電気自動車用電池セルおよびパック材料 2026-2036:技術動向、市場動向、予測Materials for Electric Vehicle Battery Cells and Packs 2026-2036: Technologies, Markets, Forecasts 電気自動車用バッテリーセルおよびパックのグローバル材料需要。バッテリーエネルギー密度の動向と技術、材料需要とトレンド、OEM戦略、詳細な市場予測。 電気自動車(EV)用電池セルおよび... もっと見る

サマリー

電気自動車用バッテリーセルおよびパックのグローバル材料需要。バッテリーエネルギー密度の動向と技術、材料需要とトレンド、OEM戦略、詳細な市場予測。

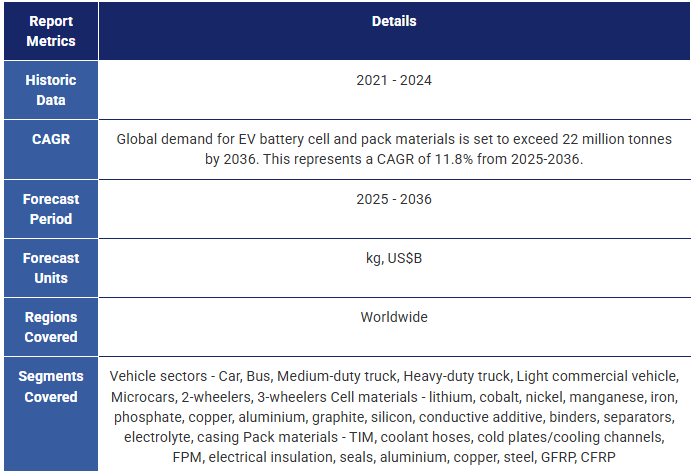

電気自動車(EV)用電池セルおよびパック材料の需要は、2025年から2036年にかけて年平均成長率(CAGR)11.8%で増加し、総需要量は3倍以上に拡大する見込み。この成長は、北米、欧州、中国の3大市場における電動化推進の進展と連動している。 中国は新車販売における電気自動車の割合が2024年と2025年に50%以上を占め、新車販売台数において引き続き先行している。しかし、北米と欧州市場は予測期間中に追い上げると見込まれており、両地域とも電気自動車販売を促進するための低排出規制を導入している。 これらの要因に加え、世界他の地域におけるEVの成長を考慮すると、EV用セルおよびパック材料の総需要は2036年までに2,200万トンに達すると予測される。

規制とサプライチェーンの現地化

電気自動車普及の主要な推進要因、ひいてはEV電池材料市場の成長要因の一つは規制である。例えば中国における電気自動車市場の急速な発展には、税額控除や政府補助金・投資が重要な役割を果たした。一方欧州では、炭素排出規制の段階的強化に焦点が当てられてきた。 EU諸国では2025年より新車1台あたりの平均炭素排出量を15%削減することが義務付けられており、これにより中期的に電気自動車の販売が増加すると予想される。当初は2035年からの内燃機関(ICE)車販売禁止を定めた追加規制が導入される予定だったが、2025年12月時点でこの方針は撤回された。これにより同地域における電気自動車販売の伸びは鈍化する可能性が高い。

一方北米では、米国のインフレ抑制法(IRA)により、米国で使用する新車電気自動車購入に対し最大7500ドルの税額控除が認められていたが、2025年9月をもってこの制度は終了した。 2025年9月以降に購入された車両は、この税額控除の対象外となる。これにより短期的には米国のBEV販売が鈍化する可能性が高いが、長期的な影響は不透明である。

地政学的緊張の高まりにより、一部地域ではサプライチェーンの現地化への注目が高まっている。これにより化学組成の多様化が進み、現地での材料採掘・加工施設の拡大が予想される。これはイノベーションの機会をもたらすとともに、コスト競争力に劣る化学組成が市場で進展する可能性も示唆している。

電池セル材料

セル材料はEV用バッテリーパックの材料需要の70%以上を占め、予測期間中も市場の大部分を構成し続けると見込まれる。 セル材料の需要は化学組成の動向、特に負極と正極の側に大きく依存する。IDTechExは、kWh当たりのコスト低減を理由に、予測期間中にNMCからLFPへの一般的な移行を予測している。一方、NMCのシェア(特に高出力用途や高級車に普及)は、高性能・高エネルギー密度とコバルト価格の上昇により、高ニッケル含有量へと移行する見込みである。 また、負極におけるシリコン含有率の増加傾向も見られ、予測期間の終盤には高性能用途向けの中シリコン負極(20-40%wt)および高シリコン負極(80-90%)の商用化が進む見込みである。負極へのシリコン導入はエネルギー密度の向上を可能とするが、サイクル寿命が制限要因となる可能性がある。

原材料価格は変動が激しく、市場に重大な影響を及ぼす。例えば2022年~2023年のリチウム価格高騰は、電気自動車需要に対するリチウム供給不足が短期的要因となり、電池価格の大幅上昇を招いた。コバルト価格も変動が激しく、2025年に急騰したため、短期的にはNMCの成長に制約が生じる可能性がある。

一方、電解液、添加剤、結合剤、セパレーター、ケーシングは、重要資源への依存度が低く製造方法の改善が進んでいるため、価格がより安定し低下傾向にあります。これらの市場は予測期間中に安定した成長が見込まれます。

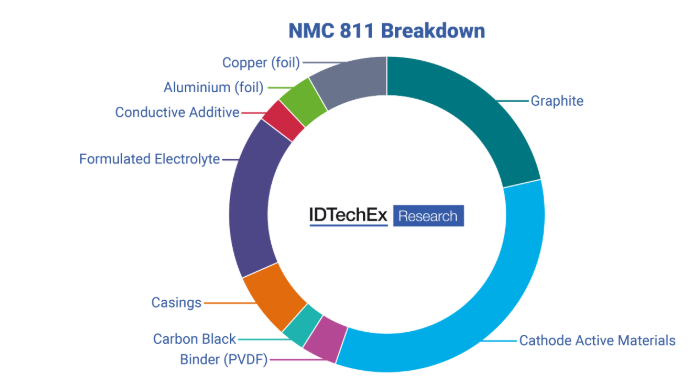

NMC 811内訳。出典:IDTechEx

バッテリーパック材料

電池パック材料は、重量ベースおよび市場価値ベースで全体の材料需要に占める割合は比較的小さいものの、この分野には依然として大きな成長の可能性があります。 重量ベースでは、バッテリーパックハウジングが残りの最大のシェアを占める。アルミニウムと鋼鉄がバッテリーパック筐体の既存技術であるが、軽量化の可能性と機械的・温度絶縁能力から、ガラス繊維強化ポリマー(GFRP)や炭素繊維強化ポリマー(CFRP)などの複合材料の採用が始まっている。

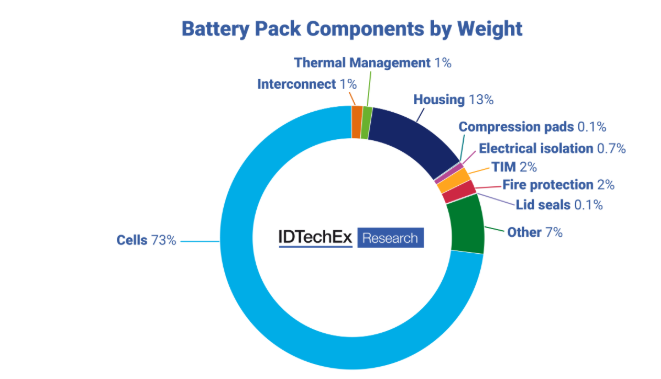

重量別バッテリーパック構成部品。出典:IDTechEx

予測概要

本レポートは、主要市場セクターの販売動向のボトムアップ分析、コスト分析、市場浸透率の適用を通じて作成された、EV用電池セルおよびパック市場向け材料の10年間予測(トン単位の材料需要量および市場価値(米ドル億単位)を含む)を提供する。 本レポートで対象とする材料は、リチウム、コバルト、ニッケル、マンガン、鉄、リン酸塩、銅、アルミニウム、グラファイト、シリコン、導電性添加剤、バインダー、セパレーター、電解質、ケーシング、熱界面材料、冷却ホース、コールドプレート/冷却チャネル、防火材料、電気絶縁体、シール材、アルミニウム、銅、鋼、ガラス繊維強化プラスチック、炭素繊維強化プラスチックである。技術、材料、市場導入状況の内訳を含む。 主要プレイヤーの分析と考察も含まれています。本報告書では、様々な正極材・負極材の比較評価も行っています。

主要な側面

自動車市場の分析:

電池セルの材料動向分析:

バッテリーパックにおける材料トレンド分析:

電池設計の分析:

10年間の市場予測と分析:

目次

1. エグゼクティブサマリー

1.1. EVバッテリー材料市場の主なポイントとIDTechExの解説

1.2. EVバッテリー材料市場の推進要因と機会

1.3. EV市場における地域別政策

1.4. EVバッテリー材料市場における課題 EV用電池材料市場の課題

1.5. 世界のEV販売台数(2011年~2025年第3四半期)

1.6. 本報告書で検討した材料

1.7. 世界の電池化学組成

1.8. BEV向けリチウムイオン電池の正極材料市場シェア(2018-2036年)

1.9. リチウムイオン電池の性能と技術タイムライン

1.10. 材料集約度はどのように変化するか?

1.11. 2021-2036年のカソード材料需要予測(kg)

1.12. アノード材料

1.13. シリコンの将来性

1.14. 2021-2036年のEV向けアノード材料需要予測 (kg)

1.15. 2021-2036 年の EV 向け電池セル材料需要予測 (kg)

1.16. セルフォーマット別市場シェア

1.17. 地域別電気自動車用電池メーカーシェア(GWh)

1.18. EV用電池設計における主な課題の概要

1.19. 材料サプライヤーがOEM向けに持続可能性を改善する方法

1.20. 重量エネルギー密度とセル対パック比率

1.21. 乗用車:パックエネルギー密度の動向

1.22. セル対パックエネルギー密度

1.23. バッテリーパックの構成部品内訳

1.24. パック材料の削減(kg/kWh)

1.25. 熱伝導率のシフト

1.26. バッテリー熱管理戦略の市場シェア

1.27. 複合材料によるエネルギー密度向上

1.28. シーラントの硬化メカニズム

1.29. セルからパックにおける熱暴走

1.30. 防火材料:主要カテゴリー

1.31. 断熱材比較

1.32. EV向けバッテリーパック材料需要予測 2021-2036 (kg)

1.33. 材料別バッテリーセルおよびパック材料総量予測 2021-2036 (kg)

1.34.車種別バッテリーセルおよびパック材料総量予測 2021-2036 (kg)

1.35. 2021-2036年の電池セルおよびパック材料の市場価値予測(米ドル)

1.36. IDTechEx サブスクリプションでさらに詳しく

2. はじめに

2.1. 電気自動車の定義

2.2. ドライブトレインの仕様

2.3. 世界のEV販売台数、2011年~2025年第3四半期

2.4. 地域別概況 - 中国

2.5. 地域別概況 - EU+英国+EFTA

2.6. 地域別概況 - 米国

2.7. 電気自動車向け電池材料

2.8. 本報告書で検討する材料

3. リチウムイオン電池の化学

3.1. リチウムイオン電池とは?

3.2. リチウム電池の化学組成

3.3. なぜリチウムなのか?

3.4. リチウムイオン電池の正極比較

3.5. リチウムイオン電池の負極比較

3.6. 世界の電池化学

3.7. 地域別電気自動車用電池メーカーシェア(GWh)

4. セルコストとエネルギー密度

4.1. 正極別エネルギー密度

4.2. リチウムイオン電池の性能と技術タイムライン

4.3. CAM価格がセル材料コストに与える影響

4.4. NMC 811とLFPの感度分析

4.5. BEV車用電池価格予測

4.6. リチウムイオン電池:技術、市場、寿命終了

5. リチウムイオン電池セル用材料

5.1. 化学組成別正極・負極材料強度

5.1.1. 材料強度の変化要因

5.1.2. 負極材料強度(外装材除く)

5.2. 原材料

5.2.1. リチウムイオン電池に使用される元素

5.2.2. リチウムイオン電池サプライチェーン

5.2.3. 原材料供給が代替化学組成の推進要因か?

5.3. 正極材料

5.3.1. リチウムイオン電池用正極の開発

5.3.2. 正極材料の強度

5.3.3. 正極材料の強度(kg/kWh)

5.3.4. BEV向けリチウムイオン電池における正極の市場シェア(2018-2036年)

5.3.5. 2021-2036年のカソード材料需要予測(kg)

5.3.6. 価格前提

5.3.7. 重要カソード材料の価値予測(2021-2036年、10億米ドル)

5.3.8. リチウム

5.3.9. リチウムの概要

5.3.10. 国別リチウム資源量

5.3.11. 地域別リチウム生産量(原料別)

5.3.12. リチウムとその用途

5.3.13. 国別リチウム生産量

5.3.14. 2020年代のリチウム価格変動

5.3.15. リチウム生産量対需要(kt LCE) 2025-2036

5.3.16. 電気自動車向けリチウム需要予測 2021-2036 (kg)

5.3.17. コバルト

5.3.18. コバルトの概要

5.3.19. コバルトの天然産出地

5.3.20. 国別コバルト生産量 2020-2024

5.3.21. 問題のあるコバルト採掘慣行

5.3.22. コバルト価格の推移

5.3.23. リチウムイオン電池におけるコバルト使用量の変化

5.3.24. 電気自動車向けコバルト需要予測 2021-2036 (kg)

5.3.25. ニッケル

5.3.26. ニッケルの概要

5.3.27. ニッケルは自然界のどこにあるのか?

5.3.28. ニッケル含有鉱物

5.3.29. 国別ニッケル採掘量

5.3.30. 2021-2036年のEV向けニッケル需要予測(kg)

5.4. 負極材料

5.4.1. 負極材料

5.4.2. EV向け負極材料需要予測 2021-2036年 (kg)

5.4.3. 負極材料価格

5.4.4. EV向け負極材料市場規模予測 2021-2036年 (米ドル)

5.4.5. 黒鉛

5.4.6. 黒鉛の概要

5.4.7. 合成黒鉛と天然黒鉛の概要

5.4.8. 電池化学による黒鉛使用量

5.4.9. 地域別黒鉛負極材販売量

5.4.10. EV向け黒鉛需要予測 2021-2036 (kg)

5.4.11. シリコン

5.4.12. シリコンの可能性

5.4.13. シリコン負極の価値提案

5.4.14. シリコン負極材料の課題

5.4.15. シリコン含有量増加に伴うセルエネルギー密度の向上

5.4.16. 商用シリコン負極市場

5.4.17. 現在のシリコン利用状況

5.4.18. シリコンとLFP

5.4.19. EV向けシリコン需要予測 2021-2036年 (kg)

5.5. 電解質、セパレーター、バインダー、導電性添加剤

5.5.1. 電池の構成要素とは?

5.5.2. リチウムイオン電池用電解質の概要

5.5.3. リチウムイオン電池用電解質の開発動向

5.5.4. 地域別電解質市場

5.5.5. セパレータの概要

5.5.6. ポリオレフィン系セパレータ

5.5.7. バインダー

5.5.8. バインダー - 水系 vs 非水系

5.5.9. リチウムイオン電池に添加剤が必要な理由

5.5.10. 導電剤

5.5.11. リチウムイオン電池セル内の集電体

5.5.12. 集電体材料

5.6. 電池セル材料総需要予測

5.6.1. EV向け電池セル材料需要予測 2021-2036年 (kg)

5.6.2. EV向け電池セル材料市場規模予測 2021-2036年 (米ドル)

6. セルおよびパック設計

6.1. セルタイプと課題

6.1.1. セルタイプ

6.1.2. セルフォーマット別市場シェア

6.1.3. リチウムイオン電池:セルからパックへ

6.1.4. パック設計

6.1.5. セルおよびパック設計の変遷

6.1.6. EV バッテリー設計における主な課題の概要

6.2. セル・トゥ・パック、セル・トゥ・シャーシ、および大型セルフォーマット:設計と発表

6.2.1. モジュラーパック設計

6.2.2. セル・トゥ・パックとは?

6.2.3. セル・トゥ・パックの推進要因と課題

6.2.4. セル・トゥ・シャーシ/ボディとは?

6.2.5. 整備・修理とリサイクル性

6.2.6. EU規制とリサイクル性

6.2.7. OEM向け持続可能性向上のための材料サプライヤー手法

6.2.8. BYDブレード式セル・トゥ・パック

6.2.9. BYDセル・トゥ・ボディ

6.2.10. CATLセル・トゥ・パック

6.2.11. CATL CTP 3.0

6.2.12. CATLセル・トゥ・シャーシ

6.2.13. GM Ultium

6.2.14. Leapmotor セル・トゥ・シャーシ

6.2.15. LG モジュール除去

6.2.16. MG セル・トゥ・パック

6.2.17. Nio ハイブリッド化学 セル・トゥ・パック

6.2.18. Our Next Energy: Aries

6.2.19. Stellantis セル・トゥ・パック

6.2.20. SVOLT - ドラゴンアーマーバッテリー

6.2.21. SK On - S-Pack

6.2.22. テスラ セル・トゥ・ボディ

6.2.23. VW セル・トゥ・パック

6.2.24. セル・トゥ・パックとセル・トゥ・ボディ設計のまとめ

6.2.25. 重量エネルギー密度とセル・トゥ・パック比率

6.2.26. 体積エネルギー密度とセル・トゥ・パック比率

6.2.27. セル・トゥ・パック&セル・トゥ・ボディ設計の見通し

6.2.28. 電極・トゥ・パック

6.3. エネルギー密度と材料利用率

6.3.1. 乗用車:パックエネルギー密度(361モデル)

6.3.2. 乗用車:パックエネルギー密度の動向

6.3.3. 乗用車:セルエネルギー密度の動向

6.3.4. セル対パックエネルギー密度

6.3.5. セルおよびパックエネルギー密度の予測 2021-2036 (Wh/kg)

6.3.6. バッテリーパックの構成部品内訳

6.3.7. パック材料の削減 (kg/kWh)

7. パック構成部品

7.1. EVバッテリーパック用熱伝導材料

7.1.1. EV向け熱伝導材料の概要

7.1.2. TIMパックおよびモジュールの概要

7.1.3. TIMの適用 - パックおよびモジュール

7.1.4. セル形状別TIMの適用

7.1.5. EV用TIMの主要特性

7.1.6. EVバッテリーにおけるギャップパッド

7.1.7. ギャップフィラーへの移行

7.1.8. TIMディスペンシングの導入と課題

7.1.9. TIMディスペンシングの課題

7.1.10. EVバッテリーにおける熱伝導性接着剤

7.1.11. 材料オプションと市場比較

7.1.12. TIMの化学的比較

7.1.13. ギャップフィラーから熱伝導性接着剤へ

7.1.14. 熱伝導率の変化

7.1.15. TCAの要件

7.1.16. 車両あたりのTIM需要

7.1.17. EVバッテリー向けTIM予測 2021-2036年 (ktpa)

7.1.18. TIMのその他の用途

7.2.コールドプレートと冷却液ホース

7.2.1.熱システムアーキテクチャ

7.2.2.EVにおける冷却液

7.2.3.EVバッテリー熱管理の概要

7.2.4.OEM別バッテリー熱管理戦略

7.2.5.バッテリー熱管理戦略の市場シェア

7.2.6. セル・トゥ・パック設計における熱管理

7.2.7. セル間ヒートスプレッダーまたは冷却プレート

7.2.8. 先進的なコールドプレート設計

7.2.9. ロールボンディングアルミニウムコールドプレート

7.2.10. コールドプレート設計の事例

7.2.11. Erbslöh Aluminum

7.2.12. ポリマー熱交換器?

7.2.13. グラファイトヒートスプレッダー

7.2.14. 筐体へのコールドプレート統合

7.2.15. コールドプレート供給業者(1)

7.2.16. コールドプレート供給業者(2)

7.2.17. コールドプレート供給業者(3)

7.2.18. EV用冷却ホース

7.2.19. 冷却ホースの材質

7.2.20. ICEとEVの熱システムの相違点

7.2.21. 代替ホース材質 (1)

7.2.22. 代替ホース材料 (2)

7.2.23. 代替ホース材料 (3)

7.2.24. 代替ホース材料 (4)

7.2.25. 代替ホース材料 (5)

7.2.26. 熱管理部品の質量予測 2021-2036 (kg)

7.3. バッテリー筐体

7.3.1. バッテリー筐体材料と競合状況

7.3.2. 鋼鉄からアルミニウムへ

7.3.3. アルミニウムによるさらなる軽量化

7.3.4. 複合材筐体への移行?

7.3.5. 複合材筐体採用EV事例 (1)

7.3.6. 複合材筐体採用EV事例 (2)

7.3.7. 複合材筐体開発プロジェクト(1)

7.3.8. 複合材筐体開発プロジェクト(2)

7.3.9. フェノール樹脂の代替材料

7.3.10. ポリマーは適切な筐体材料か?

7.3.11. Envalior - 高電圧バッテリー用プラスチック筐体

7.3.12. SABIC製プラスチック多用バッテリーパック

7.3.13. 金属に代わるポリマー

7.3.14. SMC 対 RTM/LCM

7.3.15. バッテリートレイおよび蓋用 SMC - LyondellBasell

7.3.16. バッテリー筐体用先進複合材 - INEOS Composites

7.3.17. ポリアミド6ベース筐体

7.3.18. Continental構造用プラスチック - ハニカム技術

7.3.19. 複合材部品 - TRB軽量構造

7.3.20. 防火機能付き複合材

7.3.21. オートノウム - 衝撃保護プレート

7.3.22. その他の複合材筐体材料サプライヤー (1)

7.3.23. その他の複合材筐体材料サプライヤー (2)

7.3.24. COOLBat軽量バッテリー筐体

7.3.25. 複合材筐体向けEMIシールド

7.3.26. 構造用バッテリーの課題

7.3.27. 複合材部品への防火機能追加

7.3.28. バッテリー筐体向け金属フォーム?

7.3.29. 電池筐体材料のまとめ

7.3.30. 複合材料によるエネルギー密度の向上

7.3.31. 複合材料筐体の費用対効果

7.3.32. 電池筐体材料の予測 2021-2036 (kg)

7.4. パック用シーラント

7.4.1. EV 電池筐体のシール方法

7.4.2. EV 電池のシールに関する課題

7.4.3. シーラントの硬化メカニズム

7.4.4. シーリング手法の決定

7.4.5. 各種ディスペンシング材料の選択肢

7.4.6. 主要メーカーと材料

7.4.7. バッテリーシーラントの特性

7.4.8. 射出成形バッテリーシール

7.4.9. バッテリーシーリング用テープ

7.4.10. 電池用シーラントのその他の用途(コールドプレート統合)

7.4.11. 電池用シーラントのその他の用途(テスラ構造パック)

7.4.12. 車両あたりのシーラント使用量

7.4.13. EV電池用シーラント予測 2021-2036年(kg)

7.5. 防火材料

7.5.1. EVにおける熱暴走と火災

7.5.2. バッテリー火災と関連リコール(自動車)

7.5.3. 自動車火災事例:OEMと状況

7.5.4. EV火災とICEの比較(1)

7.5.5. EV火災とICEの比較(2)

7.5.6. EVとICEの火災比較における課題

7.5.7. EV火災の深刻度

7.5.8. EV火災:発生時期は?

7.5.9. 規制の背景

7.5.10. 防火材料とは何か?

7.5.11. セルからパックへの熱暴走

7.5.12. 熱伝導性か断熱性か?

7.5.13. 防火材料:主なカテゴリー

7.5.14. 材料比較

7.5.15. 密度対熱伝導率 - 断熱性

7.5.16. 密度と熱伝導率 - 円筒形セルシステム

7.5.17. 材料市場シェア 2024

7.5.18. 防火材料予測 2021-2036 (kg)

7.5.19. 防火材料

7.6. 圧縮パッド/フォーム

7.6.1. 圧縮パッド/フォーム

7.6.2. ポリウレタン圧縮パッド

7.6.3. 旭化成

7.6.4. フロイデンベルク・シーリング・テクノロジー

7.6.5. ロジャース圧縮パッド

7.6.6. 圧縮と防火 (1)

7.6.7. 圧縮と防火 (2)

7.6.8. サンゴバン

7.6.9. サンゴバン

7.6.10. EV での使用例:フォード マスタング マッハ E

7.6.11. 圧縮パッド/フォームの予測 2021-2036 (kg)

7.7. セルの電気絶縁

7.7.1. セル間の電気的絶縁

7.7.2. 電気絶縁用フィルム

7.7.3. エイブリィ・デニソン - バッテリー用テープ

7.7.4. 誘電体コーティング

7.7.5. 絶縁材料の比較

7.7.6. セル間絶縁フォーム

7.7.7. セル間電気絶縁 2021-2036 年の予測 (kg)

7.8. 電気的相互接続と絶縁

7.8.1. バッテリー相互接続の概要

7.8.2. 相互接続におけるアルミニウム対銅

7.8.3. バスバー絶縁材料

7.8.4. テスラ モデルS P85D

7.8.5. 日産リーフ 24kWh:セル接続

7.8.6. 日産リーフ 24kWh

7.8.7. BMW i3 94Ah

7.8.8. ヒュンダイ E-GMP

7.8.9. VW ID4

7.8.10. テスラ 4680

7.8.11. 電池インターコネクトの材料量:Kg/kWh 概要

7.8.12. 電気的相互接続:アルミニウム、銅、および絶縁材の予測 2021-2036 (kg)

7.9.バッテリーパック材料の予測

7.9.1.EV向けバッテリーパック材料の需要予測 2021-2036 (kg)

7.9.2. バッテリーパック材料の価格想定

7.9.3. EV向けバッテリーパック材料の市場価値予測 2021-2036 (US$)

8. バッテリー材料/構造の例

8.1. 例:自動車

8.1.1. アウディ e-tron

8.1.2. アウディ e-tron GT

8.1.3. BMW i3

8.1.4. BYD Blade

8.1.5. CATL CTP 3.0

8.1.6. Chevrolet Bolt

8.1.7. Faraday Future FF91

8.1.8. Ford Mustang Mach-E/Transit/F150 バッテリー

8.1.9. Honda 0 Series

8.1.10. ヒュンダイ・コナ

8.1.11. ヒュンダイ・E-GMP

8.1.12. ジャガー・I-PACE

8.1.13. キア・EV9 (GMP)

8.1.14. メルセデス・EQS

8.1.15. MG ZS EV

8.1.16. MG Cell-to-pack

8.1.17. ポルシェ タイカン

8.1.18. リマック・テクノロジー

8.1.19. リビアン R1T

8.1.20. テスラ モデル3/Y 円筒形NCA

8.1.21. テスラ モデル3/Y 角形LFP

8.1.22. テスラ モデルS P85D

8.1.23. テスラ モデル S プレイド

8.1.24. テスラ 4680 パック

8.1.25. テスラ サイバートラック

8.1.26. トヨタ プリウス PHEV

8.1.27. トヨタ RAV4 PHEV

8.1.28. VW MEB プラットフォーム

8.2. 例:大型商用車、商用車、その他の車両

8.2.1. Akasol (BorgWarner)

8.2.2. MAN BatteryPack

8.2.3. Microvast & REE

8.2.4. John Deere (Kreisel)

8.2.5. Romeo Power

8.2.6. Superbike Battery Holder

8.2.7. Vertical Aerospace

8.2.8. Voltabox

8.2.9. Xerotech

8.2.10. XING Mobility

8.2.11. XING Mobility Cell-to-pack and Cell-to-chassis

9.予測と前提条件

9.1. EVセルおよびパック用材料:予測対象範囲

9.2. 本レポートで検討した材料

9.3. EV 材料予測:方法論と仮定

9.4. IDTechEx モデルデータベース

9.5. 平均バッテリー容量予測:乗用車、2輪車、3輪車、マイクロカー、バス、バン、トラック

9.6. EVバッテリー需要市場シェア予測(GWh)

9.7. 世界の電池化学

9.8. BEVにおけるリチウムイオン電池の正極市場シェア(2018-2036)

9.9. 2021-2036年の正極材料需要予測(kg)

9.10. 価格前提

9.11. 重要カソード材料の価値予測 2020-2036 (US$B)

9.12. EV向けアノード材料の需要予測 2021-2036 (kg)

9.13. アノード材料の価格

9.14. EV向けアノード材料の市場価値予測 2021-2036 (米ドル)

9.15. EV向け電池セル材料需要予測 2021-2036 (kg)

9.16. EV向け電池セル材料市場価値予測 2021-2036 (米ドル)

9.17. EV向け電池パック材料需要予測 2021-2036 (kg)

9.18. バッテリーパック材料価格の前提条件

9.19. 電気自動車向けバッテリーパック材料市場規模予測 2021-2036年 (米ドル)

9.20. 材料別 バッテリーセル・パック材料総量予測 2021-2036年 (kg)

9.21. 車種別 バッテリーセル・パック材料総量予測 2021-2036年 (kg)

9.22. 2021-2036年の電池セルおよびパック材料の市場価値予測合計(米ドル)

10. 企業プロファイル

10.1. Aerogel Core Ltd

10.2. Ampcera

10.3. 旭化成:電気自動車用バッテリーの防火対策

10.4. Beam Global (AllCell)

10.5. CFP Composites

10.6. Denka:電気自動車用バッテリー防火材料

10.7. DuPont:次世代バッテリー設計向け熱管理材料

10.8. Elven Technologies

10.9. Freudenberg Sealing Technologies:EVセル間防火技術

10.10. FTI Group:電気自動車向け防火ソリューション

10.11. LG Chem

10.12. Lubrizol: 電池用浸漬液

10.13. MAHLE: M3x バッテリーパック

10.14. 三菱化学グループ: 相変化材料

10.15. パーカー:電気自動車用電池材料

10.16. ロジャース・コーポレーション:防火機能付き圧縮パッド

10.17. SABIC:電気自動車用電池用断熱バリア

10.18. サンゴバン:セル間防火フォーム

10.19. SK Enmove:次世代冷媒

10.20. XING Mobility

Summary

Global material demand for electric vehicle battery cells and packs. Battery energy density trends and technologies, material demand and trends, OEM strategies, and granular market forecasts.

Material demand for electric vehicle (EV) battery cell and pack materials is set to grow with a CAGR of 11.8% from 2025-2036, with total material demand more than tripling. This growth is tied to increasing electrification efforts in three primary markets: North America, Europe, and China. China remains ahead of the curve in terms of new electric vehicle sales with more than 50% of new car sales in 2024 and 2025 being battery electric or plug-in hybrid. However, North American and European markets are set to catch up during the forecast period, with both regions instituting low-emission regulation to encourage electric vehicle sales. Considering these factors, alongside EV growth in the rest of the world, total material demand for EV cell and pack materials is set to reach 22 million tonnes by 2036.

Regulation and Supply Chain Localization

One of the major drivers of electric vehicle adoption, and therefore the EV battery materials market, is regulation. Tax credits and government subsidies/investment were significant factors in the rapid development of the electric vehicle market in China, for example. Meanwhile, in Europe the focus has been on gradual increasing of carbon emissions regulations. A 15% cut in average carbon emissions per newly purchased vehicle was mandated in EU countries from 2025, which is expected to increase electric vehicle sales in the medium term. Initially, further regulations would have effectively banned the sale of internal combustion engine (ICE) vehicles from 2035, however as of December 2025, this is no longer the case. It is likely this will slow the growth of electric vehicle sales in the region.

Meanwhile in North America, the US's inflation reduction act (IRA) previously allowed for tax credits of up to US$7500 for new electric vehicle purchases for use in the US, however this is no longer in effect as of September 2025. Vehicles purchased after September 2025 are not eligible for these tax credits. It is likely this will slow US BEV car sales in the short term, though it is unclear if it will have longer term consequences.

Geopolitical tensions have also led to an increasing focus on supply chain localization in some regions. This is likely to result in diversification of chemistries, and expansion of local material extraction and processing facilities. This in turn presents opportunities for innovation and for less cost-competitive chemistries to make headway in the market.

Battery Cell Materials

Cell materials make up more than 70% of material demand for EV battery packs and are expected to continue to comprise the majority of the market over the forecast period. Cell material demand is highly dependent on chemistry trends, especially on the anode and cathode side. IDTechEx predicts a general shift towards LFP over NMC over the forecast period, due to lower costs per kWh, while the NMC share (especially prevalent in high-power applications and luxury cars) will shift towards higher nickel content, due to higher performance and energy density and increasing cobalt prices. There will also be a shift towards higher percentage silicon in anodes, as well as commercialization of mid- (20-40%wt) and high-silicon (80-90%) anodes for high performance applications towards the end of the forecast period. Incorporating silicon into anodes allows for increased energy density, though cycle life can become a limiting factor.

Raw materials prices can be highly volatile and have a significant effect on the market as a result. For example, inflation of lithium prices in 2022 and 2023 led to significantly increased battery prices and resulted from short-term undersupply of lithium compared to demand from electric vehicles. Cobalt prices are also volatile and spiked significantly in 2025, which may place limitations on the growth of NMC in the short-term.

Electrolytes, additives, binders, separators and casing tend to have more stable, decreasing prices as a result of non-reliance on critical materials and improvements to manufacturing methods. These markets are expected to grow stably over the forecast period.

NMC 811 Breakdown. Source: IDTechEx

Battery Pack Materials

Battery pack materials make up a relatively smaller share of the overall material demand by weight and by market value, however, there is still significant potential for growth in this area. Battery pack housing makes up the largest remaining share by weight. Aluminium and steel are the incumbent technologies for battery pack enclosures, however composite materials such as glass-fibre reinforced polymer (GFRP) and carbon fibre reinforced polymer (CFRP) are beginning to see adoption, due to their light-weighting potential and mechanical and temperature insulating capabilities.

Battery Pack Components by Weight. Source: IDTechEx

Forecast Summary

This report offers ten-year forecasts of the materials for EV battery cells and packs market, including material demand by tonne and market value in US$B, produced through a bottom-up analysis of sales trends in major market sectors and application of cost analysis and market penetration trends. The materials covered in this report are lithium, cobalt, nickel, manganese, iron, phosphate, copper, aluminium, graphite, silicon, conductive additive, binder, separator, electrolyte, casing, thermal interface materials, coolant hoses, cold plates/cooling channels, fire protection materials, electrical insulation, seals, aluminium, copper, steel, glass fibre reinforced polymer, carbon fibre reinforced polymer. It includes a breakdown of technologies, materials and market uptake. Player analysis and discussion are also included. The report also benchmarks different cathode and anode materials.

Key Aspects

Analysis of the automotive market:

Analysis of material trends in battery cells:

Analysis of material trends in battery packs:

Analysis of battery design:

10 Year Market Forecasts & Analysis:

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Key EV battery materials market takeaways and IDTechEx commentary

1.2. Drivers and opportunities in the materials for EV batteries market

1.3. Regional policies in the EV market

1.4. Challenges for the materials for EV batteries market

1.5. Global EV sales, 2011 - Q3 2025

1.6. Materials considered in this report

1.7. Global battery chemistry

1.8. Cathode market share for Li-ion in BEVs (2018-2036)

1.9. Li-ion performance and technology timeline

1.10. How does material intensity change?

1.11. Cathode material demand forecast 2021-2036 (kg)

1.12. Anode materials

1.13. The promise of silicon

1.14. Anode material demand forecast for EVs 2021-2036 (kg)

1.15. Battery cell material demand forecast for EVs 2021-2036 (kg)

1.16. Cell format market share

1.17. Electric car battery manufacturer share by region (GWh)

1.18. Major challenges in EV battery design overview

1.19. Methods for materials suppliers to improve sustainability for the OEM

1.20. Gravimetric energy density and cell-to-pack ratio

1.21. Passenger cars: Pack energy density trends

1.22. Cell vs pack energy density

1.23. Component breakdown of a battery pack

1.24. Reduction of pack materials (kg/kWh)

1.25. Thermal conductivity shift

1.26. Battery thermal management strategy market share

1.27. Energy density improvements with composites

1.28. Cure mechanisms for sealants

1.29. Thermal runaway in cell-to-pack

1.30. Fire protection materials: Main categories

1.31. Insulation materials comparison

1.32. Battery pack material demand forecast for EVs 2021-2036 (kg)

1.33. Total battery cell and pack materials forecast by material 2021-2036 (kg)

1.34. Total battery cell and pack materials forecast by vehicle type 2021-2036 (kg)

1.35. Total battery cell and pack materials market value forecast 2021-2036 (US$)

1.36. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. Electric vehicle definitions

2.2. Drivetrain specifications

2.3. Global EV sales, 2011 - Q3 2025

2.4. Regional snapshot - China

2.5. Regional snapshot - EU + UK + EFTA

2.6. Regional snapshot - USA

2.7. Battery materials for electric vehicles

2.8. Materials considered in this report

3. LI-ION BATTERY CHEMISTRY

3.1. What is a Li-ion battery?

3.2. Lithium battery chemistries

3.3. Why lithium?

3.4. Li-ion cathode benchmark

3.5. Li-ion anode benchmark

3.6. Global battery chemistry

3.7. Electric car battery manufacturer share by region (GWh)

4. CELL COSTS AND ENERGY DENSITY

4.1. Energy density by cathode

4.2. Li-ion performance and technology timeline

4.3. Impact of CAM prices on cell material costs

4.4. NMC 811 and LFP sensitivity analyses

4.5. BEV car battery price forecast

4.6. Li-ion batteries: Technologies, markets and end of life

5. MATERIALS FOR LI-ION BATTERY CELLS

5.1. Active and inactive material intensity by chemistry

5.1.1. How does material intensity change?

5.1.2. Inactive material intensities (exc. casings)

5.2. Raw materials

5.2.1. The elements used in Li-ion batteries

5.2.2. The Li-ion supply chain

5.2.3. Raw material supply a driver for alternative chemistries?

5.3. Cathode materials

5.3.1. Li-ion cathode development

5.3.2. Cathode material intensities

5.3.3. Cathode material intensities (kg/kWh)

5.3.4. Cathode market share for Li-ion in BEVs (2018-2036)

5.3.5. Cathode material demand forecast 2021-2036 (kg)

5.3.6. Price assumptions

5.3.7. Critical cathode material value forecast 2021-2036 (US$B)

5.3.8. Lithium

5.3.9. Lithium introduction

5.3.10. Lithium resources by country

5.3.11. Regional lithium production by source

5.3.12. Lithium and its uses

5.3.13. Lithium production by country

5.3.14. Lithium price volatility in the 2020s

5.3.15. Lithium production vs demand (kt LCE) 2025-2036

5.3.16. Lithium demand forecast for EVs 2021-2036 (kg)

5.3.17. Cobalt

5.3.18. Introduction to cobalt

5.3.19. Where can cobalt be found naturally?

5.3.20. Cobalt production by country 2020-2024

5.3.21. Questionable cobalt mining practice

5.3.22. Cobalt price trend

5.3.23. Changing intensity of cobalt in Li-ion

5.3.24. Cobalt demand forecast for EVs 2021-2036 (kg)

5.3.25. Nickel

5.3.26. An overview of nickel

5.3.27. Where is nickel naturally found?

5.3.28. Nickel-bearing minerals

5.3.29. Nickel mining by country

5.3.30. Nickel demand forecast for EVs 2021-2036 (kg)

5.4. Anode materials

5.4.1. Anode materials

5.4.2. Anode material demand forecast for EVs 2021-2036 (kg)

5.4.3. Anode material prices

5.4.4. Anode material market value forecast for EVs 2021-2036 (US$)

5.4.5. Graphite

5.4.6. Introduction to graphite

5.4.7. Synthetic vs natural graphite overview

5.4.8. Graphite intensity by battery chemistry

5.4.9. Graphite anode sales volume by region

5.4.10. Graphite demand forecast for EVs 2021-2036 (kg)

5.4.11. Silicon

5.4.12. The promise of silicon

5.4.13. Value proposition of silicon anodes

5.4.14. The challenges of silicon anode material

5.4.15. Cell energy density increases with silicon content

5.4.16. Commercial silicon anode market

5.4.17. Current silicon use

5.4.18. Silicon and LFP

5.4.19. Silicon demand forecast for EVs 2021-2036 (kg)

5.5. Electrolytes, separators, binders, and conductive additives

5.5.1. What is in a cell?

5.5.2. Introduction to Li-ion electrolytes

5.5.3. Developments in Li-ion electrolytes

5.5.4. Electrolyte market by region

5.5.5. Introduction to separators

5.5.6. Polyolefin separators

5.5.7. Binders

5.5.8. Binders - aqueous vs non-aqueous

5.5.9. Why do Li-ion batteries need additives?

5.5.10. Conductive agents

5.5.11. Current collectors in a Li-ion battery cell

5.5.12. Current collector materials

5.6. Total battery cell materials forecast

5.6.1. Battery cell material demand forecast for EVs 2021-2036 (kg)

5.6.2. Battery cell material market value forecast for EVs 2021-2036 (US$)

6. CELL AND PACK DESIGN

6.1. Cell types and challenges

6.1.1. Cell types

6.1.2. Cell format market share

6.1.3. Li-ion batteries: From cell to pack

6.1.4. Pack design

6.1.5. Shifts in cell and pack design

6.1.6. Major challenges in EV battery design overview

6.2. Cell-to-pack, cell-to-chassis and Large Cell Formats: Designs and Announcements

6.2.1. Modular pack designs

6.2.2. What is cell-to-pack?

6.2.3. Drivers and challenges for cell-to-pack

6.2.4. What is cell-to-chassis/body?

6.2.5. Servicing/repair and recyclability

6.2.6. EU regulations and recyclability

6.2.7. Methods for materials suppliers to improve sustainability for the OEM

6.2.8. BYD blade cell-to-pack

6.2.9. BYD cell-to-body

6.2.10. CATL cell-to-pack

6.2.11. CATL CTP 3.0

6.2.12. CATL cell-to-chassis

6.2.13. GM Ultium

6.2.14. Leapmotor cell-to-chassis

6.2.15. LG removing the module

6.2.16. MG cell-to-pack

6.2.17. Nio hybrid chemistry cell-to-pack

6.2.18. Our Next Energy: Aries

6.2.19. Stellantis cell-to-pack

6.2.20. SVOLT - Dragon Armor Battery

6.2.21. SK On - S-Pack

6.2.22. Tesla cell-to-body

6.2.23. VW cell-to-pack

6.2.24. Cell-to-pack and cell-to-body designs summary

6.2.25. Gravimetric energy density and cell-to-pack ratio

6.2.26. Volumetric energy density and cell-to-pack ratio

6.2.27. Outlook for cell-to-pack & cell-to-body designs

6.2.28. Electrode-to-pack

6.3. Energy density and material utilization

6.3.1. Passenger cars: Pack energy density (361 models)

6.3.2. Passenger cars: Pack energy density trends

6.3.3. Passenger cars: Cell energy density trends

6.3.4. Cell vs pack energy density

6.3.5. Cell and pack energy density forecast 2021-2036 (Wh/kg)

6.3.6. Component breakdown of a battery pack

6.3.7. Reduction of pack materials (kg/kWh)

7. PACK COMPONENTS

7.1. Thermal interface materials for EV battery packs

7.1.1. Introduction to thermal interface materials for EVs

7.1.2. TIM pack and module overview

7.1.3. TIM application - pack and modules

7.1.4. TIM application by cell format

7.1.5. Key properties for TIMs in EVs

7.1.6. Gap pads in EV batteries

7.1.7. Switching to gap fillers from pads

7.1.8. Dispensing TIMs introduction and challenges

7.1.9. Challenges for dispensing TIM

7.1.10. Thermally conductive adhesives in EV batteries

7.1.11. Material options and market comparison

7.1.12. TIM chemistry comparison

7.1.13. Gap filler to thermally conductive adhesives

7.1.14. Thermal conductivity shift

7.1.15. TCA requirements

7.1.16. TIM demand per vehicle

7.1.17. TIM forecast for EV batteries 2021-2036 (ktpa)

7.1.18. Other applications for TIMs

7.2. Cold plates and coolant hoses

7.2.1. Thermal system architecture

7.2.2. Coolant fluids in EVs

7.2.3. Introduction to EV battery thermal management

7.2.4. Battery thermal management strategy by OEM

7.2.5. Battery thermal management strategy market share

7.2.6. Thermal management in cell-to-pack designs

7.2.7. Inter-cell heat spreaders or cooling plates

7.2.8. Advanced cold plate design

7.2.9. Roll bond aluminium cold plates

7.2.10. Examples of cold plate design

7.2.11. Erbslöh Aluminum

7.2.12. Polymer heat exchangers?

7.2.13. Graphite heat spreaders

7.2.14. Integrating the cold plate into the enclosure

7.2.15. Cold plate suppliers (1)

7.2.16. Cold plate suppliers (2)

7.2.17. Cold plate suppliers (3)

7.2.18. Coolant hoses for EVs

7.2.19. Coolant hose material

7.2.20. Differences between ICE and EV thermal systems

7.2.21. Alternate hose materials (1)

7.2.22. Alternate hose materials (2)

7.2.23. Alternate hose materials (3)

7.2.24. Alternate hose materials (4)

7.2.25. Alternate hose materials (5)

7.2.26. Thermal management component mass forecast 2021-2036 (kg)

7.3. Battery enclosures

7.3.1. Battery enclosure materials and competition

7.3.2. From steel to aluminium

7.3.3. Reducing weight further with aluminum

7.3.4. Towards composite enclosures?

7.3.5. Composite enclosure EV examples (1)

7.3.6. Composite enclosure EV examples (2)

7.3.7. Projects for composite enclosure development (1)

7.3.8. Projects for composite enclosure development (2)

7.3.9. Alternatives to phenolic resins

7.3.10. Are polymers suitable housings?

7.3.11. Envalior - plastic enclosure for HV battery

7.3.12. Plastic intensive battery pack from SABIC

7.3.13. Polymers replacing metals

7.3.14. SMC vs RTM/LCM

7.3.15. SMC for battery trays and lids - LyondellBasell

7.3.16. Advanced composites for battery enclosures - INEOS composites

7.3.17. Polyamide 6-based enclosure

7.3.18. Continental structural plastics - honeycomb technology

7.3.19. Composite parts - TRB lightweight structures

7.3.20. Composites with fire protection

7.3.21. Autoneum - impact protection plate

7.3.22. Other composite enclosure material suppliers (1)

7.3.23. Other composite enclosure material suppliers (2)

7.3.24. COOLBat lightweight battery enclosures

7.3.25. EMI shielding for composite enclosures

7.3.26. Challenges with structural batteries

7.3.27. Adding fire protection to composite parts

7.3.28. Metal foams for battery enclosures?

7.3.29. Battery enclosure materials summary

7.3.30. Energy density improvements with composites

7.3.31. Cost effectiveness of composite enclosures

7.3.32. Battery enclosure material forecasts 2021-2036 (kg)

7.4. Pack sealants

7.4.1. How to seal an EV battery enclosure

7.4.2. Challenges with sealing EV batteries

7.4.3. Cure mechanisms for sealants

7.4.4. Determining the sealing approach

7.4.5. A variety of dispensed materials available

7.4.6. Players and materials

7.4.7. Properties of battery sealants

7.4.8. Injection molded battery seals

7.4.9. Tapes for battery sealing

7.4.10. Other areas for battery sealants (cold plate integration)

7.4.11. Other areas for battery sealants (Tesla Structural Pack)

7.4.12. Sealant quantity per vehicle

7.4.13. EV battery sealants forecast 2021-2036 (kg)

7.5. Fire protection materials

7.5.1. Thermal runaway and fires in EVs

7.5.2. Battery fires and related recalls (automotive)

7.5.3. Automotive fire incidents: OEMs and situations

7.5.4. EV fires compared to ICEs (1)

7.5.5. EV fires compared to ICEs (2)

7.5.6. Issues with EV and ICE fire comparisons

7.5.7. Severity of EV fires

7.5.8. EV Fires: When do they happen?

7.5.9. Regulatory background

7.5.10. What are fire protection materials?

7.5.11. Thermal runaway in cell-to-pack

7.5.12. Thermally conductive or thermally insulating?

7.5.13. Fire protection materials: Main categories

7.5.14. Material comparison

7.5.15. Density vs thermal conductivity - thermally insulating

7.5.16. Density vs thermal conductivity - cylindrical cell systems

7.5.17. Material market shares 2024

7.5.18. Fire protection materials forecast 2021-2036 (kg)

7.5.19. Fire protection materials

7.6. Compression pads/foams

7.6.1. Compression pads/foams

7.6.2. Polyurethane compression pads

7.6.3. Asahi Kasei

7.6.4. Freudenberg Sealing Technology

7.6.5. Rogers compression pads

7.6.6. Compression and fire protection (1)

7.6.7. Compression and fire protection (2)

7.6.8. Saint-Gobain

7.6.9. Saint-Gobain

7.6.10. Example use in EVs: Ford Mustang Mach-E

7.6.11. Compression pads/foams forecast 2021-2036 (kg)

7.7. Cell electrical insulation

7.7.1. Inter-cell electrical isolation

7.7.2. Films for electrical insulation

7.7.3. Avery Dennison - tapes for batteries

7.7.4. Dielectric coatings

7.7.5. Insulation materials comparison

7.7.6. Insulating cell-to-cell foams

7.7.7. Inter-cell electric insulation forecast 2021-2036 (kg)

7.8. Electrical interconnects and insulation

7.8.1. Introduction to battery interconnects

7.8.2. Aluminum vs copper for interconnects

7.8.3. Busbar insulation materials

7.8.4. Tesla Model S P85D

7.8.5. Nissan Leaf 24kWh: Cell connection

7.8.6. Nissan Leaf 24kWh

7.8.7. BMW i3 94Ah

7.8.8. Hyundai E-GMP

7.8.9. VW ID4

7.8.10. Tesla 4680

7.8.11. Material quantity in battery interconnects: Kg/kWh summary

7.8.12. Electrical interconnects: Aluminum, copper, and insulation forecast 2021-2036 (kg)

7.9. Battery pack materials forecasts

7.9.1. Battery pack material demand forecast for EVs 2021-2036 (kg)

7.9.2. Battery pack materials price assumptions

7.9.3. Battery pack material market value forecast for EVs 2021-2036 (US$)

8. BATTERY MATERIAL/STRUCTURE EXAMPLES

8.1. Examples: Automotive

8.1.1. Audi e-tron

8.1.2. Audi e-tron GT

8.1.3. BMW i3

8.1.4. BYD Blade

8.1.5. CATL CTP 3.0

8.1.6. Chevrolet Bolt

8.1.7. Faraday Future FF91

8.1.8. Ford Mustang Mach-E/Transit/F150 battery

8.1.9. Honda 0 Series

8.1.10. Hyundai Kona

8.1.11. Hyundai E-GMP

8.1.12. Jaguar I-PACE

8.1.13. Kia EV9 (GMP)

8.1.14. Mercedes EQS

8.1.15. MG ZS EV

8.1.16. MG Cell-to-pack

8.1.17. Porsche Taycan

8.1.18. Rimac Technology

8.1.19. Rivian R1T

8.1.20. Tesla Model 3/Y Cylindrical NCA

8.1.21. Tesla Model 3/Y Prismatic LFP

8.1.22. Tesla Model S P85D

8.1.23. Tesla Model S Plaid

8.1.24. Tesla 4680 Pack

8.1.25. Tesla Cybertruck

8.1.26. Toyota Prius PHEV

8.1.27. Toyota RAV4 PHEV

8.1.28. VW MEB Platform

8.2. Examples: Heavy duty, commercial vehicles, and other vehicles

8.2.1. Akasol (BorgWarner)

8.2.2. MAN BatteryPack

8.2.3. Microvast & REE

8.2.4. John Deere (Kreisel)

8.2.5. Romeo Power

8.2.6. Superbike Battery Holder

8.2.7. Vertical Aerospace

8.2.8. Voltabox

8.2.9. Xerotech

8.2.10. XING Mobility

8.2.11. XING Mobility Cell-to-pack and Cell-to-chassis

9. FORECASTS AND ASSUMPTIONS

9.1. Materials for EV cells and packs: Forecast coverage

9.2. Materials considered in this report

9.3. EV materials forecast: Methodology & assumptions

9.4. IDTechEx model database

9.5. Average battery capacity forecast: Car, 2W, 3W, microcar, bus, van, and truck

9.6. EV battery demand market share forecast (GWh)

9.7. Global battery chemistry

9.8. Cathode market share for Li-ion in BEVs (2018-2036)

9.9. Cathode material demand forecast 2021-2036 (kg)

9.10. Price assumptions

9.11. Critical cathode material value forecast 2020-2036 (US$B)

9.12. Anode material demand forecast for EVs 2021-2036 (kg)

9.13. Anode material prices

9.14. Anode material market value forecast for EVs 2021-2036 (US$)

9.15. Battery cell material demand forecast for EVs 2021-2036 (kg)

9.16. Battery cell material market value forecast for EVs 2021-2036 (US$)

9.17. Battery pack material demand forecast for EVs 2021-2036 (kg)

9.18. Battery pack materials price assumptions

9.19. Battery pack material market value forecast for EVs 2021-2036 (US$)

9.20. Total battery cell and pack materials forecast by material 2021-2036 (kg)

9.21. Total battery cell and pack materials forecast by vehicle type 2021-2036 (kg)

9.22. Total battery cell and pack materials market value forecast 2021-2036 (US$)

10. COMPANY PROFILES

10.1. Aerogel Core Ltd

10.2. Ampcera

10.3. Asahi Kasei: Fire Protection for Electric Vehicle Batteries

10.4. Beam Global (AllCell)

10.5. CFP Composites

10.6. Denka: Fire Protection Materials for Electric Vehicle Batteries

10.7. DuPont: Thermal Materials for Future Battery Designs

10.8. Elven Technologies

10.9. Freudenberg Sealing Technologies: EV Inter-Cell Fire Protection

10.10. FTI Group: Fire Protection for Electric Vehicles

10.11. LG Chem

10.12. Lubrizol: Immersion Fluids for Batteries

10.13. MAHLE: M3x Battery Pack

10.14. Mitsubishi Chemical Group: Phase Change Materials

10.15. Parker: Electric Vehicle Battery Materials

10.16. Rogers Corporation: Compression Pads With Fire Protection

10.17. SABIC: Electric Vehicle Battery Thermal Barriers

10.18. Saint-Gobain: Inter-cell fire protection foams

10.19. SK Enmove: Next Gen Refrigerants

10.20. XING Mobility

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポートIDTechEx社の 自動車 - Electric Vehicles分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|