15.ミッドサマーの財務状況

5.3.16.アセントソーラーの概要

5.3.17.アセントソーラーの財務状況

5.3.18.アバンシスの概要

5.3.19.アバンシスのケーススタディ

5.3.20.ソーラークロスの概要

5.3.21.Sunpluggedの概要

5.3.22.CIGS企業の概要

5.3.23.CIGS企業の概要

5.4.ガリウムヒ素(GaAs)太陽電池

5.4.1.GaAs PVの導入

5.4.2.GaAs PVの動作

5.4.3.多接合GaAs太陽電池

5.4.4.GaAs PVの特性

5.4.5.GaAs PVの製造プロセス

5.4.6.GaAs 基板の再利用

5.4.7.GaAs PVの代替製造プロセス

5.4.8.GaAs PVの将来

5.4.9.GaAsイノベーションの機会

5.4.10.GaAs PVのSWOT

5.4.11.GaAs PVのまとめ

5.5.アモルファスシリコン(a-Si)太陽電池

5.5.1.アモルファスシリコンPVの概要

5.5.2.アモルファスシリコンPVの動作

5.5.3.アモルファスシリコンの成膜

5.5.4.アモルファスシリコンのシェア低下

5.5.5.アモルファスシリコンを使った従来のシリコン - ヘテロ接合技術

5.5.6.太陽熱集熱器

5.5.7.オニキス・ソーラーの概要

5.5.8.アモルファスシリコンに未来はあるか?

5.5.9.アモルファスシリコンPVのSWOT

5.5.10.アモルファスシリコンPVのまとめ

5.6.硫化銅亜鉛スズ(CZTS)太陽電池

5.6.1.CZTS PVの概要

5.6.2.CZTS PVの動作原理

5.6.3.カドミウムフリーバッファー層

5.6.4.CZTS溶液ベース蒸着

5.6.5.セレン化 CZTS - CZTSSe

5.6.6.正孔輸送層としての CZTS - ペロブスカイト太陽電池

5.6.7.最近のケステライト太陽電池開発

5.6.8.Crystalsol - CZTS の商業化に取り組む有名企業

5.6.9.CZTS PVのSWOT

5.6.10.CZTS PVのまとめ

5.7.無機薄膜太陽電池の応用

5.7.1.無機薄膜太陽電池のアプリケーション概要

5.7.2.ソーラーファームは安価で高効率の太陽電池モジュールに依存

5.7.3.薄膜太陽電池の屋上利用

5.7.4.BIPV-よりニッチな応用分野

5.7.5.薄膜太陽電池の自動車用途

5.7.6.アグリボルタイクス - 比較的新しい応用分野

5.7.7.無機薄膜太陽電池の用途まとめ

6.薄膜太陽電池の製造

6.1.スケーラブルな成膜技術

6.2.スパッタリング

6.3.エアロゾル補助化学気相成長法

6.4.インクジェットプリンティング

6.5.ブレードコーティング

6.6.スロットダイコーティング

6.7.スプレーコーティング

6.8.蒸着法の比較

6.9.成膜方法の選び方

6.10.ロール・ツー・ロール印刷 - 生産規模の拡大とコスト削減

6.11.薄膜PV市場における成膜法の利用

6.12.成膜法のまとめ

7.薄膜太陽電池材料

7.1.はじめに - 薄膜太陽電池用基板と封止材

7.2.基板 - 従来型基板と新興基板

7.3.硬質ガラス基板

7.4.硬質ガラス代替基板

7.5.フレキシブルガラス基板

7.6.超薄板ガラスは柔軟性を改善できる

7.7.超薄板ガラス封止の利点

7.8.コーニング・ウィローのフレキシブルガラス

7.9.ショット・ソーラーのフレキシブルガラス

7.10.NEG G-Leaf™-超薄板ガラス

7.11.プラスチック基板

7.12.バリア層が必要なプラスチック基板

7.13.金属箔基板

7.14.基板表面の粗さ

7.15.基板材料の供給機会

7.16.基板材料のコスト比較

7.17.基板材料のベンチマーク

7.18.基板材料の選択

7.19.ガラス-ガラス封止

7.20.優れた光学封止材に求められる特性とは?

7.21.ポリマー封止 7.22.従来の薄膜封止

7.23.新しい薄膜封止材-Al2O3

7.24.Ergis noDiffusion® ウルトラバリアフィルム

7.25.市販されているフレキシブル封止材

7.26.基板と封止材の材料開発機会

7.27.薄膜太陽電池用基板と封止材のまとめ

8.タンデム型太陽電池

8.1.1.タンデム型太陽電池の概要

8.1.2.単接合とタンデム太陽電池の比較

8.1.3.タンデム型太陽電池は単接合型太陽電池の理論効率の限界を超える

8.2.ペロブスカイト/シリコン・タンデム太陽電池

8.2.1.ペロブスカイト・シリコン・タンデム太陽電池の概要

8.2.2.ペロブスカイト/シリコン・タンデムの利点

8.2.3.ペロブスカイト/シリコン・タンデムの構造と構成

8.2.4.2端子と4端子のタンデムセルの比較

8.2.5.タンデムセル構成の課題

8.2.6.2端子タンデムセルの相互接続層

8.2.7.タンデムセルの製造プロセス

8.2.8.ペロブスカイト/シリコンタンデムPVロードマップ

8.2.9.ペロブスカイト/シリコン・タンデムPVのSWOT

8.2.10.ペロブスカイト・シリコン・タンデムPVの概要

8.2.11.ペロブスカイト・シリコン・タンデム型PV市場の概要

8.2.12.ペロブスカイト薄膜とペロブスカイト/シリコン・タンデム技術の両方をターゲットとする主要企業

8.2.13.ペロブスカイト・タンデム型PVプレーヤーの概要

8.2.14.ペロブスカイト・タンデム型PVプレーヤーの概要

8.3.オールペロブスカイト型タンデム太陽電池

8.3.1.オールペロブスカイト型タンデム太陽電池の技術進歩

8.3.2.ペロブスカイト/ペロブスカイト型タンデム太陽電池のバンドギャップ調整

8.3.3.ペロブスカイト/ペロブスカイトタンデム太陽電池の構造と製造

8.3.4.ワイドバンドギャップ・ペロブスカイトの課題

8.3.5.Sn の使用が鍵となる課題

8.3.6.HTL フリーのペロブスカイト太陽電池

8.3.7.炭素ベースの HTL フリー・ペロブスカイト太陽電池

8.3.8.すべてのペロブスカイト型タンデム太陽電池の長所と短所

8.3.9.オールペロブスカイト型タンデム太陽電池のSWOT

8.3.10.オールペロブスカイト型タンデム太陽電池のまとめ

8.3.11.オールペロブスカイト・タンデム技術の将来の商業化を目指す Renshine Solar

8.3.12.エナジー・マテリアル・コーポレーション - タンデム市場を狙う薄膜ペロブスカイト型プレーヤー

8.4.その他のタンデム型ペロブスカイト太陽電池技術

8.4.1.ペロブスカイト/CIGS タンデム太陽光発電の紹介

8.4.2.ペロブスカイト/CIGS タンデム太陽電池の製造と構造

8.4.3.ミッドサマーが4端子のペロブスカイト/CIGS太陽電池を開発

8.4.4.First Solar、ペロブスカイト・タンデム太陽電池を開発中

8.4.5.ペロブスカイト/CIGSタンデムPVのSWOT

8.4.6.ペロブスカイト/CdTe タンデム型太陽電池の概要

8.4.7.ペロブスカイト・タンデム型太陽電池の代替技術まとめ

8.5.タンデム型太陽電池の用途

8.5.1.用途別の技術選択

8.5.2.屋上用タンデムPV

8.5.3.タンデム太陽光発電による太陽光発電所の発電量増加

8.5.4.ペロブスカイト・シリコン・タンデムPVは窓に使えるか?

8.5.5.オールペロブスカイト・タンデム太陽電池車

8.5.6.タンデム型PVの用途まとめ

9.企業プロフィール

9.1.アセント・ソーラー

9.2.アヴァンシス

9.3.ビヨンド・シリコン

9.4.Caelux

9.5.コスモス・イノベーション

9.6.Coveme:太陽電池

9.7.Crystalsol

9.8.キュービックPV

9.9.ドラキュラ・テクノロジーズ

9.10.ドラキュラ・テクノロジーズ

9.11.エナジー・マテリアル・コーポレーション

9.12.エナジー・マテリアル・コーポレーション

9.13.エピシャイン 9.14.エピシャイン

9.15.エピシャイン 9.16.エクセガー

9.17.GCL 9.18.グラフエナジー・テック

9.19.ハンファQセルズ(ペロブスカイト)

9.20.ヘリアテック 9.21.ヘリアテック

9.22.Hiking PV

9.23.マイクロクアンタ・セミコンダクター

9.24.ミッドサマー 9.25.オニキス・ソーラー

9.26.Opteria 9.27.オックスフォードPV

9.28.ペロブスキア・ソーラー

9.29.ポリソーラー

9.30.パワーロール

9.31.レイナジーテック太陽光発電

9.32.レンシャイン・ソーラー

9.33.リベステック

9.34.サウル・テクノロジーズ

9.35.ショット

9.36.ソーラーニクス

9.37.サンプラグド

9.38.スウィフトソーラー

9.39.タンデムPV

9.40.トレドソーラー

9.41.ビクトレックス

SummaryGranular ten year thin film solar market forecasts, segmented by photovoltaic technology and application area, along with cost-analysis, detailed assessment of major players and data driven benchmarking.

The renewable energy sector is expanding rapidly, with solar power emerging as one of the fastest-growing technologies. In 2023, global annual investments into solar overtook all other power generation technologies for the first time, including global oil investments. Growth of investment continued into 2024, with the IEA predicting the sector to receive the greatest share of global funding by the end of the year. While silicon photovoltaics (PV) continue to dominate the market, a range of established and emerging technologies have, and continue, to contribute to the sector's evolution. Among them is thin film PV, which has long struggled to compete on the same scale as silicon PV. However, with rising energy demands, ambitious decarbonization targets, and increasing concerns over energy security, could thin film PV uptake be on the rise?

IDTechEx's latest report "Thin Film Photovoltaics Market 2025-2035: Technologies, Technologies, Players & Trends" comprehensively covers the entire thin film PV market. Data driven benchmarking of the established and emerging thin film PV technologies, including dye sensitized solar cells (DSSC), organic solar cells (OPV), perovskite PV, cadmium telluride (CdTe), copper indium gallium selenide (CIGS), gallium arsenide (GaAs), amorphous silicon (a-Si) and copper zinc tin sulfide (CZTS) photovoltaics, along with over 40 profiles of key market payers, helps to outline the entire thin film PV sector. Critical analysis of the major and emerging application areas including solar farms, residential rooftop, building integrated PV, agrivoltaics and wireless electronics, helps to formulate granular 10-year forecasts for the entire solar market. IDTechEx forecasts the thin film PV market to exceed US$11 billion by 2035.

Thin film solar cells are a sub-class of solar cell, manufactured by the deposition of one or more thin films of photovoltaic material onto a substrate, such as glass, plastic or metal. Aside from the electrodes, each functional layer within a thin-film solar cell generally has a thickness between 5 and 500 nm, enabling an extremely thin power generation device, of typically a few nm to a few microns thick. Thin film PV modules are therefore very lightweight and can be flexible (depending on the substrate choice), meaning they can be installed for low-weight applications, as well as on curved surfaces.

The thin film PV market share has historically remained low, reducing to around 2.5% of all solar market installations as of 2024. Thin film PV technologies have struggled to compete to the same degree as silicon PV, due to their lower performance metrics, raw material concerns, and cost of manufacturing. However, a shift in the technological landscape, along with a broadening of application scope is likely to result in significant changes to the entire thin film market over the next decade.

Novel applications helping to drive market adoption

Thin film PV can be used for traditional solar applications as well as applications where silicon solar technology is not suited. These applications include building integrated PV (BIPV), where the panels are attached to sides of buildings and are incorporated into existing infrastructures. Thin film modules can be up to 90% lighter than silicon modules and therefore are very well suited for vertical building integration, since no significant structural modifications are required. Given the sufficiently greater area of available vertical space compared to rooftop space, this application could contribute significantly to renewable energy initiatives. Some types of thin film PV can also be adjusted in transparency, making them less aesthetically obtrusive and ideally suited for windows.

Other emerging applications belong to the small self-powered electronics and Internet of Things (IoT) sector, which is expected to grow substantially in the coming years as smart electronics become more prevalent in everyday life. These small electronics typically rely on batteries which require replacement every few years at the expense of high material and labor costs. Providing power to these devices using small low-cost PV modules with greater longevity than batteries is a very promising application.

Emerging perovskite PV technology to help drive the thin film market

Perovskite PV has received significant academic and industry attention for its light weight and flexible nature, high manufacturing scalability and significantly lower cost compared to established solar technologies. Perovskite solar cells contain a perovskite active layer which can be deposited as a thin film using solution-based sheet-to-sheet or roll-to-roll compatible processes, making them very attractive from a financial perspective as processing is easily scaled and automated. Along with this, the use of relatively abundant and inexpensive raw materials to synthesize perovskites means that IDTechEx finds perovskite PV to be significantly cheaper than other thin film solar technologies as well as silicon.

As well as fabrication of single junction perovskite solar cells, this technology is also explored for its use in tandem solar cell architectures. All single junction technologies, including established silicon and thin film solar will approach an efficiency plateau. This plateau is expected since there exists a maximum theoretical efficiency limit of 30% for a single junction device. Instead, researchers are exploring the integration of perovskites with other solar technologies in order to achieve much higher power conversion efficiencies. These multi-junction cells possess a much greater theoretical efficiency limit of approximately 43%. The technologies which are receiving significant commercial attention are perovskite/silicon, all-perovskite and perovskite/CIGS tandem PV, with each device posing individual technological advantages.

Perovskite PV has entered early-stage commercialization, with many industry players touting the technology as the "next major solar generation technology". The significant innovation opportunities, rising commercial attention, and consequent predicted growth of the perovskite PV market is a considerable factor helping to revive thin film solar. Current forecasts by IDTechEx, see perovskite PV account for over 40% of all thin film solar installations by 2035.

In this report, IDTechEx further explores the growth drivers for the thin film solar market, as well as analyzing the potential pitfalls to thin film PV adoption. Despite limited market growth thus far, significant ramp up is expected by the end of the decade as the demand for clean and renewable energy continues to grow.

Key Aspects:

Full characterization of the entire thin film photovoltaic market and individual technology outlook

- Detailed analysis and data driven benchmarking of all thin film PV technologies, including dye sensitized solar cells (DSSC), organic solar cells (OPV), perovskite PV, cadmium telluride (CdTe), copper indium gallium selenide (CIGS), gallium arsenide (GaAs), amorphous silicon (a-Si) and copper zinc tin sulfide (CZTS) photovoltaics

In depth analysis of the key material trends for thin film photovoltaic technologies

Assessment of the emerging tandem photovoltaics market

Market analysis throughout

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Report introduction

1.2. What is a solar cell?

1.3. The solar power market growth

1.4. Global renewable and solar energy targets

1.5. What is a thin film solar cell?

1.6. Thin film PV technologies covered in this report

1.7. Benchmarking of thin film PV technologies (i)

1.8. Benchmarking of thin film PV technologies (ii)

1.9. Solar technology development status (TRL)

1.10. Thin film PV company landscape by technology type

1.11. Dye sensitized solar cells overview

1.12. Organic solar cells overview

1.13. Perovskite PV - emerging technology set to revive the thin film solar market

1.14. CdTe PV - dominant thin film technology suffers raw material concerns

1.15. CIGS PV - could the market be under threat

1.16. The future of GaAs PV is unknown

1.17. Amorphous silicon PV has experienced significant market decline

1.18. Tandem PV technologies to boost efficiencies at little extra cost

1.19. Manufacturing thin film PV can be scalable and low-cost

1.20. Cost of photovoltaic technologies

1.21. The applications for thin film PV

1.22. Traditional solar applications - rooftops and solar farms

1.23. Alternative thin film solar applications - Building integration and wireless electronics

1.24. Could thin-film PV market share increase?

1.25. Annual solar installation by type

1.26. Annual thin film PV revenue

1.27. Outlook for the thin-film PV market

1.28. Access More With an IDTechEx Subscription

2. THIN FILM PHOTOVOLTAICS MARKET FORECASTS

2.1. Forecast methodology

2.2. Total annual installed solar capacity

2.3. Total annual thin-film PV installed capacity

2.4. Annual thin-film PV revenue

2.5. Annual thin-film installation by application area

2.6. Annual solar farm installations

2.7. Annual solar farm revenue

2.8. Annual residential rooftop installations

2.9. Annual residential rooftop revenue

2.10. Annual wireless electronics production capacity

2.11. Solar module costs

3. INTRODUCTION

3.1. What is a solar cell?

3.2. The solar power market growth

3.3. Global solar PV investments

3.4. Current solar installations broken down by region

3.5. Global renewable and solar energy targets

3.6. China to remove feed in tariffs

3.7. Research progression in photovoltaic technology

3.8. What is a thin film solar cell?

3.9. Motivation for thin film solar cells

3.10. Key solar cell performance metrics

3.11. Thin film PV technologies covered in this report (i)

3.12. Thin film PV technologies covered in this report (ii)

3.13. The current thin film solar PV market

3.14. Could thin-film PV market share increase?

3.15. Solar technology benchmarking

3.16. Comparison of major thin film technologies

3.17. Solar technology development status

3.18. Thin film PV company landscape

3.19. Cost of PV technologies

3.20. Thin film PV benefits from greater vertical integration

4. EMERGING THIN FILM PHOTOVOLTAIC TECHNOLOGIES

4.1.1. Introduction to emerging thin film PV

4.1.2. Emerging thin film PV technology development status

4.2. Dye sensitized solar cells

4.2.1. Overview of dye sensitized solar cells

4.2.2. Interest into DSSCs

4.2.3. How do DSSCs work?

4.2.4. DSSC photosensitizer properties

4.2.5. DSSC electrolyte

4.2.6. Alternative DSSC electrolyte solutions

4.2.7. DSSC counter electrodes

4.2.8. DSSCs stability

4.2.9. Encapsulation and edge sealing of DSSCs

4.2.10. Development opportunities for DSSCs

4.2.11. Dye sensitized solar cells SWOT

4.2.12. Summary of DSSC technology

4.2.13. Company landscape

4.2.14. Exeger overview

4.2.15. Exeger's Powerfoyle technology applications

4.2.16. Exeger's commercial partnerships

4.2.17. Exeger's commercial partnerships continued

4.2.18. Solaronix overview

4.2.19. GCell by G24 Power overview

4.3. Organic solar cells

4.3.1. Introduction to organic PV

4.3.2. How do organic solar cells work?

4.3.3. Organic solar cell fundamental operation

4.3.4. Advantages and disadvantages of organic PV

4.3.5. Organic solar cell active layers

4.3.6. Organic active layer: Small molecules vs polymers

4.3.7. Non-fullerene acceptors advantages and disadvantages

4.3.8. Tunability of OPV

4.3.9. Brilliant Matter's materials used in world-record large area OPV modules

4.3.10. Current issues to achieving high efficiency large-area modules

4.3.11. OPV material opportunities

4.3.12. Organic PV SWOT

4.3.13. Summary of organic PV

4.3.14. Organic PV company landscape

4.3.15. Brilliant Matters - materials supplier

4.3.16. Brilliant Matters organic PV products

4.3.17. Raynergy Tek - Materials supplier

4.3.18. Raynergy's OPV products

4.3.19. Asca overview

4.3.20. Asca case studies

4.3.21. Asca acquired by Hering group

4.3.22. Epishine overview

4.3.23. Epishine customers and partnerships

4.3.24. Dracula Technologies overview

4.3.25. Dracula Technologies - LAYER OPV technology

4.3.26. Heliatek overview

4.3.27. Heliatek installations

4.3.28. Ribes Tech overview

4.3.29. Sunew overview

4.3.30. Organic PV company benchmarking

4.3.31. Summary of organic PV companies

4.4. Perovskite photovoltaics

4.4.1. What is a perovskite solar cell?

4.4.2. n-i-p vs p-i-n configurations

4.4.3. Scaffolds used in perovskite PV - Mesoporous perovskite solar cells

4.4.4. Manufacturing of perovskite PV

4.4.5. Perovskite stability overview

4.4.6. Extrinsic degradation

4.4.7. Intrinsic degradation mechanisms

4.4.8. Material engineering

4.4.9. Additive engineering

4.4.10. Are lead concerns justified?

4.4.11. Public perception vs reality of lead

4.4.12. Material composition of perovskites influences optics

4.4.13. Hole transport materials (HTM)

4.4.14. Inorganic transport materials

4.4.15. Recent developments within thin-film perovskite PV

4.4.16. SWOT analysis of thin film perovskite PV

4.4.17. Summary - Thin film perovskite PV

4.4.18. Overview of the thin film perovskite PV market

4.4.19. Thin film perovskite PV players overview

4.4.20. Thin film perovskite PV players overview continued

4.4.21. Saule Technologies overview

4.4.22. Microquanta overview

4.4.23. GCL overview

4.4.24. Renshine Solar overview

4.4.25. Perovskite thin-film PV major players summary

4.4.26. Summary of perovskite thin-film major players

4.5. Applications for emerging thin-film photovoltaics

4.5.1. Introduction to the applications for emerging thin-film PV

4.5.2. Current application development stage

4.5.3. How can thin film perovskite overcome the issues related to silicon PV?

4.5.4. Indoor energy harvesting and emerging IoT applications

4.5.5. Companies targeting the IoT and wireless electronics market

4.5.6. Perovskite PV could be cost-effective alternative for wireless energy harvesting

4.5.7. Could thin film PV be used in automotive applications?

4.5.8. Thin-film PV for building integration

4.5.9. Is BIPV a viable application sector?

4.5.10. Thin-film PV for building application

4.5.11. Is perovskite PV a viable option for traditional solar farms?

4.5.12. Summary of the applications for emerging thin-film PV

5. INORGANIC THIN-FILM PHOTOVOLTAICS

5.1.1. Inorganic thin film technologies - alternatives to silicon PV

5.1.2. Inorganic PV development status

5.2. Cadmium Telluride (CdTe) photovoltaics

5.2.1. Introduction to CdTe photovoltaics

5.2.2. CdTe cell function

5.2.3. The alternative CdTe PV structure

5.2.4. CdTe PV buffer layer development

5.2.5. CdTe PV degradation and doping

5.2.6. Manufacturing CdTe solar cells

5.2.7. CdTe PV market share

5.2.8. Toxicity concerns of CdTe PV

5.2.9. Tellurium raw material concerns

5.2.10. Recycling CdTe solar panels

5.2.11. The steps to recycle CdTe modules

5.2.12. CdTe vs Silicon PV

5.2.13. Alternative absorber materials to CdTe

5.2.14. Material opportunities for CdTe PV

5.2.15. CdTe PV SWOT

5.2.16. Summary of CdTe PV technology

5.2.17. The CdTe PV market overview

5.2.18. First Solar overview

5.2.19. First Solar technology and products

5.2.20. First Solar financials

5.2.21. First Solar expanding into the perovskite PV market

5.2.22. Polysolar overview

5.2.23. CTF Solar overview

5.2.24. Toledo Solar - emerging player exits market

5.2.25. Calyxo - bankruptcy history

5.3. Copper Indium Gallium Selenide (CIGS) photovoltaics

5.3.1. Introduction to CIGS PV

5.3.2. How do CIGS solar cells work?

5.3.3. Improving CIGS solar cell efficiency

5.3.4. Advantages and disadvantages of CIGS PV

5.3.5. CIGS vs silicon PV

5.3.6. Flexible CIGS solar cells

5.3.7. Manufacturing CIGS PV modules

5.3.8. The search for simple and low-cost deposition for CIGS PV

5.3.9. CIGS PV technology opportunities

5.3.10. CIGS PV SWOT

5.3.11. Summary of CIGS PV technology

5.3.12. Overview of CIGS PV market players

5.3.13. Midsummer overview

5.3.14. Midsummer partnerships

5.3.15. Midsummer financials

5.3.16. Ascent Solar overview

5.3.17. Ascent Solar financials

5.3.18. Avancis overview

5.3.19. Avancis case studies

5.3.20. Solar Cloth overview

5.3.21. Sunplugged overview

5.3.22. CIGS companies overview

5.3.23. CIGS companies summary

5.4. Gallium arsenide (GaAs) photovoltaics

5.4.1. GaAs PV introduction

5.4.2. GaAs PV operation

5.4.3. Multi-junction GaAs solar cells

5.4.4. Properties of GaAs PV

5.4.5. GaAs PV manufacturing process

5.4.6. GaAs substrate re-use

5.4.7. Alternative GaAs PV manufacturing process

5.4.8. Future of GaAs PV

5.4.9. GaAs innovation opportunities

5.4.10. GaAs PV SWOT

5.4.11. Summary of GaAs PV

5.5. Amorphous silicon (a-Si) photovoltaics

5.5.1. Introduction to amorphous silicon PV

5.5.2. Amorphous silicon PV operation

5.5.3. Deposition of amorphous silicon

5.5.4. Amorphous silicon market share decline

5.5.5. Conventional silicon using amorphous silicon - heterojunction technology

5.5.6. Photovoltaic thermal collectors

5.5.7. Onyx Solar overview

5.5.8. Does amorphous silicon have a future?

5.5.9. Amorphous silicon PV SWOT

5.5.10. Amorphous silicon PV summary

5.6. Copper zinc tin sulfide (CZTS) photovoltaics

5.6.1. Introduction to CZTS PV

5.6.2. CZTS PV operating principles

5.6.3. Cadmium free buffer layers

5.6.4. CZTS solution-based deposition

5.6.5. Selenized CZTS - CZTSSe

5.6.6. CZTS as a hole transport layer - perovskite PV

5.6.7. Recent kesterite solar cell developments

5.6.8. Crystalsol - known company working on CZTS commercialization

5.6.9. CZTS PV SWOT

5.6.10. Summary of CZTS PV

5.7. The applications for inorganic thin-film photovoltaics

5.7.1. Overview of the applications for inorganic thin film PV

5.7.2. Solar farms rely on cheap and high efficiency solar modules

5.7.3. Rooftop application of thin-film PV

5.7.4. BIPV - a more niche application area

5.7.5. Automotive applications for thin-film PV

5.7.6. Agrivoltaics - a relatively novel application area

5.7.7. Summary of the applications for inorganic thin film PV

6. MANUFACTURING THIN FILM PHOTOVOLTAICS

6.1. Deposition techniques for scalable processing

6.2. Sputtering

6.3. Aerosol assisted chemical vapor deposition

6.4. Inkjet printing

6.5. Blade coating

6.6. Slot-die coating

6.7. Spray coating

6.8. Comparison of deposition methods

6.9. How to choose a deposition method

6.10. Roll-to-roll printing - scaling up of production and lowering of costs

6.11. Thin-film PV market use of deposition methods

6.12. Summary of deposition methods

7. MATERIALS FOR THIN FILM PHOTOVOLTAICS

7.1. Introduction - Substrates and encapsulants for thin film PV

7.2. Substrates - conventional and emerging

7.3. Rigid glass substrates

7.4. Alternative substrates to rigid glass

7.5. Flexible glass substrates

7.6. Ultra-thin glass can improve flexibility

7.7. Benefits of ultra-thin glass encapsulation

7.8. Corning Willow flexible glass

7.9. Schott Solar flexible glass

7.10. NEG G-Leaf™ - ultra thin glass

7.11. Plastic substrates

7.12. Plastic substrates require barrier layers

7.13. Metal foil substrates

7.14. Substrate surface roughness

7.15. Substrate material supply opportunities

7.16. Cost comparison of substrate materials

7.17. Benchmarking of substrate materials

7.18. Choosing a substrate material

7.19. Glass-glass encapsulation

7.20. What properties are required for a good optical encapsulant material?

7.21. Polymer encapsulation

7.22. Traditional thin film encapsulation

7.23. Emerging thin film encapsulant - Al2O3

7.24. Ergis noDiffusion® ultra barrier film

7.25. Commercially available flexible encapsulants

7.26. Material opportunities for substrates and encapsulants

7.27. Summary of thin-film PV substrates and encapsulants

8. TANDEM PHOTOVOLTAICS

8.1.1. Introduction to tandem PV

8.1.2. Single junction vs tandem solar cells

8.1.3. Tandem solar cells surpass the theoretical efficiency limits of single junction cells

8.2. Perovskite/silicon tandem photovoltaics

8.2.1. Overview of perovskite on silicon tandem PV

8.2.2. Perovskite/silicon tandem advantages

8.2.3. Perovskite/Si tandem structure and configurations

8.2.4. 2-terminal and 4-terminal tandem cell comparison

8.2.5. Challenges with tandem cell configurations

8.2.6. Interconnection layer for 2-terminal tandem cells

8.2.7. Tandem cell fabrication process

8.2.8. Perovskite/silicon tandem PV roadmap

8.2.9. Perovskite/silicon tandem PV SWOT

8.2.10. Summary of perovskite/silicon tandem PV

8.2.11. Overview of the perovskite/silicon tandem PV market

8.2.12. Major companies targeting both perovskite thin film and perovskite/silicon tandem technology

8.2.13. Overview of the perovskite tandem PV players

8.2.14. Overview of the perovskite tandem PV players

8.3. All-perovskite tandem photovoltaics

8.3.1. All perovskite tandem solar cell technological advancements

8.3.2. Perovskite/perovskite tandem solar cell band gap tuning

8.3.3. Perovskite/perovskite tandem solar cell architectures and manufacturing

8.3.4. Wide band gap perovskite challenges

8.3.5. Use of Sn poses a key challenge

8.3.6. HTL free perovskite solar cells

8.3.7. Carbon-based HTL-free perovskite solar cells

8.3.8. All perovskite tandem solar cells advantages and disadvantages

8.3.9. All perovskite tandem PV SWOT

8.3.10. Summary of all-perovskite tandem PV

8.3.11. Renshine Solar targeting the future commercialization of all-perovskite tandem technology

8.3.12. Energy Materials Corporation - A thin-film perovskite player to target the tandem market

8.4. Other tandem perovskite photovoltaic technologies

8.4.1. Introduction to perovskite/CIGS tandem PV

8.4.2. Perovskite/CIGS tandem PV cell fabrication and structure

8.4.3. Midsummer develops 4-terminal perovskite/CIGS solar cell

8.4.4. First Solar exploring perovskite tandem PV

8.4.5. Perovskite/CIGS tandem PV SWOT

8.4.6. Perovskite/CdTe tandem PV overview

8.4.7. Summary of alternative perovskite tandem PV technologies

8.5. Applications for tandem photovoltaics

8.5.1. Technology choice for different applications

8.5.2. Tandem PV for roof tops

8.5.3. Tandem PV to boost utility solar farm power

8.5.4. Could perovskite/silicon tandem PV be used for windows?

8.5.5. All-perovskite tandem for solar powered vehicles

8.5.6. Summary of the applications for tandem PV

9. COMPANY PROFILES

9.1. Ascent Solar

9.2. Avancis

9.3. Beyond Silicon

9.4. Caelux

9.5. Cosmos Innovation

9.6. Coveme: Photovoltaics

9.7. Crystalsol

9.8. CubicPV

9.9. Dracula Technologies

9.10. Dracula Technologies

9.11. Energy Materials Corporation

9.12. Energy Materials Corporation

9.13. Epishine

9.14. Epishine

9.15. Epishine

9.16. Exeger

9.17. GCL

9.18. GraphEnergyTech

9.19. Hanwha Qcells (Perovskite)

9.20. Heliatek

9.21. Heliatek

9.22. Hiking PV

9.23. Microquanta Semiconductor

9.24. Midsummer

9.25. Onyx Solar

9.26. Opteria

9.27. Oxford PV

9.28. Perovskia Solar

9.29. Polysolar

9.30. Power Roll

9.31. Raynergy Tek: Photovoltaics

9.32. Renshine Solar

9.33. Ribes Tech

9.34. Saule Technologies

9.35. SCHOTT

9.36. Solaronix

9.37. Sunplugged

9.38. Swift Solar

9.39. Tandem PV

9.40. Toledo Solar

9.41. Victrex

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(太陽光)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|