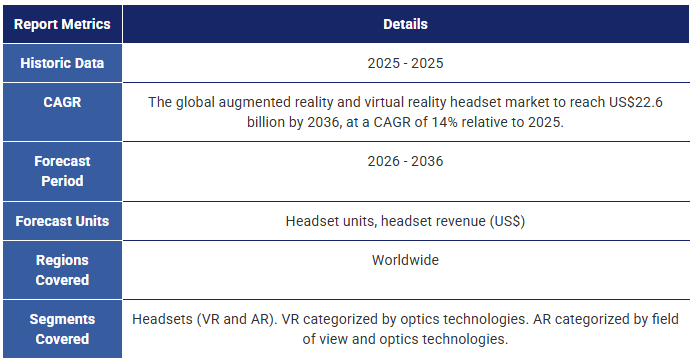

仮想現実、拡張現実、複合現実向け光学技術 2026-2036年:技術動向、予測、市場動向Optics for Virtual, Augmented and Mixed Reality 2026-2036: Technologies, Forecasts, Markets ARコンバイナー(回折型(SRGおよびホログラフィック)および反射型/幾何学的光導波路を含む)、ならびにARスマートグラスおよびAIグラス向けバードバスコンバイナー。VR用レンズ(パンケーキレンズ、フレネ... もっと見る

サマリーARコンバイナー(回折型(SRGおよびホログラフィック)および反射型/幾何学的光導波路を含む)、ならびにARスマートグラスおよびAIグラス向けバードバスコンバイナー。VR用レンズ(パンケーキレンズ、フレネルレンズ、非球面レンズを含む)。 「仮想・拡張・複合現実向け光学技術 2026-2036:技術動向・予測・市場分析」は、仮想現実(VR)、拡張現実(AR)、複合現実(MR)デバイスを実現する光学技術を評価し、2026年から2036年までの開発動向、応用分野、市場予測を分析する。 本レポートは、様々なXR製品カテゴリーで使用される光学技術を検証し、その性能、コスト、製造可能性がデバイス設計と普及に与える影響を評価します。分析対象は確立された手法と新興の代替技術の両方に及び、スマートグラスやAIグラスへの関心の高まりから得られた最新の業界データと新たな知見に基づいています。 .png)

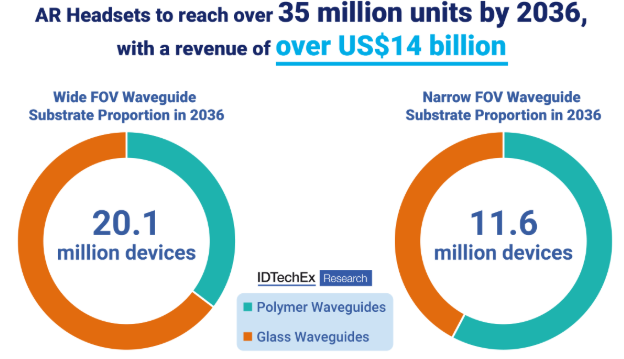

ARヘッドセット市場は2036年までに3,500万台超に達すると予測される。出典:IDTechEx

XR製品は多様な形状、没入感レベル、物理的設計制約を特徴とする。用途要件は想定使用ケースによって大きく異なる。 関連する性能指標には、効率性、消費電力、快適性、画質、視野角(FoV)、色再現性、バッテリー寿命などが含まれる。用途によっては光学効率や重量が優先される一方、広い視野角や高画質がより重要となる場合もある。この多様性がヘッドセットメーカーの光学設計選択肢を形作る。

XRデバイスに対する消費者の期待も、その目的によって異なります。日常的な着用を想定したARグラスには、軽量設計、目立たないまたはファッショナブルなスタイリング、長時間使用に耐える十分なバッテリー寿命が求められます。その結果、コンパクトな光学システムと効率的なウェーブガイド設計が特に重要となります。 対照的に、ゲームやメディア消費など没入感の高いVR用途では、重量やバッテリー寿命を犠牲にしてでも、画像の鮮明度向上、色再現性の改善、広い視野角の実現が許容される場合があります。こうしたシナリオでは、高い没入感の達成が主要な目的となることが多くなります。あらゆる消費者向けユースケースにおいて、快適性はデバイス採用率と使用時間に影響を与える重要な考慮事項であり続けます。

プロフェッショナルおよび産業用途では、異なる制約条件が許容される。多くの企業導入では、堅牢性、制御環境下での動作、アプリケーション固有の機能性が優先される。これにより、必要に応じて外部バッテリーパック、大型フォームファクター、より複雑な光学アセンブリの採用が可能となる。これらのデバイスは、単眼式ニアアイディスプレイから完全密閉型複合現実ヘッドセットまで、幅広い没入レベルをカバーする。このような多様性が、多様な光学ソリューションに対する継続的な市場需要に寄与している。

消費者向けスマートグラス分野では活発な動きが見られ、その一因はAIシステムの統合による「キラーアプリケーション」の創出にある。これらのアプリケーションには、通知・合図・状況情報を表示できる簡素で軽量な光学部品が求められる。 2025年9月に発売されたMetaのRay-Ban Displayデバイスは、このカテゴリーの最近の事例である。GoogleやSnapが2026年に投入予定の製品を含む、主要テクノロジー企業によるさらなるデバイスがこの分野に貢献する見込みだ。こうした動向により、特に薄型軽量設計を可能にする、眼鏡型フォームファクターに適した光学技術への関心が高まっている。

ARデバイスは透明性を維持しつつ映像を伝送するため、光学コンバイナーと光導波路に依存する。主な課題は、色再現性の管理、許容可能な効率の達成、適切な広視野角の確保、自然な眼球運動に対応する十分な大きさのアイボックスの提供である。処方箋の統合と封入技術も活発な開発領域だ。

VRデバイスはレンズを活用しており、メーカーは輻輳調節の矛盾に対する解決策を模索中だ。パンケーキレンズは現在、発売済みデバイスの大半で標準技術として採用されており、コンパクト性を実現するとともに、フレネルレンズの課題であったゴッドレイ現象への解決策を提供している。ただしパンケーキレンズにも、光学効率の低さ、ゴースト画像の発生、高コストといったトレードオフが存在する。

本レポートはAR・VRシステムに用いられる多様な光学技術を検証する。AR分野では、回折型・ホログラフィック型・反射型などの結合・伝搬方式を採用した導波管ベースのコンバイナー、バードバス型コンバイナー、ディスプレイ専用ヘッドセットなどが対象となる。 VR向けには、パンケーキレンズ、フレネルレンズ、非球面レンズなどの光学システムに加え、幾何位相光学などの将来技術も対象とする。各技術は、商業的・技術的要素のベンチマーク評価とSWOT分析により評価される。

本レポートでは技術クラスをこれらの基準で比較し、今後10年間で成長が見込まれる分野を分析。AR/VRデバイスの2026~2036年市場予測を、過去データと業界動向に基づき提示。光学技術の採用予測をAR/VRデバイスタイプ別に分類して掲載。 2036年までに、ARヘッドセットの出荷台数は年間約3,500万台に達し、VR出荷台数は2,700万台を超えると予測される。これらの市場は、光学部品および関連材料のサプライヤーに機会をもたらす。ARおよびVRデバイスの合計収益は、2036年までに220億米ドルを超えると予測される。この価値の部品別配分は、デバイスカテゴリーや製造コストによって異なる。

本レポートはIDTechExの広範なXR研究ポートフォリオの一部を構成する。過去の版を基盤とし、XR市場の新規分析、更新されたベンチマーク、企業環境に関するさらなる考察を加えている。インタビューと継続的な業界関与に基づき、仮想現実・拡張現実・複合現実デバイス向け光学技術の未来を形作る技術的・市場的要因について中立的な評価を提供する。

主要な側面

IDTechExによる本レポートは、以下の主要内容を網羅しています

目次

1. 要旨

1.1. 体験としてのVR、AR、MR、XR

1.2. デバイスの区分:VR対AR

1.3. AR:視野角による分類

1.4. XRは啓蒙の坂に近づいているか?

1.5. XR市場の発展

1.6. AIはスマートグラスにキラーアプリケーションをもたらすか?

1.7. 消費者市場とプロフェッショナル市場で要求が異なる

1.8. ARヘッドセットの全体予測

1.9. VRヘッドセットの全体予測

1.10. AR向け反射型ウェーブガイド:概要

1.11. AR向けSRGウェーブガイド:概要

1.12. AR向けホログラフィックウェーブガイド:概要

1.13. AR用非波導管型コンバイナー:概要

1.14. 視野角(FOV)別AR普及予測

1.15. AR向け選定光学コンバイナーの現状と市場潜在性

1.16. ARコンバイナー技術プレーヤー動向

1.17. 材料・視野角別ARコンバイナープレーヤー動向

1.18. VR用パンケーキレンズ:概要

1.19. VR用屈折レンズ:概要

1.20. VR用焦点調節レンズ:概要

1.21. VRレンズの「世代」

1.22. VR光学技術の予測:採用比率

1.23. 企業プロファイル

2. はじめに

2.1. XRと用語の入門

2.1.1. 体験としてのVR、AR、MR、XR

2.1.2. デバイスの区分:VR対AR

2.1.3. 視野角によるヘッドセットの分類

2.1.4. VRデバイスにおけるパストスルーMR

2.1.5. 用語:スタンドアロン対テザード

2.1.6. AR:視野角による分類

2.1.7. ARの概要

2.2. XR市場の概要

2.2.1. AR、MR、VR、XR:簡単な歴史

2.2.2. AR、MR、VR、XR:2010年以降

2.2.3. 2025年:スマートグラスにとってエキサイティングな時期?

2.2.4. XR市場の発展

2.2.5. VR市場の統合

2.2.6. 2025年のXRの商業的状況

2.2.7. 消費者市場とプロフェッショナル市場における要件の違い

2.2.8. XRは啓蒙の坂に近づいているのか?

2.2.9. メタバースで何が間違っていたのか?

2.2.10. VR、AR、MRの応用

2.2.11. インダストリー4.0とXR

2.2.12. 消費者向けARヘッドセットの紆余曲折の歴史

2.2.13. 消費者向けARデバイスは厳しい競争に直面

2.2.14. 他のスマートデバイスに取って代わるARヘッドセット

2.2.15. 最終目標としてのAR、スマートフォンの代替

2.2.16. AIはスマートグラスにキラーアプリケーションをもたらすか?

2.2.17. VRヘッドセット:主要プレイヤー

2.2.18. ARヘッドセット:主要プレイヤー

2.2.19. XRエコシステムプレイヤーとしてのMeta

2.2.20. Meta、メタバース予算を30%削減へ

2.2.21. XRエコシステムプレイヤーとしてのGoogleとSamsung

2.2.22. AR市場へのその他の大手テック企業の参入

2.2.23. 2024年の最大のXRニュース:Metaの長期戦略が奏功する兆し

2.2.24. スマートグラス市場は2025年に加速

2.2.25. その他の主要XR業界ニュース(I)

2.2.26. その他の主要XR業界ニュース(II)

2.2.27. 中国のXRプレイヤーを見逃すな

2.2.28. 中国のXRプレイヤー(I)

2.2.29. 中国のXRプレイヤー(II)

2.2.30. スマートコンタクトレンズ

2.2.31. XRの展望:VRとAR市場の比較

2.2.32. XR市場の概要:主なポイント

2.3. XR光学系の概要

2.3.1. XRの光学要件

2.3.2. ディスプレイとの光学系連携

2.3.3. ARとVRの光学系:開発状況と設計上の考慮点

2.3.4. 光学エンジン:XRにおけるディスプレイと光学系の統合

2.3.5. 視野角がXR体験を定義する

2.3.6. 没入型広視野角は常に必要か?

2.3.7. アイボックスとアイリリーフ:XRユーザビリティの鍵

2.3.8. 輝度と効率の測定

2.3.9. エタンデュ:光学エントロピー

2.3.10. 解像度、視野角、画素密度

2.3.11. フォービエイテッドレンダリングとディスプレイ:低解像度での高画質表示

2.3.12. 輻輳調節競合

2.3.13. コントラストとダイナミックレンジ

2.3.14. XR向けディスプレイ要件

2.3.15. 設計上の課題となる光学収差

2.3.16. VRおよびARにおける光学コーティング

2.3.17. AR用光学コンバイナー

2.3.18. AR光学系の選択肢

2.3.19. VR光学系の選択肢

2.3.20. XR市場の概要:主なポイント

3. ARおよびVR市場の予測

3.1. 予測方法論

3.1.1. ARヘッドセット予測:重要なデータソース

3.1.2. VRヘッドセット予測:重要なデータソース

3.1.3. 方法論:光学機器の数量予測

3.1.4. IDTechExのAR市場見解

3.1.5. IDTechExのVR市場見解

3.2. ヘッドセット予測

3.2.1. AR:FOV分類

3.2.2. 予測において考慮されない要素

3.2.3. ARヘッドセット:数量予測

3.2.4. ARヘッドセット:価格予測手法

3.2.5. ARヘッドセット:収益予測

3.2.6. VRハードウェア販売の周期性

3.2.7. VRヘッドセット:数量予測

3.2.8. VRヘッドセット:価格データ

3.2.9. VRヘッドセット:収益予測

3.3. AR市場予測のための光学コンバイナー

3.3.1. コンバイナー技術の将来

3.3.2. ウェーブガイドに取って代わられると予想される非ウェーブガイドコンバイナー

3.3.3. ウェーブガイドは価格面でバードバスコンバイナーとの競争を開始しつつある可能性

3.3.4. ARコンバイナ技術の採用比率予測

3.3.5. ARコンバイナ採用の過去評価:広視野角

3.3.6. 広視野角ARコンバイナ技術予測:採用比率

3.3.7. 広視野角ARコンバイナ技術予測:採用データ表

3.3.8. 広視野角ARコンバイナ技術の予測:ヘッドセット数量

3.3.9.広視野角ARコンバイナ技術の予測:数量データ表

3.3.10.SRGおよび反射型導波路:広視野角数量予測

3.3.11.ポリマーおよびガラス導波路:広視野角数量予測

3.3.12. ARコンバイナー採用の過去実績評価:狭視野角

3.3.13.狭視野角ARコンバイナー技術予測:採用比率

3.3.14.狭視野角ARコンバイナー技術予測:採用データ表

3.3.15. 狭視野ARコンバイナー技術予測:ヘッドセット数量

3.3.16. 狭視野ARコンバイナー技術予測:数量データ表

3.3.17. SRGおよび反射型導波路:狭視野数量予測

3.3.18. ポリマーおよびガラス導波路:狭視野数量予測

3.4. VR市場向けレンズ予測

3.4.1. VR光学機器採用の過去評価

3.4.2. VR光学技術予測:採用比率

3.4.3. 狭視野ARコンバイナー技術予測:採用データ表

3.4.4. VR光学技術予測:ヘッドセット数量

3.4.5. 狭視野ARコンバイナー技術予測:採用データ表

3.5. 市場予測のまとめ

3.5.1. 選定光学コンバイナーの現状と市場潜在性

3.5.2. ARコンバイナー予測:まとめ

3.5.3. VRレンズの「世代」

3.5.4. VR光学予測:まとめ

4. AR光学技術

4.1. ARにおける光学コンバイナー/導波路

4.1.1. 光学コンバイナー:定義と分類

4.1.2. AR向け光学コンバイナー

4.1.3. 導波路と他のコンバイナータイプの比較

4.1.4. 選定光学コンバイナーの現状と市場潜在性

4.1.5. ARコンバイナ技術プレーヤーの動向

4.1.6. 材料とFOV別に分類したARコンバイナプレーヤーの動向

4.2. 導波路コンバイナ

4.2.1. 一般的な導波路アーキテクチャ

4.2.2. 導波路の分類

4.2.3. 導波路へのプロジェクター入力

4.2.4. 導波路における出口瞳の拡大

4.2.5. アイグローは社会的受容性と効率性の障壁となる

4.2.6. 導波路基板材料:屈折率

4.2.7. 導波路基板用ガラスサプライヤー比較

4.2.8. 導波路基板材料:ガラス対ポリマー

4.2.9. 導波路の軽量化

4.2.10. 導波路手法の比較

4.2.11. どの導波路技術が「最良」かは依然不明

4.2.12. 導波路コンバイナ供給戦略

4.2.13. ビッグテックとAR:導波路技術

4.2.14. ビッグテックとAR:Metaの導波路技術

4.2.15. 反射型導波路

4.2.16. 導入:反射型導波路

4.2.17. 反射型導波路メーカー評価(I)

4.2.18. 反射型導波路メーカー評価(II)

4.2.19. 反射型導波路分野で依然として主導的立場にあるLumus

4.2.20. プラスチック対ガラス製反射型導波路

4.2.21. 反射型導波路:SWOT分析

4.2.22. 反射型導波路:主なポイント

4.2.23. 回折型導波路

4.2.24. 導入:回折型導波路

4.2.25. 回折型導波路:動作原理

4.2.26. 回折型導波路における色精度課題

4.2.27. 回折型導波路の色精度解決策

4.2.28. 回折型導波路の単板化開発方向性

4.2.29. 回折型導波路アーキテクチャ内の技術バリエーション

4.2.30. 回折型表面浮き彫りグレーティング(SRG)導波路

4.2.31. 導入:表面浮き彫りグレーティング導波路

4.2.32. SRG導波路メーカー評価(I)

4.2.33. SRG導波路メーカー評価(II)

4.2.34. SRG導波路メーカー評価(III)

4.2.35. SRG導波路におけるグレーティング構造

4.2.36. SRG導波路材料

4.2.37. SiC導波路:追加コストに見合うか?

4.2.38. SRG導波路:SWOT分析

4.2.39. SRG導波路:重要なポイント

4.2.40. ホログラフィック導波路

4.2.41. はじめに:ホログラフィックグレーティング導波路

4.2.42. ホログラフィック導波路プレーヤーの評価(I)

4.2.43. ホログラフィック導波路の商業的状況

4.2.44. DigiLens の SRG+ 技術

4.2.45. ホログラフィック導波路:SWOT 分析

4.2.46. ホログラフィック導波路:主なポイント

4.3. 非導波路型コンバイナ

4.3.1. 単純反射型コンバイナ

4.3.2. はじめに:単純反射型コンバイナ

4.3.3. 単純反射型コンバイナーのプレイヤー評価(I)

4.3.4. バードバス光学系:概要

4.3.5. バードバス光学系は商業的に広く採用されている

4.3.6. フリーフォームミラー:概要

4.3.7. ブギーアイコンバイナー:大規模フリーフォームミラー

4.3.8. バードバスコンバイナー:SWOT分析

4.3.9. 自由曲面ミラーコンバイナー:SWOT分析

4.3.10. ブギーアイコンバイナー:SWOT分析

4.3.11. 簡易反射型コンバイナー:主なポイント

4.3.12. 自由空間ホログラフィック光学素子(HOE)コンバイナー

4.3.13. 導入:自由空間ホログラフィック光学素子(HOE)コンバイナー

4.3.14. 自由空間ホログラフィックコンバイナ プレーヤー評価 (I)

4.3.15. HOE 自由空間コンバイナ:普及の難しさ?

4.3.16. 自由空間 HOE:SWOT 分析

4.3.17. 自由空間HOE:主なポイント

4.3.18. 非透過型ディスプレイ:光結合器不要

4.3.19. 導入:非透過型ディスプレイ

4.3.20. 非透過型ディスプレイ:SWOT分析

4.3.21. 非透過型ディスプレイ:主なポイント

4.4. AR技術のベンチマークと分析

4.4.1. AR用光結合器のベンチマーク導入

4.4.2. AR用光結合器:ベンチマークカテゴリー

4.4.3. ARにおける光結合器:技術ベンチマーク

4.4.4. ARにおける光結合器:レーダーチャート

4.4.5. SRGと反射型導波路の比較

4.4.6. ガラス基板とポリマー基板の比較:反射型導波路

4.4.7. ガラス基板とポリマー基板の比較:SRG導波路

4.4.8. 要素別性能ランキング:広視野角デバイスと狭視野角デバイス

4.4.9. 狭視野角光学技術ランキング

4.4.10. 広視野角光学技術ランキング

4.4.11. 導波路技術による高視野角での光学効率の低下

4.4.12. 技術ベンチマーク:主なポイント

4.5. ARにおける封入と処方補正

4.5.1. 現在のARデバイスにおける処方補正へのアプローチ

4.5.2. 処方補正の将来的なアプローチ:ユーザーカスタマイズ

4.5.3. なぜレンズで導波路を封入するのか?

4.5.4. 補助レンズが導波路の能力のギャップを埋める

4.5.5. 静的調節力調整

4.5.6. 処方補正:3Dプリントが提供する洗練された解決策

4.5.7. Meta、Luxexcel、AddOptics

4.5.8. AddOptics

4.5.9. 輻輳調節矛盾の補正

4.5.10. Deep Opticsと液晶レンズ

4.5.11. 将来のARアイピース開発

4.5.12. 封入技術と処方補正の主要プレイヤー

4.5.13. 封入と処方補正:重要なポイント

4.6. 光学シミュレーションソフトウェアプロバイダー

4.6.1. 光学ソフトウェアプロバイダー

4.6.2. 光学シミュレーションソフトウェア:カスタムか既製品か?

4.6.3. 光学シミュレーションソフトウェア:重要なポイント

5. VR光学技術

5.1. VR光学導入

5.1.1. VR光学技術概観

5.1.2. VRにおけるレンズ

5.1.3. パンケーキレンズが現在および近い将来のVRで主流に

5.1.4. VRレンズの「世代」

5.1.5. VRレンズ技術の現状

5.1.6. ビッグテックとVR:光学技術

5.2. パンケーキレンズ

5.2.1. パンケーキレンズ:概要

5.2.2. パンケーキレンズ:ニッチから標準へ

5.2.3. パンケーキデバイス:2025年に主流となる

5.2.4. パンケーキレンズとフレネルレンズヘッドセットの比較

5.2.5. パンケーキレンズとフレネルレンズにおけるアーティファクト

5.2.6. パンケーキレンズと新たな設計可能性

5.2.7. ホログラフィックパンケーキレンズ

5.2.8. その他のカタディオプトリックレンズ設計

5.2.9. 偏光ベースのパンケーキレンズ:SWOT分析

5.3. 屈折レンズ

5.3.1. フレネルレンズ:VRレンズにおける従来の標準

5.3.2. Metaの特許取得済みハイブリッドフレネルレンズ

5.3.3. フレネルレンズにおけるゴッドレイ軽減のその他のアプローチ

5.3.4. フレネルダブレット

5.3.5. ユーザーによるヘッドセット改造

5.3.6. VRハイエンド向け非球面レンズ

5.3.7. 非球面レンズとパンケーキレンズの比較

5.3.8. フレネルレンズ:SWOT分析

5.3.9. 非球面レンズ:SWOT分析

5.4. 焦点調整可能レンズ

5.4.1. XRにおいて動的焦点可変性が重要な理由

5.4.2. 技術成熟度別新興レンズ技術

5.4.3. XRにおける輻輳調節矛盾(VAC)の解決策

5.4.4. VAC回避策と焦点フリーシステム:SWOT分析

5.4.5. 動的光学系(焦点調整可能レンズ):SWOT分析

5.4.6. SWOT:「真の3D」ディスプレイ

5.4.7. 「真の3D」ディスプレイ

5.4.8. 「真の3D」ディスプレイ概要

5.4.9. ライトフィールドディスプレイ:複数視点からのシーン再構築

5.4.10. 解像度限界の回避:順次光場ディスプレイ

5.4.11. 事例研究:CREALの光場ニアアイディスプレイ

5.4.12. ホログラフィ:波面の再構築

5.4.13. コンピュータ生成ホログラフィ:デジタルホログラム生成

5.4.14. VividQ:AR向けホログラフィックディスプレイ

5.4.15. まとめ:焦点調節レンズの競合となる「真の3D」ディスプレイ

5.4.16. 幾何位相レンズ

5.4.17. 幾何学的位相レンズの基礎

5.4.18. 平面レンズ:回折光学素子、メタサーフェス、液晶など

5.4.19. 幾何学的位相レンズの重要性

5.4.20. 幾何学的(パンチャラトナム・ベリー)位相とは?

5.4.21. 光学異方性材料と幾何学的位相レンズ

5.4.22. 液晶と切替可能な波長板

5.4.23. GPLにおける液晶

5.4.24. メタサーフェス:幾何学的位相を適用する別の方法

5.4.25. 光学メタサーフェスの概要

5.4.26. 光学メタマテリアルの製造:ハーバード大学の研究

5.4.27. メタサーフェスの応用:ハーバード大学の研究

5.4.28. 光分配・撮像用メタサーフェス

5.4.29. 半導体製造プロセスによるメタサーフェス製造

5.4.30. ローリングマスクリソグラフィー

5.4.31. Meta社のGPLプロトタイプ

5.4.32. ヘッドセット向けGPL活用構想

5.4.33. XR向け幾何学的位相レンズ:展望

5.4.34. その他の焦点調整可能レンズ

5.4.35. 調整可能液晶レンズ

5.4.36. Meta:VAC解決に向けた様々なアプローチ

5.4.37. アルヴァレスレンズ

5.4.38. 焦点調整可能レンズ:主なポイント

5.5. VR技術ベンチマークと分析

5.5.1. VRレンズベンチマークの概要

5.5.2. ベンチマーク基準(I):商業的要因

5.5.3. ベンチマーク基準(II):技術的要因

5.5.4. ベンチマークスコア:VRレンズ

5.5.5. レンズ総合性能の比較

5.5.6. 光学レンズ性能のランキング

5.5.7. VRデバイスにおける属性重要度

5.5.8. VRレンズベンチマーク性能

5.5.9. VRレンズベンチマーク:予測立案のための結論

6. 企業プロファイル

6.1. AddOptics (2022)

6.2. AddOptics (2025)

6.3. AddOptics:2023年更新

6.4. ケンブリッジ・メカトロニクス(2022年)

6.5. ディープオプティクス(2022年)

6.6. デジレンズ(2022年)

6.7. デジレンズ(2025年)

6.8. ディスペリックス(2022年)

6.9. EverySight (2025)

6.10. HTC Vive (2022)

6.11. Inkron (2022)

6.12. Kubos Semiconductors (2025)

6.13. Kura Technologies (2022)

6.14. Lenovo: ThinkReality A3 (2022)

6.15. LetinAR (2022)

6.16. LetinAR (2024)

6.17. LetinAR: 大量生産ヘッドセットの光学技術 (2024)

6.18. LightTrans (2025)

6.19. Limbak (2022)

6.20. Limbak: Appleによる買収? (2023)

6.21. Lumus (2022)

6.22. Lumus (2023)

6.23. Lumus (2025)

6.24. Luxexcel (2022)

6.25. Luxexcel、Meta に買収される (2023)

6.26. Lynx (2022)

6.27. Lynx ? 2022 年第 2 四半期最新情報

6.28. Meta (VR 光学) (2022)

6.29. Meta:VRの業務用利用とQuest for Business (2023)

6.30. Meta:スマートグラス最新情報 (2025)

6.31. MICROOLED (2023)

6.32. Mira Reality (2022)

6.33. Mira Reality:Appleによる買収 (2023)

6.34. Mojo Vision (2022)

6.35. Morphotonics (2022)

6.36. Morphotonics (2025)

6.37. Oorym (2023)

6.38. Optiark 2025 Update

6.39. Optinvent (2022)

6.40. Optinvent (2025)

6.41. Optix (2025)

6.42. Samsung: Galaxy Event (2025)

6.43. Schott AG (2025)

6.44. Schott AG: 拡張現実/複合現実事業 (2022)

6.45. SCIL ナノインプリント (2025)

6.46. Snap: AWE 2025 (2025)

6.47. ソニー (CES 2023)

6.48. TruLife Optics (2022)

6.49. Varjo (2023)

6.50. VividQ (2022)

6.51. VividQ and Dispelix: Pairing Holographic Displays with Waveguides (2023)

6.52. VividQ: Visit and Tech Demo (2022)

SummaryAR combiners including diffractive (SRG and holographic) and reflective/geometric waveguides, and birdbath combiners for AR smart glasses and AI glasses. Lenses for VR including pancake, Fresnel and aspheric lenses. "Optics for Virtual, Augmented and Mixed Reality 2026-2036: Technologies, Forecasts, Markets" provides an assessment of the optical technologies that enable virtual, augmented, and mixed reality devices, analyzing their development, application areas, and expected market trajectory from 2026 to 2036. It examines the optical technologies used across different XR product categories and evaluates how their performance, cost, and manufacturability influence device design and adoption. The analysis covers both established approaches and emerging alternatives, supported by updated industry data and new insights from the growing interest in smart‑glasses and AI glasses.

The AR headset market is forecast to reach over 35 million units by 2036. Source: IDTechEx.

XR products span a range of form factors, levels of immersion, and physical design constraints. Application requirements vary widely depending on the intended use case. Relevant performance metrics may include efficiency, power consumption, comfort, image quality, field of view (FoV), color fidelity, and battery life. In some applications, optical efficiency and weight may be the priority, while in others, wide FoV or high image quality may be more important. This diversity shapes the optical choices available to headset manufacturers.

Consumer expectations for XR devices also depend on their intended purpose. For everyday wear, AR glasses will require a lightweight design, unobtrusive or fashionable styling, and sufficient battery life for extended use. As a result, compact optical systems and efficient waveguide designs are of particular relevance. In contrast, more immersive VR applications, such as gaming or media consumption, may allow for trade‑offs in weight or battery life in favor of enhanced image clarity, improved color fidelity, or larger field of view. In these scenarios, achieving a high level of immersion often becomes the primary objective. Across all consumer use cases, comfort remains a key consideration, influencing both device adoption and usage duration.

Professional and industrial use cases can accommodate different sets of constraints. Many enterprise deployments prioritize robustness, controlled‑environment operation, and application‑specific functionality. This can allow for acceptance of external battery packs, larger form factors, or more complex optical assemblies where necessary. These devices may cover a wide range of immersion levels, from monocular near‑eye displays to fully enclosed mixed‑reality headsets. Such variance contributes to the continued market demand for a diverse range optical solutions.

Significant activity is occurring in consumer smart glasses, driven in part by the integration of AI systems which may give smart glasses a 'killer application'. These applications require simple, lightweight optical components that can display notifications, cues, and contextual information. Meta's Ray‑Ban Display device, launched in September 2025, represents one recent example of this category. Further devices from major technology companies, including expected products from Google and Snap in 2026, are likely to contribute to this segment. These developments have increased interest in optics suitable for glasses‑like form factors, particularly those enabling thin, lightweight designs.

AR devices rely on optical combiners and waveguides to deliver imagery while maintaining transparency. Key challenges include managing color performance, achieving acceptable efficiency, ensuring a suitably wide field of view, and providing a sufficiently large eye box to accommodate natural eye movement. Prescription integration and encapsulation is another active area of development.

VR devices make use of lenses and manufacturers are exploring solutions to the vergence accommodation conflict. Pancake lenses are now the standard technology used in the vast majority of released devices, offering compactness and providing a solution to god ray issues that hampered Fresnel lenses. However, pancake lenses are not without any trade-offs, including low optical efficiency, ghost images and higher cost.

The report examines a broad range of optical technologies used in AR and VR systems. For AR, these include waveguide‑based combiners using diffractive, holographic, reflective, and other coupling and propagation methods such as birdbath combiners and display-only headsets. For VR, optical systems including pancake lenses, Fresnel lenses, and aspheric lenses, as well as potential future technologies such as geometric phase optics. Each technology is assessed via benchmarking of commercial and technological factors, alongside a SWOT analysis.

The report compares technology classes with these criteria and provides analysis on which are best positioned for growth across the coming decade. Market forecasts from 2026 to 2036 are provided for AR and VR devices, supported by historical data and industry developments. Adoption projections for optical technologies are included, with segmentation by AR and VR device type. By 2036, AR headset shipments are projected to reach around 35 million units per year, with VR shipments exceeding 27 million units. These markets create opportunities for suppliers of optical components and related materials. Combined revenues for AR and VR devices is forecast to surpass US$22 billion by 2036. The distribution of this value across components will vary depending on device category, and manufacturing costs.

This report forms part of IDTechEx's broader XR research portfolio. It builds on prior editions with new analysis of the XR market, updated benchmarking, and further discussion of the company landscape. Drawing on interviews and ongoing industry engagement, the report provides a neutral assessment of the technologies and market factors shaping the future of optics for virtual, augmented, and mixed reality devices.

Key Aspects

This report from IDTechEx covers the following key contents

Table of Contents

1. EXECUTIVE SUMMARY

1.1. VR, AR, MR and XR as experiences

1.2. Segmenting devices: VR vs AR

1.3. AR: Field of view categorization

1.4. Is XR approaching the slope of enlightenment?

1.5. XR market development

1.6. Will AI give smart glasses a killer application?

1.7. Requirements differ across consumer and professional markets

1.8. Overall AR headset forecasts

1.9. Overall VR headset forecasts

1.10. Reflective waveguides for AR: Summary

1.11. SRG waveguides for AR: Summary

1.12. Holographic waveguides for AR: Summary

1.13. Non-waveguide combiners for AR: Summary

1.14. AR adoption forecast by FOV

1.15. Status and market potential of selected optical combiners for AR

1.16. AR combiner technology player landscape

1.17. AR combiner player landscape segmented by material and FOV

1.18. Pancake lenses for VR: Summary

1.19. Dioptric lenses for VR: Summary

1.20. Focus-tunable lenses for VR: Summary

1.21. "Generations" of VR lens

1.22. VR optics technology forecast: Adoption proportions

1.23. Company profiles

2. INTRODUCTION

2.1. Introduction to XR and terminology

2.1.1. VR, AR, MR and XR as experiences

2.1.2. Segmenting devices: VR vs AR

2.1.3. Classifying headsets by field of view

2.1.4. Passthrough MR in VR devices

2.1.5. Terminology: Standalone vs tethered

2.1.6. AR: Field of view categorization

2.1.7. AR overview

2.2. Introduction to the XR market

2.2.1. AR, MR, VR and XR: A brief history

2.2.2. AR, MR, VR, and XR: 2010 onwards

2.2.3. 2025: An exciting time for smart glasses?

2.2.4. XR market development

2.2.5. The VR market is consolidating

2.2.6. The commercial status of XR in 2025

2.2.7. Requirements differ across consumer and professional markets

2.2.8. Is XR approaching the slope of enlightenment?

2.2.9. What went wrong with the metaverse?

2.2.10. Applications in VR, AR & MR

2.2.11. Industry 4.0 and XR

2.2.12. A rocky history for consumer AR headsets

2.2.13. Consumer AR devices face tough competition

2.2.14. AR headsets as a replacement for other smart devices

2.2.15. AR as the end goal, smartphone replacement

2.2.16. Will AI give smart glasses a killer application?

2.2.17. VR headsets: Selected players

2.2.18. AR headsets: Selected players

2.2.19. Meta as an XR ecosystem player

2.2.20. Meta to cut 30% of metaverse budget

2.2.21. Google and Samsung as XR ecosystem players

2.2.22. Other big tech entries to the AR market

2.2.23. The Biggest XR News in 2024: Signs of Meta's Long-Term Plays Working

2.2.24. Smart glass market shifts up a gear in 2025

2.2.25. Other key XR industry news (I)

2.2.26. Other key XR industry news (II)

2.2.27. Chinese XR players should not be overlooked

2.2.28. Chinese XR players (I)

2.2.29. Chinese XR players (II)

2.2.30. Smart contact lenses

2.2.31. The outlook for XR: Comparing the VR and AR markets

2.2.32. Introduction to the XR market: Key takeaways

2.3. Introduction to XR optics

2.3.1. Optical requirements for XR

2.3.2. Pairing optics with displays

2.3.3. AR vs VR optics: Development status and design considerations

2.3.4. Optical engines: Combining displays and optics in XR

2.3.5. Field of view defines XR experiences

2.3.6. Is an immersive wide FOV always necessary?

2.3.7. Eyebox and eye relief: Keys to XR usability

2.3.8. Measuring brightness and efficiency

2.3.9. Etendue: Optical entropy

2.3.10. Resolution, FoV, and pixel density

2.3.11. Foveated rendering and displays: Higher display quality at reduced resolution

2.3.12. The vergence-accommodation conflict

2.3.13. Contrast and dynamic range

2.3.14. Display requirements for XR

2.3.15. Optical aberrations present design challenges

2.3.16. Optic coatings in VR and AR

2.3.17. Optical combiners for AR

2.3.18. Choices of AR optic

2.3.19. Choices of VR optic

2.3.20. Introduction to the XR market: Key takeaways

3. AR AND VR MARKET FORECASTS

3.1. Forecasting methodology

3.1.1. AR headset forecasting: Important data sources

3.1.2. VR headset forecasting: Important data sources

3.1.3. Methodology: Optics volume forecasts

3.1.4. IDTechEx's view of the AR market

3.1.5. IDTechEx's view of the VR market

3.2. Headset forecasts

3.2.1. AR: FOV categorization

3.2.2. What is not considered in forecasting

3.2.3. AR headsets: Volume forecast

3.2.4. AR headsets: Pricing forecast methodology

3.2.5. AR headsets: Revenue forecast

3.2.6. Cyclic nature of VR hardware sales

3.2.7. VR headsets: Volume forecast

3.2.8. VR headsets: Pricing data

3.2.9. VR headsets: Revenue forecast

3.3. Optical combiners for AR market forecasts

3.3.1. The future of combiner technology

3.3.2. Non-waveguide combiners expected to be replaced by waveguides

3.3.3. Waveguides may be beginning to compete with birdbath combiners on price

3.3.4. Forecasting adoption proportion for AR combiner technologies

3.3.5. Historic assessment of AR combiner adoption: Wide FOV

3.3.6. Wide FOV AR combiner technology forecast: Adoption proportions

3.3.7. Wide FOV AR combiner technology forecast: Adoption data table

3.3.8. Wide FOV AR combiner technology forecast: Headset volume

3.3.9. Wide FOV AR combiner technology forecast: Volume data table

3.3.10. SRG and reflective waveguides: Wide FOV volume forecast

3.3.11. Polymer and glass waveguides: Wide FOV volume forecast

3.3.12. Historic assessment of AR combiner adoption: Narrow FOV

3.3.13. Narrow FOV AR combiner technology forecast: Adoption proportions

3.3.14. Narrow FOV AR combiner technology forecast: Adoption data table

3.3.15. Narrow FOV AR combiner technology forecast: Headset volume

3.3.16. Narrow FOV AR combiner technology forecast: Volume data table

3.3.17. SRG and reflective waveguides: Narrow FOV volume forecast

3.3.18. Polymer and glass waveguides: Narrow FOV volume forecast

3.4. Lenses for VR market forecasts

3.4.1. Historic assessment of VR optics adoption

3.4.2. VR optics technology forecast: Adoption proportions

3.4.3. Narrow FOV AR combiner technology forecast: Adoption data table

3.4.4. VR optics technology forecast: Headset volume

3.4.5. Narrow FOV AR combiner technology forecast: Adoption data table

3.5. Summary of market forecasts

3.5.1. Status and market potential of selected optical combiners

3.5.2. AR combiner forecasts: Summary

3.5.3. "Generations" of VR lens

3.5.4. VR optics forecasts: Summary

4. AR OPTICS TECHNOLOGIES

4.1. Optical combiners/waveguides in AR

4.1.1. Optical combiners: Definition and classification

4.1.2. Optical combiners for AR

4.1.3. Waveguides vs other combiner types

4.1.4. Status and market potential of selected optical combiners

4.1.5. AR combiner technology player landscape

4.1.6. AR combiner player landscape segmented by material and FOV

4.2. Waveguide combiners

4.2.1. Common waveguide architectures

4.2.2. Classes of Waveguide

4.2.3. Projector entry to waveguides

4.2.4. Exit pupil expansion in waveguides

4.2.5. Eye glow is a barrier to social acceptability and efficiency

4.2.6. Waveguide substrate materials: Refractive index

4.2.7. Comparing glass suppliers for waveguide substrates

4.2.8. Waveguide substrate materials: Glass vs polymers

4.2.9. Weight minimization in waveguides

4.2.10. Comparison between waveguide methodologies

4.2.11. It is still unclear which waveguide technology is 'best'

4.2.12. Strategies in waveguide combiner supply

4.2.13. Big Tech and AR: Waveguide technologies

4.2.14. Big Tech and AR: Meta's waveguide technologies

4.2.15. Reflective waveguides

4.2.16. Introduction: Reflective waveguides

4.2.17. Reflective waveguide players assessment (I)

4.2.18. Reflective waveguide players assessment (II)

4.2.19. Lumus still leading the way for reflective waveguides

4.2.20. Plastic vs glass reflective waveguides

4.2.21. Reflective waveguides: SWOT analysis

4.2.22. Reflective waveguides: Key takeaways

4.2.23. Diffractive waveguides

4.2.24. Introduction: Diffractive waveguides

4.2.25. Diffractive waveguides: Method of operation

4.2.26. Challenges for color accuracy in diffractive waveguides

4.2.27. Solutions to color accuracy in diffractive waveguides

4.2.28. Development direction to single plate for diffractive waveguides

4.2.29. Technology variation within diffractive waveguide architectures

4.2.30. Diffractive surface relief grating (SRG) waveguides

4.2.31. Introduction: Surface relief grating waveguides

4.2.32. SRG waveguide players assessment (I)

4.2.33. SRG waveguide players assessment (II)

4.2.34. SRG waveguide players assessment (III)

4.2.35. Grating structures in SRG waveguides

4.2.36. SRG waveguide materials

4.2.37. SiC waveguides: Worth the extra cost?

4.2.38. SRG waveguides: SWOT analysis

4.2.39. SRG waveguides: Key takeaways

4.2.40. Holographic waveguides

4.2.41. Introduction: Holographic grating waveguides

4.2.42. Holographic waveguide players assessment (I)

4.2.43. Commercial status of holographic waveguides

4.2.44. DigiLens' SRG+ technology

4.2.45. Holographic waveguides: SWOT analysis

4.2.46. Holographic waveguides: Key takeaways

4.3. Non-waveguide combiners

4.3.1. Simple reflective combiners

4.3.2. Introduction: Simple reflective combiners

4.3.3. Simple reflective combiners players assessment (I)

4.3.4. Birdbath optics: Introduction

4.3.5. Birdbath optics have significant commercial adoption

4.3.6. Freeform mirrors: Introduction

4.3.7. Bugeye combiners: Large-scale freeform mirrors

4.3.8. Birdbath combiners: SWOT analysis

4.3.9. Freeform mirror combiners: SWOT analysis

4.3.10. Bugeye combiners: SWOT analysis

4.3.11. Simple reflective combiners: Key takeaways

4.3.12. Freespace holographic optical element (HOE) combiners

4.3.13. Introduction: Free-space holographic optical element (HOE) combiners

4.3.14. Free-space holographic combiner players assessment (I)

4.3.15. HOE free-space combiners: Trouble taking off?

4.3.16. Free-space HOE: SWOT analysis

4.3.17. Free-space HOE: Key takeaways

4.3.18. Non-transparent displays: No optical combiner required

4.3.19. Introduction: Non-transparent displays

4.3.20. Non-transparent displays: SWOT analysis

4.3.21. Non-transparent displays: key takeaways

4.4. AR technology benchmarking and analysis

4.4.1. Introduction to AR optical combiner benchmarking

4.4.2. AR optical combiners: Benchmarking categories

4.4.3. Optical combiners in AR: Technology benchmarking

4.4.4. Optical combiners in AR: Radar charts

4.4.5. Comparison of SRG and reflective waveguides

4.4.6. Comparison of glass and polymer substrates: Reflective waveguides

4.4.7. Comparison of glass and polymer substrates: SRG waveguides

4.4.8. Ranking performance of factors: Wide and narrow FOV devices

4.4.9. Narrow FOV optics technology ranking

4.4.10. Wide FOV optics technology ranking

4.4.11. Reduction in optical efficiency at higher FOV by waveguide technology

4.4.12. Technology benchmarking: Key takeaways

4.5. Encapsulation and prescription correction in AR

4.5.1. Approaches to prescription correction in today's AR devices

4.5.2. Future approaches to prescription correction: User-customization

4.5.3. Why encapsulate waveguides with lenses?

4.5.4. Ancillary lenses fill gaps in waveguide capabilities

4.5.5. Static accommodation adjustment

4.5.6. Prescription correction: 3D printing offers an elegant solution

4.5.7. Meta, Luxexcel and AddOptics

4.5.8. AddOptics

4.5.9. Correcting the vergence-accommodation conflict

4.5.10. Deep Optics and liquid crystal lenses

4.5.11. Future AR eyepieces development

4.5.12. Encapsulation and prescription correction players

4.5.13. Encapsulation and prescription correction: Key takeaways

4.6. Optical simulation software providers

4.6.1. Optical software providers

4.6.2. Optical simulation software: Custom or off the shelf?

4.6.3. Optical simulation software: Key takeaways

5. VR OPTICS TECHNOLOGIES

5.1. VR optics introduction

5.1.1. The VR optics technology landscape

5.1.2. Lenses in VR

5.1.3. Pancake lenses now the dominating for current and near future VR

5.1.4. "Generations" of VR lens

5.1.5. Technological status of VR lens technologies

5.1.6. Big Tech and VR: Optics technologies

5.2. Pancake lenses

5.2.1. Pancake lenses: Introduction

5.2.2. Pancake lenses: From niche to standard

5.2.3. Pancake devices: Dominating in 2025

5.2.4. Comparing pancake and Fresnel lens headsets

5.2.5. Artefacts in pancake vs Fresnel lenses

5.2.6. Pancake lenses and new design possibilities

5.2.7. Holographic pancake lenses

5.2.8. Other catadioptric lens designs

5.2.9. Polarization-based pancake lenses: SWOT analysis

5.3. Dioptric lenses

5.3.1. Fresnel lenses: The previous standard in VR lenses

5.3.2. Meta's patented hybrid Fresnel lens

5.3.3. Other approaches to god ray mitigation in Fresnel lenses

5.3.4. Fresnel doublets

5.3.5. Users modifying headsets

5.3.6. Aspherical lenses at the high end in VR

5.3.7. Comparing aspheric and pancake lenses

5.3.8. Fresnel lenses: SWOT analysis

5.3.9. Aspherical lenses: SWOT analysis

5.4. Focus-tuneable lenses

5.4.1. Why is dynamically variable focus important for XR?

5.4.2. Emerging lens technologies by technology readiness

5.4.3. Solutions to the vergence-accommodation conflict for XR

5.4.4. VAC workarounds and focus-free systems: SWOT analysis

5.4.5. Dynamic optics (focus tunable lenses): SWOT analysis

5.4.6. SWOT: "True 3D" displays

5.4.7. "True 3D" displays

5.4.8. "True 3D" displays overview

5.4.9. Light field displays: Reconstructing scenes from multiple viewpoints

5.4.10. Avoiding the resolution limit: Sequential light field displays

5.4.11. Case study: CREAL's light field near-eye displays

5.4.12. Holography: Reconstructing wavefronts

5.4.13. Computer-generated holography: Digital hologram generation

5.4.14. VividQ: Holographic displays for AR

5.4.15. Summary: "True 3D" displays as competitors to focus-tunable lenses

5.4.16. Geometric phase lenses

5.4.17. Introduction to geometric phase lenses

5.4.18. Flat lenses: Diffractive optics, metasurfaces, liquid crystals and more

5.4.19. Why geometric phase lenses matter

5.4.20. What is geometric (Pancharatnam-Berry) phase?

5.4.21. Optically anisotropic materials and GPLs

5.4.22. Liquid crystals and switchable waveplates

5.4.23. Liquid crystals in GPLs

5.4.24. Metasurfaces: Another method to apply geometric phase

5.4.25. Introduction to optical meta-surfaces

5.4.26. Manufacturing optical metamaterials: Havard research

5.4.27. Applications for metasurfaces: Harvard research

5.4.28. Metasurfaces for distributing light and imaging

5.4.29. Manufacturing metasurfaces via semiconductor fabrication

5.4.30. Rolling mask lithography

5.4.31. Meta's GPL prototypes

5.4.32. The vision for GPL use in headsets

5.4.33. Geometric phase lenses for XR: Outlook

5.4.34. Other focus tunable lenses

5.4.35. Tunable liquid crystal lenses

5.4.36. Meta: Various approaches to solving the VAC

5.4.37. Alvarez lenses

5.4.38. Focus-tunable lenses: Key takeaways

5.5. VR technology benchmarking and analysis

5.5.1. Introduction to VR lens benchmarking

5.5.2. Benchmarking criteria (I): Commercial factors

5.5.3. Benchmarking criteria (II): Technological factors

5.5.4. Benchmark scores: VR lenses

5.5.5. Comparing overall lens performance

5.5.6. Ranking the performance of optical lenses

5.5.7. Attribute importance in VR devices

5.5.8. VR lens benchmark performance

5.5.9. VR lens benchmarking: Conclusions to inform forecasting

6. COMPANY PROFILES

6.1. AddOptics (2022)

6.2. AddOptics (2025)

6.3. AddOptics: 2023 Update

6.4. Cambridge Mechatronics (2022)

6.5. Deep Optics (2022)

6.6. DigiLens (2022)

6.7. DigiLens (2025)

6.8. Dispelix (2022)

6.9. EverySight (2025)

6.10. HTC Vive (2022)

6.11. Inkron (2022)

6.12. Kubos Semiconductors (2025)

6.13. Kura Technologies (2022)

6.14. Lenovo: The ThinkReality A3 (2022)

6.15. LetinAR (2022)

6.16. LetinAR (2024)

6.17. LetinAR: Optics in a High-Volume Headset (2024)

6.18. LightTrans (2025)

6.19. Limbak (2022)

6.20. Limbak: Acquired by Apple? (2023)

6.21. Lumus (2022)

6.22. Lumus (2023)

6.23. Lumus (2025)

6.24. Luxexcel (2022)

6.25. Luxexcel Acquired by Meta (2023)

6.26. Lynx (2022)

6.27. Lynx — Q2 2022 Update

6.28. Meta (VR Optics) (2022)

6.29. Meta: Professional Use of VR and Quest for Business (2023)

6.30. Meta: Smart Glasses Update (2025)

6.31. MICROOLED (2023)

6.32. Mira Reality (2022)

6.33. Mira Reality: Acquired by Apple (2023)

6.34. Mojo Vision (2022)

6.35. Morphotonics (2022)

6.36. Morphotonics (2025)

6.37. Oorym (2023)

6.38. Optiark 2025 Update

6.39. Optinvent (2022)

6.40. Optinvent (2025)

6.41. Optix (2025)

6.42. Samsung: Galaxy Event (2025)

6.43. Schott AG (2025)

6.44. Schott AG: Augmented/Mixed Reality Operations (2022)

6.45. SCIL Nanoimprint (2025)

6.46. Snap: AWE 2025 (2025)

6.47. Sony (CES 2023)

6.48. TruLife Optics (2022)

6.49. Varjo (2023)

6.50. VividQ (2022)

6.51. VividQ and Dispelix: Pairing Holographic Displays with Waveguides (2023)

6.52. VividQ: Visit and Tech Demo (2022)

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(光通信)の最新刊レポート

IDTechEx社の フォトニクス - Photonics分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|

.png)