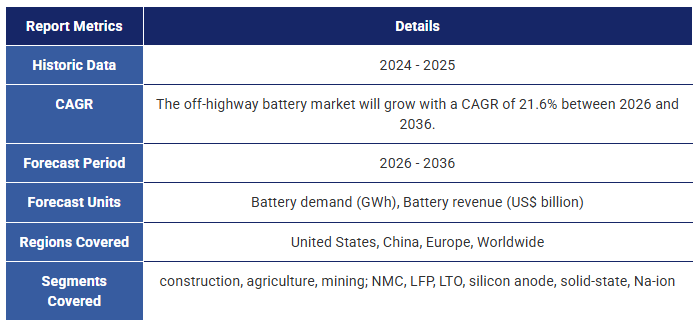

建設・農業・鉱山機械向けバッテリー市場 2026-2036年:技術動向、主要企業、予測Batteries for Construction, Agriculture, & Mining Machines 2026-2036: Technologies, Players, Forecasts 米国、中国、欧州、およびその他の地域における建設・農業・鉱山機械用バッテリーの10年予測。機械の分析、バッテリーパックのベンチマーク、主要企業、および将来のバッテリー技術。NMC、LFP、LTO、ナトリウ... もっと見る

サマリー米国、中国、欧州、およびその他の地域における建設・農業・鉱山機械用バッテリーの10年予測。機械の分析、バッテリーパックのベンチマーク、主要企業、および将来のバッテリー技術。NMC、LFP、LTO、ナトリウムイオン、シリコン負極、全固体電池

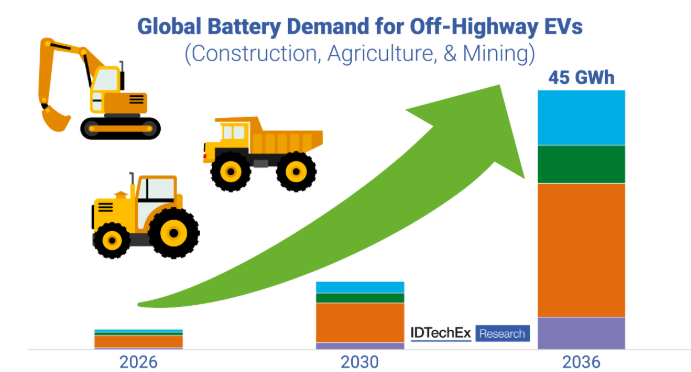

IDTechExのレポート『建設・農業・鉱山機械向けバッテリー 2026-2036:技術、主要企業、予測』は、建設、農業、鉱業といったオフハイウェイ産業における電動機械の急成長市場について深く掘り下げています。 これには、多種多様な機械に対するバッテリー要件に関する重要な知見、これらの要件を満たすことができる技術、詳細なサプライチェーン分析、および2036年までに45GWhに達すると予測されるオフハイウェイ用バッテリー需要の成長を概説する詳細な10年間の予測が含まれています。

建設、農業、鉱業用機械による世界のバッテリー需要は、2036年までに45GWhに達する見込み(出典:IDTechEx)

オフハイウェイ産業が電動機械を採用する理由は?

建設、農業、鉱業における電動機械は、環境面、経済面、運用面でのメリットから、関心と投資が高まっています。 ディーゼル燃料の代わりに電力を使用することで、現地での温室効果ガス、NOx、およびディーゼル微粒子物質の排出をゼロにすることができます。その結果、ディーゼルエンジンからの熱、騒音、振動が低減され、よりクリーンで安全な作業環境が実現します。さらに重要な点として、ディーゼル燃料に代えて電力を使用することで、エネルギーコストの大幅な削減と運用コスト(OPEX)の低減につながり、機械オペレーターにとって総所有コスト(TCO)のメリットをもたらします。

これにより、キャタピラー、コマツ、ジョンディア、XCMGといった主要OEMを含む世界中の機械メーカーから多額の投資が行われ、各社は電動モデルの市場投入を積極的に進めています。 特に建設業界では、OEMの投資と、都市部での建設機械の排出ガスを規制しようとする政府の取り組みの両方に後押しされ、これまでで最大の電動化が進んでいます。鉱業、とりわけ農業分野では依然として遅れをとっていますが、バッテリー技術の成熟と法規制の強化により、今後、電動化のペースが加速すると予想されます。

機械の要件に適合するバッテリー技術への需要

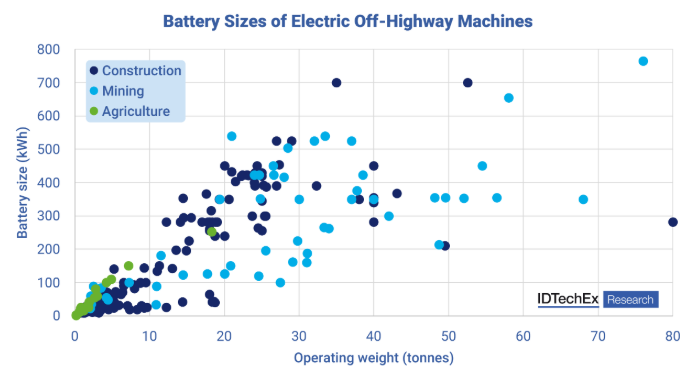

オフハイウェイ機械は、サイズが多岐にわたり、要求事項、用途、使用プロファイルも大きく異なります。 例えば、ミニショベルは重量が6トン未満で1日の稼働時間は8時間未満であるのに対し、鉱業用の運搬トラックは重量が200トン以上に達し、重い荷物を積載した状態でほぼ24時間365日稼働することが求められます。その結果、オフハイウェイ機械の電動化を成功させるには、異なる機械のニーズを満たすために、幅広いバッテリーサイズ、性能パラメータ、および技術が必要となります。

現在、機械に使用されているバッテリーの容量は10kWhから2MWhまで多岐にわたりますが、容量だけでなく、エネルギー密度、出力、電圧、充電速度、サイクル寿命、コストの観点からも最適化される必要があります。エネルギー密度や充電速度の向上は一般的にサイクル寿命の短縮を伴うため、これらの要素は相互にトレードオフを迫られる可能性があります。これらの要素のバランスは機械の種類によって異なり、それぞれに適したバッテリー技術の選定に影響を与えます。

IDTechExのレポートでは、各種機械の要件および市販のターンキーバッテリーパックに関する詳細なベンチマークを提供しており、バッテリーおよび主要なバッテリーメーカーがオフハイウェイ用バッテリーの需要にどのように対応しているかを明確に示しています。

オフハイウェイEVは稼働重量が大きく異なるため、あらゆる機械タイプでの電動化を成功させるには、幅広いサイズのバッテリーが必要となる。出典:IDTechEx

将来のバッテリー技術の役割

これまで、オフハイウェイ用バッテリー市場は自動車市場の足跡をほぼ追う形で、NMCおよびLFP技術が主導的な地位を占めてきました。これらの技術は成熟しており、容易に入手可能で、一般的なオフハイウェイ市場のニーズを満たしています。しかし、オフハイウェイ用バッテリーの要件が多様であるため、NMCやLFP以外の新興バッテリー技術がより広く活用される機会が生まれています。

その一例がチタン酸リチウム(LTO)であり、これはグラファイトの代わりにNMCやLFPの正極と組み合わせることができる代替負極材料です。LTOパックは一般的なグラファイトベースのパックに比べてエネルギー密度がはるかに低く、リチウム含有量が高いためコストも大幅に高くなります。 しかし、LTOは急速充電に優れており、最大20,000サイクルという非常に高いサイクル寿命を実現可能です。これにより、長年にわたりほぼ連続運転が行われる鉱山機械の要件に最適となります。電気機械においては、サイクル寿命が長く、充電が速いほどダウンタイムを削減できるため、大きなメリットとなります。

シリコン負極、全固体電池、ナトリウムイオン電池といった技術も、オフハイウェイ市場において重要な役割を果たすことになるでしょう。LTOとは異なり、これらの技術は現時点ではまだ市場に浸透していませんが、IDTechExは今後10年以内に市場投入されると予測しています。 シリコン負極や全固体電池の高いエネルギー密度、ならびにナトリウムイオン電池の低コスト化の可能性とLFP(リン酸鉄リチウム)電池に匹敵する性能は、オフハイウェイ機械への採用に向けた適切な市場機会を生み出しています。

IDTechExのレポートでは、現在および新興の電池技術について、技術的成熟度、価値提案、オフハイウェイ機器に提供可能な特性など、詳細な評価を提供するとともに、各技術が異なる機械タイプとどの程度適合するかをベンチマークしています。

市場動向、予測、および主要企業のプロファイル

IDTechExのレポートは、上記のトレンドなどをすべて網羅し、分析において主要な性能、経済、規制、その他の技術的および市場的要因を考慮しています。主要な機械OEMおよびバッテリーメーカー、ならびにそれぞれの製品について詳細なベンチマークを行い、現在および新興のバッテリー技術が機械のニーズをどのように満たすことができるかについて、深い理解を提供しています。

世界のオフハイウェイ用バッテリー需要(GWh)およびバッテリー売上高(10億米ドル)について、10年単位の詳細な予測が提示されています。 予測は、オフハイウェイのセグメント(建設、農業、鉱業)、機械の種類、地域(米国、中国、欧州、その他の地域)、およびバッテリー技術(NMC、LFP、LTO、シリコン負極、全固体、Naイオン)ごとに分類されています。

本IDTechExレポートでは、電動機械のOEM、バッテリーパックサプライヤー、充電サービスプロバイダーを含む56社の企業プロファイルにアクセスでき、市場に対するより深い洞察を得ることができます。

主な内容

本レポートでは、以下の重要な情報を提供しています:

目次

1. エグゼクティブ・サマリー

1.1. レポートの主な調査結果

1.2. オフハイウェイ電化の主な利点と推進要因

1.3. オフハイウェイ電動化の主な障壁と課題

1.4. :オフハイウェイ各セグメント間で異なる電動化の推進要因

1.5. 建設機械の概要

1.6. 電動化の対象となる主要な農業機械

1.7. 電動化の対象となる主要な農業機械

1.8. オフハイウェイ機械のベンチマーク:バッテリー容量

1.9. オフハイウェイ機械のベンチマーク:電圧

1.10. 機械のサイズがバッテリー化学種の選定に与える影響

1.11. 機械の寿命とバッテリーの寿命

1.12. 機械の種類別バッテリーパックの要件

1.13. オフハイウェイ車両の電動化におけるコスト要件

1.14. オフハイウェイ向けターンキーバッテリーパック:化学組成とセル形式の動向

1.15. オフハイウェイ向けターンキーバッテリーパック:電圧

1.16. オフハイウェイ向けターンキーバッテリーパック:放電Cレート

1.17. サイクル寿命とエネルギー密度のトレードオフ

1.18. 機械充電におけるBESSの応用

1.19. オフハイウェイ機械向けターンキーメーカー

1.20. ターンキーメーカー:買収およびスピンアウト活動の概要

1.21. オフハイウェイ機械における将来のバッテリー技術の応用

1.22. 現行および将来のバッテリー技術の比較

1.23. オフハイウェイ機械向けバッテリー技術の互換性

1.24. セグメント別 世界のオフハイウェイ用バッテリー需要(GWh)2024-2036

1.25. 地域別オフハイウェイ用バッテリー需要(GWh)2024-2036

1.26. 2024-2036年の技術別世界のオフハイウェイ用バッテリー需要(GWh)

1.27. 世界のオフハイウェイ用バッテリー売上高(10億米ドル)2024-2036年(セグメント別)

1.28. 世界のオフハイウェイ用バッテリー売上高(10億米ドル) 2024-2036年(地域別)

1.29. 世界のオフハイウェイ用バッテリー市場規模(2024-2036年、技術別、10億米ドル)

1.30. IDTechExのサブスクリプションでさらに多くの情報にアクセス

2. 電動オフハイウェイ機械の概要

2.1. 電動化の概要

2.1.1. 機械の電動化のメリットと障壁

2.1.2. 建設、農業、鉱業における電動化の主な推進要因

2.2. 電動建設機械

2.2.1. 電動化の対象となる主要な建設機械

2.2.2. 主要建設機器メーカーの電動化動向

2.2.3. ミニショベル

2.2.4. ショベル

2.2.5. コンパクトローダー (1)

2.2.6. コンパクトローダー (2)

2.2.7. バックホー

2.2.8. ホイールローダー

2.2.9. テレハンドラー

2.2.10. 移動式クレーン

2.2.11. セメントミキサー車

2.2.12. ローラー

2.2.13. その他の建設機械

2.3. 電動農業機械

2.3.1. 電動化に向けた主要農業機械

2.3.2. 主要農業機器メーカーの電動化動向

2.3.3. サブコンパクトトラクター

2.3.4. コンパクトトラクター

2.3.5. ユーティリティトラクター

2.3.6. その他の農業機械

2.4. 電気式鉱山機械

2.4.1. 電動化に向けた の主要農業機械

2.4.2. 主要農業機器メーカーの電動化動向

2.4.3. 運搬用トラック

2.4.4. ダンプトラック

2.4.5. ホイールローダー

2.4.6. 坑内用ローダー

2.4.7. 坑内用トラック

2.4.8. 鉱山用軽車両

2.4.9. その他の鉱山機械

3. 電気式オフハイウェイ機械のバッテリー要件

3.1. 要点 - バッテリー性能要件

3.2. バッテリーの容量選定

3.3. 50トン未満の機械におけるバッテリーの選定

3.4. バッテリー容量の内訳

3.5. 標準化されたバッテリー容量選定

3.6. バッテリー電力要件

3.7. 業界別の 電力要件

3.8. バッテリー放電率

3.9. バッテリーの充電速度

3.10. バッテリー電圧 (1)

3.11. バッテリー電圧 (2)

3.12. 100V未満の バッテリー電圧

3.13. バッテリーの化学組成と機械のサイズ

3.14. さまざまなオフハイウェイ産業における の化学組成の選択肢

3.15. 地域ごとの化学組成の選択肢

3.16. バッテリーの寿命要件

3.17. 機械タイプ別のバッテリーパック全体要件

3.18. コスト要件

4. ターンキーバッテリー技術およびベンチマーク

4.1. ターンキー技術の概要

4.1.1. ターンキーバッテリーサプライヤーの概要

4.2. ターンキーパックの地域別供給状況

4.2.1. 各地域におけるターンキーパックプロバイダー

4.2.2. 各地域における異なる化学組成の供給状況

4.2.3. セル形式の地域別供給状況

4.3. ターンキーパックの性能ベンチマーク( )

4.3.1. 主なポイント - オフハイウェイ向けターンキーバッテリーの特性

4.3.2. ターンキーパックのサイズと機械要件の比較

4.3.3. バッテリーの寸法とフォームファクター

4.3.4. バッテリー電圧分布

4.3.5. 化学組成別のラゴーネプロット(重量比出力対エネルギー密度)

4.3.6. セル形式別の ラゴーネプロット

4.3.7. ターンキーバッテリーの放電Cレート

4.3.8. ターンキーパックの充電Cレート

4.3.9. サイクル寿命とエネルギー密度のトレードオフ

4.3.10. 体積エネルギー密度と質量エネルギー密度の比較

4.4. 熱管理戦略

4.4.1. 熱管理の概要

4.4.2. 空冷

4.4.3. 液体冷却

4.4.4. の浸漬冷却

4.4.5. 熱管理のベンチマーク

4.4.6. ターンキーパックの 熱管理および充電性能

4.4.7. IDTechExのバッテリー熱管理に関するレポート

4.5. オフハイウェイ用バッテリーにおけるセル・トゥ・パックおよびセル・トゥ・ボディ

4.5.1. セル・トゥ・パックとは

4.5.2. CTPの推進要因と課題

4.5.3. CATLのCTPバッテリー

4.5.4. CATLのCTP 3.0

4.5.5. セル・トゥ・ボディ

4.5.6. BYD CTBバッテリー

4.5.7. オフハイウェイ分野における のCTPおよびCTB:市場における継続的な変化の兆し

4.5.8. 電極-パック(Electrode-to-Pack)の台頭

4.5.9. IDTechExによるCTPおよびCTBに関するレポート

4.6. オフハイウェイ機械の充電

4.6.1. 建設、農業、鉱業における充電ソリューション

4.6.2. オフハイウェイ充電向け BESS:リープヘル

4.6.3. オフハイウェイ充電向け BESS:ボルボ&キャタピラー

4.6.4. オフハイウェイ充電向け BESS:Turntide

4.6.5. オフハイウェイ充電向け BESS:AMPD

4.6.6. IDTechExによるオフハイウェイ充電用BESSに関するレポート

5. バッテリーサプライヤーおよび事例研究

5.1. ターンキー型バッテリーメーカー

5.1.1. 地域別 ターンキーメーカー

5.1.2. 化学組成別 ターンキーメーカー

5.1.3. セル形状別 ターンキーメーカー

5.1.4. 熱管理別 ターンキーメーカー

5.1.5. Microvast

5.1.6. Forsee Power

5.1.7. ボルグワーナー

5.1.8. Webasto

5.1.9. レクラッシュ

5.1.10. ABB

5.1.11. クライゼル・エレクトリック

5.1.12. Proventia

5.1.13. IMPACT Clean Power Technology

5.1.14. アメリカン・バッテリー・ソリューションズ(コマツの子会社)

5.1.15. デベロン(現代自動車)

5.2. ハイブリッド用途向け LTOパック

5.2.1. ハイブリッド車向け LTOパックとその用途

5.2.2. 、Forsee Power、およびクボタ - マイクロハイブリッドエンジン

5.2.3. ハイブリッド車向け Proventia低電圧バッテリー

5.2.4. ハイブリッド車向け Hyliionバッテリーモジュール

5.3. バッテリーサプライヤーに関する の買収、スピンアウト、および清算

5.3.1. 概要と主なポイント

5.3.2. 活動概要

5.3.3. :Proterraがボルボに買収される

5.3.4. :American Battery Solutionsがコマツに買収される

5.3.5. クライゼル(Kreisel)がジョン・ディア(John Deere)に買収される

5.3.6. ヤンマーによるエレオの買収

5.3.7. ターントライドによるハイパードライブの買収

5.3.8. フロイデンベルクによるXALT Energyの買収

5.3.9. Accelera - カミンズからのスピンアウト

5.3.10. ZQuip - ムーグからのスピンアウト

5.3.11. Northvoltの破産およびScaniaによる買収

5.3.12. その他の活動:XerotechおよびAkasol

5.4. バッテリーサプライヤーとOEMの関係

5.4.1. OEMとバッテリーサプライヤーの関係の概要

5.4.2. バッテリー供給関係 (1)

5.4.3. バッテリー供給関係 (2)

5.4.4. バッテリー供給関係 (3)

5.4.5. バッテリー供給関係 (4)

5.4.6. バッテリー供給の関連性 (5)

6. オフハイウェイ電気機械向け将来のバッテリー技術

6.1. 将来のバッテリー技術の概要

6.1.1. 将来のバッテリー技術の概要

6.1.2. バッテリー技術間の主な相違点

6.1.3. 将来のバッテリー技術に関するIDTechExレポート

6.2. NMC および LFP

6.2.1. リチウム電池の化学組成

6.2.2. 代表的なリチウムイオン電池オプションの比較評価

6.2.3. リチウムイオン電池の正極材料 - LCOおよびLFP

6.2.4. リチウムイオン電池の正極材料 - NMC、NCA、およびLMO

6.2.5. 高ニッケル層状酸化物への移行

6.2.6. 高マンガン正極材

6.2.7. NMC 811 と高マンガン正極材料の比較

6.2.8. オフハイウェイ用途向けリチウムイオン技術の革新

6.3. LTO およびニオブ酸塩

6.3.1. チタン酸リチウム(LTO)の概要

6.3.2. LTOと黒鉛負極材の比較

6.3.3. オフハイウェイ機械向けLTO

6.3.4. ニオブ酸塩の台頭

6.3.5. Nb系負極:Nyobolt

6.3.6. Nb系負極:Echion

6.4. シリコン負極

6.4.1. Si負極の定義

6.4.2. Si負極セルの利点

6.4.3. シリコン負極セルの課題

6.4.4. 高シリコン含有量負極の価値提案

6.4.5. オフハイウェイ向けシリコン負極の用途

6.5. リチウム金属

6.5.1. リチウム金属(Li-metal)負極の概要

6.5.2. リチウム金属電池の課題

6.5.3. 固体電解質を使用しないリチウム金属電池の実現

6.5.4. エネルギー密度におけるリチウム金属とリチウムイオンの比較

6.5.5. 負極のないリチウム金属電池の設計

6.5.6. オフハイウェイ用途向けリチウム金属電池

6.6. 固体電池

6.6.1. 固体電池(SSB)の概要

6.6.2. SSBの長所と短所の分析

6.6.3. SSBのエネルギー密度の向上

6.6.4. 固体電池(SSB)のパック設計上の考慮事項

6.6.5. オフハイウェイ用途向けSSB

6.7. リチウム硫黄

6.7.1. リチウム硫黄(Li-S)の概要

6.7.2. リチウム硫黄(Li-S)電池の利点

6.7.3. Li-S 電池の課題

6.7.4. オフハイウェイ用途におけるLi-S

6.8. ナトリウムイオン

6.8.1. ナトリウムイオン(Na-ion)の概要

6.8.2. ナトリウムイオン対リチウムイオン

6.8.3. ナトリウムイオン用正極材料

6.8.4. ナトリウムイオン(Na-ion)用負極材料

6.8.5. ナトリウムイオン電池の特性

6.8.6. ナトリウムイオン電池の価値提案

6.8.7. オフハイウェイ用途向けナトリウムイオン電池

6.9. 亜鉛系電池

6.9.1. 亜鉛系電池(Zn系電池)の概要

6.9.2. 亜鉛系電池のメリットとデメリット

6.9.3. オフハイウェイ用途向け亜鉛系電池

6.10. 電池技術の概要およびオフハイウェイ用途への適用性

6.10.1. 電池技術の比較

6.10.2. バッテリー技術の適合性:構造 (1)

6.10.3. バッテリー技術の適合性:建設 (2)

6.10.4. バッテリー技術の適合性:鉱業

6.10.5. バッテリー技術の互換性:農業

7. 予測

7.1. 提供される の予測の概要

7.2. 予測の概要および解説

7.3. 予測手法 (1): 対象市場およびオフハイウェイEV販売台数

7.4. セグメント別 世界のオフハイウェイEV販売台数(2024-2036年、単位:千台)

7.5. 予測手法 (2):バッテリー需要、技術、および収益

7.6. 予測の前提条件

7.7. バッテリーパック価格の前提条件(米ドル/kWh)

7.8. セグメント別世界のオフハイウェイ用バッテリー需要(GWh)2024-2036

7.9. 地域別世界オフハイウェイ用バッテリー需要(GWh)2024-2036

7.10. 機械タイプ別世界のオフハイウェイ用バッテリー需要(GWh)2024-2036 (1)

7.11. 機械種別別世界のオフハイウェイ用バッテリー需要(GWh) 2024-2036 (2)

7.12. 技術別世界のオフハイウェイ用バッテリー需要(GWh) 2024-2036 (1)

7.13. 技術別世界のオフハイウェイ用バッテリー需要(GWh)2024-2036 (2)

7.14. セグメント別世界のオフハイウェイ用バッテリー売上高(10億米ドル) 2024-2036

7.15. 地域別世界のオフハイウェイ用バッテリー売上高(10億米ドル) 2024-2036

7.16. 技術別世界のオフハイウェイ用バッテリー売上高(10億米ドル) 2024-2036

7.17. 世界の建設用バッテリー需要(技術別)(GWh) 2024-2036

7.18. 技術別世界の農業用バッテリー需要(GWh) 2024-2036

7.19. 技術別世界の鉱業用バッテリー需要(GWh)2024-2036

8. 企業プロファイル

8.1. ABB:オフハイウェイ向けバッテリーおよびドライブトレイン

8.2. ABB:鉱業の電動化

8.3. AMPD

8.4. AutoNXT

8.5. BatteryOne

8.6. BluVein

8.7. ボブキャット:完全電動スキッドステアローダー

8.8. Briggs & Stratton

8.9. Carrar:浸漬冷却

8.10. キャタピラー

8.11. キャタピラー:電動建設機械

8.12. キャタピラー:ハイブリッドホイールローダー

8.13. カボテック

8.14. CNHインダストリアル

8.15. デベロン

8.16. Dieci:電動テレハンドラー

8.17. エピロック

8.18. First Mode

8.19. Genie

8.20. Hitachi CM:電動運搬トラック

8.21. Hixal:オフハイウェイ機械向け充電

8.22. HYDAC:オフハイウェイ機械の電動化

8.23. ヒュンダイ・コンストラクション・イクイップメント

8.24. ヤコブ・マイニング・ビークルズ

8.25. ジャマ・マイニング・マシーンズ

8.26. ジョン・ディア:電気式および自律走行トラクター

8.27. ジョン・ディア:電動建設機械

8.28. カトー:電動ミニショベル

8月29日 コベルコ

8月30日 コマツ:建設機械の電動化

8月31日 コヴァテラ

8.32. クライゼル・エレクトリック

8.33. クボタ

8.34. L-Charge

8.35. LiuGong

8.36. ノルメット:SmartDrive

8.37. PowerCharge:オフハイウェイ用電気機器の充電

8.38. Rokion

8.39. Sandvik

8.40. SANY:電動移動式クレーン

8.41. スカニア:鉱山用電気トラック

8.42. Sinoboom

8.43. スノケル

8.44. ソレクトラック

8.45. サンワード

8.46. サンワード:電気ショベルカー

8.47. Tonly

8.48. Tritium:鉱山用電気自動車の充電

8.49. ターンタイド

8.50. ボルボCE

8.51. WAE Technologies

8.52. WATTALPS:オフハイウェイ機械用バッテリー

8.53. XCMG:電気式および自律走行型鉱山車両

8.54. ヤンマー

8.55. ズームライオン:電気鉱山車両

8.56. ZQuip:建設機械用バッテリー

Summary10-year forecasts for batteries for construction, agriculture, & mining machines across US, China, Europe & RoW. Machine analysis, battery pack benchmarking, key players & future battery technologies. NMC, LFP, LTO, Na-ion, silicon anode, solid-state.

IDTechEx's report "Batteries for Construction, Agriculture, & Mining Machines 2026-2036: Technologies, Players, Forecasts" provides a deep-dive into the fast-growing markets for electric machinery in the off-highway industries of construction, agriculture, and mining. This includes critical insights into battery requirements for the diverse range of machines, which technologies can meet these requirements, detailed supply chain analysis, and granular 10-year forecasts which outline the growth of off-highway battery demand to reach 45 GWh by 2036.

Global battery demand from construction, agriculture, and mining machines to reach 45 GWh by 2036, Source: IDTechEx

Why are off-highway industries adopting electric machines?

Electric machines across construction, agriculture, and mining are seeing increased interest and investment due to the environmental, financial, and operational benefits they can provide. The use of electricity instead of diesel allows for zero local greenhouse gas, NOx, and diesel particulate matter emissions. The result is a cleaner and safer workplace that also benefits from less heat, noise, and vibration from diesel engines. Crucially, the use of electricity over diesel leads to significant energy cost savings and lower OPEX, helping to provide total cost of ownership (TCO) benefits to machine operators.

This has led to significant investment from machine manufacturers around the world, including major OEMs such as Caterpillar, Komatsu, John Deere, and XCMG that are actively looking to bring electric machine models to market. The construction industry in particular has seen the greatest electrification to date, driven both by OEM investment and by governments looking to limit the emissions of city-based construction machines. While mining and especially agriculture remain further behind, the maturation of battery technology and a greater legislative push are expected to increase the rate of electrification moving forward.

Demand for battery technologies to fit machine requirements

Off-highway machinery comes in a wide variety of sizes with highly variable demands, applications, and usage profiles. For example, mini-excavators weigh under 6 tonnes and have daily runtimes of under 8 hours a day, while haul trucks in mining can weigh upwards of 200 tonnes and are required to operate nearly 24/7 while carrying heavy loads. As a result, successful electrification of off-highway machines will call for a wide range of battery sizes, performance parameters, and technologies in order to meet the needs of different machines.

Battery sizes currently used in machines can range from 10 kWh up to 2 MWh, but beyond capacity alone, batteries must also be optimized in terms of energy density, power output, voltage, charging rates, cycle life, and cost. These factors may need to be traded off against each other, as energy density and charging speed generally come at the cost of cycle life. The balance between these factors will differ among machine types and will influence which battery technologies they are each suited to.

The IDTechEx report provides detailed benchmarking of the requirements of various machine types and of commercially-available turnkey battery packs, providing clarity on how batteries and key battery players are meeting off-highway battery demand.

Off-highway EVs vary widely in operating weight, requiring a broad range of battery sizes for successful electrification across machine types, Source: IDTechEx

The role of future battery technologies

Up until now, the off-highway battery market has largely followed in the footsteps of the automotive market, with NMC and LFP technologies leading the way. These technologies are mature, readily available, and serve the needs of the general off-highway market. However, the diversity in off-highway battery requirements creates opportunities for emerging battery technologies outside of NMC and LFP to see greater use.

One example of such a technology is lithium titanate oxide (LTO) which is an alternative anode material that can be paired with NMC or LFP cathodes instead of graphite. LTO packs have far lower energy density than typical graphite-based packs, and their high lithium intensity also leads to much higher cost. However, LTO excels at fast-charging and can have very high cycle lives of up to 20,000 cycles. This makes it a good fit for the demands of mining machinery, where near-constant operation over many years means that electric machines will benefit from long cycle lives and faster charging which can reduce downtime.

Technologies such as silicon anodes, solid-state batteries, and Na-ion batteries will also play a role in the off-highway market. Unlike LTO, these technologies have not made their way to the market as of yet, but IDTechEx expects this will happen within the coming decade. The high energy density of silicon anode and solid-state batteries, as well as the low-cost potential and LFP-like performance of Na-ion batteries, create suitable market opportunities for their use in off-highway machinery.

The IDTechEx report provides detailed appraisals of current and emerging battery technologies, including on their state of technological readiness, value propositions, and properties they can offer to off-highway equipment, benchmarking each for their compatibility with different machine types.

Market trends, forecasts, and player profiles

IDTechEx's report brings together all of the above trends and more, accounting for key performance, economic, regulatory, and other technical and market factors in its analysis. Key machine OEMs and battery manufacturers, along with their respective products, are benchmarked in detail - providing in-depth understanding of how current and emerging battery technologies can meet the needs of machines.

10-year granular forecasts are provided for global off-highway battery demand (in GWh) and battery revenue (in US$ billion). Forecasts are segmented by off-highway segment (construction, agriculture, mining), machine type, region (US, China, Europe, Rest of the World), and battery technology (NMC, LFP, LTO, silicon anode, solid-state, and Na-ion).

This IDTechEx report provides access to 56 company profiles, including electric machine OEMs, battery pack suppliers, and charging providers, allowing greater insight into the market.

Key Aspects

This report provides the following critical information:

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Key report findings

1.2. Key advantages and drivers for off-highway electrification

1.3. Key barriers and challenges for off-highway electrification

1.4. Electrification drivers differ between off-highway segments

1.5. Construction machines overview

1.6. Key agriculture machines for electrification

1.7. Key agriculture machines for electrification

1.8. Off-highway machine benchmarking: Battery size

1.9. Off-highway machine benchmarking: Voltage

1.10. Machine size impacts battery chemistry selection

1.11. Lifetime of machines vs batteries

1.12. Battery pack requirements by machine type

1.13. Cost requirements for off-highway electrification

1.14. Turnkey battery packs for off-highway: Chemistry and cell format trends

1.15. Turnkey battery packs for off-highway: Voltage

1.16. Turnkey battery packs for off-highway: Discharge C-rates

1.17. Tradeoffs between cycle life and energy density

1.18. Applications of BESS for machine charging

1.19. Turnkey manufacturers for off-highway machines

1.20. Turnkey manufacturers: Summary of acquisition & spinout activity

1.21. Applications of future battery technology in off-highway machines

1.22. Comparison of current & future battery technologies

1.23. Compatibility of battery technologies for off-highway machines

1.24. Global off-highway battery demand (GWh) 2024-2036 by segment

1.25. Global off-highway battery demand (GWh) 2024-2036 by region

1.26. Global off-highway battery demand (GWh) 2024-2036 by technology

1.27. Global off-highway battery revenue (US$ billion) 2024-2036 by segment

1.28. Global off-highway battery revenue (US$ billion) 2024-2036 by region

1.29. Global off-highway battery revenue (US$ billion) 2024-2036 by technology

1.30. Access more with an IDTechEx subscription

2. INTRODUCTION TO ELECTRIC OFF-HIGHWAY MACHINES

2.1. Electrification overview

2.1.1. Advantages of & barriers to machine electrification

2.1.2. Key electrification drivers in construction, agriculture, and mining

2.2. Electric construction machines

2.2.1. Key construction machines for electrification

2.2.2. Electrification activity of major construction OEMs

2.2.3. Mini-excavators

2.2.4. Excavators

2.2.5. Compact loaders (1)

2.2.6. Compact loaders (2)

2.2.7. Backhoes

2.2.8. Wheel loaders

2.2.9. Telehandlers

2.2.10. Mobile cranes

2.2.11. Cement trucks

2.2.12. Rollers

2.2.13. Other construction machines

2.3. Electric agriculture machines

2.3.1. Key agriculture machines for electrification

2.3.2. Electrification activity of major agriculture OEMs

2.3.3. Sub-compact tractors

2.3.4. Compact tractors

2.3.5. Utility tractors

2.3.6. Other agriculture machines

2.4. Electric mining machines

2.4.1. Key agriculture machines for electrification

2.4.2. Electrification activity of major agriculture OEMs

2.4.3. Haul trucks

2.4.4. Dump trucks

2.4.5. Wheel loaders

2.4.6. Underground loaders

2.4.7. Underground trucks

2.4.8. Mining light vehicles

2.4.9. Other mining machines

3. BATTERY REQUIREMENTS OF ELECTRIC OFF-HIGHWAY MACHINES

3.1. Key takeaways - battery performance requirements

3.2. Battery sizing

3.3. Battery sizing for machines under 50 tonnes

3.4. Battery size breakdown

3.5. Normalized battery sizing

3.6. Battery power requirements

3.7. Power requirements by industry

3.8. Battery discharge rate

3.9. Battery charging rates

3.10. Battery voltage (1)

3.11. Battery voltage (2)

3.12. Battery voltages under 100V

3.13. Battery chemistry and machine size

3.14. Chemistry choices in different off-highway industries

3.15. Regional chemistry choices

3.16. Battery lifetime requirements

3.17. Overall battery pack requirements by machine type

3.18. Cost requirements

4. TURNKEY BATTERY TECHNOLOGIES & BENCHMARKING

4.1. Introduction to turnkey technologies

4.1.1. Introduction to turnkey battery suppliers

4.2. Regional availability of turnkey packs

4.2.1. Turnkey pack providers in each region

4.2.2. Regional availability of different chemistries

4.2.3. Regional availability of cell formats

4.3. Performance benchmarking of turnkey packs

4.3.1. Key takeaways - turnkey battery characteristics for off-highway

4.3.2. Comparing turnkey pack sizes with machine requirements

4.3.3. Battery dimensions and form factor

4.3.4. Battery voltage distribution

4.3.5. Ragone plot (gravimetric power vs energy density) by chemistry

4.3.6. Ragone plot by cell format

4.3.7. Turnkey battery discharge C-rates

4.3.8. Charging C-rates of turnkey packs

4.3.9. Tradeoffs between cycle life and energy density

4.3.10. Volumetric vs gravimetric energy density

4.4. Thermal management strategies

4.4.1. Thermal management overview

4.4.2. Air cooling

4.4.3. Liquid Cooling

4.4.4. Immersion Cooling

4.4.5. Thermal management benchmarking

4.4.6. Thermal management & charging performance of turnkey packs

4.4.7. IDTechEx reports on thermal management for batteries

4.5. Cell-to-pack & cell-to-body in off-highway batteries

4.5.1. What is cell-to-pack

4.5.2. Drivers & challenges of CTP

4.5.3. CATL CTP batteries

4.5.4. CATL CTP 3.0

4.5.5. Cell-to-body

4.5.6. BYD CTB batteries

4.5.7. CTP & CTB in off-highway signalling a continued shift in the market

4.5.8. Emergence of electrode-to-pack

4.5.9. IDTechEx reports on CTP & CTB

4.6. Charging for off-highway machinery

4.6.1. Charging solutions in construction, agriculture, and mining

4.6.2. BESS for off-highway charging: Liebherr

4.6.3. BESS for off-highway charging: Volvo & Caterpillar

4.6.4. BESS for off-highway charging: Turntide

4.6.5. BESS for off-highway charging: AMPD

4.6.6. IDTechEx reports on BESS for off-highway charging

5. BATTERY SUPPLIERS & CASE STUDIES

5.1. Turnkey battery manufacturers

5.1.1. Turnkey manufacturers by region

5.1.2. Turnkey manufacturers by chemistry

5.1.3. Turnkey manufacturers by cell format

5.1.4. Turnkey manufacturers by thermal management

5.1.5. Microvast

5.1.6. Forsee Power

5.1.7. BorgWarner

5.1.8. Webasto

5.1.9. Leclanche

5.1.10. ABB

5.1.11. Kreisel Electric

5.1.12. Proventia

5.1.13. IMPACT Clean Power Technology

5.1.14. American Battery Solutions (subsidiary of Komatsu)

5.1.15. Develon (Hyundai)

5.2. LTO packs for hybrid applications

5.2.1. LTO packs and applications in hybrids

5.2.2. Forsee Power and Kubota - micro-hybrid engine

5.2.3. Proventia low-voltage batteries

5.2.4. Hyliion battery module for hybrids

5.3. Acquisitions, spinouts, and liquidations of battery suppliers

5.3.1. Summary and key takeaways

5.3.2. Summary of activity

5.3.3. Proterra acquired by Volvo

5.3.4. American Battery Solutions acquired by Komatsu

5.3.5. Kreisel acquired by John Deere

5.3.6. Yanmar acquisition of Eleo

5.3.7. Hyperdrive acquired by Turntide

5.3.8. XALT Energy acquired by Freudenberg

5.3.9. Accelera - spinout from Cummins

5.3.10. ZQuip - spinout from Moog

5.3.11. Northvolt bankruptcy and acquisition by Scania

5.3.12. Other activities: Xerotech and Akasol

5.4. Battery supplier & OEM relationships

5.4.1. Overview of OEM-battery supplier relationships

5.4.2. Battery supply relationships (1)

5.4.3. Battery supply relationships (2)

5.4.4. Battery supply relationships (3)

5.4.5. Battery supply relationships (4)

5.4.6. Battery supply relationships (5)

6. FUTURE BATTERY TECHNOLOGIES FOR ELECTRIC OFF-HIGHWAY MACHINES

6.1. Overview of future battery technologies

6.1.1. Introduction to future battery technologies

6.1.2. Key differences between battery technologies

6.1.3. IDTechEx reports on future battery technologies

6.2. NMC & LFP

6.2.1. Lithium battery chemistries

6.2.2. Benchmarking typical Li-ion battery options

6.2.3. Li-ion cathode materials - LCO and LFP

6.2.4. Li-ion cathode materials - NMC, NCA and LMO

6.2.5. Moving to high-nickel layered oxides

6.2.6. High-manganese cathodes

6.2.7. Comparing NMC 811 with high-manganese cathodes

6.2.8. Li-ion innovations for off-highway applications

6.3. LTO & niobates

6.3.1. Introduction to lithium titanate oxide (LTO)

6.3.2. Comparing LTO and graphite anodes

6.3.3. LTO for off-highway machines

6.3.4. Emergence of niobates

6.3.5. Nb-based anodes: Nyobolt

6.3.6. Nb-based anodes: Echion

6.4. Silicon anodes

6.4.1. Si-anode definitions

6.4.2. Advantages of Si-anode cells

6.4.3. Challenges of Si-anode cells

6.4.4. Value proposition of high silicon content anodes

6.4.5. Applications of Si-anode for off-highway

6.5. Lithium-metal

6.5.1. Overview of lithium-metal (Li-metal) anodes

6.5.2. Challenges of Li-metal batteries

6.5.3. Enabling Li-metal batteries without solid electrolytes

6.5.4. Comparing Li-metal vs Li-ion on energy density

6.5.5. Anode-less Li-metal cell designs

6.5.6. Li-metal batteries for off-highway applications

6.6. Solid-state batteries

6.6.1. Overview of solid-state batteries (SSBs)

6.6.2. Analyzing benefits and drawbacks of SSBs

6.6.3. Energy density improvement of SSBs

6.6.4. Pack considerations for SSBs

6.6.5. SSBs for off-highway applications

6.7. Lithium-sulphur

6.7.1. Introduction to lithium-sulphur (Li-S)

6.7.2. Advantages of Li-S batteries

6.7.3. Challenges of Li-S batteries

6.7.4. Li-S for off-highway applications

6.8. Sodium-ion

6.8.1. Introduction to sodium-ion (Na-ion)

6.8.2. Na-ion vs Li-ion

6.8.3. Cathode materials for Na-ion

6.8.4. Anode materials for Na-ion

6.8.5. Na-ion battery characteristics

6.8.6. Value proposition of Na-ion batteries

6.8.7. Na-ion for off-highway applications

6.9. Zinc-based batteries

6.9.1. Introduction to zinc-based (Zn-based batteries)

6.9.2. Benefits & drawbacks of Zn-based batteries

6.9.3. Zn-based batteries for off-highway applications

6.10. Summary of battery technologies & applicability to off-highway

6.10.1. Battery technology comparison

6.10.2. Battery technology compatibility: Construction (1)

6.10.3. Battery technology compatibility: Construction (2)

6.10.4. Battery technology compatibility: Mining

6.10.5. Battery technology compatibility: Agriculture

7. FORECASTS

7.1. Overview of forecasts provided

7.2. Forecasts summary & commentary

7.3. Forecast methodology (1): Addressable market & off-highway EV sales

7.4. Global off-highway EV sales by segment (1000s of unit sales) 2024-2036

7.5. Forecast methodology (2): Battery demand, technologies, and revenue

7.6. Forecast assumptions

7.7. Battery pack price assumptions (US$/kWh)

7.8. Global off-highway battery demand by segment (GWh) 2024-2036

7.9. Global off-highway battery demand by region (GWh) 2024-2036

7.10. Global off-highway battery demand by machine type (GWh) 2024-2036 (1)

7.11. Global off-highway battery demand by machine type (GWh) 2024-2036 (2)

7.12. Global off-highway battery demand by technology (GWh) 2024-2036 (1)

7.13. Global off-highway battery demand by technology (GWh) 2024-2036 (2)

7.14. Global off-highway battery revenue by segment (US$ billion) 2024-2036

7.15. Global off-highway battery revenue by region (US$ billion) 2024-2036

7.16. Global off-highway battery revenue by technology (US$ billion) 2024-2036

7.17. Global construction battery demand by technology (GWh) 2024-2036

7.18. Global agriculture battery demand by technology (GWh) 2024-2036

7.19. Global mining battery demand by technology (GWh) 2024-2036

8. COMPANY PROFILES

8.1. ABB: Batteries & Drivetrains for Off-Highway

8.2. ABB: Electrification of Mining

8.3. AMPD

8.4. AutoNXT

8.5. BatteryOne

8.6. BluVein

8.7. Bobcat: Fully Electric Skid Steer Loader

8.8. Briggs & Stratton

8.9. Carrar: Immersion Cooling

8.10. Caterpillar

8.11. Caterpillar: Electric Construction Machines

8.12. Caterpillar: Hybrid Wheel Loader

8.13. Cavotec

8.14. CNH Industrial

8.15. Develon

8.16. Dieci: Electric Telehandler

8.17. Epiroc

8.18. First Mode

8.19. Genie

8.20. Hitachi CM: Electric Haul Truck

8.21. Hixal: Charging for Off-Highway Machines

8.22. HYDAC: Electrification of Off-Highway Machines

8.23. Hyundai Construction Equipment

8.24. Jakob Mining Vehicles

8.25. Jama Mining Machines

8.26. John Deere: Electric & Autonomous Tractors

8.27. John Deere: Electric Construction Machines

8.28. Kato: Electric Mini-Excavators

8.29. Kobelco

8.30. Komatsu: Electrification of Construction Machines

8.31. Kovatera

8.32. Kreisel Electric

8.33. Kubota

8.34. L-Charge

8.35. LiuGong

8.36. Normet: SmartDrive

8.37. PowerCharge: Charging for Electric Off-Highway

8.38. Rokion

8.39. Sandvik

8.40. SANY: Electric Mobile Cranes

8.41. Scania: Electric Trucks for Mining

8.42. Sinoboom

8.43. Snorkel

8.44. Solectrac

8.45. Sunward

8.46. Sunward: Electric Excavators

8.47. Tonly

8.48. Tritium: Charging for Mining Electric Vehicles

8.49. Turntide

8.50. Volvo CE

8.51. WAE Technologies

8.52. WATTALPS: Batteries for Off-Highway Machines

8.53. XCMG: Electric & Autonomous Mining Vehicles

8.54. Yanmar

8.55. Zoomlion: Electric Mining Vehicles

8.56. ZQuip: Batteries for Construction Machines

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|