ドローン市場2026-2036年:技術、市場、機会Drones Market 2026-2036: Technologies, Markets, and Opportunities AI、自律性、群制御、BVLOS、軍事用ドローン、ロジスティクス、検査、マッピング、農業、VTOL、センサーフュージョン、推進力、コネクティビティ、対UAS、世界のUAV市場 世界のドローン市場... もっと見る

サマリー

AI、自律性、群制御、BVLOS、軍事用ドローン、ロジスティクス、検査、マッピング、農業、VTOL、センサーフュージョン、推進力、コネクティビティ、対UAS、世界のUAV市場

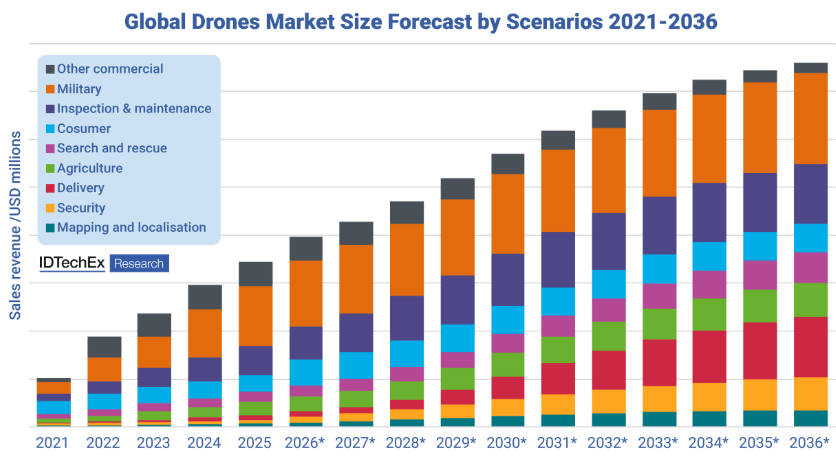

世界のドローン市場は2036年までに1478億米ドルに到達、商業的拡大、規制の成熟、センサーの普及が原動力

過去10年間で、ドローンは実験的なツールから農業、ロジスティクス、エネルギー、セキュリティ、公共部門の業務にわたる重要なインフラへと移行した。2036年までに、商業用と消費者用の両方のプラットフォームにまたがる世界のドローン市場は、2026年の690億米ドルから成長し、年平均成長率7.9%で1,478億米ドルに達するとIDTechExは予測している。商業ベースでの導入は急速に加速しており、2036年には出荷台数が900万台を突破すると予想されている。この成長は、規制の明確化、技術スタックの成熟化、ハードウェアコストの低下、自律的でデータ駆動型のオペレーションへの移行を反映している。

世界のドローン市場収益予測(2026-2036年)。出典:IDTechExIDTechEx

農業は大規模デジタル農業の時代に突入

農業用ドローンは、特に中国、米国、東南アジアにおいて、初期の試験段階から完全な商業的成熟へと進化している。散布、播種、作物モニタリングなどのコア・アプリケーションは収益性が高く、広く採用されるようになった。マルチローター・プラットフォームが依然として優勢だが、固定翼とハイブリッドVTOL(垂直離着陸)ドローンが、大面積の農地マッピングや長距離自律ミッションでシェアを伸ばしている。

2025年には、世界の大規模農場の30%以上が圃場作業にドローンを使用していると推定されている。AIビジョン、マルチスペクトル画像処理、精密分析の統合により、データ中心の農業モデルが可能になり、拡大が続く。今後の成長は、ドローンのデータをスマート農業エコシステムと連携させ、自動化された農学的判断を行うことに大きく依存するだろう。

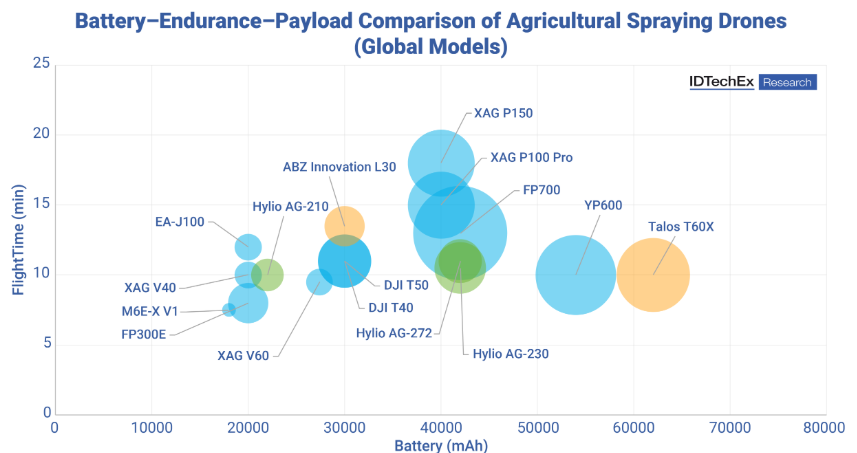

農業用散布ドローンのバッテリー耐久性とペイロードの比較

バブルの大きさはペイロード容量を示す:大きなバブルはより高い液体運搬能力を持つドローンを表す。色は原産地を示す:青=中国、緑=米国、オレンジ=欧州。

出典IDTechEx

検査とメンテナンスが急成長分野に

エネルギー、公益事業、インフラ事業者は、風力タービン、送電線、パイプライン、石油・ガス資産の自動ドローンによる検査に急速にシフトしている。LiDAR、赤外線画像、AIを活用した欠陥検出機能を備えたドローンは、コストのかかる危険な手動検査に取って代わりつつある。

2025年以降、ドローン・イン・ア・ボックス・システム、遠隔フリート管理、AIクラウド分析など、完全自動化ワークフローの導入が進むと予想される。点検・メンテナンスは、2030年までに商業用ドローン全体の売上の25%を超え、農業を抜いて主要セグメントになると予測されている。

宅配ドローンは試験運用から地域商業化へ成熟

規制やロジスティクスの課題にもかかわらず、ドローン宅配は現在、本格的な商業的牽引力を獲得しつつある。米国、欧州、中国の大手企業は、電子商取引、食品、医療輸送のラストワンマイル配送を拡大しており、遠隔地や島嶼部の供給ルートでは中距離の物流ドローンが台頭している。

自動積載、コールドチェーン・ドローン・ロジスティクス、U-space/UTM(無人交通管理)フレームワークにおける業界の進歩は、大規模なオペレーションへの道を開いている。配送ドローンの長期的な軌道は、BVLOS(Beyond Visual Line of Sight)の承認と国家的なUTMの展開に大きく依存する。

セキュリティ、軍事、公共安全が強い勢いを維持

政府や法執行機関は、国境警備、監視、交通管理、群衆監視、緊急対応にドローンを採用している。

ハイブリッド固定翼VTOLドローンは、広域での長時間飛行を可能にし、AIベースのビデオ解析は状況認識を強化する。公共安全は、2036年まで安定し、着実に拡大するセグメントであり続けると予想される。

軍事用ドローンが最大の収益貢献者であり続ける

軍事用ドローン分野は、絶対収益でドローン市場全体をリードし続けている。2022年以降、地域紛争が偵察ドローン、中距離戦術ドローン、浮遊弾薬の需要を加速させている。

また、軍隊はドローンを航空機や装甲車と統合する有人-無人チーム(MUM-T)コンセプトに向かっている。デュアルユース技術が防衛に再利用されつつある一方で、中核的な軍事用ドローン分野は今後も高い収益性を維持し、戦略的に不可欠である。

災害対応は引き続きドローンの能力に依存する

赤外線、光学、音響センサーを搭載したドローンは、夜間の捜索任務、地震の救助、山火事の監視、災害後の評価に重要な役割を果たす。

マルチドローン連携やAIベースのジオロケーションアルゴリズムの進歩により、運用効率が大幅に向上している。絶対的な売上規模は小さいものの、この分野は政府の強力なバックアップを受けており、長期的に安定した成長を続けている。

世界的な規制の調和とリスクベースのフレームワークへの移行

ドローン規制は、リスクベースの段階的な認証システムを中心にますます整合性が高まっている。米国(パート107)、EU(C0-C6)、英国(CAP722)、中国はいずれも商業運航、特にBVLOSのためのより明確な経路を確立している。

共通する規制テーマは以下の通り

北米とEUは調和のとれた枠組みでリードしているが、アジア太平洋、中南米、中近東諸国は依然として断片的である。

センサーの普及がドローンのペイロード構成を再形成

2025年から2036年にかけて、商業用ドローンの出荷台数は2.3倍に成長すると予想されるが、センサーの出荷台数は4倍に成長し、センサー密度の向上とより高度な自律性への大きなシフトを示す。

2036年までに、多くの産業用ドローンやBVLOSドローンは、1機当たり10~15センサーを超えると予想され、その原動力は以下の通りである:

IDTechExによる2026-2036年完全再構築予測

本レポートは、運用を形作る規制上の制約や各地域における展開の成熟度を含め、消費者、商業、防衛の各セクターにわたる世界のドローン産業の進展について包括的な概要を提供している。また、農業や検査からロジスティクスや公共安全まで、主要な用途で使用されるあらゆるセンシングとペイロードの構成を検証し、異なるコスト構造とミッション要件がプラットフォームの選択をどのように促すかを説明している。さらに、代表的な商業用ドローンのモデル、その技術仕様、センサースイート、価格帯、市場での位置づけの詳細なリストと、収益、出荷台数、センサーの統合動向を網羅した2026年~2036年の完全最新予測を掲載している。

IDTechExは、完全に更新された10年間のドローン市場予測を提供しています

主要な側面

本レポートは、消費者向け、商業用、防衛用プラットフォーム、およびすべての主要なアプリケーション分野を網羅し、世界のドローン産業に関する重要な市場情報を提供します。内容は以下の通りです:

ドローンシステムを支える背景、技術、規制のレビュー

主要なドローン用途分野ごとの完全な市場特性

市場分析を通じて

目次1.エグゼクティブ・サマリー

1.1.1.エグゼクティブ・イントロダクション

1.1.2.エグゼクティブ・イントロダクション

1.1.3.最新ドローンのカテゴリーと市場構造の概要

1.2.主要アプリケーションと成長動向

1.2.1.主要アプリケーション分野の概要

1.2.2.ケーススタディ:コスト構成と価値分布

1.2.3.農業:ドローンイメージングに使用されるセンサーの比較

1.2.4.農業産業:ドローンイメージングで使用されるセンサーの比較

1.2.5.ドローンセンサー市場動向

1.2.6.農業産業:ドローンの自律化が進む

1.3.各産業におけるドローンのプレーヤーとモデルのまとめ

1.3.1.市販されている農業用散布ドローン

1.3.2.市販されている農業用散布ドローン

1.3.3.市販の農作物モニタリングドローン

1.3.4.産業・インフラ点検(送電網、風力タービン、石油・ガスパイプライン)

1.3.5.線形資産検査(送電線、パイプライン、鉄道)

1.3.6.近距離精密検査(インフラ、電力、風力タービン)

1.3.7.特殊環境(閉鎖空間/非破壊検査)

1.3.8.メタン/排出ガスモニタリング(ESG & コンプライアンス)

1.3.9.UAVベースのメタン検知技術のマスター比較

1.3.10.範囲別物流・貨物ドローンの商業化状況

1.3.11.物流・荷役用ドローンのキーポイント

1.3.12.物流・貨物配送ドローン概況と成熟度評価(1)

1.3.13.物流・貨物配送ドローン:概況と成熟度評価(2)

1.3.14.軍事・防衛の主要な要点:浮遊軍需品

1.3.15.軍事・防衛浮遊する軍需品

1.4.予測

1.4.1.商業用ドローンの台数予測(2026年-2036年)

1.4.2.ドローン全体の台数予測(2026年-2036年)

1.4.3.商用ドローンの収益予測(2026年-2036年)

1.4.4.ドローンの世界市場シナリオ別収益予測(2026年-2036年)

1.4.5.ドローンの世界市場収益シナリオ別予測(1)

1.4.6.シナリオ別ドローンの世界市場収益予測(2)

1.4.7.ドローンの世界市場シナリオ別収益予測(3)

1.4.8.ドローンセンサーの市場規模予測(2026-2036年)

1.4.9.ドローンセンサーの市場規模予測(2026-2036年)

1.4.10.ドローンセンサ市場規模予測(2026-2036)

2.はじめに

2.1.ドローンとは?

2.2.はじめに

2.3.センサーフュージョン:ナビゲーショナル・オートノミーに向けて

3.グローバルな規制の枠組み

3.1.規制-国別のハイレベル規制要件

3.2.世界のドローン規制

3.3.中国

3.4.米国空域と操縦免許の枠組み

3.5.米国新たな BVLOS 規制(1)

3.6.米国:新たなBVLOS規制(2)

3.7.EU

3.8.欧州連合オペレーショナル・カテゴリーとリスク・ベースの監督

3.9.英国

3.10.英国

3.11.ブラジルドローン規制の概要(1)

3.12.ブラジルドローン規制の概要(2)

4.主な応用分野

4.1.商業市場製品

4.1.1.ドローンアプリケーション・パイプライン

4.1.2.ドローンアプリケーションパイプライン(1)

4.1.3.ドローンアプリケーション・パイプライン(2)

4.2.商業市場製品-農業用ドローン

4.2.1.農業用ドローン産業のバリューチェーン(1)

4.2.2.農業用ドローン産業のバリューチェーン(2)

4.2.3.農業用ドローン産業のバリューチェーン(3)

4.2.4.農業用ドローン主な用途

4.2.5.農業用ドローンの主な種類

4.2.6.農業用散布ドローン-農薬と肥料

4.2.7.市販されている農業用散布ドローン

4.2.8.市販されている農業用散布ドローン

4.2.9.作物のモニタリングと分析におけるドローン

4.2.10.農業におけるレーダー - Sarmap

4.2.11.クランフィールド大学 - UAVレーダーによる土壌水分モニタリング

4.2.12.市販の農作物モニタリング用ドローン

4.2.13.市販されている農作物モニタリング用ドローン

4.2.14.ドローン・イメージングに使用されるセンサーの比較

4.2.15.ドローン・イメージングに使用されるセンサーの比較

4.2.16.ドローン vs 人工衛星 vs 飛行機

4.2.17.ドローン散布はどこで規制承認されているか?

4.2.18.EUの農業用ドローン管理の進展

4.2.19.米国の農業用ドローン管理の進展

4.2.20.中国の農業用ドローン管理の進展

4.2.21.欧州における農業ドローン農薬管理 - ISO 23117-1:2023 / ISO 23117-2:2025 (1)

4.2.22.欧州における農業用ドローン農薬管理 - ISO 23117-1:2023 / ISO 23117-2:2025 (2)

4.2.23.ドローンの自律化が進む

4.2.24.BVLOSを可能にするインフラと技術

4.2.25.農業用ドローン企業ランドスケープ

4.2.26.農業用ドローンにおける潜在的ソフトウェア機会

4.2.27.Tevel Aerobotics Technologiesのフルーツピッキングドローン

4.2.28.HayBeeSee社のCropHopper

4.2.29.垂直農法におけるデジタルモニタリング

4.3.商業市場製品-産業・インフラ検査

4.3.1.産業・インフラ検査(送電網、風力タービン、石油・ガスパイプライン)

4.3.2.リニア検査(送電線、パイプライン、鉄道)

4.3.3.リニア検査(送電線、パイプライン、鉄道)

4.3.4.近距離精密検査(インフラ、電力、風力タービン)

4.3.5.近距離精密検査(インフラ、電力、風力タービン)

4.3.6.特殊環境(閉鎖空間/非破壊検査)

4.3.7.特殊環境(閉鎖空間/非破壊検査)

4.3.8.メタン/排出ガスモニタリング(ESG & コンプライアンス)

4.3.9.メタン/排出ガスモニタリング(ESG&コンプライアンス)

4.3.10.メタン検知技術 - 比較(1)

4.3.11.メタン検知技術 - 比較(2)

4.3.12.UAVベースのメタン検知技術のマスター比較

4.3.13.データプラットフォーム&サービス(AI/デジタルツイン)

4.3.14.エクセター大学の側溝清掃 - ドローンによるデータ収集

4.3.15.UAVによる原子力施設の廃止措置 - ユースケース・スタディ:英国セラフィールド

4.3.16.クランフィールド大学 - 鉄道操車場監視のための無人航空機システムコンセプトデザイン

4.4.商業市場製品-物流

4.4.1.物流と貨物配送(ラストマイル、緊急物資)

4.4.2.ラストマイル、ミッドマイル、長距離ドローン配送の概要

4.4.3.ラストマイル、ミッドマイル、長距離ドローン配送のシナリオ

4.4.4.物流・貨物用ドローンの航続距離別商品化状況

4.4.5.物流・貨物用ドローンの地域別商品化状況:米国

4.4.6.物流・貨物用ドローンの地域別商品化状況

4.4.6:EU

4.4.7.物流・貨物用ドローンの地域別商品化状況:中国

4.4.8:中国

4.4.8.物流・貨物配送ドローン概況と成熟度評価(1)

4.4.9.物流・貨物配送ドローン概況と成熟度評価(2)

4.4.10.物流・貨物配送ドローン

4.4.11。FAA Part 108 BVLOS規制と産業展望2025(1)

4.4.12.FAA Part 108 BVLOS規制と業界の2025年展望(2)

4.4.13.ジップライン

4.4.14.ウイング(アルファベット)

4.4.15.ケーススタディWing vs Zipline - 欧米のドローン物流における競合の道 (1)

4.4.16.ケーススタディWing vs Zipline - 欧米のドローン物流における競合の道 (2)

4.4.17.ケーススタディ中国のドローン物流競争 - SF Express vs JD (1)

4.4.18.ケーススタディ中国のドローン物流競争 - SF Express vs JD (2)

4.4.19.陸上からUAV、UAVから陸上への物流インターチェンジを含むマルチモーダル確率論的ロジスティクス最適化手法 - Solent Transport

4.4.20.医療用ドローン-ソレント運輸

4.4.21.ウィンドレーサーズ(Windracers) - 低コストの自空飛行貨物機のOEM - 南極の科学調査ミッション

4.5.軍事市場製品

4.5.1.軍事・防衛

4.5.2.軍事・防衛

4.5.3.軍事・防衛浮遊軍需品

4.5.4.軍事・防衛徘徊する軍需品

4.5.5.軍事と防衛徘徊する軍需品

4.5.6.軍事・防衛滞空弾

4.5.7.戦術的 COTS 改造 UAV

4.5.8.戦術的COTS改造UAV

4.5.9.ファイバー制御とRF制御:技術の乖離と戦術的 FPV UAV アプリケーション

4.5.10.スカイフォール

4.5.11.バヴォフナ・ミルテック

4.5.12.ウクライナのドローン

4.5.13.TechEx

4.5.14.ケーススタディロシア・ウクライナ紛争における中長距離一方向攻撃ドローン

4.5.15.ケーススタディロシア・ウクライナ紛争における中長距離一方向攻撃ドローン

4.6.災害と救助

4.6.1.災害対応・捜索救助用ドローン

4.6.2.法執行機関のユースケース:空中監視と運用調整の強化

4.6.3.ZenaDrone - 遠隔空中監視ソリューション

4.6.4.消防・災害対応:複雑で危険な環境におけるリアルタイムの空中インテリジェンス

4.6.5.捜索救助/緊急対応:被害者の位置特定を迅速化し、より安全な活動を可能にする

4.6.6.熱センサーとマルチセンサーペイロード

4.6.7.熱センサーとマルチセンサーペイロード

4.6.8.公共安全ドローン用の主流の赤外線画像ペイロード

4.6.9.Xtrafly Systems - 検知とセキュリティにおける潜在的使用例

4.6.10.山火事と煙の早期検知(1)-補足訓練データセットのための生成AI

4.6.11.山火事と煙の早期検知(2)

5.キーテクノロジー

5.1.1.ロボット工学のためのソフトウェア

5.1.2.さまざまな抽象化レベル

5.1.3.ローカライゼーションとマッピング、なぜ同時に?

5.1.4.飛行制御システム(FCS)

5.1.5.SLAM(ローカライゼーションとマッピングの同時実行)

5.1.6.SLAM(ローカライゼーションとマッピングの同時実行)

5.1.7.視覚SLAMとLiDAR SLAMの比較

5.1.8.マルチセンサーSLAM

5.1.9.Exynテクノロジー

5.1.10.様々なSLAMアプローチの利点とIDTechEx

5.1.11.ロボティクスのための視覚言語アクション(VLA)モデル

5.1.12.VLAモデルの進展

5.2.通信とネットワーキング

5.2.1.通信とネットワーキングC2コマンド&コントロール

5.2.2.通信とネットワークセルラーネットワーク

5.2.3.ドローン運用におけるセルラー・アプリケーション

5.2.4.セルラー市場、エコシステムの状況、規制の動向

5.2.5.地域別ドローン運用における 5G 対応状況

5.2.6. 地域別ドローン運用における 5G 対応状況 - 英国と EU

5.2.7.地域別ドローン運用のための5G準備状況 - 米国

5.2.8.地域別ドローン運用のための5G準備状況 - 中国

5.2.9.5.2.9. 地域別ドローン運用に向けた 5G の準備態勢 - UAE およびその他の湾岸諸国

5.3.群制御

5.3.1.群制御:協調分散ドローン運用へのパラダイムシフト

5.3.2.群制御の価値:より高い効率性、より高い回復力、用途の拡大

5.3.3.群制御の価値:より高い効率、より大きな回復力、拡大するアプリケーション

5.3.4.群制御モードとそれを可能にする技術:リーダー・フォロワーとマルチグループ

5.3.5.群制御ソリューション・プロバイダー:グローバル・ランドスケープ(1)

5.3.6.群制御ソリューション・プロバイダー:グローバル・ランドスケープ(2)

5.3.7.群制御技術の準備と商業展開状況

5.3.8.UAV群制御の技術的課題と将来展望

6.ドローンのセンサー

6.1.新たな画像センサー

6.1.1.新興画像センサーの概要

6.1.2.新たな画像センサー主要結論のまとめ

6.1.3.新興イメージセンサー主要プレイヤーの概要(I)

6.1.4.新興イメージセンサー主要プレーヤーの概要(Ⅱ)

6.1.5.SWIR イメージング:概要と主要結論

6.1.6.SWIRイメージング:新たな技術オプション

6.1.7.SWIRセンサー:アプリケーションと主要プレイヤー

6.1.8.OPD-on-CMOS ハイブリッドイメージセンサ:概要、結論、主要プレーヤー

6.1.9.OPD-on-CMOS 検出器:アプリケーション別技術準備レベルロードマップ

6.1.10.QD-on-Si/QD-on-CMOS イメージング:基礎、価値提案、主要結論

6.1.11.ハイパースペクトルイメージング:概要と主要結論

6.1.12.ハイパースペクトル・イメージング:波長範囲とスペクトル分解能

6.1.13.小型分光計:概要と主要結論

6.1.14.小型分光計:幅広い分野をターゲットに

6.1.15.小型化分光計:主要プレーヤーと主な差別化要因

6.1.16.イベントベース・センシング:概要と主要結論

6.1.17.イベントベースのビジョン:アプリケーション要件

6.1.18.LIDAR:動作原理の概要

6.1.19.ロボット工学におけるレーダーとLiDAR

6.1.20.LIDAR:価値提案

6.1.21.LIDAR:エコシステムと主要プレーヤー

6.1.22.カメラの紹介

6.1.23.SWOT-RGB/可視光カメラ

6.1.24.移動プラットフォームとしてのドローン 産業、農業、法執行のための小型軽量ガスセンサーを価値あるものに

6.2.ガスセンサー

6.2.1.ガスセンサー部門の概要とアナリストの視点

6.2.2.ガスセンサー市場の概要

6.2.3.ガスセンサー市場の概要:変化の原動力は?

6.2.4.金属酸化物(MOx)ガスセンサの概要

6.2.5.MOxセンサーの主要メーカーの特定

6.2.6.MOxガスセンサーに関する主要結論とSWOT分析

6.2.7.電気化学式ガスセンサの紹介

6.2.8.電気化学センサーの主要メーカー

6.2.9.電気化学ガスセンサーの主要結論とSWOT分析

6.2.10.赤外線ガスセンサー入門

6.2.11.主要赤外線ガスセンサーメーカーの特定

6.2.12.赤外線ガスセンサーの主要結論とSWOT分析

6.2.13.光イオン化検出器(PID)の紹介

6.2.14.イオン化検出器メーカーの分類

6.2.15.光イオン化検出器の主要結論とSWOT分析

6.2.16.光学式粒子カウンター

6.2.17.光学式粒子計測器の主要メーカーの特定

6.2.18.光学式粒子カウンターのSWOT分析

6.2.19.主要結論:光学式パーティクルカウンター

6.2.20.感知原理:光音響

6.2.21.センシリオンとインフィニオンは小型光音響式二酸化炭素センサを提供

6.2.22.光音響式ガスセンサのSWOT 分析

6.2.23.センシングの原理E-Nose

6.2.24.E-ノーズのセンサータイプの利点と欠点

6.2.25.E-ノーズメーカーの分類

6.2.26.E-ノーズのSWOT分析

6.2.27.E-ノーズのまとめ:鼻よりも特定のアロマがチャンス

6.3.AI入門スライド

6.3.1.AI入門:ゴールポストの移動

6.3.2.人工知能のサブセットとしての機械学習

6.3.3.機械学習のアプローチ

6.3.4.教師あり学習

6.3.5.教師なし学習

6.3.6.教師あり学習と教師なし学習における問題クラス

6.3.7.強化学習

6.3.8.半教師付き学習と能動学習

6.3.9.ニューラルネットワーク-入門

6.3.10.学習プロセスにおける人工ニューロン

6.3.11.ニューラルネットワークの種類

7.予測

7.1.市場予測:方法論の概要

7.2.商業用ドローンの台数予測(2026-2036年)

7.3.全体ドローン台数予測(2026-2036)

7.4.商業用ドローンの収益予測(2026年-2036年)

7.5.ドローンの世界市場収益シナリオ別予測(2026年-2036年)

7.6.ドローンの世界市場シナリオ別収益予測(1)

7.7.ドローンの世界市場収益シナリオ別予測(2)

7.8.シナリオ別ドローンの世界市場収益予測(3)

7.9.ドローン1機あたりのセンサー数予測(2026年-2036年)

7.10.ドローンセンサー市場規模予測(2026年-2036年)

7.11.ドローンセンサー市場規模予測(2026年-2036年)

Summary

AI, autonomy, swarm control, BVLOS, military drones, logistics, inspection, mapping, agriculture, VTOL, sensor fusion, propulsion, connectivity, counter-UAS, global UAV markets

Global Drone Market Set to Reach US$147.8 Billion by 2036, Driven by Commercial Expansion, Regulatory Maturity, and Sensor Proliferation

Over the past decade, drones have moved from experimental tools into critical infrastructure across agriculture, logistics, energy, security, and public-sector operations. By 2036, the global drone market, spanning both commercial and consumer platforms, is forecast by IDTechEx to reach US$147.8 billion, growing from US$69 billion in 2026, with a CAGR of 7.9%. Commercial deployments are accelerating rapidly, with unit shipments expected to surpass 9 million in 2036. This growth reflects increasing regulatory clarity, maturing technology stacks, falling hardware costs, and the transition toward autonomous, data-driven operations.

Global Drone Market Revenue Forecast (2026-2036). Source: IDTechEx

Agriculture enters the era of large-scale digital farming

Agricultural drones have evolved from early trials to full commercial maturity, especially in China, the US, and Southeast Asia. Core applications such as spraying, seeding, and crop monitoring have become profitable and widely adopted. Multirotor platforms still dominate, but fixed-wing and hybrid VTOL (Vertical Take-Off and Landing) drones are gaining share for large-area farmland mapping and long-range autonomous missions.

In 2025, more than 30% of large farms worldwide are estimated to be using drones for field operations. Integration of AI vision, multispectral imaging, and precision analytics enables a data-centric farming model that continues to expand. Future growth will rely heavily on linking drone data with smart farming ecosystems and automated agronomic decisions.

Comparison of Battery-Endurance-Payload of Agricultural Spraying Drones

Bubble size indicates payload capacity: larger bubbles represent drones with higher liquid-carrying capacity. Colors denote regions of origin: blue = China, green = United States, orange = Europe.

Source: IDTechEx

Inspection and maintenance becomes the fastest-growing segment

Energy, utilities, and infrastructure operators are rapidly shifting toward automated drone-based inspection of wind turbines, powerlines, pipelines, and oil & gas assets. Equipped with LiDAR, thermal imaging, and AI-powered defect detection, drones are replacing costly and hazardous manual inspections.

From 2025 onward, operators are expected to increasingly adopt fully automated workflows, including drone-in-a-box systems, remote fleet management, and AI cloud analytics. Inspection & maintenance is projected to exceed 25% of all commercial drone revenue by 2030, surpassing agriculture as the leading segment.

Delivery drones mature from trials to regional commercialization

Despite regulatory and logistical challenges, drone delivery is now gaining real commercial traction. Leading companies in the US, Europe, and China are expanding last-mile delivery for e-commerce, food, and medical transport, while mid-range logistics drones are emerging for remote and island supply routes.

Industry progress in automated loading, cold-chain drone logistics, and U-space/UTM (Unmanned Traffic Management) frameworks is paving the way for scaled operations. The long-term trajectory of delivery drones will depend heavily on BVLOS (Beyond Visual Line of Sight) approvals and national UTM deployment.

Security, military, and public safety maintain strong momentum

Government and law enforcement agencies are adopting drones for border patrol, surveillance, traffic management, crowd monitoring, and emergency response.

Hybrid fixed-wing VTOL drones enable long-endurance operations over large areas, while AI-based video analytics enhance situational awareness. Public safety is expected to remain a stable and steadily expanding segment through 2036.

Military drones remain the largest revenue contributor

The military drone sector continues to lead the total drone market in absolute revenue. Since 2022, regional conflicts have accelerated demand for reconnaissance drones, medium-range tactical drones, and loitering munitions.

Armed forces are also moving toward Manned-Unmanned Teaming (MUM-T) concepts, integrating drones with aircraft and armored vehicles. While dual-use technologies are increasingly repurposed for defense, the core military drone segment will continue to be highly profitable and strategically essential.

Disaster response continues to rely on drone capabilities

Drones equipped with thermal, optical, and acoustic sensors play a critical role in night-time search missions, earthquake rescue, wildfire monitoring, and post-disaster assessment.

Advances in multi-drone collaboration and AI-based geolocation algorithms have significantly improved operational efficiency. Though smaller in absolute revenue, this segment has strong government backing and consistent long-term growth.

Global regulations move toward harmonization and risk-based frameworks

Drone regulation is increasingly aligned around risk-based, tiered certification systems. The US (Part 107), EU (C0-C6), UK (CAP722), and China have all established clearer pathways for commercial operations, especially for BVLOS.

Common regulatory themes include

North America and the EU lead in harmonized frameworks, while Asia-Pacific, Latin America, and MENA remain more fragmented.

Sensor proliferation reshapes drone payload configurations

From 2025 to 2036, commercial drone shipments are expected to grow 2.3×, but sensor shipments grow 4×, illustrating a major shift toward higher sensor density and more advanced autonomy.

By 2036, many industrial and BVLOS drones are expected to exceed 10-15 sensors per drone, driven by:

A fully rebuilt 2026-2036 forecast from IDTechEx

This report offers a comprehensive overview of the global drone industry's progress across consumer, commercial, and defense sectors, including the regulatory constraints that shape operations and the deployment maturity in different regions. It also examines the full range of sensing and payload configurations used across major applications, from agriculture and inspection to logistics and public safety, explaining how different cost structures and mission requirements drive platform choices. Additionally, it includes a detailed list of representative commercial drone models, their technical specifications, sensor suites, pricing ranges, and market positioning, together with a fully updated 2026-2036 forecast covering revenue, unit shipments, and sensor integration trends.

IDTechEx provides a completely updated ten-year drone market forecast, including

Key Aspects

This report provides critical market intelligence about the global drone industry, covering consumer, commercial, and defense platforms and all major application sectors. This includes:

A review of the context, technology, and regulation behind drone systems

Full market characterization for each major drone application sector

Market analysis throughout

Table of Contents1. EXECUTIVE SUMMARY

1.1.1. Executive Introduction

1.1.2. Executive Introduction

1.1.3. Overview of Modern Drone Categories and Market Structure

1.2. Major Applications and Growth Trends

1.2.1. Overview of Major Application Areas

1.2.2. Case Study: Cost Composition and Value Distribution

1.2.3. Agricultural Industry: Comparison of Sensors Used in Drone Imaging

1.2.4. Agricultural Industry: Comparison of sensors used in drone imaging

1.2.5. Drone Sensor Market Trends

1.2.6. Agricultural Industry: Drones are Becoming Increasingly Autonomous

1.3. Summary of Drone Players and Models in Different Industries

1.3.1. Commercially Available Agricultural Spraying Drones

1.3.2. Commercially Available Agricultural Spraying Drones

1.3.3. Commercially Available Agricultural Crop Monitoring Drones

1.3.4. Industrial and Infrastructure Inspection (power grids, wind turbines, oil & gas pipelines)

1.3.5. Linear Asset Inspection (Power Lines, Pipelines, Railways)

1.3.6. Close-Range Precision Inspection (Infrastructure, Power, Wind Turbines)

1.3.7. Special Environments (Confined Spaces / NDT Testing)

1.3.8. Methane / Emissions Monitoring (ESG & Compliance)

1.3.9. Master Comparison of UAV-Based Methane Detection Technologies

1.3.10. Commercialization Status of Logistics and Cargo Drones by Range

1.3.11. Key Takeaways of Logistics and Cargo Delivery Drones

1.3.12. Logistics and Cargo Delivery Drones: Landscape and Maturity Assessment (1)

1.3.13. Logistics and Cargo Delivery Drones: Landscape and Maturity Assessment (2)

1.3.14. Key Takeaways of Military and Defense: Loitering Munitions

1.3.15. Military and Defense: Loitering Munitions

1.4. Forecasts

1.4.1. Commercial Drone Volume Forecasts (2026-2036)

1.4.2. Overall Drone Volume Forecasts (2026-2036)

1.4.3. Commercial Drone Revenue Forecasts (2026-2036)

1.4.4. Global Drone Market Revenue Forecast by Scenarios 2026-2036

1.4.5. Global Drone Market Revenue Forecast by Scenarios (1)

1.4.6. Global Drone Market Revenue Forecast by Scenarios (2)

1.4.7. Global Drone Market Revenue Forecast by Scenarios (3)

1.4.8. Drones Sensor Market Size Forecast (2026-2036)

1.4.9. Drones Sensor Market Size Forecast (2026-2036)

1.4.10. Drones Sensor Market Size Forecast (2026-2036)

2. INTRODUCTION

2.1. What is a Drone?

2.2. Introduction

2.3. Sensor fusion: Towards Navigational Autonomy

3. GLOBAL REGULATORY FRAMEWORK

3.1. Regulations - High Level Regulatory Requirements by Country

3.2. Global Drone Regulations

3.3. China

3.4. United States: Airspace and Pilot Licensing Framework

3.5. United States: Emerging BVLOS Regulations (1)

3.6. United States: Emerging BVLOS Regulations (2)

3.7. EU

3.8. European Union: Operational Categories and Risk-Based Oversight

3.9. UK

3.10. UK

3.11. Brazil: Drone Regulation Overview (1)

3.12. Brazil: Drone Regulation Overview (2)

4. KEY APPLICATION AREAS

4.1. Commercial Market Product

4.1.1. Drones: Application Pipeline

4.1.2. Drones: Application Pipeline (1)

4.1.3. Drones: Application Pipeline (2)

4.2. Commercial Market Product-Agricultural Drone

4.2.1. Agricultural Drone Industry Value Chain (1)

4.2.2. Agricultural Drone Industry Value Chain (2)

4.2.3. Agricultural Drone Industry Value Chain (3)

4.2.4. Agricultural Drones: Main Applications

4.2.5. Mainstream Agricultural Drone Types

4.2.6. Agricultural Spraying Drones - Pesticide and Fertilizer

4.2.7. Commercially Available Agricultural Spraying Drones

4.2.8. Commercially Available Agricultural Spraying Drones

4.2.9. Drones in Crop Monitoring and Analysis

4.2.10. Radar in Agriculture - Sarmap

4.2.11. Cranfield University - Soil Moisture Monitoring with UAV-Radar

4.2.12. Commercially Available Agricultural Crop Monitoring Drones

4.2.13. Commercially Available Agricultural Crop Monitoring Drones

4.2.14. Comparison of Sensors Used in Drone Imaging

4.2.15. Comparison of Sensors Used in Drone Imaging

4.2.16. Drones vs Satellites vs Aeroplanes

4.2.17. Where Does Drone Spraying Have Regulatory Approval?

4.2.18. EU Progress on Agri-Drone Management

4.2.19. US Progress on Agri-Drone Management

4.2.20. China Progress on Agri-Drone Management

4.2.21. Agricultural Drone Pesticide Management in Europe - ISO 23117-1:2023 / ISO 23117-2:2025 (1)

4.2.22. Agricultural Drone Pesticide Management in Europe - ISO 23117-1:2023 / ISO 23117-2:2025 (2)

4.2.23. Drones are Becoming Increasingly Autonomous

4.2.24. BVLOS Enabling Infrastructure & Technologies

4.2.25. Agricultural Drones: Company Landscape

4.2.26. Potential Software Opportunities in Agricultural Drones

4.2.27. Fruit picking drones by Tevel Aerobotics Technologies

4.2.28. CropHopper by HayBeeSee

4.2.29. Digital Monitoring in Vertical Farming

4.3. Commercial Market Product-Industrial and Infrastructure Inspection

4.3.1. Industrial and Infrastructure Inspection (Power Grids, Wind Turbines, Oil & Gas Pipelines)

4.3.2. Linear Asset Inspection (Power Lines, Pipelines, Railways)

4.3.3. Linear Asset Inspection (Power Lines, Pipelines, Railways)

4.3.4. Close-Range Precision Inspection (Infrastructure, Power, Wind Turbines)

4.3.5. Close-Range Precision Inspection (Infrastructure, Power, Wind Turbines)

4.3.6. Special Environments (Confined Spaces / NDT Testing)

4.3.7. Special Environments (Confined Spaces / NDT Testing)

4.3.8. Methane / Emissions Monitoring (ESG & Compliance)

4.3.9. Methane / Emissions Monitoring (ESG & Compliance)

4.3.10. Methane Detection Technologies - Comparison (1)

4.3.11. Methane Detection Technologies - Comparison (2)

4.3.12. Master Comparison of UAV-Based Methane Detection Technologies

4.3.13. Data Platforms & Services (AI / Digital Twin)

4.3.14. University of Exeter's Gutter Cleaning - Drones Enabled Data Collection

4.3.15. Decommissioning Nuclear Sites With UAVs - Use Case Study: Sellafield UK

4.3.16. Cranfield University - Unmanned Aerial System Concept Design for Rail Yard Monitoring

4.4. Commercial Market Product-Logistics

4.4.1. Logistics and Cargo Delivery (Last-mile, Emergency Supplies)

4.4.2. Last-Mile, Mid-Mile, and Long-Haul Drone Delivery Overview

4.4.3. Last-Mile, Mid-Mile, and Long-Haul Drone Delivery Scenarios

4.4.4. Commercialization Status of Logistics and Cargo Drones by Range

4.4.5. Commercialization Status of Logistics and Cargo Drones by Region: US

4.4.6. Commercialization Status of Logistics and Cargo Drones by Region: EU

4.4.7. Commercialization Status of Logistics and Cargo Drones by Region: China

4.4.8. Logistics and Cargo Delivery Drones: Landscape and Maturity Assessment (1)

4.4.9. Logistics and Cargo Delivery Drones: Landscape and Maturity Assessment (2)

4.4.10. Logistics and Cargo Delivery Drones: Landscape and Maturity Assessment (3)

4.4.11. FAA Part 108 BVLOS Regulations and Industry Outlook 2025 (1)

4.4.12. FAA Part 108 BVLOS Regulations and Industry Outlook 2025 (2)

4.4.13. Zipline

4.4.14. Wing (Alphabet)

4.4.15. Case Study: Wing vs Zipline - Competing Paths in Western Drone Logistics (1)

4.4.16. Case Study: Wing vs Zipline - Competing Paths in Western Drone Logistics (2)

4.4.17. Case Study: China's Drone Logistics Race - SF Express vs JD (1)

4.4.18. Case Study: China's Drone Logistics Race - SF Express vs JD (2)

4.4.19. A multi-modal Stochastic Logistics Optimiser involving land-to-UAV and UAV-to land logistics interchanges - Solent Transport

4.4.20. Drones for Medical Applications - Solent Transport

4.4.21. Windracers - OEM of Low-cost Self-flying Cargo Aircraft - Scientific Survey Missions of the Antarctic

4.5. Military Market Product

4.5.1. Military and Defense

4.5.2. Military and Defense

4.5.3. Military and Defense: Loitering Munitions

4.5.4. Military and Defense: Loitering Munitions

4.5.5. Military and Defense: Loitering Munitions

4.5.6. Military and Defense: Loitering Munitions

4.5.7. Tactical COTS-Modified UAVs

4.5.8. Tactical COTS-Modified UAVs

4.5.9. Fiber vs RF Control: Technological Divergence and Tactical FPV UAV Applications

4.5.10. SkyFall

4.5.11. BAVOVNA MILTECH

4.5.12. Drones of Ukraine

4.5.13. TechEx

4.5.14. Case Study: Mid- to Long-Range One-Way Attack Drones in the Russia-Ukraine Conflict

4.5.15. Case Study: Mid- to Long-Range One-Way Attack Drones in the Russia-Ukraine Conflict

4.6. Disaster and Rescue

4.6.1. Disaster Response and Search-and-Rescue Drones

4.6.2. Law Enforcement Use Case: Enhancing Aerial Oversight and Operational Coordination

4.6.3. ZenaDrone - Remote Aerial Surveillance Solutions

4.6.4. Fire and Disaster Response: Real-Time Aerial Intelligence in Complex and Hazardous Environments

4.6.5. Search and Rescue / Emergency Response: Accelerating Victim Location and Enabling Safer Operations

4.6.6. Thermal and Multi-Sensor Payloads

4.6.7. Thermal and Multi-Sensor Payloads

4.6.8. Mainstream Thermal Imaging Payloads for Public Safety Drones

4.6.9. Xtrafly Systems - Potential Use Cases in the Detection and Security

4.6.10. Wildfire and Smoke Early Detection (1) - Generative AI for Supplementary Training Dataset

4.6.11. Wildfire and Smoke Early Detection (2)

5. KEY TECHNOLOGIES

5.1.1. Software for Robotics Introduction

5.1.2. Different Abstraction Levels

5.1.3. Localization and Mapping, and Why Simultaneously?

5.1.4. Flight Control Systems (FCS)

5.1.5. SLAM (Simultaneous Localization and Mapping)

5.1.6. SLAM (Simultaneous Localization and Mapping)

5.1.7. Visual SLAM vs LiDAR SLAM

5.1.8. Multi Sensor SLAM

5.1.9. Exyn Technologies

5.1.10. Advantages of Different SLAM Approaches and IDTechEx Take

5.1.11. Vision Language Action (VLA) Models for Robotics

5.1.12. Progress of VLA Models

5.2. Communication and Networking

5.2.1. Communication and Networking: C2 Command and Control

5.2.2. Communication and Networking: Cellular Networks

5.2.3. Cellular Applications in Drone Operations

5.2.4. Cellular Market, Ecosystem Landscape, and Regulatory Developments

5.2.5. 5G Readiness for Drone Operations by Region

5.2.6. 5G Readiness for Drone Operations by Region - UK and EU

5.2.7. 5G Readiness for Drone Operations by Region - US

5.2.8. 5G Readiness for Drone Operations by Region - China

5.2.9. 5G Readiness for Drone Operations by Region - UAE and other Gulf countries

5.3. Swarm Control

5.3.1. Swarm Control: A Paradigm Shift Toward Cooperative, Distributed Drone Operations

5.3.2. The Value of Swarm Control: Higher Efficiency, Greater Resilience, Expanded Applications

5.3.3. The Value of Swarm Control: Higher Efficiency, Greater Resilience, Expanded Applications

5.3.4. Swarm Control Modes and Their Enabling Technologies: Leader-Follower and Multi-Group

5.3.5. Swarm Control Solution Providers: Global Landscape (1)

5.3.6. Swarm Control Solution Providers: Global Landscape (2)

5.3.7. Swarm Control Technology Readiness & Commercial Deployment Status

5.3.8. Technical Challenges and Future Outlook for UAV Swarm Control

6. SENSORS IN DRONES

6.1. Emerging Image Sensors

6.1.1. Overview of the Emerging Image Sensors Section

6.1.2. Emerging Image Sensors: Summary of Key Conclusions

6.1.3. Emerging Image Sensors: Key Players Overview (I)

6.1.4. Emerging Image Sensors: Key Players Overview (II)

6.1.5. SWIR Imaging: Overview and Key Conclusions

6.1.6. SWIR Imaging: Emerging Technology Options

6.1.7. SWIR Sensors: Applications and Key Players

6.1.8. OPD-on-CMOS Hybrid Image Sensors: Overview, Conclusions and Key Players

6.1.9. OPD-on-CMOS Detectors: Technology Readiness Level Roadmap by Application

6.1.10. QD-on-Si/QD-on-CMOS Imaging: Fundamentals, Value Proposition and Key Conclusions

6.1.11. Hyperspectral Imaging: Overview and Key Conclusions

6.1.12. Hyperspectral Imaging: Wavelength Range vs Spectral Resolution

6.1.13. Miniaturized Spectrometers: Overview and Key Conclusions

6.1.14. Miniaturized Spectrometers: Targeting a Wide Range of Sectors

6.1.15. Miniaturized Spectrometers: Key Players and Key Differentiators

6.1.16. Event-based Sensing: Overview and Key Conclusions

6.1.17. Event-based Vision: Application Requirements

6.1.18. LIDAR: Overview of Operating Principles

6.1.19. Radar and LiDAR in Robotics

6.1.20. LIDAR: Value Proposition

6.1.21. LIDAR: Ecosystem and Key Players

6.1.22. Introduction to Cameras

6.1.23. SWOT - RGB/Visible Light Camera

6.1.24. Drones as Mobile Platforms Value the Low Size and Weight of Miniaturised Gas Sensors for Industry, Agriculture and Law-enforcement

6.2. Gas Sensors

6.2.1. Overview of the Gas Sensor Section and Analyst Viewpoint

6.2.2. The Gas Sensor Market 'At a Glance'

6.2.3. Gas Sensor Market Summary: Drivers for Change?

6.2.4. Overview of Metal Oxide (MOx) Gas Sensors

6.2.5. Identifying Key MOx Sensors Manufacturers

6.2.6. Key Conclusions and SWOT Analysis of MOx Gas Sensors

6.2.7. Introduction to Electrochemical Gas Sensors

6.2.8. Major Manufacturers of Electrochemical Sensors

6.2.9. Key Conclusions and SWOT Analysis of Electrochemical Gas Sensors

6.2.10. Introduction to Infrared Gas Sensors

6.2.11. Identifying Key Infra-red Gas Sensor Manufacturers

6.2.12. Key Conclusions and SWOT Analysis of Infra-red Gas Sensors

6.2.13. Introduction to Photoionization Detectors (PID)

6.2.14. Categorization of Ionization Detector Manufacturers

6.2.15. Key Conclusions and SWOT Analysis of Photo-ionization Detectors

6.2.16. Optical Particle Counter

6.2.17. Identifying Key Optical Particle Counter Manufacturers

6.2.18. SWOT Analysis of Optical Particle Counters

6.2.19. Key Conclusions: Optical Particle Counters

6.2.20. Principle of Sensing: Photoacoustic

6.2.21. Sensirion and Infineon Offer a Miniaturized Photo-acoustic Carbon Dioxide Sensor

6.2.22. SWOT Analysis of Photo Acoustic Gas Sensors

6.2.23. Principle of Sensing: E-Nose

6.2.24. Advantages and Disadvantages of Sensor Types for E-nose

6.2.25. Categorization of E-Nose Manufacturers

6.2.26. SWOT Analysis of E-Noses

6.2.27. E-nose Summary: Specific Aromas a Better Opportunity than a Nose

6.3. Intro to AI slides

6.3.1. An Introduction to AI: Shifting Goalposts

6.3.2. Machine Learning as a Subset of Artificial Intelligence

6.3.3. Machine Learning Approaches

6.3.4. Supervised Learning

6.3.5. Unsupervised Learning

6.3.6. Problem Classes in Supervised and Unsupervised Learning

6.3.7. Reinforcement Learning

6.3.8. Semi-supervised and Active Learning

6.3.9. Neural Networks - an Introduction

6.3.10. An Artificial Neuron in the Training Process

6.3.11. Types of Neural Network

7. FORECASTS

7.1. Market Forecasts: Methodology Outline

7.2. Commercial Drone Volume Forecasts (2026-2036)

7.3. Overall Drone Volume Forecasts (2026-2036)

7.4. Commercial Drone Revenue Forecasts (2026-2036)

7.5. Global Drone Market Revenue Forecast by Scenarios 2026-2036

7.6. Global Drone Market Revenue Forecast by Scenarios (1)

7.7. Global Drone Market Revenue Forecast by Scenarios (2)

7.8. Global Drone Market Revenue Forecast by Scenarios (3)

7.9. Sensor per Drone Forecast (2026-2036)

7.10. Drones Sensor Market Size Forecast (2026-2036)

7.11. Drones Sensor Market Size Forecast (2026-2036)

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(通信・IT)の最新刊レポート

IDTechEx社の 5G, 6G, RFID, IoT分野 での最新刊レポート

関連レポート(キーワード「ドローン」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|