クリティカル・マテリアル回収 2026-2046年:技術、市場、プレーヤーCritical Material Recovery 2026-2046: Technologies, Markets, Players 二次ソースの重要材料抽出技術、重要材料回収技術、レアアースリサイクル、リチウムイオン電池技術の金属回収、重要半導体回収、白金族金属回収の市場 IDTechExは、2046年までに年間810万トン... もっと見る

サマリー二次ソースの重要材料抽出技術、重要材料回収技術、レアアースリサイクル、リチウムイオン電池技術の金属回収、重要半導体回収、白金族金属回収の市場

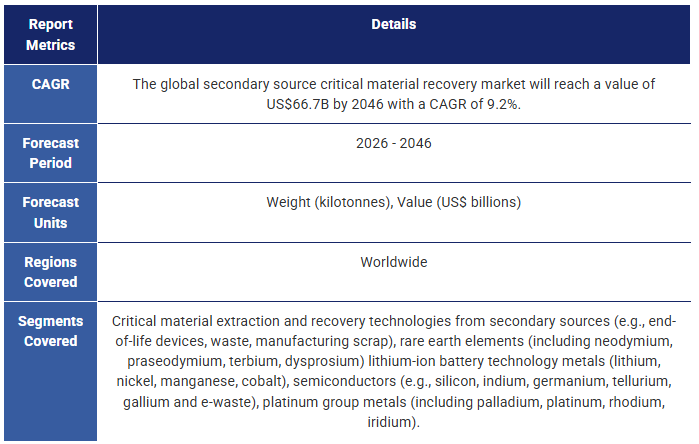

IDTechExは、2046年までに年間810万トンを超える重要材料が廃棄物から回収され、これは660億米ドルを超える価値のある材料に相当すると予測している。使用済み機器、自動車、電気自動車、電子廃棄物、製造スクラップを含む二次原料は、貴重な重要材料の急速な出現源である。本レポートでは、重要素材回収市場、主要な抽出・回収技術、新たな二次原料、市場プレイヤーを特徴付けています。希土類元素、リチウムイオン電池材料、白金族金属、重要半導体を含む4つの主要な重要材料セグメントについて、最新の重要材料回収イノベーションを調査しています。IDTechExは、重要材料回収市場が2026年から2046年にかけて年平均成長率9.2%で成長すると予測し、価値機会の拡大を特定している。

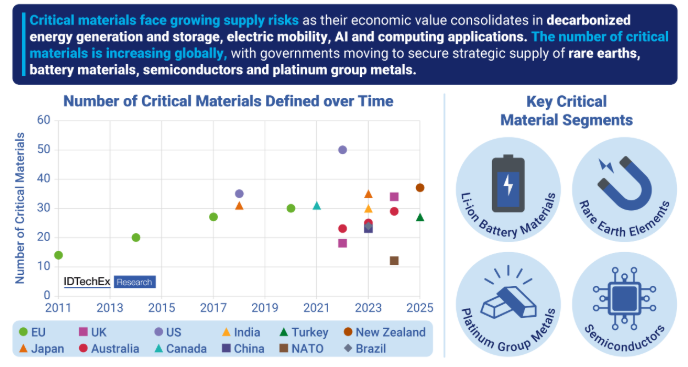

重要材料とは、供給リスクが高く、地域経済にとって経済的価値の高い戦略的材料と定義される。リチウム、ニッケル、コバルト、グラファイト、レアアース、白金族金属、シリコン、その他の半導体などの重要材料は、輸送、エネルギー、通信、産業、消費者、防衛の各用途で不可欠である。重要素材のサプライチェーンが地理的に局所化していることは、世界経済に大きなリスクをもたらし、輸出規制の強化が圧力をかけ続けている。世界中で重要素材が増加するにつれ、戦略的素材供給を多様化し再保有するために、代替ソースからの重要素材回収を求める強い市場牽引力が存在する。

製造スクラップ、使用済み製品、廃棄物などの二次的な供給源から重要素材を回収することで、廃棄物の流れを有効利用しながら供給リスクを軽減することができる。重要材料が電気自動車、脱炭素エネルギー、高性能コンピューティング、AIアプリケーションに集約されるにつれて、消費時点で生産される使用済み機器が重要な重要材料供給源となる。IDTechExの報告書では、主要な新興重要材料原料の特徴を明らかにし、重要材料リサイクルの経済性と回収を支えるビジネスモデルを評価している。

重要材料の回収技術は、ほぼ準備が整っている。次の問題は、二次的な材料源としてどれだけ容易に再利用できるかである。一次鉱物処理のために開拓された高温冶金および湿式冶金による重要物質回収技術は、高い回収効率で拡張可能であるため、二次原料の流れに展開するのに適している。未解決の課題は、二次原料の複雑な組成プロファイルに回収プロセスを適合させることである。二次原料は、一般的に、プラスチック、接着剤、低価金属、無機材料と重要材料の混合物を含む。本レポートでは、13の重要材料抽出技術を評価し、SWOT分析、技術準備レベルのベンチマーク、商業応用に関するケーススタディを提供している。

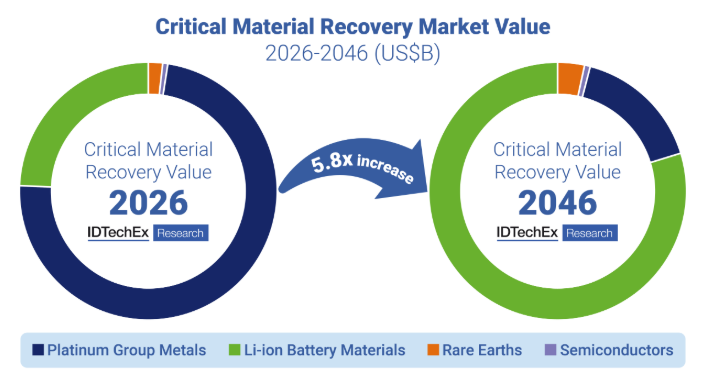

このIDTechEx調査レポートは、4つの重要材料セグメントを調査している:リチウムイオン電池材料、希土類元素、白金族金属、重要半導体である。白金族金属回収は、最も成熟した重要材料回収セグメントであり、世界的な一次供給量の少なさと、白金、パラジウム、イリジウム、ロジウム金属の本質的価値の高さに牽引されている。IDTechExは、自動車触媒、宝飾品、電子機器からの大量プラチナ族金属回収が、いかにして新たな重要素材回収市場へのロードマップとなり得るかについて論じている。本レポートはまた、水素燃料電池と水電解槽技術における白金族金属の役割を特徴付け、グリーン水素触媒リサイクルの発展を評価する。

重要な電池材料回収は最も急成長している市場セグメントであり、IDTechExは2046年までに年平均成長率15.9%で成長すると予測している。リチウムイオンバッテリーのリサイクルは、大量の電気自動車が使用済みとなり、リチウム、ニッケル、コバルト、グラファイト、銅、マンガンの二次供給の新たな流れが生まれることから、2030年代半ばに本格化すると見られている。IDTechExの本レポートは、湿式冶金、乾式冶金、直接リチウムイオン電池リサイクル技術を包括的に評価し、ベンチマークを行っている。また、規制、リチウムイオンバッテリーリサイクルの経済性、リサイクル能力、主要なバッテリーリサイクル業者、ビジネスモデルなどの市場動向についても論じています。

磁石からの重要なレアアースリサイクルは、レアアース元素が世界的に輸出規制の強化に直面しているため、主要な成長市場となっています。レアアースは、電気自動車モーター、風力タービンエネルギー発電機、ハードディスクドライブのアクチュエーターに使用される高性能NdFeBおよびSmCo磁石の重要な材料です。世界のレアアース磁石供給の88%以上が中国に集約されており、重要なレアアース元素のリサイクル技術には強い市場牽引力が存在します。本レポートでは、ロングループおよびショートループのレアアース磁石リサイクルのための溶媒抽出、液体クロマトグラフィー、水素脱硝、粉末冶金技術を批判的に評価しています。IDTechExは、2026年から2046年にかけての新たな循環型サプライチェーン、レアアースリサイクラー、リサイクル能力、供給原料の入手可能性を特徴づけています。

電子廃棄物(e-waste)と太陽光発電からの重要な半導体回収は、リサイクル技術の革新に依存する。クリティカル半導体の回収には自動分解技術が台頭しており、高価値材料コンポーネントの効率的な回収と、太陽光発電リサイクルのOpExコストの最適化を提供する。本レポートでは、2026年における重要なシリコン、インジウム、ガリウム、ゲルマニウム、テルルの回収技術と、リサイクルを支える市場ダイナミクスを特徴づける。

本レポートの主な内容

二次ソースからの重要材料抽出および重要材料回収技術のレビュー

主要な二次ソースセグメントにおける重要材料回収技術の完全な市場特性評価

重要素材回収市場分析

目次1.要旨

1.1.重要素材とは何か

1.2.クリティカルマテリアルの数は世界的に増加している

1.3.一次および二次ソースからの重要素材回収

1.4.二次資源からの重要素材回収技術

1.5.クリティカルマテリアル回収のための確立された二次ソースと新興の二次ソース

1.6.二次資源からの重要物質回収のビジネスモデル

1.7.重要物質抽出技術の概要

1.8.重要物質抽出技術の技術準備評価

1.9.主要な性能指標により評価される重要物質抽出法

1.10.重要物質抽出技術の価値提案の進化

1.11.重要素材回収技術の概要

1.12.重要金属回収技術の評価と比較

1.13.二次材料からの重要材料回収技術 - 主な調査結果

1.14.レアアース磁石を廃棄物からリサイクルするための主要技術の概要

1.15.2025年のレアアース磁石リサイクルはロングループ技術が主流

1.16.使用済み廃棄物の利用可能性が高まるまで、磁石製造廃棄物はリサイクル業者にとって重要な原料になる

1.17.重要なリチウムイオン電池技術の金属回収 - 主な結論

1.18.リチウムイオン電池リサイクル技術の概要と比較

1.19.リチウムイオン電池のリサイクル政策と規制 - 世界地図

1.20.二次ソースからの重要半導体材料回収 - 主な結論

1.21.重要半導体材料回収のビジネスモデル

1.22.二次資源からの重要な白金族金属回収 - 主要結論

1.23.白金族金属リサイクルのビジネスモデルと確立されたプレーヤー

1.24.水素燃料電池と水電解槽からの重要金属リサイクルは2040年代まで実現しない

1.25.2026~2046年までの20年間の世界回収重要材料全体予測、年間価値予測

1.26.白金族金属からリチウムイオン電池材料への重要材料回収価値の移転を促す電化

1.27.20年間の材料別回収重要材料の世界全体予測、年間重量予測、2026-2046年

2.市場予測

2.1.予測方法と主要更新情報

2.1.1.予測方法

2.1.2.再生可能エネルギー用途からの二次ソースの供給途絶

2.1.3.重要なリチウムイオン電池材料価格の前提

2.1.4.重要なレアアース材料価格の前提

2.1.5.重要な白金族金属価格の前提

2.1.6.前回から更新された注目すべき予測(1/2)

2.1.7.前回から更新された注目すべき予測(2/2)

2.2.重要素材回収予測

2.2.1.2026年から2046年までの20年間の世界全体の回収重要素材予測、年間重量予測

2.2.2. 2026年から2046年リチウムイオン電池材料を除く、回収される主要材料の世界全体予測(年間重量)

2.2.3.重要回収材料の20年世界全体材料別予測(年間重量予測) 2026-2046年

2.2.4.リチウムイオン電池材料を除く、20年間の回収重要材料の元素別世界全体予測(年間重量予測) 2026-2046年

2.2.5.2026~2046年、リチウムイオン電池材料を除く、回収された重要材料の20年世界全体予測、年間価値予測

2.2.6. 2026~2046年、リチウムイオン電池材料を除く、回収された重要材料の20年世界全体予測、年間価値予測

2.2.7.白金族金属からリチウムイオン電池材料への重要材料回収価値の移動を促す電化

2.2.8.20年間の世界の回収重要レアアース元素予測、年間重量予測、2026~2046年

2.2.9.20年の重要レアアース元素回収量の世界予測(二次供給源別、年間重量予測、2026~2046年)

2.2.10.20年の重要レアアース元素回収の世界予測、年間金額予測、2026~2046年

2.2.11. リチウムイオン電池から回収される重要物質の20年間の世界的回収量、年間重量予測、2026~2046年

2.2.12. リチウムイオン電池から回収される重要物質の20年間の世界的回収量、年間金額予測、2026~2046年

2.2.13. 半導体重要物質の20年間の回収量予測、年間重量予測、2026~2046年

2.2.14. 半導体重要物質の20年間の回収量予測、年間重量予測(シリコンを除く)、2026~2046年

2.2.15. 半導体重要物質の20年間の回収量予測、年間金額予測、2026~2046年

2.2.16. 白金族金属の20年間の回収量予測、年間重量予測、2026~2046年

2.2.17. 20年間の世界の回収済み重要白金族金属予測(原料別、年間重量予測、2026~2046年)

2.2.18. 20年間の世界の回収済み重要白金族金属予測(年間価値予測、2026~2046年)

2.2.17.20年半導体回収重要材料の世界予測、年間重量予測、2026~2046

2.2.14.重要半導体材料回収の20年世界予測、年間重量予測、シリコンを除く、2026~2046年

2.2.15. 重要半導体材料回収の20年世界予測、年間金額予測、2026~2046年

2.2.16.重要白金族金属回収量の世界20年予測、年間重量予測、2026年~2046年

2.2.17. 重要白金族金属回収量の世界20年予測、原料供給源別セグメント、年間重量予測、2026年~2046年

2.2.18. 重要白金族金属回収量の世界20年予測、年間金額予測、2026年~2046年

3.序論

3.1.重要素材とは何か

3.2.鉱物経済の台頭と重要素材の出現

3.3.クリティカル・マテリアルの需要増が世界供給の伸びを牽引

3.4.クリティカル・マテリアルの数は世界的に増加している

3.5.輸出規制の高まりが供給リスクを強め、重要素材戦略の開発を促す

3.6.一次および二次ソースからの重要素材回収

3.7.一次産品からの重要素材回収の確立

3.8.採掘事業への投資が減少するにつれて、重要物質のリサイクルの重要性が増している

3.9.二次資源からの重要物質の回収方法

3.10.二次資源からの重要物質回収技術

3.11.重要物質の供給、価値、リサイクル率の概要

3.12.確立された重要白金族金属回収市場からの教訓

3.13.確立された重要素材回収市場における特徴の定義

3.14.二次ソースからの重要素材回収の市場促進要因

3.15.重要素材回収のための確立された二次ソースと新興の二次ソース

3.16.二次ソースからの重要素材回収のビジネスモデル

3.17.リサイクル収益性に影響を与え続ける重要素材価格圧力

3.18.重要素材回収を可能にするために必要な技術革新と商業革新

3.19.重要素材回収のレポート内容と概要

4.二次資料からの重要素材抽出技術

4.1.重要素材抽出の概要

4.1.1.二次資料からの臨界物質抽出技術 - 章の概要

4.1.2.臨界物質抽出技術の概要

4.1.3.臨界物質抽出:抽出技術

4.2.臨界物質抽出技術

4.2.1.湿式冶金抽出

4.2.2.二次原料からの湿式冶金金属抽出に使用される冶金剤

4.2.3.重要物質の湿式冶金抽出のSWOT分析

4.2.4.乾式製錬による金属抽出はじめに

4.2.5.高温冶金抽出:方法

4.2.6.高温冶金抽出のSWOT分析

4.2.7.バイオ冶金はじめに

4.2.8.バイオリーチングプロセスと重要素材への適用

4.2.9.バイオ冶金:開発分野

4.2.10.重要物質抽出のためのバイオ冶金のSWOT分析

4.2.11.イオン液体と深部共晶溶媒

4.2.12.イオン液体と深部共晶溶媒技術の商業化が直面する課題

4.2.13.重要物質抽出のためのイオン液体と深部共晶溶媒のSWOT分析

4.2.14.電気浸出抽出

4.2.15.重要物質抽出のための電気化学的浸出のSWOT分析

4.2.16.超臨界流体抽出

4.2.17.超臨界流体抽出技術のSWOT分析

4.3.まとめと結論

4.3.1.二次資料からの重要物質抽出のまとめ

4.3.2.臨界物質抽出技術の技術準備評価

4.3.3.重要素材抽出技術と採用状況

4.3.4.主要指標別に評価した重要素材抽出手法

4.3.5.重要素材抽出技術の価値提案の進化

5.二次資料からの重要物質回収技術

5.1.重要素材回収の概要

5.1.1.二次資源からの重要物質回収技術-章概要

5.1.2.クリティカルマテリアル回収:序論とプロセスの概要

5.1.3.臨界金属回収:回収技術

5.2.臨界物質回収技術

5.2.1.溶媒抽出による臨界物質回収

5.2.2.溶媒抽出によるレアアース元素回収

5.2.3.溶媒抽出によるリチウムイオン電池、燃料電池、電解槽からの重要金属回収と関連課題

5.2.4.溶媒抽出回収技術のSWOT分析

5.2.5.イオン交換回収

5.2.6.イオン交換樹脂を用いた臨界金属抽出

5.2.7.イオン交換樹脂回収技術のSWOT分析

5.2.8.イオン液体(IL)と深部共晶溶媒(DES)の回収

5.2.9.イオン液体/深部共晶溶媒回収と電着との結合

5.2.10.イオン液体・深部共晶溶媒回収技術が直面する課題

5.2.11.臨界物質回収のためのイオン液体と深部共晶溶媒のSWOT分析

5.2.12.沈殿による重要金属回収

5.2.13.沈殿効率を高める選択的凝集と凝集

5.2.14.臨界物質回収のための沈殿のSWOT分析

5.2.15.バイオ吸着を用いた重要金属回収

5.2.16.重要物質回収のための生物吸着のSWOT分析

5.2.17.電解採取による臨界金属回収

5.2.18.電解採取によるリチウムイオン電池と家電廃棄物からのニッケルとコバルトの回収

5.2.19.溶融塩電解を用いたレアアース酸化物(REO)処理

5.2.20.重要物質回収のための新しい電解採取システムと技術革新の分野

5.2.21.重要物質回収のための電解採取のSWOT分析

5.2.22.直接回収アプローチ:水素減容によるレアアース磁石のリサイクル

5.2.23.直接回収アプローチ:焼結によるリチウムイオン電池正極の直接リサイクル

5.2.24.直接重要材料回収技術のSWOT分析

5.3.まとめと結論

5.3.1.重要金属回収技術の評価と比較

5.3.2.二次材料からの重要材料回収技術-主な調査結果

5.3.3.二次材料からの重要材料回収技術の技術準備

5.3.4.重要材料回収技術の進化する要件

6.重要レアアース元素の回収

6.1.レアアースリサイクルの概要

6.1.1.レアアース磁石のリサイクル - 章の概要

6.1.2.レアアースリサイクルの動向

6.1.3.重要なレアアース元素はじめに

6.1.4.重要レアアース元素:製品市場と用途

6.1.5.重要レアアース元素:一次材料サプライチェーンの地理的集中

6.1.6.磁石用途に集中するレアアース需要

6.1.7.レアアース元素回収のための一次および二次材料の流れ

6.1.8.二次材料源のレアアース含有量

6.2.レアアースのリサイクル技術

6.2.1.廃棄物からレアアース磁石をリサイクルするための主要技術の概要

6.2.2.ロングループおよびショートループのレアアースリサイクル方法

6.2.3.水素減容によるショートループレアアース磁石リサイクル

6.2.4.粉末冶金によるショートループレアアース磁石リサイクル

6.2.5.ショートループ再生磁石はバージン磁石に比べて磁気特性が弱い

6.2.6.ショートループレアアース磁石リサイクルのSWOT分析

6.2.7.ロングループ磁石リサイクル

6.2.8.ロングループレアアース磁石リサイクル:回収技術

6.2.9.溶媒抽出によるロングループ磁石回収

6.2.10.溶媒抽出を使用したロングループリサイクルの運転経費(OpEx)の内訳

6.2.11.液体クロマトグラフィーのレアアース分離技術は供給原料の柔軟性を提供する

6.2.12.液体クロマトグラフィーではイオン交換樹脂を使用して磁石をリサイクルする

6.2.13.イオン交換/液体クロマトグラフィーを利用したレアアース回収の新たなビジネスモデル

6.2.14.商業的レアアース分離技術の比較

6.2.15.ロングループレアアース磁石リサイクル回収のSWOT分析

6.2.16.ショートループおよびロングループレアアース磁石リサイクル:概要と主要プレーヤー

6.2.17.磁石リサイクルにおける廃棄物の前処理と自動化の役割

6.3.レアアースリサイクル市場

6.3.1.2025年のレアアース磁石リサイクルはロングループ技術が主流

6.3.2.主要レアアースリサイクラー概要

6.3.3.新興のレアアース磁石リサイクルのバリューチェーン

6.3.4.世界のレアアース磁石リサイクル業者

6.3.5.重要なレアアースの循環型サプライチェーンが必要に迫られて台頭

6.3.6.2030年までのレアアース磁石リサイクル能力の増加により、利用率を最大化するための原料調達拡大の必要性が浮き彫りに

6.3.7.電気モーター、エネルギー発電機、ハードディスクドライブがレアアースの重要な二次供給源として浮上

6.3.8.電気ローターからのレアアース磁石リサイクルの前処理の課題

6.3.9.リサイクル用磁石の入手可能性は、統合製品の寿命とリサイクル効率に影響される

6.3.10.使用済み廃棄物の利用可能性が高まるまで、磁石製造廃棄物はリサイクル業者にとって重要な原料になる

6.3.11.多くのロングループ・リサイクラーは、二次的供給源がオンラインになるまでの間、一次鉱物原料の確保に重点を置く

6.3.12.レアアース磁石回収の成長を実現するための成長の障壁と開発が必要な分野

6.4.重要なレアアース回収の概要と展望

6.4.1.レアアース磁石回収技術の概要と展望

6.4.2.レアアース磁石市場の概要と展望

6.4.3.ロングループおよびショートループのレアアース磁石リサイクル技術の機会と傾向の概要

6.4.4.レアアース磁石リサイクルの革新分野

6.4.5.レアアース磁石リサイクルのバリューチェーン

7.重要なリチウムイオン電池材料の回収

7.1.リチウムイオン電池リサイクルの概要

7.1.1.重要なリチウムイオン電池技術の金属回収 - 章の概要

7.1.2.重要なリチウムイオン電池金属はじめに

7.1.3.重要な電池材料需要に影響を与える主な動向(1)

7.1.4.重要な電池材料需要に影響を与える主な動向(2)

7.1.5.リチウムイオン電池のリサイクルとLIB循環経済の紹介

7.1.6.リチウムイオン電池リサイクル市場の概要と主な最新情報

7.1.7.電気自動車用バッテリーのクローズドループ型バリューチェーン - LIB リサイクル原料の供給源と材料の流れ

7.1.8.世界の LIB リサイクル容量とプレーヤーマップ

7.1.9.詳細はIDTechExのレポートを参照:リチウムイオン電池リサイクル市場2025-2045:市場、予測、技術、プレーヤー

7.2.リチウムイオン電池の金属回収技術

7.2.1.リチウムイオン電池リサイクル技術の概要

7.2.2.乾式リチウムイオン電池のリサイクル

7.2.3.湿式リチウムイオン電池のリサイクル

7.2.4.リチウムイオン電池の直接リサイクル法

7.2.5.リサイクル技術の概要と比較

7.2.6.リチウムイオン電池からの黒鉛リサイクル

7.2.7.黒鉛リサイクル技術のまとめ

7.3.リチウムイオン電池の金属回収市場

7.3.1.電気自動車用バッテリーのリサイクル・バリューチェーン

7.3.2.リチウムイオン電池はいつリサイクルされるのか?

7.3.3.リチウムイオン電池のリサイクルは経済的か?

7.3.4.正極化学物質がリサイクル経済性に及ぼす影響

7.3.5.リサイクル規制と政策

7.3.6.地域別の具体的な政策目標と資金調達の概要

7.3.7.リチウムイオン電池のリサイクル政策と規制 - 世界地図

7.3.8.リチウムイオン電池のリサイクル:セクターの関与

7.3.9.地域別リチウムイオン電池リサイクル技術の内訳

7.3.10.地域別およびリサイクル技術の種類(機械的、湿式冶金/精製)別の新しい LIB リサイクル能力

8.クリティカル半導体材料回収

8.1.重要な半導体材料回収の概要

8.1.1.半導体材料回収 - 章の概要

8.1.2.重要な半導体材料:はじめに

8.1.3.重要な半導体材料:高まる需要とサプライチェーンの課題

8.1.4.重要半導体材料:用途とリサイクル率

8.2.電子廃棄物(e-waste)

8.2.1.電子廃棄物は急速に蓄積されているが、リサイクルは追いつかない

8.2.2.主要アプリケーションにおける半導体のばらつきと含有率の低さが回収を妨げている

8.2.3.電子廃棄物からの重要な半導体回収は、より効果的な前処理に依存する

8.2.4.電子廃棄物リサイクルの動向と新たな原料

8.2.5.電子廃棄物原料組成の動向

8.2.6.電子廃棄物からの重要半導体の回収

8.2.7.回収のための一次および二次ガリウムの供給源

8.2.8.ガリウムとインジウムのリサイクル業者の概要

8.2.9.二次ソースからの確立されたゲルマニウム回収

8.2.10.重要半導体材料回収のビジネスモデル

8.2.11.e-wasteリサイクルにおいて重要半導体回収は貴金属の後塵を拝する

8.3.太陽光発電とソーラー技術

8.3.1.太陽光発電パネルにおけるクリティカル半導体:はじめに

8.3.2.太陽光発電におけるクリティカル半導体:セルスタックの構成と設計

8.3.3.太陽光発電からの臨界半導体回収

8.3.4.結晶シリコンと薄膜太陽電池モジュールのリサイクルには異なるプロセスが必要

8.3.5.結晶シリコン太陽電池のシリコン回収技術

8.3.6.シリコン太陽電池モジュールのリサイクルにおける価値の大半は卑金属と貴金属の回収にある

8.3.7.シリコンPVパネルリサイクルからの回収価値の内訳

8.3.8.CdTe 薄膜太陽電池からのテルル回収

8.3.9.薄膜 CdTe PV リサイクルが直面する課題

8.3.10.ソーラーパネルメーカーとリサイクル能力 (I)

8.3.11.ソーラーパネルメーカーとリサイクル能力(II)

8.4.市場の概要と展望

8.4.1.重要半導体材料回収の結論と市場展望

8.4.2.重要半導体回収技術の技術準備

8.4.3.クリティカル半導体回収:主要プレーヤーの概要

8.4.4.クリティカル半導体回収の市場促進要因、機会、障壁

8.4.5.臨界半導体二次材料の流れを解き放つために対処すべき主要課題

9.クリティカル・マテリアル回収

9.1.クリティカル・マテリアル回収の概要

9.1.1.プラチナ族金属回収 - 章の概要

9.1.2.重要なプラチナ族金属:はじめに

9.1.3.重要なプラチナ族金属:サプライチェーンの考察

9.1.4.世界のプラチナ族金属の需要と用途区分

9.1.5.重要なプラチナ族金属:用途とリサイクル率

9.1.6.重要プラチナ族金属の回収は高い金属本来の価値によって推進される

9.1.7.過去のプラチナ族金属価格の変動

9.1.8.過去のイリジウム需給

9.2.使用済み自動車触媒からのPGM回収

9.2.1.自動車触媒中の重要PGM

9.2.2.使用済み自動車触媒からの重要PGM回収

9.2.3.自動車用スクラップからの白金、パラジウム、ロジウムの世界回収

9.2.4.自動車触媒リサイクルの世界の主要企業

9.3.水素電解槽と燃料電池からのPGM回収

9.3.1.水素経済にとっての重要金属

9.3.2.プロトン交換膜電解槽材料・コンポーネント

9.3.3.グリーン水素の重要材料への影響

9.3.4.技術的進歩とPGMリサイクルの重要性

9.3.5.新しい PEMEL 触媒への移行における課題と PGM リサイクルの役割

9.3.6.触媒コーティング膜(CCM)からの重要PGMの回収

9.3.7.燃料電池触媒からの重要PGMのリサイクル

9.3.8.プロトン交換膜触媒とアイオノマーのリサイクル:プレーヤーの概要

9.3.9.水素燃料電池と水電解槽からの重要金属リサイクルは2040年代まで実現しない

9.3.10.燃料電池用触媒の主要サプライヤー

9.4.市場の概要と展望

9.4.1.重要なPGM回収:結論と展望

9.4.2.二次ソースからの臨界的PGM回収の技術準備

9.4.3.プラチナ族金属リサイクルのビジネスモデルと既存プレーヤー

9.4.4.クリティカルPGM回収の成長機会と脅威

9.4.5.リチウムイオン電池と電気自動車産業からの貴重な教訓は、水素技術からのプラチナ族金属回収にどのような形で応用できるか

10.企業プロフィール

10.1.アキュレック・リサイクリングGmbH

10.2.ACE グリーンリサイクル

10.3.アルティリウム

10.4.アセンド・エレメンツ

10.5.オーストラリアン・ストラテジック・マテリアルズ社(ASM)

10.6.バラード・パワー・システムズ

10.7.ケアスター(ケアマグ)

10.8.ケアスター(ケアマグ)

10.9.セルサークル(バッテリーリサイクル)

10.10.サーバ・ソリューションズ

10.11.サーバ・ソリューションズ

10.12.サイクリック・マテリアル

10.13.サイクリック・マテリアル

10.14.サイリブ

10.15.エコグラフ

10.16.エコプロジェッティ

10.17.エキシゴ・リサイクル

10.18.エグジットコム・リサイクリング(バッテリーリサイクル)

10.19.フォータム(バッテリーリサイクル)

10.20.ガーナー・プロダクツ

10.21.グリーン・グラファイト・テクノロジーズ

10.22.ヘレウス水素経済用触媒

10.23.華友リサイクル

10.24.ハイプロマグ

10.25.ハイプロマグ社

10.26.イオニック・テクノロジーズ

10.27.JLマグ

10.28.リサイクル

10.29.リブレック

10.30.リチウムオーストラリア

10.31.ローム

10.32.メカウェア

10.33.ネオ・パフォーマンス・マテリアルズ - レアメタル

10.34.ノベオン・マグネティクス

10.35.オントテクノロジー

10.36.ポスコ(バッテリーリサイクル)

10.37.プリモビウス

10.38.レアアース・テクノロジーズ・インク(RETi)

10.39.レッドウッド・マテリアルズ

10.40.リエレメント・テクノロジーズ

10.41.リーテック

10.42.セロキシウム

10.43.ソーラー・マテリアル

10.44.サンイール・ハイテック

10.45.ユミコア(バッテリーリサイクル)

10.46.ヴェオリア(バッテリーリサイクル)

SummaryMarket for secondary source critical material extraction technology, critical material recovery technology, rare earth recycling, lithium-ion battery technology metal recovery, critical semiconductor recovery, platinum group metal recovery

IDTechEx forecasts that over 8.1 million tonnes of critical materials will be recovered from waste annually by 2046, equivalent to over US$66B in valuable materials. Secondary raw materials, including end-of-life equipment, automotive vehicles, electric vehicles, e-waste and manufacturing scrap, represent a rapidly emerging source of valuable critical materials. This report characterizes the critical material recovery market, key extraction and recovery technologies, emerging secondary sources and market players. The latest critical material recovery innovations are explored across four key critical material segments, including rare earth elements, Li-ion battery materials, platinum group metals, and critical semiconductors. IDTechEx identifies a growing value opportunity, with the critical material recovery market forecast to grow at a CAGR of 9.2% from 2026-2046.

Critical materials are defined as strategic materials with high supply risks and high economic value to regional economies. Critical materials such as lithium, nickel, cobalt, graphite, rare earths, platinum group metals, silicon and other semiconductors are vital in transportation, energy, communications, industrial, consumer, and defense applications. The high geographical localization of critical material supply chains presents major risks to global economies, with intensifying export controls continuing to mount pressure. As the number of critical materials increases across the world, there exists a strong market pull for critical material recovery from alternative sources to diversify and reshore strategic material supply.

Critical material recovery from secondary sources such as manufacturing scrap, end-of-life products and waste materials can mitigate supply risks while valorizing waste streams. As critical materials consolidate in electric vehicles, decarbonized energy, high performance computing and AI applications, end-of-life equipment produced at the point of consumption will become important critical material sources. IDTechEx's report characterizes key emerging critical material feedstocks, evaluating the economics of critical material recycling and business models underpinning recovery.

Critical material recovery technologies are largely ready to go: the next question is how easily they can be repurposed for secondary material sources. Pyrometallurgical and hydrometallurgical critical material recovery technologies pioneered for primary mineral processing are scalable with high recovery efficiency, making them well-positioned for deployment in secondary source streams. The outstanding challenge remains adapting the recovery processes to the complex composition profile of secondary materials, which commonly contain mixtures of critical materials with plastics, adhesives, low value metals and inorganic materials. This report evaluates 13 critical material extraction technology, providing SWOT analysis, technology readiness level benchmarking, and case studies on commercial application.

This IDTechEx research report examines four critical material segments: Li-ion battery materials, rare earth elements, platinum group metals, and critical semiconductors. Platinum group metal recovery is the most mature critical material recovery segment, driven by low global primary supply and the high intrinsic value of platinum, palladium, iridium, and rhodium metals. IDTechEx discusses how established high volume platinum group metal recycling from automotive catalysts, jewelry, and electronics can provide a roadmap for emerging critical material recovery markets. This report also characterizes the role of platinum group metals in hydrogen fuel cell and water electrolyzer technology, evaluating the developments in green hydrogen catalyst recycling.

Critical battery material recovery represents the fastest growing market segment, which IDTechEx forecasts will grow at a CAGR of 15.9% by 2046. Li-ion battery recycling is set to take-off in the mid-2030s as significant volumes of electric vehicles reach end-of-life, unlocking a new stream of secondary lithium, nickel, cobalt, graphite, copper and manganese supply. This IDTechEx report comprehensively evaluates and benchmarks hydrometallurgical, pyrometallurgical, and direct lithium-ion battery recycling technology. This report also discusses market trends in regulations, Li-ion battery recycling economics, recycling capacities, key battery recyclers and business models.

Critical rare earth recycling from magnets is a key growth market, as rare earth elements face increasing export restrictions globally. Rare earths are critical materials in high performance NdFeB and SmCo magnets used in electric vehicle motors, wind turbine energy generators, and hard disk drive actuators. With over 88% of global rare earth magnet supply consolidated in China, a strong market pull exists for critical rare earth element recycling technology. This report critically evaluates solvent extraction, liquid chromatography, hydrogen decrepitation and powder metallurgy technology for long-loop and short-loop rare earth magnet recycling. IDTechEx characterizes emerging circular supply chains, rare earth recyclers, recycling capacities and feedstock availability between 2026-2046.

Critical semiconductor recovery from electronic waste (e-waste) and photovoltaics will rely on recycling technology innovation. Automated disassembly technologies are emerging for critical semiconductor recovery, offering efficient recovery of high value material components and optimized OpEx costs within photovoltaic recycling. This report characterizes critical silicon, indium, gallium, germanium and tellurium recovery technologies and market dynamics underpinning recycling in 2026.

Key aspects of this report:

A review of technologies for critical material extraction and critical material recovery from secondary sources

Full market characterization of critical material recovery technology in key secondary source segments

Critical material recovery market analysis

Table of Contents1. EXECUTIVE SUMMARY

1.1. What are critical materials

1.2. The number of critical materials is increasing globally

1.3. Critical material recovery from primary and secondary sources

1.4. Technologies for critical material recovery from secondary sources

1.5. Established and emerging secondary sources for critical material recovery

1.6. Business models for critical material recovery from secondary sources

1.7. Critical material extraction technology overview

1.8. Technology readiness evaluation of critical material extraction techniques

1.9. Critical material extraction methods evaluated by key performance metrics

1.10. Evolution of the value proposition for critical material extraction technologies

1.11. Critical material recovery technology overview

1.12. Critical metal recovery technologies evaluated and compared

1.13. Critical material recovery technologies from secondary materials - Key findings

1.14. Overview of key technologies for recycling rare earth magnets from waste

1.15. Rare earth magnet recycling in 2025 dominated by long-loop technology

1.16. Magnet manufacturing waste to become a key feedstock for recyclers until end-of-life waste availability increases

1.17. Critical Li-ion battery technology metal recovery - Key conclusions

1.18. Li-ion battery recycling technologies summary & comparison

1.19. Li-ion battery recycling policies and regulations - global map

1.20. Critical semiconductor material recovery from secondary sources - Key conclusions

1.21. Business models for critical semiconductor material recovery

1.22. Critical platinum group metal recovery from secondary sources - Key conclusions

1.23. Business models and established players in platinum group metal recycling

1.24. Critical metal recycling from hydrogen fuel cells and water electrolyzers won't happen until 2040s

1.25. 20-year overall global recovered critical materials forecast, annual value forecast, 2026-2046

1.26. Electrification driving transfer of critical material recovery value from platinum group metals to Li-ion battery materials

1.27. 20-year overall global recovered critical materials forecast by material, annual weight forecast, 2026-2046

2. MARKET FORECASTS

2.1. Forecasting methodology and key updates

2.1.1. Forecasting methodology

2.1.2. Discontinuity in secondary source availability from renewable energy applications

2.1.3. Critical Li-ion battery material price assumptions

2.1.4. Critical rare earth material price assumptions

2.1.5. Critical platinum group metal price assumptions

2.1.6. Notable forecast updates since previous report edition (1/2)

2.1.7. Notable forecast updates since previous report edition (2/2)

2.2. Critical material recovery forecasts

2.2.1. 20-year overall global recovered critical materials forecast, annual weight forecast, 2026-2046

2.2.2. 20-year overall global recovered critical materials forecast, annual weight forecast, excluding from Li-ion batteries materials, 2026-2046

2.2.3. 20-year overall global recovered critical materials forecast by material, annual weight forecast, 2026-2046

2.2.4. 20-year overall global recovered critical materials forecast by element, annual weight forecast, excluding Li-ion battery materials, 2026-2046

2.2.5. 20-year overall global recovered critical materials forecast, annual value forecast, 2026-2046

2.2.6. 20-year overall global recovered critical materials forecast, annual value forecast, excluding from Li-ion batteries, 2026-2046

2.2.7. Electrification driving transfer of critical material recovery value from platinum group metals to Li-ion battery materials

2.2.8. 20-year global recovered critical rare earth element forecast, annual weight forecast, 2026-2046

2.2.9. 20-year global recovered critical rare earth element forecast, segmented by secondary source, annual weight forecast, 2026-2046

2.2.10. 20-year global recovered critical rare earth element forecast, annual value forecast, 2026-2046

2.2.11. 20-year global recovered critical materials from Li-ion batteries, annual weight forecast, 2026-2046

2.2.12. 20-year global recovered critical materials from Li-ion batteries, annual value forecast, 2026-2046

2.2.13. 20-year global recovered critical semiconductor material forecast, annual weight forecast, 2026-2046

2.2.14. 20-year global recovered critical semiconductor material forecast, annual weight forecast, excluding silicon, 2026-2046

2.2.15. 20-year global recovered critical semiconductor material forecast, annual value forecast, 2026-2046

2.2.16. 20-year global recovered critical platinum group metal forecast, annual weight forecast, 2026-2046

2.2.17. 20-year global recovered critical platinum group metal forecast, segmented by feedstock source, annual weight forecast, 2026-2046

2.2.18. 20-year global recovered critical platinum group forecast, annual value forecast, 2026-2046

3. INTRODUCTION

3.1. What are critical materials

3.2. The rise of the mineral economy and the emergence of critical materials

3.3. Increasing critical material demand drives growth in global supply

3.4. The number of critical materials is increasing globally

3.5. Growing export restrictions intensify supply risks and drive critical material strategy development

3.6. Critical material recovery from primary and secondary sources

3.7. Established critical material recovery from primary sources

3.8. Critical material recycling increasingly important as investment in mining operations reduces

3.9. How critical materials are recovered from secondary sources

3.10. Technologies for critical material recovery from secondary sources

3.11. Overview of critical material supply, value, and recycling rates

3.12. Lessons from the established critical platinum group metal recovery market

3.13. Defining Traits in Established Critical Material Recovery Markets

3.14. Market drivers for critical material recovery from secondary sources

3.15. Established and emerging secondary sources for critical material recovery

3.16. Business models for critical material recovery from secondary sources

3.17. Critical material price pressures continue to impact recycling profitability

3.18. Enabling technological and commercial innovation required to unlock critical material recovery

3.19. Critical material recovery report content and outline

4. CRITICAL MATERIAL EXTRACTION TECHNOLOGY FROM SECONDARY SOURCES

4.1. Overview of critical material extraction

4.1.1. Critical material extraction technology from secondary sources - Chapter overview

4.1.2. Critical material extraction technology overview

4.1.3. Critical material extraction: Extraction technologies

4.2. Critical material extraction technologies

4.2.1. Hydrometallurgical extraction

4.2.2. Lixiviants used in hydrometallurgical metal extraction from secondary material sources

4.2.3. SWOT analysis of hydrometallurgical extraction of critical material

4.2.4. Pyrometallurgical extraction: Introduction

4.2.5. Pyrometallurgical extraction: Methods

4.2.6. SWOT analysis of pyrometallurgical extraction of critical materials

4.2.7. Biometallurgy: Introduction

4.2.8. Bioleaching processes and their applicability to critical materials

4.2.9. Biometallurgy: Areas of development

4.2.10. SWOT analysis of biometallurgy for critical material extraction

4.2.11. Ionic liquids and deep eutectic solvents

4.2.12. Challenges facing commercialization of ionic liquid and deep eutectic solvent technologies

4.2.13. SWOT analysis of ionic liquids and deep eutectic solvents for critical material extraction

4.2.14. Electroleaching extraction

4.2.15. SWOT analysis of electrochemical leaching for critical material extraction

4.2.16. Supercritical fluid extraction

4.2.17. SWOT analysis of supercritical fluid extraction technology

4.3. Summary and conclusions

4.3.1. Summary of critical material extraction from secondary sources

4.3.2. Technology readiness evaluation of critical material extraction techniques

4.3.3. Critical material extraction technologies and state of adoption

4.3.4. Critical material extraction methods evaluated by key metric

4.3.5. Evolution of the value proposition for critical material extraction technologies

5. CRITICAL MATERIAL RECOVERY TECHNOLOGY FROM SECONDARY SOURCES

5.1. Overview of critical material recovery

5.1.1. Critical material recovery technology from secondary sources - Chapter overview

5.1.2. Critical material recovery: Introduction and process overview

5.1.3. Critical metal recovery: Recovery technologies

5.2. Critical material recovery technologies

5.2.1. Critical material recovery by solvent extraction

5.2.2. Rare-earth element recovery by solvent extraction

5.2.3. Critical metal recovery from Li-ion batteries, fuel cells and electrolysers with solvent extraction and associated challenges

5.2.4. SWOT analysis of solvent extraction recovery technology

5.2.5. Ion exchange recovery

5.2.6. Critical metal extraction using ion exchange resins

5.2.7. SWOT analysis of ion exchange resin recovery technology

5.2.8. Ionic liquid (IL) and deep eutectic solvent (DES) recovery

5.2.9. Coupling ionic liquid / deep eutectic solvent recovery with electrodeposition

5.2.10. Challenges facing ionic liquid and deep eutectic solvent recovery technology

5.2.11. SWOT analysis of ionic liquids and deep eutectic solvents for critical material recovery

5.2.12. Critical metal recovery by precipitation

5.2.13. Selective coagulation and flocculation to enhance precipitation efficiency

5.2.14. SWOT analysis of precipitation for critical material recovery

5.2.15. Critical metal recovery using biosorption

5.2.16. SWOT analysis of biosorption for critical material recovery

5.2.17. Critical metal recovery by electrowinning

5.2.18. Nickel and cobalt recovery from Li-ion batteries and consumer electronics waste using electrowinning

5.2.19. Rare-earth oxide (REO) processing using molten salt electrolysis

5.2.20. Emerging electrowinning systems for critical material recovery and areas for innovation

5.2.21. SWOT analysis of electrowinning for critical material recovery

5.2.22. Direct recovery approaches: Rare-earth magnet recycling by hydrogen decrepitation

5.2.23. Direct recovery approaches: Direct recycling of Li-ion battery cathodes by sintering

5.2.24. SWOT analysis of direct critical material recovery technology

5.3. Summary and Conclusions

5.3.1. Critical metal recovery technologies evaluated and compared

5.3.2. Critical material recovery technologies from secondary materials - Key findings

5.3.3. Technology readiness of critical material recovery technologies by secondary material sources

5.3.4. Evolving requirements of critical material recovery technologies

6. CRITICAL RARE EARTH ELEMENT RECOVERY

6.1. Overview of rare earth recycling

6.1.1. Rare earth magnet recycling - Chapter overview

6.1.2. Trends in rare earth recycling

6.1.3. Critical rare earth elements: Introduction

6.1.4. Critical rare earth elements: Product markets and applications

6.1.5. Critical rare earth elements: Geographic concentration of primary material supply chain

6.1.6. Rare earth element demand concentrating in magnet applications

6.1.7. Primary and secondary material streams for rare-earth element recovery

6.1.8. Rare earth element content in secondary material sources

6.2. Rare earth recycling technologies

6.2.1. Overview of key technologies for recycling rare earth magnets from waste

6.2.2. Long-loop and short-loop rare earth recycling methods

6.2.3. Short-loop rare-earth magnet recycling by hydrogen decrepitation

6.2.4. Short-loop rare-earth magnet recycling by powder metallurgy

6.2.5. Short-loop recycled magnets show weaker magnetic properties compared to virgin magnets

6.2.6. SWOT analysis of short-loop rare-earth magnet recycling

6.2.7. Long-loop magnet recycling

6.2.8. Long-loop rare-earth magnet recycling: Recovery technologies

6.2.9. Long-loop magnet recovery using solvent extraction

6.2.10. Breakdown of operating expenditure (OpEx) of long-loop recycling using solvent extraction

6.2.11. Liquid chromatography rare earth separation technology offers feedstock flexibility

6.2.12. Liquid chromatography uses ion exchange resins to recycle magnets

6.2.13. Emerging business model for rare earth recovery using ion exchange / liquid chromatography

6.2.14. Comparison of Commercial Rare Earth Separation Technologies

6.2.15. SWOT analysis of long-loop rare earth magnet recycling recovery

6.2.16. Short-loop and long-loop rare earth magnet recycling: Summary and key players

6.2.17. The role of waste pre-processing and automation in magnet recycling

6.3. Rare earth recycling markets

6.3.1. Rare earth magnet recycling in 2025 dominated by long-loop technology

6.3.2. Overview of key rare earth recyclers

6.3.3. Emerging rare earth magnet recycling value chain

6.3.4. Global rare earth magnet recyclers

6.3.5. Circular supply chains for critical rare earths are emerging out of necessity

6.3.6. Increasing rare earth magnet recycling capacity by 2030 highlights need for greater feedstock sourcing to maximize utilization

6.3.7. Electric motors, energy generators, and hard disk drives emerge as key secondary sources of rare earths

6.3.8. Pre-processing challenges for rare-earth magnet recycling from electric rotors

6.3.9. Availability of magnets for recycling influenced by lifetimes of integrated products and recycling efficiency

6.3.10. Magnet manufacturing waste to become a key feedstock for recyclers until end-of-life waste availability increases

6.3.11. Many long-loop recyclers focus on securing primary mineral feedstocks until secondary sources come online

6.3.12. Barriers to growth and areas requiring development for rare earth magnet recovery growth to be realized

6.4. Critical Rare earth recovery summary and outlook

6.4.1. Rare earth magnet recovery technology summary and outlook

6.4.2. Rare-earth magnet market summary and outlook

6.4.3. Overview of opportunities and trends for long-loop and short-loop rare earth magnet recycling technologies

6.4.4. Innovation areas for rare-earth magnet recycling

6.4.5. Rare earth magnet recycling value chain

7. CRITICAL LI-ION BATTERY MATERIAL RECOVERY

7.1. Overview of Li-ion battery recycling

7.1.1. Critical Li-ion battery technology metal recovery - Chapter overview

7.1.2. Critical Li-ion battery metals: Introduction

7.1.3. Key trends impacting critical battery material demand (1)

7.1.4. Key trends impacting critical battery material demand (2)

7.1.5. Introduction to Li-ion battery recycling and LIB circular economy

7.1.6. Li-ion battery recycling market summary and key updates

7.1.7. Closed-loop value chain of electric vehicle batteries - sources of LIB recycling feedstock and flow of materials

7.1.8. Global LIB recycling capacity and player map

7.1.9. More information can be found in IDTechEx's report: Li-ion Battery Recycling Market 2025-2045: Markets, Forecasts, Technologies, and Players

7.2. Li-ion battery metal recovery technologies

7.2.1. Overview of Li-ion battery recycling technologies

7.2.2. Pyrometallurgical Li-ion battery recycling

7.2.3. Hydrometallurgical Li-ion battery recycling

7.2.4. Direct Li-ion battery recycling methods

7.2.5. Recycling technologies summary & comparison

7.2.6. Graphite recycling from Li-ion batteries

7.2.7. Graphite recycling technology summary

7.3. Li-ion battery metal recovery markets

7.3.1. Electric vehicle battery recycling value chain

7.3.2. When will Li-ion batteries be recycled?

7.3.3. Is recycling Li-ion batteries economical?

7.3.4. Impact of cathode chemistries on recycling economics

7.3.5. Recycling regulations and policies

7.3.6. Specific policy targets and funding summary by region

7.3.7. Li-ion battery recycling policies and regulations - global map

7.3.8. Li-ion battery recycling: Sector involvement

7.3.9. Li-ion battery recycling technology breakdown by region

7.3.10. New LIB recycling capacity by region and type of recycling technology (mechanical, hydrometallurgical / refining)

8. CRITICAL SEMICONDUCTOR MATERIAL RECOVERY

8.1. Overview of critical semiconductor material recovery

8.1.1. Semiconductor material recovery - Chapter overview

8.1.2. Critical semiconductor materials: Introduction

8.1.3. Critical semiconductor materials: Rising demand and supply chain challenges

8.1.4. Critical semiconductors: Applications and recycling rates

8.2. Electronic waste (e-waste)

8.2.1. E-waste is rapidly accumulating but recycling struggles to keep up

8.2.2. Disparate and low semiconductor content in key applications is prohibiting recovery

8.2.3. Critical semiconductor recovery from e-waste will rely on more effective pre-processing

8.2.4. Trends in electronic waste recycling and emerging feedstocks

8.2.5. Trends in e-waste feedstock composition

8.2.6. Recovery of critical semiconductors from e-waste

8.2.7. Sources of primary and secondary gallium for recovery

8.2.8. Overview of gallium and indium recyclers

8.2.9. Established germanium recovery from secondary sources

8.2.10. Business models for critical semiconductor material recovery

8.2.11. Critical semiconductor recovery takes the backseat to precious metals in e-waste recycling

8.3. Photovoltaic and solar technologies

8.3.1. Critical semiconductors in photovoltaic panels: Introduction

8.3.2. Critical semiconductors in photovoltaics: Cell stack composition and design

8.3.3. Critical semiconductor recovery from photovoltaics

8.3.4. Different processes are required to recycle crystalline silicon and thin-film photovoltaic modules

8.3.5. Silicon recovery technology for crystalline-Si PVs

8.3.6. Most of the value in silicon photovoltaic module recycling resides in base and precious metal recovery

8.3.7. Breakdown of value recovered from silicon PV panel recycling

8.3.8. Tellurium recovery from CdTe thin-film photovoltaics

8.3.9. Challenges facing thin film CdTe PV recycling

8.3.10. Solar panel manufacturers and recycling capabilities (I)

8.3.11. Solar panel manufacturers and recycling capabilities (II)

8.4. Market summary and outlook

8.4.1. Conclusions for critical semiconductor material recovery and market outlook

8.4.2. Technology readiness of critical semiconductor recovery technologies

8.4.3. Critical semiconductor recovery: Key player overview

8.4.4. Market drivers, opportunities and barriers for critical semiconductor recovery

8.4.5. Key challenges that must be addressed to unlock the secondary critical semiconductor material stream

9. CRITICAL PLATINUM GROUP METAL RECOVERY

9.1. Overview of critical platinum group metal recovery

9.1.1. Platinum group metal recovery - Chapter overview

9.1.2. Critical platinum group metals: Introduction

9.1.3. Critical platinum group metals: Supply chain considerations

9.1.4. Global PGM demand and application segmentation

9.1.5. Critical platinum group metals: Applications and recycling rates

9.1.6. Critical platinum group metal recovery is driven by high intrinsic metal value

9.1.7. Historical PGM price volatility

9.1.8. Historical iridium supply and demand

9.2. PGM recovery from spent automotive catalysts

9.2.1. Critical PGMs in automotive catalysts

9.2.2. Critical PGM recovery from spent automotive catalysts

9.2.3. Global recovery of platinum, palladium and rhodium from automotive scrap

9.2.4. Key global automotive catalyst recycling players

9.3. PGM recovery from hydrogen electrolyzers and fuel cells

9.3.1. Critical metals for the hydrogen economy

9.3.2. Proton exchange membrane electrolyzer materials & components

9.3.3. Green hydrogen's influence on critical materials

9.3.4. Importance of technological advancements & PGM recycling

9.3.5. Challenges in transitioning to new PEMEL catalysts and the role of PGM recycling

9.3.6. Recovering critical PGMs from catalyst coated membranes (CCMs)

9.3.7. Recycling of critical PGMs from fuel cell catalysts

9.3.8. Proton exchange membrane catalyst and ionomer recycling: Player overview

9.3.9. Critical metal recycling from hydrogen fuel cells and water electrolyzers won't happen until 2040s

9.3.10. Key suppliers of catalysts for fuel cells

9.4. Market summary and outlook

9.4.1. Critical PGM recovery: Conclusions and outlook

9.4.2. Technology readiness of critical PGM recovery from secondary sources

9.4.3. Business models and established players in platinum group metal recycling

9.4.4. Opportunities and threats to growth for critical PGM recovery

9.4.5. What valuable lessons from the LIB & EV industries can be applied to PGM recovery from hydrogen technology

10. COMPANY PROFILES

10.1. Accurec Recycling GmbH

10.2. ACE Green Recycling

10.3. Altilium

10.4. Ascend Elements

10.5. Australian Strategic Materials Ltd (ASM)

10.6. Ballard Power Systems

10.7. Carester (Caremag)

10.8. Carester (Caremag)

10.9. CellCircle (Battery Recycling)

10.10. Cirba Solutions

10.11. Cirba Solutions

10.12. Cyclic Materials

10.13. Cyclic Materials

10.14. Cylib

10.15. EcoGraf

10.16. Ecoprogetti

10.17. Exigo Recycling

10.18. Exitcom Recycling (Battery Recycling)

10.19. Fortum (Battery Recycling)

10.20. Garner Products

10.21. Green Graphite Technologies

10.22. Heraeus: Catalysts for the Hydrogen Economy

10.23. Huayou Recycling

10.24. HyProMag

10.25. HyProMag Ltd

10.26. Ionic Technologies

10.27. JL Mag

10.28. Li-Cycle

10.29. Librec

10.30. Lithium Australia

10.31. Lohum

10.32. Mecaware

10.33. Neo Performance Materials - Rare Metals

10.34. Noveon Magnetics

10.35. OnTo Technology

10.36. POSCO (Battery Recycling)

10.37. Primobius

10.38. Rare Earth Technologies Inc. (RETi)

10.39. Redwood Materials

10.40. ReElement Technologies

10.41. REETec

10.42. Seloxium

10.43. Solar Materials

10.44. SungEel Hi-Tech

10.45. Umicore (Battery Recycling)

10.46. Veolia (Battery Recycling)

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の 先端材料 - Advanced Materials&Crisical Minerals分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|