RFID 2026-2036:予測、プレーヤー、ビジネスチャンスRFID 2026-2036: Forecasts, Players and Opportunities 世界のRFID産業の完全分析 IDTechExはRFID業界を約20年にわたり調査してきました。「RFIDの予測、プレーヤー、機会 2026-2036年」は最新のRFID市場調査であり、パッシブRFID(UHF帯、HF帯、LF... もっと見る

サマリー

世界のRFID産業の完全分析

IDTechExはRFID業界を約20年にわたり調査してきました。「RFIDの予測、プレーヤー、機会 2026-2036年」は最新のRFID市場調査であり、パッシブRFID(UHF帯、HF帯、LF帯)、バッテリーアシスト型パッシブRFID、アクティブRFID、チップレスRFIDの技術、プレーヤー、市場を徹底的にレビューしている。本レポートは、バリューチェーン全体の主要プレーヤー(その多くは、データの集計を可能にする秘密保持契約に基づいてIDTechExにデータを提供している)へのインタビューを通じて収集した一次データと、入手可能なあらゆる情報源からの二次データを公平に分析したものであり、IDTechExのRFID業界に関する専門知識に基づいている。本レポートは、他の情報源にはない詳細な予測と分析を提供している。

IDTechExによると、RFIDの世界市場規模は2024年の150億米ドルから2025年には156億米ドルに拡大する見込みである。これは、RFIDラベル、カード、フォブ、その他あらゆるフォームファクター、およびパッシブRFIDとアクティブRFIDの両方のタグ、リーダー、ソフトウェア/サービスで構成される。

UHF分野では、タグ数で最大のRFIDアプリケーション分野である小売業がRFIDを採用し、力強い成長を続けている。IDTechExの調査によると、2025年には小売アパレルだけで310億個以上のRFIDタグが必要になるという。さらにIDTechExは、アパレル以外の小売商品へのタグ付けに関するウォルマートのような義務化によって、一般小売市場は成長を続けると予測している。これにより、この分野では引き続き大幅な数量成長が見込まれる。

非接触型カード販売は、主に非接触型決済、交通機関、セキュアアクセスアプリケーションに牽引され、HFセクターで最も成功を収めており、2025年には31億4,000万枚のカード需要が見込まれる。しかしIDTechExは、モバイルウォレットが非接触型カードに取って代わり続けるため、この需要は減少すると予想している。

動物(豚、羊、ペットなど)のタグ付けは、より多くの地域で法的要件となっているため、LFセクターでは依然として重要であり、2025年にはこのセクターで約9億3,000万個のタグが使用されると予想される。

全体として、IDTechExは2025年には約550億個のパッシブRFIDタグが販売されると予測しており、2024年の500億個から増加し、前年比10%の増加を示している。この成長の大部分はパッシブUHF RFIDラベルによるものである。しかし、2025年には、UHF (RAIN RFID)タグの販売額はHFタグの販売額(NFCを含む)の60% になると予想される。これは、セキュリティー(支払い、入退室など)に使 用されるHFタグの価格帯が高く、物品へのタグ付けに使用される安価で主に使い捨て のUHF(RAIN)タグに対抗するためである。しかし、UHF市場の活発化とHF市場の衰退により、タグ全体の売上高の差は縮小している。

地域別の成長機会と市場分布

パッシブRFIDタグの地域別最終用途別市場価値の分布は、RFID予測、プレーヤーと機会2026年から2036年の中で詳細に調査されている。IDTechExによるこの分析は、南北アメリカ、ヨーロッパ、アジア太平洋、中東アフリカ(MEA)の4つの主要地域に焦点を当てている。

2025年には、米州とアジア太平洋地域がパッシブRFIDタグの2大市場となり、米州は世界の最終用途の38%を占め、アジア太平洋地域は37%と僅差で続く。米州は、世界のUHFタグ使用の60%以上を占めるUHF RFIDの強力な採用により、わずかにリードしている。これは主に、ウォルマートやUPSのような企業による小売、アパレル、物流での広範な導入によるものである。アジア太平洋地域の地位は、非接触型カードに使用されるHF RFIDの歴史的に高い使用量によって支えられている。しかし、同地域では、モバイルウォレットの普及がカード発行を減少させ始めたため、2024年から2025年にかけて高周波タグの使用量が7%近く減少した。

欧州はパッシブRFID市場全体では第3位で、2025年の世界の最終用途の20%を占める。この地域の市場は主にUHF帯RFIDが牽引しており、欧州は世界のUHF帯最終用途の30%近くを占めている。成長を支えているのは、小売やアパレルなどの分野における大規模な展開と、2026年から一部の製品カテゴリーにアイテムレベルのトレーサビリティを義務付けるEUデジタル製品パスポートなどの今後の規制変更である。

中東・アフリカ地域は、パッシブRFIDの市場としては最も小さく、最も浸透しておらず、2025年の世界の最終用途の4%を占める。同地域最大のRFIDセグメントはHFであり、主に決済システムのデジタル化、現金離れ、非接触カードの採用拡大が牽引している。

地域別内訳と市場動向に関するより詳細な洞察は、レポート「RFID 2026-2036:予測、プレーヤー、機会」でご覧いただけます。

.png)

詳細な市場分析

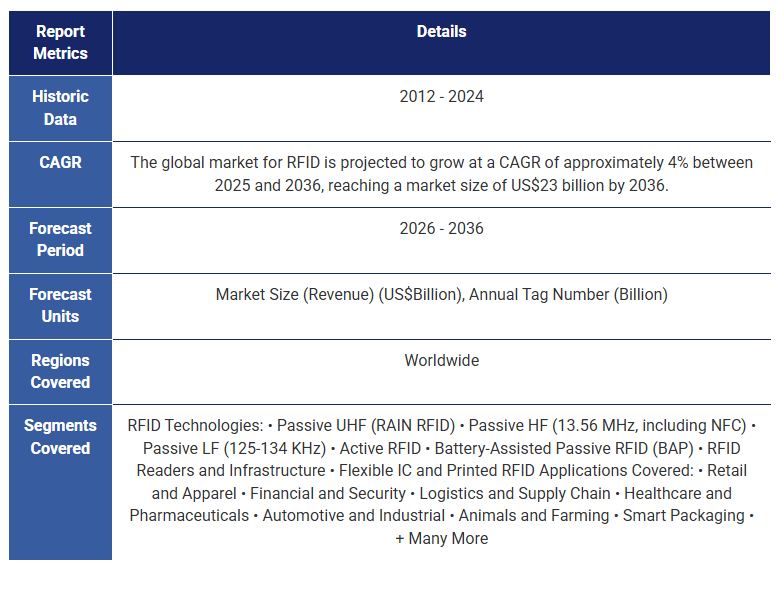

IDTechExでは、IDTechExのリサーチアナリストがグローバルに収集した新しくユニークな情報を用いて、RFID業界を様々な方法で評価しています。各市場は徹底的に調査され、2012年から2024年までのアプリケーションタイプ別の詳細な過去データが提供され、その後2026年以降2031年まで毎年予測されます。IDTechExは2036年までの長期予測も提供している。本レポートに含まれる主な予測は以下の通りである:パッシブRFID、バッテリーアシスト型パッシブRFID、アクティブRFID、RFIDリーダーのタグ数、平均販売価格、市場価格の10年予測、パッシブタグのエンドユース地域別市場規模予測。

さらに、以下のカテゴリーにおけるRFIDリーダーの販売台数、平均販売価格、合計金額を提供している。

IDTechExが実施した調査では、最終的にタグ、リーダーを含むアプリケーション分野別の10年予測を提供している、

地域別動向、バリューチェーンの位置づけ、NFC、チップ対チップレスなど、その他の分野についてもデータを提供している。RFIDの累積売上高を分析。数百のサプライヤーのマトリックスに加え、主要企業の進捗状況も提供。パッシブRFIDインレイの2つの主要タイプ、UHFとHF RFIDの価格分解を実施。

本レポートで回答する主な質問

IDTechExは本レポートの主要データを評価し、以下のような主な質問に回答している

例えば、IDTechEx は、サプライヤーへの包括的なインタビューを実施した結果、現在では様々な技術にわたるバリューチェーンのほとんどの場所で確立されたリーダーが存在することを発見したが、1億米ドル以上の収益をあげている企業はわずかであった。しかし、1億米ドル以上の収益を上げている企業はわずかであった。IDTechExの詳細分析レベルでは、バリューチェーン全体のデータを考慮することが可能であり、例えば、インレイの売上高はICの売上高に数ヶ月遅れており、これは予測において考慮されている。

主な市場予測は以下の通り:

10年間のRFID市場予測(周波数別、対応アプリケーション分野別)

1.パッシブUHF帯のタグ数および市場価値は以下の分野にセグメント化される

2.以下の分野でセグメント化されたパッシブHFタグ数と市場価値

3.以下の分野でセグメント化されたパッシブLFタグ数と市場価値

4.アクティブRFID5.RFIDリーダー6.パッシブRFID市場

目次1.要旨と結論

1.1.RFIDの歴史

1.2.2036年までのRFID市場

1.3.2024~2036年のRFID総市場規模、10億ドル

1.4.2024~2036年のアプリケーション別タグ価値別市場規模、百万ドル

1.5.2024〜2036年、アプリケーション別タグ価値別市場規模、百万ドル

1.6.2024~2036年のアプリケーション別、ハードウェア、ソフトウェア別市場規模、10億ドル

1.7.2025年対2036年の最大市場

1.8.好まれるRFID周波数

1.9.バリューチェーンとRFIDタグの種類

1.10.パッシブUHF(RAIN)RFIDタグ数 2024~2036年、百万個

1.11.パッシブUHF(RAIN)RFIDタグ数 2024~2036年、百万枚

1.12.パッシブUHF(RAIN)RFIDの用途別平均販売価格 2024-2036年、米セント

1.13.アプリケーション別UHF(RAIN)RFIDインレイの総額 2024-2036年、百万ドル

1.14.UHF(RAIN)RFIDインレイのアプリケーション別総額、2024~2036年、百万ドル

1.15.ウォルマートはRFIDを義務化

1.16.UHF(RAIN)RFID:ハイライト

1.17.UHF(RAIN)RFID:今後の展開

1.18.パッシブHF(13.56MHz、NFC)RFIDタグ数 2024~2036年、百万個

1.19.パッシブHF(13.56MHz、NFC)RFIDタグ数 2024~2036年、百万枚

1.20.パッシブHF(13.56MHz)RFIDのアプリケーション別平均販売価格 2024-2036, US cents

1.21.アプリケーション別高周波(13.56MHz)RFIDインレイとカードの総額 2024-2036年、百万ドル

1.22.2024~2036年における高周波(13.56MHz)RFIDインレイとカードのアプリケーション別総額、百万ドル

1.23.モバイル・ウォレットの出現により非接触カードの使用は減少している

1.24.フレキシブル集積回路がスマート・パッケージング向けにNFCを拡大する可能性

1.25.HF/NFC RFID:ハイライト

1.26.パッシブLF(125KHz、134KHz)RFIDタグ数 2024~2036年、百万個

1.27.パッシブLF (125KHz, 134KHz) RFID タグ数 2024-2036, millions

1.28.パッシブLF(13.56MHz)RFIDのアプリケーション別平均販売価格(2024~2036年)、USセント

1.29.2024~2036年、アプリケーション別LF RFIDインレイとカードの総額(百万ドル)

1.30.LF RFIDインレイとカードの合計金額(アプリケーション別) 2024-2036年、百万ドル

1.31.LF RFID: ハイライト

1.32.バッテリーアシスト型パッシブRFID、アクティブRFIDタグ数のRFID市場予測 2024-2036, millions

1.33.バッテリーアシストパッシブRFID、アクティブRFIDタグ数のRFID市場予測 2024-2036, millions

1.34.バッテリーアシスト型RFIDとアクティブRFIDのアプリケーション別合計金額 2024-2036年、百万ドル

1.35.BLEとLPWANによるアクティブRFIDシステムの変化

1.36.パッシブRFIDインレイのトップレベル市場価値と最終用途 地域別、2024~2036年、百万ドル

1.37.米州のRFID利用:主な結論

1.38.アジア太平洋地域のRFID利用:主な結論

1.39.欧州のRFID利用:主要結論

1.40.中東・アフリカ地域のRFID利用:主要結論主要結論

1.41.RFID企業の売上総利益

1.42.RFID市場成長の阻害要因

1.43.RFIDの展望

2.RFIDの導入、歴史的売上高、対応可能な機会

2.1.RFID

2.2.RFIDシステムの選択

2.3.RFID技術:全体像

2.4.RFIDバリューチェーン

2.5.パッシブRFID

2.6.パッシブRFIDシステム

2.7.バッテリーアシストパッシブ/セミアクティブタグ

2.8.バッテリーアシストパッシブ(BAP)RFIDセンサーの例

2.9.RFIDセンサー

2.10.アクティブRFID

2.11.アクティブRFIDで遠くのものを識別する

2.12.リアルタイム・ロケーティング・システム(RTLS)

2.13.BLEとLPWANによるアクティブRFIDシステムの変化

2.14.歴史的なパッシブLF(125KHz、134KHz)RFIDタグの販売 2012~2024年

2.15.パッシブLF(125KHz、134KHz)RFIDタグの販売個数(2012~2024年)

2.16.パッシブLF(125KHz、134KHz)RFIDタグの平均販売価格、2012~2024年

2.17.パッシブLF(125KHz、134KHz)RFIDタグ市場規模、2012~2024年

2.18.パッシブHF(13.56MHz、NFC)RFIDタグの歴史的販売枚数 2012~2024

2.19.パッシブHF(13.56MHz、NFC)RFIDタグの販売個数(2012~2024年)

2.20.パッシブHF(13.56MHz、NFC)RFIDタグの平均販売価格(2012~2024年)

2.21.パッシブHF(13.56MHz、NFC)RFIDタグ市場規模、2012年~2024年

2.22.パッシブUHF(RAIN)RFIDタグの歴史的売上高:2012~2024年

2.23.パッシブUHF(RAIN)RFIDタグの販売個数(2012~2024年)

2.24.パッシブUHF(RAIN)RFIDタグの平均販売価格、2012~2024年

2.25.パッシブUHF(RAIN)RFIDタグ市場規模推移、2012年~2024年

2.26.アクティブRFIDタグの歴史的販売枚数(2017年~2024年)

2.27.アクティブタグ販売個数(単位)、2017年~2024年

2.28.アクティブタグの平均販売価格、2017年~2024年

2.29.アクティブタグ市場規模、2017年~2024年

2.30.パッシブRFIDインテロゲータ(リーダー)タグ売上高推移 2012~2024

2.31.パッシブRFIDインテロゲータ(リーダー)売上(単位)、2012年~2024年

2.32.パッシブRFIDインテロゲータ市場規模(2012年~2024年)

2.33.RFID規格(ISO)

2.34.高周波RFIDとNFCアプリケーション

2.35.HF RFID/NFCの成長

2.36.UHF(RAIN)RFIDの動向

2.37.RAIN RFIDの4つの推進要因

2.38.EPC Gen2v3

2.39.RFIDシステム/ミドルウェア

2.40.RFIDソフトウェアビジネス(1)

2.41.RFIDソフトウェア事業(2)

2.42.RFIDソフトウェアビジネス(3)

2.43.RFID最量販の阻害要因

3.アプリケーション別市場とバリューチェーンの位置づけ

3.1.RFID総市場規模 2024-2036, 10億ドル

3.2.アプリケーション別タグ価値別市場規模 2024-2036, $ millions

3.3.アプリケーション別タグ価値別市場規模 2024-2036, $ millions

3.4.アプリケーション別、ハードウェアとソフトウェアによる市場規模 2024-2036, $ billions

3.5.アプリケーション分野別の現在と将来の回収形態

3.6.ヘルスケアと医薬品

3.7.ヘルスケアと医薬品におけるRFID

3.8.医療と医薬品におけるRFIDアプリケーション

3.9.病院におけるリアルタイム位置情報システム

3.10.RFIDのペイバック例 医療・医薬品

3.11.新たな規制と導入の障壁

3.12.ヘルスケアと医薬品のケーススタディ

3.13.英国プリマスNHS、医療機器の追跡にRFIDを使用

3.14.Bluesight社、2,400の病院でRFIDによる投薬追跡を拡大

3.15.Becton Dickinson社がプレフィルドシリンジのアイテムレベル追跡用のRFIDを試作

3.16.インプラントキャスト社におけるRFIDによるインプラント物流の合理化

3.17.医療分野におけるRFID導入の障壁

3.18.IDTechExの展望:医療/ヘルスケアにおけるRFIDの現在の役割

3.19.小売&消費者向けパッケージ商品

3.20.パレット/ケースタギング:誤ったスタート

3.21.小売アパレル、アイテムレベル(1)

3.22.小売アパレル、アイテムレベル(2)

3.23.小売一般&アパレル

3.24.世界のUHF帯RFID普及率は小売・アパレルがリード

3.25.EUのデジタル・プロダクト・パスポート(DPP)がアイテム・レベルのトレーサビリティ要件を推進

3.26.ウォルマートの義務化による影響

3.27.ウォルマートのRFID義務化の拡大

3.28.M&S RFIDの展開

3.29.小売アパレルの回収

3.30.偽造防止のためのRFID

3.31.アパレルと小売のケーススタディ

3.32.RAIN RFIDを導入し、成長している小売企業の事例

3.33.2023年以降にRFIDを導入した小売企業

3.34.2023年以降にRFIDを導入した小売企業

3.35.日本の経済産業省、2025年までに1,000億タグ/年の目標は実現せず

3.36.ケーススタディRFID Demand Pull (1)

3.37.ケーススタディRFIDデマンドプル(2)

3.38.小売・アパレルにおけるRFID クイックサマリー

3.39.飲食料品小売業

3.40.RFIDを使った食品と飲料のタグ付け

3.41.現在の課題と障害、そしてなぜ導入が低いままなのか

3.42.米国FDAは2026年1月までに食品トレーサビリティを義務化

3.43.クローガー社のRFID展開は鮮度と持続可能性を目標としている

3.44.航空業界

3.45.空港と航空会社は手荷物受取にRFIDを利用

3.46.航空会社と空港のRFID成長

3.47.RFIDに対抗する技術:コンピュータ・ビジョン

3.48.エアアジア、RFIDを使ってライフジャケットを追跡

3.49.安全なアクセスと非接触決済

3.50.金融取引におけるNFCと高周波RFID

3.51.安全なアクセスと非接触決済

3.52.スマート・チケッティング

3.53.スマート・チケッティング

3.54.スマート・チケッティングと非接触決済の比較

3.55.スマート・チケッティングの競合技術のベンチマーク

3.56.物流、小包、郵便:資産追跡、製造

3.57.物流と小包の取り扱いはRFID成長の新たなフロンティア

3.58.郵便・宅配便

3.59.UPSは施設を通じてRFIDを展開する

3.60.物流、資産追跡、製造

3.61.物流コンテナの追跡

3.62.RFIDは自動車のボディパネルを追跡する

3.63.食品及びその他の物流業界におけるRFIDのケーススタディ

3.64.Chipotle社はトレーサビリティと食品安全のためにパレットレベルのRFIDを使用

3.65.マクドナルドは持続可能性と効率性のためにRFIDを利用している

3.66.ランドリー/レンタルテキスタイル

3.67.ランドリー/レンタルテキスタイル

3.68.その他

3.69.電子パスポート

3.70.動物のタグ付け

3.71.RFIDは消費者のエンゲージメントを高め、より多くのデータ利用を可能にする

3.72.家電機器へのRFID組み込み(1)

3.73.家電機器に埋め込まれるRFID(2)

3.74.RFIDセンサー

3.75.RFIDセンサーの種類

3.76.RFIDセンサー:主な選択肢

3.77.パワーキャストのRFIDセンサー

3.78.パッシブRFIDセンサー(電子式):ケーススタディ

3.79.プリンテッドエレクトロニクスによるパッシブUHF RFIDセンサー

3.80.LG センシング・スマートカード:水の塩分濃度を検査するための印刷アンテナ付き商用製品。韓国で発売

3.81.有機光検出器を使った薄型指紋センサー

3.82.スマート・パッケージング

3.83.NFCの機能的応用 消費財のスマート包装内

3.84.高級品分野におけるNFC スマート・パッケージングとアパレル

3.85.NFCスマートパッケージング採用への障壁

3.86.フレキシブル・ハイブリッド・エレクトロニクスによるスマート包装

3.87.フレキシブル集積回路はスマート包装用のNFC を拡大する可能性がある

3.88.循環経済のためのフレキシブルIC パイロットとケーススタディ

3.89.温度と動きの「センサーレス」センシング

3.91.FMCG分野におけるNFC スマートパッケージングとアパレル

3.92.コネクテッド・エクスペリエンスのためにNFC を使用するシャープエンド

3.93.RFIDとスマート・パッケージング:SWOT分析

3.94.RFIDとスマート包装:結論

4.パッシブRFID:タグコストの内訳、市場価値、新たな技術オプション

4.1.パッシブRFIDタグ、総数2024~2036年、10億個

4.2.パッシブRFIDタグ、市場価値、2024~2036年、百万ドル

4.3.RFID 範囲対コスト

4.4.パッシブRFID:動作周波数別技術

4.5.パッシブHFタグとUHFタグの構造

4.6.HF/NFCコイルとの接触における課題

4.7.アンテナ技術の選択

4.8.アンテナ製造技術:比較表

4.9.RFIDアンテナ:新技術

4.10.印刷 RFID アンテナは普及に苦戦:銅インクは解決策か?

4.11.RFID とスマート・パッケージングに必要な導電性インク

4.12.IC アタッチメント

4.13.IC 取り付けプロセス

4.14.今日のインレイ・アセンブリー

4.15.ラベル変換

4.16.RFID製造トレンド

4.17.パッシブRFIDの価格、HFとUHF

4.18.コモディティ・インレイ市場での生き残り

4.19.完全印刷ICはシリコンとの競争に苦戦

4.20.プリンテッドロジックへの現在のアプローチ

4.21.フレキシブル金属酸化物IC

4.22.フレキシブル/プリンテッド・ロジックの利点

4.23.IC実装コストの削減?

4.24.酸化金属ICへの投資は続く

4.25.UHFとNFCアプリケーションに革命を起こすプラグマティックFlexICのさらなる計画

4.26.SWOT分析:フレキシブル基板上の蒸着金属酸化物IC

5.パッシブRFIDへの脅威

5.1.パッシブ RFID - SWOT 分析

5.2.QR コード/バーコード - SWOT 分析

5.3.マシンビジョン - SWOT分析

5.4.パッシブRFIDへの脅威:マシンビジョン?

5.5.アマゾン・フレッシュ、RFID技術をアマゾン・フレッシュ店舗内に置き換える

5.6.顔認識システム

5.7.RFIDとコンピュータ・ビジョンを組み合わせる?

5.8.パッシブBluetooth

6.パッシブUHF(レイン)RFIDの市場データ

6.1.パッシブUHF(レイン)RFIDタグ数 2024~2036年、百万枚

6.2.パッシブ UHF(レイン)RFID タグ数 2024-2036 年、百万枚

6.3.パッシブUHF(RAIN)RFIDのアプリケーション別平均販売価格 2024-2036年、米セント

6.4.アプリケーション別UHF(RAIN)RFIDインレイの総額 2024-2036年、百万ドル

6.5.UHF(RAIN)RFIDインレイのアプリケーション別合計金額 2024-2036年、百万ドル

6.6.UHF (RAIN) RFID: ハイライト

6.7.UHF(RAIN)RFID:今後の展開

6.8.RAIN RFID ICとタグ販売数の比較

6.9.方法論に関するコメント

7.パッシブHF(およびNFC)RFIDの市場データ

7.1.パッシブ HF(13.56MHz、NFC)RFID タグ数 2024-2036 年、百万枚

7.2.パッシブHF(13.56MHz、NFC)RFIDタグ数 2024~2036年、百万枚

7.3.パッシブHF(13.56MHz)RFIDのアプリケーション別平均販売価格 2024-2036年, US cents

7.4.アプリケーション別高周波(13.56MHz)RFIDインレイとカードの合計金額 2024-2036年, millions

7.5.2024~2036年におけるHF帯(13.56MHz)RFIDインレイとカードのアプリケーション別合計金額(百万ドル)

7.6.HF/NFC RFID市場の動向

8.パッシブ LF(125KHz、134KHz)RFID タグの市場データ

8.1.パッシブLF(125KHz、134KHz)RFIDタグの数 2024-2036年, 百万ドル

8.2.パッシブ LF (125KHz, 134KHz) RFID タグ数 2024-2036年, 百万

8.3.パッシブ LF(13.56MHz)RFIDのアプリケーション別平均販売価格 2024-2036年, US cents

8.4.アプリケーション別 2024-2036 年の LF RFID インレイとカードの合計金額(百万ドル)

8.5.アプリケーション別 2024-2036 年の LF RFID インレイとカードの合計金額(百万ドル)

9.アクティブRFIDの市場と収益性

9.1.アクティブRFID市場

9.2.BLEとLPWANによるアクティブRFIDシステムの変化

9.3.競合するLPWAN技術は

9.4.無線技術の概要

9.5.WLANネットワークプロトコルの比較

9.6.LPWAN 機能の比較

9.7.バッテリーアシスト型パッシブRFID、アクティブRFIDタグ数のRFID市場予測 2024-2036年, 百万ドル

9.8.バッテリーアシストパッシブRFID、アクティブRFIDタグ数のRFID市場予測 2024-2036年, 百万ドル

9.9.バッテリーアシスト型RFIDとアクティブ型RFIDのアプリケーション別合計金額 2024-2036年, 百万ドル

10.RFIDインテロゲータ市場

10.1.(RFIDリーダー)

10.2.概要

10.3.クアルコムがSnapdragonプラットフォームへのUHF統合を発表

10.4.RFIDインテロゲータ(リーダー)数 2024-2036年, 百万ドル

10.5.RFIDインテロゲータ(リーダー)価格 2024~2036年、米セント

10.6.RFIDインテロゲータ(リーダー)市場価値 2024-2036年、百万ドル

10.7.RFIDインテロゲータ(リーダー)市場価値 2024-2036年、百万ドル

11.地域別市場

11.1.パッシブ LF(125KHz、134KHz)RFID インレイの地域別合計金額、2024~2036 年、百万ドル

11.2.パッシブ LF(125KHz、134KHz)RFID インレーの地域別合計金額、2024~2036 年、百万ドル

1.3.パッシブ HF(13.56MHz、NFC)RFID インレーの地域別合計金額、2024~2036 年、百万ドル

11.4.パッシブ HF(13.56MHz、NFC)RFID インレイの地域別合計金額、2024~2036 年、百万ドル

11.5.UHF (RAIN) RFID インレーの地域別市場合計金額、2024~2036 年、百万ドル

11.6.地域別 UHF(RAIN)RFIDインレーの合計市場価値、2024~2036年、百万ドル

11.7.パッシブ RFID インレーの地域別合計金額、2024~2036 年、百万ドル

11.8.パッシブRFIDインレーの地域別合計金額、2024-2036年、百万ドル

11.9.パッシブRFIDインレイのトップレベル市場価値と最終用途 地域別、2024~2036年、百万ドル

11.10.パッシブRFIDインレイと最終用途地域のトップレベル市場価値、2024~2036年、百万ドル

11.11.米州のRFID利用:主要結論

11.12.アジア太平洋地域の RFID 用途:主要結論

11.13.欧州 RFID 用途:主要結論

11.14.中東・アフリカ地域のRFID利用:主要結論

11.15.RFID企業の本社所在地

11.16.方法論に関するコメント

12.成功、失敗、トレンド、機会

12.1.RFIDバリューチェーンのダイナミクス

12.2.タグ製造バリューチェーン

12.3.主要企業の買収(1)

12.4.主要企業の買収(2)

12.5.RFIDの収益性(1)

12.6.RFIDの収益性(2)

12.7.最大の受注、最も売れている製品、今後の有力サプライヤー

12.8.チップの最大サプライヤー

12.9.タグ、インレット、ストラップの最大サプライヤー、大量生産のための詳細なバリューチェーン

12.10.チップからラベルまでのバリューチェーンにおける企業の例

12.11.UHF RFIDリーダー

12.12.機器の供給

12.13.RFID の展望

13.RFIDソリューション・プロバイダー

13.1.RFIDバリューチェーン(1)

13.2.RFIDバリューチェーン(2)

14.企業プロファイル

14.1.IDTechExポータルの企業プロファイルへのアクセス

Summary

The complete analysis of the global RFID industry.

IDTechEx has been researching the RFID industry for nearly two decades. "RFID Forecasts, Players, and Opportunities 2026-2036" is the most recent RFID market research study, offering a thorough review of passive RFID (for UHF, HF, and LF bands), battery assisted passive, active RFID, and chipless RFID technologies, players, and markets. This report provides an unbiased analysis of primary data gathered through interviews with key players throughout the value chain (many of whom supply data to IDTechEx under non-disclosure agreements that allows aggregation of the data into a total) as well as secondary data from all available sources, and it builds on IDTechEx's RFID industry expertise. This report provides in-depth forecasts and analysis that no other source can match.

Current market and outlook

The future of RFID is looking bright, the global RFID market is expected to expand further in 2025; according to IDTechEx, the market will be worth US$15.6 billion in 2025, up from US$15 billion in 2024. This comprises RFID labels, cards, fobs, and any other form factors, as well as tags, readers, and software/services for both passive and active RFID.

In the UHF sector, the retail business, the largest RFID application sector in terms of tag numbers, adopting RFID continues to grow strongly. According to IDTechEx study, retail apparel alone will require over 31 billion RFID tags in 2025 - though there is still some way to go, with RFID accounting for only about 40% of the total addressable market for apparel. Furthermore, IDTechEx anticipates that the general retail market will continue to grow driven by mandates such as Walmart's on tagging retail items other than apparel. This is anticipated to continue to generate significant volume growth for the sector.

Contactless card sales remain the most successful in the HF sector, driven primarily by contactless payment, transit, and secure access applications, with 3.14 billion cards anticipated to be demanded in 2025. However IDTechEx expects a decrease in demand for this as mobile wallets continue to replace contactless cards.

Animal tagging (such as pigs, sheep, and pets) remains important in the LF sector because it is still a legal requirement in many more areas, with around 930 million tags expected to be used in this sector in 2025.

Overall, IDTechEx forecasts that around 55 billion passive RFID tags will be sold in 2025, up from 50 billion in 2024, indicating a 10% year on year increase. The bulk of this growth is due to passive UHF RFID labels. However, in 2025, UHF (RAIN RFID) tag sales by value will be 60% of HF tag sales (including NFC), due to the higher price point of HF tags used for security (such as payments, access, etc) against the cheaper, largely disposable UHF (RAIN) tags used for tagging items. However, the gap between the overall tag sales is shrinking due to increased activity in UHF market and decline of HF market.

Geographic Growth Opportunities and Market Distribution

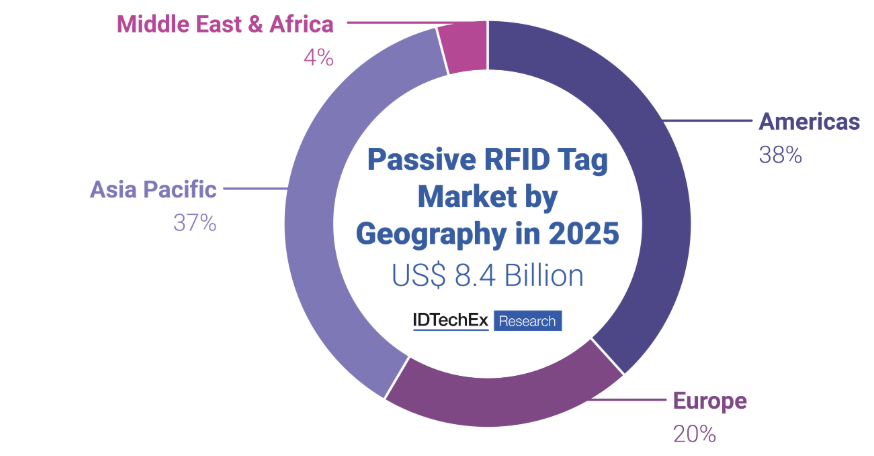

The distribution of passive RFID tag market value by end use across regions is explored in detail within RFID Forecasts, Players and Opportunities 2026 to 2036. This analysis by IDTechEx focuses on four key regions: the Americas, Europe, Asia Pacific, and the Middle East and Africa (MEA).

In 2025, the Americas and Asia-Pacific are the two largest markets for passive RFID tags, with the Americas accounting for 38 percent of global end use and Asia-Pacific close behind at 37 percent. The Americas holds a slight lead, driven by strong adoption of UHF RFID, which makes up over 60 percent of global UHF tag use. This is largely due to widespread deployments in retail, apparel, and logistics by companies such as Walmart and UPS. Asia-Pacific's position is supported by historically high volumes of HF RFID used in contactless cards. However, the region saw a nearly 7 percent decline in HF tag use from 2024 to 2025 as the growing use of mobile wallets began to reduce card issuance.

Europe ranks third in the passive RFID market overall, accounting for 20% of global end use in 2025. The region's market is primarily driven by UHF RFID, with Europe making up nearly 30% of global UHF end use. Growth is supported by large-scale deployments in sectors such as retail and apparel, as well as upcoming regulatory changes including the EU Digital Product Passport, which mandates item-level traceability for select product categories starting in 2026.

The Middle East and Africa region is the smallest and least penetrated market for passive RFID, accounting for four percent of global end use in 2025. The region's largest RFID segment is HF, mainly driven by the digitalization of payment systems, a shift away from cash, and growing adoption of contactless cards.

More detailed insights into the regional breakdown and market trends can be found in the report "RFID 2026-2036: Forecasts, Players and Opportunities".

In-depth market analysis

IDTechEx assesses the RFID industry in a variety of ways using new and unique information gathered globally by IDTechEx research analysts. Each market is thoroughly examined, with detailed historical data by application type provided from 2012 to 2024, followed by a prediction from 2026 and every year thereafter until 2031. IDTechEx also provides a long-term forecast for 2036. Key forecasts included in this report are: 10-year prediction of tag numbers, average sales price, and market value of Passive RFID, Battery-assisted Passive RFID, Active RFID, and RFID readers, Forecast for the Passive tag market size by end use geography.

Additionally, the report provides units, average selling price and total value for RFID readers in the following categories

The research conducted by IDTechEx ultimately provides ten-year forecasts by application area including tags, readers, software and services for the following markets

Data is also provided for other sectors including trends by territory, value chain positioning, NFC, chip vs chipless and more. Cumulative sales of RFID are analyzed. Progress of key companies is provided in addition to a matrix of hundreds of suppliers. A price teardown is conducted for the two main types of passive RFID inlays - UHF and HF RFID.

Key questions answered in this report

IDTechEx evaluates the key data in this report to answer key questions such as

For example, IDTechEx discovered that there are now established leaders in most places of the value chain across the various technologies after conducting comprehensive interviews with suppliers, but that only a few businesses had revenues of more than US$100 million. There are still numerous opportunities, which are evaluated in this report. IDTechEx's level of detailed analysis allows us to account for data throughout the value chain, for example, inlay sales lag the number of IC sales by several months which is considered in our forecasts.

Key market forecasts include:

10-year Market forecast of RFID segmented by each frequency and corresponding application sectors

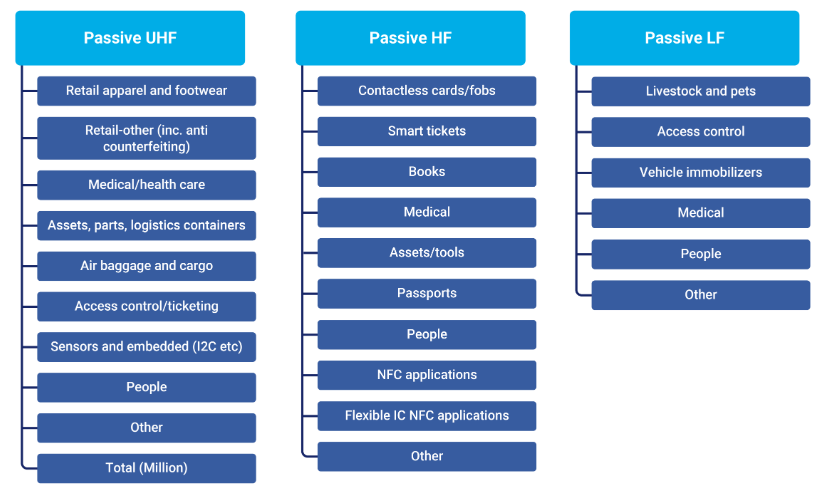

1. Passive UHF tag numbers and market value segmented in the following sectors

2. Passive HF tag numbers and market value segmented in the following sectors

3. Passive LF tag numbers and market value segmented in the following sectors

4. Active RFID5. RFID readers6. Passive RFID market value segmented in the following regions

Table of Contents1. EXECUTIVE SUMMARY AND CONCLUSIONS

1.1. Brief History of RFID

1.2. RFID Market to 2036

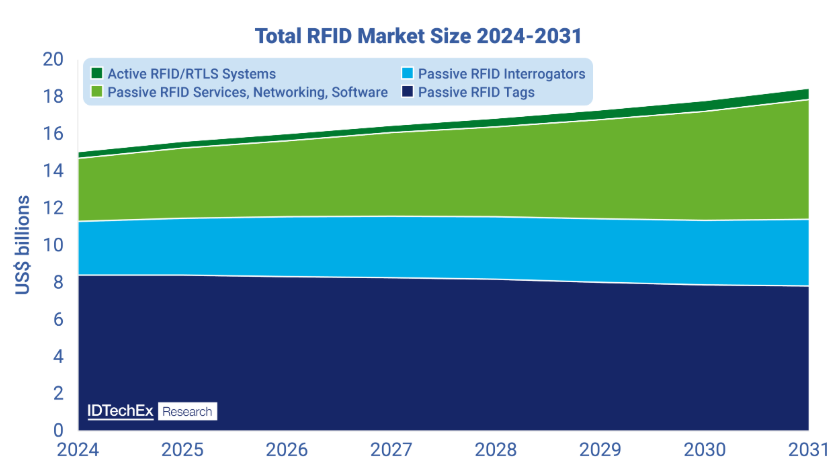

1.3. Total RFID Market Size 2024-2036, $ billions

1.4. Market size by tag value by application 2024-2036, $ millions

1.5. Market size by tag value by application 2024-2036, $ millions

1.6. Market size by application, hardware and software 2024-2036, $ billions

1.7. Largest markets in 2025 vs 2036

1.8. Favourite RFID frequencies

1.9. Value chain and RFID tag types

1.10. Passive UHF (RAIN) RFID tag numbers 2024-2036, millions

1.11. Passive UHF (RAIN) RFID tag numbers 2024-2036, millions

1.12. Average sales price of passive UHF (RAIN) RFID by application 2024-2036, US cents

1.13. Total Value of UHF (RAIN) RFID inlays by application 2024-2036, $ millions

1.14. Total Value of UHF (RAIN) RFID inlays by application, 2024-2036, $ millions

1.15. Walmart Grows its RFID Mandate

1.16. UHF (RAIN) RFID: The Highlights

1.17. UHF (RAIN) RFID: Forthcoming Developments

1.18. Passive HF (13.56MHz, NFC) RFID tag numbers 2024-2036, millions

1.19. Passive HF (13.56MHz, NFC) RFID tag numbers 2024-2036, millions

1.20. Average sales price of passive HF (13.56MHz) RFID by application 2024-2036, US cents

1.21. Total value of HF (13.56MHz) RFID inlays and cards by application 2024-2036, $ millions

1.22. Total value of HF (13.56MHz) RFID inlays and cards by application 2024-2036, $ millions

1.23. The use of contactless cards is decreasing with the advent of mobile wallets

1.24. Flexible Integrated Circuits May Scale NFC for Smart Packaging

1.25. HF/NFC RFID: The Highlights

1.26. Passive LF (125KHz, 134KHz) RFID tag numbers 2024-2036, millions

1.27. Passive LF (125KHz, 134KHz) RFID tag numbers 2024-2036, millions

1.28. Average sales price of passive LF (13.56MHz) RFID by application 2024-2036, US cents

1.29. Total value of LF RFID inlays and cards by application 2024-2036, $ millions

1.30. Total value of LF RFID inlays and cards, by application 2024-2036, $ millions

1.31. LF RFID: The Highlights

1.32. RFID market forecasts for battery assisted passive RFID, active RFID tag numbers 2024-2036, millions

1.33. RFID market forecasts for battery assisted passive RFID, active RFID tag numbers 2024-2036, millions

1.34. Total value of battery assisted and active RFID by application 2024-2036, $ millions

1.35. Change in active RFID systems due to BLE and LPWAN

1.36. Top Level Market Value of Passive RFID inlays and end use Geography, 2024-2036, $ millions

1.37. Americas RFID Use: Key Conclusions

1.38. Asia-Pacific RFID Use: Key Conclusions

1.39. Europe RFID Use: Key Conclusions

1.40. Middle East & Africa RFID Use: Key Conclusions

1.41. RFID companies by gross sales

1.42. Impediments to the growth of RFID markets

1.43. Outlook for RFID

2. INTRODUCTION, HISTORIC RFID SALES, AND ADDRESSABLE OPPORTUNITY

2.1. RFID

2.2. RFID system choices

2.3. RFID technologies: The big picture

2.4. The RFID value chain

2.5. Passive RFID

2.6. Passive RFID Systems

2.7. Battery Assisted Passive /Semi Active tags

2.8. Examples of Battery Assisted Passive (BAP) RFID sensors

2.9. RFID sensors

2.10. Active RFID

2.11. Distinguishing things a long way away with active RFID

2.12. Real Time Locating Systems (RTLS)

2.13. Change in active RFID systems due to BLE and LPWAN

2.14. Historic Passive LF (125KHz, 134KHz) RFID tag sales 2012 to 2024

2.15. Passive LF (125KHz, 134KHz) RFID tag sales in units, 2012- 2024

2.16. Passive LF (125KHz, 134KHz) RFID tag Average Selling Price, 2012- 2024

2.17. Passive LF (125KHz, 134KHz) RFID tag market size, 2012- 2024

2.18. Historic Passive HF (13.56MHz, NFC) RFID tag sales 2012 to 2024

2.19. Passive HF (13.56MHz, NFC) RFID tag sales in units, 2012- 2024

2.20. Passive HF (13.56MHz, NFC) RFID tag Average Selling Price, 2012- 2024

2.21. Passive HF (13.56MHz, NFC) RFID tag market size, 2012- 2024

2.22. Historic Passive UHF (RAIN) RFID tag sales 2012 to 2024

2.23. Passive UHF (RAIN) RFID tag sales in units, 2012- 2024

2.24. Passive UHF (RAIN) RFID tag Average Selling Price, 2012- 2024

2.25. Passive UHF (RAIN) RFID tag market size, 2012- 2024

2.26. Historic Active RFID tag sales 2017 to 2024

2.27. Active tag sales in units, 2017- 2024

2.28. Active tag Average Selling Price, 2017- 2024

2.29. Active tag market size, 2017- 2024

2.30. Historic Passive RFID Interrogators (Readers) tag sales 2012 to 2024

2.31. Passive RFID Interrogators sales in units, 2012- 2024

2.32. Passive RFID Interrogators market size, 2012- 2024

2.33. RFID Standards (ISO)

2.34. HF RFID & NFC Applications

2.35. HF RFID/NFC Growth

2.36. UHF (RAIN) RFID Trends

2.37. Four Drivers of RAIN RFID

2.38. EPC Gen2v3

2.39. RFID Systems/Middleware

2.40. RFID Software Business (1)

2.41. RFID Software Business (2)

2.42. RFID Software business (3)

2.43. Impediments to highest volume RFID

3. MARKETS BY APPLICATION AND VALUE CHAIN POSITION

3.1. Total RFID Market Size 2024-2036, $ billions

3.2. Market size by tag value by application 2024-2036, $ millions

3.3. Market size by tag value by application 2024-2036, $ millions

3.4. Market size by application, hardware and software 2024-2036, $ billions

3.5. Current and future forms of payback by applicational sector

3.6. Healthcare & Pharmaceuticals

3.7. RFID in Healthcare and pharmaceuticals

3.8. RFID Applications in Healthcare and Pharmaceuticals

3.9. Real Time Locating Systems in Hospitals

3.10. Example of RFID paybacks Healthcare and pharmaceuticals

3.11. New Regulations and Adoption Barriers

3.12. Case Studies of Healthcare & Pharmaceuticals

3.13. Plymouth NHS, UK, uses RFID to Track Their Medical Devices

3.14. Bluesight Scales RFID Medication Tracking Across 2,400 Hospitals

3.15. Becton Dickinson Prototypes RFID for Item Level Tracking of Pre-Filled Syringes

3.16. RFID Streamlines Implant Logistics at Implantcast

3.17. Barriers of RFID adoption in healthcare sectors

3.18. IDTechEx Outlook: RFID Current Role within Medical / Healthcare

3.19. Retail & Consumer Packaged Goods

3.20. Pallet/case tagging: False start

3.21. Retail apparel, item level (1)

3.22. Retail apparel, item level (2)

3.23. Retail General & Apparel

3.24. Retail & Apparel Lead in Global UHF RFID Penetration

3.25. EU Digital Product Passport (DPP) Drives Item-Level Traceability Requirements

3.26. The impact from Walmart's mandate

3.27. Walmart Grows its RFID Mandate

3.28. M&S RFID roll-out

3.29. Retail Apparel Payback

3.30. RFID for anti-counterfeiting

3.31. Case Studies of Apparel & Retail

3.32. Examples of retailers using RAIN RFID and growing

3.33. Retail Companies Who have implemented RFID since 2023

3.34. Retail Companies Who have implemented RFID since 2023

3.35. METI, Japan, target 100 billion tags/year by 2025 is not be realized

3.36. Case Study: RFID Demand Pull (1)

3.37. Case Study: RFID Demand Pull (2)

3.38. RFID in Retail & Apparel Quick Summary

3.39. Retail Food & Drink

3.40. Using RFID to Tag Food and Drink

3.41. Current Challenges and Obstacles and why adoption remains low

3.42. US FDA Mandated Food traceability by January 2026

3.43. Kroger's RFID Rollout Targets Freshness and Sustainability

3.44. Aviation Industry

3.45. Airports and Airlines use RFID for baggage claim

3.46. Airline and Airport for RFID Growth

3.47. Competing technologies to RFID: Computer vision

3.48. AirAsia Tracks Life Jackets Using RFID

3.49. Secure access and contactless payment

3.50. NFC and HF RFID within Financial Transactions

3.51. Secure access and contactless payment

3.52. Smart ticketing

3.53. Smart ticketing

3.54. Smart ticketing vs contactless payments

3.55. Benchmark of competing technologies for smart ticketing

3.56. Logistics, Parcels & Postal: Asset Tracking, Manufacturing

3.57. Logistics and Parcel Handling Are Emerging Frontiers for RFID Growth

3.58. Postal and courier services

3.59. UPS to deploy RFIDs through its facilities

3.60. Logistics, Asset Tracking, Manufacturing

3.61. Tracking Logistics Containers

3.62. RFID tracks automotive body panels

3.63. Case studies of RFID in food and other logistics industry

3.64. Chipotle Uses Pallet-Level RFID for Traceability and Food Safety

3.65. McDonalds uses RFID for Sustainability & Efficiency

3.66. Laundry/rented textiles

3.67. Laundry/rented textiles

3.68. Others

3.69. E-Passports

3.70. Animal Tagging

3.71. RFID provides more consumer engagement and enables more data use

3.72. RFID embedded in consumer electronics devices (1)

3.73. RFID embedded in consumer electronics devices (2)

3.74. RFID Sensors

3.75. RFID Sensor Types

3.76. RFID Sensors: Main choices

3.77. Powercast's RFID Sensor

3.78. Passive RFID Sensors (Electronic): Case studies

3.79. Passive UHF RFID sensors with printed electronics

3.80. LG Sensing Smart Card: Commercial product with a printed antenna to test water salinity. Launched in Korea

3.81. Thin finger print sensors using organic photodetectors

3.82. Smart Packaging

3.83. Functional applications of NFC Within Smart packaging on Consumer goods

3.84. NFC Smart Packaging & Apparel within the Luxury Sector

3.85. Barriers To NFC Smart packaging Adoption

3.86. Smart packaging with flexible hybrid electronics

3.87. Flexible Integrated Circuits May Scale NFC for Smart Packaging

3.88. Flexible IC Pilots and Case Studies for Circular Economy

3.89. NFC for product registration and authentication

3.90. 'Sensor-less' sensing of temperature and movement

3.91. NFC Smart Packaging & Apparel within the FMCG Sector

3.92. SharpEnd using NFC for connected experiences

3.93. RFID and Smart Packaging: SWOT analysis

3.94. RFID and smart packaging: Conclusions

4. PASSIVE RFID: TAG COST TEARDOWN, MARKET VALUE AND EMERGING TECHNOLOGY OPTIONS

4.1. Passive RFID tags, total number 2024-2036, billions

4.2. Passive RFID tags, market value, 2024-2036, $ millions

4.3. RFID Range versus cost

4.4. Passive RFID: Technologies by operating frequency

4.5. Anatomy of passive HF and UHF tags

4.6. Challenges in contacting HF/NFC coils

4.7. Antenna Technology Choices

4.8. Antenna Manufacturing Technologies: Comparison Table

4.9. RFID Antennas: New Technologies

4.10. Printed RFID antennas struggle for traction: Is copper ink a solution?

4.11. Conductive ink requirements for RFID and smart packaging

4.12. IC Attachment

4.13. IC attachment processes

4.14. Inlay assembly today

4.15. Label Conversion

4.16. RFID Manufacturing trends

4.17. Passive RFID price teardown, HF and UHF

4.18. Surviving in a commodity inlay market

4.19. Fully printed ICs have struggled to compete with silicon

4.20. Current approaches to printed logic

4.21. Flexible metal oxide ICs

4.22. Benefits of flexible/printed logic

4.23. Save on IC attach cost?

4.24. Investment into metal oxide ICs continues

4.25. Pragmatic FlexIC further plan to revolutionises UHF and NFC Applications

4.26. SWOT analysis: Evaporated metal oxide ICs on flexible substrates

5. THREATS TO PASSIVE RFID

5.1. Passive RFID - SWOT Analysis

5.2. QR codes/Barcodea - SWOT Analysis

5.3. Machine vision - SWOT Analysis

5.4. Threats to passive RFID: Machine vision?

5.5. Amazon Fresh Replaces RFID technology within Amazon Fresh Stores

5.6. Facial recognition system

5.7. Combine RFID and computer vision?

5.8. Passive Bluetooth

6. MARKET DATA FOR PASSIVE UHF (RAIN) RFID

6.1. Passive UHF (RAIN) RFID tag numbers 2024-2036, millions

6.2. Passive UHF (RAIN) RFID tag numbers 2024-2036, millions

6.3. Average sales price of passive UHF (RAIN) RFID by application 2024-2036, US cents

6.4. Total Value of UHF (RAIN) RFID inlays by application 2024-2036, $ millions

6.5. Total Value of UHF (RAIN) RFID inlays by application, 2024-2036, $ millions

6.6. UHF (RAIN) RFID: The Highlights

6.7. UHF (RAIN) RFID: Forthcoming Developments

6.8. RAIN RFID ICs versus tag numbers sold

6.9. Comment on methodology

7. MARKET DATA FOR PASSIVE HF (AND NFC) RFID

7.1. Passive HF (13.56MHz, NFC) RFID tag numbers 2024-2036, millions

7.2. Passive HF (13.56MHz, NFC) RFID tag numbers 2024-2036, millions

7.3. Average sales price of passive HF (13.56MHz) RFID by application 2024-2036, US cents

7.4. Total value of HF (13.56MHz) RFID inlays and cards by application 2024-2036, $ millions

7.5. Total value of HF (13.56MHz) RFID inlays and cards by application 2024-2036, $ millions

7.6. HF/NFC RFID Market Trends

8. MARKET DATA FOR PASSIVE LF (125KHZ, 134KHZ) RFID TAG

8.1. Passive LF (125KHz, 134KHz) RFID tag numbers 2024-2036, millions

8.2. Passive LF (125KHz, 134KHz) RFID tag numbers 2024-2036, millions

8.3. Average sales price of passive LF (13.56MHz) RFID by application 2024-2036, US cents

8.4. Total value of LF RFID inlays and cards by application 2024-2036, $ millions

8.5. Total value of LF RFID inlays and cards, by application 2024-2036, $ millions

9. MARKETS AND PROFITABILITY OF ACTIVE RFID

9.1. Active RFID Market

9.2. Change in active RFID systems due to BLE and LPWAN

9.3. How many competing LPWAN technologies?

9.4. Overview of wireless technologies

9.5. Comparison of WLAN networking protocols

9.6. Comparison of LPWAN capabilities

9.7. RFID market forecasts for battery assisted passive RFID, active RFID tag numbers 2024-2036, millions

9.8. RFID market forecasts for battery assisted passive RFID, active RFID tag numbers 2024-2036, millions

9.9. Total value of battery assisted and active RFID by application 2024-2036, $ millions

10. MARKET FOR RFID INTERROGATORS

10.1. (RFID readers)

10.2. Overview

10.3. Qualcomm Announces UHF Integration into Snapdragon Platform

10.4. RFID Interrogator (reader) numbers 2024-2036, millions

10.5. RFID Interrogator (reader) price 2024-2036, US cents

10.6. RFID Interrogator (reader) market value 2024-2036, $ millions

10.7. RFID Interrogator (reader) market value 2024-2036, $ millions

11. MARKETS BY GEOGRAPHY

11.1. Total Value of Passive LF (125KHz, 134KHz) RFID inlays by Geography, 2024-2036, $ millions

11.2. Total Value of Passive LF (125KHz, 134KHz) RFID inlays by Geography, 2024-2036, $ millions

11.3. Total Value of Passive HF (13.56MHz, NFC) RFID inlays by Geography, 2024-2036, $ millions

11.4. Total Value of Passive HF (13.56MHz, NFC) RFID inlays by Geography, 2024-2036, $ millions

11.5. Total Market Value of UHF (RAIN) RFID inlays by Geography, 2024-2036, $ millions

11.6. Total Value of UHF (RAIN) RFID inlays by Geography, 2024-2036, $ millions

11.7. Total Value of Passive RFID inlays by Geography, 2024-2036, $ millions

11.8. Total Value of Passive RFID inlays by Geography, 2024-2036, $ millions

11.9. Top Level Market Value of Passive RFID inlays and end use Geography, 2024-2036, $ millions

11.10. Top Level Market Value of Passive RFID inlays and end use Geography, 2024-2036, $ millions

11.11. Americas RFID Use: Key Conclusions

11.12. Asia-Pacific RFID Use: Key Conclusions

11.13. Europe RFID Use: Key Conclusions

11.14. Middle East & Africa RFID Use: Key Conclusions

11.15. RFID Companies Headquarter Geography

11.16. Comment on methodology

12. SUCCESSES, FAILURES, TRENDS, OPPORTUNITIES

12.1. Dynamics of the RFID value chain

12.2. Tag manufacturing value chain

12.3. Key company acquisition (1)

12.4. Key company acquisition (2)

12.5. RFID profitability (1)

12.6. RFID profitability (2)

12.7. Largest orders, best selling products, dominant suppliers in future

12.8. Largest suppliers of chips

12.9. Largest suppliers of tags, inlets, straps and detailed value chain for high volume

12.10. Examples of companies in the chip to label value chain

12.11. UHF RFID readers

12.12. Equipment supply

12.13. Outlook for RFID

13. RFID SOLUTION PROVIDERS

13.1. The RFID value chain (1)

13.2. The RFID value chain (2)

14. COMPANY PROFILES

14.1. Access to company profiles on the IDTechEx portal

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(センサ・MEMS)の最新刊レポート

IDTechEx社の センサー、触覚とディスプレイ - Sensors,Haptics & Display分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|