グローバル中性原子量子コンピューティング市場 2026-2036年The Global Neutral-Atom Quantum Computing Market 2026-2036 中性原子量子コンピューティングは、量子コンピューティング産業において最も有望かつ急速に発展している分野の一つである。この技術は、光学ピンセットと呼ばれる精密に集束されたレーザービームを用い... もっと見る

サマリー

中性原子量子コンピューティングは、量子コンピューティング産業において最も有望かつ急速に発展している分野の一つである。この技術は、光学ピンセットと呼ばれる精密に集束されたレーザービームを用いて捕捉・操作される個々の中性原子(通常はルビジウム、セシウム、ストロンチウムなどのアルカリ金属)を利用する。 捕獲イオンとは異なり、中性原子は電気的に帯電していないため、量子ビット間のクロストークを最小限に抑えつつ、柔軟な二次元および三次元配列を形成することが可能である。

中性原子システムの基本的な魅力は、その本質的なスケーラビリティと運用上の利点にあります。これらのプラットフォームは長いコヒーレンス時間を示し、持続的な量子操作とエラー訂正の可能性の向上を可能にします。この技術は、よく理解されている原子物理学の原理の恩恵を受け、超伝導量子ビットシステムに必要な極端な極低温冷却を不要とし、その結果、エネルギー消費量の削減とインフラの複雑さの低減をもたらします。 現行の運用システムは100~300原子の配列を備え、主要企業は数千~数万量子ビットへの急速な拡張を進めている。

競争環境では、戦略的ポジションを確立する複数の資金力あるプレイヤーが存在している。米国拠点のQuEra ComputingはGoogleから多額の投資を獲得し、中性原子プラットフォームがスケーラブル量子コンピューティングへの有効な道筋であることを実証した。この提携により、QuEraのハードウェア専門知識とGoogleの量子ソフトウェアリソース・クラウドインフラが統合される。Atom ComputingはMicrosoftと並行して提携を結び、安定した核スピン量子ビット配列を備えたPhoenixシステムをAzure Quantumのクラウドプラットフォームに統合している。 この分野のフランス主導企業Pasqalは、2024年に1,000量子ビット達成という重要なマイルストーンを成し遂げ、2026年までに10,000量子ビットへ拡張する野心的な計画を発表した。その他のプレイヤーには、ドイツのPlanqc、香港のQUANTier、スロベニアのAtom Quantum Labsが含まれ、各社とも中性原子アーキテクチャに向けた独自のアプローチを開発中である。

技術ロードマップでは2035年までの積極的な拡張が予測される。現行システム(2025-2026年)は1,000-10,000原子で動作し、単一量子ビット忠実度約99.9%、2量子ビット忠実度99.7%を達成。 2027-2028年までに、1万~10万原子を目標とするシステムは、エラー訂正機能を備えた99.99%の単一量子ビット忠実度を目指す。 2029-2030年には10万原子以上で耐障害性論理量子ビット操作を実現し、2032-2035年までに完全耐障害性を備えた百万原子規模システムと産業展開を目指す。

主な応用分野は量子シミュレーション、最適化問題、量子化学、機械学習タスクに及ぶ。特に複雑な物理系シミュレーション、凝縮系研究、分子構造解析において優れた性能を発揮する。製薬、化学、金融サービス産業が中性原子ソリューションを追求する主要市場分野である。

課題としては、コヒーレンス時間の延長、ゲート速度の向上(現在のシミュレーションサイクルは約1Hzに制限)、計算中の原子損失の解決、エラー訂正と耐障害性量子コンピューティングに必要な量子非破壊測定技術の開発などが残されている。 こうした課題にもかかわらず、中性原子量子コンピューティングは常温動作、自然なスケーラビリティ、柔軟性を強みとして超伝導プラットフォームに対する有力な競合技術として台頭しており、2026年から2036年の予測期間を通じて大幅な商業的成長が見込まれる。

本レポートは、技術カテゴリー、応用分野、顧客タイプ、地域別に分類した、2026年から2036年までの完全な市場規模と10年間の予測を提供します。戦略的分析では、競争上のポジショニング、投資動向、技術成熟度評価、中性原子エコシステムを形成する32社の詳細な企業プロファイルをカバーしています。

レポート内容

本レポートでは、中性原子量子コンピューティングのバリューチェーン全体にわたる32社の包括的な企業プロファイルを掲載。対象企業にはAMD(アドバンスト・マイクロ・デバイセズ)、Atom Computing、Atom Quantum Labs、CAS Cold Atom、data cybernetics ssc GmbH、GDQLABS、 浜松ホトニクス、インフレクション、レイクショア・クライオトロニクス、エムラボ、メンロシステムズGmbH、マイクロソフト社(Azure Quantum)、ナノファイバー・クオンタム・テクノロジーズ、ネクサス・フォトニクスなどが含まれます。

目次

1 エグゼクティブサマリー

1.1 市場概要と主な調査結果

1.2 技術成熟度と商業的実現可能性

1.3 市場予測

1.4 市場関係者

1.5 製品およびシステムの比較

1.5.1 現行システム

1.5.2 システムの価格とアクセスモデル

1.5.3 ロードマップ比較

2 中立原子技術と製品

2.1 テクノロジーの進化

2.1.1 使用される原子種

2.1.2 アクセシビリティ

2.1.3 商業的に実現可能な量子システムの研究

2.2 中性原子コンポーネント

2.2.1 原子制御ハードウェアおよび読み出しコンポーネント

2.2.2 光子および写真部品

2.2.3 クライオスタット

2.2.3.1 極低温要件と比較

2.2.4 コスト

2.2.5 総所有コスト分析

2.3 Neutral Atom 関連ソフトウェア

2.3.1 ソフトウェアスタックの構成要素と機能

2.3.2 使用したプログラミング言語とフレームワーク

2.4 技術の準備状況

2.4.1 技術的制約と課題

2.4.2 競合量子技術に対する優位性

2.4.3 インフラストラクチャと運用上の利点

2.4.4 性能ベンチマークとスケーラビリティ

3 市場とアプリケーション

3.1 量子コンピューティングの応用分野

3.1.1 中性原子コンピュータにおける分散量子コンピューティング

3.1.2 データセンターにおける中性原子コンピュータ

3.1.3 中性原子コンピュータのその他の応用

3.2 エコシステム

3.2.1 市場制御のダイナミクス

3.2.2 エコシステム開発

3.3 中性原子コンピュータ向けサプライチェーン

3.3.1 製造とサプライチェーン

3.3.2 部品調達と依存関係

3.3.3 比較サプライチェーン分析:極低温システムと常温システムの比較

3.4 国の投資および政策イニシアチブ

3.5 市場セグメンテーション

3.5.1 エンタープライズ

3.5.2 クラウドサービスプロバイダー

3.5.3 政府および防衛

3.5.4 アカデミアおよび研究

4 中性原子技術

4.1 中性原子コンピュータ

4.1.1 概要

4.1.2 企業

4.2 中立原子コンポーネントとサブシステム

4.2.1 概要

4.2.2 コンポーネント市場バリューチェーン

4.2.3 企業

4.3 ソフトウエア

4.3.1 概要

4.3.2 ソフトウェアプラットフォームの比較

4.3.3 ソフトウェアスタックアーキテクチャ

4.3.4 開発ツールとフレームワーク

4.3.5 オープンソースとプロプライエタリソリューションの比較

4.3.6 企業

4.3.7 開発ツールとフレームワーク

4.3.8 オープンソースとプロプライエタリソリューションの比較

4.4 プラットフォーム

4.4.1 クラウドプラットフォーム

4.4.2 プラットフォームの機能と性能

4.4.3 企業とセンター

5 市場規模と成長(2026-2036年)

5.1 グローバル市場規模予測 2026-2036年

5.2 セグメント別収益予測

5.3 地域別市場分布

5.4 市場浸透シナリオ

5.5 成長の推進要因と制約

5.6 グローバル設置分析

6 技術開発ロードマップ

6.1 ハードウェアのスケーリングとエラー訂正

6.1.1 量子ビットのスケーリング軌道

6.1.2 エラー訂正の進捗

6.2 ソフトウェアスタックの進化

6.3 従来型コンピューティングとの統合

6.4 製造プロセスの改善

6.4.1 製造のスケールアップ:中性原子プラットフォームと極低温プラットフォームの比較

7 投資と資金調達

7.1 ベンチャーキャピタルと民間投資

7.2 政府資金と国家イニシアチブ

7.3 企業の研究開発投資動向

8 課題とリスク要因

8.1 技術的ハードルと開発リスク

8.2 市場導入障壁

8.3 代替技術による競争上の脅威

8.4 規制およびセキュリティ上の考慮事項

9 将来の市場機会

9.1 新興アプリケーション分野

9.2 技術の融合による機会

9.3 破壊的潜在力評価

10 企業プロファイル(31社)

11 研究方法論

11.1 レポートの範囲と目的

11.2 研究方法とデータソース

11.3 市場定義とセグメンテーション

12 参考文献

図表リスト

表の一覧

表1 中性原子量子コンピュータの初期化、操作、および読み出し

表2 低温原子量子コンピュータとシミュレータの長所と短所

表3 技術成熟度レベル定義と量子コンピューティング基準

表4 量子コンピューティングプラットフォーム別TRL評価(2025年)

表5 主要次元におけるTRL比較

表6 サブシステム別TRL - 中性原子詳細評価

表7 応用分野別TRL比較

表8 プラットフォーム別主要TRL推進要因

表9 2026-2036年グローバル市場規模予測

表10 主な中性原子量子ビット市場プレイヤー

表11 現行中性原子システムの仕様

表12 中性原子システムの価格とアクセス

表13 企業ロードマップ比較

表14 中性原子システムで使用される原子種

表15 アクセシビリティ指標比較

表16 主要ハードウェアコンポーネントと仕様

表17 初期化、操作、および読み出し方法

表18 光学部品および撮像部品仕様

表19 クライオスタットの要求事項と仕様

表20 クライオスタット要求事項と仕様の比較

表21 超電導システムにおける多段階温度環境

表22 部品コスト内訳分析

表23 他の量子技術とのコスト比較

表24 総所有コスト比較(5年間、1000量子ビットシステム)

表25 インフラストラクチャ拡張コスト予測

表26 ソフトウェアスタックの構成要素と機能

表27 使用プログラミング言語とフレームワーク

表28 技術的課題と対策

表29 他の量子技術との性能比較

表30 インフラストラクチャ優位性の比較

表31 現行システムの達成目標(2024-2025年)

表32 中性原子ハードウェア開発ロードマップ

表33 分散コンピューティングのユースケースと要件

表34 分散中性原子コンピューティングの主要技術要件

表35 新興アプリケーション領域と市場潜在性

表36 アプリケーション導入のタイムライン要因

表37 主要なエコシステムパートナーシップと提携

表38 エコシステム・バリューチェーン分析

表39 サプライチェーン構造と主要参加者

表40 サプライチェーンリスク評価

表41 重要部品の依存関係とリスク軽減策

表42 プラットフォーム別サプライチェーン比較

表43 極低温部品サプライヤーの概況

表44 国家的投資と政策イニシアチブ

表45 企業の導入推進要因と障壁

表46 企業の関与モデル

表47 クラウドプラットフォーム中立型アトム統合

表48 政府・防衛市場の特性

表49 学術・研究市場の構造

表50 中立アトムコンピューティングに関する学術研究の優先事項

表51 中性原子コンピューター企業

表52 コンポーネント市場のバリューチェーン

表53 中性原子システムの価値分布

表54 中性原子コンポーネントおよびサブシステム企業

表55 コンポーネント市場バリューチェーン

表56 ソフトウェアプラットフォーム比較

表57 プラットフォーム・エコシステム統合

表58 開発ツールとフレームワーク

表59 ソフトウェア市場収益予測

表60 オープンソース対プロプライエタリソリューション

表61 ハイブリッド導入モデル

表62 ソフトウェア企業

表63 ソフトウェアプラットフォーム比較

表64 プラットフォームエコシステム統合

表65 開発ツールとフレームワーク

表66 オープンソース対プロプライエタリソリューション

表67 プラットフォームの機能と能力

表68 プラットフォーム企業とセンター

表69 ユーザー採用と成長指標

表70 価格モデルとコスト分析

表71 コスト比較例(1,000回路実行)

表72 グローバル市場規模予測 2026-2036年

表73 カテゴリー別市場規模詳細

表74 量子コンピューティング全体に対する市場ポジション(10億米ドル)

表75 アプリケーションセグメント別収益予測(10億米ドル)

表76 顧客セグメント別収益(10億米ドル)

表77 地域別市場成長予測(10億米ドル)

表78 地域別市場動向

表79 地域別設置台数予測(台)

表80 顧客タイプ別地域別設置台数予測(台)

表81 市場浸透シナリオ(保守的、基本、楽観的)

表82 年次別市場規模範囲(10億ドル)

表83 成長要因の影響分析

表84 市場制約とリスク要因

表85 グローバル中性原子量子コンピュータ設置予測

表86 主要設置場所(現在および発表済み)

表87 ハードウェアスケーリングのマイルストーン

表88 企業別スケーリング経路

表89 主要スケーリング技術

表90 エラー訂正の進捗予測

表91 中性原子向け誤り訂正符号

表92 ゲート忠実度の軌跡

表93 論理量子ビット実証のタイムライン

表94 ソフトウェア進化ロードマップ

表95 段階別ソフトウェア開発優先順位

表96 製造コスト削減曲線

表97 統合ロードマップ:

表98 主要製造領域

表99 技術開発タイムライン

表100 製造複雑性の比較

表101 プラットフォーム別生産量予測

表102 ベンチャーキャピタルおよび民間投資

表103 企業別量子技術資金調達額(2022-2025年、百万米ドル)

表104 政府資金と国家イニシアチブ

表105 地域別政府投資比較(2023-2025年、10億米ドル)

表106 投資動向 2020-2025年および2036年までの予測

表107 主要テクノロジー企業別研究開発投資

表108 中性原子分野におけるコーポレートベンチャー投資

表109 2026-2036年の投資予測(百万米ドル)

表110 技術プラットフォーム別投資額(実績と予測)

表111 エンドユーザー産業における量子対応投資

表112 主要投資要因と動向

表113 リスク評価マトリックス

表114 市場導入障壁

表115 顧客セグメント別導入障壁の影響

表116 代替技術による競争上の脅威

表117 地域別規制枠組み比較

表118 新興アプリケーション市場の潜在的可能性

表119 技術融合の機会

表120 新興アプリケーション市場の潜在的可能性

図一覧

図1 様々な構成に配置された中性原子(緑の点)

図2 中性原子ハードウェアのロードマップ

図3 2026-2036年の中性原子量子コンピューティング世界市場規模

図4 中性原子技術開発のタイムライン

図5 中性原子システム構成図

図6 技術成熟度レベル評価

図7 2026-2036年のスケーラビリティ予測

図8 データセンター統合アーキテクチャ

図9 アプリケーション導入タイムライン

図10 市場支配力と影響力マッピング

図11 製造プロセスフロー

図12 クラウドプロバイダー統合タイムライン

図13 中性原子量子処理ユニット(QPU)間におけるリピーター対応長距離ネットワーク構想

図14 アプリケーションセグメント別収益予測(10億米ドル)

図15 顧客セグメント別収益(10億米ドル)

図16 地域別市場成長予測(10億米ドル)

図17 ColdQuantaの量子コア(左)、物理ステーション(中央)、原子制御チップ(右)

図18 Pasqalの中性原子量子コンピュータ

Summary

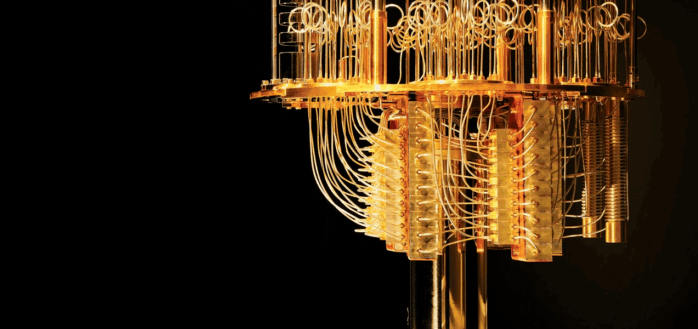

Neutral-atom quantum computing represents one of the most promising and rapidly advancing segments of the quantum computing industry. This technology leverages individual neutral atoms—typically alkali metals like rubidium, cesium, or strontium—trapped and manipulated using precisely focused laser beams called optical tweezers. Unlike trapped ions, neutral atoms are not electrically charged, allowing them to be arranged in flexible two-dimensional and three-dimensional arrays with minimal crosstalk between qubits.

The fundamental appeal of neutral-atom systems lies in their inherent scalability and operational advantages. These platforms demonstrate long coherence times, enabling sustained quantum operations and increased error correction possibilities. The technology benefits from well-understood atomic physics principles and eliminates the need for the extreme cryogenic cooling required by superconducting qubit systems, resulting in lower energy consumption and reduced infrastructure complexity. Current operational systems feature 100-300 atom arrays, with leading companies rapidly scaling toward thousands and tens of thousands of qubits.

The competitive landscape features several well-funded players establishing strategic positions. QuEra Computing, based in the United States, has secured significant investment from Google, validating neutral-atom platforms as viable paths to scalable quantum computing. This partnership combines QuEra's hardware expertise with Google's quantum software resources and cloud infrastructure. Atom Computing has forged a parallel partnership with Microsoft, integrating its Phoenix system—featuring stable nuclear-spin qubit arrays—with Azure Quantum's cloud platform. Pasqal, the French leader in this space, achieved a significant milestone by reaching 1,000 qubits in 2024 and has announced ambitious plans to scale to 10,000 qubits by 2026. Additional players include Planqc in Germany, QUANTier in Hong Kong, and Atom Quantum Labs in Slovenia, each developing distinctive approaches to neutral-atom architectures.

The technology roadmap projects aggressive scaling through 2035. Current systems (2025-2026) operate with 1,000-10,000 atoms achieving single-qubit fidelities around 99.9% and two-qubit fidelities of 99.7%. By 2027-2028, systems targeting 10,000-100,000 atoms aim for 99.99% single-qubit fidelity with error correction capabilities. The 2029-2030 horizon envisions 100,000+ atoms with fault-tolerant logical qubit operations, progressing toward million-atom systems with full fault tolerance and industrial deployment by 2032-2035.

Primary applications span quantum simulations, optimization problems, quantum chemistry, and machine learning tasks. The technology excels particularly in simulating complex physical systems, condensed matter research, and molecular structure analysis. The pharmaceutical, chemical, and financial services industries represent key market verticals pursuing neutral-atom solutions.

Challenges remain, including achieving longer coherence times, improving gate speeds (currently limited to approximately 1 Hz simulation cycles), addressing atom loss during computation, and developing quantum non-demolition measurement capabilities required for error correction and fault-tolerant quantum computing. Despite these hurdles, neutral-atom quantum computing has emerged as a serious competitor to superconducting platforms, with its room-temperature operation, natural scalability, and flexibility positioning it for significant commercial growth through the 2026-2036 forecast period.

This report provides complete market sizing and ten-year forecasts from 2026 through 2036, segmented by technology category, application domain, customer type, and geographic region. Strategic analysis covers competitive positioning, investment trends, technology readiness assessments, and detailed company profiles of 32 organizations shaping the neutral-atom ecosystem.

Report Contents Include

This report features comprehensive profiles of 32 companies across the neutral-atom quantum computing value chain including AMD (Advanced Micro Devices), Atom Computing, Atom Quantum Labs, CAS Cold Atom, data cybernetics ssc GmbH, GDQLABS, Hamamatsu, Infleqtion, Lake Shore Cryotronics, M-Labs, Menlo Systems GmbH, Microsoft Corporation (Azure Quantum), Nanofiber Quantum Technologies, Nexus Photonics and more.

Table of Contents

1 EXECUTIVE SUMMARY

1.1 Market Overview and Key Findings

1.2 Technology Readiness and Commercial Viability

1.3 Market Forecasts

1.4 Market Players

1.5 Product and System Comparison

1.5.1 Current Systems

1.5.2 System Pricing and Access Models

1.5.3 Roadmap Comparison

2 NEUTRAL ATOM TECHNOLOGY AND PRODUCTS

2.1 Technology Evolution

2.1.1 Atoms Species Used

2.1.2 Accessibility

2.1.3 Research to commercially viable quantum systems

2.2 Neutral Atom Components

2.2.1 Atomic Control Hardware and Readout Components

2.2.2 Photonic and Photographic Components

2.2.3 Cryostats

2.2.3.1 Cryogenic Requirements and Comparison

2.2.4 Costs

2.2.5 Total Cost of Ownership Analysis

2.3 Neutral Atom-related Software

2.3.1 Software Stack Components and Functions

2.3.2 Programming Languages and Frameworks Used

2.4 Technology Readiness

2.4.1 Technical Limitations and Challenges

2.4.2 Advantages Over Competing Quantum Technologies

2.4.3 Infrastructure and Operational Advantages

2.4.4 Performance Benchmarks and Scalability

3 MARKETS AND APPLICATIONS

3.1 Applications

3.1.1 Distributed Quantum Computing on Neutral Atom Computers

3.1.2 Neutral Atom Computers in the Data Center

3.1.3 Other Applications for Neutral Atom Computers

3.2 Ecosystems

3.2.1 Market Control Dynamics

3.2.2 Ecosystem Development

3.3 Supply Chain for Neutral Atom Computers

3.3.1 Manufacturing and Supply Chain

3.3.2 Component Sourcing and Dependencies

3.3.3 Comparative Supply Chain Analysis: Cryogenic vs. Room Temperature Systems

3.4 National Investment and Policy Initiatives

3.5 Market Segmentation

3.5.1 Enterprise

3.5.2 Cloud Service Providers

3.5.3 Government and Defence

3.5.4 Academia and Research

4 NEUTRAL ATOM TECHNOLOGIES

4.1 Neutral-Atom Computers

4.1.1 Overview

4.1.2 Companies

4.2 Neutral Atom Components and Subsystems

4.2.1 Overview

4.2.2 Component Market Value Chain

4.2.3 Companies

4.3 Software

4.3.1 Overview

4.3.2 Software Platform Comparison

4.3.3 Software Stack Architecture

4.3.4 Development Tools and Frameworks

4.3.5 Open Source vs. Proprietary Solutions

4.3.6 Companies

4.3.7 Development Tools and Frameworks

4.3.8 Open Source vs. Proprietary Solutions

4.4 Platforms

4.4.1 Cloud Platform

4.4.2 Platform Features and Capabilities

4.4.3 Companies and Centres

5 MARKET SIZE AND GROWTH (2026-2036)

5.1 Global Market Size Forecast 2026-2036

5.2 Revenue Forecasts by Segment

5.3 Geographic Market Distribution

5.4 Market Penetration Scenarios

5.5 Growth Drivers and Constraints

5.6 Global Installations Analysis

6 TECHNOLOGY DEVELOPMENT ROADMAP

6.1 Hardware Scaling and Error Correction

6.1.1 Qubit Scaling Trajectory

6.1.2 Error Correction Progress

6.2 Software Stack Evolution

6.3 Integration with Classical Computing

6.4 Manufacturing Improvements

6.4.1 Manufacturing Scaling: Neutral Atom vs. Cryogenic Platforms

7 INVESTMENT AND FUNDING

7.1 Venture Capital and Private Investment

7.2 Government Funding and National Initiatives

7.3 Corporate R&D Investment Trends

8 CHALLENGES AND RISK FACTORS

8.1 Technical Hurdles and Development Risks

8.2 Market Adoption Barriers

8.3 Competitive Threats from Alternative Technologies

8.4 Regulatory and Security Considerations

9 FUTURE MARKET OPPORTUNITES

9.1 Emerging Application Areas

9.2 Technology Convergence Opportunities

9.3 Disruptive Potential Assessment

10 COMPANY PROFILES (31 company profiles)

11 RESEARCH METHODOLOGY

11.1 Report Scope and Objectives

11.2 Research Methodology and Data Sources

11.3 Market Definition and Segmentation

12 REFERENCES

List of Tables/Graphs

List of Tables

Table1 Initialization, manipulation and readout for neutral-atom quantum computers

Table2 Pros and cons of cold atoms quantum computers and simulators

Table3 Technology Readiness Level Definitions and Quantum Computing Criteria

Table4 TRL Assessment by Quantum Computing Platform (2025)

Table5 TRL Comparison Across Key Dimensions

Table6 TRL by Subsystem - Neutral Atom Detailed Assessment

Table7 TRL Comparison by Application Domain

Table8 Key TRL Advancement Drivers by Platform

Table9 Global Market Size Forecast 2026-2036

Table10 Main neural atom qubit market players

Table11 Current Neutral Atom System Specifications

Table12 Neutral Atom System Pricing and Access

Table13 Company Roadmap Comparison

Table14 Atomic Species Used in Neutral Atom Systems

Table15 Accessibility Metrics Comparison

Table16 Key Hardware Components and Specifications

Table17 Initialization, Manipulation, and Readout Methods

Table18 Photonic and Imaging Component Specifications:

Table19 Cryostat Requirements and Specifications

Table20 Cryostat Requirements and Specifications Comparison

Table21 Multi-Stage Temperature Environment in Superconducting Systems

Table22 Component Cost Breakdown Analysis

Table23 Cost Comparison with Other Quantum Technologies:

Table24 Total Cost of Ownership Comparison (5-Year, 1000-Qubit System)

Table25 Infrastructure Scaling Cost Projections

Table26 Software Stack Components and Functions

Table27 Programming Languages and Frameworks Used

Table28 Technical Challenges and Mitigation Strategies

Table29 Performance Comparison with Other Quantum Technologies

Table30 Infrastructure Advantage Comparison

Table31 Current System Achievements (2024-2025)

Table32 Neutral Atom Hardware Development Roadmap

Table33 Distributed Computing Use Cases and Requirements

Table34 Key Technical Requirements for Distributed Neutral Atom Computing

Table35 Emerging Application Areas and Market Potential

Table36 Application Adoption Timeline Factors

Table37 Key Ecosystem Partnerships and Alliances

Table38 Ecosystem Value Chain Analysis

Table39 Supply Chain Structure and Key Participants

Table40 Supply Chain Risk Assessment

Table41 Critical Component Dependencies and Risk Mitigation

Table42 Supply Chain Comparison by Platform

Table43 Cryogenic Component Supplier Landscape

Table44 National Investment and Policy Initiatives

Table45 Enterprise Adoption Drivers and Barriers

Table46 Enterprise Engagement Models

Table47 Cloud Platform Neutral Atom Integration

Table48 Government and Defense Market Characteristics

Table49 Academic and Research Market Structure

Table50 Academic Research Priorities for Neutral Atom Computing

Table51 Neutral Atom Computer Companies

Table52 Component Market Value Chain

Table53 Value Distribution in Neutral Atom Systems

Table54 Neutral Atom Components and Subsystems Companies

Table55 Component Market Value Chain

Table56 Software Platform Comparison

Table57 Platform Ecosystem Integration

Table58 Development Tools and Frameworks

Table59 Software Market Revenue Projections

Table60 Open Source vs. Proprietary Solutions

Table61 Hybrid Deployment Models

Table62 Software companies

Table63 Software Platform Comparison

Table64 Platform Ecosystem Integration

Table65 Development Tools and Frameworks

Table66 Open Source vs. Proprietary Solutions

Table67 Platform Features and Capabilities

Table68 Platform Companies and Centres

Table69 User Adoption and Growth Metrics

Table70 Pricing Models and Cost Analysis

Table71 Cost Comparison Example (1,000 Circuit Executions)

Table72 Global Market Size Forecast 2026-2036

Table73 Market Size by Category Detail

Table74 Market Position Relative to Total Quantum Computing (Billions USD)

Table75 Revenue Forecasts by Application Segment (Billions USD)

Table76 Revenue by Customer Segment (Billions USD)

Table77 Regional Market Growth Projections (Billions USD)

Table78 Regional Market Dynamics

Table79 Regional Installation Forecast (Units)

Table80 Regional Installation Forecast (Units) by Customer Type

Table81 Market Penetration Scenarios (Conservative, Base, Optimistic)

Table82 Market Size Range by Year ($ Billions)

Table83 Growth Drivers Impact Analysis

Table84 Market Constraints and Risk Factors

Table85 Global Neutral Atom Quantum Computer Installations Forecast

Table86 Key Installation Locations (Current and Announced)

Table87 Hardware Scaling Milestones

Table88 Scaling Pathway by Company

Table89 Key Scaling Technologies

Table90 Error Correction Progress Projections

Table91 Error Correction Codes for Neutral Atoms

Table92 Gate Fidelity Trajectory

Table93 Logical Qubit Demonstrations Timeline

Table94 Software Evolution Roadmap

Table95 Software Development Priorities by Phase

Table96 Manufacturing Cost Reduction Curve

Table97 Integration Roadmap:

Table98 Key Manufacturing Domains

Table99 Technology Development Timeline

Table100 Manufacturing Complexity Comparison

Table101 Production Volume Projections by Platform

Table102 Venture Capital and Private Investment

Table103 Quantum Technology Funding by Company (2022-2025, Millions USD)

Table104 Government Funding and National Initiatives

Table105 Regional Government Investment Comparison (2023-2025, USD Billions)

Table106 Investment Trends 2020-2025 and Projections to 2036

Table107 Corporate R&D Investment by Major Technology Companies

Table108 Corporate Venture Investment in Neutral Atom

Table109 Investment Projections 2026-2036 (USD Millions)

Table110 Investment by Technology Platform (Historical and Projected)

Table111 End-User Industry Investment in Quantum Readiness

Table112 Key Investment Drivers and Trends

Table113 Risk Assessment Matrix

Table114 Market Adoption Barriers

Table115 Adoption Barrier Impact by Customer Segment

Table116 Competitive Threats from Alternative Technologies

Table117 Regulatory Framework Comparison by Region

Table118 Emerging Application Market Potential

Table119 Technology Convergence Opportunities

Table120 Emerging Application Market Potential

List of Figures

Figure1 Neutral atoms (green dots) arranged in various configurations

Figure2 Neutral Atom Hardware Roadmap

Figure3Global Neutral Atom Quantum Computing Market Size 2026-2036

Figure4 Timeline of Neutral Atom Technology Development

Figure5 Neutral Atom System Architecture Diagram

Figure6 Technology Readiness Level Assessment

Figure7 Scalability Projections 2026-2036

Figure8 Data Center Integration Architecture

Figure9 Application Adoption Timeline

Figure10 Market Control and Influence Mapping

Figure11 Manufacturing Process Flow

Figure12 Cloud Provider Integration Timeline

Figure13 Vision for a repeater-enabled long-distance network between neutral atom quantum processing units (QPUs)

Figure14 Revenue Forecasts by Application Segment (Billions USD)

Figure15 Revenue by Customer Segment (Billions USD)

Figure16 Regional Market Growth Projections (Billions USD)

Figure17 ColdQuanta Quantum Core (left), Physics Station (middle) and the atoms control chip (right)

Figure18 Pasqal's neutral-atom quantum computer

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(通信・IT)の最新刊レポート

Future Markets, inc.社の 量子テクノロジー分野 での最新刊レポート関連レポート(キーワード「量子コンピューティング」)

よくあるご質問Future Markets, inc.社はどのような調査会社ですか?Future Markets, inc.は先端技術に焦点をあてたスウェーデンの調査会社です。 2009年設立のFMi社は先端素材、バイオ由来の素材、ナノマテリアルの市場をトラッキングし、企業や学... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|