先進リチウムイオン電池2025-2035年:技術、プレーヤー、市場、予測Advanced Li-ion Batteries 2025-2035: Technologies, Players, Markets, Forecasts 次世代負極(シリコン、リチウム金属、金属酸化物)、先進正極材料(LMFP、Li-Mnリッチ、LNMO)、リチウム硫黄電池、固体電池 リチウムイオン電池セルの世界市場だけでも、2035年までに4,000億... もっと見る

サマリー

次世代負極(シリコン、リチウム金属、金属酸化物)、先進正極材料(LMFP、Li-Mnリッチ、LNMO)、リチウム硫黄電池、固体電池

リチウムイオン電池セルの世界市場だけでも、2035年までに4,000億米ドルを超えると予測されており、これは主にバッテリー式電気自動車と自動車の需要に牽引されている。電気自動車の普及を確実なものにし、電子機器やツールの長時間駆動と高機能化を可能にするには、電池の性能とコストの改善が必要であり、次世代リチウムイオン技術の開発競争が激化している。本レポートでは、シリコン負極、Li金属負極、正極材料(LMFP、Li-Mnリッチ、硫黄など)、合成イノベーション、固体電池の開発紹介など、先進的な次世代Liイオン電池材料と設計の詳細な分析、動向、開発状況を紹介しています。各技術分野の主要プレーヤーや新興企業の詳細が概説され、シリコン、リチウム金属、正極材料のシェアについて、対応可能な市場と予測が提供されている。

これまで民生用電子機器の需要が牽引してきたEVと定置型蓄電市場は、ますます重要性を増している。定置型エネルギー貯蔵市場では、多くの電池とエネルギー貯蔵オプションが利用可能になりつつあるが、電子機器や携帯機器、電気自動車や電気自動車に高いエネルギー密度が要求されるため、リチウムイオン電池が主要な電池化学であり続けることは確実である。しかし、依然として改良が求められている。コンシューマー機器やポータブル機器では、増加するコンピューティング・パワーに対応し、AIを活用したサービスや機器により高い機能を提供するために、より長い駆動時間とより高速な充電機能が必要とされている。潜在的な利益をもたらすEV市場では、航続距離の延長、充電時間の短縮、そしてもちろんコストと価格の低減が、普及の鍵を握っている。バッテリー電気自動車市場は、多くのバッテリー技術開発にとって重要なターゲットであり、市場の短期的な不確実性にもかかわらず、2030年までにバッテリー需要が2600GWhを超えて成長すると予測される市場に供給する機会を提供している。確かに、先進的な次世代リチウムイオン技術の開発は、さまざまな分野や、市場での成功や地位の維持を目指すバッテリー企業にとって極めて重要である。

負極

新しい負極材料は、バッテリー性能、特にエネルギー密度と急速充電能力を大幅に向上させる可能性がある。リチウムイオンに対する最もエキサイティングな材料開発の2つは、シリコン負極とリチウム金属負極の開発と採用である。この興奮は主に、これらの負極材料がエネルギー密度を大幅に向上させる可能性に起因しており、現在の最先端のリチウムイオン電池と比較して最大50%の向上が実現可能である。特にシリコン負極の開発者は、レート能力、安全性、環境プロファイル、さらにはコストの向上にも注目している。しかし、添加剤としてのシリコン酸化物の使用から高重量%への移行や、リチウム金属負極の使用は、電池のサイクル寿命と長寿命に深刻な問題を引き起こしており、これまでのところ商業的な採用が遅れ、制限されている。本レポートでは、開発中の解決策を網羅・分析し、高エネルギー負極材料と設計の商業化に着手している様々な企業を取材している。また、チタン酸リチウムやニオブ酸化物などの金属酸化物をベースとする高レート負極材料についてもカバーしている。

正極

新たな正極材料は、既存の正極材料や直接の競合材料よりも改善されることが期待されるものの、リチウムイオン電池の性能限界を大幅に押し上げる可能性は低い。その代わり、正極の開発は、ある化学物質を他の化学物質より導入する際に内在するトレードオフを最適化し、最小化するのに役立つ。材料コストとサプライチェーンの問題も、次世代正極材料の開発において重要な役割を果たす。例えば、各社は性能を最大化しコバルト依存度を低減するために、NMC正極のニッケル含有量を押し上げ続けている。LMFP正極は、同様のコストプロファイルを維持しながらLFPよりも高いエネルギー密度を提供し、Li-Mnリッチ正極はコバルトとニッケル含有量を低減しながらNMC材料と同様のエネルギー密度を提供することができる。正極活物質の代替製造方法もまた、廃棄物の発生や排出を削減し、重要な点であるコストを削減するために開発中である。IDTechExのレポートでは、様々な次世代リチウムイオン正極材料の評価を行い、それぞれの長所と短所、特定の用途や市場に提供する、あるいは提供し得る価値提案を強調している。

リチウム硫黄

リチウム硫黄電池は、インターカレーション正極を変換型硫黄に置き換え、負極を一般的にリチウム金属で構成することで、従来のリチウムイオン技術から大きく逸脱している。硫黄とリチウムは高容量かつ低密度であるため、リチウム硫黄電池を開発している企業は450Wh/kgという高い重量エネルギー密度を実証している。ニッケルやコバルトといった材料の代わりに、低コストで広く入手可能な硫黄を使用することで、コスト面やサプライ・チェーン面でのメリットも期待できる。しかし、このようなコストメリットを達成するためには、セル設計の特殊性と製造規模が極めて重要である一方、Li-S電池は一般的にサイクル寿命とレート性能が低いという問題を抱えており、商業化前に克服すべき課題が数多くあることが浮き彫りになっている。

セルと電池の設計

セルや電池パックの設計の開発も、性能の継続的な向上において同様に重要な役割を果たすことができる。セル・レベルでは、電極構造、集電体設計、電解液添加剤と配合、カーボン・ナノチューブなどの添加剤の使用が、さまざまな用途でリチウムイオン性能を最大化する上で引き続き役割を果たす。パック・レベルでは、エネルギー密度を最適化する手段として、セル・トゥ・パックの設計が電気自動車向けにますます普及しており、BYD、CATL、テスラなどのプレーヤーによって開発が進められている。より革新的なバッテリー管理システムと分析もまた、バッテリー改良の重要なルートを示しており、エネルギー密度、レート能力、寿命、安全性などの性能特性を同時に改善する数少ない方法の一つを提供している。

商業化

現在のリチウムイオン材料加工とセル製造は、アジアと中国が中心となっている。特に米国と欧州は現在、独自のバッテリー・サプライ・チェーンを開発・育成しようとしているが、価値を獲得し、国産化するための1つのルートは、技術革新と次世代技術開発をリードすることである。この点では、米国と欧州の方がやや優れている。イノベーションの代用指標として新興企業を地域別に見ると、米国が次世代技術のリーダーであることがわかる。欧州もまた、電池産業と新興企業が成長している地域であるが、大手電池メーカーや素材企業の存在感が強いため、アジアでの開発が過小評価されている可能性が高いことに留意する必要がある。本レポートは、バッテリー技術とイノベーションの様々な分野にわたる企業の関わりを網羅した企業プロファイルのセレクションで補完されている。

IDTechExのレポートは、開発・商業化されている様々な次世代リチウムイオン技術の評価を提供している。本レポートでは、シリコンとリチウム金属負極、マンガンリッチ正極、超高ニッケルNMC、LMFP、リチウム硫黄電池、最適化されたセルと電池設計など、先進的な次世代リチウムイオン電池における主要な技術進歩の多くを網羅し分析している。各技術の主要企業や新興企業に関する詳細を概説し、次世代負極および正極材料について、対応可能な市場と予測を提供している。

主な内容本レポートでは、以下の情報を提供しています:

目次

1.要旨

1.1. 2025年リチウムイオン市場の動向

1.2.先進リチウムイオン技術の要点

1.3.リチウムイオンの性能と技術年表

1.4.主要技術開発

1.5.先進リチウムイオン開発企業

1.6.電池技術-新興企業の動き

1.7.電池技術-地域別活動レベル

1.8.電池技術の新興企業-地域的活動

1.9.地域的な取り組み

1.10.電池技術の比較

1.11.一般的なセル化学による性能比較

1.12.シリコン負極は、潜在的に大きな性能上の利点をもたらす...

1.13.シリコンは大きなデメリットももたらす

1.14.シリコン負極のまとめ

1.15.シリコン負極の性能まとめ

1.16.複数の次世代シリコン負極材料設計

1.17.主要シリコン負極企業の技術と性能

1.18.シリコン負極からの材料開発機会

1.19.リチウム金属負極

1.20.リチウム金属電池開発企業

1.21.金属酸化物負極

1.22.負極材料の比較

1.23.固体電池について

1.24.固体電解質システムの比較

1.25.各社のSSB技術概要

1.26.正極開発のまとめ

1.27.高ニッケル・超高ニッケルNMCの利点

1.28.高ニッケルCAM安定化

1.29.LMR-NMC / Li-Mnリッチのコストプロファイル

1.30.LMFPの比較

1.31.先進カソード化学の比較

1.32.代替正極合成ルート

1.33.先進カソード技術へのプレーヤーの関与

1.34.リチウムSの性能比較

1.35.リチウム硫黄コストの比較

1.36.Li-Sプレーヤー

1.37.セルと電池の設計

1.38.技術準備レベルのスナップショット

1.39.新しい電池技術の商業化におけるリスクと課題

1.40.新しい電池技術の商業化におけるリスクと課題

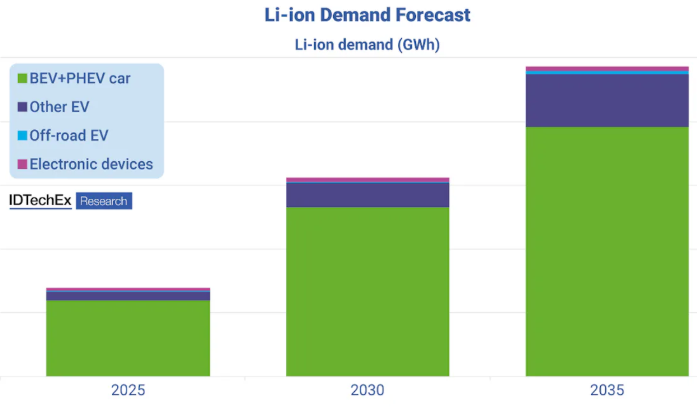

1.41.BEV正極の予測(GWh)

1.42.BEV負極の予測(GWh)

1.43.先進負極の予測(GWh)

1.44.先進負極の予測(kt, US$B)

2.序論

2.1.先進リチウムイオン電池の範囲の定義

2.2.リチウムイオン市場の動向

2.3.リチウムイオン電池とは

2.4.リチウムイオン正極材料 - LCOとLFP

2.5.リチウムイオン正極材料 - NMC、NCA、LMO

2.6.リチウムイオン負極材-黒鉛、LTO

2.7.リチウムイオン負極材料 - シリコン、リチウム金属

2.8.リチウムイオン電解質

2.9.リチウムイオンバリューチェーン(米ドル)

3.負極

3.1.はじめに

3.1.1.負極によるリチウム電池の種類

3.1.2.負極材料の考察

3.1.3.負極材料の考察

3.1.4.負極材料の長所と短所

3.1.5.リチウムイオン負極材料の比較

3.1.6.シリコン負極の技術と性能

3.1.7.シリコン負極市場

3.1.8.シリコン負極メーカーのプロフィール例

3.2.リチウム金属負極

3.2.1.序論

3.2.2.固体電池とリチウム金属負極

3.2.3.固体電解質なしでリチウムメタルを可能にする

3.2.4.リチウム金属負極は電池のエネルギー密度を高めることができる

3.2.5.リチウム金属電池開発者

3.2.6.SES

3.2.7.SES技術

3.2.8.SESセルの性能

3.2.9.Sion Power

3.2.10.Sion Powerの技術

3.2.11.リチウムメタルの用途

3.2.12.薄くて安いリチウム箔の必要性

3.2.13.リチウムメタルコーポレーション

3.2.14.ピュアリチウムコーポレーション

3.2.15.ピュアリチウムのLi箔電極生産

3.2.16.Liメタル負極のリチウム需要への影響

3.2.17.無負極セル設計

3.2.18.アノードレス・リチウムメタル電池の利点

3.2.19.アノードレス・リチウムメタル電池開発者

3.2.20.ハイブリッド電池は負極レスを可能にするかもしれない

3.2.21.高エネルギーLiイオン負極技術の概要

3.2.22.タイムライン例

3.2.23.リチウム金属負極のまとめ

3.3.金属酸化物負極

3.3.1.チタン酸リチウム酸化物(LTO)の紹介

3.3.2.LTOはどこで活躍するのか

3.3.3.LTOとグラファイトの比較

3.3.4.商用LTOの比較

3.3.5.金属酸化物アノード

3.3.6.チタン酸リチウムからニオブチタン酸化物

3.3.7.ニオブベースのアノード - Nyobolt

3.3.8.エキオン・テクノロジーズ

3.3.9.酸化バナジウム陽極 - タイファスト

3.3.10.LTO、ニオブ、バナジウム系アノードの概要

4.カソード

4.1.はじめに

4.1.1.正極の紹介

4.1.2.正極技術の要旨

4.1.3.先進正極の展望

4.1.4.リチウムイオン正極の概要

4.2.高・超高ニッケルNMC

4.2.1.高ニッケル層状酸化物の定義と命名法

4.2.2.高ニッケル・超高ニッケルNMCの利点

4.2.3.高ニッケル/ニッケルリッチ・サイクル寿命と安定性の問題

4.2.4.高ニッケル層状酸化物の主要課題

4.2.5.高ニッケルカソード安定化への道

4.2.6.高ニッケルカソードへの道

4.2.7.単結晶カソード

4.2.8.単結晶の性能

4.2.9.SM研単結晶カソード

4.2.10.高ニッケルCAM安定化

4.2.11.ユミコア

4.2.12.エコプロBM

4.2.13.SVolt

4.2.14.高ニッケル製品

4.2.15.超高ニッケル正極のタイムライン

4.2.16.高ニッケルの展望-解説

4.3.ゼロコバルトNMx

4.3.1.ゼロコバルトNMx

4.3.2.NMAカソード

4.3.3.高ニッケルNMA

4.3.4.超高ニッケル・ゼロコバルト正極

4.3.5.中Ni電圧の延長

4.3.6.高電圧NMC運転の影響

4.3.7.高電圧動作の影響

4.4.リチウムマンガンリッチ(Li-Mn-Rich, LMR-NMC)

4.4.1.リチウムマンガンリッチ、過リチウム化、LMR-NMCカソード

4.4.2.LMR-NMCカソードの概要

4.4.3.リチウムとマンガンリッチの安定化

4.4.4.LMR-NMCのエネルギー密度

4.4.5.Li-Mnリッチ/リチウムマンガンリッチ/LMR-NMCのコストプロファイル

4.4.6.商業用リチウムマンガンリッチ正極の開発

4.4.7.リチウムマンガンリッチ LXMO

4.4.8.ストラタス社による安全性強化の報告

4.4.9.CAMX Power社が高Mnカソードを実証

4.4.10.ユミコアのMnリッチ高リチウムマンガン正極

4.4.11.マンガンリッチのハイブリッド電池化学設計

4.4.12.リチウムマンガンリッチ正極開発者

4.4.13.リチウムマンガンリッチ正極のSWOT

4.5.LNMO

4.5.1.高電圧スピネル正極LNMO

4.5.2.LNMOの開発

4.5.3.LNMOの性能例

4.5.4.LNMOエネルギー密度の比較

4.5.5.LNMOの材料強度

4.5.6.正極化学がリチウム消費に与える影響

4.5.7.LNMOのコストへの影響

4.5.8.LNMO正極のSWOT

4.6.LMFP

4.6.1.LMFP正極材料の紹介

4.6.2.LMFP市場の現状

4.6.3.リン酸マンガン鉄リチウム(LMFP)の特性

4.6.4.LMFPの比較

4.6.5.LMFP のエネルギー密度分析

4.6.6.LMFP のコスト分析

4.6.7.LMFP の性能特性

4.6.8.Saftリン酸塩系カソード

4.6.9.Saftの次世代製品

4.6.10.Mitra Chem、米国でのL(M)FP生産を開発

4.6.11.ミトラケムのLMFP開発

4.6.12.LMFPのレート能力は潜在的な問題

4.6.13.HCMのLMFP性能

4.6.14.HCMブレンドNMC/LMFPセル

4.6.15.LFMPバッテリーの性能

4.6.16.報告されているLMFPセルの性能

4.6.17.LFMP電池の性能

4.6.18.LMFP正極のSWOT

4.7.LMFPの市場展望

4.7.1.LMFPの商業開発

4.7.2.LMFP正極開発企業

4.7.3.LMFP性能の見通し

4.7.4.LMFPの展望

4.8.硫黄

4.8.1.リチウム硫黄の要旨

4.8.2.リチウム硫黄(Li-S)電池の概要

4.8.3.リチウム電池の種類

4.8.4.リチウム硫黄電池の作動原理

4.8.5.リチウム硫黄電池の利点

4.8.6.リチウムSの利点と使用例

4.8.7.リチウム硫黄の課題

4.8.8.多硫化物の溶解

4.8.9.リチウム硫黄の課題 - 硫黄の利用不足と過剰電解液

4.8.10.エネルギー密度の議論

4.8.11.商業的Li-Sに対する工学的課題

4.8.12.リチウムSの課題に対する解決策

4.8.13.リチウムSのエネルギー密度とコストのモデル化

4.8.14.Li-Sのエネルギー密度のモデル化

4.8.15.Li-S性能の比較

4.8.16.Li-S性能特性の比較

4.8.17.リチウムSのコスト構造

4.8.18.リチウム硫黄材料の組成

4.8.19.リチウム-硫黄材料の原単位と組成

4.8.20.リチウムS電池のリチウム強度

4.8.21.リチウム硫黄のコスト構造

4.8.22.リチウム硫黄のコスト

4.8.23.リチウムS電池の価値提案

4.8.24.バリューチェーンと対象市場

4.8.25.リチウム硫黄電池にはどのような市場があるのか?

4.8.26.リチウム硫黄の学術活動

4.8.27.最近のリチウム硫黄の学術的ハイライト

4.8.28.リチウム硫黄についてのまとめ

4.9.企業

4.9.1.最近のLi-S開発

4.9.2.Li-Sプレーヤー

4.9.3.リチウム硫黄のプレーヤー

4.9.4.リチウム硫黄の商業化

4.9.5.ライテン - 背景

4.9.6.ライテン - 技術

4.9.7.ライテン - 製造

4.9.8.ゼータ・エナジー

4.9.9.ジェリオン

4.9.10.リエスエナジー

4.9.11.コヒーレント社

4.9.12.ネクステック

4.9.13.ポリマー硫黄カソード

4.9.14.白金族金属の使用

4.9.15. theion

4.9.16.Oxis Energy - ケーススタディ

4.9.17.オキシス・エナジー - 電池性能

4.10.代替正極製造ルート

4.10.1.はじめに

4.10.2.正極製造コスト削減の機会

4.10.3.代替正極合成ルート

4.10.4.従来のNMC合成

4.10.5.従来のLFP合成

4.10.6.乾式正極合成

4.10.7.代替合成ルート

4.10.8. 6K Inc

4.10.9.6Kエナジーテクノロジー

4.10.10.ナノワン

4.10.11.ナノワン材料技術

4.10.12.シルバテックス

4.10.13.ノボニックス

4.10.14.ノボニックス正極技術

4.10.15.HiTナノ

4.10.16.HiTナノテクノロジー

4.10.17.ゼリオン

4.10.18.Xerionカソード

4.10.19. eJouleの背景

4.10.20.テスラCAMの生産計画

4.10.21.カソード合成の環境影響

4.10.22.代替カソード生産企業

4.10.23.新しいカソード合成の展望

4.10.24.リサイクル正極

4.10.25.正極リサイクル開発

4.10.26.リサイクルCAM

4.11.結論

4.11.1.正極開発の結論

4.11.2.正極化学がリチウム消費に与える影響

4.11.3.主要正極材料開発の概要

4.11.4.正極の将来展望

4.11.5.将来の正極技術概要

4.11.6.正極の比較

4.11.7.正極の比較

4.11.8.プレーヤーの先進正極技術

4.11.9.先進正極材プレーヤー

4.11.10.正極材の対応可能市場

5.固体電池

5.1.固体電池開発の現状

5.2.固体電池に関するエグゼクティブサマリー

5.3.固体電池の紹介

5.4.固体電解質の分類

5.5.固体電解質システムの比較

5.6.固体電解質の技術アプローチ

5.7.固体電解質の特徴の分析

5.8.固体電解質技術のまとめ

5.9.現在の電解質の課題と解決策

5.10.固体電解質材料の比較

5.11.SSB企業の商業計画

5.12.自動車OEMによる固体電池の共同開発/投資

5.13.主要固体電池企業の所在地

5.14.各社の技術概要

5.15.シリコン負極と固体電池

5.16.シリコン負極を使ったSSB - Solid Power

5.17.シリコン負極を使ったSSBの性能

5.18.ブルーカレント

5.19.WeLion半固体電池の特許事例(1)

5.20.WeLion半固体電池特許ケーススタディ(2)

5.21.SSB用パックの考察

6.セルと電池の設計

6.1.セル設計と不活性材料

6.1.1.4680タブレスセル

6.1.2.セルの大型化

6.1.3.バイポーラセル設計

6.1.4.厚いフォーマットの電極

6.1.5.厚型電極 - 24m

6.1.6.二重電解質リチウムイオン

6.1.7.多層電極 - EnPower

6.1.8.多層電極設計のインパクト

6.1.9.プリエトの3Dセル設計(1/2)

6.1.10.プリエトの3Dセル設計(2/2)

6.1.11.アディオニクスの3D集電体

6.1.12.電解液の分解

6.1.13.電解質添加剤 1

6.1.14.電解質添加剤 2

6.1.15.電解質添加剤 3

6.1.16.電解質の開発

6.1.17.電解質特許トピックの比較-主要電池メーカー

6.1.18.電解質特許トピックの比較-主要電解質プレーヤー

6.1.19.リチウムイオンにおけるカーボンナノチューブ

6.1.20.主要サプライチェーン関係

6.1.21.リチウムイオン電極におけるCNT使用の影響を示す結果

6.1.22.LFP電池におけるSWCNTの改善を示す結果

6.1.23.高Cレートでの性能向上

6.1.24.エネルギー貯蔵における分散の意義

6.1.25.リチウムイオン用グラフェンコーティング

6.2.進化するセル性能

6.2.1.正極別のエネルギー密度

6.2.2.BEVセルのエネルギー密度トレンド

6.2.3.セルエネルギー密度のトレンド

6.2.4.セル性能仕様例

6.2.5.セル仕様(2022~2030年)

6.2.6.市販セル化学物質の比較

6.3.電池パックとBMS

6.3.1.セル・ツー・パックとは

6.3.2.セル・ツー・パックかモジュールか

6.3.3.セル・トゥ・パックの推進要因と課題

6.3.4.セル・ツー・シャーシ/ボディとは

6.3.5.BYD Bladeバッテリー

6.3.6.CATL セル・ツー・パック

6.3.7.セル・ツー・パックとセル・ツー・ボディの設計概要

6.3.8.重量エネルギー密度とセル対パック比

6.3.9.体積エネルギー密度とセル対パック比

6.3.10.セル・ツー・パック設計とセル・ツー・ボディ設計の展望

6.3.11.バイポーラ電池

6.3.12.バイポーラ対応CTP

6.3.13.プロロジウム「MAB」EVバッテリーパックアセンブリ

6.3.14.電気自動車用ハイブリッドバッテリーパック

6.3.15.CATLハイブリッド・リチウムイオンおよびNaイオン・パックのコンセプト

6.3.16.CATLハイブリッド・パックの設計

6.3.17.次のエネルギー

6.3.18.高エネルギー+高サイクル寿命

6.3.19.ニオのデュアルケミストリー電池

6.3.20.熱性能を向上させるNioの設計

6.3.21.Nioハイブリッド・バッテリーの動作

6.3.22.ハイブリッド電池+スーパーキャパシター

6.3.23.ハイブリッド・バッテリーのまとめ

6.3.24.BMSの導入

6.3.25.BMSの機能

6.3.26.BMS開発による電池性能の向上

6.3.27.BMSの革新

6.3.28.高度なBMS活動

6.3.29.急速充電の影響

6.3.30.急速充電プロトコル

6.3.31.急速充電用BMSソリューション

6.3.32.ワイヤレスBMSの開発

6.3.33.ワイヤレスBMSの長所と短所

6.3.34.BMS開発のまとめ

7.予測

7.1.対応可能な総市場

7.2.技術別対応可能市場

7.3.電気・電子機器の出力範囲

7.4.対応可能市場-電気自動車タイプ

7.5.機器の部品表におけるリチウムイオン電池の寄与

7.6.新技術参入の例

7.7.アプリケーション電池性能の優先順位

7.8.総アドレス可能市場(GWh)

7.9.総需要予測データ(GWh)

7.10.BEV車用正極の予測(GWh)

7.11.BEVカソード予測(GWh)

7.12.EV用正極予測(GWh)

7.13.シリコン負極の予測方法

7.14.BEV負極予測(GWh)

7.15.BEV負極予測(kt, US$B)

7.16.EV用負極の予測(GWh)

7.17.オンロードEV負極予測(GWh)

7.18.オフロードEV

7.19.コンシューマーデバイス用負極の予測(GWh)

7.20.先進負極の予測(GWh, kt, US$B)

7.21.先進陽極材の予測(GWh)

7.22.先進陽極材の予測(kt, US$B)

8.企業プロファイル

8.1.6K エネルギー

8.2.Addionics

8.3.Addionics:機械学習手法の利用

8.4.北京 WeLion 新エネルギー技術

8.5.ブルー・ソリューションズ

8.6.CAMX Power:新しい正極プラットフォーム

8.7.CENSマテリアル

8.8.コアシェル

8.9.大樹電子材料

8.10.イーマジー

8.11.イートロンテクノロジーズ

8.12.エノビックス

8.13.フォージナノ

8.14.GDI

8.15.グループ14テクノロジーズ

8.16.HiT Nano

8.17.IBU-tec Advanced Materials AG

8.18.イオンブロックス

8.19.イオントラ

8.20.ライデンジャー・テクノロジーズ

8.21.ライテンリチウム硫黄の開発

8.22.ナノラミック・ラボラトリーズ

8.23.ネクセオン

8.24.NIO(バッテリー)

8.25.ノボニクス

8.26.ワンディー・バッテリー・サイエンシズ

8.27.アワ・ネクスト・エナジー(ONE)

8.28.上海普泰来

8.29.深圳ダイナノニック

8.30.シコナ・バッテリー

8.31.シラ・ナノテクノロジーズ

8.32.サウス・エイト・テクノロジーズ

8.33.ストアドット電池開発AI

8.34.ストラタス・マテリアルズ

8.35.シルバテックス

8.36:結晶ウエハーを用いたリチウム硫黄電池の開発

8.37.WAEテクノロジーズ

8.38.Xerion Advanced Battery Corp.

Summary

Next Generation Anodes (silicon, lithium metal, metal oxides), Advanced Cathode Materials (LMFP, Li-Mn-rich, LNMO), Lithium-Sulfur and Solid-state Batteries

The global market for Li-ion battery cells alone is forecast to exceed US$400 billion by 2035, driven primarily by demand for battery electric cars and vehicles. Improvements to battery performance and cost are required to ensure widespread deployment of electric vehicles and to enable longer runtime and functionality of electronic devices and tools, leading to strong competition in the development of next-generation Li-ion technologies. This report provides in-depth analysis, trends and developments in advanced and next-generation Li-ion cell materials and designs, including silicon anodes, Li-metal anodes, cathode material (e.g. LMFP, Li-Mn-rich, sulfur) and synthesis innovations, and an introduction to solid-state battery developments, amongst other areas of development. Details of the key players and start-ups in each technology space are outlined and addressable markets and forecasts are provided for silicon, Li-metal, and cathode material shares.

Historically driven by demand for consumer electronic devices, the EV and stationary storage markets have become increasingly important. While numerous battery and energy storage options are becoming available for the stationary energy storage market, the high energy density requirements of electronic and portable devices, and electric cars and vehicles, ensures that Li-ion batteries will remain the dominant battery chemistry. However, improvements are still sought after. For consumer and portable devices, longer run-times and faster charging capabilities are needed to keep up with increasing computing power and to offer greater functionality in the wake of AI enabled services and devices. For the potentially lucrative EV market, longer ranges, shorter charging times, and of course lower costs and prices are still key to widespread adoption. The battery electric car market is a key target for many battery technology developments, offering the opportunity to supply a market where battery demand is forecast to grow beyond 2600 GWh by 2030, despite short-term uncertainties in the market. Certainly, the development of advanced and next-generation Li-ion technologies will be critical to various sectors, as well as for battery companies aiming to succeed or maintain their place in the market.

Anodes

New anode materials offer the chance of significantly improved battery performance, particularly energy density and fast charge capability. Two of the most exciting material developments to Li-ion are the development and adoption of silicon anodes and Li-metal anodes, the latter often but not always in conjunction with solid-electrolytes. The excitement stems primarily from the possibility of these anode materials significantly improving energy density, where improvements of up to 50% over current state-of-the-art Li-ion cells are feasible. Enhancements to rate capability, safety, environmental profile, and even cost, are also being highlighted by silicon anode developers in particular. However, shifting from the use of silicon oxides as an additive to higher weight percentages, and the use of lithium-metal anodes have posed serious problems to battery cycle life and longevity, which has delayed and limited commercial adoption so far. This report covers and analyzes the solutions being developed and provides coverage of the various companies starting to commercialise their high energy anode materials and designs. The report also provides coverage of high-rate anode materials based on metal oxides such as lithium titanate and niobium oxides.

Cathodes

While new cathode materials are expected to provide improvements over incumbents and direct competitors, they are unlikely to push the performance envelope of Li-ion batteries significantly. Instead, cathode development can help to optimise and minimise the trade-off inherent in deploying one chemistry over another. Material costs and supply chain concerns also play a critical role in the development of next-generation cathodes materials. For example, companies continue to push nickel content in NMC cathodes to maximise performance and reduce cobalt reliance, LMFP cathodes offer a higher energy density than LFP whilst maintaining a similar cost profile, while Li-Mn-rich cathodes can provide similar energy densities to NMC materials whilst reducing cobalt and nickel content. Alternative methods of producing cathode active materials are also under development to reduce waste production, emissions and importantly, costs. IDTechEx's report provides an appraisal of the various next-generation Li-ion cathode materials, highlighting their respective strengths and weaknesses and the value proposition they offer, or could offer, to specific applications and markets.

Lithium-sulfur

Lithium-sulfur batteries represent a greater departure from conventional Li-ion technology with the intercalation cathode replaced with conversion-type sulfur and with the anode typically comprising lithium-metal. The high capacity and low density of sulfur, and lithium, means companies developing Li-S batteries have demonstrated gravimetric energy densities as high as 450 Wh/kg - approximately 50% higher than state-of-the-art Li-ion. The use of low-cost and widely available sulfur, in place of materials such as nickel and cobalt, also offers the potential for cost and supply chain benefits. However, cell-design specifics and manufacturing scale are critical for achieving these cost benefits, while Li-S batteries typically suffer from poor cycle life and rate capability, highlighting a number of challenges that need to be overcome prior to commercialization.

Cell and battery design

Developments to cell and battery pack design can play a similarly important role in ongoing performance gains. At the cell level, electrode structure, current collector design, electrolyte additives and formulations, and the use of additives such as carbon nanotubes will continue to play a role in maximising Li-ion performance across various applications. At the pack level, cell-to-pack designs are becoming increasingly popular for electric cars as a means to optimise energy density and are being developed by players such as BYD, CATL, and Tesla, amongst others. More innovative battery management systems and analytics also represents a key route to battery improvement, offering one of only a few ways to improve performance characteristics including energy density, rate capability, lifetime, and safety simultaneously - a feat that is notoriously difficult to achieve.

Commercialization

Current Li-ion materials processing and cell manufacturing is dominated by Asia and China. While the US and Europe in particular are now looking to develop and nurture their own battery supply chains, one route to capturing and domesticating value could be to lead the way in innovation and next-generation technology development. Here, the US and Europe fare slightly better. Looking at start-up companies by geography, as a proxy for innovation, and the US comes out as a leader in next generation technology. Europe is also home to a growing battery industry and start-up landscape, though it needs to be noted that development in Asia is likely under-represented given the stronger presence of major battery manufacturers and materials companies. The report is complemented with a selection of company profiles covering company involvement across various areas of battery technology and innovation.

IDTechEx's report provides an appraisal of the various next-generation Li-ion technologies being developed and commercialised. This report covers and analyzes many of the key technological advancements in advanced and next-generation Li-ion batteries, including silicon and lithium-metal anodes, manganese-rich cathodes, ultra-high nickel NMC, LMFP, lithium-sulfur batteries, as well as optimised cell and battery designs. Details on the key players and start-ups in each technology are outlined and addressable markets and forecasts are provided for next-generation anode and cathode materials.

Key aspectsThis report provides the following information:

Table of Contents1. EXECUTIVE SUMMARY

1.1. 2025 trends in the Li-ion market

1.2. Advanced Li-ion technology key takeaways

1.3. Li-ion performance and technology timeline

1.4. Key technology developments

1.5. Advanced Li-ion developers

1.6. Battery technologies - start-up activity

1.7. Battery technologies - level of regional activity

1.8. Battery technology start-ups - regional activity

1.9. Regional efforts

1.10. Battery technology comparison

1.11. Performance comparison by popular cell chemistries

1.12. Silicon Anodes Offer Potentially Significant Performance Benefits...

1.13. Silicon Also Presents Significant Disadvantages

1.14. Silicon anode summary

1.15. Si-anode performance summary

1.16. Multiple next-gen silicon anode material designs

1.17. Key silicon-anode company technologies and performance

1.18. Material opportunities from silicon anodes

1.19. Li-metal anodes

1.20. Li-metal battery developers

1.21. Metal oxide anodes

1.22. Anode materials comparison

1.23. Remarks on solid-state batteries

1.24. Comparison of solid-state electrolyte systems

1.25. SSB technology summary of various companies

1.26. Cathode development summary

1.27. Benefits of high and ultra-high nickel NMC

1.28. High-nickel CAM stabilisation

1.29. LMR-NMC / Li-Mn-rich cost profile

1.30. LMFP comparison

1.31. Advanced cathode chemistry comparison

1.32. Alternative cathode synthesis routes

1.33. Player involvement in advanced cathode technologies

1.34. Li-S performance compared

1.35. Lithium-sulfur cost comparison

1.36. Li-S players

1.37. Cell and battery design

1.38. Technology readiness level snapshot

1.39. Risks and challenges in new battery technology commercialisation

1.40. Risks and challenges in new battery technology commercialisation

1.41. BEV cathode forecast (GWh)

1.42. BEV anode forecast (GWh)

1.43. Advanced anode forecast (GWh)

1.44. Advanced anode forecast (kt, US$B)

2. INTRODUCTION

2.1. Defining the scope of advanced Li-ion batteries

2.2. Trends in the Li-ion market

2.3. What is a Li-ion battery?

2.4. Li-ion cathode materials - LCO and LFP

2.5. Li-ion cathode materials - NMC, NCA and LMO

2.6. Li-ion anode materials - graphite and LTO

2.7. Li-ion anode materials - silicon and lithium metal

2.8. Li-ion electrolytes

2.9. Li-ion value chain (US$)

3. ANODES3.1. Introduction

3.1.1. Types of lithium battery by anode

3.1.2. Anode materials discussion

3.1.3. Anode materials discussion

3.1.4. Strengths and weaknesses of anode materials

3.1.5. Li-ion anode materials compared

3.1.6. Silicon Anode Technology and Performance

3.1.7. Silicon Anode Market

3.1.8. Silicon Anode Player Profile Examples

3.2. Lithium-Metal Anodes

3.2.1. Introduction

3.2.2. Solid-state batteries and lithium metal anodes

3.2.3. Enabling Li-metal without solid-electrolytes

3.2.4. Li-metal anodes can increase battery energy density

3.2.5. Li-metal battery developers

3.2.6. SES

3.2.7. SES technology

3.2.8. SES cell performance

3.2.9. Sion Power

3.2.10. Sion Power technology

3.2.11. Applications for Li-metal

3.2.12. The need for thin and cheap lithium foils

3.2.13. Li-metal corp

3.2.14. Pure Lithium Corporation

3.2.15. Pure Lithium's Li-foil electrode production

3.2.16. Impact of Li-metal anodes on lithium demand

3.2.17. Anode-less cell design

3.2.18. Anode-less lithium-metal cell benefits

3.2.19. Anode-less lithium-metal cell developers

3.2.20. Hybrid batteries could enable anode-free use

3.2.21. High energy Li-ion anode technology overview

3.2.22. Example timelines

3.2.23. Concluding remarks on Li-metal anodes

3.3. Metal Oxide Anodes

3.3.1. Introduction to lithium titanate oxide (LTO)

3.3.2. Where will LTO play a role?

3.3.3. Comparing LTO and graphite

3.3.4. Commercial LTO comparisons

3.3.5. Metal oxide anodes

3.3.6. Lithium titanate to niobium titanium oxide

3.3.7. Niobium based anodes - Nyobolt

3.3.8. Echion Technologies

3.3.9. Vanadium oxide anodes - TyFast

3.3.10. Overview of LTO, niobium and vanadium based anodes

4. CATHODES4.1. Introduction

4.1.1. Cathode introduction

4.1.2. Cathode technology executive summary

4.1.3. Advanced cathode outlook

4.1.4. Overview of Li-ion cathodes

4.2. High and Ultra-High Nickel NMC

4.2.1. High-nickel layered oxides definition and nomenclature

4.2.2. Benefits of high and ultra-high nickel NMC

4.2.3. High-Ni / Ni-rich cycle life and stability issues

4.2.4. Key issues with high-nickel layered oxides

4.2.5. Routes to high nickel cathode stabilisation

4.2.6. Routes to high-nickel cathodes

4.2.7. Single crystal cathodes

4.2.8. Single crystal performance

4.2.9. SM Lab single crystal cathodes

4.2.10. High-nickel CAM stabilisation

4.2.11. Umicore

4.2.12. EcoPro BM

4.2.13. SVolt

4.2.14. High-nickel products

4.2.15. Ultra-high nickel cathode timelines

4.2.16. Outlook on high-Ni - commentary

4.3. Zero-Cobalt NMx

4.3.1. Zero-cobalt NMx

4.3.2. NMA cathode

4.3.3. High-nickel NMA

4.3.4. Ultra-high nickel, zero-cobalt cathode

4.3.5. Extending mid-Ni voltage

4.3.6. Impact of high-voltage NMC operation

4.3.7. Impact of high-voltage operation

4.4. Lithium-Manganese-Rich (Li-Mn-Rich, LMR-NMC)

4.4.1. Lithium-manganese-rich, over-lithiated, LMR-NMC cathodes

4.4.2. Overview of Li-Mn-rich cathodes LMR-NMC

4.4.3. Stabilising lithium and manganese-rich

4.4.4. LMR-NMC energy density

4.4.5. Li-Mn-rich / lithium-manganese-rich / LMR-NMC cost profile

4.4.6. Commercial lithium-manganese-rich cathode development

4.4.7. Lithium-manganese-rich LXMO

4.4.8. Safety enhancements reported by Stratus

4.4.9. CAMX Power demonstrate high-Mn cathode

4.4.10. Umicore Mn-rich high-lithium-manganese cathode

4.4.11. Hybrid battery chemistry design for manganese-rich

4.4.12. Lithium-manganese-rich cathode developers

4.4.13. Lithium-manganese-rich cathode SWOT

4.5. LNMO

4.5.1. High-voltage spinel cathode LNMO

4.5.2. LNMO development

4.5.3. LNMO performance examples

4.5.4. LNMO energy density comparison

4.5.5. LNMO material intensity

4.5.6. Cathode chemistry impact on lithium consumption

4.5.7. LNMO cost impact

4.5.8. LNMO cathode SWOT

4.6. LMFP

4.6.1. Introduction to LMFP cathode material

4.6.2. Status of the LMFP market

4.6.3. Lithium manganese iron phosphate (LMFP) characteristics

4.6.4. LMFP comparison

4.6.5. LMFP energy density analysis

4.6.6. LMFP cost analysis

4.6.7. LMFP performance characteristics

4.6.8. Saft phosphate-based cathodes

4.6.9. Saft next generation products

4.6.10. Mitra Chem developing US-based L(M)FP production

4.6.11. Mitra Chem LMFP development

4.6.12. LMFP rate capability a potential issue

4.6.13. HCM's LMFP performance

4.6.14. HCM blended NMC/LMFP cells

4.6.15. LFMP battery performance

4.6.16. Reported LMFP cell performance

4.6.17. LFMP battery performance

4.6.18. LMFP cathode SWOT

4.7. LMFP Market Landscape

4.7.1. LMFP commercial development

4.7.2. LMFP cathode developers

4.7.3. LMFP performance outlook

4.7.4. LMFP outlook

4.8. Sulfur

4.8.1. Li-S executive summary

4.8.2. Introduction to lithium-sulfur (Li-S) batteries

4.8.3. Types of lithium battery

4.8.4. Operating principle of Li-S

4.8.5. Lithium-sulfur batteries - advantages

4.8.6. Li-S advantages and use cases

4.8.7. Challenges with lithium-sulfur

4.8.8. Polysulphide dissolution

4.8.9. Li-S challenges - poor sulfur utilisation and excess electrolyte

4.8.10. Energy density discussion

4.8.11. Engineering challenges to commercial Li-S

4.8.12. Solutions to Li-S challenges

4.8.13. Modelling Li-S energy density and cost

4.8.14. Modelling Li-S energy density

4.8.15. Li-S performance compared

4.8.16. Li-S performance characteristics compared

4.8.17. Li-S cost structure

4.8.18. Lithium-sulfur material composition

4.8.19. Lithium-sulfur material intensity and composition

4.8.20. Lithium intensity of Li-S batteries

4.8.21. Lithium-sulfur cost structure

4.8.22. Lithium-sulfur cost

4.8.23. Value proposition of Li-S batteries

4.8.24. Value chain and targeted markets

4.8.25. What markets exist for lithium sulfur batteries?

4.8.26. Academic lithium-sulfur activity

4.8.27. Recent Li-S academic highlights

4.8.28. Concluding remarks on Li-S

4.9. Companies

4.9.1. Recent Li-S developments

4.9.2. Li-S players

4.9.3. Lithium-sulfur players

4.9.4. Li-sulfur commercialisation

4.9.5. Lyten - background

4.9.6. Lyten - technology

4.9.7. Lyten - manufacturing

4.9.8. Zeta Energy

4.9.9. Gelion

4.9.10. Li-S Energy

4.9.11. Coherent Inc

4.9.12. NexTech

4.9.13. Polymer sulfur cathodes

4.9.14. Use of platinum group metals

4.9.15. theion

4.9.16. Oxis Energy - case study

4.9.17. Oxis Energy - battery performance

4.10. Alternative Cathode Production Routes

4.10.1. Introduction

4.10.2. Cathode production cost reduction opportunity

4.10.3. Alternative cathode synthesis routes

4.10.4. Conventional NMC synthesis

4.10.5. Conventional LFP synthesis

4.10.6. Dry cathode synthesis

4.10.7. Alternative synthesis routes

4.10.8. 6K Inc

4.10.9. 6K Energy technology

4.10.10. Nano One

4.10.11. Nano One Materials technology

4.10.12. Sylvatex

4.10.13. Novonix

4.10.14. Novonix cathode technology

4.10.15. HiT Nano

4.10.16. HiT Nano technology

4.10.17. Xerion

4.10.18. Xerion cathode

4.10.19. eJoule background

4.10.20. Tesla CAM production plans

4.10.21. Cathode synthesis environmental impact

4.10.22. Alternative cathode production companies

4.10.23. New cathode synthesis outlook

4.10.24. Recycled cathodes

4.10.25. Cathode recycling developments

4.10.26. Recycled CAM

4.11. Conclusions

4.11.1. Concluding remarks on cathode development

4.11.2. Cathode chemistry impact on lithium consumption

4.11.3. Key cathode material developments overview

4.11.4. Future cathode prospects

4.11.5. Future cathode technology overview

4.11.6. Cathode comparisons

4.11.7. Cathode comparisons

4.11.8. Player advanced cathode technologies

4.11.9. Advanced cathode material players

4.11.10. Cathode material addressable markets

5. SOLID-STATE BATTERIES

5.1. State of SSB development

5.2. Executive summary on solid-state batteries

5.3. Introduction to solid-state batteries

5.4. Classifications of solid-state electrolyte

5.5. Comparison of solid-state electrolyte systems

5.6. Solid-state electrolyte technology approach

5.7. Analysis of SSB features

5.8. Summary of solid-state electrolyte technology

5.9. Current electrolyte challenges and solutions

5.10. Solid electrolyte material comparison

5.11. SSB company commercial plans

5.12. Solid state battery collaborations /investment by Automotive OEMs

5.13. Location overview of major solid-state battery companies

5.14. Technology summary of various companies

5.15. Silicon anodes and solid-state batteries

5.16. SSB with silicon anode - Solid Power

5.17. SSB with silicon anode performance

5.18. Blue Current

5.19. WeLion semi-solid battery patent case study (1)

5.20. WeLion semi-solid battery patent case study (2)

5.21. Pack considerations for SSBs

6. CELL AND BATTERY DESIGN6.1. Cell Design and Inactive Materials

6.1.1. 4680 tabless cell

6.1.2. Increasing cell sizes

6.1.3. Bipolar cell design

6.1.4. Thick format electrodes

6.1.5. Thick format electrodes - 24m

6.1.6. Dual electrolyte Li-ion

6.1.7. Multi-layer electrodes - EnPower

6.1.8. Impact of multi-layer electrode design

6.1.9. Prieto's 3D cell design (1/2)

6.1.10. Prieto's 3D cell design (2/2)

6.1.11. Addionics 3D current collector

6.1.12. Electrolyte decomposition

6.1.13. Electrolyte additives 1

6.1.14. Electrolyte additives 2

6.1.15. Electrolyte additives 3

6.1.16. Electrolyte developments

6.1.17. Electrolyte patent topic comparisons - key battery players

6.1.18. Electrolyte patent topic comparisons - key electrolyte players

6.1.19. Carbon nanotubes in Li-ion

6.1.20. Key Supply Chain Relationships

6.1.21. Results showing impact of CNT use in Li-ion electrodes

6.1.22. Results showing SWCNT improving in LFP batteries

6.1.23. Improved performance at higher C-rate

6.1.24. Significance of dispersion in energy storage

6.1.25. Graphene coatings for Li-ion

6.2. Evolving Cell Performance

6.2.1. Energy density by cathode

6.2.2. BEV cell energy density trend

6.2.3. Cell energy density trend

6.2.4. Cell performance specification examples

6.2.5. Cell specifications (2022-2030)

6.2.6. Comparing commercial cell chemistries

6.3. Battery Packs and BMS

6.3.1. What is Cell-to-pack?

6.3.2. Cell-to-pack or modular?

6.3.3. Drivers and Challenges for Cell-to-pack

6.3.4. What is Cell-to-chassis/body?

6.3.5. BYD Blade battery

6.3.6. CATL cell-to-pack

6.3.7. Cell-to-pack and cell-to-body designs summary

6.3.8. Gravimetric energy density and cell-to-pack ratio

6.3.9. Volumetric energy density and cell-to-pack ratio

6.3.10. Outlook for Cell-to-pack & cell-to-body designs

6.3.11. Bipolar batteries

6.3.12. Bipolar-enabled CTP

6.3.13. ProLogium: "MAB" EV battery pack assembly

6.3.14. Electric vehicle hybrid battery packs

6.3.15. CATL hybrid Li-ion and Na-ion pack concept

6.3.16. CATL hybrid pack designs

6.3.17. Our Next Energy

6.3.18. High energy plus high cycle life

6.3.19. Nio's dual-chemistry battery

6.3.20. Nio's design to improve thermal performance

6.3.21. Nio hybrid battery operation

6.3.22. Hybrid battery + supercapacitor

6.3.23. Concluding remarks on hybrid batteries

6.3.24. BMS introduction

6.3.25. Functions of a BMS

6.3.26. Improvements to battery performance from BMS development

6.3.27. Innovations in BMS

6.3.28. Advanced BMS activity

6.3.29. Impact of fast-charging

6.3.30. Fast charging protocols

6.3.31. BMS solutions for fast charging

6.3.32. Development of wireless BMS

6.3.33. Wireless BMS pros and cons

6.3.34. Concluding remarks on BMS development

7. FORECASTS

7.1. Total addressable markets

7.2. Addressable markets by technology

7.3. Power range of electrical and electronic devices

7.4. Addressable markets - electric car types

7.5. Li-ion battery contribution to device bill of materials

7.6. Examples of new technology entry

7.7. Application battery performance priorities

7.8. Total addressable markets (GWh)

7.9. Total addressable markets forecast data (GWh)

7.10. BEV car cathode forecast (GWh)

7.11. BEV cathode forecast (GWh)

7.12. EV cathode forecast (GWh)

7.13. Silicon anode forecast methodology

7.14. BEV anode forecast (GWh)

7.15. BEV anode forecast (kt, US$B)

7.16. EV Anode forecast (GWh)

7.17. On-road EV Anode forecast (GWh)

7.18. Off-road EV

7.19. Consumer devices Anode forecast (GWh)

7.20. Advanced anode forecast (GWh, kt, US$B)

7.21. Advanced anode forecast (GWh)

7.22. Advanced anode forecast (kt, US$B)

8. COMPANY PROFILES

8.1. 6K Energy

8.2. Addionics

8.3. Addionics: Use of Machine Learning Methods

8.4. Beijing WeLion New Energy Technology

8.5. Blue Solutions

8.6. CAMX Power: New Cathode Platforms

8.7. CENS Materials

8.8. Coreshell

8.9. Daejoo Electronic Materials

8.10. E-magy

8.11. Eatron Technologies

8.12. Enovix

8.13. Forge Nano

8.14. GDI

8.15. Group14 Technologies

8.16. HiT Nano

8.17. IBU-tec Advanced Materials AG

8.18. Ionblox

8.19. Iontra

8.20. LeydenJar Technologies

8.21. Lyten: Developing Lithium-Sulfur

8.22. Nanoramic Laboratories

8.23. Nexeon

8.24. NIO (Battery)

8.25. Novonix

8.26. OneD Battery Sciences

8.27. Our Next Energy (ONE)

8.28. Shanghai Putailai

8.29. Shenzhen Dynanonic

8.30. Sicona Battery

8.31. Sila Nanotechnologies

8.32. South 8 Technologies

8.33. StoreDot: Battery Development AI

8.34. Stratus Materials

8.35. Sylvatex

8.36. theion: Developing Lithium-Sulfur Batteries Using Crystalline Wafers

8.37. WAE Technologies

8.38. Xerion Advanced Battery Corp

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(エネルギー貯蔵)の最新刊レポート

IDTechEx社の 電池 、エネルギー- Batteries & Energy Storage分野 での最新刊レポート

関連レポート(キーワード「リチウム」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|