センサー市場2026-2036年:技術、動向、プレーヤー、予測Sensor Market 2026-2036: Technologies, Trends, Players, Forecasts 将来のモビリティ、LiDAR、レーダー、カメラ、IR、MEMS、ウェアラブル、AI、エッジセンサー、量子センサー、プリンテッドセンサー、ガスセンサー、バッテリーセンサー、シリコンフォトニクス、イメージセ... もっと見る

サマリー

将来のモビリティ、LiDAR、レーダー、カメラ、IR、MEMS、ウェアラブル、AI、エッジセンサー、量子センサー、プリンテッドセンサー、ガスセンサー、バッテリーセンサー、シリコンフォトニクス、イメージセンサーを含む世界のセンサー市場、10年間の粒状センサー市場予測付き

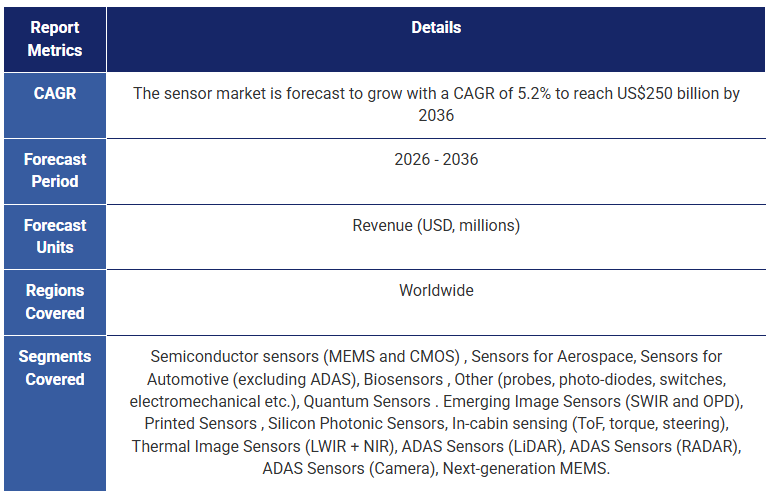

センサー技術市場は2036年までに250億米ドルに成長

IDTechExは、モビリティ、AI、ロボティクス、6Gコネクティビティ、IoTの世界的なメガトレンドがセンサー需要を促進するため、世界のセンサー市場は2036年までに2500億米ドルに達すると予測している。IDTechExのセンサーレポートは、58社の企業プロファイルと20以上の関連センサーレポートから収集した洞察を含む、世界のセンサー市場の広範な分析を提供しています。IDTechExの広範なセンサーレポートポートポートポートフォリオを要約すると、この調査には、将来のモビリティ、IoT、ウェアラブル、バイオメディカル、エッジコンピューティング、環境センシングなどにわたる35以上のセンサー技術のSWOT分析、24の技術準備レベルのロードマップ、材料要件、サプライヤー情報が含まれています。このセンサー市場分析には、センサー技術別に区分された10年間のきめ細かなセンサー予測の更新が含まれています。

.png)

世界のセンサー市場10年予測(2026-2036年)、センサー技術別に区分。出典IDTechEx.

毎年数億個のセンサーが生産され、通信、輸送、産業、ヘルスケア、エネルギー、消費者、ビルなどのアプリケーションでいたるところで使用されている。センサーそのものは大手エレクトロニクス企業の年間売上高のごく一部に過ぎないが、それでもセンサー技術は数十億ドル規模の世界市場を形成している。

2026年においても、成熟したセンサー技術が市場を支配し続けるだろう。IDTechExの調べでは、光学センサー、半導体センサー(MEMSを含む)、バイオセンサー、従来型トランスデューサーが2026年のセンサー市場総売上の85%を占める。確立されたセンサー技術は、航空宇宙、自動車、産業、消費者、ヘルスケア、環境市場を含むほとんどの市場垂直方向で成熟したアプリケーションを持っている。

成熟市場において確立されたセンサーの収益成長が鈍化しているにもかかわらず、メーカー各社は成長を促進するため、新しいセンサー技術と新興アプリケーションにますます注目している。今日のセンサーイノベーションを牽引するメガトレンドには、人工知能(AI)とデータセンター、モノのインターネット(IoT)、インダストリー4.0とロボティクス、将来のモビリティ(自律性、電動化、ドライバーモニタリング)、ウェアラブル技術の採用、6Gの商用化などが含まれる。IDTechExは、新興市場におけるセンサーの成長が、主に新興センサー技術とアプリケーションに牽引され、2036年まで世界のセンサー売上高を年平均成長率5.2%で成長させると予測している。

.png)

2026年の世界のセンサー技術市場とアプリケーションの概要。出典:IDTechEx:IDTechEx.

IDTechExの調査は、主要センサー市場における新興技術がどのように進化しているかを追跡している。センサーの設計トレンドは、プリンテッドエレクトロニクス、フォトニック集積回路、次世代MEMSの技術を用いた製品やアプリケーション内での統合と性能の向上に焦点を当てている。新たなセンサー技術は、小型化・省電力化、より多くの測定基準の測定能力、感度と精度の向上、新たなフォームファクターによって競争することになる。

IDTechExの調査レポート「センサー市場2026-2036:技術、動向、プレーヤー、予測」は、センサー技術の革新と新興アプリケーション市場を幅広く評価しています。本レポートでは、量子センサー、プリンテッドセンサー、ナノカーボンセンサー、イメージセンサー、ADASセンサーなどの新興センサー技術市場を取り上げている。

未来のモビリティが自動車のセンサー需要を再形成し続ける

自動車の電動化、自動化、車内モニタリング、ソフトウェア定義車(SDV)が自動車のセンサー需要を進化させ続けている。新たな将来のモビリティトレンドは、さまざまなセンサー技術にまたがる幅広い機会を生み出している。先進的なEVバッテリーパックセンサーは、バッテリー監視のために温度、電流、電圧、ガスセンサーを使用し、LiDAR、レーダー、赤外線イメージング、カメラ技術は先進運転支援システム(ADAS)の中核となる。

ドライバー・モニタリング・システム(DMS)、そして将来的には乗員モニタリングがいくつかの地域で義務化されつつあり、車載センサーの成長を牽引している。視線追跡が重要な指標であることから、赤外線(IR)、飛行時間(ToF)、レーダーなどのセンサーがADASシステムのドライバー・モニタリング用に登場し、ドライバーがまだ道路に集中しているかどうかをチェックしている。将来的には、車内センシング技術は、コネクテッド・ソフトウェア・デファインド・ビークルにおけるfeatures-as-a-serviceビジネスモデルを実現するためのバイオメトリクス認証にも使用されるかもしれない。

IDTechExの調査では、将来のモビリティ向けセンサーの評価とベンチマークを行い、2036年までに自動車用センサー収益の26%を占める成長機会としてLiDARと赤外線画像センサー分野を特定している。本レポートは、新たな未来のモビリティ技術、アプリケーション、要件、需要を特定し、批判的に評価しています。

ロボット工学、インダストリー4.0、インダストリー5.0向けセンサー

2025年、センサー技術はロボット工学、AI、オートメーションの進歩の結節点にある。コネクテッドデバイスや機器用のエッジAIやIoTセンサーから、協働ロボットやヒューマノイドロボットまで、センサー技術の革新は将来の産業オートメーションソリューションの中心的存在となる。

カメラ、LiDAR、超音波センサー、IMU、力センサー、トルクセンサー、触覚センサーはすべて、産業用ロボット、協働ロボット、ヒューマノイドロボットにおけるナビゲーション、定位、近接検知、作動タスクに不可欠です。

今後10年間で、オートメーション用のセンサーは、自動車、産業、製造、航空宇宙、防衛の各アプリケーションに大きな影響を与えることになるでしょう。インダストリーX.0技術の主な課題は、長い投資回収期間と特注のアプリケーション要件である。IDTechExの調査は、ロボット工学におけるセンサー要件、製品ロードマップ、製造と物流における新たなアプリケーションを包括的に評価している。

ウェアラブルセンサーは多くの指標を提供するが、統合された製品が成功を定義する

ウェアラブルセンサー技術の展望は幅広いセンサータイプをカバーし、ウェアラブルのフォームファクターの配列に統合することができる。2025年には、MetaとXiaomiが製品を発売し、Snap、Amazon、Samsungがすぐに続くと予想されるため、スマートグラス市場で復活が見られる。ウェアラブルセンサーは、ARやXRデバイスの視線追跡、3D空間マッピング、ジェスチャーコントロールを可能にする重要なコンポーネントである。

手首に装着するデバイスに統合されたウェアラブルセンサーは、EMGセンサーやドライ電極の使用によるユーザーインターフェイスや、光学センサーを使用した活動や健康のトラッキングなど、新しい機能を実現し続けている。

本レポートでは、ウェアラブル技術のフォームファクターと、それに関連するウェアラブルセンサー技術の機会を概観する。XR用センサー、モーションセンサー、光学センサーとイメージング、ウェアラブル電極、力、ひずみ、温度、化学センサーを調べ、医療、消費者、プロシューマー、産業用アプリケーションで比較する。

AIを活用するIoTセンサー

2025年、IoTの大きなトレンドは、コネクテッドセンサーからAIを活用したインテリジェントセンサーへの移行である。実際の操作データに基づいて構築・訓練されたAIモデルは、意思決定を自動化し、予測機能を提供するために、センサーやIoTソリューションに組み込まれつつある。エッジAIセンサー、デジタル・ツインニング、スマート・ウェアラブル・デバイスはすべて、生産性の向上を約束する重要な実現技術である。産業、環境、消費者向けIoTは、センサー・メーカーにとって引き続き重要なターゲットである。

産業用IoTセンサー技術の主な新興アプリケーションには、産業用ロボティクスとオートメーション、機械のヘルスモニタリングと予知保全、作業員の安全、在庫管理とロジスティクスが含まれる。産業用センサーソリューションからのデータインサイトは、プロセス効率の最適化、安全性の向上、運用コストの削減を実現します。本レポートでは、レガシーインフラの統合を含む、IoTセンサーアプリケーションが直面する歴史的な課題と、新たな成功事例に関するケーススタディを特徴付ける。

環境IoTソリューションで使用されるガスセンサー技術は、特に規制が強化される中、屋内の空気品質と屋外の汚染監視に依然として関連している。これらの用途以外にも、水素インフラのスケールアップは、安全性と漏れ検知、燃料電池車への燃料補給、定置型エネルギー用途でガスセンサーに新たな機会をもたらしている。本レポートでは、環境モニタリング、水素・メタン検知、PFAS検知に使用される光学式パーティクルカウンター、金属酸化物センサー、電気化学センサー、赤外線センサー、光イオン化検知器、光音響センサーなど、新たなガスセンサー技術を探る。

エッジ・センサ市場の離陸が始まる

低消費電力で高性能なコンピューティングは、デバイスのインテリジェンスと意思決定能力を高めるため、オンセンサでもインセンサでも、エッジへの統合が進んでいる。センサーに統合されたエッジ・コンピューティングは、しばしばエッジ・センシングと呼ばれ、実際の操作データに基づいて学習されたAIモデルがセンサー・データをリアルタイムで処理、解釈、処理することを可能にする。MEMS、ガス、画像センサーは、予知保全、自動品質検査、作業員の安全監視などのアプリケーションでエッジAIを統合する最初の技術の一つである。

IDTechExのレポートでは、新しいエッジセンサー技術、実現技術、主要メーカー、新興アプリケーションを分析し、成長市場の商業ロードマップを提供している。

高い成長機会をもたらす新興センサー技術の革新

IDTechExは、フォトニック集積回路、量子センサー、プリンテッドセンサー、イメージセンサーの進歩が成長を促進するため、新興センサー技術は2036年までに年平均成長率17%で成長すると予測している。

IDTechExの「センサー市場 2026-2036」レポートは、次世代MEMSセンサーをはじめ、市場に影響を与える主要センサー技術革新の包括的な概要を提供しています

主要な側面

10年間のセンサー市場予測&分析:

本レポートでカバーしているセンサーは以下の通りです

本レポートは、測定するセンサー技術を特徴づけています

目次1.要旨

1.1.センサー技術の紹介

1.2.主要センサー技術市場の概要

1.3.数十億ドル規模のエレクトロニクス企業の多くが、確立されたセンサー市場で競合しているが、その収益シェアはより専門的なプレーヤーに匹敵することもある

1.4.2024-2025年を通しての注目すべきセンサー市場の発展

1.5.2026~2036年の世界センサー市場全体予測:年間収益(米ドル、10億ドル)

1.6.2026~2036年の粒度別10年間のセンサー市場年間収益予測(米ドル、10億ドル)

1.7.新興センサーカテゴリーのセンサー市場規模予測とCAGR

1.8.動作原理、測定基準、製造形式の接続

1.9.2025年の世界イベントと技術メガトレンドがセンサー市場と需要に与える影響

1.10.将来市場における主要センサー技術革新とアプリケーションの概要

1.11.センサー技術市場のロードマップ

1.12. 主要センサー技術市場の2025年動向と発展

1.13.医療用とウェルネス用のウェアラブルデバイスの重複が進む

1.14.IoT技術のメタトレンドとセンサーへの影響

1.15.将来のモビリティ市場向けセンサーの要点

1.16.新興センサー市場:モビリティ向けセンサーの10年間市場シェア予測(2026~2036年)、年間収益(米ドル、百万ドル)

1.17.センサーのインテリジェント化が進み、エッジコンピューティングとAI機能を搭載したセンサーのシェアが拡大

1.18.センサー技術開発がインダストリー4.0のイノベーションを牽引し、センサーを活用した人間とロボットの協働がインダストリー5.0を生み出す

1.19.人型ロボットがロボット用センサーの新たな需要を牽引し、自動車と物流での採用が2030年までに成長機会をもたらす

1.20.自動化用センサーの進歩は自動車、産業、ロボット、航空宇宙、防衛の各市場でますます重なり合うようになる

2.市場予測

2.1.市場予測手法

2.1.1.市場予測方法論の概要

2.1.2.センサー市場予測に含まれるセンサー市場カテゴリー

2.1.3.主要センサーメーカーの年次報告書と財務諸表分析によるボトムアップセンサー市場サイジングの更新

2.2.市場予測

2.2.1.2026~2036年の世界センサー市場全体予測:年間売上高(米ドル、10億ドル)

2.2.2.2026~2036年の粒状10年センサー市場年間収益予測(米ドル、10億ドル)

2.2.3.新興センサーカテゴリーのセンサー市場規模予測とCAGR

2.2.4.確立されたセンサー市場10年間のガスセンサー技術予測(2026~2036年)、年間収益(米ドル、百万ドル)

2.2.5.確立されたセンサー市場:半導体センサー技術の10年予測(2026~2036年)、年間売上高(USD、百万ドル)

2.2.6.確立されたセンサー市場:自動車・航空宇宙用センサー技術の10年予測(2026~2036年)、年間売上高(USD、百万ドル)

2.2.7.確立されたセンサー市場:10年間のバイオセンサー技術予測(2026~2036年)、年間収入(米ドル、百万ドル)

2.2.8.新興センサー市場:10年間の新興イメージセンサー技術予測(2026~2036年)、年間収入(米ドル、百万ドル)

2.2.9.新興センサー市場:プリントセンサー技術の10年予測(2026~2036年)、年間売上高(米ドル、百万ドル)

2.2.10.新興センサー市場:フォトニック集積回路センサー技術の10年後予測(2026~2036年)、年間売上高(US$、百万ドル)

2.2.11.新興センサー市場:量子センサー技術の10年予測(2026~2036年)、年間収入(米ドル、百万ドル)

2.2.12.新興センサー市場:将来モビリティ向けセンサーの10年予測(2026~2036年)、年間売上高(US$、百万ドル);LiDAR、RADAR、CAMERA、IR、車内センサー

2.2.13.新興センサー市場:モビリティ向けセンサーの10年市場シェア予測(2026~2036年)、年間収益(US$、百万ドル)

2.2.14.センサー市場全体2026-2036年:年間収益(米ドル、百万ドル) - データ表

3.序章とセンサー市場の動向

3.1.センサー市場の概要

3.2.センサー技術の紹介

3.3.主要センサー技術市場の概要

3.4.数十億ドル規模のエレクトロニクス企業の多くが、確立されたセンサー市場で競合しているが、その収益シェアはより専門的なプレーヤーに匹敵することもある

3.5.2024-2025 年を通しての注目すべきセンサー市場の発展

3.6.代表的なセンサー技術製品カテゴリーの概要

3.7.動作原理、測定基準、製造形式の接続

3.8.新興センサー技術と既存センサー技術を分ける一般的傾向

3.9.2025 年の世界的な出来事と技術のメガトレンドがセンサー市場と需要に与える影響

3.10.主要センサー技術市場における 2025 年の市場動向

3.11.センサー技術市場のロードマップ

3.12.将来の市場における主要センサー技術の革新とアプリケーションの概要

3.13.AI、自律性、エネルギー、未来の航空、ロボット工学のメガトレンドへの注力を強調する市場リーダーのセンサー新製品発表

3.14.未来のモビリティにおけるメガトレンドとは?

3.15.未来のモビリティ技術におけるセンサーの役割とは?

3.16.クラウドからエッジへの移行に伴い、IoT市場のトレンドはエッジ・センシングに集中する

3.17.センサーはよりインテリジェント化し続け、エッジ・コンピュートとAI機能を搭載したセンサーのシェアは拡大する

3.18.センサー技術開発がインダストリー4.0のイノベーションを牽引し、センサーを活用した人間とロボットの協働がインダストリー5.0を生み出す

3.19.人型ロボットがロボット用センサーの新たな需要を牽引、自動車と物流での採用が2030年までに成長機会をもたらす

3.20.自動化用センサーの進歩は、自動車、産業、ロボット、航空宇宙、防衛の各市場でますます重複するようになる

3.21.ウェアラブル・センサー・イノベーションの展望

3.22.ウェアラブル技術におけるメガトレンドのロードマップ

3.23.6G の紹介と、5G と比較して期待されるセンシングの改善

3.24.モバイル通信以外の 6G アプリケーションの概要 - THz センシングとイメージングを含む

3.25.センシングにおけるmmWaveとTHz周波数の価値提案

3.26.センサー技術市場に関する主な結論技術とトレンド

4.次世代センサー技術の革新

4.1.はじめに

4.1.1.章概要と関連 IDTechEx レポート

4.2.新興イメージセンサー

4.2.1.4.2.2.新興イメージセンサー部門の概要新興イメージセンサー主要結論のまとめ

4.2.3.新興イメージセンサー主要プレーヤーの概要(I)

4.2.4.新興イメージセンサー主要プレーヤーの概要(Ⅱ)

4.2.5.SWIRイメージング:概要と主な結論

4.2.6.SWIRイメージング:新たな技術オプション

4.2.7.SWIRセンサー:アプリケーションと主要プレーヤー

4.2.8.OPD-on-CMOS ハイブリッドイメージセンサー:概要、結論、主要プレーヤー

4.2.9.OPD-on-CMOS 検出器:アプリケーション別技術準備レベルロードマップ

4.2.10.QD-on-Si/QD-on-CMOS イメージング:基礎、価値提案、主要結論

4.2.11.ハイパースペクトルイメージング:概要と主要結論

4.2.12.ハイパースペクトルイメージング:波長範囲とスペクトル分解能

4.2.13.小型分光計:概要と主な結論

4.2.14.小型分光器:幅広い分野をターゲットに

4.2.15.小型分光器:主要プレーヤーと主な差別化要因

4.2.16.イベントベースセンシング:概要と主な結論

4.2.17.イベントベースビジョン:アプリケーション要件

4.2.18.LiDAR:動作原理の概要

4.2.19.LiDAR:価値提案

4.2.20.LiDAR:技術的課題

4.2.21.LiDAR:エコシステムと主要プレーヤー

4.3.ガスセンサー

4.3.1.ガスセンサー部門の概要とアナリストの視点

4.3.2.ガスセンサー市場の「一覧」

4.3.3.ガスセンサー市場の概要:変化の原動力は?

4.3.4.金属酸化物(MOx)ガスセンサーの概要

4.3.5.MOxセンサーの主要メーカーの特定

4.3.6.MOxガスセンサーの主な結論とSWOT分析

4.3.7.電気化学式ガスセンサの紹介

4.3.8.電気化学センサーの主要メーカー

4.3.9.電気化学式ガスセンサの主要結論とSWOT分析

4.3.10.赤外線ガスセンサの紹介

4.3.11.赤外線ガスセンサー主要メーカーの特定

4.3.12.赤外線ガスセンサの主要結論とSWOT分析

4.3.13.光イオン化検出器(PID)の紹介

4.3.14.イオン化検出器メーカーの分類

4.3.15.光イオン化検出器の主な結論とSWOT分析

4.3.16.光学式パーティクルカウンター

4.3.17.光微粒子計数器の主要メーカーの特定

4.3.18.光学式パーティクルカウンターのSWOT分析

4.3.19.主な結論光学式パーティクルカウンター

4.3.20.感知原理:光音響

4.3.21.センシリオンとインフィニオンは小型光音響式炭酸ガスセンサを提供

4.3.22.光音響式ガスセンサのSWOT分析

4.3.23.センシングの原理E-Nose

4.3.24.E-ノーズのセンサータイプの利点と欠点

4.3.25.E-ノーズメーカーの分類

4.3.26.E-ノーズのSWOT分析

4.3.27.E-ノーズのまとめ:鼻よりも特定のアロマが好機

4.4.プリンテッド・フレキシブルセンサー

4.4.1.印刷・フレキシブルセンサー市場の紹介

4.4.2.プリンテッド・フレキシブルセンサー技術別主要要点

4.4.3.ピエゾ抵抗センサー:アプリケーションとプレイヤーの市場マップ

4.4.4.プリント圧電センサーが直面する課題

4.4.5.プリント圧電センサーの準備レベルのスナップショット

4.4.6.プリント型フレキシブル圧電センサーの結論

4.4.7.大面積フレキシブル・センシングにおける印刷光検出器の機会

4.4.8.サプライヤーの概要薄膜光センサー

4.4.9.印刷・フレキシブルイメージセンサーの結論

4.4.10.プリント温度センサーは熱管理用途で引き続き注目されている

4.4.11.プリント温度センサーのサプライヤー概要

4.4.12.プリント温度センサーとフレキシブル温度センサーの結論

4.4.13.プリント歪みセンサーの機会は、モーションキャプチャーのみならず、長期的にはバッテリー管理へと拡大する可能性がある

4.4.14.まとめ:ひずみセンサー

4.4.15.印刷ガスセンサー技術の展望

4.4.16.ITO コーティングの革新とインジウム価格の安定化が印刷型静電容量センサー成長市場に影響を与える

4.4.17.印刷静電容量式タッチセンサーの材料と技術の準備レベル

4.4.18.印刷型静電容量式センサーのコンフォーマルおよび曲面タッチセンシング用途が台頭

4.4.19.印刷型静電容量式タッチセンサーとフレキシブル静電容量式タッチセンサーの結論

4.4.20.ウェアラブル市場における印刷電極の機会

4.4.21.各印刷センサーカテゴリーのSWOT分析(I)

4.4.22.プリントセンサーカテゴリー別のSWOT分析(II)

4.4.23.プリントセンサーカテゴリー別SWOT分析(III)

4.4.24.プリントセンサー技術の主要成長市場のまとめ

4.4.25.自動車のメガトレンドとプリントセンサの機会

4.4.26.プリントセンサーは飽和した製品市場で差別化を提供しなければならない

4.4.27.医療用ウェアラブルにおけるプリントセンサー技術の商業化

4.4.28.主要プレーヤーのターゲット市場は、利用可能な商業化戦略のスペクトルを浮き彫りにする

4.5.シリコンフォトニクス

4.5.1.フォトニック集積回路(PIC)とは?

4.5.2.電子集積回路とフォトニック集積回路の比較

4.5.3.PICセンサーの可能性:バイオメディカル

4.5.4.PICバイオセンサーを開発する市場プレーヤー

4.5.5.ロックレー・フォトニクスIP売却とPIC関与の終了の可能性

4.5.6.PICセンサーの機会:ガスセンサー

4.5.7.PIC ベースのガスセンサーを開発する市場プレーヤー

4.5.8.PIC センサーのビジネスチャンス:構造ヘルスセンサー

4.5.9.分光 PIC を開発する市場プレイヤー

4.5.10.車載用 LiDAR

4.5.11.PIC センサーのビジネスチャンス:LiDAR センサー

4.5.12.LiDAR の中核的側面

4.5.13.PICベースLiDARを開発する市場プレイヤー(1)

4.5.14.PICベースLiDARを開発する市場プレイヤー(2)

4.5.15.LiDARの波長と材料の動向

4.5.16.PICベースFMCW LiDARの主な課題

4.5.17.車載用電子鼻

4.6.量子センサー

4.6.1.量子センサーとは?

4.6.2.量子センサー市場「一覧」

4.6.3.量子センサー:アナリストの視点

4.6.4.量子センサーの価値提案はハードウェアアプローチ、アプリケーション、競合によって異なる

4.6.5.量子センサー産業市場マップ

4.6.6.量子センサーの主要産業

4.6.7.原子時計はクロック・ドリフトを自己校正する

4.6.8.原子時計SWOT分析

4.6.9.原子時計セクターロードマップ

4.6.10.感度が量子磁場センサーの価値提案の鍵

4.6.11.光励起磁力計(OPM)の動作原理

4.6.12.光励起型磁力計:SWOT分析

4.6.13.NVセンター磁界センサーの紹介

4.6.14.N-V中心磁場センサー:SWOT分析

4.6.15.量子磁力計:セクターロードマップ

4.6.16.量子重力計の概要

4.6.17.原子干渉法による量子重力計の動作原理

4.6.18.量子重力計SWOT分析

4.6.19.量子重力計セクターロードマップ

4.6.20.原子量子ジャイロスコープの動作原理

4.6.21.MEMS 製造プロセスにより、原子ジャイロスコープ技術を小型化し、より大量に応用できる

4.6.22.慣性量子センサー:セクター・ロードマップ

4.6.23.量子 RF センサーの価値提案

4.6.24.量子 RF センサーの種類の概要

4.6.25.量子 RF センサー:セクターロードマップ

4.6.26.単一光子検出器の紹介

4.6.27.単一光子イメージングと量子イメージング - 3つの主要トレンド

4.6.28.単一光子検出器セクターロードマップ

4.7.バイオセンサー

4.7.1.バイオセンサーのレイアウト

4.7.2.バイオレセプター:各タイプの利点と欠点

4.7.3.光トランスデューサー:各タイプの利点と欠点

4.7.4.電気化学変換器:各タイプの利点と欠点

4.7.5.ポイントオブケアにおけるバイオセンサーの応用

4.7.6.体外診断

4.7.7.成長する体外診断用医薬品市場

4.7.8.ポイントオブケア検査の価値

4.7.9.ポイントオブケア検査(POCT)に向かう体外診断薬

4.7.10.ラテラルフローアッセイのメカニズム

4.7.11.一体型カートリッジによるサンプルハンドリングの最小化

4.7.12.POCTデバイスのバリューエコシステム

4.7.13.市場ダイナミクス

4.8.ナノカーボンセンサー

4.8.1.グラフェン - はじめに

4.8.2.電子基板としてのグラフェンと化学気相成長(CVD)グラフェンの生産

4.8.3.グラフェン・ウェハーの生産能力と採用の拡大

4.8.4.グラフェンを用いたセンサーの産業事例

4.8.5.組み込み型SHM用ナノカーボンセンサー

4.8.6.グラフェン・センサー - ガスセンサー

4.8.7.グラフェン・センサー - ガスセンサー(2)

4.8.8.食品安全モニタリング用グラフェン・センサー

4.8.9.バイオセンサー - 電気化学トランスデューサの概要

4.8.10.グラフェンを用いたバイオFET

4.8.11.グラフェンを用いたバイオセンサー

4.8.12.ホール効果センサー

4.8.13.高速グラフェン光センサー

4.8.14.グラフェンを利用した光検出器の商用例

4.8.15.シリコンフォトニクスにおける新たな役割

4.8.16.グラフェン・フォトニクスの新興企業

4.8.17.グラフェン中間層を用いたQD-on-CMOS

4.8.18.グラフェンを用いた光脳センサー

4.8.19.グラフェン皮膚電極

4.8.20.カーボンナノチューブ(CNT)

4.8.21.ガスセンサーにおけるCNT:概要

4.8.22.CNTベースのガスセンサー - C2Sense

4.8.23.CNTベースのガスセンサー - AerNos

4.8.24.CNTベースのガスフィンガープリント用電子ノーズ(PARC)

4.8.25.カーボンナノチューブを使った印刷湿度・水分センサー

4.8.26.CNT 温度センサー(Brewer Science)

4.8.27.CNTを用いたLiDARセンサー

4.8.28.センサーにおける炭素材料の展望

4.9.次世代MEMSセンサー

4.9.1.MEMSとは?

4.9.2.センシングにおける次世代MEMS

4.9.3.慣性計測装置(IMU)の概要

4.9.4.慣性航法システム(INS)の技術状況

4.9.5.IMUのアプリケーショングレード

4.9.6.IMU市場の展望

4.9.7.MEMS加速度センサーの概要

4.9.8.加速度計アプリケーションの概要

4.9.9.次世代MEMS加速度センサーの産業展望

4.9.10.幾何学的アンチスプリング加速度ピックアップ

4.9.11.共振ビーム加速度ピックアップ

4.9.12.熱MEMS加速度ピックアップ

4.9.13.ウィスパリング・ギャラリー・モード共振器

4.9.14.MEMS加速度センサーの産業動向

4.9.15.ジャイロスコープ技術の展望

4.9.16.MEMSマクロスケールの半球共振ジャイロ(HRG)

4.9.17.μHRGの製造方法の概要

4.9.18.μHRGの商業活動

4.9.19. μHRGはMEMSジャイロに大きな飛躍をもたらす

5.エッジセンシングとAI

5.1.エッジセンシングはじめに

5.1.1.エッジセンシング概要

5.1.2.エッジセンシングとは

5.1.3.新たなセンサーアプリケーションにおけるエッジコンピューティングとクラウドコンピューティング

5.1.4.エッジセンシングの台頭は、クラウドコンピューティングからエッジコンピューティングへの広範な業界シフトに追随している

5.1.5.エッジセンシングの市場促進要因

5.2.エッジセンシング:技術

5.2.1.エッジセンサー:技術的内訳と主要コンポーネント

5.2.2.エッジセンシングのモノのインターネットアーキテクチャ

5.2.3.クラウド、エッジ、エンドポイント・センシングと関連する実現技術の評価

5.2.4.高効率コンピューティング・ハードウェアがエッジセンシングを解き放つ

5.2.5.エッジ・センサ・デバイスには低消費電力設計が不可欠

5.2.6.ケーススタディ:低消費電力エッジセンサー資産トラッカー

5.2.7.エッジセンシングとエッジAIは収束しつつあり、予測・予見機能を解放する

5.2.8.エッジAIはエンドポイントデバイスでのデータ処理と推論を可能にする

5.2.9.エッジAIはカメラモジュール上で画像の分類と処理を可能にする

5.2.10.オンチップのエッジAIイメージセンサーが早期に商業販売を獲得

5.2.11.エッジAI対応カメラモジュールの応用

5.2.12.エッジセンサーが直面する課題

5.3.エッジセンシング:市場とアプリケーション

5.3.1.エッジセンサー:市場概要

5.3.2.ビル自動化によるスマートビルのエネルギー効率改善の機会

5.3.3.エッジセンサーによる低消費電力居住モニタリングとスマートセキュリティ

5.3.4.エッジセンシングが産業用 IoT における予知保全を解き放つ

5.3.5.ケーススタディアナログ・デバイセズ - 予知保全エッジAIセンサー

5.3.6.予知保全ハードウェアとソフトウェアの主要サプライヤー

5.3.7.産業用IoTにおけるセンサーの進化する役割のロードマップ

5.3.8.エッジセンサーは遠隔地や危険な場所での作業場の安全性を向上させる

5.3.9.エッジAI対応センシングで構造ヘルスモニタリングの洞察がより豊かに

5.3.10.エッジAIによる品質検査と異常検知

5.3.11.ウェアラブルにおけるAI対応エッジセンシング

5.3.12.エッジセンサーとエッジAIは、既存の家電アプリケーションとスマート小売における革新の継続を約束する

5.3.13.エッジセンシング・アプリケーション要件の評価

5.3.14.主要エッジセンサー市場:新たなアプリケーション、機会、脅威

5.4.エッジセンシング結論

5.4.1.エッジセンサー技術と市場展望のまとめ

5.4.2.エッジセンサー・アプリケーションの技術準備レベル

5.4.3.エッジセンサーとエッジAIのSWOT分析

5.4.4.エッジセンシングの主要企業:センサーと製品インテグレーター

5.4.5.エッジセンシングの主要プレイヤー:IC、SoC、クラウドサービスサプライヤー

6.ウェアラブルセンサー

6.1.ウェアラブルセンサーの概要

6.1.1.ウェアラブル・センサーのセクションとテクノロジー・ランドスケープの概要

6.1.2.ウェアラブル技術には様々な形態がある

6.1.3.ウェアラブル・センサー・タイプの概要

6.1.4.フォームファクター、ウェアラブルセンサー、メトリクスの接続

6.1.5.ウェアラブルセンサー技術のロードマップ(1)

6.1.6.ウェアラブルセンサー技術のロードマップ(主要バイオメトリクス別)

6.1.7.医療用とウェルネス用のウェアラブルデバイスの重複が増加

6.2.ウェアラブルモーションセンサー

6.2.1.ウェアラブルモーションセンサー:はじめに

6.2.2.スマートウォッチ用IMU:主要プレーヤーと業界動向

6.2.3.ウェアラブル地磁気センサーのサプライヤーと業界動向

6.2.4.ウェアラブルモーションセンサーの新たなユースケースの概要

6.2.5.ウェアラブルモーションセンシング用MEMSベースIMU:SWOT分析

6.2.6.ウェアラブルモーションセンサー:セクターロードマップ

6.2.7.ウェアラブルモーションセンサー結論

6.3.ウェアラブル光学センサー

6.3.1.ウェアラブル光学センサーはじめに

6.3.2.ウェアラブル光学センサー光電式容積脈波(PPG)

6.3.3.ウェアラブル用光学部品の主要メーカー

6.3.4.ウェアラブルPPG:アプリケーションと主要プレーヤー

6.3.5.ウェアラブル心拍数:使用例、機会、サンプルプレーヤー

6.3.6.ウェアラブル光学センサー:PPGからの血中酸素の取得

6.3.7.ウェアラブル光学センサー:パルスオキシメトリーの市場展望と技術準備

6.3.8.ウェアラブル光センサー非侵襲的血圧測定の進展

6.3.9.カフレス血圧の技術概要

6.3.10.ウェアラブル光学センサー:心拍数、脈拍、血圧、グルコースモニタリングのSWOT分析

6.3.11.ウェアラブル光学センサー:主な結論

6.4.ウェアラブル電極

6.4.1.ウェアラブル電極:主なタイプの概要

6.4.2.ウェアラブル電極:湿式と乾式

6.4.3.EEG用ドライ電極の材料イノベーション

6.4.4.BCIアプリケーションのためのEEGのデバイスレベル統合:ドライ電極を使用するフォームファクターと主要プレーヤー

6.4.5.マイクロニードル電極

6.4.6.ウェアラブル電極:電子スキン(「表皮エレクトロニクス」とも呼ばれる)

6.4.7.ウェアラブル電極:用途と製品タイプ

6.4.8.電子テキスタイル、皮膚パッチ、時計におけるウェアラブル電極の主要プレーヤー

6.4.9.ウェアラブル電極:連結SWOT分析

6.4.10.ウェアラブル電極主な結論

6.5.ウェアラブル温度センサー

6.5.1.ウェアラブルにおける温度センサーの2つの主な役割

6.5.2.温度センサーの種類

6.5.3.ウェアラブル体温センサーの主要プレーヤー、フォームファクター、アプリケーション

6.5.4.ウェアラブル体温センサーのマッピング

6.5.5.ウェアラブル体温センサーSWOT分析

6.5.6.ウェアラブル体温センサー:主な結論

6.6.ウェアラブル化学センサー

6.6.1.ウェアラブル化学センサー概要

6.6.2.ウェアラブル化学センサー:分析物の選択と入手可能性

6.6.3.ウェアラブル化学センサー典型的なCGMデバイスの動作原理

6.6.4.CGM:主要企業の概要

6.6.5.ウェアラブルグルコースセンサー:化学物質と代替物質のSWOT分析

6.6.6.ウェアラブル化学センサー:グルコースセンシングのロードマップと主要結論

6.6.7.ウェアラブル化学センサー:ウェアラブルアルコールセンサーの使用事例、利害関係者、主要プレーヤー、SWOT分析

6.6.8.ウェアラブル化学センサー:ウェアラブル乳酸/乳酸センサーの使用事例、関係者、主要プレーヤー、SWOT分析

6.6.9.ウェアラブル化学センサー:ウェアラブル水分センサーの使用事例、利害関係者、主要プレーヤー、SWOT分析

6.6.10.新規バイオメトリクス用ウェアラブルセンサーの市場準備

6.6.11.新規バイオメトリクス用ウェアラブルセンサー:主要結論

6.7.XRデバイス用ウェアラブルセンサー

6.7.1.VR、AR、MR、XRとは何か?

6.7.2.コントローラとセンシングはARとVRデバイスを環境とユーザーにつなぐ

6.7.3.位置トラッキングを超えて:XRヘッドセットは他に何をトラッキングするのか?

6.7.4.XRセンサーはどこにあるのか?

6.7.5.3Dイメージングとモーションキャプチャー

6.7.6.深度センシング用飛行時間(ToF)カメラ

6.7.7.AR/VRへの応用を狙う低消費電力イメージセンサー

6.7.8.3Dセンシング用低消費電力飛行時間センサー

6.7.9.構造化光

6.7.10.XRアプリケーション向け3Dイメージング技術の比較

6.7.11.XR用センサー:位置と動きのトラッキング、セクターロードマップ

6.7.12.ウェアラブル・ジェスチャー・コントロール - 主な結論

6.7.13.なぜAR/VRデバイスで視線追跡が重要なのか?

6.7.14.視線追跡センサーのカテゴリー

6.7.15.マシンビジョンとカメラを使ったアイトラッキング

6.7.16.従来のNIRカメラとマシンビジョンソフトウェアに基づくアイトラッキング企業

6.7.17.XR用センサー:AR/VRアイトラッキング用イベントベースビジョン

6.7.18.レーザースキャニングMEMSによるアイトラッキング

6.7.19.視線の動きの静電容量センシング

6.7.20.XR向けアイトラッキング:セクター・ロードマップ

7.将来のモビリティ市場向けセンサー

7.1.将来のモビリティ向けセンサーの紹介

7.1.1.未来のモビリティのメガトレンドとは?

7.1.2.未来のモビリティのためのセンサー各章の概要

7.1.3.未来のモビリティ・アプリケーションにおけるセンサーの概要と展望

7.1.4.主な結論将来のモビリティ市場向けセンサー

7.2.電動化のためのセンサー

7.2.1.電気自動車:基本原理

7.2.2.電流、電圧、時間、温度のモニタリングはBMS機能の中核

7.2.3.バッテリ管理システムの動向 - 状態推定の高度化に最も関連するセンサ

7.2.4.センサーはEV充電インフラで進化する役割を果たす

7.2.5.EVの台頭により、ガスセンサの役割は排出ガス試験からバッテリー管理へとシフトする可能性がある

7.2.6.先進的センサーの導入が解決する問題

7.2.7.電池監視におけるガスセンサの価値提案:早期熱暴走検知

7.2.8.規制の背景:電気自動車

7.2.9.電気自動車用センサーのベンチマーク

7.3.自動化のためのセンサー

7.3.1.自動車における自動化のSAEレベル

7.3.2.ビッグ3センサー

7.3.3.高い自動化レベルは車両当たりのセンサー数を増やす

7.3.4.レベル1からレベル4までのセンサースイートの進化

7.3.5.センサースイートのコスト

7.3.6.車両カメラのアプリケーション

7.3.7.IRスペクトルとアプリケーション

7.3.8.主要なSWIRイメージセンサー技術の技術比較

7.3.9.車載におけるLWIR

7.3.10.非冷却センサー材料の選択

7.3.11.ADAS 向け LWIR:利点と欠点

7.3.12.LWIR の潜在的普及に影響を与える主な法律

7.3.13.Autoliv、Veoneer、Magna ナイトビジョン・ジェネレーション

7.3.14.フロントレーダーとサイドレーダーの用途

7.3.15.レーダーの動向:台数と設置面積

7.3.16.より高度な半導体技術の採用が自動車用レーダーの進歩の鍵を握る

7.3.17.車載用LiDAR

7.3.18.車載用LiDAR:要件

7.3.19.レーダーかLiDARか

7.4.車内センシング(または車内モニタリングシステム)

7.4.1.車内モニタリングにおけるDMSとOMSシステムの概要

7.4.2.SAEレベル1からレベル4までのDMSセンサーの進化

7.4.3.車室内モニタリングシステム(IMS)の最新技術

7.4.4.技術の分類:ドライバー・モニタリング・システム(DMS)

7.4.5.OEM別車室内センサーの概要(1)

7.4.6.OEM別車載センサーの概要(2)

7.4.7.DMSにおける赤外線(IR)カメラ

7.4.8.トレンド - ADAS を備えたミラーやディスプレイへの統合

7.4.9.潜在的な統合分野

7.4.10.DMS用ToFカメラ - 原理

7.4.11.ToF イメージングセンサー:解像度と価格のベンチマーク

7.4.12.車載レーダーの比較

7.4.13.DMSにおける静電容量式センサーの現状

7.4.14.HOD用トルクセンサー - 動作原理

7.4.15.キャビン内センシングの主要センサー動向

7.4.16.車内センシング技術の概要

7.5.コネクテッド・ビークルとソフトウェア・デファインド・ビークルのためのセンサー

7.5.1.ソフトウェア定義車両レベルガイド

7.5.2.コネクテッド・ビークルの主要用語

7.5.3.特定の V2V/V2I のユースケースは、コネクテッドカーと自律性の相互作用を強調するものであり、そのようなものとしてセンサーの役割を強調するものである

8.モノのインターネット(IoT)のためのセンサー

8.1.IoT の概要

8.1.1.モノのインターネット(IoT)とは何か?

8.1.2.センサーは IoT プラットフォームの中の一要素に過ぎない

8.1.3.新たなIoT市場とアプリケーション

8.1.4.IoT 技術のメタトレンドとセンサーへの影響

8.2.産業用 IoT(IIoT)

8.2.1.産業用 IoT:はじめに

8.2.2.産業トレンドとインダストリー 5.0

8.2.3.センサー技術の産業用 IoT アプリケーション

8.2.4.IIoT センサー産業用ロボットとオートメーション

8.2.5.ロボットにおけるセンサーの応用

8.2.6.物体検出用センサー

8.2.7.ナビゲーションと衝突検知センサーの比較:LiDAR、レーダー、カメラ、1D/3D超音波センサー

8.2.8.ナビゲーションとマッピングセンサー

8.2.9.LiDAR、レーダー、カメラ、超音波センサーの比較 - (1)

8.2.10.LiDAR、レーダー、カメラ、超音波センサーの比較 - (2)

8.2.11.市販または開発中の各種 LiDAR の性能比較

8.2.12.カメラの紹介

8.2.13.SWOT-RGB/可視光カメラ

8.2.14.ロボット工学におけるレーダーとLiDAR

8.2.15. 人型ロボットの周囲を感知する3D視覚システム

8.2.16.ヒューマノイドロボットにおけるカメラとLiDARの展望

8.2.17.近接センサの検出原理の紹介

8.2.18.近接センサの比較

8.2.19.力センサーとトルクセンサー - はじめに

8.2.20.様々なトルクセンサと力センサの比較

8.2.21.ヒューマノイドロボット用触覚センサー

8.2.22.触覚センサーの技術別ベンチマーク

8.2.23.Paxini - ヒューマノイドロボット指用触覚センサー

8.2.24.触覚センサーのまとめ

8.2.25.IIoT センサー:機械のモニタリングと予知保全

8.2.26.機械のヘルスモニタリングと予知保全におけるセンサー

8.2.27.機械のヘルスモニタリング用インジケータ

8.2.28.機械のヘルスモニタリングのための振動センシング

8.2.29.機械のヘルスモニタリングと予知保全の新技術

8.2.30.IoT におけるデジタル・ツインニングと仮想環境が遠隔操作と自動化を可能にする

8.2.31.IIoT センサー労働者の安全

8.2.32.産業職場の安全のコスト

8.2.33.ウェアラブルセンサーは遠隔地や危険な場所での作業安全性を向上させる

8.2.34.水分補給モニタリング用に登場した印刷型ウェアラブルセンサー

8.2.35.IIoT センサー:在庫管理と物流

8.2.36.資産追跡のための IIoT センサー

8.2.37.RFIDセンサーの種類

8.2.38.RFID センサー:主な選択肢

8.2.39.IIoT は低消費電力センサーの需要を促進し、エネルギーハーベスティングの機会を提供する

8.2.40.低消費電力センサーは資産追跡装置のバッテリー寿命を大幅に延ばす

8.2.41.IIoT センサーはエネルギーハーベスティングによって自己発電できる

8.2.42.エネルギーハーベスティング IIoT センサー:太陽エネルギーと運動エネルギーによるアプローチ

8.2.43.無線周波数エネルギーハーベスティングは無線給電センサーを可能にする

8.2.44.在庫管理システム用のプリント力センサー

8.2.45.IIoT センサー:結論と展望

8.2.46.IIoT センサー:主な結論とアナリストの見解

8.2.47.IIoT におけるセンサーの機会と脅威のまとめ

8.2.48.既存センサーメーカーと新興センサーメーカーの IIoT 展望

8.2.49.IIoT が直面する市場の課題

8.2.50.センサーは産業用IoTの長い投資回収期間への影響が小さい

8.2.51.IIoT バリューチェーンと主要プレーヤー

8.3.環境モニタリング IoT

8.3.1.IoT における環境ガスセンサー市場の概要

8.3.2.屋外汚染モニタリングの主要分析物

8.3.3.屋外の大気質に関する規制強化や勧告により、高感度ガスセンサーへのニーズが高まっている

8.3.4.規制値を監視するために技術はどのように使われるのか?

8.3.5.都市排出ガス監視用センサー

8.3.6.屋外汚染監視は「スマートシティ」におけるガスセンサーの機会を生み出す

8.3.7.既存技術の課題-固定監視ステーションは大規模で高価である

8.3.8.屋外汚染モニタリングのための主要な小型ガスセンサー技術

8.3.9.屋外の大気質モニタリング「ノード」における小型ガスセンサの役割

8.3.10.スマートシティ向けの大気質モニタリングは、小型ガスセンサー技術の市場規模が比較的小さい

8.3.11.規制圧力の欠如が屋外汚染モニタリング用小型ガスセンサの採用を制限している

8.3.12.都市部での屋外汚染モニタリング用低コストガスセンサの採用拡大にはインフラ整備が不可欠

8.3.13.屋外汚染モニタリングのためのモバイルプラットフォームは、超ローカルなデータ収集のためのセンサネットワークに代わる、より効率的なものとして台頭しつつある

8.3.14.エネルギー部門の排出量モニタリング用センサー

8.3.15.産業市場では、スマートシティと比較して、低コストのガスセンサーノードのビジネスケ ースが明確になる

8.3.16.メタンの検知は安全、環境、規制遵守のために極めて重要

8.3.17.メタン検知のためのイメージング技術の概要と自動化・定量化に伴う課題

8.3.18.次世代単光子アバランシェ・ダイオード(SPAD)の革新

8.3.19.シリコンの範囲を超える赤外波長を解き放つ代替半導体 SPAD

8.3.20.コア環境ガスセンサー技術の主要仕様の比較

8.3.21. ガス安全市場における期待の高まりが新技術採用の原動力

8.3.22.メタン検知用の新型センサー:センシリオンとインフィニオンは小型化した光音響式メタンセンサーを提供

8.3.23.移動プラットフォームとしてのドローン:産業、農業、法執行のための小型軽量ガスセンサー

8.3.24.水素ガス検知アプリケーションの展望

8.3.25.水素漏れは危険なリスクをもたらし、検出が必要である

8.3.26.水素リーク検知は、光検知器、超音波センサー、電気化学センサーを用いて実現できる

8.3.27.その他の注目すべき水素検知アプリケーション

8.3.28.水素経済におけるセンシングの機会

8.3.29.屋外汚染モニタリング用ガスセンサー市場マップとバリューチェーン

8.3.30.屋外汚染モニタリング用小型ガスセンサー:結論と展望

8.3.31.屋内空気品質モニタリングの主要分析物

8.3.32.室内汚染に関連する健康リスクの概要

8.3.33.屋内空気汚染は、規制にもかかわらず、高所得国では依然として重大な健康リスクである

8.3.34.北半球では換気不足がラドンのリスクを増大させる

8.3.35.ガスセンサー技術は現在、室内空気質への取り組みにどのように利用されているか?

8.3.36.スマートビルディング」の価値提案とセンサー要件の概要

8.3.37.スマートビルディング市場のセグメント化

8.3.38.ガスセンサー市場における技術タイプ別ベンチマーキング機会

8.3.39.スマートビルディング市場におけるガスセンサー機会への室内空気品質規制の影響(2)

8.3.40.健康ビル」基準における空気品質重視がスマートビル市場の成長を徐々に促進

8.3.41.スマートビルにおける火災安全性 - ガスセンサーに依存するが、新技術の採用には高い障壁がある

8.3.42.室内空気質に関するビル管理システムの概要

8.3.43.スマートビルディングにおける室内空気品質:市場概要とガスセンサーによる機会

8.3.44.専門家による空気品質管理サービスはどのように差別化されているか?

8.3.45.スマートビルの屋内空気品質モニタリングは屋外汚染センシングよりも市場規模が大きい

8.3.46.スマートビルの室内モニタリング用小型ガスセンサー:結論と展望

8.3.47.PFAS用センサー - 概要

8.3.48.PFASの紹介

8.3.49.PFASの確立された応用分野

8.3.50.PFASの概要:非ポリマーとポリマーの区分

8.3.51.飲料水中のPFASの世界的規制値:概要

8.3.52.PFASモニタリングと安全飲料水限界に関する規制

8.3.53.各国における個々のPFASの最大汚染物質限度(MCL)

8.3.54.PFASの悪影響に関する懸念の高まり

8.3.55.既存の装置ベースの方法の限界とセンサーの必要性

8.3.56.商業的PFASセンサー開発における課題:永遠の化学物質は本質的に検出が難しいクラスである

8.3.57.PFAS センサー・ソリューション開発者

8.3.58.通販検査キットとの競争

8.4.消費者向けIoT:スマートホーム(大気質センサー)

8.4.1.スマートホーム技術のOEMはまだ「主流」になることに賭けている

8.4.2.室内空気品質モニタリングのスマートホーム市場の紹介

8.4.3.OEMはどのようにしてポストコビッドの室内空気品質モニターの大衆市場にアクセスできるのか?

8.4.4.スマートホーム空気品質モニターの技術仕様の比較

8.4.5.スマート清浄機は空気環境悪化の解決策としてますます人気が高まっている

8.4.6.市場リーダーは粒子状物質センサーを製品に含める

8.4.7.空気品質とモノのインターネット

8.4.8.室内空気清浄製品のどのビジネスモデルが持続可能か?

8.4.9.ウェルネス・フィットネス・モニタリングにおける空気品質モニタリングの機会

8.4.10.空気品質規制とテクノロジーの関係

8.4.11.スマートホームの室内空気品質モニタリング:市場マップと展望

8.4.12.IAQモニタリング用スマートホーム技術の機器コストの比較

8.4.13.スマートホームにおける室内空気品質デバイスの課題

8.4.14.スマートホームにおける室内モニタリング用小型ガスセンサー:結論と展望

9.企業プロフィール

9.1.AMS オスラム

9.2.Arbe:4Dイメージング・レーダーのリーダー

9.3.アーム

9.4.アーティラックス社

9.5.ボッシュ・センサーテック

9.6.ボッシュ・センサーテック(ウェアラブルセンサー)

9.7.ボストンエレクトロニクス

9.8.カナトゥ

9.9.CPI EDB(量子センシング)

9.10.Datwyler(ドライ電極)

9.11.デックスコム

9.12.ドラキュラ・テクノロジーズ

9.13.イヤスイッチ

9.14.エムテック・リミテッド

9.15.エネルギア・マイクロバードバス共振ジャイロスコープ

9.16.エピコア・バイオシステムズ

9.17.エクセリタス

9.18.FLEXOO

9.19.フラウンホーファーCAP

9.20.ヒナリア・イメージング

9.21.ハネウェル - BESSセンサー

9.22.ハネウェル・エアロスペース・テクノロジーズ新しいMEMS IMU

9.23.ハネウェル熱管理用先進センサー

9.24.アイメック

9.25.インフィテックス

9.26.イノセイズ・センサ・テクノロジーズナノG MEMS加速度センサー

9.27.マテリジェントGmbH

9.28.Meta(ニューラル・インターフェイス・リストバンド)

9.29.モービルアイ自動車用レーダー

9.30.村田製作所

9.31.車載レーダーと湿度センサー

9.32.ニューラルリンク

9.33.NIQS Technology Ltd.

9.34.ペラテック

9.35.フォトンフォース

9.36.フォトロン

9.37.ポラリトン・テクノロジーズ

9.38.ポジファ・テクノロジーズバッテリーパック用ガスセンシング

9.39.パワーキャスト

9.40.Q-CTRL(量子ナビゲーション)

9.41.QDIシステムズ

9.42.センセル

9.43.センセオニクス

9.44.Sensirion - バッテリー管理システム用先進センサー

9.45.シーメンス・ヘルティニアーズ

9.46.シリコン・マイクログラビティ社:MEMS加速度計と重力計

9.47.シルバレイ

9.48.ソニーセミコンダクタソリューションズエッジAIイメージセンサー

9.49.STマイクロエレクトロニクス

9.50.蘇州山河光電子科技有限公司

9.51.TDK(受動部品)

9.52.TDK SensEI

9.53.テレダイン・フリアー

9.54.テミ・グローバル

9.55.ウェーブアイ画像レーダーへのコスト効率の高いアプローチ

9.56.ウェアラブルデバイス

9.57.Wisear

9.58.ザブベオフォトニクスに基づくレーダーのパラダイムシフト

Summary

Global sensor market including future mobility, LiDAR, radar, cameras, IR; MEMS, wearables; AI, edge sensors; quantum sensors; printed sensors; gas sensors; battery sensors; silicon photonics, image sensors, with 10-year granular sensor market forecast

Sensor technology market to grow to US$250 by 2036

IDTechEx forecasts that the global sensor market will reach US$250B by 2036 as global mega-trends in mobility, AI, robotics, 6G connectivity and IoT drive sensor demand. IDTechEx's Sensors report provides extensive analysis of the global sensor market, including 58 company profiles and insights collected from over 20 related sensor reports. Summarizing IDTechEx's extensive sensors report portfolio, this research contains over 35 sensor technology SWOT analyses, 24 technology readiness level roadmaps, material requirements and supplier information across future mobility, IoT, wearables, biomedical, edge computing, environmental sensing and more. This sensor market analysis includes updated granular ten-year sensor forecasts, segmented by sensor technology.

Ten-year global sensor market forecast (2026-2036), segmented by sensor technology. Source: IDTechEx.

Hundreds of millions of sensors are produced each year and are ubiquitously used in communications, transport, industry, healthcare, energy, consumer, and buildings applications. While sensors themselves only compose a fraction of the annual revenue generated by major electronics companies, sensor technology nevertheless represents a multi-billion-dollar global market.

In 2026, mature sensor technologies will continue dominating the market. IDTechEx finds that optical sensors, semiconductor sensors (including MEMS), biosensors and conventional transducers represent 85% of total sensor market revenue in 2026. Established sensor technology has mature applications in most market verticals, including aerospace, automotive, industrial, consumer, healthcare, environmental markets.

Despite slowing of established sensor revenue growth within mature markets, manufacturers increasingly look towards new sensor technology and emerging applications to drive growth. Mega-trends driving sensor innovation today include artificial intelligence (AI) and data centers, internet-of-things (IoT), Industry 4.0 and robotics, future mobility (autonomy, electrification and driver monitoring), wearable technology adoption and the commercialization of 6G. IDTechEx forecasts that sensor growth in emerging markets will drive global sensor revenue to grow at a 5.2% CAGR through 2036, driven primarily by emerging sensor technologies and applications.

Overview of global sensor technology market and applications in 2026. Source: IDTechEx.

IDTechEx's research tracks how emerging technologies in key sensor markets are evolving. Sensor design trends focus on improved integration and performance within products and applications using technologies in printed electronics, photonic integrated circuits, and next-generation MEMS. Emerging sensor technologies will compete through reduced size and power, ability to measure more metrics, improved sensitivity and accuracy, and through new form-factors.

IDTechEx's report, "Sensor Market 2026-2036: Technologies, Trends, Players, Forecasts", extensively evaluates innovations in sensor technology and emerging application markets. This report covers emerging sensors technology markets in quantum sensors, printed sensors, nanocarbon sensors, image sensors, ADAS sensors, and more.

Future mobility continues to reshape sensor demand in vehicles

Vehicle electrification, automation, in-cabin monitoring, and software defined vehicles (SDV) continue to evolve automotive sensor demand. Emerging future mobility trends are creating broad opportunities across various sensor technologies. Advanced EV battery pack sensors will use temperature, current, voltage and gas sensors for battery monitoring, while LiDAR, radar, infrared imaging and camera technology are central to advanced driver assistance systems (ADAS).

Driver monitoring systems (DMS), and in the future passenger monitoring, are becoming increasingly mandated in several regions, driving growth for in-cabin sensors. With gaze tracking a key metric, sensors such as infrared (IR), time-of-flight (ToF), and radar are emerging for driver monitoring in ADAS systems, to check if the driver is still focused on the road. In the future, in-cabin sensing technologies may also be used for biometric authentication to enable features-as-a-service business models in connected software defined vehicles.

IDTechEx's research evaluates and benchmarks sensors for future mobility, identifying LiDAR and thermal imaging sensor segments as growth opportunities, set to represent 26% of automotive sensor revenue by 2036. This report identifies and critically evaluates emerging future mobility technology, applications, requirements, and demand.

Sensors for robotics, Industry 4.0 and Industry 5.0

In 2025, sensor technology is at the nexus of advancements in robotics, AI, and automation. From edge AI and IoT sensors for connected devices and equipment, to collaborative robots and humanoid robots, sensor technology innovations are central to future industrial automation solutions.

Cameras, LiDAR, ultrasonic sensors, IMUs, force, torque and tactile sensors are all crucial for navigation, localization, proximity detection, and actuation tasks in industrial, collaborative, and humanoid robotics.

Over the next decade, sensors for automation are set to have significant impact across automotive, industrial, manufacturing, aerospace and defense applications. Key challenges for Industry X.0 technologies remain long return on investment timelines and bespoke application requirements. IDTechEx's research comprehensively evaluates sensor requirements in robotics, product roadmaps and emerging applications in manufacturing and logistics.

Wearable sensors offer many metrics, but integrated products define success

The wearable sensor technology landscape covers a wide range of sensor types, which can be integrated into an array of wearable form-factors. 2025 has seen a resurgence in the smart glasses market, as Meta and Xiaomi launch products, with Snap, Amazon and Samsung set to follow soon after. Wearable sensors are key components that enable eye-tracking, 3D spatial mapping, and gesture control in AR and XR devices.

Wearable sensors integrated into wrist-worn devices continue to enable new functionality, such as user interfacing through the use of EMG sensors and dry electrodes, and activity and health tracking using optical sensors.

This report provides an overview of wearable technology form factors and the wearable sensor technology opportunities associated. Sensors for XR, motion sensors, optical sensors and imaging, wearable electrodes, force, strain, temperature and chemical sensors are examined and compared across medical, consumer, prosumer, and industrial applications.

IoT sensors set to capitalize on AI

In 2025, the big trend within IoT is moving from connected to intelligent sensors using AI. AI models built and trained on real operation data are being augmented into sensors and IoT solutions to automate decision making and offer predictive functionality. Edge AI sensors, digital twinning, and smart wearable devices are all key enabling technologies promising to boost productivity. Industrial, environmental, and consumer IoT continue to represent key targets for sensor manufacturers.

Key emerging applications for industrial IoT sensor technology include industrial robotics and automation, machine health monitoring and predictive maintenance, worker safety, inventory management and logistics. Data insights from industrial sensors solutions offer optimized process efficiencies, improved safety, and reduced operating costs. This report characterizes the historic challenges facing IoT sensor applications, including legacy infrastructure integration, and case studies on emerging success stories.

Gas sensor technology used in environmental IoT solutions remains relevant for indoor air quality and outdoor pollution monitoring, particularly as regulation grows. Beyond these applications, scale-up of hydrogen infrastructure is presenting new opportunities for gas sensors in safety and leak detection, refueling & fuel cell vehicles, and stationary energy applications. This report explores emerging gas sensor technologies, including optical particle counters, metal oxide sensors, electrochemical sensors, infra-red sensors, photo-ionization detectors and photoacoustic sensors for use in environmental monitoring, hydrogen and methane detection, and PFAS detection.

Edge sensor market take-off begins

Low power, high performance compute is increasingly being integrated at the edge, both on- and in-sensor, to unlock greater device intelligence and decision-making capability. Edge computing integrated into sensors, often referred to as edge sensing, enables AI models trained on real operation data to process, interpret, and action on sensor data in real-time. MEMS, gas, and image sensors are amongst the first technologies to integrate edge AI in applications such as predictive maintenance, automated quality inspection, and worker safety monitoring.

IDTechEx's report analyzes new edge sensor technology, enabling technologies, key manufacturers, emerging applications, and provides commercial roadmaps for growth markets.

Emerging sensor technology innovations to yield high growth opportunities

IDTechEx predicts that emerging sensor technologies will grow at a CAGR of 17% by 2036, as advancements in photonic integrated circuits, quantum sensors, printed sensors and image sensors drive growth.

IDTechEx's Sensor Market 2026-2036 report provides a comprehensive overview of key sensor technology innovations impacting the market, including

Key aspects

10 Year Sensor Market Forecasts & Analysis:

Sensors covered in this report include:

This report characterizes sensor technology measuring:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Introduction to Sensor Technology

1.2. Overview of major sensor technology markets

1.3. Many multi-billion-dollar electronics companies compete for the established sensor market - but their revenue share can be comparable to more specialist players

1.4. Notable sensor market developments throughout 2024-2025

1.5. Total Global Sensor Market Forecast 2026-2036: Annual Revenue (US$, Billions)

1.6. Granular 10-year Sensor Market Annual Revenue Forecast, 2026-2036 (US$, Billions)

1.7. Sensor market size forecast and CAGR of emerging sensor categories

1.8. Connecting operating principles, metrics and manufacturing formats

1.9. How 2025 global events and technology mega-trends are influencing sensor markets and demand

1.10. Overview of key sensor technology innovations and applications for future markets

1.11. Sensor technology market roadmap

1.12. 2025 trends and developments in major sensor technology markets

1.13. Wearable devices for medical and wellness applications increasingly overlap

1.14. IoT technology meta-trends and impact on sensors

1.15. Key Takeaways for Sensors for Future Mobility Markets

1.16. Emerging Sensor Market: Ten-year sensors for mobility market share forecast (2026-2036), annual revenue (US$, Millions)

1.17. Sensors continue to become more intelligent, with the share of sensors containing edge compute and AI capability set to grow

1.18. Sensor technology development drives innovation in Industry 4.0, while sensor-enabled human-robot collaboration gives rise to Industry 5.0

1.19. Humanoid robots driving new demand in sensors for robotics, as adoption in automotive and logistics presents growth opportunities by 2030

1.20. Advancements in sensors for automation increasingly overlap across automotive, industrial, robotics, aerospace and defense markets

1.21. For more information on IDTechEx's latest sensor technology and related research:

2. MARKET FORECASTS

2.1. Market forecast methodology

2.1.1. Market Forecasts: Methodology Outline

2.1.2. Sensor market categories included in sensor market forecasts

2.1.3. Updated bottom-up sensor market sizing from annual report and financial statement analysis of leading sensor manufacturers

2.2. Market forecasts

2.2.1. Total Global Sensor Market Forecast 2026-2036: Annual Revenue (US$, Billions)

2.2.2. Granular 10-year Sensor Market Annual Revenue Forecast, 2026-2036 (US$, Billions)

2.2.3. Sensor market size forecast and CAGR of emerging sensor categories

2.2.4. Established Sensor Market: 10-year gas sensor technology forecast (2026-2036), annual revenue (USD, Millions)

2.2.5. Established Sensor Market: 10-year semiconductor sensor technology forecast (2026-2036), annual revenue (USD, Millions)

2.2.6. Established Sensor Market: 10-year automotive and aerospace sensor technology forecast (2026-2036), annual revenue (USD, Millions)

2.2.7. Established Sensor Market: 10-year biosensor sensor technology forecast (2026-2036), annual revenue (US$, Millions)

2.2.8. Emerging Sensor Market: 10-year emerging image sensor technology forecast (2026-2036), annual revenue (US$, Millions)

2.2.9. Emerging Sensor Market: 10-year printed sensor technology forecast (2026-2036), annual revenue (US$, Millions)

2.2.10. Emerging Sensor Market: 10-year photonic integrated circuit sensor technology forecast (2026-2036), annual revenue (US$, Millions)

2.2.11. Emerging Sensor Market: 10-year quantum sensor technology forecast (2026-2036), annual revenue (US$, Millions)

2.2.12. Emerging Sensor Market: 10-year sensors for future mobility forecast (2026-2036), annual revenue (US$, Millions); LiDAR, RADAR, CAMERA, IR and in-cabin-sensing

2.2.13. Emerging Sensor Market: Ten-year sensors for mobility market share forecast (2026-2036), annual revenue (US$, Millions)

2.2.14. Total Sensor Market 2026-2036: Annual Revenue (US$, Millions) - Data Table

3. INTRODUCTION AND SENSOR MARKET DEVELOPMENTS

3.1. Introduction to the Sensor Market - Chapter Overview

3.2. Introduction to Sensor Technology

3.3. Overview of major sensor technology markets

3.4. Many multi-billion-dollar electronics companies compete for the established sensor market - but their revenue share can be comparable to more specialist players

3.5. Notable sensor market developments throughout 2024-2025

3.6. Overview of some typical sensor technology product categories

3.7. Connecting operating principles, metrics and manufacturing formats

3.8. General trends separating emerging and established sensor technology

3.9. How 2025 global events and technology mega-trends are influencing sensor markets and demand

3.10. 2025 market trends in major sensor technology markets

3.11. Sensor technology market roadmap

3.12. Overview of key sensor technology innovations and applications for future markets

3.13. New sensor product launches by market leaders underscore focus on mega-trends in AI, autonomy, energy, future aviation, and robotics

3.14. What are the mega trends in future mobility?

3.15. What is the role of sensors in future mobility technology?

3.16. Near term IoT markets trends set to revolve around edge sensing as the industry shifts from the cloud to the edge

3.17. Sensors continue to become more intelligent, with the share of sensors containing edge compute and AI capability set to grow

3.18. Sensor technology development drives innovation in Industry 4.0, while sensor-enabled human-robot collaboration gives rise to Industry 5.0

3.19. Humanoid robots driving new demand in sensors for robotics, as adoption in automotive and logistics presents growth opportunities by 2030

3.20. Advancements in sensors for automation increasingly overlap across automotive, industrial, robotics, aerospace and defense markets

3.21. Overview of the landscape for wearable sensor innovation

3.22. Roadmap of the mega-trends in wearable technology

3.23. Introduction to 6G and expected improvements in sensing compared to 5G

3.24. Overview of 6G applications beyond mobile communications - including THz sensing and imaging

3.25. The value proposition of mmWave and THz frequencies for sensing

3.26. Key conclusions on the sensor technology market: Technologies and trends

4. NEXT GENERATION SENSOR TECHNOLOGY INNOVATIONS

4.1. Introduction

4.1.1. Chapter Overview and Related IDTechEx Reports

4.2. Emerging Image Sensors

4.2.1. Overview of the Emerging Image Sensors Section

4.2.2. Emerging image sensors: Summary of key conclusions

4.2.3. Emerging image sensors: Key players overview (I)

4.2.4. Emerging image sensors: Key players overview (II)

4.2.5. SWIR imaging: Overview and key conclusions

4.2.6. SWIR imaging: Emerging technology options

4.2.7. SWIR sensors: Applications and key players

4.2.8. OPD-on-CMOS hybrid image sensors: Overview, conclusions and key players

4.2.9. OPD-on-CMOS detectors: Technology readiness level roadmap by application

4.2.10. QD-on-Si/QD-on-CMOS imaging: Fundamentals, value proposition and key conclusions

4.2.11. Hyperspectral imaging: Overview and key conclusions

4.2.12. Hyperspectral imaging: Wavelength range vs spectral resolution

4.2.13. Miniaturized spectrometers: Overview and key conclusions

4.2.14. Miniaturized spectrometers: Targeting a wide range of sectors

4.2.15. Miniaturized spectrometers: Key players and key differentiators

4.2.16. Event-based sensing: Overview and key conclusions

4.2.17. Event-based vision: Application requirements

4.2.18. LiDAR: Overview of operating principles

4.2.19. LiDAR: Value proposition

4.2.20. LiDAR: Technology Challenges

4.2.21. LiDAR: Ecosystem and key players

4.3. Gas Sensors

4.3.1. Overview of the gas sensor section and analyst viewpoint

4.3.2. The gas sensor market 'at a glance'

4.3.3. Gas Sensor Market Summary: Drivers for change?

4.3.4. Overview of Metal Oxide (MOx) gas sensors

4.3.5. Identifying key MOx sensors manufacturers

4.3.6. Key conclusions and SWOT analysis of MOx gas sensors

4.3.7. Introduction to electrochemical gas sensors

4.3.8. Major manufacturers of electrochemical sensors

4.3.9. Key conclusions and SWOT analysis of electrochemical gas sensors

4.3.10. Introduction to infrared gas sensors

4.3.11. Identifying key infra-red gas sensor manufacturers

4.3.12. Key conclusions and SWOT analysis of infra-red gas sensors

4.3.13. Introduction to photoionization detectors (PID)

4.3.14. Categorization of ionization detector manufacturers

4.3.15. Key conclusions and SWOT analysis of photo-ionization detectors

4.3.16. Optical Particle Counter

4.3.17. Identifying key optical particle counter manufacturers

4.3.18. SWOT analysis of Optical Particle Counters

4.3.19. Key Conclusions: Optical particle counters

4.3.20. Principle of Sensing: Photoacoustic

4.3.21. Sensirion and Infineon offer a miniaturized photo-acoustic carbon dioxide sensor

4.3.22. SWOT analysis of photo acoustic gas sensors

4.3.23. Principle of Sensing: E-Nose

4.3.24. Advantages and disadvantaged of sensor types for E-Nose

4.3.25. Categorization of e-nose manufacturers

4.3.26. SWOT analysis of E-noses

4.3.27. E-nose Summary: Specific aromas a better opportunity than a nose

4.4. Printed and Flexible Sensors

4.4.1. Introduction to the printed and flexible sensor market

4.4.2. Key takeaways segmented by printed/flexible sensor technology

4.4.3. Piezoresistive Sensors: Market map of applications and players

4.4.4. Challenges facing printed piezoelectric sensors

4.4.5. Readiness level snapshot of printed piezoelectric sensors

4.4.6. Conclusions for printed and flexible piezoelectric sensors

4.4.7. Opportunities for printed photodetectors in large area flexible sensing

4.4.8. Supplier overview: Thin film photodetectors

4.4.9. Conclusions for printed and flexible image sensors

4.4.10. Printed temperature sensors continue to attract interest for thermal management applications

4.4.11. Printed temperature sensor supplier overview

4.4.12. Conclusions for printed and flexible temperature sensors

4.4.13. Opportunities for printed strain sensors could expand beyond motion capture into battery management long term

4.4.14. Summary: Strain sensors

4.4.15. Outlook for printed gas sensor technology

4.4.16. ITO coating innovations and indium price stabilization impact printed capacitive sensor growth markets

4.4.17. Readiness level of printed capacitive touch sensors materials and technologies

4.4.18. Conformal and curved surface touch sensing applications emerge for printed capacitive sensors

4.4.19. Conclusions for printed and flexible capacitive touch sensors

4.4.20. Opportunities for printed electrodes in the wearables market

4.4.21. SWOT analysis for each printed sensor category (I)

4.4.22. SWOT analysis for each printed sensor category (II)

4.4.23. SWOT analysis for each printed sensor category (III)

4.4.24. Summary of key growth markets for printed sensor technology

4.4.25. Automotive mega-trends and printed sensor opportunities

4.4.26. Printed sensor must offer feature differentiation in saturated product markets

4.4.27. Commercialization of printed sensor technologies in medical wearables

4.4.28. Key player target markets highlight the spectrum of commercialization strategies available

4.5. Silicon Photonics

4.5.1. What are Photonic Integrated Circuits (PICs)?

4.5.2. Electronic and Photonic Integrated Circuits Compared

4.5.3. Opportunities for PIC Sensors: Biomedical

4.5.4. Market players developing PIC Biosensors

4.5.5. Rockley Photonics: IP sale and likely end of PIC involvement

4.5.6. Opportunities for PIC Sensors: Gas Sensors

4.5.7. Market players developing PIC-based Gas Sensors

4.5.8. Opportunities for PIC Sensors: Structural Health Sensors

4.5.9. Market players developing Spectroscopic PICs

4.5.10. LiDAR in automotive applications

4.5.11. Opportunities for PIC Sensors: LiDAR Sensors

4.5.12. Core Aspects of LiDAR

4.5.13. Market players developing PIC-based LiDAR (1)

4.5.14. Market players developing PIC-based LiDAR (2)

4.5.15. LiDAR Wavelength and Material Trends

4.5.16. Major challenges of PIC-based FMCW LiDARs

4.5.17. E-Noses for Automotive

4.6. Quantum sensors

4.6.1. What are quantum sensors?

4.6.2. The quantum sensor market 'at a glance'

4.6.3. Quantum sensors: Analyst viewpoint

4.6.4. The value proposition of quantum sensors varies by hardware approach, application and competition

4.6.5. Quantum sensor industry market map

4.6.6. Key industries for quantum sensors

4.6.7. Atomic clocks self-calibrate for clock drift

4.6.8. Atomic Clocks: SWOT analysis

4.6.9. Atomic clocks: Sector roadmap

4.6.10. Sensitivity is key to the value proposition for quantum magnetic field sensors

4.6.11. Operating principles of Optically Pumped Magnetometers (OPMs)

4.6.12. Optically Pumped Magnetometers: SWOT analysis

4.6.13. Introduction to NV center magnetic field sensors

4.6.14. N-V Center Magnetic Field Sensors: SWOT analysis

4.6.15. Quantum magnetometers: Sector roadmap

4.6.16. Overview of quantum gravimeters

4.6.17. Operating principles of atomic interferometry-based quantum gravimeters

4.6.18. Quantum Gravimeters: SWOT analysis

4.6.19. Quantum gravimeters: Sector roadmap

4.6.20. Operating principles of atomic quantum gyroscopes

4.6.21. MEMS manufacturing processes can miniaturize atomic gyroscope technology for higher volume applications

4.6.22. Inertial quantum sensors: Sector roadmap

4.6.23. Value proposition of quantum RF sensors

4.6.24. Overview of types of quantum RF sensors

4.6.25. Quantum RF sensors: Sector roadmap

4.6.26. Introduction to single photon detectors

4.6.27. Single photon imaging and quantum imaging - 3 key trends

4.6.28. Single photon detectors: Sector roadmap

4.7. Biosensors

4.7.1. Layout of a biosensor

4.7.2. Bioreceptors: Benefits and drawbacks of each type

4.7.3. Optical transducers: Benefits and drawbacks of each type

4.7.4. Electrochemical transducers: Benefits and drawbacks of each type

4.7.5. Applications for biosensors at the point-of-care

4.7.6. In vitro diagnostics

4.7.7. Growing market for in vitro diagnostics

4.7.8. The value of point-of-care testing

4.7.9. In vitro diagnostics trending toward point-of-care testing (POCT)

4.7.10. Mechanism of the lateral flow assay

4.7.11. Minimalizing sample handling with integrated cartridges

4.7.12. Value ecosystem of POCT devices

4.7.13. Market dynamics

4.8. Nanocarbon Sensors

4.8.1. Graphene - Introduction

4.8.2. Producing graphene as an electronic substrate and chemical vapor deposition (CVD) graphene

4.8.3. Expanding graphene wafer capacity and adoption

4.8.4. Industry examples of graphene-based sensors

4.8.5. Nanocarbon sensors for embedded SHM

4.8.6. Graphene Sensors - Gas Sensors

4.8.7. Graphene Sensors - Gas Sensors (2)

4.8.8. Graphene sensor for food safety monitoring

4.8.9. Biosensor - electrochemical transducer overview

4.8.10. Graphene-based BioFET

4.8.11. Biosensors using graphene

4.8.12. Hall-effect sensor

4.8.13. Fast graphene photosensor

4.8.14. Commercial example of graphene-enabled photodetector

4.8.15. Emerging role in silicon photonics

4.8.16. Emerging graphene photonic companies

4.8.17. QD-on-CMOS with graphene interlayer

4.8.18. Optical brain sensors using graphene

4.8.19. Graphene skin electrodes

4.8.20. Carbon Nanotubes (CNTs)

4.8.21. CNTs in gas sensors: Overview

4.8.22. CNT based gas sensor - C2Sense

4.8.23. CNT based gas sensor - AerNos

4.8.24. CNT based electronic nose for gas fingerprinting (PARC)

4.8.25. Printed humidity and moisture sensors using carbon nanotubes

4.8.26. CNT temperature sensors (Brewer Science)

4.8.27. CNT enabled LiDAR sensors

4.8.28. Outlook for carbon materials in sensors

4.9. Next-generation MEMS sensors

4.9.1. What are MEMS?

4.9.2. Next-generation MEMS in sensing

4.9.3. Overview of Inertial Measurement Units (IMUs)

4.9.4. Inertial Navigation Systems (INS) Technology Landscape

4.9.5. Application Grades of IMUs

4.9.6. IMU Market Landscape

4.9.7. MEMS Accelerometers Overview

4.9.8. Summary of Accelerometer Applications

4.9.9. Next-Gen MEMS Accelerometers Industry Landscape

4.9.10. Geometric Anti-Spring Accelerometers

4.9.11. Resonant Beam Accelerometer

4.9.12. Thermal MEMS Accelerometers

4.9.13. Whispering Gallery Mode Resonator

4.9.14. MEMS Novel Accelerometers Industry Landscape

4.9.15. Gyroscope Technology Landscape

4.9.16. MEMS Macro-scale Hemispherical Resonator Gyros (HRGs)

4.9.17. Summary of Manufacturing Methods for μHRG

4.9.18. Commercial Activity in μHRGs

4.9.19. μHRG Offers a Significant Leap for MEMS Gyros

5. EDGE SENSING AND AI

5.1. Edge sensing: Introduction

5.1.1. Edge sensing: Chapter overview

5.1.2. What is edge sensing

5.1.3. Edge versus cloud computing for emerging sensor applications

5.1.4. The rise of edge sensing tracks with a broader industry shift from cloud to edge computing

5.1.5. Market drivers for edge sensing

5.2. Edge sensing: Technologies

5.2.1. Edge sensors: Technical breakdown and key components

5.2.2. Edge sensing internet of things architecture

5.2.3. Evaluating cloud, edge, and endpoint sensing and associated enabling technologies

5.2.4. High efficiency computing hardware has unlocked edge sensing

5.2.5. Low-power designs are critical for edge sensor devices

5.2.6. Case study: Low-power edge sensor asset tracker

5.2.7. Edge sensing and edge AI are converging and will unlock predictive and proscriptive functionality

5.2.8. Edge AI enables data processing and inference on endpoint devices

5.2.9. Edge AI enables image classification and processing on camera modules

5.2.10. On-chip edge AI image sensor gains early commercial sales

5.2.11. Applications of edge AI enabled camera modules

5.2.12. Challenges facing edge sensors

5.3. Edge sensing: Markets and applications

5.3.1. Edge sensors: Market overview

5.3.2. Opportunity for improving energy efficiency in smart buildings with building automation

5.3.3. Edge sensors enabling low-power occupancy monitoring and smart security

5.3.4. Edge sensing will unlock predictive maintenance in industrial IoT

5.3.5. Case Study: Analog Devices - Predictive Maintenance Edge AI Sensor

5.3.6. Major Suppliers of Predictive Maintenance Hardware and Software

5.3.7. Roadmap of the evolving role of sensors in industrial IoT

5.3.8. Edge sensors can improve workplace safety in remote and hazardous locations

5.3.9. Richer structural health monitoring insight with edge AI-enabled sensing

5.3.10. Quality Inspection and Anomaly Detection with Edge AI

5.3.11. AI-enabled edge sensing in wearables

5.3.12. Edge sensor and edge AI promise continues innovation in established consumer electronics applications and smart retail

5.3.13. Evaluation of edge sensing application requirements

5.3.14. Key edge sensor markets: Emerging applications, opportunities and threats

5.4. Edge sensing: Conclusions

5.4.1. Summary of edge sensor technologies and market outlook

5.4.2. Technology readiness level of edge sensor applications

5.4.3. SWOT analysis of edge sensors and edge AI

5.4.4. Key players in edge sensing: Sensors and product integrators

5.4.5. Key players in edge sensing: IC, SoC, and cloud service suppliers

6. WEARABLE SENSORS

6.1. Overview of wearable sensors

6.1.1. Overview of the wearable sensors section and technology landscape

6.1.2. Wearable technology takes many form factors

6.1.3. Overview of wearable sensor types

6.1.4. Connecting form factors, wearable sensors, and metrics

6.1.5. Roadmap of wearable sensor technology segmented by key biometrics (1)

6.1.6. Roadmap of wearable sensor technology segmented by key biometrics

6.1.7. Wearable devices for medical and wellness applications increasingly overlap

6.2. Wearable Motion Sensors

6.2.1. Wearable motion sensors: Introduction

6.2.2. IMUs for smart-watches: Major players and industry dynamic

6.2.3. Wearable magnetometer suppliers and industry dynamic

6.2.4. Overview of emerging use-cases for wearable motion sensors

6.2.5. MEMS-based IMUs for wearable motion sensing: SWOT Analysis

6.2.6. Wearable motion sensors: Sector roadmap

6.2.7. Wearable motion sensors: Conclusions

6.3. Wearable Optical Sensors

6.3.1. Wearable optical sensors: Introduction

6.3.2. Wearable optical sensors: Photoplethysmography (PPG)

6.3.3. Leading manufacturers of optical components for wearables

6.3.4. Wearable PPG: Applications and key players

6.3.5. Wearable heart-rate: Use cases, opportunities and sample players

6.3.6. Wearable optical sensors: Obtaining blood oxygen from PPG

6.3.7. Wearable optical sensors: Market outlook and technology readiness of pulse oximetery

6.3.8. Wearable optical sensors: Progress of non-invasive blood pressure sensing

6.3.9. Overview of technologies for cuff-less blood pressure

6.3.10. Wearable optical sensors: SWOT Analysis for heart-rate, pulse-ox, blood pressure and glucose monitoring

6.3.11. Wearable optical sensors: Key conclusions

6.4. Wearable Electrodes

6.4.1. Wearable electrodes: Overview of key types

6.4.2. Wearable electrodes: Wet vs dry

6.4.3. Material innovations in dry electrodes for EEG

6.4.4. Device level integration of EEG for BCI applications: Form-factors and key players using dry electrodes

6.4.5. Microneedle electrodes

6.4.6. Wearable electrodes: Electronic skins (also known as 'epidermal electronics')

6.4.7. Wearable electrodes: Applications and product types

6.4.8. Key players in wearable electrodes in e-textiles, skin patches and watches

6.4.9. Wearable electrodes: Consolidated SWOT analysis

6.4.10. Wearable electrodes: Key conclusions

6.5. Wearable Temperature Sensors

6.5.1. Two main roles for temperature sensors in wearables

6.5.2. Types of temperature sensor

6.5.3. Key players, form factors and applications for wearable body temperature sensors

6.5.4. Mapping the wearable temperature sensor landscape

6.5.5. Wearable temperature sensors: SWOT analysis

6.5.6. Wearable temperature sensors: Key conclusions

6.6. Wearable Chemical Sensors

6.6.1. Wearable Chemical Sensors: Overview

6.6.2. Wearable chemical sensors: Analyte selection and availability

6.6.3. Wearable chemical sensors: Operating principle of a typical CGM device

6.6.4. CGM: Overview of key players

6.6.5. Wearable glucose sensors SWOT analysis of chemical vs alternatives

6.6.6. Wearable chemical sensors: Roadmap for glucose sensing and key conclusions

6.6.7. Wearable chemical sensors: Use-cases, stakeholders, key players and SWOT analysis of wearable alcohol sensors

6.6.8. Wearable chemical sensors: Use-cases, stakeholders, key players and SWOT analysis of wearable lactate/lactic acid sensors

6.6.9. Wearable chemical sensors: Use-cases, stakeholders, key players and SWOT analysis of wearable hydration sensors

6.6.10. Market readiness of wearable sensors for novel biometrics

6.6.11. Wearable sensors for novel biometrics: Key conclusions

6.7. Wearable Sensors for XR Devices

6.7.1. What are VR, AR, MR and XR?

6.7.2. Controllers and sensing connect AR and VR devices to the environment and the user

6.7.3. Beyond positional tracking: What else might XR headsets track?

6.7.4. Where are XR sensors located?

6.7.5. 3D imaging and motion capture

6.7.6. Time of Flight (ToF) cameras for depth sensing

6.7.7. Low-power image sensors target applications in AR/VR

6.7.8. Low-power time-of-flight sensors for 3D sensing

6.7.9. Structured light

6.7.10. Comparison of 3D imaging technologies for XR applications

6.7.11. Sensors for XR: Positional and motion tracking, sector roadmap

6.7.12. Wearable Gesture Control - Key Conclusions

6.7.13. Why is eye-tracking important for AR/VR devices?

6.7.14. Eye-Tracking Sensor Categories

6.7.15. Eye-tracking using cameras with machine vision

6.7.16. Eye tracking companies based on conventional/NIR cameras and machine vision software

6.7.17. Sensors for XR: Event-based vision for AR/VR eye tracking

6.7.18. Eye tracking with laser scanning MEMS

6.7.19. Capacitive sensing of eye movement

6.7.20. Eye tracking for XR: Sector roadmap

7. SENSORS FOR FUTURE MOBILITY MARKETS

7.1. Introduction to sensors for future mobility

7.1.1. What are the mega trends in future mobility?

7.1.2. Sensors for Future Mobility: Chapter Overview

7.1.3. Summary and outlook for sensors in future mobility applications

7.1.4. Main conclusions: Sensors for Future Mobility Markets

7.2. Sensors for Electrification

7.2.1. Electric Vehicles: Basic Principle

7.2.2. Monitoring current, voltage, time and temperature is core to BMS functionality

7.2.3. Trends in battery management systems - sensors most relevant to greater sophistication in state estimation

7.2.4. Sensors play an evolving role in EV charging infrastructure

7.2.5. The rise of the EV could shift the role of gas sensors from emissions testing to battery management

7.2.6. Problems solved by advanced sensor deployments

7.2.7. Value proposition of gas sensors on battery monitoring: Early thermal runaway detection

7.2.8. Regulatory background: Electric vehicles

7.2.9. Benchmarking sensors for electric vehicles

7.3. Sensors for Automation

7.3.1. SAE Levels of Automation in Cars

7.3.2. The Big Three Sensors

7.3.3. High Levels of Autonomy Means More Sensors per Vehicle

7.3.4. Evolution of Sensor Suite From Level 1 to Level 4

7.3.5. Sensor Suite Costs

7.3.6. Vehicle Camera Applications

7.3.7. The IR Spectrum and Applications

7.3.8. Technology Comparison of Carious SWIR Image Sensor Technologies

7.3.9. LWIR in Automotive

7.3.10. Uncooled Sensor Material Choice Summary

7.3.11. LWIR for ADAS: Advantages and Disadvantages

7.3.12. Key legislation impacting the potential uptake of LWIR

7.3.13. Autoliv, Veoneer and Magna Night Vision Generations

7.3.14. Front Radar and Side Radar Applications

7.3.15. Radar Trends: Volume and Footprint

7.3.16. The Adoption of More Advanced Semiconductor Technology is a Key Part of the Automotive Radar Advancements

7.3.17. LiDARs in automotive applications

7.3.18. Automotive LiDAR: Requirements

7.3.19. Radar or LiDAR

7.4. In-Cabin Sensing (or Interior Monitoring Systems)

7.4.1. An Overview of DMS and OMS Systems Within In-Cabin Monitoring

7.4.2. Evolution of DMS Sensor Suite from SAE Level 1 to Level 4

7.4.3. Current Technologies for Interior Monitoring System (IMS)

7.4.4. Technologies Categorization: Driver Monitoring System (DMS)

7.4.5. Overview of In-Cabin Sensors by OEM (1)

7.4.6. Overview of In-Cabin Sensors by OEM (2)

7.4.7. Infrared (IR) Cameras in DMS

7.4.8. Trend - Integration into Mirrors or Displays with ADAS

7.4.9. Potential Integration Areas

7.4.10. ToF Camera for DMS - Principles

7.4.11. ToF Imaging Sensors: Resolution and Price Benchmarking

7.4.12. Comparison of In-Cabin Radars

7.4.13. Current Status of Capacitive Sensors in DMS

7.4.14. Torque Sensor for HOD - Working Principles

7.4.15. Key sensor trends for in-cabin sensing

7.4.16. In-Cabin Sensing Technology Overview

7.5. Sensors for Connected Vehicles and Software Defined Vehicles

7.5.1. Software-Defined Vehicle Level Guide

7.5.2. Connected Vehicles Key Terminology

7.5.3. Certain V2V/V2I use cases highlight the interplay between connected vehicles and autonomy - and as such the role of sensors

8. SENSORS FOR THE INTERNET OF THINGS (IOT)

8.1. Overview of IoT

8.1.1. What is internet-of-things (IoT)?

8.1.2. Sensors represent just one element within an IoT platform

8.1.3. Emerging IoT markets and applications

8.1.4. IoT technology meta-trends and impact on sensors

8.2. Industrial IoT (IIoT)

8.2.1. Industrial IoT: Introduction

8.2.2. Industrial trends and Industry 5.0

8.2.3. Industrial IoT applications for sensor technology

8.2.4. IIoT sensors: Industrial robotics and automation

8.2.5. Applications of Sensors in Robots

8.2.6. Sensors for object detection

8.2.7. Comparison of Navigation and Collision Detection Sensors: LiDAR, Radar, Cameras, and 1D/3D Ultrasonic Sensors

8.2.8. Navigation and mapping sensors

8.2.9. Comparisons of LiDAR, radar, camera & ultrasonic sensors - (1)

8.2.10. Comparisons of LiDAR, radar, camera & ultrasonic sensors - (2)

8.2.11. Performance comparison of different LiDARs on the market or in development

8.2.12. Introduction to Cameras

8.2.13. SWOT - RGB/Visible light camera

8.2.14. Radar and LiDAR in Robotics

8.2.15. 3D visual systems to sense the surroundings in humanoid robots

8.2.16. Outlook for cameras and LiDAR in humanoid robots

8.2.17. Introduction of detection principle of proximity sensors

8.2.18. Comparison of proximity sensors

8.2.19. Force and Torque Sensors - Introduction

8.2.20. Comparison of different torque and force sensors

8.2.21. Tactile sensors for humanoid robotics

8.2.22. Benchmarking tactile sensors by technology

8.2.23. Paxini - Tactile sensors for humanoid robot fingers

8.2.24. Summary of tactile sensors

8.2.25. IIoT sensors: Machine monitoring and predictive maintenance

8.2.26. Sensors in machine health monitoring and predictive maintenance

8.2.27. Indicators for machine health monitoring

8.2.28. Vibration sensing for machine health monitoring

8.2.29. Emerging machine health monitoring and predictive maintenance technologies

8.2.30. Digital twinning and virtual environments in IoT enable remote operation and automation

8.2.31. IIoT sensors: Worker safety

8.2.32. The cost of industrial workplace safety

8.2.33. Wearable sensors can improve workplace safety in remote and hazardous locations

8.2.34. Printed wearable sensors emerging for hydration monitoring

8.2.35. IIoT sensors: Inventory management and logistics

8.2.36. IIoT sensors for asset tracking

8.2.37. RFID Sensor Types

8.2.38. RFID Sensors: Main choices

8.2.39. IIoT driving demand for low-power sensors and present opportunities for energy harvesting

8.2.40. Low-power sensors significantly prolong battery lifetime of asset trackers

8.2.41. IIoT sensors can be self-powered by harvesting energy

8.2.42. Energy harvesting IIoT sensor: Solar and kinetic approaches

8.2.43. Radio frequency energy harvesting enable wirelessly powered sensors

8.2.44. Printed force sensors for inventory management systems

8.2.45. IIoT sensors: Conclusions and outlook

8.2.46. IIoT sensors: Key conclusions and analyst opinion

8.2.47. Summary of sensor opportunities and threats in IIoT

8.2.48. IIoT outlook for established and emerging sensor manufacturers

8.2.49. Market challenges facing IIoT

8.2.50. Sensors have minimal influence on long return on investment period for industrial IoT

8.2.51. IIoT Value chain and key players

8.3. Environmental Monitoring IoT

8.3.1. Overview of environmental gas sensor markets within IoT

8.3.2. Key analytes for outdoor pollution monitoring

8.3.3. Tighter regulations and recommendations for outdoor air quality are increasing the need for sensitive gas sensors

8.3.4. How will technology be used to monitor regulatory limits?

8.3.5. Sensors for monitoring urban emissions

8.3.6. Outdoor pollution monitoring creates an opportunity for gas sensors in 'smart-cities'

8.3.7. Incumbent technology challenges- fixed monitoring stations are large and expensive

8.3.8. Key miniaturized gas sensor technologies for outdoor pollution monitoring

8.3.9. The role of miniaturized gas sensors in outdoor air quality monitoring 'nodes'

8.3.10. Air quality monitoring for smart-cities have been a relatively low volume market for miniaturized gas sensor technology

8.3.11. Lack of regulatory pressure limits adoption of miniaturized gas sensors for outdoor pollution monitoring

8.3.12. Infrastructure improvements are essential for increased adoption of low-cost gas sensors for outdoor pollution monitoring in towns and cities

8.3.13. Mobile platforms for outdoor pollution monitoring is emerging as a more efficient alternative to sensor networks for hyper-local data collection

8.3.14. Sensors for monitoring energy sector emissions

8.3.15. Industrial markets create a clearer business case for low-cost gas sensor nodes compared to smart-cities

8.3.16. Detecting methane is crucial for safety, the environment, and regulatory compliance

8.3.17. Overview of imaging technologies for methane detection and challenges associated with automation and quantification

8.3.18. Innovation in the next generation of Single-Photon Avalanche Diodes (SPADs)

8.3.19. Alternative semiconductor SPADs unlock infrared wavelengths beyond the range of silicon

8.3.20. Comparing key specifications of core environmental gas sensor technologies

8.3.21. Increased expectations in the gas safety market are a driver for adoption of new technology

8.3.22. Emerging sensors for methane detection: Sensirion and Infineon offer a miniaturized photo-acoustic methane sensor

8.3.23. Drones as mobile platforms value the low size and weight of miniaturized gas sensors for industry, agriculture and law-enforcement

8.3.24. The landscape of hydrogen gas sensing applications

8.3.25. Hydrogen leakage poses hazardous risks and requires detection

8.3.26. Hydrogen leak detection can be achieved using photodetectors, ultrasonic and electrochemical sensors

8.3.27. Other notable hydrogen sensing applications

8.3.28. Opportunities for sensing in the hydrogen economy

8.3.29. Gas sensors for outdoor pollution monitoring: Market map and value chain

8.3.30. Miniaturized gas sensors for outdoor pollution monitoring: Conclusions and outlook

8.3.31. Key analytes for indoor air quality monitoring

8.3.32. Overview of health risks associated with indoor pollution

8.3.33. Indoor air pollution remains a significant health risk in high-income nations despite regulation

8.3.34. Lack of ventilation can compound the risk of radon in the northern hemisphere

8.3.35. How is gas sensor technology currently being used to tackle indoor air quality?

8.3.36. Overview of the 'smart-building' value proposition and sensor requirements

8.3.37. Segmenting the smart-building market

8.3.38. Benchmarking opportunities in the gas sensor market by technology type

8.3.39. Impact of indoor air quality regulation on the gas sensor opportunity in the smart-buildings market (2)

8.3.40. Air quality focus in 'health building' standards is gradually driving growth for the smart-building market

8.3.41. Fire safety in smart-buildings - gas sensor dependent but with high barriers to adoption for new-tech

8.3.42. Overview of building management systems for indoor air quality

8.3.43. Indoor air quality in smart-buildings: Market overview and gas sensor opportunities

8.3.44. How are specialist air quality management services differentiating?

8.3.45. Indoor air quality monitoring for smart-buildings a higher-volume market than outdoor pollution sensing

8.3.46. Miniaturized gas sensors for indoor monitoring in smart buildings: Conclusions and outlook

8.3.47. Sensors for PFAS - Overview

8.3.48. Introduction to PFAS

8.3.49. Established application areas for PFAS

8.3.50. Overview of PFAS: Segmented by non-polymers vs polymers

8.3.51. Global limits on PFAS in drinking water: Overview

8.3.52. Regulation relating to PFAS monitoring and safe drinking water limits

8.3.53. Maximum contaminant limits (MCLs) for individual PFAS in different countries

8.3.54. Growing concerns about the negative impact of PFAS

8.3.55. Limitations of existing instrument-based methods and the need for sensors

8.3.56. Challenges in commercial PFAS sensor development: Forever chemicals are inherently a hard to detect class

8.3.57. PFAS sensor solution developers

8.3.58. Competition with mail order test kits

8.4. Consumer IoT: Smart Home (Air Quality Sensors)

8.4.1. Smart Home technology OEMs are still betting on it going 'mainstream'

8.4.2. Introduction to the Smart Home market for indoor air quality monitoring

8.4.3. How can OEMs access the mass market for indoor air quality monitors post-covid?

8.4.4. Comparing technology specs of smart-home air quality monitors

8.4.5. Smart purifiers are an increasingly popular solution for poor air quality

8.4.6. Market leaders include particulate matter sensors in product offerings

8.4.7. Air quality and the internet of things

8.4.8. Which business models for indoor air quality products are sustainable?

8.4.9. Opportunity for air quality monitoring within wellness and fitness monitoring remains

8.4.10. Relationship between air quality regulations and technology

8.4.11. Smart-home indoor air quality monitoring: Market map and outlook

8.4.12. Comparing device costs of smart-home technology for IAQ monitoring

8.4.13. Challenges for indoor air quality devices in the smart-home

8.4.14. Miniaturized gas sensors for indoor monitoring in smart home: Conclusions and outlook

9. COMPANY PROFILES

9.1. AMS Osram

9.2. Arbe: 4D Imaging Radar Leader

9.3. Arm

9.4. Artilux Inc

9.5. Bosch Sensortec

9.6. Bosch Sensortec (Wearable Sensors)

9.7. Boston Electronics

9.8. Canatu

9.9. CPI EDB (Quantum Sensing)

9.10. Datwyler (Dry Electrodes)

9.11. Dexcom

9.12. Dracula Technologies

9.13. EarSwitch

9.14. Emteq Limited

9.15. Enertia Micro: Birdbath Resonator Gyroscopes

9.16. Epicore Biosystems

9.17. Excelitas

9.18. FLEXOO

9.19. Fraunhofer CAP

9.20. Hinalea Imaging

9.21. Honeywell - BESS sensors

9.22. Honeywell Aerospace Technologies: New MEMS IMU

9.23. Honeywell: Advanced Sensors for Thermal Management

9.24. Imec

9.25. Infi-Tex

9.26. Innoseis Sensor Technologies: Nano-G MEMS Accelerometer

9.27. Mateligent GmbH

9.28. Meta (Neural Interface Wristband)

9.29. Mobileye: Automotive Radar

9.30. Murata

9.31. muRata: In-Cabin Radars and Humidity Sensors

9.32. Neuralink

9.33. NIQS Technology Ltd

9.34. Peratech

9.35. Photon Force

9.36. Photron

9.37. Polariton Technologies

9.38. Posifa Technologies: Gas Sensing for Battery Packs

9.39. Powercast

9.40. Q-CTRL (quantum navigation)

9.41. QDI Systems

9.42. Sensel

9.43. Senseonics

9.44. Sensirion - advanced sensors for battery management systems

9.45. Siemens Healthineers

9.46. Silicon Microgravity Ltd: MEMS Accelerometers and Gravimeters

9.47. Silveray

9.48. Sony Semiconductor Solutions: Edge AI Image Sensors

9.49. ST Microelectronics

9.50. Suzhou ShanHe Optoelectronic Technology Co., Ltd

9.51. TDK (Passive Components)

9.52. TDK SensEI

9.53. Teledyne FLIR

9.54. Temi Global

9.55. Waveye: Cost-Effective Approach to Imaging Radars

9.56. Wearable Devices Ltd.

9.57. Wisear

9.58. Xavveo: A Photonics-Based Paradigm Shift for Radar

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(センサ・MEMS)の最新刊レポート

IDTechEx社の センサー、触覚とディスプレイ - Sensors,Haptics & Display分野 での最新刊レポート

関連レポート(キーワード「センサ」)