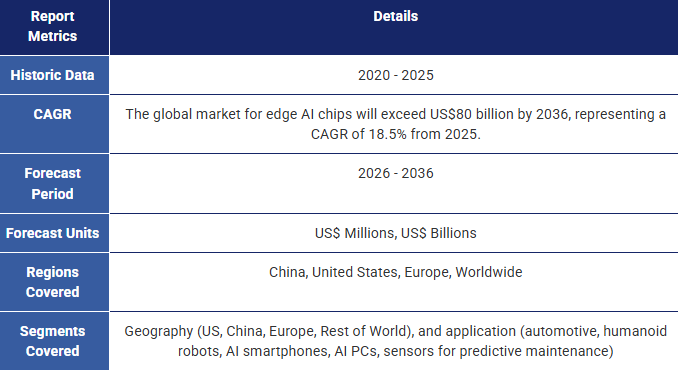

エッジアプリケーション向けAIチップ 2026-2036年:技術動向、市場動向、予測AI Chips for Edge Applications 2026-2036: Technologies, Markets, Forecasts エッジAIチップの10年予測:自動車、民生用電子機器、ヒューマノイドロボット、予知保全など多様な用途別。CPU、NPU、GPUを含むサプライチェーン分析。自動運転、インテリジェントコックピット、AIスマートフ... もっと見る

サマリーエッジAIチップの10年予測:自動車、民生用電子機器、ヒューマノイドロボット、予知保全など多様な用途別。CPU、NPU、GPUを含むサプライチェーン分析。自動運転、インテリジェントコックピット、AIスマートフォン、AI PC。

エッジアプリケーション向けAIチップ 2026-2036:技術動向・市場規模・予測

エッジデバイス向けグローバルAIチップ市場は2036年までに800億米ドルを超える見込み。市場規模で最大の応用分野は自動車とAIスマートフォン。人工知能(AI)は既に、高頻度取引における不正検知から、文書作成の時間を大幅に節約する生成AIの活用、創造的なプロンプトとしての利用に至るまで、様々な応用分野で変革をもたらす可能性を示している。 ニューラルネットワークアーキテクチャを採用した半導体チップ(機械学習ワークロードの処理に特に適したアーキテクチャであり、機械学習は機能するAIの不可欠な要素である)の使用はデータセンター内で一般的であるが、AI導入の大きな機会はエッジ側にある。 エッジデバイスに多様な機能を提供すること、また特定のアプリケーションでは人的作業をインテリジェントシステムに完全に外注できることのエンドユーザーへの利点は非常に大きい。AIは既に世界トップクラスのメーカーのフラッグシップスマートフォンに搭載されており、乗用車からヒューマノイドロボットまで、様々なデバイスへの展開が予定されている。

IDTechExは、グローバルなエッジAIチップ技術動向と関連市場に関する独自の独立した洞察を提供する市場レポートを発表した。 本レポートでは、エッジデバイス向けAIチップ設計に関わる主要プレイヤーの包括的分析に加え、技術革新と市場動向の詳細な評価を掲載。市場分析と予測は総収益に焦点を当て、地域別(中国、欧州、米国、その他地域)および用途別(自動車、ヒューマノイドロボット、AIスマートフォン、AIノートPC、予知保全用エッジセンサー)に細分化した予測を提供。

本レポートは主要プレイヤーのデータ分析と知見を提示し、IDTechExの半導体・コンピューティング・エレクトロニクス分野における専門性を基盤としています。

本調査は以下のような企業に有益な知見を提供します:

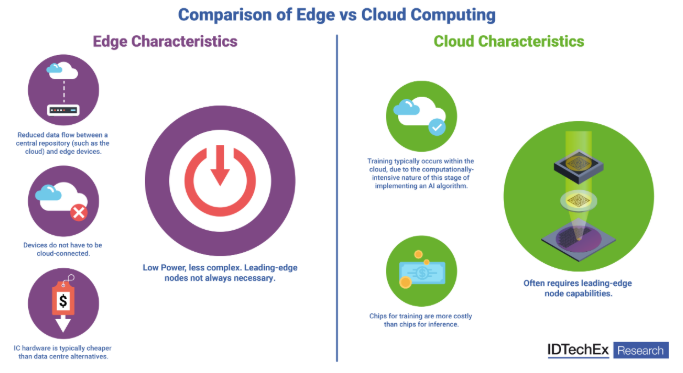

コンピューティングは、ネットワーク内のどこで計算が行われるか(つまり、クラウド内かネットワークのエッジか)によって区分できます。本レポートは、AIおよび機械学習アプリケーション向けにエッジに展開される専用チップに焦点を当てています。

エッジにおける人工知能

エッジとクラウドのコンピューティング環境の差異は軽視できない。各環境には固有の要件と能力があるからだ。エッジコンピューティング環境とは、ネットワークの端(つまりユーザーに近い位置)にあるデバイス(通常はデータが生成されるデバイスそのもの)上で計算が実行される環境を指す。 これはネットワークの中心にあるクラウドやデータセンターでのコンピューティングとは対照的である。このようなエッジデバイスには、自動車、カメラ、ノートパソコン、携帯電話、自律走行車などが含まれる。計算はユーザーに近い、データが存在するネットワークのエッジで実行される。このエッジコンピューティングの定義から、エッジAIとはネットワークのエッジにおけるAIアプリケーションの展開を指す。 エッジデバイス上でAIアプリケーションを実行する利点には、計算を実行するためにクラウドとエッジデバイス間でデータを往復させる必要がないことが含まれる。したがって、AIアルゴリズムを実行するエッジデバイスは、インターネットやクラウドへの接続を必要とせずに迅速に意思決定を行うことができる。 多くのエッジデバイスはバッテリー駆動であるため、データセンター内よりも消費電力が低いAIチップが必要となり、これらのデバイス上で効果的に動作させることが可能となる。その結果、より少ない電力を必要とする、一般的に単純化されたアルゴリズムが導入される傾向にある。

エッジにおけるAIの成長

2036年までに800億米ドルを超えると予測されているにもかかわらず、今後10年間のエッジAI市場の大幅な成長は容易ではない。これは、既存のチップセットに既にAIアーキテクチャを採用している特定の市場の飽和状態と、大量展開前に厳格なテストが必要な状況によるものである。 例えばスマートフォン市場は既に飽和状態に入りつつある。高級化傾向(販売台数に占める高級スマートフォンの割合が年々増加)は継続しているが、AI収益は高級スマートフォンの販売増加に伴って拡大する。これらの端末はチップセットにAIコプロセッシング機能を組み込んでいるため、今後10年でこの分野自体も飽和状態に達すると予想される。

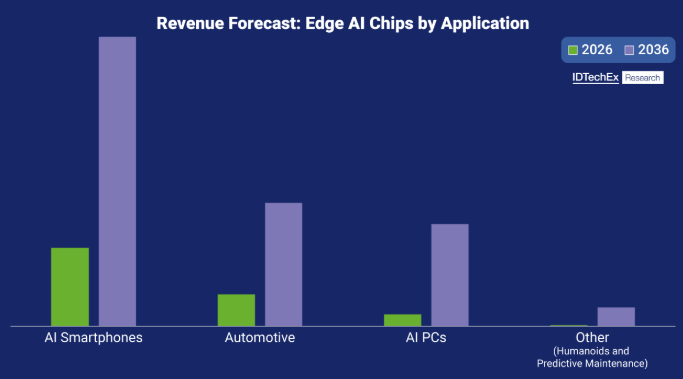

IDTechExは、エッジAIチップの最大市場として、民生用電子機器(AIスマートフォン・AI PC)と自動車(自動運転・インテリジェントコックピット機能)を予測している。出典:IDTechExレポート「AI Chips for Edge Applications 2026-2036: Technologies, Markets, Forecasts」

自動車向けエッジAI

自動車技術会(SAE)が定義するレベル0(自動化なし)からレベル5(完全自動化)までの高度な自動運転は、自動車分野におけるメガトレンドである。ロボットタクシーは世界的に新たな都市へ拡大を続け、一方、自動運転機能を備えた個人所有車両も増加する見込みだ。 2026年には、SAEレベル2+(ハンドル操作不要、視線操作必要)からレベル3(条件付き視線操作不要)への移行により、特定のシナリオにおいて車両の責任がドライバーからOEM(自動車メーカー)へ移行する。したがって、信頼性・一貫性・安全性を保証するため、こうした車両ではエッジAI能力の強化が不可欠であり、さもなければOEMは法的リスクに直面する可能性がある。 さらに、インテリジェントコックピットには追加のAI演算能力が必要となり、これは別チップに統合されるか、単一チップ上で自動運転やADAS(先進運転支援システム)と統合される可能性がある。

ヒューマノイド向けエッジAI

2026年現在、ヒューマノイドロボットは特に自動車製造現場において、普及と展開が加速している。自動車産業が導入の起点となる一方、今後10年間でIDTechExは、パトロール・監視・家庭環境など、より開放的で過酷な環境での展開を予測している。

ヒューマノイドロボット市場全体の成長と並行して、IDTechExはロボット1台あたりに必要なAI演算能力が大幅に増加すると予測している。これは、製造現場で現行のヒューマノイドロボットが担当する典型的なピッキング・配置作業やその他の物流業務から、より高度なタスクが割り当てられるためである。

民生電子機器向けエッジAI

2026年1月時点で、主要スマートフォンOEM各社は、生成型写真編集からパーソナライズされたコンテンツ作成に至るまで、AI対応機能をフラッグシップモデルに搭載している。IDTechExは、スマートフォン向けAIチップ市場がエッジAIチップ市場全体を支配すると予測しており、AIチップはフラッグシップモデルでは標準装備となり、ミッドレンジモデルでも普及が進む見込みだ。 最小プロセスノードにおける最先端ハードウェアのコストが上昇し続ける中、メーカーは利益率を維持するため上位機種の普及を推進するため、中級機種が低価格機種の市場シェアを徐々に侵食していく見込みである。

IDTechExは、システムオンチップ(SoC)の一部として専用AIチップを搭載し、性能が40 TOPS(テラ演算/秒)を超えるPCをAI PCと定義している。 2025年時点では新興市場であり、新規PC販売の10%未満がこの定義に該当した。LenovoやAppleなどの主要メーカーがAI PC販売比率の拡大を表明していることから、IDTechExは2030年代初頭までに新規PC販売の大半がAI PCになると予測している。

センサー向けエッジAI

予知保全向けエッジAIは、ボッシュなどの主要センサーサプライヤーやスタートアップ企業にとって急速に注目の的となっている。センサー上で機械学習手法をローカルに実行することで、システムは実際に発生する前にメンテナンスや修理が必要な時期を予測でき、稼働時間の大幅な増加と潜在的なコスト削減をもたらす。 必要なAI演算量は、自律走行車やAI PCなどと比べて通常はるかに低く、したがってコストも抑えられます。今後10年間でスマート工場の増加が見込まれる中、より多くのMEMSセンサーやIMUセンサーにエッジ側でのAI機能が組み込まれるでしょう。

主要な側面

本レポートは、エッジにおけるAIハードウェア、特に機械学習ワークロードの高速化に用いられるチップに関する重要な市場情報を提供する。内容は以下の通り:

目次

1. エグゼクティブサマリー

1.1. エッジAI

1.2. IDTechExによるエッジAIの定義

1.3. エッジとクラウドの特性比較

1.4. AIチップを採用したエッジデバイス

1.5. 主要AIスマートフォンSoCベンダーのロードマップ

1.6. フラグシップAI SoCを採用する主要OEMスマートフォン

1.7. クラムシェル型ノートブック向け主要AI PC SoCベンダーのロードマップ

1.8. AI PC OSプラットフォームにおけるAI機能

1.9. 自動運転ソフトウェアシステム

1.10. 視線離脱運転における演算処理とセンサー要件

1.11. AIを活用したヒューマンマシンインタラクション機能を備えた自動車メーカー

1.12. AI音声アシスタント

1.13. 製造業におけるエッジAIの主要推進要因

1.14. エッジセンシングとエッジAIの融合が予測・予防機能を実現

1.15. エッジセンシングIoTアーキテクチャ

1.16. ロボティクスの進化

1.17. ヒューマノイドAIチップ:テスラ

1.18. エッジAIチップ市場(2025-2036年)用途別

1.19. IDTechEx サブスクリプションでさらに多くの情報にアクセス

2. はじめに

2.1. AIとは何か?

2.2. AIチップとは何か?

2.3. AIアクセラレーション

2.4. AIチップ製品カテゴリーの種類

2.5. 主要AIチップ市場の概要

2.6. エッジAI

2.7. エッジAIの必要性

2.8. エッジとクラウドの特性比較

2.9. AIチップを採用したエッジデバイス

2.10. AIの基礎

2.11. AIの基礎:アルゴリズム、データ、ハードウェア

2.12. トレーニングと推論

2.13. AIチップは低精度演算を利用する

2.14. AIチップにおける一般的な数値表現

2.15. 並列計算:データ並列処理とモデル並列処理

2.16. ディープラーニング:AIアルゴリズムの実装方法

2.17. ニューラルネットワークの解説

2.18. ニューラルネットワークの種類

2.19. ニューラルネットワークの種類とユースケース

3. エッジAIチップ

3.1. CPU、GPU、およびNPU

3.2. エッジAIチップの種類

3.3. GPU

3.4. GPUの歴史的背景

3.5. 2010年代以降のGPUの普及

3.6. GPUのアーキテクチャ

3.7. CPUとGPUの主要なアーキテクチャ上の相違点

3.8. GPUとCPUにおけるレイテンシとスループットの処理方法

3.9. NPU

3.10. NPUとは何か?

3.11. NPUがエッジAIチップを変える

3.12. 商用マイクロコントローラ(MCU)におけるNPUのベンチマーク

4. トランジスタと製造

4.1. トランジスタの動作原理:p-n接合

4.2. ムーアの法則

4.3. 20nm未満における平面型FETへのゲート長縮小の課題

4.4. トランジスタ数の増加

4.5. 平面型FETからFinFETへ

4.6. GAAFET、MBCFET、リボンFET

4.7. TSMCの最先端ノードロードマップ

4.8. インテルファウンドリの最先端ノードロードマップ

4.9. サムスンファウンドリの最先端ノードロードマップ

4.10. GAAFETスケーリングを超えた次世代トランジスタ(CFET)

4.11. デバイスアーキテクチャロードマップ(I)

4.12. スケーリング技術ロードマップ概要

4.13. ICサプライチェーンのプレイヤー分類

4.14. 集積回路サプライチェーンモデル

4.15. IDM製造能力

4.16. ファウンドリ能力

4.17. 製造プロセス別サプライチェーン

5. 消費者向け電子機器

5.1. AIスマートフォン

5.2. AIスマートフォンとエッジAI統合の概要

5.3. モバイルデバイスの競争環境

5.4. 主要SoCベンダー向けモバイルアプリケーションプロセッサ比較

5.5. 主要AIスマートフォンSoCベンダーのロードマップ

5.6. 主要OEMが採用するフラッグシップAI SoC搭載スマートフォン

5.7. フラグシップAIスマートフォンプロセッサ向け現行オンデバイスAI機能

5.8. AIスマートフォン向け主要ハードウェア動向:CPU

5.9. AIスマートフォン向け主要ハードウェア動向:NPU、メモリ、GPU

5.10. AI PC

5.11. AI PC 概要とエッジ統合

5.12. AI PCの現状

5.13. 主要SoCベンダーのAI PCアプリケーションプロセッサ比較

5.14. クラムシェルノートブック向け主要AI PC SoCベンダーのロードマップ

5.15. AI PC OSプラットフォームにおけるAI機能(I)

5.16. AI PC OSプラットフォームにおけるAI機能(II)

5.17. OEMエッジ/ハイブリッドAIアプリケーションの差別化

5.18. AI PC向け主要ハードウェア動向

5.19. AI PC向け主要ハードウェア動向

5.20. ディスクリートNPU:DellとQualcommの事例研究

6. 自動車向けエッジAIチップ

6.1. 自動車におけるエッジAIの必要性

6.2. 自動運転車両におけるAI

6.3. 運転自動化のレベル

6.4. 高度な自動運転レベルは車両あたりのセンサー数を増加させる

6.5. 運転中の視線離脱:演算処理とセンサー要件

6.6. ADS SoCチップの競争環境

6.7. ADS SoCチップの競争環境 - 事例研究

6.8. 高性能SoC

6.9. 高性能SoCチップ - SoCチップの性能進化

6.10. まとめ

6.11. ADASおよび自動運転におけるエッジAI

6.12. 自動運転ソフトウェアシステム

6.13. モジュラーシステムにおける位置特定、予測、計画のためのエッジAI

6.14. エンドツーエンド(E2E)アーキテクチャ

6.15. 端から端までの自動運転のためのトレーニング手法

6.16. 商業利用可能/産業導入済みエンドツーエンドアーキテクチャ

6.17. 大規模AIモデルを採用する主要な米国/欧州のADAS/ADシステム

6.18. 大規模AIモデルを採用する主要な中国製ADAS/ADシステム

6.19. まとめ

6.20. インテリジェントコックピット

6.21. インテリジェントコックピットハードウェア

6.22. エッジAIを活用した主要センシング・ヒューマンマシンインタラクション機能(I)

6.23. エッジAIを活用した主要センシング人機インタラクション機能(II)

6.24. キー操作によるAIを用いたヒューマンマシンインタラクション機能(I)

6.25. 人工知能を用いた人間と機械の相互作用機能の制御(II)

6.26. AIを活用した人間と機械の相互作用機能を備えた自動車メーカー

6.27. AI音声アシスタント

6.28. まとめ

7. エンタープライズエッジAI

7.1. 農業分野におけるエッジAI

7.2. 医療分野における エッジAI

7.3. 製造業およびインダストリー4.0における エッジAI

7.4. 製造業における エッジAI

7.5. 製造業における エッジAIの主要推進要因

7.6. エッジAI対応センシングによる構造健全性モニタリングの高度な洞察

7.7. エッジAIによる品質検査と異常検知

7.8. エッジAIによる適応プロセス制御

7.9. エッジAIによる資産追跡、RTLS、および稼働率管理

7.10. 重要度評価

7.11. エッジAIセンシングと予知保全

7.12. センサーはますます知能化が進み、エッジコンピューティングとAI機能を備えたセンサーのシェアは拡大する見込み

7.13. 産業用IoTにおけるセンサーの進化する役割のロードマップ

7.14. エッジセンシングとエッジAIの融合が予知保全・予防保全機能を実現

7.15. エッジセンシングIoTアーキテクチャ

7.16. クラウド、エッジ、エンドポイントセンシングおよび関連する基盤技術の評価

7.17. 製造・産業分野における計画外ダウンタイムのコスト

7.18. 予知保全

7.19. 事例研究:TI 予測保全エッジシステム

7.20. 事例研究:アナログ・デバイセズ - 予知保全エッジAIセンサー

7.21. 予知保全ハードウェア・ソフトウェアの主要サプライヤー

7.22. 展望 - エッジセンシングが産業用IoTにおける予知保全を実現する

8. ロボットと協働ロボット

8.1. ロボット工学の進化

8.2. エンドエフェクタはロボットと協働ロボット産業をどう変えるか?

8.3. コボット

8.4. ソフトウェアとAI機能 - ユニバーサルロボティクス

8.5. AI駆動型コボットの概要

8.6. ヒューマノイドロボット

8.7. ヒューマノイドロボットの概要

8.8. ヒューマノイドサミットにおける主要なAI知見

8.9. ヒューマノイドのAI/ソフトウェアアーキテクチャ

8.10. ソフトウェアと機能の概要

8.11. ビジョン・言語・アクション(VLA)モデルとその実現を可能にするハードウェア動向

8.12. ソフトウェア - シミュレーション/トレーニング環境と知覚/センシング

8.13. ソフトウェア - モーションプランニングと制御

8.14. ソフトウェア - 基盤モデル

8.15. トレーニングデータの不足 - AIの課題点 - 合成データ生成

8.16. NVIDIA Isaac GR00T - 合成データ生成

8.17. AIハードウェアとソフトウェアの紹介

8.18. ヒューマノイドAIチップ:テスラ

8.19. ヒューマノイドAIチップ:NVIDIA

8.20. 事例研究:NVIDIA Jetson Thor T5000

8.21. エッジAIのVLA基盤モデルへの採用

9. 予測

9.1. IDTechExの予測手法

9.2. エッジAIチップ市場 2025-2036:用途別

9.3. エッジAIチップ市場 2025-2036:スマートフォン

9.4. エッジAIチップ市場 2025-2036:PC

9.5. エッジAIチップ市場 2025-2036: 自動車

9.6. エッジAIチップ市場 2025-2036: ヒューマノイド

9.7. エッジAIチップ市場 2025-2036: 予知保全用センサー

10. 10. 企業プロファイル

10.1. 企業プロファイル

SummaryTen-year forecasts of edge AI chips for different applications: automotive, consumer electronics, humanoid robots, predictive maintenance. Supply chain analysis, including CPUs, NPUs, GPUs. Autonomous driving, intelligent cockpits, AI smartphones, AI PCs.

AI Chips for Edge Applications 2026-2036: Technologies, Markets, Forecasts

The global AI chips market for edge devices will exceed US$80 billion by 2036, with the largest applications by market size being automotive and AI smartphones. Artificial Intelligence (AI) is already displaying significant transformative potential across a number of different applications, from fraud detection in high-frequency trading to the use of generative AI as a significant time-saver for the preparation of written documentation, as well as a creative prompt. While the use of semiconductor chips with neural network architectures (these architectures being especially well-equipped in handling machine learning workloads, machine learning being an integral facet to functioning AI) is prevalent within data centers, it is at the edge where significant opportunity for adoption of AI lies. The benefits to end-users of providing a greater array of functionalities to edge devices, as well as, in certain applications, being able to fully outsource human-hours to intelligent systems, is significant. AI has already found its way into the flagship smartphones of the world's leading designers and is set to be rolled out across several different devices, from passenger vehicles to humanoid robots.

IDTechEx has published a market report that offers unique independent insights into the global edge AI chip technology landscape and corresponding markets. The report contains a comprehensive analysis of players involved with AI chip design for edge devices, as well as a detailed assessment of technology innovations and market dynamics. The market analysis and forecasts focus on total revenue, with granular forecasts that are segmented by geography (China, Europe, US, and Rest of World) and application (automotive, humanoid robots, AI smartphones, AI laptops, edge sensors for predictive maintenance).

The report presents an analysis of data and insights from key players, and it builds on IDTechEx's expertise in the semiconductor, computing and electronics sectors.

This research delivers valuable insights for:

Computing can be segmented by where computation takes place within the network (i.e. within the cloud or at the edge of the network). This report focuses on specialized chips deployed at the edge for AI and machine learning applications.

Artificial Intelligence at the Edge

The differentiation between edge and cloud computing environments is not a trivial one, as each environment has its own requirements and capabilities. An edge computing environment is one in which computations are performed on a device - usually the same device on which the data is created - that is at the edge of the network (and, therefore, close to the user). This contrasts with cloud or data center computing, which is at the center of the network. Such edge devices include cars, cameras, laptops, mobile phones, autonomous vehicles, etc. Computation is carried out close to the user, at the edge of the network where the data is located. Given this definition of edge computing, edge AI is therefore the deployment of AI applications at the edge of the network. The benefits of running AI applications on edge devices include not having to send data back and forth between the cloud and the edge device to carry out the computation; as such, edge devices running AI algorithms can make decisions quickly without needing a connection to the internet or the cloud. Given that many edge devices run on a power cell, AI chips used for such edge devices need to have lower power consumption than within data centers, in order to be able to run effectively on these devices. This results in typically simpler algorithms being deployed, that don't require as much power.

The growth of AI at the edge

Despite being predicted to exceed US$80 billion by 2036, the substantial growth of the edge AI market over the coming decade will not be straightforward. This is due to the saturation and stop-start nature of certain markets that have already employed AI architectures in their incumbent chipsets, and where rigorous testing is necessary prior to high volume rollout, respectively. For example, the smartphone market has already begun to saturate. Though premiumization of smartphones continues (where the percentage share of total smartphones sold given over to premium smartphones increases year-on-year), where AI revenue increases as more premium smartphones are sold. Because these smartphones incorporate AI coprocessing in their chipsets, it is expected that this will itself begin to saturate over the next ten years.

IDTechEx forecasts consumer electronics (AI smartphones and AI PCs) and automotive (autonomous driving and intelligent cockpit functions) to be the largest markets for edge AI chips. Source: IDTechEx's report "AI Chips for Edge Applications 2026-2036: Technologies, Markets, Forecasts".

Edge AI for automotive

Higher degrees of autonomy, as defined by the Society of Automotive Engineers (SAE) from levels 0 (no automation) to 5 (full automation) is a megatrend in the automotive sector. Robotaxis continue to expand into new cities globally, while an increasing number of private vehicles will have autonomous features. In 2026, a shift from SAE level 2+ (hands off, eyes on), to level 3 (conditional eyes off) pushes responsibility of the vehicle from the driver to the OEM in some scenarios. Edge AI capabilities will therefore be greater for such vehicles to guarantee reliable, consistent, and safe behavior, or OEMs could face legal issues. Furthermore, intelligent cockpits will require further AI compute, which can be integrated onto a separate chip, or combined with autonomous driving and ADAS (advanced driver assistance systems) on a single chip.

Edge AI for humanoids

As of 2026, humanoid robots are gaining more traction and beginning to see scaling and deployments, particularly on automotive manufacturing floors. While the automotive industry is where deployments will start, over the next decade IDTechEx is expecting to see deployments in more open, challenging environments, such as for patrolling, surveillance, and households.

In parallel to the overall growth of the humanoid robots market, IDTechEx expects the required AI compute per robot to increase significantly, as they are assigned more challenging tasks from the typical picking, placing, and other logistics work deployed by current humanoid robots on manufacturing floors.

Edge AI for consumer electronics

As of January 2026, every major smartphone OEM has AI enabled features on its flagship phones, ranging from generative photo editing to personalized content creation. IDTechEx forecasts the AI chips for smartphones market to dominate the overall edge AI chip market, with AI chips becoming standard in flagship phones and more common in mid-range phones. Mid-range phones will gradually eat into market share of budget phones, as manufacturers will push for higher-range phones to maintain margins as the cost of leading edge hardware on the smallest process nodes continues to increase.

IDTechEx defines AI PCs as those with dedicated AI chips as part of the system-on-chip (SoC) with performance exceeding 40 TOPS (tera-operations per second). In 2025, this was an emerging market, with less than 10% of new PC sales fitting this definition. With leading manufacturers such as Lenovo and Apple committing to a greater proportion of AI PC sales, IDTechEx expects the majority of new PC sales to be AI PCs by the early 2030s.

Edge AI for sensors

Edge AI for predictive maintenance is quickly becoming a topic of focus for major sensor suppliers such as Bosch, as well as start-ups. By running machine learning methods locally on the sensor, systems can predict when maintenance and repair is required before it actually happens, yielding a significant increase in uptime and potential money savings. The AI compute required is typically much lower than in autonomous vehicles or AI PCs, for example, and will therefore be less expensive. With an increasing number of smart factories expected over the next ten years, more MEMS and IMU sensors will be embedded with AI capabilities on the edge.

Key Aspects

This report provides critical market intelligence concerning AI hardware at the edge, particularly chips used for accelerating machine learning workloads. This includes:

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Edge AI

1.2. IDTechEx definition of Edge AI

1.3. Edge vs Cloud characteristics

1.4. Edge devices that employ AI chips

1.5. Leading AI Smartphone SoC Vendor Roadmaps

1.6. Leading OEM Smartphones using Flagship AI SoCs

1.7. Leading AI PC SoC Vendor Roadmaps for Clamshell Notebooks

1.8. AI Features on AI PC OS Platforms

1.9. Autonomous Driving Software Systems

1.10. Eyes Off Driving Compute and Sensor Requirements

1.11. Car Manufacturers with Human-Machine Interaction Functions using AI

1.12. AI Voice Assistants

1.13. Key Drivers of Edge AI in Manufacturing

1.14. Edge Sensing and Edge AI are Converging and Will Unlock Predictive and Proscriptive Functionality

1.15. Edge Sensing Internet Of Things Architecture

1.16. The Evolution of Robotics

1.17. Humanoid AI Chips: Tesla

1.18. Edge AI Chips Market 2025-2036 by Application

1.19. Access more with an IDTechEx subscription

2. INTRODUCTION

2.1. What is AI?

2.2. What is an AI chip?

2.3. AI acceleration

2.4. Types of AI chip product categories

2.5. Overview of major AI chip markets

2.6. Edge AI

2.7. The case for edge AI

2.8. Edge vs Cloud characteristics

2.9. Edge devices that employ AI chips

2.10. Fundamentals of AI

2.11. Fundamentals of AI: Algorithms, Data, and Hardware

2.12. Training and inference

2.13. AI chips use low-precision computing

2.14. Common number representations in AI chips

2.15. Parallel computing: Data parallelism and model parallelism

2.16. Deep learning: How an AI algorithm is implemented

2.17. Neural networks explained

2.18. Types of Neural Networks

2.19. Types of neural networks and use cases

3. EDGE AI CHIPS

3.1. CPUs, GPUs, and NPUs

3.2. Types of Edge AI Chips

3.3. GPUs

3.4. Historical background of GPUs

3.5. GPUs popularity since the 2010s

3.6. Architectures of GPUs

3.7. Key architectural differences between CPUs and GPUs

3.8. Threads show how latency and throughput is handled by GPUs and CPUs

3.9. NPUs

3.10. What is an NPU?

3.11. How NPUs are Changing Edge AI Chips

3.12. Benchmark of NPUs in Commercialized Microcontrollers (MCUs)

4. TRANSISTORS AND MANUFACTURING

4.1. How transistors operate: p-n junctions

4.2. Moore's law

4.3. Gate length reductions pose challenges to planar FETs below 20nm

4.4. Increasing Transistor Count

4.5. Planar FET to FinFET

4.6. GAAFET, MBCFET, RibbonFET

4.7. TSMC's leading-edge nodes roadmap

4.8. Intel Foundry's leading-edge nodes roadmap

4.9. Samsung Foundry's leading-edge nodes roadmap

4.10. CFETs to be used beyond GAAFET scaling

4.11. Device architecture roadmap (I)

4.12. Scaling technology roadmap overview

4.13. IC supply chain player categories

4.14. Integrated circuit supply chain models

4.15. IDM fabrication capabilities

4.16. Foundry capabilities

4.17. Supply chain by production process

5. CONSUMER ELECTRONICS

5.1. AI Smartphones

5.2. Introduction to AI Smartphones & Edge AI Integration

5.3. Mobile device competitive landscape

5.4. Mobile Application Processor Comparison for Leading SoC Vendors

5.5. Leading AI Smartphone SoC Vendor Roadmaps

5.6. Leading OEM Smartphones using Flagship AI SoCs

5.7. Current On-Device AI Features for Flagship AI Smartphone Processors

5.8. Key Hardware Trends for AI Smartphones: CPUs

5.9. Key Hardware Trends for AI Smartphones: NPUs, Memory, and GPUs

5.10. AI PC

5.11. AI PC Introduction and Edge Integration

5.12. AI PC Landscape

5.13. AI PC Application Processor Comparison for Leading SoC Vendors

5.14. Leading AI PC SoC Vendor Roadmaps for Clamshell Notebooks

5.15. AI Features on AI PC OS Platforms (I)

5.16. AI Features on AI PC OS Platforms (II)

5.17. OEM Edge/Hybrid AI Application Differentiation

5.18. Key Hardware Trends for AI PCs

5.19. Key Hardware Trends for AI PCs

5.20. Discrete NPUs: Dell and Qualcomm Case Study

6. AUTOMOTIVE EDGE AI CHIPS

6.1. The Case for Edge AI in Automotive

6.2. AI in Autonomous Vehicles

6.3. Levels of Driving Automation

6.4. High Levels of Autonomy Means More Sensors per Vehicle

6.5. Eyes Off Driving Compute and Sensor Requirements

6.6. Competitive Landscape of ADS SoC Chips

6.7. Competitive Landscape of ADS SoC Chips - Case study

6.8. High-performance SoCs

6.9. High-performance SoC Chips - Performance Evolution of SoC Chips

6.10. Summary

6.11. Edge AI in ADAS and AD

6.12. Autonomous Driving Software Systems

6.13. Edge AI for Localization, Prediction, and Planning in Modular Systems

6.14. End-to-End (E2E) Architecture

6.15. Training Approaches for End-to-End Autonomous Driving

6.16. Commercially Available / Industry-Deployed E2E Architectures

6.17. Major US/European ADAS/AD Systems Using Large AI Models

6.18. Major Chinese ADAS/AD Systems Using Large AI Models

6.19. Summary

6.20. Intelligent Cockpits

6.21. Intelligent Cockpit Hardware

6.22. Key Sensing Human-Machine Interaction Functions using Edge AI (I)

6.23. Key Sensing Human-Machine Interaction Functions using Edge AI (II)

6.24. Key Directing Human-Machine Interaction Functions using AI (I)

6.25. Key Directing Human-Machine Interaction Functions using AI (II)

6.26. Car Manufacturers with Human-Machine Interaction Functions using AI

6.27. AI Voice Assistants

6.28. Summary

7. ENTERPRISE EDGE AI

7.1. Edge AI in Agriculture

7.2. Edge AI in Health Care

7.3. Edge AI in Manufacturing, and Industry 4.0

7.4. Edge AI in Manufacturing

7.5. Key Drivers of Edge AI in Manufacturing

7.6. Richer Structural Health Monitoring Insight With Edge AI-enabled Sensing

7.7. Quality Inspection and Anomaly Detection with Edge AI

7.8. Adaptative Process Control with Edge AI

7.9. Asset Tracking, RTLS, and Utilization with Edge AI

7.10. Critical assessment

7.11. Edge AI Sensing and Predictive Maintenance

7.12. Sensors continue to become more intelligent, with the share of sensors containing edge compute and AI capability set to grow

7.13. Roadmap of the Evolving Role of Sensors in Industrial IoT

7.14. Edge Sensing and Edge AI are Converging and Will Unlock Predictive and Proscriptive Functionality

7.15. Edge Sensing Internet Of Things Architecture

7.16. Evaluating Cloud, Edge, and Endpoint Sensing and Associated Enabling Technologies

7.17. The Cost of Unplanned Downtime in Manufacturing and Industrial

7.18. Predictive Maintenance

7.19. Case Study: TI Predictive - Maintenance Edge Systems

7.20. Case Study: Analog Devices - Predictive Maintenance Edge AI Sensor

7.21. Major Suppliers of Predictive Maintenance Hardware and Software

7.22. Outlook - Edge Sensing Will Unlock Predictive Maintenance in Industrial IoT

8. ROBOTS AND COBOTS

8.1. The Evolution of Robotics

8.2. How Do End-effectors Change The Robot And Cobot Industry?

8.3. Cobots

8.4. Software And AI Features - Universal Robots

8.5. Overview of AI-Driven Cobots

8.6. Humanoid Robots

8.7. Humanoid Robotics Overview

8.8. Humanoid's Summit Key AI Findings

8.9. AI/software architecture of humanoids

8.10. Summary of Software and Functions

8.11. Vision Language Action (VLA) Model and its Enabling Hardware Trend

8.12. Software - Simulation/Training Environments And Perception/Sensing

8.13. Software - Motion Planning And Control

8.14. Software - Foundation Model

8.15. Lack Of Training Data - Pain Points Of AI - Synthetic Data Generation

8.16. NVIDIA Isaac GR00T - Synthetic Data Generation

8.17. AI Hardware and Software Introduction

8.18. Humanoid AI Chips: Tesla

8.19. Humanoid AI Chips: NVIDIA

8.20. Case Study: NVIDIA Jetson Thor T5000

8.21. Adoption of Edge AI for VLA Foundation Models

9. FORECASTS

9.1. IDTechEx's Forecast Methodology

9.2. Edge AI Chips Market 2025-2036 by Application

9.3. Edge AI Chips Market 2025-2036: Smartphones

9.4. Edge AI Chips Market 2025-20-36: PCs

9.5. Edge AI Chips Market 2025-2036: Automotive

9.6. Edge AI Chips Market 2025-2036: Humanoids

9.7. Edge AI Chips Market 2025-2036: Sensors for Predictive Maintenance

10. 10. COMPANY PROFILES

10.1. Company profiles

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(通信・IT)の最新刊レポート

IDTechEx社の 5G, 6G, RFID, IoT分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|