量子センサー市場 2026-2046年:技術、動向、プレイヤー、予測Quantum Sensors Market 2026-2046: Technology, Trends, Players, Forecasts 原子時計、量子磁場センサー、重力計、ジャイロスコープ、加速度計、量子RF、単一光子検出器などの主要プレーヤー、技術、アプリケーション、材料、20年間の粒状量子センサー市場予測。 量子セ... もっと見る

サマリー

原子時計、量子磁場センサー、重力計、ジャイロスコープ、加速度計、量子RF、単一光子検出器などの主要プレーヤー、技術、アプリケーション、材料、20年間の粒状量子センサー市場予測。

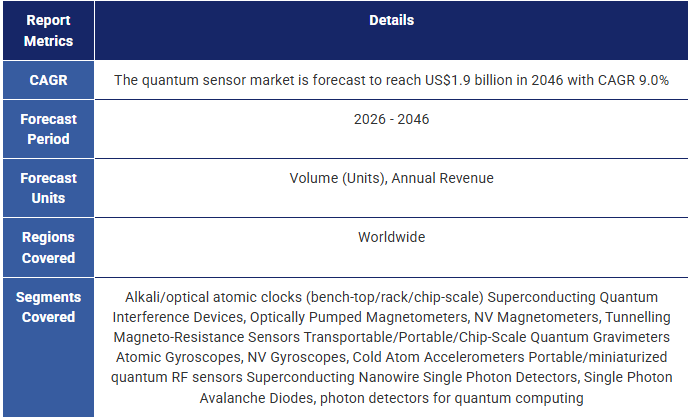

量子センサー市場は2046年までに19億米ドルに成長

量子センサーはその飛躍的な高感度化により、GPSの否定的ナビゲーション、医療画像、リモート電流センシングなどの画期的な進歩を可能にする。IDTechExの「量子センサー市場 2026-2046」レポートは、技術開発者とエンドユーザーからの一次情報に基づく40社以上の企業プロファイルを含む、量子センサー市場の広範な分析を提供しています。多様なプラットフォームとアプリケーションをカバーする本レポートは、複数のタイプの原子時計、磁場センサー、単一光子検出器を含む20種類の量子センシング技術を分析している。各技術について、動作原理、競合状況、主要アプリケーション、20年間の詳細な予測を示している。

量子センサーは、量子現象を利用して、電界、磁界、電流、重力、直線加速度、角加速度、タイミング、光など、さまざまな物理特性の高感度測定を可能にする。古典的なセンサーに比べて感度が優れているため、量子センサーは電気自動車や自律走行車、脳スキャナー、量子コンピューター、地下マッピング装置、人工衛星、顕微鏡、さらには家電製品などの用途で注目を集めている。さらに、コンピューティングや通信といった他の量子テクノロジーとの相乗効果も、量子センサー分野への関心と投資を後押ししている。

幅広い技術と用途

センサーは、現代の自動車、医療機器、家電製品の動作を支えている。例えば、量子ジャイロスコープや原子時計によってGPSを無視したより正確な自動車ナビゲーションを可能にしたり、量子磁力計によって高精度で利用しやすい脳イメージングを実現したりすることで、量子センサーは様々な技術の能力を向上させる。量子センサーの分野では、その技術やアプリケーションの多様性から、TRL(Technology Readiness Level)や市場規模に大きなばらつきがある。例えば、何百万というチップスケールのトンネル磁気抵抗(TMR)センサーは、遠隔電流センシングのために自動車分野ですでに販売されている一方、量子磁力計を使ったナビゲーションは、Q-CTRLやSandboxAQのような企業の努力によって市場に参入したばかりである。本レポートでは、研究センターや技術開発者との対話を通じて、各量子センシング技術の技術的・商業的な準備レベルを評価し、将来の開発ロードマップを提供している。

この包括的なレポートでは、原子時計、量子磁場センサー、量子ジャイロスコープ、量子加速度計、量子重力計、量子RFセンサー、単一光子検出器、量子イメージング、量子センサー用コンポーネントを取り上げている。各量子センサカテゴリは、SWOT分析と技術ベンチマーク表を用いて評価されている。主要企業は、その能力と目的から分類され、製品(入手可能な場合)は、相互および従来の既存企業に対してベンチマークされている。アプリケーションとしては、タイミング・イナーシャルナビゲーション、リモート電流センシング、生体磁気イメージング、地下資産マッピング、量子コンピューティング読み出し、ガスLiDAR、RFテストなどがある。

材料と部品はSWaP-Cを削減する上で極めて重要である

それぞれの異なるセンシング・プラットフォームには、その製造と小型化の可能性におけるユニークな課題がある。原子時計はすでにチップ・スケールまで小型化されているが、その割高なコストから、現在の使用例は航空宇宙や潜水艇のハイエンド・ナビゲーションに限られている。とはいえ、原子量子センサーの製造を最適化するために、蒸気セルやチップ・スケールのレーザーなどの主要コンポーネントの製造コストを削減する努力が続けられている。本レポートでは、量子センサーのSWaP-C(サイズ、重量、消費電力+コスト)を改善し、自律走行車やコンシューマー・エレクトロニクスにおける測位、ナビゲーション、タイミング(PNT)などの大量生産アプリケーションを実現するための材料と製造の課題を解説する。

一方、ダイヤモンド中の窒素空孔欠陥に基づく量子センサーは、そのコンパクトで堅牢な性質と室温での動作により注目を集めている。しかし、NVダイヤモンド量子センサーの普及は、Element SixやDiatopeのような、量子アプリケーション用の合成ダイヤモンドの製造を専門とするサプライチェーン企業にかかっている。本レポートでは、センサーOEMだけでなく、材料サプライヤーやエンドユーザーにも焦点を当て、様々な量子センシングコンポーネントの材料特性とサプライチェーンダイナミクスを調査している。

量子センシングの20年展望

この市場調査の結果を要約するため、量子センサー市場レポートでは、20種類の量子センシング技術の数量と年間収益の両方について20年間の予測を掲載している。それぞれのケースにおいて、明確な市場シナリオが示されており、他のセンサー市場や将来のモビリティのような隣接するトピックにおけるIDTechEx研究の幅広い専門知識を活用しながら、異なる量子センサーが互いに、また従来の既存企業からどのように市場シェアを獲得するかを予測している。

量子センサー市場レポートの主要な側面

本レポートでは、量子センシングの全体的な状況をハイレベルで評価しています。基本技術、主要センサータイプ、アプリケーションをカバーしています。

内容は以下の通りです:

目次1.要旨

1.1.量子センサー市場「概観」

1.2.量子センサー:アナリストの視点

1.3.量子センサーとは何か?

1.4.量子センサー技術とアプリケーションの概要

1.5.量子センサーの価値提案は、ハードウェアのアプローチ、アプリケーション、競合によって異なる

1.6.主要量子センシング技術の長期市場規模(数量ベース)の比較

1.7.量子センサーの主要産業

1.8.なぜナビゲーションが量子センサーの大衆市場向けアプリケーションとして最も有望なのか?

1.9.ケーススタディ陸・海・空の量子ナビゲーション

1.10.量子センサーへの投資は拡大中

1.11.量子センサー産業市場マップ

1.12.量子センサー市場は「新興」から「成長」へ

1.13.チップスケールの量子センサーでは、小型物理パッケージの製造規模拡大が重要な課題

1.14.原子およびダイヤモンドベースの量子センサー用特殊部品

1.15.量子センサー市場全体の年間売上高 2026-2046

1.16.量子センサー市場 - 主要予測結果(1)

1.17.量子センサー市場 - 主要予測結果(2)

1.18.量子センサー市場における中期的なビジネスチャンスの特定:市場規模とCAGRの比較(2026~2036年)

1.19.量子センサー市場における長期的ビジネスチャンスの特定:市場規模とCAGRの比較(2036~2046年)

1.20.量子センサー市場 - 粒状年間収益(TMRを除く) 2026-2046

1.21.原子時計:セクターロードマップ

1.22.量子磁力計:セクター別ロードマップ

1.23.量子重力計セクターロードマップ

1.24.慣性量子センサーセクター・ロードマップ

1.25.量子RFセンサーセクター・ロードマップ

1.26.単一光子検出器セクターロードマップ

1.27.IDTechEx サブスクリプションでさらにアクセス

2.量子センサー入門

2.1.市場概要

2.1.1.量子センサーとは?

2.1.2.古典と量子

2.1.3.量子現象が高感度量子センシングを可能にする

2.1.4.量子センシングの主要技術プラットフォーム

2.1.5.量子センシング技術とアプリケーションの概要

2.1.6.量子センサーの価値提案は、ハードウェアのアプローチ、アプリケーション、競争によって異なる

2.1.7.量子センサー市場は「新興」から「成長」へ

2.1.8.量子センサーへの投資は拡大傾向にある

2.1.9.チップスケールの量子センサーにとって、小型化された物理パッケージの製造規模を拡大することは重要な課題である

2.1.10.マーケティングにおける「量子センサー」の使用

2.2.主要産業と応用

2.2.1.量子センサーの主要産業

2.2.2.量子センサーの主要アプリケーション

2.2.3.なぜナビゲーションが量子センサーの最も可能性の高い大衆市場向けアプリケーションなのか?

2.2.4.ケーススタディ:陸・海・空の量子ナビゲーション

2.2.5.商用量子センサー開発への提言

3.原子時計

3.1.原子時計原子時計の概要 3.2:技術概要

3.2.はじめに高精度クロックのための高周波発振器

3.3.水晶時計の課題

3.4.超微細エネルギー準位とセシウム時間標準

3.5.原子時計は時計のドリフトを自己校正する

3.6.破壊的な原子時計技術の特定(1)

3.7.破壊的な原子時計技術の特定(2)

3.8.光原子時計

3.9.光クロックと光量子システムのための周波数コム

3.10.新しいモダリティが原子時計の分数不確かさを向上させる

3.11.携帯可能な高精度計時用チップスケール原子時計

3.12.確実な測位、航法、タイミング(PNT)は、チップスケールの原子時計の重要な用途である

3.13.ラック・サイズの原子時計は、よりコンパクトで持ち運び可能なフォーム・ファクターで高性能を提供する

3.14.精度、安定性、コストを犠牲にすることなく原子時計を小型化することが課題である

3.15.原子時計:主要プレーヤー

3.16.原子時計のハードウェア開発における主要プレーヤーの比較

3.17.キープレイヤー実験室ベースのマイクロ波原子時計

3.18.チップスケール原子時計プレーヤーのケーススタディ:マイクロセミとテレダイン

3.19.原子時計:セクター別サマリー

3.20.原子時計:エンドユーザーと対応可能市場

3.21.原子クロック:セクターロードマップ

3.22.原子時計:SWOT分析

3.23.原子時計:結論と展望

4.磁場センサー

4.1.1.量子磁場センサー:章概要

4.1.2.はじめに:磁場の測定

4.1.3.感度が量子磁界センサーの価値提案の鍵

4.1.4.ヘルスケアと量子コンピューティングにおける高感度アプリケーションは、量子磁界センサーの重要な市場機会である

4.1.5.磁界センサー・ハードウェアの分類

4.2.超伝導量子干渉素子(SQUID)-技術、応用、主要プレーヤー

4.2.1.SQUIDの応用

4.2.2.SQUID の動作原理

4.2.3.SQUID 製造サービスは専門ファウンドリによって提供されている

4.2.4.SQUIDの商業応用と市場機会

4.2.5.SQUIDの知的財産(IP)を持つ主要プレーヤーの比較

4.2.6.SQUID:SWOT分析

4.3.光励起磁力計(OPM)-技術、アプリケーション、主要プレーヤー

4.3.1.光励起型磁力計(OPM)の動作原理

4.3.2.光励起磁力計(OPM)の応用

4.3.3.新たな用途に向けたOPMの小型化

4.3.4.INSに代わるナビゲーションとしてのOPM

4.3.5.MEMS製造技術と非磁性センサーパッケージが小型光励起磁力計の鍵

4.3.6.OPMの知的財産(IP)を持つ主要プレーヤーの比較

4.3.7.医療用小型OPMを開発する主要企業の技術アプローチを比較する

4.3.8.OPM:SWOT分析

4.4.トンネル磁気抵抗センサー(TMR)-技術、用途、主要プレーヤー

4.4.1.トンネル磁気抵抗センサー(TMR)の紹介

4.4.2.トンネル磁気抵抗センサー(TMR)の動作原理と利点

4.

4.3.TMRの知的財産(IP)を持つ主要プレーヤーの比較

4.4.4.TMRの商業的応用と市場機会

4.4.5.TMR:SWOT分析

4.5.ダイヤモンド中の窒素空孔(NVセンター)-技術、用途、主要プレーヤー

4.5.1.NVセンター磁界センサーの紹介

4.5.2.NVセンター磁界センサーの動作原理

4.5.3.NV中心磁場センサーの潜在的応用範囲

4.5.4.NVダイヤモンドの利点とその応用

4.5.5.電磁場マッピング用NVダイヤモンド顕微鏡

4.5.6.量子センシングにおける合成ダイヤモンドのバリューチェーンの概要

4.5.7.量子グレードダイヤモンドのベンチマーク

4.5.8.N-Vセンター磁場センサー:SWOT分析

4.6.量子磁界センサーセクター別概要

4.6.1.量子磁界センサーの市場機会を比較する

4.6.2.量子磁界センサーの市場機会を比較する

4.6.3.磁界センサーの性能評価

4.6.4.最小検出磁場とSWaP特性の比較

4.6.5.量子磁力計:セクターロードマップ

4.6.6.結論と展望

5.重力計

5.1.1.量子重力計:章の概要

5.2.量子重力計:技術、用途、主要プレーヤー

5.2.1.重力センサーの主な用途は、公共施設や埋蔵資産のマッピング

5.2.2.原子干渉法に基づく量子重力計の動作原理

5.2.3.地下マッピングにおける量子重力センシングと既存技術の比較

5.2.4.量子重力計の主要プレイヤーの比較

5.2.5.量子重力計の開発は、レーザーメーカー、センサーOEM、エンドユーザーの協力にかかっている

5.3.量子重力計セクター別概要

5.3.1.量子重力計:SWOT分析

5.3.2.量子重力計:SWOT分析分野のロードマップ

5.3.3.結論と展望

6.慣性量子センサー(ジャイロスコープ&加速度センサー)

6.1.慣性量子センサー:序論と応用

6.1.1.量子慣性センサー:概要

6.1.2.慣性計測ユニット(IMU):入門編

6.1.3.推測航法によるナビゲーション

6.1.4.ドリフトの蓄積

6.1.5.IMUの主要アプリケーション

6.1.6.小型衛星コンステレーション・ナビゲーション・システムにおける慣性量子センサーの主な応用

6.1.7.GNSS が否定された環境でのナビゲーションは、チップスケールの慣性量子センサの将来のアプリケーションになる可能性がある

6.1.8.次世代 MEMS 加速度計とジャイロスコープが量子センサーと競合

6.2.量子ジャイロスコープ:技術、開発、主要プレイヤー

6.2.1.原子量子ジャイロスコープの動作原理

6.2.2.MEMS 製造プロセスにより原子ジャイロスコープ技術を小型化し、より大量生産が可能

6.2.3.ジャイロスコープ技術の展望

6.2.4.量子ジャイロスコープと MEMS ジャイロスコープ、光学ジャイロスコープとの比較

6.2.5.原子ジャイロスコープの知的財産(IP)を持つ主要プレイヤーの比較

6.2.6.量子ジャイロスコープの開発はレーザーメーカー、センサーOEM、エンドユーザーの協業にかかっている

6.2.7.量子ジャイロの主要プレーヤーを比較する

6.2.8.量子ジャイロスコープ:SWOT分析

6.3.量子加速度センサー:技術、開発、主要プレイヤー

6.3.1.量子加速度ピックアップの動作原理

6.3.2.グレーティングMOTが冷原子量子センサーの小型化を可能にする

6.3.3.加速度センサー・アプリケーションの展望

6.3.4.量子加速度センサーの主要企業の比較

6.3.5.量子加速度センサー:SWOT分析

6.3.6.慣性量子センサー:セクターサマリー

6.4.慣性量子センサーセクターロードマップ

6.4.1.結論と展望

7.高周波(RF)センサー

7.1.1.量子 RF センサーは古典的センサーの基本的課題を克服する

7.1.2.量子 RF センサーの価値提案

7.1.3.量子 RF センサーの商業的ユースケース

7.1.4.量子 RF センサー:サイズとコストの開発動向

7.1.5.量子RFセンサーの種類の概要

7.2.リュードベリ原子電界センサーと RF 受信機

7.2.1.リュードベリ原子の原理:電場センシングの実現

7.2.2.リュードベリRFセンシングの原理:EIT分光法

7.2.3.リュードベリRFレシーバーは、SIトレーサビリティを含むさらなる利点を提供する

7.2.4.次世代5G通信を可能にするリュードベリRF

7.2.5.商業用リュードベリ無線:Infleqtion、Rydberg Technologies、TZH Quantum Tech

7.2.6.計測と無線試験がリュードベリRFの短期的な商業利用を可能にする

7.2.7.リュードベリRFセンサー/レシーバーに関するトップ特許保有者

7.2.8.研究機関および中国の主要特許

7.2.9.SWOT分析:リュードベリ原子RFセンサー

7.3.窒素空孔中心電界センサーとRFレシーバー

7.3.1.NV中心RFレシーバーの原理

7.3.2.高周波アナライザーとしてのNVダイヤモンド

7.3.3.利点は応用の可能性につながる

7.3.4.EUが支援するAMADEUSプロジェクトがNVセンサーの商業的開発を主導

7.3.5.NVセンター電場・RFセンサーの現在の課題 - 磁場センシングの影に隠れている?

7.3.6.量子グレード・ダイヤモンドのベンチマーク

7.3.7.SWOT分析:NVダイヤモンド電界センサーとRFレシーバー

7.4.量子RFセンサー:分野のまとめ

7.4.1.量子RFセンサーの現在の市場概況

7.4.2.量子RFセンサー:分野のロードマップ

7.4.3.結論と展望:量子 RF センサー

8.単一光子検出器と量子イメージング

8.1.1.セクションの概要:単一光子検出器と量子イメージング

8.1.2.セクションの概要目次

8.1.3.単一光子イメージングと量子イメージング - 3つの主要トレンド

8.2.単一光子検出器

8.2.1.単一光子検出器の紹介

8.2.2.本レポートにおける単一光子検出器の分類

8.3.半導体単一光子検出器

8.4.背景と文脈

8.4.1.半導体光子検出器の紹介

8.4.2.SPADの動作原理アバランシェフォトダイオード(APD)の基礎

8.4.3.単一光子アバランシェダイオード(SPAD)の動作原理

8.4.4.SPADを直列に並べたアレイは、従来のPMTに代わる固体光電子増倍管(SiPM)を形成することができる

8.4.5.SPAD/SiPMと従来のフォトダイオードとの比較

8.5.次世代 SPAD

8.5.1.次世代 SPAD の革新

8.5.2.次世代SPADの主要プレーヤーとイノベーター

8.5.3.分解能とタイミング性能のトレードオフで形成される SPAD のアプリケーション

8.5.4.主要 SPAD プレーヤーグループの開発動向

8.5.5.SPAD アレイの画素数とタイミング機能の向上を可能にする高度な半導体パッケージング技術

8.5.6.ケーススタディ:カメラ大手のキヤノンとソニーが低照度イメージングと LiDAR 用の高解像度 SPAD アレイを開発

8.5.7.代替半導体 SPAD がシリコンの範囲を超える赤外波長を解き放つ(1)

8.5.8.代替半導体 SPAD がシリコンの範囲を超える赤外波長を解き放つ(2)

8.5.9.TCSPCとSPADの使用により、ピコ秒精度のバイオイメージングとシングルフォトンLiDARが可能になる

8.5.10.SWIR SPAD アレイによる高性能タイミング分解能が温室効果ガス LiDAR を可能にする

8.5.11.水中イメージングにおけるTCSPC SPAD LiDAR

8.5.12.SPAD のバイオイメージング応用

8.5.13.量子通信と量子コンピューティングにおける SPAD と SNSPD の競争か協力か?

8.5.14.新興 SPAD:SWOT分析

8.6.超伝導単一光子検出器

8.7.超伝導ナノワイヤー単一光子検出器(SNSPD)

8.7.1.超伝導ナノワイヤー単一光子検出器(SNSPD)

8.7.2.SNSPD の応用は、極低温のバルクやコストを正当化できるほど性能を高く評価する必要がある

8.7.3.キロピクセルを超える SNSPD アレイのスケーリング研究

8.7.4.超伝導材料の進歩が SNSPD 開発の原動力

8.7.5.商用SNSPDプレーヤーの比較

8.7.6.SWOT分析:超伝導ナノワイヤー単一光子検出器(SNSPD)

8.8.運動インダクタンス検出器(KID)とトランジション・エッジ・センサ(TES)

8.8.1.運動インダクタンス検出器(KID)

8.8.2.トランジション・エッジ・センサ(TES)

8.8.3.KID と TES が研究段階にとどまっている間に、SNSPD はどのように普及したのか?

8.9.単一光子検出器まとめ

8.9.1.単一光子検出器技術の比較

8.9.2.単一光子検出器のロードマップ

8.9.3.単一光子検出器の3つのポイント

8.10.量子イメージング

8.10.1.量子イメージング入門

8.10.2.量子もつれ:量子レーダーとゴーストイメージングの実現

8.10.3.ゴーストイメージングの紹介

8.10.4.EUのFastGhostプロジェクトがゴーストイメージングの商業的開発を主導

8.10.5.非線形干渉計(量子ホログラフィー)

8.10.6.QUANCERプロジェクトは、癌検出のための量子ホログラフィーを開発している

8.10.7.がん検出のための中赤外非線形干渉計を開発するDigistain

8.10.8.グルコース・モニタリングのための量子イメージングが実用化の初期段階にある

8.10.9.量子レーダー

8.10.10.量子イメージングの一般的利点

8.10.11.量子粒子センサーは光の重ね合わせ状態を利用して、より多くの情報を探ることができる

8.10.12.SWOT分析:量子イメージング

8.10.13.量子イメージングのための3つのポイント

9.量子センシングのためのコンポーネント

9.1.セクションの概要量子センシング用コンポーネント

9.2.原子およびダイヤモンドベースの量子センシング用特殊コンポーネント

9.3.量子センシング用コンポーネントの主要企業

9.4.蒸気電池:背景と文脈

9.5.量子センシングにおける蒸気セルの商業的製造における革新

9.6.量子センシング用蒸気セルの高真空製造要件を克服するために使用されるアルカリアジド

9.7.チップスケールの蒸気電池開発における主要企業の比較

9.8.SWOT分析:小型化ベーパーセル

9.9.VCSEL:背景と文脈

9.10.VCSEL は量子センサーとコンポーネントの小型化を可能にする

9.11.量子センシング用 VCSEL の主要プレーヤーを比較する

9.12.SWOT 分析:VCSEL

9.13.量子センサーの高性能化を可能にするために必要な特殊な制御エレクトロニクスと光学パッケージ

9.14.量子のためのフォトニックと半導体の統合製品は開発されているが、まだ大量市場の開拓には至っていない

9.15.量子を既存のフォトニクスに統合するためのハードウェアの課題

9.16.量子センシングコンポーネントのロードマップ

9.17.量子センシングコンポーネントとそのアプリケーションのロードマップ

10.市場予測

10.1.1.予測の概要

10.1.2.予測手法の概要

10.1.3.主要量子センシング技術の長期市場規模(数量ベース)の比較

10.1.4.量子センサー市場全体-年間売上高 2026-2046

10.1.5.量子センサー市場 - 主要予測結果(1)

10.1.6.量子センサー市場 - 主要予測結果(2)

10.1.7.量子センサー市場における中期的なビジネスチャンスの特定:市場規模とCAGRの比較(2026~2036年)

10.1.8.量子センサー市場における長期的なビジネスチャンスの特定:市場規模とCAGRの比較(2036~2046年)

10.1.9.量子センサー市場全体-粒度別年間収益(2026年~2046年)

10.1.10.量子センサー市場 - 粒状年間収益(TMRを除く) 2026-2046

10.2.原子時計

10.2.1.原子時計市場動向の概要:年間売上高予測 2026-2046

10.2.2.ベンチ/ラックスケール原子時計:年間販売数量予測 2026-2046

10.2.3.チップスケール原子時計:年間販売数量予測 2026-2036

10.2.4.チップスケール原子時計、年間販売数量予測 2026-2046

10.2.5.原子時計技術の市場予測まとめ

10.3.量子磁界センサー

10.3.1.量子磁界センサー市場動向の概要

10.3.2.量子センサー市場に長期的な影響を与える世界の自動車販売動向

10.3.3.TMRセンサー、年間販売台数予測 2026-2046

10.3.4.TMRセンサー、年間売上高予測 2026-2046

10.3.5.SQUID、OPM、NVM - 年間販売数量予測 2026-2046

10.3.6.SQUID、OPM、NVM - 年間販売数量予測 2026-2046

10.3.7.量子磁界センサー技術の市場予測まとめ

10.3.8.慣性量子センサー(ジャイロスコープと加速度センサー)

10.3.9.量子ジャイロスコープと加速度センサーの年間売上高 2026-2046

10.4.慣性量子センサー、年間販売数量予測 2026-2046

10.4.1.量子ジャイロスコープ&加速度センサーの予測に関する主な結論

10.5.量子重力計

10.5.1.量子重力計の年間売上高 2026-2046

10.5.2.量子重力計の年間販売台数予測 2026-2046

10.5.3.量子重力計の技術予測に関する主要結論のまとめ

10.6.量子RFセンサー

10.6.1.量子RFセンサーの年間売上高 2026-2046

10.6.2.量子 RF センサーの年間販売量予測 2026-2046

10.7.単一光子検出器

10.7.1.単一光子検出器の年間売上高 2026-2046

10.7.2.単一光子検出器の年間販売量予測 2026-2046

10.7.3.単一光子検出器の予測分析:フォトニック量子コンピューティング

11.企業プロファイル

11.1.エージック

11.2.Artilux Inc

11.3.ビヨンド・ブラッド・ダイアグノスティックス

11.4.BT (Quantum Radio Research)

11.5.CEA Leti(量子テクノロジー)

11.6.セルカ・マグネティクス

11.7.コベシオン社

11.8.CPI EDB(量子センシング)

11.9.クロッカス・テクノロジー

11.10.ダイアトープ

11.11.デジステイン(量子センシング)

11.12.エレメント・シックス(量子テクノロジー)

11.13.フラウンホーファーCAP

11.14.ID Quantique(単一光子検出器)

11.15.Infleqtion (Cold Quanta)

11.16.メンロ・システムズ社

11.17.ニューラニクス

11.18.NIQSテクノロジー社

11.19.オードナンス・サーベイ

11.20.フォトンフォース

11.21.ポラリトン・テクノロジーズ

11.22.パワーレイズ

11.23.PsiQuantum

11.24.Q-CTRL(量子ナビゲーション)

11.25.Q.ANT

11.26.青源天紫光センシングテクノロジー

11.27.QLMテクノロジーメタン感知LiDAR

11.28.量子コンピューティング社

11.29.量子経済開発コンソーシアム(QED-C)

11.30.クォンタム・テクノロジーズ

11.31.クォンタム・バレー・アイデア・ラボ

11.32.QuiX Quantum

11.33.QZabre

11.34.RobQuant

11.35.リュードベリ・テクノロジーズ

11.36.サンドボックスAQ(量子センシング)

11.37.SEEQC

11.38.セミワイズ

11.39.センコーアドバンスコンポーネンツ

11.40.シングル・クォンタム

11.41.ダルムシュタット工科大学(量子イメージング)

11.43.VTTマニュファクチャリング(量子テクノロジー)

11.44.XeedQ

Summary

Key players, technologies, applications, materials, and 20-year granular quantum sensor market forecasts for: atomic clocks, quantum magnetic field sensors, gravimeters, gyroscopes, accelerometers, quantum RF, and single photon detectors.

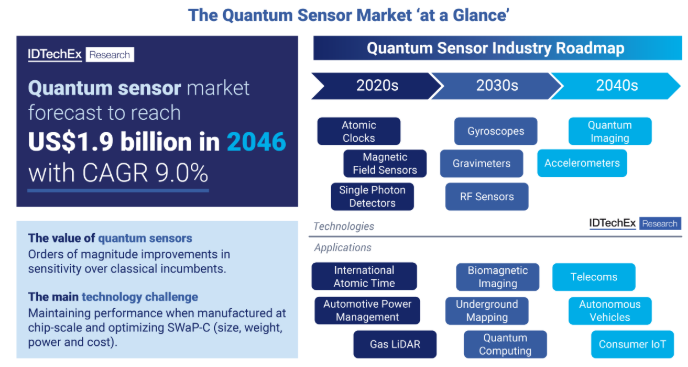

Quantum sensor market to grow to US$1.9B by 2046

Quantum sensors enable breakthroughs in GPS denied navigation, medical imaging, remote current sensing, and more through their dramatically increased sensitivity. IDTechEx's Quantum Sensor Market 2026-2046 report provides an extensive analysis of the quantum sensor market, including over 40 company profiles based on primary information from technology developers and end users. Covering a diverse range of platforms and applications, this report analyses 20 different quantum sensing technologies including multiple types of atomic clocks, magnetic field sensors, and single photon detectors. For each technology the operating principles, competitive landscape, key applications, and a granular 20-year forecast are presented.

Quantum sensors use quantum phenomena to enable highly sensitive measurements of a range of physical properties including electric and magnetic fields, current, gravity, linear and angular acceleration, timing, and light. Superior sensitivity relative to their classical counterparts means that quantum sensors are attracting interest for applications including in electric and autonomous vehicles, brain scanners, quantum computers, underground mapping equipment, satellites, microscopes, and even consumer electronics. Furthermore, growing hype and synergistic development with other quantum technologies such as computing and communications assist in driving interest and investment into the quantum sensor space.

A Wide Range of Technologies and Applications

Sensors underpin the operation of modern vehicles, medical devices, and consumer electronics. Quantum sensors are set to enhance the capabilities of a range of technologies, for example by enabling more accurate GPS-denied navigation in vehicles through quantum gyroscopes and atomic clocks, or by unlocking highly accurate and accessible brain imaging through quantum magnetometers. Given the diversity of technologies and target applications, there is significant variation of technology readiness level (TRL) and addressable market size across the quantum sensor space. For example, millions of chip-scale tunnelling magneto resistance (TMR) sensors have already been sold into the automotive sector for remote current sensing, whilst navigation with quantum magnetometers is just entering the market through the efforts of companies like Q-CTRL and SandboxAQ. Through conversations with both research centers and technology developers, this report assesses the technical and commercial readiness level of each underlying quantum sensing technology and provides a roadmap for future development.

This comprehensive report covers atomic clocks, quantum magnetic field sensors, quantum gyroscopes, quantum accelerometers, quantum gravimeters, quantum RF sensors, single photon detectors, quantum imaging, and components for quantum sensors. Each quantum sensor category is assessed using SWOT analyses and technical benchmarking tables. Key players are classified in terms of their capabilities and aims, and products (where available) are benchmarked against each other and their classical incumbents. Applications explored include timing and inertial navigation, remote current sensing, biomagnetic imaging, underground asset mapping, quantum computing readout, gas LiDAR, and RF testing.

Materials and Components are Pivotal to Reducing SWaP-C

With each different sensing platform comes a unique set of challenges in their manufacture and potential for miniaturization. While atomic clocks have already been brought down to the chip-scale, their premium cost limits current use cases to high-end navigation in aerospace and submersibles. Nevertheless, there are ongoing efforts to reduce the cost of producing key components such as vapor cells and chip-scale lasers to optimize the production of atomic quantum sensors. This report breaks down the materials and manufacturing challenges in improving the SWaP-C (size, weight, and power + cost) of quantum sensors to unlock higher-volume applications such as positioning, navigation, and timing (PNT) in autonomous vehicles or consumer electronics.

Meanwhile, quantum sensors based on nitrogen-vacancy defects in diamond are garnering attention due to their compact, robust nature and operation at room temperature. However, any wider adoption of NV diamond quantum sensors will hinge on players in the supply chain that specialize in manufacturing synthetic diamond for quantum applications such as Element Six and Diatope. This report explores the material properties and supply chain dynamics for a range of quantum sensing components, focusing not only on sensor OEMs but also materials suppliers and end users.

20-year Outlook for Quantum Sensing

To summarize the results of this market research, the Quantum Sensors Market report contains 20-year forecasts for both the volume and annual revenue of 20 different quantum sensing technologies. In each case, clear market narratives are presented, predicting how different quantum sensors will claim market share from each other and from classical incumbents, drawing on the wider expertise of IDTechEx research in other sensor markets and adjacent topics such as future mobility.

Key Aspects of the Quantum Sensors Market Report

This report provides a high-level assessment of the overall quantum sensing landscape. Covering fundamental technologies, key sensor types, and applications. This includes:

Table of Contents1. EXECUTIVE SUMMARY

1.1. The quantum sensor market 'at a glance'

1.2. Quantum sensors: Analyst viewpoint

1.3. What are quantum sensors?

1.4. Overview of quantum sensing technologies and applications

1.5. The value proposition of quantum sensors varies by hardware approach, application and competition

1.6. Comparing the scale of long-term markets (in volume) for key quantum sensing technologies

1.7. Key industries for quantum sensors

1.8. Why is navigation the most likely mass-market application for quantum sensors?

1.9. Case studies: Quantum navigation for land, sea, and air

1.10. Investment in quantum sensing is growing

1.11. Quantum sensor industry market map

1.12. The quantum sensors market will transition from 'emerging' to 'growing'

1.13. Scaling up manufacture of miniaturized physics packages is a key challenge for chip-scale quantum sensors

1.14. Specialized components for atomic and diamond-based quantum sensing

1.15. Total quantum sensor market - annual revenue 2026-2046

1.16. Quantum sensor market - Key forecasting results (1)

1.17. Quantum sensor market - Key forecasting results (2)

1.18. Identifying medium term opportunities in the quantum sensor market: Market size vs CAGR (2026-2036)

1.19. Identifying long term opportunities in the quantum sensor market: Market size vs CAGR (2036-2046)

1.20. Quantum sensor market - Granular annual revenue (excluding TMR) 2026-2046

1.21. Atomic clocks: Sector roadmap

1.22. Quantum magnetometers: Sector roadmap

1.23. Quantum gravimeters: Sector roadmap

1.24. Inertial quantum sensors: Sector roadmap

1.25. Quantum RF sensors: Sector roadmap

1.26. Single photon detectors: Sector roadmap

1.27. Access More With an IDTechEx Subscription

2. INTRODUCTION TO QUANTUM SENSORS

2.1. Market Overview

2.1.1. What are quantum sensors?

2.1.2. Classical vs Quantum

2.1.3. Quantum phenomena enable highly-sensitive quantum sensing

2.1.4. Key technology platforms for quantum sensing

2.1.5. Overview of quantum sensing technologies and applications

2.1.6. The value proposition of quantum sensors varies by hardware approach, application and competition

2.1.7. The quantum sensors market will transition from 'emerging' to 'growing'

2.1.8. Investment in quantum sensing is growing

2.1.9. Scaling up manufacture of miniaturized physics packages is a key challenge for chip-scale quantum sensors

2.1.10. The use of 'quantum sensor' in marketing

2.2. Key Industries & Applications

2.2.1. Key industries for quantum sensors

2.2.2. Highlighting the key applications for quantum sensors

2.2.3. Why is navigation the most likely mass-market application for quantum sensors?

2.2.4. Case studies: Quantum navigation for land, sea, and air

2.2.5. Recommendations for the development of commercial quantum sensors

3. ATOMIC CLOCKS

3.1. Atomic Clocks: Chapter Overview Atomic Clocks: Technology Overview

3.2. Introduction: High frequency oscillators for high accuracy clocks

3.3. Challenges with quartz clocks

3.4. Hyperfine energy levels and the cesium time standard

3.5. Atomic clocks self-calibrate for clock drift

3.6. Identifying disruptive atomic-clock technologies (1)

3.7. Identifying disruptive atomic-clock technologies (2)

3.8. Optical atomic clocks

3.9. Frequency combs for optical clocks and optical quantum systems

3.10. New modalities enhance fractional uncertainty of atomic clocks

3.11. Chip Scale Atomic Clocks for portable precision time-keeping

3.12. Assured positioning, navigation, and timing (PNT) is a key application for chip-scale atomic clocks

3.13. Rack-sized clocks offer high performance in a more compact and portable form-factor

3.14. A challenge remains to miniaturize atomic clocks without compromising on accuracy, stability and cost

3.15. Atomic Clocks: Key Players

3.16. Comparing key players in atomic clock hardware development

3.17. Key players: Lab-based microwave atomic clocks

3.18. Chip-scale atomic clock player case study: Microsemi and Teledyne

3.19. Atomic Clocks: Sector Summary

3.20. Atomic clocks: End users and addressable markets

3.21. Atomic clocks: Sector roadmap

3.22. Atomic Clocks: SWOT analysis

3.23. Atomic clocks: Conclusions and outlook

4. MAGNETIC FIELD SENSORS

4.1.1. Quantum magnetic field sensors: chapter overview

4.1.2. Introduction: Measuring magnetic fields

4.1.3. Sensitivity is key to the value proposition for quantum magnetic field sensors

4.1.4. High-sensitivity applications in healthcare and quantum computing are key market opportunities for quantum magnetic field sensors

4.1.5. Classifying magnetic field sensor hardware

4.2. Superconducting Quantum Interference Devices (SQUIDs) - Technology, Applications and Key Players

4.2.1. Applications of SQUIDs

4.2.2. Operating principle of SQUIDs

4.2.3. SQUID fabrication services are offered by specialist foundries

4.2.4. Commercial applications and market opportunities for SQUIDs

4.2.5. Comparing key players with SQUID intellectual property (IP)

4.2.6. SQUIDs: SWOT analysis

4.3. Optically Pumped Magnetometers (OPMs) - Technology, Applications, and Key Players

4.3.1. Operating principles of Optically Pumped Magnetometers (OPMs)

4.3.2. Applications of optically pumped magnetometers (OPMs)

4.3.3. Miniaturizing OPMs for emerging applications

4.3.4. OPMs as a navigation alternative to INS

4.3.5. MEMS manufacturing techniques and non-magnetic sensor packages key for miniaturized optically pumped magnetometers

4.3.6. Comparing key players with OPM intellectual property (IP)

4.3.7. Comparing the technology approaches of key players developing miniaturized OPMs for healthcare

4.3.8. OPMs: SWOT analysis

4.4. Tunneling Magneto Resistance Sensors (TMRs) - Technology, Applications, and Key Players

4.4.1. Introduction to tunneling magnetoresistance sensors (TMR)

4.4.2. Operating principle and advantages of tunneling magnetoresistance sensors (TMR)

4.4.3. Comparing key players with TMR intellectual property (IP)

4.4.4. Commercial applications and market opportunities for TMRs

4.4.5. TMRs: SWOT analysis

4.5. Nitrogen Vacancy in Diamond (NV Centers) - Technology, Applications, and Key Players

4.5.1. Introduction to NV center magnetic field sensors

4.5.2. Operating Principles of NV center magnetic field sensors

4.5.3. A range of potential applications of NV center magnetic field sensors

4.5.4. Advantages of NV diamonds and their applications

4.5.5. NV diamond microscopes for electromagnetic field mapping

4.5.6. Overview of the synthetic diamond value chain in quantum sensing

4.5.7. Quantum grade diamond benchmarked

4.5.8. N-V Center Magnetic Field Sensors: SWOT analysis

4.6. Quantum Magnetic Field Sensors: Sector Summary

4.6.1. Comparing market opportunities for quantum magnetic field sensors

4.6.2. Comparing market opportunities for quantum magnetic field sensors

4.6.3. Assessing the performance of magnetic field sensors

4.6.4. Comparing minimum detectable field and SWaP characteristics

4.6.5. Quantum magnetometers: Sector roadmap

4.6.6. Conclusions and outlook

5. GRAVIMETERS

5.1.1. Quantum gravimeters: Chapter overview

5.2. Quantum Gravimeters: Technologies, Applications and Key Players

5.2.1. The main application for gravity sensors is for mapping utilities and buried assets

5.2.2. Operating principles of atomic interferometry-based quantum gravimeters

5.2.3. Comparing quantum gravity sensing with incumbent technologies for underground mapping

5.2.4. Comparing key players in quantum gravimeters

5.2.5. Quantum gravimeter development depends on collaboration between laser manufacturers, sensor OEMs and end-users

5.3. Quantum gravimeters: Sector Summary

5.3.1. Quantum Gravimeters: SWOT analysis

5.3.2. Quantum gravimeters: Sector roadmap

5.3.3. Conclusions and outlook

6. INERTIAL QUANTUM SENSORS (GYROSCOPES & ACCELEROMETERS)

6.1. Inertial Quantum Sensors: Introduction and Applications

6.1.1. Quantum inertial sensors: Chapter overview

6.1.2. Inertial Measurement Units (IMUs): An introduction

6.1.3. Navigation by Dead Reckoning

6.1.4. Drift Accumulation

6.1.5. IMU key applications

6.1.6. Key application for inertial quantum sensors in small-satellite constellation navigation systems

6.1.7. Navigation in GNSS denied environments could be a future application for chip-scale inertial quantum sensors

6.1.8. Next-generation MEMS accelerometers and gyroscopes compete with quantum sensors

6.2. Quantum Gyroscopes: Technologies, Developments and Key Players

6.2.1. Operating principles of atomic quantum gyroscopes

6.2.2. MEMS manufacturing processes can miniaturize atomic gyroscope technology for higher volume applications

6.2.3. Gyroscope technology landscape

6.2.4. Comparing quantum gyroscopes with MEMS gyroscopes and optical gyroscopes

6.2.5. Comparing key players with atomic gyroscope intellectual property (IP)

6.2.6. Quantum gyroscope development depends on collaboration between laser manufacturers, sensor OEMs and end-users

6.2.7. Comparing key players in quantum gyroscopes

6.2.8. Quantum Gyroscopes: SWOT analysis

6.3. Quantum Accelerometers: Technologies, Developments and Key Players

6.3.1. Operating principles of quantum accelerometers

6.3.2. Grating MOTs enable the miniaturization of cold atom quantum sensors

6.3.3. Accelerometer application landscape

6.3.4. Comparing key players in quantum accelerometers

6.3.5. Quantum Accelerometers: SWOT Analysis

6.3.6. Inertial Quantum Sensors: Sector Summary

6.4. Inertial Quantum Sensors: Sector roadmap

6.4.1. Conclusions and outlook

7. RADIO FREQUENCY (RF) SENSORS

7.1.1. Quantum RF sensors overcome fundamental challenges of their classical counterparts

7.1.2. Value proposition of quantum RF sensors

7.1.3. Commercial use cases for quantum RF sensors

7.1.4. Quantum RF sensors: Size and cost development trends

7.1.5. Overview of types of quantum RF sensors

7.2. Rydberg Atom Electric Field Sensors and RF Receivers

7.2.1. Principles of Rydberg atoms: Enabling electric field sensing

7.2.2. Principles of Rydberg RF sensing: EIT spectroscopy

7.2.3. Rydberg RF receivers offer additional benefits including SI-traceability

7.2.4. Rydberg RF to enable next-gen 5G communications

7.2.5. Commercial Rydberg Radio: Infleqtion, Rydberg Technologies and TZH Quantum Tech

7.2.6. Metrology and over-the-air testing offers a near term commercial use for Rydberg RF

7.2.7. Top patent holders on Rydberg RF sensors/receivers

7.2.8. Research institutes & China leading patents

7.2.9. SWOT analysis: Rydberg atom RF sensors

7.3. Nitrogen-Vacancy Centre Electric Field Sensors and RF Receivers

7.3.1. Principles of NV center RF receivers

7.3.2. NV diamonds as radio frequency analysers

7.3.3. Advantages translate into potential applications

7.3.4. EU-backed AMADEUS project leading commercial NV sensor development

7.3.5. Current challenges for NV center electric field and RF sensors - overshadowed by magnetic field sensing?

7.3.6. Quantum grade diamond benchmarked

7.3.7. SWOT analysis: NV diamond electric field sensors and RF receivers

7.4. Quantum RF Sensors: Sector Summary

7.4.1. Summary of the current market landscape for quantum RF sensors

7.4.2. Quantum RF sensors: Sector roadmap

7.4.3. Conclusions and Outlook: Quantum Radio Frequency Field Sensors

8. SINGLE PHOTON DETECTORS AND QUANTUM IMAGING

8.1.1. Section overview: Single photon detectors and quantum imaging

8.1.2. Section overview: Contents

8.1.3. Single photon imaging and quantum imaging - 3 key trends

8.2. Single Photon Detectors

8.2.1. Introduction to single photon detectors

8.2.2. Classification of single photon detectors in this report

8.3. Semiconductor Single Photon Detectors

8.4. Background and Context

8.4.1. Introduction to semiconductor photon detectors

8.4.2. Operating principles of SPADs: Avalanche photodiode (APD) basics

8.4.3. Operating principles of single-photon avalanche diodes (SPADs)

8.4.4. Arrays of SPADs in series can form silicon photomultipliers (SiPMs) as a solid-state alternative to traditional PMTs

8.4.5. Comparison of SPAD/SiPM to established photodiodes

8.5. Next generation SPADs

8.5.1. Innovation in the next generation of SPADs

8.5.2. Key players and innovators in the next generation of SPADs

8.5.3. Applications of SPADs formed in a trade-off of resolution and timing performance

8.5.4. Development trends for groups of key SPAD players

8.5.5. Advanced semiconductor packaging techniques enabling higher pixel counts and timing functionality for SPAD arrays

8.5.6. Case Study: Camera giants Canon and Sony developing high-res SPAD arrays for low-light imaging & LiDAR

8.5.7. Alternative semiconductor SPADs unlock infrared wavelengths beyond the range of silicon (1)

8.5.8. Alternative semiconductor SPADs unlock infrared wavelengths beyond the range of silicon (2)

8.5.9. Use of SPADs with TCSPC enables picosecond precision bioimaging and single photon LiDAR

8.5.10. High-performance timing resolution with SWIR SPAD arrays enables greenhouse gas LiDAR

8.5.11. TCSPC SPAD LiDAR in underwater imaging

8.5.12. Bioimaging applications of SPADs

8.5.13. Competition or cooperation for SPADs and SNSPDs in quantum communications and computing?

8.5.14. Emerging SPADs: SWOT analysis

8.6. Superconducting single photon detectors

8.7. Superconducting nanowire single photon detector (SNSPD)

8.7.1. Superconducting nanowire single photon detectors (SNSPDs)

8.7.2. SNSPD applications must value performance highly enough to justify the bulk/cost of cryogenics

8.7.3. Research in scaling SNSPD arrays beyond kilopixel

8.7.4. Advancements in superconducting materials drives SNSPD development

8.7.5. Comparison of commercial SNSPD players

8.7.6. SWOT analysis: Superconducting nanowire single photon detectors (SNSPDs)

8.8. Kinetic inductance detector (KID) and transition edge sensor (TES)

8.8.1. Kinetic Inductance Detectors (KIDs)

8.8.2. Transition edge sensors (TES)

8.8.3. How have SNSPDs gained traction while KIDs and TESs remain in research?

8.9. Single photon detectors: Summary

8.9.1. Comparison of single photon detector technology

8.9.2. Single photon detector roadmap

8.9.3. 3 key takeaways for single photon detectors

8.10. Quantum Imaging

8.10.1. Introduction to quantum imaging

8.10.2. Quantum entanglement: Enabling quantum radar and ghost imaging

8.10.3. Introduction to ghost imaging

8.10.4. EU FastGhost project leads commercial development of ghost imaging

8.10.5. Nonlinear interferometry (quantum holography)

8.10.6. QUANCER project developing quantum holography for cancer detection

8.10.7. Digistain developing mid-IR nonlinear interferometry for cancer detection

8.10.8. Quantum imaging for glucose monitoring is in the early stages of commercialization

8.10.9. Quantum radar

8.10.10. General advantages of quantum imaging

8.10.11. Quantum particle sensors could probe more information using superposition states of light

8.10.12. SWOT analysis: Quantum imaging

8.10.13. 3 key takeaways for quantum imaging

9. COMPONENTS FOR QUANTUM SENSING

9.1. Section overview: Components for quantum sensing

9.2. Specialized components for atomic and diamond-based quantum sensing

9.3. Key players in components for quantum sensing technologies

9.4. Vapor cells: Background and context

9.5. Innovation in commercial manufacture of vapor cells in quantum sensing

9.6. Alkali azides used to overcome high-vacuum fabrication requirements of vapor cells for quantum sensing

9.7. Comparing key players in chip-scale vapor cell development

9.8. SWOT analysis: Miniaturized vapor cells

9.9. VCSELs: Background and context

9.10. VCSELs enable miniaturization of quantum sensors and components

9.11. Comparing key players in VCSELs for quantum sensing

9.12. SWOT analysis: VCSELs

9.13. Specialized control electronics and optics packages needed to enable the high performance of quantum sensors

9.14. Integrated photonic and semiconductor products for quantum are developing but not yet unlocking the mass market

9.15. Hardware challenges for quantum to integrate into established photonics

9.16. Roadmap for components in quantum sensing

9.17. Roadmap for quantum sensing components and their applications

10. MARKET FORECASTS

10.1.1. Forecasting chapter overview

10.1.2. Forecasting methodology overview

10.1.3. Comparing the scale of long-term markets (in volume) for key quantum sensing technologies

10.1.4. Total quantum sensor market - annual revenue 2026-2046

10.1.5. Quantum sensor market - Key forecasting results (1)

10.1.6. Quantum sensor market - Key forecasting results (2)

10.1.7. Identifying medium term opportunities in the quantum sensor market: Market size vs CAGR (2026-2036)

10.1.8. Identifying long term opportunities in the quantum sensor market: Market size vs CAGR (2036-2046)

10.1.9. Total quantum sensor market - Granular annual revenue 2026-2046

10.1.10. Quantum sensor market - Granular annual revenue (excluding TMR) 2026-2046

10.2. Atomic Clocks

10.2.1. Overview of atomic clock market trends: Annual revenue forecast 2026-2046

10.2.2. Bench/rack-scale atomic clocks, annual sales volume forecast 2026-2046

10.2.3. Chip-scale atomic clocks, annual sales volume forecast 2026-2036

10.2.4. Chip-scale atomic clocks, annual sales volume forecast 2026-2046

10.2.5. Summary of market forecasts for atomic clock technology

10.3. Quantum Magnetic Field Sensors

10.3.1. Overview of quantum magnetic field sensor market trends

10.3.2. Global car sales trends to impact the quantum sensor market long-term

10.3.3. TMR sensors, annual sales volume forecast 2026-2046

10.3.4. TMR sensors, annual revenue forecast 2026-2046

10.3.5. SQUIDs, OPMs, and NVMs - Annual sales volume forecast 2026-2046

10.3.6. SQUIDs, OPMs, and NVMs - Annual sales volume forecast 2026-2046

10.3.7. Summary of market forecasts for quantum magnetic field sensor technology

10.3.8. Inertial Quantum Sensors (Gyroscopes and Accelerometers)

10.3.9. Annual revenue for quantum gyroscopes and accelerometers 2026-2046

10.4. Inertial quantum sensors, annual sales volume forecast 2026-2046

10.4.1. Key conclusions for quantum gyroscope & accelerometer forecasts

10.5. Quantum Gravimeters

10.5.1. Annual revenue for quantum gravimeters 2026-2046

10.5.2. Quantum gravimeters, annual sales volume forecast 2026-2046

10.5.3. Summary of key conclusions for quantum gravimeter technology forecasts

10.6. Quantum RF Sensors

10.6.1. Annual revenue for quantum RF sensors 2026-2046

10.6.2. Annual sales volume forecast for quantum RF sensors 2026-2046

10.7. Single Photon Detectors

10.7.1. Annual revenue for single photon detectors 2026-2046

10.7.2. Annual sales volume forecast for single photon detectors 2026-2046

10.7.3. Analysis of single photon detector forecasts: photonic quantum computing

11. COMPANY PROFILES

11.1. Aegiq

11.2. Artilux Inc

11.3. Beyond Blood Diagnostics

11.4. BT (Quantum Radio Research)

11.5. CEA Leti (Quantum Technologies)

11.6. Cerca Magnetics

11.7. Covesion Ltd

11.8. CPI EDB (Quantum Sensing)

11.9. Crocus Technology

11.10. Diatope

11.11. Digistain (Quantum Sensing)

11.12. Element Six (Quantum Technologies)

11.13. Fraunhofer CAP

11.14. ID Quantique (Single Photon Detectors)

11.15. Infleqtion (Cold Quanta)

11.16. Menlo Systems Inc

11.17. Neuranics

11.18. NIQS Technology Ltd

11.19. Ordnance Survey

11.20. Photon Force

11.21. Polariton Technologies

11.22. Powerlase Ltd

11.23. PsiQuantum

11.24. Q-CTRL (quantum navigation)

11.25. Q.ANT

11.26. Qingyuan Tianzhiheng Sensing Technology Co., Ltd

11.27. QLM Technology: Methane-Sensing LiDAR

11.28. Quantum Computing Inc

11.29. Quantum Economic Development Consortium (QED-C)

11.30. Quantum Technologies

11.31. Quantum Valley Ideas Lab

11.32. QuiX Quantum

11.33. QZabre

11.34. RobQuant

11.35. Rydberg Technologies

11.36. SandboxAQ (Quantum Sensing)

11.37. SEEQC

11.38. SemiWise

11.39. Senko Advance Components Ltd

11.40. Single Quantum

11.41. sureCore Ltd

11.42. TU Darmstadt (Quantum Imaging)

11.43. VTT Manufacturing (Quantum Technologies)

11.44. XeedQ

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の ロボティクスと自律性 - Robotics & Autonomy 分野 での最新刊レポート

関連レポート(キーワード「センサ」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|