バイオマニュファクチャリング特殊化学品 2026-2036年:技術、市場、プレーヤー、予測Biomanufacturing Specialty Chemicals 2026-2036: Technologies, Markets, Players, Forecasts 食品、化粧品、顔料、酵素にわたる特殊化学品の工業的バイオ製造。発酵ベースの生産合成生物学における技術ベンチマークとトレンド。市場展望、プレーヤー、10年予測。 スペシャリティ・ケミ... もっと見る

サマリー

食品、化粧品、顔料、酵素にわたる特殊化学品の工業的バイオ製造。発酵ベースの生産合成生物学における技術ベンチマークとトレンド。市場展望、プレーヤー、10年予測。

スペシャリティ・ケミカルは、高度な食品処方や化粧品活性剤から工業用触媒や機能性コーティングに至るまで、幅広い高性能製品を支えている。汎用化学品とは異なり、スペシャリティ・ケミカルは量ではなく、正確な機能を提供し、厳しい規制要件を満たし、一貫した純度と性能を達成する能力によって定義される。配合のわずかな変化でさえ、製品の市場での成否を左右するため、その製造は化学産業において技術的に要求が高く、戦略的に重要な分野となっている。

微生物、酵素、生体触媒プロセスの工業的応用であるホワイト・バイオテクノロジーは、これらの化学物質をより持続的に製造するための強力なルートを提供する。再生可能な原料と精密なバイオプロセスを用いることで、石油化学的ルートでは合成が困難な複雑な分子や不斉分子にアクセスし、温室効果ガスの排出を削減し、有害な副産物を最小限に抑えることができる。合成生物学、菌株の最適化、代替原料利用の進歩により、現在、バイオ製造が経済的に実行可能な特殊化学品の種類が増えつつあり、技術革新と市場差別化の新たな機会が開かれている。

特殊化学品は、汎用化学品よりも生産量が少なく、性能、純度、厳格な技術基準や規制基準への準拠に基づいて販売される。特殊化学品には、食品、化粧品、工業用途の機能性原料が含まれ、配合のわずかな変更が製品の成功を左右することがある。燃料、プラスチック、基礎化学品などのバルク製品とは対照的に、特殊化学品は狭い市場に対応し、高い利幅を要求し、より複雑で精密な製造方法を正当化することができる。

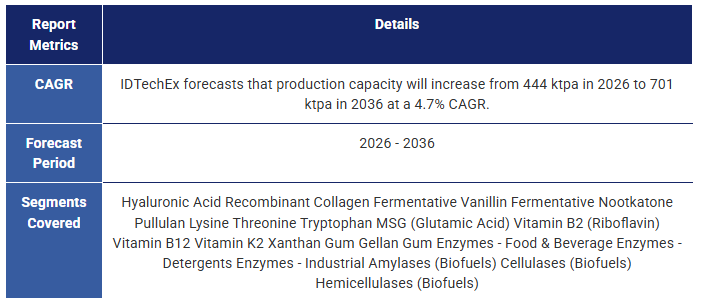

ホワイトバイオテクノロジーはこの分野に適している。微生物発酵や酵素合成は、分子精度を高め、複雑な構造やキラル構造にアクセスし、石油化学的な方法では入手が困難でコストがかかる生物学的同一化合物や新規化合物を可能にする。これらのプロセスはまた、再生可能な原料を使用し、排出物や有害な副産物の発生が少ないという持続可能性の利点もある。IDTechExでは、このセクターの生産能力は444kt/年から701kt/年に成長し、年平均成長率は4.7%になると予測している。この成長を支えているのは、合成生物学の進歩、プロセスの最適化、代替原料の採用であり、これらすべてが性能と経済性の両方を向上させている。

IDTechExのレポート「特殊化学品のバイオ製造 2026-2036年」は、食品添加物、化粧品・パーソナルケア成分、顔料、酵素に焦点を当て、特殊化学品の製造におけるホワイトバイオテクノロジーの役割を調査している。酵素については、バイオエネルギーから脱炭素、リサイクルに至るまで、いくつかの産業用途をカバーしている。本レポートでは、製造方法、技術的な利点、商業的な課題、開発に積極的な企業について批判的に分析している。また、この分野の将来を形成する実現技術、市場促進要因、競争力学についても考察しています。

ホワイトバイオテクノロジーとは?

バイオ経済とは、農業、漁業、林業から得られる再生可能な生物資源を利用して、食料、材料、化学物質、エネルギーを生産する経済システムのことである。このシステムの中で、工業的バイオ製造と呼ばれることもあるホワイト・バイオテクノロジーは、工業的規模での化学物質や材料の持続可能な生産を可能にする上で、極めて重要な役割を果たしている。ホワイト・バイオテクノロジーは、農業におけるグリーン・バイオテクノロジーやヘルスケアにおけるレッド・バイオテクノロジーなど、バイオテクノロジーの他の「色」と並んで位置づけられるが、化石燃料への依存を減らし、新たな分子の可能性を可能にすることによって、化学物質生産を変革する独自の立場にある。

ホワイト・バイオテクノロジーは、洗剤の細菌酵素から発酵由来の食品添加物まで、何十年も前から利用されてきたが、特殊化学品への応用は急速に拡大している。合成生物学、菌株の最適化、原料の多様化などの進歩により、より小規模で高価値な市場での競争力が高まっている。同時に、規制の変更、企業の持続可能性へのコミットメント、バイオベース製品に対する消費者の需要により、バイオベース製品の採用に有利な条件が整いつつある。

なぜ特殊化学品なのか?

特殊化学品は、魅力的な利幅と、バイオ製造が十分に対応できる技術的要件を兼ね備えているため、ホワイト・バイオテクノロジーにとって戦略的成長分野となっている。これらの製品の多くは、市場が確立されているものの、持続可能性の圧力、調達の制約、コストの変動に直面するサプライチェーンに依存している。また、既存の生産ルートが非効率的であったり、拡張性に乏しいニッチ原料もある。

バイオマニュファクチャリング能力を開発している企業にとって、特殊市場は、小規模で製品を商品化しながらも実行可能な価格設定を実現する機会を提供する。このような市場は、新しい菌株、原料、プロセス技術のための実験場として機能し、その教訓を後に大量生産市場に応用することができる。CHEMUK 2025における産業界の議論では、持続可能な技術のスケーリングと、実験室での技術革新と商業展開のギャップを埋めるための自動化の統合に焦点が当てられ、この軌跡が強調された。重要なメッセージは、スペシャリティケミカルは、技術的実現可能性、商業的実現可能性、持続可能性へのコミットメントが収束する実験場としての役割を果たし続けるということであった。加えて、特殊化学品市場は細分化されているため、小規模な生産者であっても、大量生産で大手化学品メーカーとすぐに正面から競争することなく、競争力を確立することができる。

特殊化学品分野でのバイオ製造の推進

特殊化学品分野は、合成生物学の急速な進歩の恩恵を受けており、これにより収率、安定性、特異性が向上した人工バイオ触媒が実現しつつある。リグノセルロース系バイオマス、廃ガス、農業副産物などの代替原料が、新たな生産経路を生み出している。新規の生体触媒は利用可能な分子の範囲を拡大し、カーボンニュートラルやカーボンネガティブの生産ルートは、より広範な脱炭素化への取り組みの一環として出現している。無細胞システムは、全細胞発酵の制限を受けずに高価値分子を生産することを可能にしている。菌株の最適化と代謝工学の進歩により、生産性が向上し、下流の処理コストが削減されつつある。これらの技術トレンドが相まって、特殊市場に新たな機会が開かれ、以前は技術的にも経済的にも実現不可能であった製品が可能になりつつある。IDTechExのレポートでは、こうした進歩を分析し、特殊化学品向けバイオ製造の未来を形成している技術、企業、ケーススタディを紹介している。

市場の原動力、課題、経済的実現可能性

消費者の嗜好、ブランドへのこだわり、特に食品と化粧品における規制強化により、持続可能なバイオベースの代替品への需要が高まっている。しかし、経済性は依然として決定的な要因である。プロセスの歩留まり、スケールアップの容易さ、バイオ触媒の選択といった内的要因は、プロジェクトが商業的に成功するかどうかを決定する可能性があり、一方、外的要因としては、石油価格の変動、規制の枠組み、グリーン・プレミアムを支払う顧客の意欲などが挙げられる。生産者はまた、精密細胞工場の開発とスケールアップにかかる高いコスト、改質が必要な場合の採用の遅れ、規制当局の承認プロセスの長さ、複数のニッチ用途に関与する必要のある断片的な市場にも直面している。本レポートでは、バイオ製造のスケールアップに成功した事例と失敗した事例の両方を紹介しながら、企業がこれらの障壁にどのように対処しているかを検証する。

用途と市場展望

IDTechExは主要な特殊分子のプロフィールを詳細に記載し、それぞれについて製造プロセスと主要なバイオ触媒、石油化学的または抽出された同等品に対する技術的優位性、現在の課題、川下用途、技術準備レベルについて説明している。各プロフィールには、2036年までの市場展望とともに、活発な生産者とその生産能力も掲載されている。10年予測では、生産能力、採用の可能性、技術準備に基づき、主要分子グループごとに市場を区分している。

本レポートの対象範囲

このIDTechExレポートは、ホワイトバイオテクノロジーの特殊化学品セグメントに焦点を当てています。対象には、ビタミン、アミノ酸、香料、フレーバーエンハンサー、ゲル化剤、特殊酸などの食品添加物が含まれる。また、生物活性化合物、天然香料、機能性添加物などの化粧品およびパーソナルケア成分についても調査しています。また、天然色素から高価なバイオ由来染料までの顔料や、バイオエネルギーから脱炭素、リサイクルまでの産業用途の酵素も取り上げています。

燃料、プラスチック、その他の汎用化学品については、関連レポート「ホワイト・バイオテクノロジー2025-2035」で取り上げており、本レポートでは文脈を説明するためにのみ記載している。

本レポートは、食品、化粧品、顔料、酵素にわたるバイオ製造特殊化学品に関する重要な市場情報を提供する。以下の内容が含まれる

目次1.要旨

1.1.バイオテクノロジーの色

1.2.ホワイト・バイオテクノロジーとは何か?

1.3.白色バイオテクノロジー特殊化学品2026-2036年:スコープ

1.4.白色バイオテクノロジーの動向と推進要因(1)

1.5.ホワイトバイオテクノロジーの動向と推進要因(2)

1.6.ホワイトバイオテクノロジーに応用される合成生物学

1.7.ホワイトバイオテクノロジーの技術動向

1.8.ホワイトバイオテクノロジーの代替原料の概要

1.9.ホワイトバイオテクノロジーに関する主な市場課題

1.10.ホワイトバイオテクノロジーが直面する技術的課題

1.11.ホワイトバイオテクノロジーから得られる製品:概要

1.12.工業的バイオ製造によって生産できる分子カテゴリー

1.13.ホワイトバイオテクノロジーにおける企業状況

1.14.バイオ製造の香料と芳香剤:新興企業の状況

1.15.その他の新興バイオ製造美容製品とその現状

1.16.技術成熟度(TRL):美容製品

1.17.技術準備完了レベル(TRL):美容製品

1.18.バイオ界面活性剤:企業ランドスケープ

1.19.バイオエネルギー酵素の技術的課題と機会

1.20.技術成熟度(TRL):バイオエネルギー用途の酵素

1.21.耐熱性酵素のコストパフォーマンス指標

1.22.バイオエネルギーにおける酵素応用の技術準備レベル

1.23.CO2回収と変換のための選択された酵素的アプローチ

1.24.バイオ製造特殊化学品2026~2036年全体市場

1.25.汎用化学品向けホワイトバイオテクノロジー 2025-2035年

1.26.IDTechEx サブスクリプションでさらにアクセス

2.序論

2.1.特殊化学品

2.2.バイオテクノロジーの色

2.3.ホワイトバイオテクノロジーとは?

2.4.バイオエコノミーとホワイトバイオテクノロジー

2.5.ホワイトバイオテクノロジー特殊化学品2026-2036年:範囲

2.6.ホワイトバイオテクノロジー由来の製品概要

2.7.工業的バイオ製造によって生産できる分子

2.8.工業的バイオ製造によって生産できる分子

2.9.工業的バイオ製造によって生産できる分子

2.10.工業的バイオ製造によって生産できる分子

2.11.ホワイトバイオテクノロジーにおける企業展望

2.12.ホワイトバイオテクノロジーにおける企業展望

2.13.ホワイトバイオテクノロジーの動向と推進要因(1)

2.14.ホワイトバイオテクノロジーの動向と推進要因(2)

3.市場分析

3.1.ホワイトバイオテクノロジーの市場促進要因

3.1.1.市場促進要因:バイオベース製品に対する需要

3.1.2.市場促進要因バイオテクノロジーに対する政府の支援

3.1.3.市場促進要因炭素税

3.2.ホワイトバイオテクノロジーの経済的実行可能性

3.2.1.ホワイト・バイオテクノロジー・プロジェクトの経済的実行可能性に影響を与える要因

3.2.2.ブレント原油価格がバイオベース製品に及ぼす影響

3.2.3.グリーン・プレミアム

3.2.4.原料価格の上昇

3.2.5.セル工場のコストへの影響

3.2.6.スケールアップがコストに与える影響

3.2.7.ザイマーゲン社:合成生物学の経済性に関するケーススタディ

3.2.8.ケーススタディ:ランザテック

3.2.9.ケーススタディソラザイム社

3.2.10.合成生物学:汎用製品から少量高価値市場へのシフト

3.2.11.ホワイトバイオテクノロジーにとっての主な市場課題

4.ホワイトバイオテクノロジー用細胞工場

4.1.1.バイオ製造のための細胞工場:考慮すべき要因

4.1.2.バイオ製造のための細胞工場:様々な生物(1)

4.1.3.バイオマニュファクチャリングのための細胞工場:様々な生物

4.1.4.大腸菌(E.coli)

4.1.5.コリネバクテリウム・グルタミカム(C. glutamicum)

4.1.6.枯草菌(B. subtilis)

4.1.7.サッカロマイセス・セレビシエ(S. cerevisiae)

4.1.8.ヤロウィア・リポリティカ(Y. lipolytica)

4.1.9.様々なバイオ製造プロセスで使用される微生物

4.1.10.白色バイオテクノロジーの非モデル生物

5.技術開発

5.1.合成生物学

5.1.1.合成生物学:生物システムの設計と工学

5.1.2.合成生物学:セントラルドグマの操作

5.1.3.合成生物学の広大な範囲

5.1.4.合成生物学のプロセス:設計、構築、試験

5.1.5.合成生物学:なぜ今なのか

5.1.6.合成生物学:医薬品から消費者製品へ

5.1.7.合成生物学:既存のサプライチェーンを破壊する

5.1.8.合成生物学:導入の推進要因と障壁

5.1.9.ホワイトバイオテクノロジーに応用される合成生物学

5.2.合成生物学のツールと技術

5.2.1.合成生物学のツールと技術概要

5.2.2.DNA合成

5.2.3.CRISPR-Cas9の紹介

5.2.4.CRISPR-Cas9:細菌の免疫システム

5.2.5.合成生物学におけるCRISPR-Cas9の重要性

5.2.6.タンパク質/酵素工学

5.2.7.コンピュータ支援設計

5.2.8.工業的応用における工学的タンパク質の商業的例

5.2.9.株の構築と最適化

5.2.10.合成生物学と代謝工学の相乗効果

5.2.11.産業用微生物株開発のフレームワーク

5.2.12.規模の問題

5.2.13.無細胞システムの紹介

5.2.14.無細胞系と細胞系システム

5.2.15.ホワイトバイオテクノロジーにおける無細胞システム

5.2.16.ホワイトバイオテクノロジーにおける無細胞システム

5.2.17.無細胞システムの商業的導入:Solugen

5.2.18.ホワイトバイオのための無細胞システムを追求する新興企業(1/2)

5.2.19.ホワイトバイオのための無細胞システムを追求する新興企業(2/2)

5.2.20.ホワイトバイオテクノロジーにおける固定化酵素

5.2.21.ホワイトバイオテクノロジーにおける固定化触媒

5.2.22.ロボット工学:ハンズフリーでハイスループットの科学を可能にする

5.2.23.ロボットによるクラウドラボラトリー

5.2.24.生物設計の自動化とループの閉鎖

5.2.25.人工知能と機械学習

5.2.26.機械学習によるde novoタンパク質予測

5.2.27.バイオ製造における機械学習による改善の概要

5.2.28.AI主導の発酵プラットフォーム企業

5.3.バイオ製造プロセスの改善

5.3.1.連続バイオ製造とバッチバイオ製造

5.3.2.連続バイオ製造の利点と課題

5.3.3.連続バイオ製造とバッチバイオ製造:主要発酵パラメーターの比較

5.3.4.機械学習によるバイオ製造プロセスの改善

5.3.5.下流工程(DSP)の改善(1)

5.3.6.ダウンストリームプロセッシング(DSP)の改善(2)

5.3.7.灌流バイオリアクター

5.3.8.下流バイオプロセスにおけるタンジェンシャルフローろ過(TFF)

5.3.9.バイオテクノロジーと化学のハイブリッドアプローチ

5.3.10.プロセス集約化と高セル密度発酵

5.4.持続可能性のためのホワイトバイオテクノロジー

5.4.1.持続可能な技術としてのホワイトバイオテクノロジー

5.4.2.ホワイトバイオテクノロジーにおける炭素捕獲のルート

5.4.3.バイオ製造による炭素回収のための独立栄養細菌

5.4.4. 5.バイオ製造のための5つの代替原料

5.4.5.なぜホワイトバイオテクノロジーに代替原料を使うのか?

5.4.6.食糧、土地、水の競合

5.4.7.C1原料:代謝経路

5.4.8.C1原料:経済的利益

5.4.9.C1原料:経済的利益

5.4.9:課題

5.4.10.メタン以外のC1原料

5.4.11.C1原料製品

5.4.12.C1原料ガス発酵

5.4.13.C2原料

5.4.14.C2原料原料別に区分された製品

5.4.15.C1およびC2原料商業活動

5.4.16.C1およびC2原料:商業活動

5.4.17.リグノセルロース系バイオマス原料

5.4.18.リグノセルロース系バイオマス原料:課題

5.4.19.リグノセルロース系バイオマス原料:課題

5.4.20.リグノセルロース系バイオマス原料製品

5.4.21.リグノセルロース系バイオマス原料:製品

5.4.22.リグノセルロース系バイオマス原料:商業活動

6.ブルーバイオテクノロジー

6.1.ブルーバイオテクノロジーとは何か

6.2.ブルーバイオテクノロジーの主な生体触媒:シアノバクテリアと藻類

6.3.シアノバクテリア

6.4.藻類

6.5.ブルーバイオテクノロジーの主要推進要因と課題

6.6.ブルー・バイオテクノロジーにおける主な新興企業

7.ホワイトバイオテクノロジー由来の製品

7.1.1.ホワイトバイオテクノロジー由来の製品:概要

7.2.化粧品用バイオ製造製品

7.2.1.美容分野におけるバイオ製造

7.2.2.既存の美容成分サプライチェーン(1)

7.2.3.既存の美容成分サプライチェーン(2)

7.2.4.美容成分サプライチェーンの既存企業(1)

7.2.5.美容成分サプライチェーンの既存企業の状況(2)

7.2.6.バイオ製造美容成分サプライチェーンと加工

7.2.7.確立されたバイオテクノロジー由来の美容成分

7.2.8.新興バイオテクノロジー由来美容成分

7.2.9.バイオ製造美容成分セクターの課題

7.2.10.香料と芳香族化合物

7.2.11.フレグランスと芳香族化合物の概要

7.2.12.フレグランスと芳香族化合物

7.2.13.バイオ製造の香料と芳香族化合物新興企業の動向

7.2.14.バイオ製造の香料と芳香族化合物新興企業の展望

7.2.15.フレグランスと芳香化合物企業の概況(1)

7.2.16.フレグランスと芳香族化合物企業動向(2)

7.2.17.バイオテクノロジー由来のフレグランス前駆体

7.2.18.アンブロキサン

7.2.19.化粧品用バイオサーファクタント

7.2.20.バイオ界面活性剤:SLSとSLESのマイルドで生分解性の代替品(1)

7.2.21.バイオサーファクタント:SLSとSLESのマイルドで生分解性の代替品(2)

7.2.22.バイオサーファクタント:企業の概況(1)

7.2.23.バイオサーファクタント企業の概況(2)

7.2.24.バイオ製造界面活性剤企業の概況

7.2.25.界面活性剤:ホワイトバイオテクノロジーにおける機能的役割と市場の重要性

7.2.26.ラムノリピッド

7.2.27.ソホロリピッド

7.2.28.マンノシルエリスリトール脂質(MEL)

7.2.29.セロビオース脂質

7.2.30.合成生物学によるデザイナー糖脂質とリポペプチド

7.2.31.多糖類ベースの両親媒性物質

7.2.32.白色バイオテクノロジー界面活性剤の商業的展望

7.2.33.ヒアルロン酸

7.2.34.ヒアルロン酸:保湿のための発酵ベースの生産

7.2.35.ヒアルロン酸保湿のための発酵生産(2)

7.2.36.バイオテクノロジー由来ヒアルロン酸製剤の機能主導型カスタマイズ

7.2.37.バイオテクノロジー由来ヒアルロン酸製剤の機能主導型カスタマイズ

7.2.38.ヒアルロン酸技術:機能と主要プレーヤー

7.2.39.ヒアルロン酸カンパニーランドスケープ(1)

7.2.40.ヒアルロン酸カンパニーランドスケープ(2)

7.2.41.ヒアルロン酸

7.2.42.エモリエント成分

7.2.43.スクワレンとスクワラン:サメ肝油に代わるホワイトバイオテクノロジー

7.2.44.スクワレンとスクワラン:サメ肝油に代わるバイオテクノロジー製品

7.2.45.スクアレン

7.2.46.スクアレンとスクアラン:会社の概況

7.2.47.スクアレンとスクアラン企業の概況

7.2.48.コラーゲン

7.2.49.スキンケア製品とパーソナルケア製品に含まれるコラーゲン

7.2.50.スキンケア製品とパーソナルケア製品に含まれるコラーゲン

7.2.51.コラーゲンカンパニーランドスケープ

7.2.52.コラーゲンカンパニーランドスケープ(2)

7.2.53.コラーゲン企業の概況

7.2.54.ネイティブ、加水分解、リコンビナントコラーゲン構造の比較

7.2.55.天然、加水分解、組み換えコラーゲン構造の比較

7.2.56.生理活性を高めた人工コラーゲン誘導体

7.2.57.コラーゲン(ゲルトールなど)

7.2.58.色素

7.2.59.バイオベースのUVフィルターおよび光保護化合物

7.2.60.メラニン

7.2.61.インディゴイジン

7.2.62.ケーススタディOneSkin - OS 01セノセラピーペプチド

7.2.63.市場分析とベンチマーキング

7.2.64.バイオ製造美容成分生産能力

7.2.65.バイオ製造品と従来品の比較(1)

7.2.66.バイオ製造製品と従来製品の比較(2)

7.2.67.従来の調達とバイオ製造の比較(1)

7.2.68.従来の調達とバイオ製造の比較(2)

7.2.69.バイオ原料の測定基準の比較

7.2.70.バイオ原料の評価指標の比較(2)

7.2.71.バイオテクノロジー原料の比較指標 - IDTechExのフレームワーク(その1)

7.2.72.バイオ原料の比較指標-IDTechExのフレームワーク(その2)

7.2.73.バイオ製造美容成分の展望

7.2.74.美容分野におけるバイオ製造の一般的課題

7.2.75.その他の新興バイオ製造美容製品と現状

7.2.76.その他の新興バイオ製造美容製品と現状

7.2.77.技術準備レベル(TRL):美容製品

7.2.78.技術準備完了レベル(TRL):美容製品

7.2.79.バイオ製造成分と従来の代替品との比較

7.2.80.バイオ製造原料と従来の代替品との比較

7.3.バイオ製造食品添加物

7.3.1.ビタミン

7.3.2.ホワイトバイオテクノロジーで製造されたビタミン

7.3.3.ビタミンB2(リボフラビン)

7.3.4.ビタミンB12(コバラミン)

7.3.5.ビタミンC(アスコルビン酸)

7.3.6.ビタミンB7(ビオチン)

7.3.7.ビタミンB3(ナイアシン/ニコチン酸)

7.3.8.ビタミンB9(葉酸/葉酸塩)

7.3.9.アミノ酸

7.3.10.ホワイトバイオテクノロジーで生産されたアミノ酸

7.3.11.リジン

7.3.12.グルタミン酸(グルタミン酸ナトリウム、MSG)

7.3.13.メチオニン

7.3.14.技術成熟度(TRL):食品添加物

7.3.15.風味増強剤

7.3.16.風味増強剤

7.3.17.イノシン酸二ナトリウム(IMP)

7.3.18.グアニル酸二ナトリウム(GMP)

7.3.19.モナチン

7.4.工業用酵素

7.4.1.バイオ製造酵素

7.4.2.概要酵素のためのホワイトバイオテクノロジー

7.4.3.工業用酵素生産のための微生物プラットフォーム

7.4.4.工業的酵素生産のための微生物プラットフォーム

7.4.5.酵素生産の動向

7.4.6.主要な酵素生産者と技術プロバイダー

7.4.7.主要酵素生産者の比較状況

7.4.8.製品の強みと弱み 企業比較

7.5.バイオエネルギー用途の酵素

7.5.1.バイオエネルギー用途の酵素

7.5.2.バイオエネルギーのバリューチェーン:実現技術としての酵素

7.5.3.技術成熟度(TRL):バイオエネルギー用途の酵素

7.5.4.技術成熟度(TRL):バイオエネルギー用途の酵素

7.5.5.リグノセルロース由来のバイオエタノール用酵素

7.5.6.リグノセルロース系バイオエタノール用セルラーゼ

7.5.7.ヘミセルラーゼと相乗酵素カクテル

7.5.8.バイオマス加水分解におけるキシラナーゼと付属酵素

7.5.9.第一世代バイオエタノールにおけるアミラーゼ

7.5.10.酵素バイオディーゼル生産におけるリパーゼ

7.5.11.バイオマス前処理のための酸化酵素(ラッカーゼ、ペルオキシダーゼ)

7.5.12.過酷な処理条件下での耐熱性酵素と極限環境用酵素

7.5.13.耐熱性酵素:商業的な例と工業的応用

7.5.14.耐熱性酵素のコストパフォーマンス指標

7.5.15.酵素バイオエネルギー処理の経済的競争力

7.5.16.バイオエネルギーにおける酵素応用の技術準備レベル

7.5.17.バイオエネルギー酵素の技術的課題と機会

7.6.脱炭素とCO₂利用のための酵素

7.6.1.低炭素プロセス開発における触媒としての酵素

7.6.2.CO₂回収技術における炭酸脱水酵素

7.6.3.ギ酸脱水素酵素とCO₂-to-chemicals経路

7.6.4.酵素結合CO₂-to-FuelあるいはCO₂-to-Chemicalシステム

7.6.5.CCUSにおける酵素の統合

7.6.6.酵素ベースの CO₂ システムの商業的展開への障壁

7.6.7.CO₂の回収と変換に対する選択された酵素的アプローチ

7.7.プラスチックリサイクルのための酵素

7.7.1.酵素的解重合の概要

7.7.2.プラスチックの解重合に使われる酵素(1)

7.7.3.プラスチック解重合に用いられる酵素(2)

7.7.4.酵素解重合の課題

7.7.5.酵素解重合における混合プラスチックの課題

7.7.6.汚染が酵素活性に及ぼす影響

7.7.7.プラスチックリサイクルのための酵素生産

7.8.ホワイトバイオテクノロジーから得られるその他の製品

7.8.1.オンワード用の酵素ノボザイムズ

7.8.2.バイオ製造からのセメント代替品:バイオメイソン

7.8.3.精密発酵:定義と範囲

8.バイオ製造特殊化学品の予測

8.1.方法論:世界の発酵ベースの生産能力(ktpa)の予測(1)

8.2.方法論:世界の発酵ベースの生産能力(ktpa)の予測(2)

8.3.バイオ製造特殊化学品2026-2036年全体市場

8.4.バイオ製造美容・パーソナルケア化学品 2026-2036年

8.5.バイオ製造食品・飲料・栄養化学品 2026-2036年

8.6.バイオ製造工業用化学品 2026-2036年

8.7.バイオ燃料・エネルギー化学品 2026-2036年

8.8.バイオ製造の美容・パーソナルケア用化学品 2026-2036年

8.9.バイオ製造食品・飲料・栄養化学品 2026-2036年

8.10.バイオ製造工業用化学品 2026-2036年

8.11.バイオ燃料・エネルギー化学品 2026-2036年

9.企業プロファイル

9.1.アフィレン

9.2.アルゼダ

9.3.バイオメイソン

9.4.バイオサーキュラー・テクノロジーズ

9.5.ボルトスレッド

9.6.ブラスケム・バイオプラスチックス

9.7.カーボンブリッジ

9.8.セルティック・リニューアブルズ

9.9.チェーンクラフト

9.10.CJバイオマテリアル

9.11.シアノキャプチャー

9.12.ダニマー・サイエンティフィック

9.13.エコバティブ・フォレジャー

9.14.Enginzyme

9.15.エンザイマスター

9.16.フォータム:INGAプラスチック

9.17.河南徳光バイオテクノロジー

9.18.ホリフェルム

9.19.Huitong Biomaterials

9.20.工業用微生物

9.21.カネカPHA

9.22.クレイグ・バイオクラフト研究所

9.23.ランザテック

9.24.ランザテック

9.25.マンゴーマテリアル

9.26.モダン・メドウ

9.27.ネイチャーワークス

9.28.ニューエナジーブルー

9.29.ノボザイムズ

9.30.オウロビオ

9.31.パケス・バイオマテリアル

9.32.Qパワー

9.33.スパイバー

9.34.帝人フロンティアPLA

9.35.トータルエナジー・コルビオン

Summary

Industrial biomanufacturing of specialty chemicals across food, cosmetics, pigments, and enzymes. Fermentation-based production. Technology benchmarking and trends in synthetic biology. Market outlook, players, and 10-year forecasts.

Specialty chemicals underpin a wide range of high-performance products, from advanced food formulations and cosmetic actives to industrial catalysts and functional coatings. Unlike commodity chemicals, they are defined not by volume but by their ability to deliver precise functions, meet strict regulatory requirements, and achieve consistent purity and performance. Even minor variations in their formulation can determine whether a product succeeds or fails in the market, making their production a technically demanding and strategically important segment of the chemical industry.

White biotechnology, the industrial application of microorganisms, enzymes, and biocatalytic processes, offers a powerful route to manufacturing these chemicals more sustainably. By using renewable feedstocks and precision bioprocessing, it can access complex or chiral molecules that are challenging to synthesize via petrochemical routes, reduce greenhouse gas emissions, and minimize hazardous by-products. Advances in synthetic biology, strain optimization, and alternative feedstock utilization are now making biomanufacturing economically viable for an increasing range of specialty chemicals, opening new opportunities for innovation and market differentiation.

Specialty chemicals are produced in lower volumes than their commodity counterparts and are sold on the basis of performance, purity, and compliance with strict technical or regulatory standards. They include functional ingredients for food, cosmetics, and industrial applications where small changes in formulation can determine product success. In contrast to bulk products such as fuels, plastics, or base chemicals, specialty chemicals serve narrower markets, command higher margins, and can justify more complex or precise production methods.

White biotechnology is well suited to this space. Microbial fermentation and enzymatic synthesis can deliver molecular precision, access complex or chiral structures, and enable bio-identical or novel compounds that are difficult or costly to obtain via petrochemical routes. These processes also offer sustainability advantages, using renewable feedstocks and generating fewer emissions or hazardous by-products. IDTechEx forecasts growth in production capacity from 444 ktpa to 701 ktpa in this sector with a CAGR of 4.7%. This growth is supported by advances in synthetic biology, process optimization, and the adoption of alternative feedstocks, all of which are improving both performance and economics.

IDTechEx's report "Biomanufacturing Specialty Chemicals 2026-2036" examines the role of white biotechnology in producing specialty chemicals, focusing on food additives, cosmetic and personal care ingredients, pigments, and enzymes. Its coverage of enzymes spans several industrial applications, from bioenergy to decarbonization and recycling. The report critically analyses production methods, technical benefits, commercial challenges, and the companies active in their development. It also considers the enabling technologies, market drivers, and competitive dynamics shaping the sector's future.

What is White Biotechnology?

The bioeconomy is an economic system built on the use of renewable biological resources, from agriculture, fisheries, and forestry, to produce food, materials, chemicals, and energy. Within this system, white biotechnology, sometimes called industrial biomanufacturing, plays a pivotal role in enabling the sustainable production of chemicals and materials at industrial scale. It sits alongside other "colors" of biotechnology, such as green biotechnology in agriculture and red biotechnology in healthcare but is uniquely positioned to transform chemical production by reducing reliance on fossil fuels and enabling new molecular possibilities.

Although white biotechnology has been used for decades, from bacterial enzymes in detergents to fermentation-derived food additives, its applications in specialty chemicals are expanding rapidly. Advances in synthetic biology, strain optimization, and feedstock diversification have made it increasingly competitive in smaller, higher-value markets. At the same time, regulatory changes, corporate sustainability commitments, and consumer demand for bio-based products are creating favourable conditions for adoption.

Why Specialty Chemicals?

Specialty chemicals represent a strategic growth area for white biotechnology because they combine attractive margins with technical requirements that biomanufacturing is well placed to meet. Many of these products have established markets but rely on supply chains that face sustainability pressures, sourcing constraints, or cost volatility. Others are niche ingredients where existing production routes are inefficient or poorly scalable.

For companies developing biomanufacturing capabilities, specialty markets offer an opportunity to commercialize products at smaller scales while still achieving viable pricing. They can act as a proving ground for new strains, feedstocks, and process technologies, with lessons that can later be applied to larger-volume markets. Industry discussions at CHEMUK 2025 reinforced this trajectory, highlighting the focus on scaling sustainable technologies and integrating automation to bridge the gap between laboratory innovation and commercial deployment. The key message was that specialty chemicals will continue to serve as the proving ground where technical feasibility, commercial viability, and sustainability commitments converge. In addition, the fragmented nature of specialty markets allows smaller producers to establish competitive positions without immediately competing head-to-head with the largest chemical companies on bulk output.

Advances Driving Biomanufacturing in Specialty Chemicals

The specialty chemicals sector is benefiting from rapid advances in synthetic biology, which is enabling engineered biocatalysts with improved yield, stability, and specificity. Alternative feedstocks such as lignocellulosic biomass, waste gases, and agricultural by-products are creating new pathways for production. Novel biocatalysts are expanding the range of accessible molecules, while carbon-neutral and carbon-negative production routes are emerging as part of wider decarbonization efforts. Cell-free systems are making it possible to produce high-value molecules without the limitations of whole-cell fermentation. Advances in strain optimization and metabolic engineering are increasing productivity and reducing downstream processing costs. Together, these technology trends are opening new opportunities for specialty markets and enabling products that were previously not technically or economically viable. IDTechEx's report analyses these advances, profiling the technologies, companies, and case studies that are shaping the future of biomanufacturing for specialty chemicals.

Market Drivers, Challenges, and Economic Viability

Demand for sustainable, bio-based alternatives is rising due to consumer preferences, brand commitments, and tightening regulations, particularly in food and cosmetics. However, economic viability remains a decisive factor. Internal factors such as process yield, ease of scale-up, and choice of biocatalyst can determine whether a project succeeds commercially, while external influences include oil price volatility, regulatory frameworks, and the willingness of customers to pay a green premium. Producers also face high development and scale-up costs for precision cell factories, slow adoption where reformulation is needed, lengthy regulatory approval processes, and fragmented markets that require engagement with multiple niche applications. This report examines how companies are addressing these barriers, with case studies of both successful and unsuccessful attempts to scale biomanufacturing.

Applications and Market Outlook

IDTechEx profiles key specialty molecules in detail, describing for each the production process and key biocatalysts, technical advantages over petrochemical or extracted equivalents, current challenges, downstream applications, and technology readiness level. Each profile also lists active producers and their capacities, along with a market outlook to 2036. A 10-year forecast segments the market by major molecule groups based on production capacity, adoption potential, and technology readiness.

Scope of This Report

This IDTechEx report focuses on the specialty chemicals segment of white biotechnology. Coverage includes food additives such as vitamins, amino acids, flavorings, flavor enhancers, gelling agents, and specialty acids. It examines cosmetic and personal care ingredients including bioactive compounds, natural fragrances, and functional additives. It also covers pigments, from natural colors to high-value bio-derived dyes, and enzymes for industrial applications, from bioenergy to decarbonization and recycling.

Fuels, plastics, and other commodity chemicals are discussed in our companion report "White Biotechnology 2025-2035" and are included here only for context.

This report provides critical market intelligence about biomanufactured specialty chemicals across food, cosmetics, pigments, and enzymes. This includes

Table of Contents1. EXECUTIVE SUMMARY

1.1. Colors of biotechnology

1.2. What is white biotechnology?

1.3. White biotechnology specialty chemicals 2026-2036: Scope

1.4. Trends and drivers in white biotechnology (1)

1.5. Trends and drivers in white biotechnology (2)

1.6. Synthetic biology as applied to white biotechnology

1.7. Technology trends in white biotechnology

1.8. Overview of alternative feedstocks for white biotechnology

1.9. Major market challenges for white biotechnology

1.10. Technical challenges facing white biotechnology

1.11. Products derived from white biotechnology: overview

1.12. Molecule categories that can be produced through industrial biomanufacturing

1.13. Company landscape in white biotechnology

1.14. Bio-manufactured fragrances and aromatics: Emerging company landscape

1.15. Other emerging bio-manufactured beauty products and status

1.16. Technology Readiness Level (TRL): Beauty products

1.17. Technology Readiness Level (TRL): Beauty products

1.18. Biosurfactants: Company landscape

1.19. Technology challenges and opportunities for bioenergy enzymes

1.20. Technology Readiness Level (TRL): Enzymes for bioenergy applications

1.21. Cost-performance metrics for thermostable enzymes

1.22. Technology readiness levels of enzyme applications in bioenergy

1.23. Selected enzymatic approaches to CO2 capture and conversion

1.24. Bio-manufactured Specialty Chemicals 2026-2036 overall market

1.25. White biotechnology for commodity chemicals 2025-2035

1.26. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. Specialty chemicals

2.2. Colors of biotechnology

2.3. What is white biotechnology?

2.4. The bioeconomy and white biotechnology

2.5. White biotechnology specialty chemicals 2026-2036: scope

2.6. Products derived from white biotechnology: Overview

2.7. Molecules that can be produced through industrial biomanufacturing

2.8. Molecules that can be produced through industrial biomanufacturing

2.9. Molecules that can be produced through industrial biomanufacturing

2.10. Molecules that can be produced through industrial biomanufacturing

2.11. Company landscape in white biotechnology

2.12. Company landscape in white biotechnology

2.13. Trends and drivers in white biotechnology (1)

2.14. Trends and drivers in white biotechnology (2)

3. MARKET ANALYSIS

3.1. Market Drivers for White Biotechnology

3.1.1. Market drivers: Demand for biobased products

3.1.2. Market drivers: Government support of biotechnology

3.1.3. Market drivers: Carbon taxes

3.2. Economic Viability of White Biotechnology

3.2.1. Factors affecting the economic viability of white biotechnology projects

3.2.2. Effect of the price of Brent crude on biobased products

3.2.3. The Green Premium

3.2.4. Rising feedstock prices

3.2.5. Effect of cell factory on cost

3.2.6. How scale-up affects cost

3.2.7. Zymergen: Case study on economics of synthetic biology

3.2.8. Case study: LanzaTech

3.2.9. Case study: Solazyme

3.2.10. Synthetic biology: Shift from commodity products to lower volume, high value markets

3.2.11. Major market challenges for white biotechnology

4. CELL FACTORIES FOR WHITE BIOTECHNOLOGY

4.1.1. Cell factories for biomanufacturing: Factors to consider

4.1.2. Cell factories for biomanufacturing: A range of organisms (1)

4.1.3. Cell factories for biomanufacturing: A range of organisms

4.1.4. Escherichia coli (E.coli)

4.1.5. Corynebacterium glutamicum (C. glutamicum)

4.1.6. Bacillus subtilis (B. subtilis)

4.1.7. Saccharomyces cerevisiae (S. cerevisiae)

4.1.8. Yarrowia lipolytica (Y. lipolytica)

4.1.9. Microorganisms used in different biomanufacturing processes

4.1.10. Non-model organisms for white biotechnology

5. TECHNOLOGY DEVELOPMENTS

5.1. Synthetic Biology

5.1.1. Synthetic biology: The design and engineering of biological systems

5.1.2. Synthetic biology: Manipulating the central dogma

5.1.3. The vast scope of synthetic biology

5.1.4. The process of synthetic biology: Design, build and test

5.1.5. Synthetic biology: Why now?

5.1.6. Synthetic biology: From pharmaceuticals to consumer products

5.1.7. Synthetic biology: Disrupting existing supply chains

5.1.8. Synthetic biology: Drivers and barriers for adoption

5.1.9. Synthetic biology as applied to white biotechnology

5.2. Tools and Techniques of Synthetic Biology

5.2.1. Tools and techniques of synthetic biology: Overview

5.2.2. DNA synthesis

5.2.3. Introduction to CRISPR-Cas9

5.2.4. CRISPR-Cas9: A bacterial immune system

5.2.5. CRISPR-Cas9's importance to synthetic biology

5.2.6. Protein/enzyme engineering

5.2.7. Computer-aided design

5.2.8. Commercial examples of engineered proteins in industrial applications

5.2.9. Strain construction and optimization

5.2.10. Synergy between synthetic biology and metabolic engineering

5.2.11. Framework for developing industrial microbial strains

5.2.12. The problem with scale

5.2.13. Introduction to cell-free systems

5.2.14. Cell-free versus cell-based systems

5.2.15. Cell-free systems in the context of white biotechnology

5.2.16. Cell-free systems for white biotechnology

5.2.17. Commercial implementation of cell-free systems: Solugen

5.2.18. Startups pursuing cell-free systems for white biotechnology (1/2)

5.2.19. Startups pursuing cell-free systems for white biotechnology (2/2)

5.2.20. Immobilized enzymes in white biotechnology

5.2.21. Immobilized catalysts in white biotechnology

5.2.22. Robotics: enabling hands-free and high throughput science

5.2.23. Robotic cloud laboratories

5.2.24. Automating organism design and closing the loop

5.2.25. Artificial intelligence and machine learning

5.2.26. Machine learning de novo protein prediction

5.2.27. Overview of machine learning based improvements for biomanufacturing

5.2.28. AI-driven fermentation platform companies

5.3. Improvement of Biomanufacturing Processes

5.3.1. Continuous vs batch biomanufacturing

5.3.2. Benefits and challenges of continuous biomanufacturing

5.3.3. Continuous vs batch biomanufacturing: Key fermentation parameter comparison

5.3.4. Machine learning to improve biomanufacturing processes

5.3.5. Downstream processing (DSP) improvements (1)

5.3.6. Downstream processing (DSP) improvements (2)

5.3.7. Perfusion bioreactors

5.3.8. Tangential flow filtration (TFF) in downstream bioprocessing

5.3.9. Hybrid biotechnological-chemical approaches

5.3.10. Process intensification and high-cell-density fermentation

5.4. White Biotechnology for Sustainability

5.4.1. White biotechnology as a sustainable technology

5.4.2. Routes for carbon capture in white biotechnology

5.4.3. Autotrophic bacteria for carbon capture through biomanufacturing

5.4.4. 5.5 Alternative Feedstocks for Biomanufacturing

5.4.5. Why use alternative feedstocks for white biotechnology?

5.4.6. Food, land, and water competition

5.4.7. C1 feedstocks: Metabolic pathways

5.4.8. C1 feedstocks: Economic benefits

5.4.9. C1 feedstocks: Challenges

5.4.10. Non-methane C1 feedstocks

5.4.11. C1 feedstocks: Products

5.4.12. C1 feedstocks: Gas fermentation

5.4.13. C2 feedstocks

5.4.14. C2 feedstocks: Products segmented by feedstock

5.4.15. C1 and C2 feedstocks: Commercial activity

5.4.16. C1 and C2 feedstocks: Commercial activity

5.4.17. Lignocellulosic biomass feedstocks

5.4.18. Lignocellulosic biomass feedstocks: Challenges

5.4.19. Lignocellulosic biomass feedstocks: Challenges

5.4.20. Lignocellulosic biomass feedstocks: Products

5.4.21. Lignocellulosic biomass feedstocks: Products

5.4.22. Lignocellulosic feedstocks: Commercial activity

6. BLUE BIOTECHNOLOGY

6.1. What is blue biotechnology?

6.2. Main biocatalysts of blue biotechnology: Cyanobacteria and algae

6.3. Cyanobacteria

6.4. Algae

6.5. Key drivers and challenges for blue biotechnology

6.6. Selected startups in blue biotechnology

7. PRODUCTS DERIVED FROM WHITE BIOTECHNOLOGY

7.1.1. Products derived from white biotechnology: Overview

7.2. Bio-manufactured Products for Cosmetics

7.2.1. Biomanufacturing in the beauty sector

7.2.2. Incumbent beauty ingredient supply chain (1)

7.2.3. Incumbent beauty ingredient supply chain (2)

7.2.4. Incumbent beauty ingredient supply chain company landscape (1)

7.2.5. Incumbent beauty ingredient supply chain company landscape (2)

7.2.6. Bio-manufactured beauty ingredient supply chain and processing

7.2.7. Established Biotech-Derived Beauty Ingredients

7.2.8. Emerging Biotech-Derived Beauty Ingredients

7.2.9. Challenges in the bio-manufactured beauty ingredients sector

7.2.10. Fragrances and Aromatic Compounds

7.2.11. Fragrances and aromatic compounds overview

7.2.12. Fragrances and aromatic compounds

7.2.13. Bio-manufactured fragrances and aromatics: Emerging company landscape

7.2.14. Bio-manufactured fragrances and aromatics: Emerging company landscape

7.2.15. Fragrances and aromatic compounds: Company landscape (1)

7.2.16. Fragrances and aromatic compounds: Company landscape (2)

7.2.17. Biotech-derived fragrance precursors

7.2.18. Ambroxan

7.2.19. Biosurfactants for Cosmetics

7.2.20. Biosurfactants: Mild, biodegradable alternatives to SLS and SLES (1)

7.2.21. Biosurfactants: Mild, biodegradable alternatives to SLS and SLES (2)

7.2.22. Biosurfactants: Company landscape (1)

7.2.23. Biosurfactants: Company landscape (2)

7.2.24. Bio-manufactured surfactants: Company landscape

7.2.25. Surfactants: Functional roles and market importance in White Biotechnology

7.2.26. Rhamnolipids

7.2.27. Sophorolipids

7.2.28. Mannosylerythritol lipids (MELs)

7.2.29. Cellobiose lipids

7.2.30. Designer glycolipids and lipopeptides via synthetic biology

7.2.31. Polysaccharide-based amphiphiles

7.2.32. White biotechnology surfactants commercial landscape

7.2.33. Hyaluronic Acid

7.2.34. Hyaluronic acid: Fermentation-based production for moisturizing

7.2.35. Hyaluronic acid: Fermentation-based production for moisturizing (2)

7.2.36. Function-driven customization of biotech-derived hyaluronic acid formulations

7.2.37. Function-driven customization of biotech-derived hyaluronic acid formulations

7.2.38. Hyaluronic acid technologies: Functions and key players

7.2.39. Hyaluronic acid: Company landscape (1)

7.2.40. Hyaluronic acid: Company landscape (2)

7.2.41. Hyaluronic Acid

7.2.42. Emollients

7.2.43. Squalene and Squalane: White biotechnology alternatives to shark liver oil

7.2.44. Squalene and Squalane: White biotechnology alternatives to shark liver oil

7.2.45. Squalene

7.2.46. Squalene and Squalane: Company landscape

7.2.47. Squalene and Squalane: Company landscape

7.2.48. Collagen

7.2.49. Collagen in skin and personal care products

7.2.50. Collagen in skin and personal care products

7.2.51. Collagen: Company landscape

7.2.52. Collagen: Company landscape (2)

7.2.53. Collagen: Company landscape

7.2.54. Comparison of native, hydrolyzed, and recombinant collagen structures

7.2.55. Comparison of native, hydrolyzed, and recombinant collagen structures

7.2.56. Engineered collagen derivatives with enhanced bioactivity

7.2.57. Collagen (e.g. Geltor)

7.2.58. Pigments

7.2.59. Bio-based UV filters and photoprotective compounds

7.2.60. Melanin

7.2.61. Indigoidine

7.2.62. Case study: OneSkin - OS 01 Senotherapeutic Peptide

7.2.63. Market Analysis and Benchmarking

7.2.64. Bio-manufactured beauty ingredient production capacities

7.2.65. Comparing bio-manufactured and conventional products (1)

7.2.66. Comparing bio-manufactured and conventional products (2)

7.2.67. Comparing conventional sourcing and biomanufacturing (1)

7.2.68. Comparing conventional sourcing and biomanufacturing (2)

7.2.69. Biotech ingredients metrics comparison

7.2.70. Biotech ingredients metrics comparison (2)

7.2.71. Biotech ingredient comparison metrics - IDTechEx framework (Part 1)

7.2.72. Biotech ingredient comparison metrics - IDTechEx framework (Part 2)

7.2.73. Outlook for bio-manufactured beauty ingredients

7.2.74. General challenges for biomanufacturing in the beauty sector

7.2.75. Other emerging bio-manufactured beauty products and status

7.2.76. Other emerging bio-manufactured beauty products and status

7.2.77. Technology Readiness Level (TRL): Beauty products

7.2.78. Technology Readiness Level (TRL): Beauty products

7.2.79. Bio-manufactured ingredients vs conventional alternatives

7.2.80. Bio-manufactured ingredients vs conventional alternatives

7.3. Bio-manufactured Food Additives

7.3.1. Vitamins

7.3.2. Vitamins produced using white biotechnology

7.3.3. Vitamin B2 (Riboflavin)

7.3.4. Vitamin B12 (Cobalamin)

7.3.5. Vitamin C (Ascorbic Acid)

7.3.6. Vitamin B7 (Biotin)

7.3.7. Vitamin B3 (Niacin / Nicotinic Acid)

7.3.8. Vitamin B9 (Folic Acid / Folate)

7.3.9. Amino Acids

7.3.10. Amino acids produced using white biotechnology

7.3.11. Lysine

7.3.12. Glutamate (Monosodium Glutamate, MSG)

7.3.13. Methionine

7.3.14. Technology Readiness Level (TRL): Food additives

7.3.15. Flavor Enhancers

7.3.16. Flavor enhancers

7.3.17. Disodium Inosinate (IMP)

7.3.18. Disodium Guanylate (GMP)

7.3.19. Monatin

7.4. Enzymes for Industrial Applications

7.4.1. Bio-manufactured enzymes

7.4.2. Overview: White biotechnology for enzymes

7.4.3. Microbial platforms for industrial enzyme production

7.4.4. Microbial platforms for industrial enzyme production

7.4.5. Trends in enzyme production

7.4.6. Leading enzyme producers and technology providers

7.4.7. Comparative landscape of leading enzyme producers

7.4.8. Product strengths and weaknesses company comparison

7.5. Enzymes for Bioenergy Applications

7.5.1. Enzymes for bioenergy applications

7.5.2. Bioenergy value chain: Enzymes as enabling technologies

7.5.3. Technology Readiness Level (TRL): Enzymes for bioenergy applications

7.5.4. Technology Readiness Level (TRL): Enzymes for bioenergy applications

7.5.5. Enzymes for lignocellulosic derived bioethanol

7.5.6. Cellulases for lignocellulosic bioethanol

7.5.7. Hemicellulases and synergistic enzyme cocktails

7.5.8. Xylanases and accessory enzymes in biomass hydrolysis

7.5.9. Amylases in first-generation bioethanol

7.5.10. Lipases for enzymatic biodiesel production

7.5.11. Oxidative enzymes (Laccases, Peroxidases) for biomass pretreatment

7.5.12. Thermostable and extremophilic enzymes for harsh processing conditions

7.5.13. Thermostable enzymes: Commercial examples and industrial applications

7.5.14. Cost-performance metrics for thermostable enzymes

7.5.15. Economic competitiveness of enzymatic bioenergy processing

7.5.16. Technology readiness levels of enzyme applications in bioenergy

7.5.17. Technology challenges and opportunities for bioenergy enzymes

7.6. Enzymes for Decarbonization and CO₂ Utilization

7.6.1. Enzymes as catalysts in low-carbon process development

7.6.2. Carbonic anhydrase in CO₂ capture technologies

7.6.3. Formate dehydrogenase and CO₂-to-chemicals pathways

7.6.4. Enzyme-coupled CO₂-to-Fuel or CO₂-to-chemical systems

7.6.5. Enzyme integration in CCUS

7.6.6. Barriers to commercial deployment of enzyme-based CO₂ systems

7.6.7. Selected enzymatic approaches to CO2 capture and conversion

7.7. Enzymes for Plastics Recycling

7.7.1. Enzymatic depolymerization overview

7.7.2. Enzymes used for plastics depolymerization (1)

7.7.3. Enzymes used for plastics depolymerization (2)

7.7.4. Challenges in enzymatic depolymerization

7.7.5. The challenges of mixed plastics for enzymatic depolymerization

7.7.6. The effect of contamination on enzyme activity

7.7.7. Enzyme production for plastics recycling

7.8. Other Products Derived from White Biotechnology

7.8.1. Enzymes for onward use: Novozymes

7.8.2. Cement alternatives from biomanufacturing: BioMason

7.8.3. Precision fermentation: Definition and scope

8. FORECASTS FOR BIO-MANUFACTURING SPECIALTY CHEMICALS

8.1. Methodology: Forecasting global fermentation-based production capacity (ktpa) (1)

8.2. Methodology: Forecasting global fermentation-based production capacity (ktpa) (2)

8.3. Bio-manufactured Specialty Chemicals 2026-2036 overall market

8.4. Bio-manufactured beauty and personal care chemicals 2026-2036

8.5. Bio-manufactured food, beverage & nutrition chemicals 2026-2036

8.6. Bio-manufactured industrial applications chemicals 2026-2036

8.7. Bio-manufactured biofuels and energy chemicals 2026-2036

8.8. Bio-manufactured beauty and personal care chemicals 2026-2036

8.9. Bio-manufactured food, beverage & nutrition chemicals 2026-2036

8.10. Bio-manufactured industrial applications chemicals 2026-2036

8.11. Bio-manufactured biofuels and energy chemicals 2026-2036

9. COMPANY PROFILES

9.1. Afyren

9.2. Arzeda

9.3. Biomason

9.4. Biotic Circular Technologies

9.5. Bolt Threads

9.6. Braskem Bioplastics

9.7. CarbonBridge

9.8. Celtic Renewables

9.9. Chaincraft

9.10. CJ Biomaterials

9.11. CyanoCapture

9.12. Danimer Scientific

9.13. Ecovative Forager

9.14. Enginzyme

9.15. Enzymaster

9.16. Fortum: INGA Plastic

9.17. Henan Techuang Biotechnology

9.18. Holiferm

9.19. Huitong Biomaterials

9.20. Industrial Microbes

9.21. Kaneka: PHAs

9.22. Kraig Biocraft Laboratories

9.23. LanzaTech

9.24. LanzaTech

9.25. Mango Materials

9.26. Modern Meadow

9.27. NatureWorks

9.28. New Energy Blue

9.29. Novozymes

9.30. Ourobio

9.31. Paques Biomaterials

9.32. Q Power

9.33. Spiber

9.34. Teijin Frontier: PLA

9.35. TotalEnergies Corbion

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の 先端材料 - Advanced Materials&Crisical Minerals分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|