レアアース マグネット 2026-2036年:技術、供給、市場、予測Rare Earth Magnets 2026-2036: Technologies, Supply, Markets, Forecasts レアアースマグネット市場、電気自動車、ロボット、エネルギー、データセンター向けのNdFeB磁石とSmCo磁石。採掘、精製、磁石生産を含むレアアースサプライチェーン。磁石の需給とリサイクル市場予測 &nbs... もっと見る

サマリー

レアアースマグネット市場、電気自動車、ロボット、エネルギー、データセンター向けのNdFeB磁石とSmCo磁石。採掘、精製、磁石生産を含むレアアースサプライチェーン。磁石の需給とリサイクル市場予測

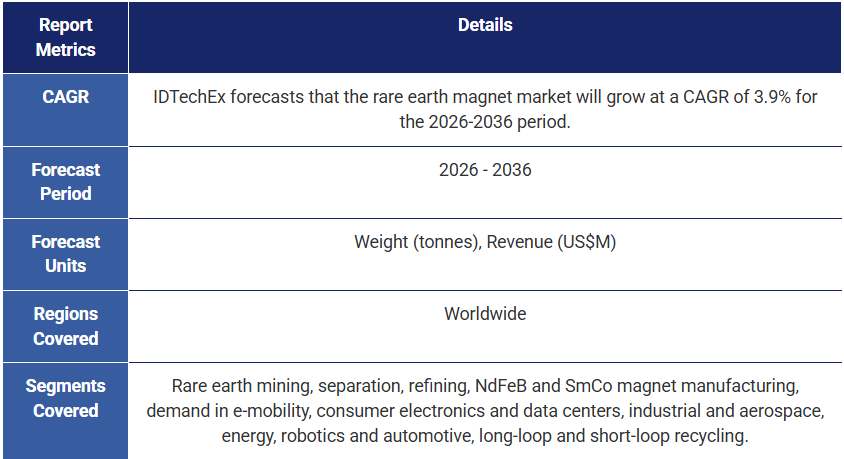

レアアースマグネット市場は需要拡大により2036年までに91億9000万米ドルを超える

IDTechExでは、世界のレアアースマグネット市場は電気自動車、ロボット、風力エネルギー、データセンター市場が高性能レアアースマグネットの需要を牽引し、2036年までに91億9000万米ドルに達すると予測している。このIDTechExレポートは、ネオジムマグネットとサマリウムコバルトマグネットを含むレアアースマグネット技術の包括的分析とベンチマークを提供しています。電気モーター、エネルギー発生装置、アクチュエーターアプリケーションへのレアアースマグネットの設計と統合における製造技術革新とトレンドについて論じています。IDTechExのレポートでは、世界のレアアースマグネットサプライチェーンの能力、拡張計画、新興のマグネットリサイクル市場を調査しています。NdFeBマグネットとSmCoマグネットについて、重量(トン)ごとのマグネット供給、需要、リサイクルを含む10年間のレアアースマグネット市場予測と年間収益予測(百万米ドル)を示しています。

.png) 高性能レアアースマグネットはますます重要な材料となる

NdFeB や SmCo などのレアアースマグネットは、2025 年に市販される高性能マグネットの中で最も強度が高い。NdFeB磁石は最高のマグネット(残留磁束)と最大エネルギー積(磁石に蓄えられる最大磁気エネルギー)を示し、ほとんどの用途に適している。一方、SmCoマグネットはNdFeBマグネットよりも減磁に対する耐性(保磁力)が高く、動作温度も高い(最高350℃)。レアアースマグネットの高性能と重量あたりの優れた特性は、モーター、アクチュエーション、音響、およびセンシングの用途において重要な材料となっています。

しかし、マグネットに使用されるレアアース元素は重要な材料であり、中国からの供給が高度に集約され、脱炭素エネルギーおよび輸送用途における経済的重要性が高まっています。過去10年間で、世界各国はマグネットに使用されるレアアース(ネオジム、サマリウム、ジスプロシウム、テルビウムなど)を重要材料として認識するようになっています。IDTechExのレポートは、マグネット用途におけるレアアース元素の重要性の高まりを評価しています。

サプライチェーンのボトルネックがレアアースマグネット生産の革新を促進

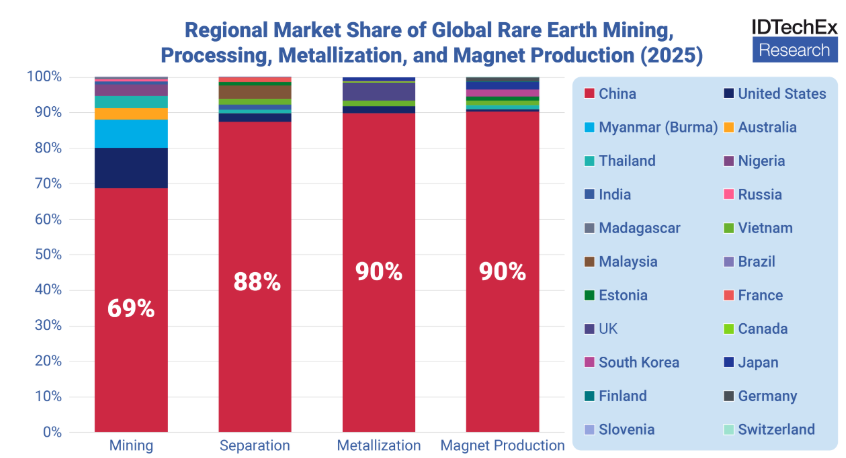

2025年の世界のレアアース採掘量の69%を中国が占め、このシェアはレアアース分離、金属化、マグネット生産段階を経て下流に向かうにつれて90%へと増加する。国内の大規模なレアアース採掘事業と高度に統合されたサプライチェーンにより、中国は世界のレアアースマグネット生産をリードすることができ、世界の重要なレアアースのほとんどがこの地域内でいずれかの段階で処理されています。

高度に統合された重要なレアアースマグネットの生産は、米国、欧州、アジアの各地域でレアアースサプライチェーンの成長を牽引しており、この地域は供給リスクの軽減に取り組んでいます。2025年4月にジスプロシウム、テルビウム、NdFeB材料に課された最近の輸出規制は、供給リスクをさらに露呈させ、代替マグネットソースの推進力となっている。IDTechExのレポートは、レアアースマグネットのサプライチェーン分析、年間生産量、今後のプロジェクト、タイムライン、採掘・分離から精製・マグネット生産までのサプライチェーン全体にわたる生産能力予測を提供しています。

新しいレアアースサプライチェーンの開発は、レアアース分離、精製、マグネット生産における技術革新の機会を生み出しています。新たな中流企業が市場に参入し、生産能力を拡大しつつあり、一次(採掘)および二次(リサイクル)原料の両方を受け入れることができる溶媒抽出および液体クロマトグラフィー技術に重点を置いています。川下では、重希土類が高コストで入手しにくいため、重希土類含有量を減らしながら希土類磁石の特性を改善できる倹約技術の革新が進んでいます。IDTechExのレポートでは、SWOT分析、性能ベンチマーク、主要サプライヤー情報など、レアアース精製、磁石技術革新を評価しています。

レアアースマグネットは、エネルギー、輸送、およびロボット工学における重要な材料技術です

レアアースマグネットの量産市場アプリケーションには、電気自動車モーター、家電製品、産業用モーター、風力タービンエネルギー発電機が含まれます。ほとんどの市場分野では、電気モーターが数量と重量で支配的なレアアースマグネットアプリケーションを占めており、レアアースマグネットは高い磁気強度と電力密度の特性を提供します。

NdFeBマグネットは、2025年の世界需要の96%を占める主要なレアアースマグネット技術です。最高使用温度は他の材料よりも低いものの、ほとんどのマグネットアプリケーションは-40℃~150℃で動作するため、NdFeBマグネットが最適なソリューションとなっている。IDTechExのレポートでは、e-モビリティ、ロボット、家電・データセンター、産業・航空宇宙、エネルギー、自動車、その他の主要なレアアースマグネット市場におけるマグネット統合、部品組立、競合マグネット技術の動向を評価している。

脱炭素エネルギーと輸送、自動化、AIのメガトレンドは、今後10年間のレアアースマグネット需要に影響を与えるでしょう。この調査レポートは、e-モビリティ、ヒューマノイドロボット、風力エネルギーなどの主要なレアアース磁石成長市場について解説しています。

レアアースマグネットリサイクルは2036年までに6.5倍に成長

レアアースの供給リスクと製品需要の増加が、レアアースマグネットリサイクル技術の成長機会を促進しています。重要なレアアースがマグネット用途にますます統合されるにつれて、マグネットリサイクルは、世界のレアアース供給全体に貢献する重要な供給源として浮上しています。

IDTechExは、レアアースマグネットリサイクルは今後10年間で6.5倍に増加し、2036年までに世界供給の最大10%を占めるようになると予測しています。ロングループ、マグネットから酸化物へのレアアース リサイクラーは、使用済みマグネット廃棄物の量と回収効率が改善されるまで、一次および二次原料の両方を処理する立場にあります。同時に、価値のあるマグネット合金を回収するショートループのマグネット間リサイクル業者は、リサイクルレアアースマグネットの生産と販売の促進に重点を置いています。

レアアースマグネットリサイクルの成長機会は、循環型レアアースサプライチェーンの確立を目指すe-モビリティ(Ford、BMW、JLR、Polestarなど)、エネルギー、コンシューマーエレクトロニクスの川下顧客からの関与の増加によって促進されます。IDTechExのレポートでは、湿式冶金溶媒抽出、液体クロマトグラフィー、粉末冶金、水素減容法などの新たなレアアースマグネットリサイクル技術を包括的に評価しています。

レアアースマグネット市場は供給懸念にもかかわらず成長へ

IDTechExは、レアアースマグネット市場はe-モビリティ、風力エネルギー、ロボット用途での需要拡大に牽引され、2036年には年間収益が91億9000万米ドルを超えるまでに成長すると予測しています。この調査レポートは、10年間の粒状レアアース磁石の供給、需要、リサイクル予測を、地域、用途、材料別に重量(トン)と収益(米ドル)で区分して掲載しています。

この調査レポートは世界のレアアースマグネットの供給、需要、リサイクルに関する重要な市場情報を提供し、マグネット材料、新興技術、主要企業、サプライチェーン、市場予測などを網羅しています。

内容は以下の通りです:

目次1.要旨

1.1.レアアースマグネットとは

1.2.レアアースマグネットは、ほとんどの指標で競合技術を凌駕している

1.3.レアアースマグネットは、電動モビリティ、家電製品、データセンター、産業、航空宇宙、およびエネルギー市場で応用されている

1.4.レアアースは重要な材料である

1.5.レアアースの採掘、加工、金属化、マグネット生産の地域別市場シェア

1.6.歴史的な価格変動と最近の技術および材料の輸出規制が、レアアース供給の不確実性を煽っている

1.7.2036年までに出現するレアアースサプライチェーンのクラスター

1.8.レアアースマグネットサプライチェーンの概要:主要プレーヤー

1.9.新興レアアースサプライチェーンが直面する課題

1.10.世界のレアアース採掘の要点と展望

1.11.レアアース分離技術は依然として既存プレーヤーに好まれるが、新興プレーヤーの戦略は異なる

1.12.レアアースの金属化およびマグネット生産の動向と要点

1.13.中国以外の新興レアアースマグネット生産の見通し(2025~2036年)

1.14.2025年の世界のレアアースマグネット需要の概要

1.15.NdFeBとSmCoの需要と一般的用途別市場シェア

1.16.主要市場におけるレアアース永久マグネット製品の動向

1.17.e-モビリティにおけるNdFeBマグネットの電動機タイプ市場シェア予測と展望

1.18.風力タービンの容量拡大とマグネット使用量の増加がネオジムマグネットの成長を牽引

1.19.人型ロボットがロボット工学におけるレアアースマグネットの需要を牽引する

1.20.レアアースマグネットアプリケーションの垂直技術動向と市場動向

1.21.廃棄物からレアアースマグネットをリサイクルする主要技術の概要

1.22.ロングループおよびショートループのレアアースマグネットリサイクル技術評価と主要プレーヤー

1.23.ロングループおよびショートループレアアースマグネットリサイクル技術の機会と動向の概要

1.24.統合製品の寿命とリサイクル効率に影響されるリサイクル用マグネットの入手可能性

1.25.地域別レアアースマグネット生産量の10年世界予測(トン)、2026~2036年

1.26.10年間のレアアースマグネットの世界用途別売上高予測(百万米ドル)、2026~2036年

1.27.10年間のレアアースマグネットリサイクル・生産能力の世界予測(原料供給源別)(トン)、2026~2036年

1.28.回収材料別レアアースマグネットリサイクル価値の世界10年予測(US$M)、2026-2036年

1.29.IDTechEx サブスクリプションでさらにアクセス

2.はじめに

2.1.レアアースマグネットとは

2.はじめに

2.2.レアアースマグネットはほとんどの指標で競合技術を上回る

2.3.レアアースは重要な材料である

2.4.レアアース元素の需要はマグネット用途に集中している

2.5.NdFeB マグネットは高い磁気強度を提供し、SmCo マグネットは高温動作に適している

2.6.レアアースマグネットは電動モビリティ、家電、データセンター、産業、航空宇宙、エネルギー市場に応用されている

2.7.レアアースマグネットサプライチェーンの概要

2.8.レアアース供給とマグネット生産は中国に集約されている

2.9.歴史的な価格変動と最近の技術および材料の輸出規制が、レアアース供給の不確実性を煽っている

2.10.新興レアアースサプライチェーンの推進要因

2.11.レアアース供給に関する新たな政策と規制

3.レアアースの採掘、加工、マグネット生産

3.1.レアアースマグネットサプライチェーンの概要

3.2.1.レアアースマグネットサプライチェーンの概要

3.2.2.レアアース採掘、加工、金属化、マグネット生産の地域市場シェア

3.2.3.2036年までに出現するレアアースサプライチェーンのクラスター

3.2.4.レアアースマグネットサプライチェーンの概要:主要プレーヤー

3.2.5.新興レアアース・サプライチェーンが直面する課題

3.2.レアアース鉱業

3.2.1.世界のレアアース鉱業の概要

3.2.2.世界のレアアース採掘の要点と展望

3.2.3.レアアース採鉱プロジェクトは、ほんの一握りの鉱物に焦点を当てている

3.2.4.バストネサイト、モナザイト、ゼノタイム鉱物中のレアアース含有量

3.2.5.硬岩とイオン性粘土のレアアース鉱床の比較

3.2.6.世界中で産出するレアアースと鉱床

3.2.7.世界のレアアース生産は中国が主導し、米国、ミャンマー、オーストラリアが主要生産国

3.2.8.世界の主要レアアース採鉱プロジェクトの概要

3.2.9.レアアース採掘の地域別内訳

3.2.10.世界のレアアース鉱山の生産能力は増加しているが、2036年までに中国がレアアース鉱山の世界的リーダーであり続ける

3.2.11.世界のレアアース鉱山拡張の概要、2025~2036年

3.2.12.中国はレアアース生産を増やし続け、世界の主要生産国であり続ける

3.2.13.中国における注目すべき採鉱プロジェクトと開発

3.2.14.アジアのレアアース鉱山生産は、中国の加工・分離インフラに近いという利点がある

3.2.15.ミャンマーでのレアアース生産は着実に増加しており、中国への輸出の恩恵を受けている

3.2.16.イオン吸着粘土からのレアアースの原位置浸出

3.2.17.北米のレアアース鉱山生産の概要

3.2.18.北米:マウンテンパス

3.2.19.北米ネカラチョ鉱山とターディフ・プロジェクト

3.2.20.カナダにおける今後のレアアース鉱山プロジェクト

3.2.21.オーストラリアのレアアース鉱山生産の概要と新興プロジェクト

3.2.22.オーストラリアマウント・ウェルド

3.2.23.オーストラリアヤンギバナ・プロジェクト

3.2.24.オーストラリアノーランズ・プロジェクト

3.2.25.オーストラリアゴッシェン・プロジェクトとキャニー・プロジェクト

3.2.26.アフリカにおけるレアアース採掘の高い可能性を秘めた数多くのプロジェクト

3.2.27.アフリカにおける今後のレアアース採鉱プロジェクトの概要

3.2.28.南米におけるレアアース採掘と機会

3.2.29.欧州の新興レアアース採鉱プロジェクトの概要

3.2.30.欧州の先進的プロジェクトの鉱物学

3.2.31.軽レアアースが欧州の埋蔵量の大半を占めるが、レアアース酸化物の総含有量は世界の高品位鉱床に比べて低い

3.2.32.欧州:フェン・プロジェクト

3.2.33.欧州:Olserum レアアース・プロジェクト

3.2.34.レアアース鉱山の開発と経済

3.2.35.レアアース鉱物発見のライフサイクル:活動とリスク

3.2.36.レアアース鉱物発見の寿命と価値機会

3.2.37.生産に向けた新規レアアース鉱山開発が直面する課題

3.2.38.レアアース酸化物価格の変動は、新規鉱山の資金調達に課題をもたらし、既存鉱山の収益性に影響を与える

3.2.39.保証会社は、新規鉱山に対するレアアース価格変動の影響を軽減できる可能性があるが、まだ検証されていない

3.3.レアアースの加工と分離

3.3.1.レアアースの加工、分離、および原料供給源の概要

3.3.2.世界のレアアース処理および分離の主要要点と展望

3.3.3.レアアースの加工および分離技術

3.3.4.レアアース処理および分離の概要:鉱石から酸化物まで

3.3.5.レアアース精鉱の分解と浸出

3.3.6.バストネサイト、モナザイト、混合レアアース精鉱の湿式冶金処理

3.3.7.バイオリーチングは新たなレアアース抽出技術であるが、従来の分解・浸出アプローチに取って代わる可能性は低い

3.3.8.レアアース抽出のためのバイオリーチングのSWOT分析

3.3.9.レアアース分離のための溶媒抽出とクロマトグラフィー技術

3.3.10.溶媒抽出は、液液抽出を使用してレアアースの逐次分離を実現する

3.3.11.軽レアアースと重レアアースを完全に分離するには、複数の溶媒抽出ラインが必要である

3.3.12.レアアース分離に使用される一般的な化学物質と配位子

3.3.13.溶媒抽出レアアース分離技術のSWOT分析

3.3.14.液体クロマトグラフィーによるレアアース分離技術は供給原料の柔軟性を提供する

3.3.15.レアアース分離のためのクロマトグラフィー技術と材料要件の概要

3.3.16.液体クロマトグラフィーによるレアアース分離技術のSWOT分析

3.3.17.液体クロマトグラフィー技術の採用は増加しているが、溶媒抽出は依然として標準的なレアアース分離技術

3.3.18.世界のレアアース処理・分離能力と拡張計画

3.3.19.2024年の世界のレアアース分離・加工の概要

3.3.20.世界のレアアース分離能力と主要プレーヤー

3.3.21.中国はレアアース処理と分離の世界的リーダーであり続け、2024年に25万

4,000トン以上の分離レアアース酸化物を生産する

3.3.22.中国は引き続きレアアース処理と分離を強化する

3.3.23.中国における軽質および重質レアアースの分離・精製能力

3.3.24.中国以外のレアアース処理能力は2036年までに5倍に増加する見込み

3.3.25.中国におけるレアアース処理と分離の増加の見通し

3.3.26.アジア、北米、欧州の生産能力増加にもかかわらず、中国は2036年までに世界のレアアース分離の大半のシェアを維持する

3.3.27.アジアは中国以外の主要なレアアース加工・分離ハブである

3.3.28.リナス・マレーシアはレアアース加工の東部ハブであり、マウント・ウェルド鉱山の重要な下流加工業者である

3.3.29.アジアは、中国以外の重要な世界的レアアース加工ハブであり続ける

3.3.30.欧州でのレアアース処理が拡大し、溶媒抽出と液体クロマトグラフィーの両技術にチャンスがもたらされる

3.3.31.欧州の主なレアアース分離プロジェクト

3.3.32.欧州における新たなレアアース分離:プロジェクト、能力、スケジュール

3.3.33.北米のレアアース処理能力は、2035年までに7倍に増加する可能性がある

3.3.34.北米のレアアース分離プロジェクト

3.3.35.北米の新興レアアース分離プロジェクト

3.3.36.オーストラリアのレアアース炭酸塩生産は増加するが、分離能力は依然限定的

3.3.37.レアアース処理・分離市場の展望と課題

3.3.38.新興プレーヤーでは戦略が異なるが、既存プレーヤーでは依然として溶媒抽出が好ましいレアアース分離技術

3.3.39.中流のレアアース加工・分離業者が直面する課題

3.3.40.レアアース分離は鉱山業者のOpExコストの大半を占める

3.3.41.レアアース価格の低迷は、中流の加工業者の経済的実行可能性に引き続き課題をもたらしている

3.3.42.マグネットに使用されるレアアース酸化物が、原料価値の大部分を占めている

3.4.レアアースの金属化とマグネット生産

3.4.1.レアアースの金属化、合金、マグネット生産の概要

3.4.2.レアアースの金属化およびマグネット生産:要約と要点

3.4.3.レアアースの金属化および合金生産

3.4.4.金属化:一般的なレアアースマグネット金属および合金製品

3.4.5.レアアース金属は製錬と還元によって生産される

3.4.6.溶融塩電解と金属熱処理によるレアアースの金属化

3.4.7.レアアースの金属化には溶融塩電解精製が好ましい

3.4.8.重レアアースの精製には減圧蒸留が用いられる

3.4.9.NdFeBとSmCo合金の保磁力と残留磁化を調整するためのストリップ鋳造

3.4.10.中国は世界のレアアースの90%をマグネット用途に精製している

3.4.11.2025年の世界のレアアース精製能力

3.4.12.中国以外のレアアース精錬企業と開発計画(1/2)

3.4.13.中国以外のレアアース精錬企業と開発計画(2/2)

3.4.14.レアアース精錬の機会と課題

3.4.15.2025年のジスプロシウム、テルビウム、NdFeB合金の輸出規制は、レアアース金属化の代替品不足を浮き彫りにする

3.4.16.レアアース金属化の展望

3.4.17.レアアースマグネット技術と生産

3.4.18.レアアースマグネット技術

3.4.19.確立されたマグネット技術とレアアースマグネットの概要

3.4.20.レアアースマグネットはほとんどの指標で競合技術を上回る

3.4.21.NdFeBマグネットは2025年に市販されるマグネットの中で最も強度が高い

3.4.22.プラセオジムと重レアアースがネオジムマグネットの性能を向上させる

3.4.23.NdFeB マグネットのグレードと性能特性

3.4.24.NdFeBマグネットの特性に対するジスプロシウム合金の影響と、異なるマグネットグレードの一般的な用途

3.4.25.レアアース金属の高コストが、NdFeB マグネット全体の価格に最も大きな影響を与える

3.4.26.SmCo マグネットは、高い磁気強度と高い熱安定性のバランスがとれている

3.4.27.NdFeB マグネットは高い磁力を持ち、SmCo マグネットは高温動作に適している

3.4.28.焼結レアアースマグネットの製造方法

3.4.29.ボンドレアアースマグネットは、焼結材に比べて機械的強度とコストを改善する

3.4.30.焼結レアアースマグネット用コーティングのベンチマーク

3.4.31.射出成形と圧縮成形を使用したボンドレアアースマグネットの製造

3.4.32.レアアースマグネット製造の革新分野は、性能の向上、レアアース含有量の削減、および工程効率の改善に重点を置いている

3.4.33.粒界拡散は、ジスプロシウムとテルビウム合金を粒表面に局在化させることで重レアアース含有量を削減する

3.4.34.焼結 NdFeB マグネットおよび粒界拡散 NdFeB マグネットにおける重レアアースドーピングの評価

3.4.35.粒界拡散による重レアアース含有量低減の戦略

3.4.36.NdFeB マグネットのレアアース含有量を低減するために粒界拡散を利用するメーカーと製品 OEM

3.4.37.重レアアースを使用せずにネオジムマグネットの保磁力を向上させる高度なジェットミリング技術

3.4.38.レアアースマグネット製造におけるその他のイノベーション

3.4.39.レアアースマグネット市場と世界生産

3.4.40.2025年のレアアースマグネットの世界生産と生産能力の概要

3.4.41.レアアースマグネットの世界生産と地域別主要メーカー

3.4.42.NdFeB材料が世界のマグネット生産を支配し、SmCo材料は市場のニッチにサービスを提供する

3.4.43.中国が世界のレアアースマグネット生産をリード、追加生産能力もあり

3.4.44.マグニフィセント・シックス」:中国のレアアースマグネット生産は複数のプレーヤーが独占

3.4.45.中国のレアアースマグネット生産能力は今後10年間でほぼ倍増

3.4.46.世界のマグネットメーカー、中国での生産能力と操業の確立が進む

3.4.47.中国、2025年4月にNdFeBとSmCoマグネットの輸出規制を実施

3.4.48.アジアは中国以外の主要なレアアースマグネット生産地域だが、生産能力の拡大は限定的

3.4.49.日本、ベトナム、韓国、タイはアジアにおけるレアアースマグネット製造の主要拠点

3.4.50.アジアの地域別市場概要と動向

3.4.51.欧州のレアアースマグネット製造能力は、台頭する国内中流に合わせて成長する

3.4.52.エストニアとドイツは欧州におけるレアアースマグネット製造の主要拠点

3.4.53.ネオ・パフォーマンス・マテリアルズ、2025年にエストニアで生産開始

3.4.54.レアアースマグネットの生産では米国が後れを取るが、国内では大規模な採掘事業が行われている

3.4.55.米国で計画されているレアアースマグネット製造の拡張

3.4.56.世界のレアアースマグネット生産予測、2025~2036年

3.4.57.中国以外の新興レアアースマグネット生産の見通し(2025~2036年)

3.4.58.レアアースマグネットメーカーはエネルギー、電動モビリティ、家電、産業用途の顧客にとって戦略的パートナー

3.4.59.マグネット製造における新規参入者の機会と課題

4.レアアースマグネットの用途

4.1.レアアースマグネット需要の概要

4.1.1.レアアースマグネットの用途と需要:概要と要点

4.1.2.レアアースマグネット用途の垂直技術動向と市場動向

4.1.3.レアアース永久マグネット用途市場の概要

4.1.4.2025 年の世界のレアアースマグネット需要の概要

4.1.5.NdFeB と SmCo の需要と一般的用途別市場シェア

4.1.6.主要用途におけるレアアース永久マグネットの重量需要

4.1.7.主要市場におけるレアアース永久マグネット製品の動向

4.2.電気自動車とe-モビリティ

4.2.1.レアアースマグネットのe-モビリティ市場の概要

4.2.2.新規販売台数の電動化シェア

4.2.3.トラクションモーターのタイプ別概要

4.2.4.車両別電動モータータイプ市場シェア

4.2.5.2023年の車両カテゴリー別平均モーター出力(kW)

4.2.6.電気自動車 - モータサイジング

4.2.7.モータータイプの出力密度ベンチマーク

4.2.8.e-モビリティにおけるNdFeBマグネットの電動モータータイプ市場シェア予測と展望

4.2.9.主要自動車メーカーによるPMモーターへの収束

4.2.10.電気バス用トラクションモーター

4.2.11.ローターの磁性材料分布

4.2.12.ID4対リーフ対モデル3のローター

4.2.13.EVモーター材料のボラティリティ

4.2.14.レアアースを排除する市場の動き

4.2.15.テスラの次世代モーター

4.2.16.テスラによるレアアース廃止の可能性(1)

4.2.17.テスラがレアアースを排除する方法 (2)

4.2.18.テスラによるレアアース削減の可能性 (3)

4.2.19.日本におけるレアアース削減の進展

4.2.20.トヨタのネオジム還元マグネット

4.2.21.モーターにおけるフェライトの性能とネオジムの比較

4.2.22.フェライトの性能とネオジムの比較

4.2.23.レアアースを排除するOEM & Tier 1のアプローチ

4.2.24.マグネット輸出規制の自動車産業への影響

4.2.25.Eモビリティ技術と市場に関するIDTechExの関連調査

4.3.エネルギー(風力タービン)

4.3.1.風力エネルギー分野の紹介とレアアースマグネットの役割

4.3.2.従来の風力タービンの構造と材料

4.3.3.風力タービン用レアアース永久マグネット同期発電機(PMSG)

4.3.4.風力タービンの軽量化と高効率化を可能にするレアアースマグネット

4.3.5.ダイレクトドライブおよびギヤードドライブ風力タービンにおけるレアアースマグネット

4.3.6.風力タービンにおけるレアアースマグネットの使用はブレードの回転速度に依存する

4.3.7.風力タービンのブレードのサイズと容量は成長を続けている

4.3.8.世界の企業別風力タービン製造能力

4.3.9.風力タービンの容量拡大とマグネット使用量の増加がネオジムマグネットの成長を牽引

4.4.家電とデータセンター

4.4.1.レアアースマグネットの家電・データセンター用途の概要

4.4.2.家電におけるマグネット需要

4.4.3.HDDとは?どのように機能するのか?

4.4.4.HDD市場の歴史的変遷

4.4.5.ソリッド・ステート・メモリがトップ・クラスとして台頭する中、エッジ・アプリケーションでのHDD需要が減少

4.4.6.ハードディスク・ドライブの需要はクラウドとデータセンター・アプリケーションに集約

4.4.7.ハードディスク・ドライブ用途における永久マグネット需要の見通し

4.5.ロボット

4.5.1.ロボット分野におけるレアアースマグネットの概要

4.5.2.ロボットにおけるレアアースマグネットの機能例

4.5.3.人型ロボットがロボット用レアアースマグネットの需要を牽引する

4.5.4.ヒューマノイドロボット

4.5.5.ヒューマノイドロボットの概要

4.5.6.ヒューマノイドロボットの採用を加速させているものは?

4.5.7.アクチュエーター - 技術比較と課題

4.5.8.普及が進む電動モーター

4.5.9.ヒューマノイドロボット各社のモーターまとめ

4.5.10.NdFeB - レアアース永久マグネット

4.5.11.レアアースは電気自動車によく使われており、人型ロボット産業へのサプライチェーンシナジーにつながる

4.5.12.ダイレクトドライブモーター - フレームレスモーター

4.5.13.フレームレスモーター - ダイレクトドライブアクチュエーターまたはギアードアクチュエーターに使用できる

4.5.14.ブラシ付き/ブラシレスモーター

4.5.15.コアレスモーター - ブラシ付きモーターの一種

4.5.16.モーターの概要

4.5.17.使用例:テスラ・オプティマスのモーター

4.5.18.コンポーネント別コスト分析

4.5.19.用途別ヒューマノイドロボット商品化の成熟度

4.5.20.国別・主要用途別のヒューマノイド市場

4.5.21.物流業界におけるヒューマノイドロボットが扱う作業の推定スケジュール

4.5.22.協働ロボット

4.5.23.協働ロボット(コボット)

4.5.24.従来の産業用ロボットと協働ロボットの比較

4.5.25.産業別コボットのロードマップと成熟度分析

4.5.26.商業化されたコボットの概要

4.5.27.モバイルロボット

4.5.28.イントラロジスティックにおけるモバイルロボット

4.5.29.移動ロボットのサプライチェーン分析

4.5.30.自動搬送台車(AGV/Cs)

4.5.31.エクソテック・システムズ

4.6.その他のマグネット成熟市場

4.6.1.自動車技術におけるレアアースマグネット

4.6.2.産業用レアアースマグネット

4.6.3.医療用画像処理におけるネオジムマグネット

4.6.4.レアアースマグネットの航空宇宙および海洋用途

5.レアアースマグネットのリサイクル

5.1.レアアースマグネットリサイクルの概要

5.1.1.レアアースマグネットリサイクル - 章の概要

5.1.2.レアアースマグネットリサイクルの動向

5.1.3.重要なレアアース元素:製品市場と用途

5.1.4.重要なレアアース元素:一次材料サプライチェーンの地理的集中

5.1.5.マグネット用途に集中するレアアース元素の需要

5.1.6.レアアース元素回収のための一次および二次材料の流れ

5.1.7.二次材料源のレアアース含有量

5.2.レアアースのリサイクル技術

5.2.1.廃棄物からレアアースマグネットをリサイクルするための主要技術の概要

5.2.2.ロングループおよびショートループのレアアースリサイクル方法

5.2.3.水素減容によるショートループレアアースマグネットリサイクル

5.2.4.粉末冶金によるショートループレアアースマグネットリサイクル

5.2.5.ショートループ再生マグネットはバージンマグネットに比べて磁気特性が弱い

5.2.6.ショートループレアアースマグネットリサイクルの SWOT 分析

5.2.7.ロングループマグネットリサイクル

5.2.8.ロングループレアアースマグネットリサイクル:回収技術

5.2.9.溶媒抽出によるロングループマグネット回収

5.2.10.溶媒抽出を使用したロングループリサイクルの営業費用(OpEx)の内訳

5.2.11.液体クロマトグラフィーによるレアアース分離技術は、原料の柔軟性を提供する

5.2.12.液体クロマトグラフィーではイオン交換樹脂を使用してマグネットをリサイクルする

5.2.13.イオン交換/液体クロマトグラフィーを利用したレアアース回収の新たなビジネスモデル

5.2.14.ロングループレアアースマグネットリサイクル回収のSWOT分析

5.2.15.ショートループおよびロングループレアアースマグネットリサイクル:概要と主要プレーヤー

5.2.16.マグネットリサイクルにおける廃棄物の前処理と自動化の役割

5.3.レアアースリサイクル市場

5.3.2.2025年のレアアースマグネットリサイクルはロングループ技術が主流

5.3.2.主要レアアースリサイクラー概要

5.3.3.新興のレアアースマグネットリサイクルバリューチェーン

5.3.4.世界のレアアースマグネットリサイクル業者

5.3.5.重要なレアアースの循環型サプライチェーンが必要性から出現している

5.3.6.2030年までのレアアースマグネットリサイクル能力の増加により、利用率を最大化するための原料調達拡大の必要性が浮き彫りに

5.3.7.電気モーター、エネルギー発電機、ハードディスクドライブがレアアースの重要な二次供給源として浮上

5.3.8.電気ローターからのレアアースマグネットリサイクルの前処理の課題

5.3.9.リサイクル用マグネットの入手可能性は、統合製品の寿命とリサイクル効率に影響される

5.3.10.使用済み廃棄物の利用可能性が高まるまで、マグネット製造廃棄物はリサイクル業者にとって重要な原料になる

5.3.11.多くのロングループ・リサイクラーは、二次的供給源がオンラインになるまで、一次鉱物原料の確保に重点を置く

5.3.12.レアアースマグネット回収の成長を実現するための成長の障壁と開発が必要な分野

5.4.まとめと展望

5.4.1.レアアースマグネット回収技術の概要と展望

5.4.2.レアアースマグネット市場の概要と展望

5.4.3.ロングループおよびショートループのレアアースマグネットリサイクル技術の機会と傾向の概要

5.4.4.レアアースマグネットリサイクルの革新分野

5.4.5.レアアースマグネットリサイクルのバリューチェーン

6.レアアースマグネットの市場予測

6.1.予測方法

6.1.1.予測方法

6.1.2.予測の前提

6.1.3.予測価格の前提

6.1.4.再生可能エネルギー用途からのリサイクル用原料入手の不連続性

6.2.レアアースマグネット供給予測

6.2.1.地域別レアアースマグネット生産量10年予測(トン)、2026~2036年

6.2.2.中国を除く地域別の10年間のレアアースマグネット世界生産量予測(トン)、2026~2036年

6.3.レアアースマグネットの需要予測

6.3.1.用途別レアアースマグネットの世界10年需要予測(トン)、2026~2036年

6.3.2.用途別レアアースマグネット世界需要シェア(重量、トン)、2026~2036年

6.3.3.成熟市場におけるレアアースマグネットの世界10年需要予測(トン)、2026~2036年

6.3.4.e-モビリティおよび電気自動車におけるレアアースマグネットの10年世界需要予測(トン)、2026~2036年

6.3.5.風力タービンの10年世界レアアースマグネット需要予測(トン)、2026~2036年

6.3.6.ロボット用レアアースマグネットの10年世界需要予測(トン)、2026~2036年

6.3.7.材料別レアアースマグネットの10年世界需要予測(トン)、2026~2036年

6.3.8.10年間のレアアースマグネットの世界需要予測(鉄を除く)(トン)、2026~2036年

6.3.9.レアアースマグネットの10年世界需要予測(素材別)(トン)、2026~2036年

6.3.10.10年間のレアアースマグネットの世界需要予測(マグネット材料別)(トン)、2026~2036年

6.3.11.10年間のレアアースマグネットの世界用途別売上高予測(百万米ドル), 2026-2036

6.3.12.10年間の世界のレアアースマグネット需給予測(トン), 2026-2036

6.4.マグネットのリサイクル予測

6.4.1.原料供給源別レアアースマグネットリサイクル・容量の10年世界予測(トン)、2026~2036年

6.4.2.レアアースマグネットリサイクルの世界10年予測、原料供給源別(トン)、2026~2036年

6.4.3.レアアースマグネットリサイクル原料組成の10年予測、2026年~2036年

6.4.4. レアアースマグネットリサイクルの技術別世界10年予測(トン)、2026年~2036年

6.4.5.レアアースマグネット生産の10年世界予測(一次および二次供給源別)、2026~2036年

6.4.6.10年間のレアアースマグネットリサイクル世界予測、回収材料別(トン)、2026~2036年

6.4.7.回収材料別レアアースマグネットリサイクル価値の世界10年予測(百万米ドル)、2026年~2036年

7.企業プロファイル

7.1.1X Technologies

7.2.アドバンスト・エレクトリック・マシーンズレアアースフリーモーター

7.3.アプトロニック社

7.4.オーストラリアン・ストラテジック・マテリアルズ社(ASM)

7.5.ケアスター(ケアマグ)

7.6.ケアスター(ケアマグ)

7.7.サイクリックマテリアル

7.8.サイクリックマテリアル

7.9.EVRモーターズ

7.10.ガーナー・プロダクツ

7.11.GeMMe(ジオリソース、ミネラルエンジニアリング、抽出冶金)

7.12.ハイプロマグ

7.13.ハイプロマグ社

7.14.イオン性レアアース

7.15.イオンテクノロジー

7.16.JLマグ

7.17.メタライシス

7.18.モーダルモーターズ

7.19.Monumo:AIモーター設計

7.20.ニーロン・マグネティクスレアアースフリー永久マグネット

7.21.ノベオン・マグネティクス

7.22.QuantumScape

7.23.レアアース・テクノロジーズ・インク(RETi)

7.24.リエレメント・テクノロジーズ

7.25.リーテック

7.26.セロキシウム

7.27.テスラオプティマス・リヴェール

7.28.ユニツリー・ロボティクスヒューマノイド・ロボティクス

7.29.ビクトレックス

7.30.ZF: SELECTドライブユニット

Summary

Rare earth magnet market, NdFeB magnets and SmCo magnets for electric vehicles, robotics, energy and data centers. Rare earth supply chains, including mining, refining, magnet production. Magnet supply, demand and recycling market forecasts

Rare earth magnet market to exceed US$9.19B by 2036 as demand grows

IDTechEx forecasts that the global rare earth magnet market will reach US$9.19B by 2036, with electric vehicle, robotics, wind energy, and data center markets driving demand for high-performance rare earth magnets. This IDTechEx report provides comprehensive analysis and benchmarking of rare earth magnet technologies, including neodymium magnets and samarium-cobalt magnets. Manufacturing innovations and trends in design and integration of rare earth magnets into electric motor, energy generator, and actuator applications are discussed. IDTechEx's report surveys global rare earth magnet supply chain capacity, expansion plans and the emerging magnet recycling market. Granular 10-year rare earth magnet market forecasts, including magnet supply, demand and recycling by weight (tonnes) and annual revenue forecasts (US$M) are presented for NdFeB and SmCo magnets.

High-performance rare earth magnets are increasingly critical materials

Rare earth magnets, such as NdFeB and SmCo, are the strongest commercially available high-performance magnets in 2025. NdFeB magnets demonstrate the highest magnetic strength (remanence) and maximum energy product (maximum magnetic energy stored in the magnet) and are suitable for most applications. SmCo magnets on the other hand offer greater resistance to demagnetization (coercivity) and higher operating temperatures (up to 350°C) than NdFeB. The high-performance and superior performance-per-weight attributes of rare earth magnets make them critical materials in motor, actuation, acoustic, and sensing applications.

However, rare earth elements used in magnets are critical materials, with highly consolidated supply from China and increasing economic importance in decarbonized energy and transport applications. Over the last decade, countries across the world have increasingly identified rare earths used in magnets (such as neodymium, samarium, dysprosium, terbium) as critical materials. IDTechEx's report evaluates the increasing criticality of rare earth elements in magnet applications.

Supply chain bottlenecks drive innovation in rare earth magnet production

China represents 69% of global rare earth element mining in 2025, with this share increasing towards 90% moving downstream through rare earth separation, metallization, and magnet production stages. Large domestic rare earth mining operations and highly integrated supply chains have enabled China to lead global rare earth magnet production and ensures that most of the world's critical rare earths are processed at one stage or another within the region.

Highly consolidated critical rare earth magnet production is driving rare earth supply chain growth across the USA, Europe, and Asia, as regions move to derisk supply. Recent export restrictions placed on dysprosium, terbium, and NdFeB materials in April 2025 further exposed supply risks and represents a driver for alternative magnet sources. IDTechEx's report provides rare earth magnet supply chain analysis, annual production, upcoming projects, timelines, and capacity forecasts across the entire supply chain, from mining and separation to refining and magnet production.

The development of new rare earth supply chains is creating opportunities for technological innovation in rare earth separation, refining, and magnet production. New midstream players are entering the market and scaling capacity, focused on solvent extraction and liquid chromatography technologies capable of accepting both primary (mining) and secondary (recycling) feedstocks. Downstream, the high cost and low availability of heavy rare earths is driving innovation in thrifting technologies that can improve rare earth magnet properties while reducing heavy rare earth content. IDTechEx's report evaluates rare earth refining, magnet technology innovations, including SWOT analysis, performance benchmarking, and key supplier information.

Rare earth magnets are key material technologies in energy, transport, and robotics

High-volume rare earth magnet market applications include electric vehicle motors, consumer electronics, industrial motors and wind turbine energy generators. Across most market verticals, electric motors represent the dominant rare earth magnet application by volume and weight, where rare earth magnets offer high magnetic strength and power density properties.

NdFeB magnets are the dominant rare earth magnet technology, representing 96% of global demand in 2025. Despite having a lower maximum operating temperature than other materials, most magnet applications operate between -40°C and 150°C, making NdFeB magnets the best solution. IDTechEx's report evaluates trends in magnet integration, component assembly, and competing magnet technologies in e-mobility, robotics consumer electronics and data centers, industrial and aerospace, energy, automotive and other key rare earth magnet markets.

Mega trends in decarbonized energy and transport, automation and AI will influence rare earth magnet demand over the next decade. This research report discusses key rare earth magnet growth markets, including e-mobility, humanoid robotics, and wind energy.

Rare earth magnet recycling set to grow 6.5x by 2036

Rare earth supply risks and increasing product demand are driving growth opportunities for rare earth magnet recycling technology. As critical rare earths increasingly consolidate in magnet applications, magnet recycling is emerging as an important source contributing towards overall global rare earth supply.

IDTechEx predicts that rare earth magnet recycling will increase 6.5x over the next decade and will represent up to 10% of global supply by 2036. Long-loop, magnet-to-oxide rare earth recyclers are positioned to process both primary and secondary feedstocks until end-of-life magnet waste volume and collection efficiencies improve. At the same time, short-loop magnet-to-magnet recyclers recovering valorized magnet alloys focus on advancing production and sale of recycled rare earth magnets.

Growth opportunities for rare earth magnet recycling are fueled by increasing engagement from downstream customers in e-mobility (e.g., Ford, BMW, JLR, Polestar), energy, and consumer electronics moving to establish circular rare earth supply chains. IDTechEx's report comprehensively evaluates emerging rare earth magnet recycling technologies, including hydrometallurgical solvent extraction, liquid chromatography, powder metallurgy and hydrogen decrepitation.

Rare earth magnet market to grow despite supply concerns

IDTechEx forecasts that the rare earth magnet market will grow to exceed US$9.19B in annual revenue in 2036, driven by growing demand in e-mobility, wind energy and robotics applications. This research report provides 10-year granular rare earth magnet supply, demand, and recycling forecasts, by weight (tonnes) and revenue (US$) segmented by region, application and materials.

Key aspects of this report

This report provides critical market intelligence on global rare earth magnet supply, demand, and recycling, covering magnet materials, emerging technology, key players, supply chains, and market forecasts. This includes:

This report provides critical market intelligence on global rare earth magnet supply, demand, and recycling, covering magnet materials, emerging technology, key players, supply chains, and market forecasts. This includes:

Table of Contents1. EXECUTIVE SUMMARY

1.1. What are rare earth magnets

1.2. Rare earth magnets outperform competing technologies on most metrics

1.3. Rare earth magnets are applied in electric mobility, consumer electronics, data center, industrial, aerospace and energy markets

1.4. Rare earths are critical materials

1.5. Regional market share of rare earth mining, processing, metallization, and magnet production

1.6. Historical price volatility and recent technology and material export restrictions fuel rare earth supply uncertainty

1.7. Clusters of rare earth supply chains set to emerge by 2036

1.8. Rare earth magnet supply chain overview: Key players

1.9. Challenges facing emerging rare earth supply chains

1.10. Key takeaways and outlook for global rare earth mining

1.11. Solvent extraction remains the preferred rare earth separation technology amongst incumbent players as strategies diverge for emerging players

1.12. Rare earth metallization and magnet production trends and key takeaways

1.13. Emerging rare earth magnet production outlook outside of China, 2025-2036

1.14. Overview of global rare earth magnet demand in 2025

1.15. NdFeB and SmCo market share by demand and common applications

1.16. Rare earth permanent magnet product trends in key markets

1.17. Electric motor type market share forecast and outlook for NdFeB magnets in e-mobility

1.18. Wind turbine capacity expansion and increasing magnet usage will drive growth for NdFeB magnets

1.19. Humanoid robots are set to drive demand for rare earth magnets in robotics

1.20. Technology and market trends in rare earth magnet application verticals

1.21. Overview of key technologies for recycling rare earth magnets from waste

1.22. Long-loop and short-loop rare earth magnet recycling technology assessment and key players

1.23. Overview of opportunities and trends for long-loop and short-loop rare earth magnet recycling technologies

1.24. Availability of magnets for recycling influenced by lifetimes of integrated products and recycling efficiency

1.25. 10-year global rare earth magnet production forecast by region (tonnes), 2026-2036

1.26. 10-year global rare earth magnet revenue forecast by application (US$M), 2026-2036

1.27. 10-year global rare earth magnet recycling and capacity forecast by feedstock source (tonnes), 2026-2036

1.28. 10-year global rare earth magnet recycling value forecast by material recovered (US$M), 2026-2036

1.29. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. What are rare earth magnets

2.2. Rare earth magnets outperform competing technologies on most metrics

2.3. Rare earths are critical materials

2.4. Rare earth element demand is concentrating in magnet applications

2.5. NdFeB magnets offer high magnetic strength while SmCo magnets are suited for high temperature operation

2.6. Rare earth magnets are applied in electric mobility, consumer electronics, data center, industrial, aerospace and energy markets

2.7. Overview of rare earth magnet supply chain

2.8. Rare earth supply and magnet production is consolidated in China

2.9. Historical price volatility and recent technology and material export restrictions fuel rare earth supply uncertainty

2.10. Drivers for emerging rare earth supply chains

2.11. Emerging policy and regulations on rare earth supply

3. RARE EARTH MINING, PROCESSING, AND MAGNET PRODUCTION

3.1. Overview of rare earth magnet supply chains

3.1.1. Overview of rare earth magnet supply chain

3.1.2. Regional market share of rare earth mining, processing, metallization, and magnet production

3.1.3. Clusters of rare earth supply chains set to emerge by 2036

3.1.4. Rare earth magnet supply chain overview: Key players

3.1.5. Challenges facing emerging rare earth supply chains

3.2. Rare earth mining

3.2.1. Overview of global rare earth mining

3.2.2. Key takeaways and outlook for global rare earth mining

3.2.3. Rare earth mining projects focus on just a handful of minerals

3.2.4. Rare earth content in bastnäsite, monazite, and xenotime minerals

3.2.5. Comparing hard rock and ionic clay rare earth deposits

3.2.6. Rare earth occurrences and deposits available across the world

3.2.7. Global rare earth production led by China, with USA, Myanmar and Australia key producers

3.2.8. Overview of major global rare earth mining projects

3.2.9. Regional breakdown of rare earth mining

3.2.10. China set to remain global leader in rare earth mine production by 2036, despite increasing capacity worldwide

3.2.11. Global rare earth mining expansion overview, 2025-2036

3.2.12. China continues to increase rare earth production, remaining major global producer

3.2.13. Notable mining projects and developments in China

3.2.14. Rare earth mine production in Asia benefits from proximity to processing and separation infrastructure in China

3.2.15. Rare earth production in Myanmar has steadily increased, benefiting from exports to China

3.2.16. In-situ leaching of rare earths from ion-adsorption clays

3.2.17. Overview of rare earth mine production in North America

3.2.18. North America: Mountain Pass

3.2.19. North America: Nechalacho Mine and Tardiff Project

3.2.20. Future rare earth mining projects in Canada

3.2.21. Overview of rare earth mine production in Australia and emerging projects

3.2.22. Australia: Mount Weld

3.2.23. Australia: Yangibana Project

3.2.24. Australia: Nolans Project

3.2.25. Australia: Goschen and Cannie Projects

3.2.26. Numerous projects hold high potential for rare earth mining in Africa

3.2.27. Overview of upcoming rare earth mining projects in Africa

3.2.28. Rare earth mining and opportunities in South America

3.2.29. Overview of emerging rare earth mining projects in Europe

3.2.30. Mineralogy of advanced projects in Europe

3.2.31. Light rare earths dominate European reserves, but total rare earth oxide content low compared to high grade deposits globally

3.2.32. Europe: Fen Project

3.2.33. Europe: Olserum Rare Earth Project

3.2.34. Rare earth mine development and economics

3.2.35. The lifecycle of rare earth mineral discovery: Activity and risks

3.2.36. Rare earth mineral discovery lifetime and value opportunities

3.2.37. Challenges facing new rare earth mine development towards production

3.2.38. Rare earth oxide price volatility presents challenges for financing new mines and impacts profitability of existing mines

3.2.39. Guarantors could derisk rare earth price volatility impact on new mines, but have yet to be validated

3.3. Rare earth processing and separation

3.3.1. Overview of rare earth processing, separation, and feedstock sources

3.3.2. Key takeaways and outlook for global rare earth processing and separation

3.3.3. Rare earth processing and separation technologies

3.3.4. Overview of rare earth processing and separation: From ore to oxide

3.3.5. Cracking and leaching rare earth concentrates

3.3.6. Hydrometallurgical processing of bastnaesite, monazite, and mixed rare earth concentrates

3.3.7. Bioleaching is an emerging rare earth extraction technology, but is unlikely to displace conventional cracking and leaching approaches

3.3.8. SWOT analysis of bioleaching for rare earth extraction

3.3.9. Solvent extraction and chromatography technologies for rare earth separation

3.3.10. Solvent extraction achieves sequential separation of rare earths using liquid-liquid extraction

3.3.11. Multiple solvent extraction lines are required to fully separate light and heavy rare earths from one another

3.3.12. Common chemicals and ligands used for rare earth separation

3.3.13. SWOT analysis of solvent extraction rare earth separation technology

3.3.14. Liquid chromatography rare earth separation technology offers feedstock flexibility

3.3.15. Overview of chromatography technologies and material requirements for rare earth separation

3.3.16. SWOT analysis of liquid chromatography rare earth separation technology

3.3.17. Solvent extraction remains standard rare earth separation technology, despite increasing liquid chromatography technology adoption

3.3.18. Global rare earth processing and separation capacity and expansion plans

3.3.19. Overview of global rare earth separation and processing in 2024

3.3.20. Global rare earth separation capacity and key players

3.3.21. China remains world leader in rare earth processing and separation, producing over 254,000 tonnes of separated rare earth oxides in 2024

3.3.22. China continues to ramp up rare earth processing and separation

3.3.23. Light and heavy rare earth separation and refining capacity in China

3.3.24. Rare earth processing capacity outside of China expected to increase five-fold by 2036

3.3.25. Outlook for increased rare earth processing and separation in China

3.3.26. China set to retain majority share of global rare earth separation by 2036, despite increasing capacity in Asia, North America, and Europe

3.3.27. Asia is a major rare earth processing and separation hub outside of China

3.3.28. Lynas Malaysia is an eastern hub for rare earth processing and crucial downstream processor for the Mount Weld mine

3.3.29. Asia set to remain important global rare earth processing hub outside of China

3.3.30. Rare-earth processing in Europe to expand, presenting opportunities for both solvent extraction and liquid chromatography technologies

3.3.31. Major rare earth separation projects in Europe

3.3.32. Emerging rare earth separation in Europe: Projects, capacities, timelines

3.3.33. Rare earth processing in North America could achieve 7-fold increase in capacity by 2035

3.3.34. Rare earth separation projects in North America

3.3.35. Emerging rare earth separation projects in North America

3.3.36. Australia rare earth carbonate production to ramp up, but separation capacity remains limited

3.3.37. Rare earth processing and separation market outlook and challenges

3.3.38. Solvent extraction remains the preferred rare earth separation technology amongst incumbent players as strategies diverge for emerging players

3.3.39. Challenges facing rare earth processors and separators in the midstream

3.3.40. Rare earth separation contributes the majority of OpEx costs for miners

3.3.41. Depressed rare earth prices continue to pose a challenge to the economic viability of midstream processors

3.3.42. Rare earth oxides used in magnets disproportionally dominate feedstock value

3.4. Rare earth metallization and magnet production

3.4.1. Overview of rare earth metallization, alloy and magnet production

3.4.2. Rare earth metallization and magnet production: Summary and key takeaways

3.4.3. Rare earth metallization and alloy production

3.4.4. Metallization: Common rare earth magnet metals and alloy products

3.4.5. Rare earth metals are produced by smelting and reduction

3.4.6. Rare earth metallization by molten salt electrolysis and metallothermic processing

3.4.7. Molten salt electrolysis refining is preferred for rare earth metallization

3.4.8. Vacuum distillation is used to purify heavy rare earths

3.4.9. Strip casting used to tune coercivity and remanence of NdFeB and SmCo alloys

3.4.10. China refines 90% of global rare earth metals for magnet applications

3.4.11. Global rare earth refining capacity in 2025

3.4.12. Rare earth metal refiners outside of China and development plans (1/2)

3.4.13. Rare earth metal refiners outside of China and development plans (2/2)

3.4.14. Opportunities and challenges for rare earth refining

3.4.15. 2025 export restrictions on dysprosium, terbium, and NdFeB alloys underscore lack of alternatives for rare earth metallization

3.4.16. Outlook for rare earth metallization

3.4.17. Rare earth magnet technologies and production

3.4.18. Rare earth magnet technologies

3.4.19. Overview of established magnet technologies and rare earth magnets

3.4.20. Rare earth magnets outperform competing technologies on most metrics

3.4.21. NdFeB magnets are the strongest commercially available magnets in 2025

3.4.22. Praseodymium and heavy rare earths improve performance of NdFeB magnets

3.4.23. NdFeB magnet grades and performance characteristics

3.4.24. Influence of dysprosium alloying on NdFeB magnet properties and common applications of different magnet grades

3.4.25. High rare earth metal costs have the biggest influence on overall NdFeB magnet price

3.4.26. SmCo magnets balance high magnetic strength with high thermal stability

3.4.27. NdFeB magnets offer high magnetic strength while SmCo magnets are suited for high temperature operation

3.4.28. Manufacturing methods for sintered rare earth magnets

3.4.29. Bonded rare earth magnets improve mechanical strength and cost compared to sintered materials

3.4.30. Benchmarking of coatings for sintered rare earth magnets

3.4.31. Manufacturing bonded rare earth magnets using injection molding and compression molding

3.4.32. Rare earth magnet manufacturing innovation areas focus on improving performance, reducing rare earth content, and improving process efficiency

3.4.33. Grain boundary diffusion reduces heavy rare earth content by localizing dysprosium and terbium alloys on grain surfaces

3.4.34. Evaluation of heavy rare earth doping in sintered and grain boundary engineered NdFeB magnets

3.4.35. Strategies for reducing heavy rare earth content by grain boundary diffusion

3.4.36. Manufacturers and product OEMs take advantage of grain boundary diffusion to lower rare earth content of NdFeB magnets

3.4.37. Advanced jet milling technologies to improve coercivity of NdFeB magnets without heavy rare earths

3.4.38. Other innovations in rare earth magnet manufacturing

3.4.39. Rare earth magnet market and global production

3.4.40. Overview of global rare earth magnet production and capacity in 2025

3.4.41. Global rare earth magnet production and key manufacturers by region

3.4.42. NdFeB materials dominate global magnet production, as SmCo materials service market niches

3.4.43. China leads global rare earth magnet production, with additional capacity available

3.4.44. The 'MAGnificent Six': Rare earth magnet production in China dominated by several players

3.4.45. Rare earth magnet production capacity in China to almost double over the next decade

3.4.46. Global magnet manufacturers increasingly establishing production capacity and operations in China

3.4.47. China imposes export restrictions on NdFeB and SmCo magnets in April 2025

3.4.48. Asia represents key rare earth magnet production region outside of China, but production capacity expansion limited

3.4.49. Japan, Vietnam, South Korea and Thailand represent key rare earth magnet manufacturing hubs in Asia

3.4.50. Regional market overview and trends in Asia

3.4.51. Rare earth magnet manufacturing capacity in Europe set to grow in line with an emerging domestic midstream

3.4.52. Estonia and Germany are key rare earth magnet manufacturing hubs in Europe

3.4.53. Neo Performance Materials begins production at site in Estonia in 2025

3.4.54. USA trails in rare earth magnet production, despite significant domestic mining operations

3.4.55. Planned rare earth magnet manufacturing expansion in USA

3.4.56. Global rare earth magnet production forecast, 2025-2036

3.4.57. Emerging rare earth magnet production outlook outside of China, 2025-2036

3.4.58. Rare earth magnet manufacturers are strategic partners for customers in energy, electric mobility, consumer electronics, and industrial applications

3.4.59. Opportunities and challenges for new entrants in magnet manufacturing

4. RARE EARTH MAGNET APPLICATIONS

4.1. Overview of rare earth magnet demand

4.1.1. Rare earth magnet applications and demand: Overview and key takeaways

4.1.2. Technology and market trends in rare earth magnet application verticals

4.1.3. Overview of rare earth permanent magnet application markets

4.1.4. Overview of global rare earth magnet demand in 2025

4.1.5. NdFeB and SmCo market share by demand and common applications

4.1.6. Rare earth permanent magnet weight demand in key applications

4.1.7. Rare earth permanent magnet product trends in key markets

4.2. Electric vehicles and e-mobility

4.2.1. Overview of e-mobility markets for rare earth magnets

4.2.2. Electrified Share of New Sales

4.2.3. Summary of Traction Motor Types

4.2.4. Electric Motor Type Market Share by Vehicle

4.2.5. Average Motor Power 2023 by Vehicle Category (kW)

4.2.6. Electric Vehicles - Motor Sizing

4.2.7. Motor Type Power Density Benchmark

4.2.8. Electric motor type market share forecast and outlook for NdFeB magnets in e-mobility

4.2.9. Convergence on PM Motors by Major Automakers

4.2.10. Traction Motors of Choice for Electric Buses

4.2.11. Magnetic Material Distribution in Rotors

4.2.12. ID4 vs Leaf vs Model 3 Rotors

4.2.13. Volatility of EV Motor Materials

4.2.14. The Market Drive to Eliminate Rare Earths

4.2.15. Tesla's Next Generation Motor

4.2.16. How Tesla Could Eliminate Rare-earths (1)

4.2.17. How Tesla Could Eliminate Rare-earths (2)

4.2.18. How Tesla Could Eliminate Rare-earths (3)

4.2.19. Rare Earth Reduction Progress in Japan

4.2.20. Toyota's Neodymium Reduced Magnet

4.2.21. Ferrite Performance vs Neodymium in Motors

4.2.22. Ferrite Performance vs Neodymium

4.2.23. OEM & Tier 1 Approaches to Eliminate Rare Earths

4.2.24. Impact of magnet export restrictions on automotive industry

4.2.25. Related IDTechEx Research on E-Mobility Technologies and Markets

4.3. Energy (Wind Turbines)

4.3.1. Introduction to the wind energy sector and the role of rare earth magnets

4.3.2. Traditional wind turbine structure and materials

4.3.3. Rare earth permanent magnet synchronous generators (PMSG) for wind turbines

4.3.4. Rare earth magnets enable weight reduction and greater efficiency in wind turbines

4.3.5. Rare earth magnets in direct drive and geared drive wind turbines

4.3.6. Rare earth magnet usage in wind turbines depends on blade rotational speed

4.3.7. Wind turbine blades size and capacity continues to grow

4.3.8. Global wind turbine manufacturing capacity by company

4.3.9. Wind turbine capacity expansion and increasing magnet usage will drive growth for NdFeB magnets

4.4. Consumer electronics and data centers

4.4.1. Overview of consumer electronics and data center applications of rare earth magnets

4.4.2. Magnet demand in consumer electronics

4.4.3. What are HDDs? How Do They Work?

4.4.4. HDDs Market Historically

4.4.5. HDD demand drops in edge applications as solid-state memory emerging as top of class

4.4.6. Hard disk drive demand consolidates in cloud and data center applications

4.4.7. Outlook for permanent magnet demand in hard disk drive applications

4.5. Robotics

4.5.1. Overview of rare earth magnets in robotics

4.5.2. Example functions of rare earth magnets in robotics

4.5.3. Humanoid robots are set to drive demand for rare earth magnets in robotics

4.5.4. Humanoid robots

4.5.5. Humanoid Robotics Overview

4.5.6. What is accelerating the adoption of humanoid robots?

4.5.7. Actuator - technical comparison and challenges

4.5.8. Electric motors are getting increasingly popular

4.5.9. A summary of motors for different humanoid robotics companies

4.5.10. NdFeB - rare earth permanent magnets

4.5.11. Rare earth metals are commonly used in electric vehicles, leading to supply chain synergies to humanoid robotics industry

4.5.12. Direct drive motors - frameless motors

4.5.13. Frameless motors - can be used for direct drive actuator or geared actuation

4.5.14. Brushed/Brushless motors

4.5.15. Coreless motors - type of brushed motors

4.5.16. Summary of motors

4.5.17. Use case: Tesla Optimus motors

4.5.18. Cost analysis by component

4.5.19. Maturity of commercialization of humanoid robots by application

4.5.20. Humanoids market by country and primary use-case

4.5.21. Estimated timeline of tasks handled by humanoid robots in the logistics industry

4.5.22. Collaborative robots

4.5.23. Collaborative robots (Cobots)

4.5.24. Traditional industrial robots vs. collaborative robots

4.5.25. Roadmap and Maturity Analysis of Cobots by Industry

4.5.26. Overview of commercialized cobots

4.5.27. Mobile robots

4.5.28. Mobile Robotics in Intralogistic

4.5.29. Supply Chain Analysis of Mobile Robots

4.5.30. Automated Guide Vehicles & Carts (AGV/Cs)

4.5.31. Exotec Systems

4.6. Other magnet mature markets

4.6.1. Rare earth magnets in automotive technologies

4.6.2. Rare earth magnets in industrial applications

4.6.3. NdFeB magnets in medical imaging

4.6.4. Aerospace and marine applications of rare earth magnets

5. RARE EARTH MAGNET RECYCLING

5.1. Overview of rare earth magnet recycling

5.1.1. Rare earth magnet recycling - Chapter overview

5.1.2. Trends in rare earth magnet recycling

5.1.3. Critical rare earth elements: Product markets and applications

5.1.4. Critical rare earth elements: Geographic concentration of primary material supply chain

5.1.5. Rare earth element demand concentrating in magnet applications

5.1.6. Primary and secondary material streams for rare-earth element recovery

5.1.7. Rare earth element content in secondary material sources

5.2. Rare earth recycling technologies

5.2.1. Overview of key technologies for recycling rare earth magnets from waste

5.2.2. Long-loop and short-loop rare earth recycling methods

5.2.3. Short-loop rare-earth magnet recycling by hydrogen decrepitation

5.2.4. Short-loop rare-earth magnet recycling by powder metallurgy

5.2.5. Short-loop recycled magnets show weaker magnetic properties compared to virgin magnets

5.2.6. SWOT analysis of short-loop rare-earth magnet recycling

5.2.7. Long-loop magnet recycling

5.2.8. Long-loop rare-earth magnet recycling: Recovery technologies

5.2.9. Long-loop magnet recovery using solvent extraction

5.2.10. Breakdown of operating expenditure (OpEx) of long-loop recycling using solvent extraction

5.2.11. Liquid chromatography rare earth separation technology offers feedstock flexibility

5.2.12. Liquid chromatography uses ion exchange resins to recycle magnets

5.2.13. Emerging business model for rare earth recovery using ion exchange / liquid chromatography

5.2.14. SWOT analysis of long-loop rare earth magnet recycling recovery

5.2.15. Short-loop and long-loop rare earth magnet recycling: Summary and key players

5.2.16. The role of waste pre-processing and automation in magnet recycling

5.3. Rare earth recycling markets

5.3.1. Rare earth magnet recycling in 2025 dominated by long-loop technology

5.3.2. Overview of key rare earth recyclers

5.3.3. Emerging rare-earth magnet recycling value chain

5.3.4. Global rare earth magnet recyclers

5.3.5. Circular supply chains for critical rare earths are emerging out of necessity

5.3.6. Increasing rare earth magnet recycling capacity by 2030 highlights need for greater feedstock sourcing to maximize utilization

5.3.7. Electric motors, energy generators, and hard disk drives emerge as key secondary sources of rare earths

5.3.8. Pre-processing challenges for rare-earth magnet recycling from electric rotors

5.3.9. Availability of magnets for recycling influenced by lifetimes of integrated products and recycling efficiency

5.3.10. Magnet manufacturing waste to become a key feedstock for recyclers until end-of-life waste availability increases

5.3.11. Many long-loop recyclers focus on securing primary mineral feedstocks until secondary sources come online

5.3.12. Barriers to growth and areas requiring development for rare earth magnet recovery growth to be realized

5.4. Summary and outlook

5.4.1. Rare-earth magnet recovery technology summary and outlook

5.4.2. Rare-earth magnet market summary and outlook

5.4.3. Overview of opportunities and trends for long-loop and short-loop rare earth magnet recycling technologies

5.4.4. Innovation areas for rare-earth magnet recycling

5.4.5. Rare earth magnet recycling value chain

6. MARKET FORECASTS FOR RARE EARTH MAGNETS

6.1. Forecasting methodology

6.1.1. Forecasting methodology

6.1.2. Forecasting assumptions

6.1.3. Forecasting price assumptions

6.1.4. Discontinuity in feedstock availability from renewable energy applications for recycling

6.2. Rare earth magnet supply forecasts

6.2.1. 10-year global rare earth magnet production forecast by region (tonnes), 2026-2036

6.2.2. 10-year global rare earth magnet production forecast by region, excluding China (tonnes), 2026-2036

6.3. Rare earth magnet demand forecasts

6.3.1. 10-year global rare earth magnet demand forecast by application (tonnes), 2026-2036

6.3.2. Global rare earth magnet demand share by application (weight, tonnes), 2026-2036

6.3.3. 10-year global rare earth magnet demand forecast in mature markets (tonnes), 2026-2036

6.3.4. 10-year global rare earth magnet demand in e-mobility and electric vehicles forecast (tonnes), 2026-2036

6.3.5. 10-year global rare earth magnet demand in wind turbines forecast (tonnes), 2026-2036

6.3.6. 10-year global rare earth magnet demand in robotics forecast (tonnes), 2026-2036

6.3.7. 10-year global rare earth magnet demand forecast by material (tonnes), 2026-2036

6.3.8. 10-year global rare earth magnet demand forecast by material, excluding iron (tonnes), 2026-2036

6.3.9. 10-year global rare earth magnet demand forecast by material (tonnes), 2026-2036

6.3.10. 10-year global rare earth magnet demand forecast by magnet material (tonnes), 2026-2036

6.3.11. 10-year global rare earth magnet revenue forecast by application (US$M), 2026-2036

6.3.12. 10-year global rare earth magnet supply and demand forecast (ktonnes), 2026-2036

6.4. Magnet recycling forecasts

6.4.1. 10-year global rare earth magnet recycling and capacity forecast by feedstock source (tonnes), 2026-2036

6.4.2. 10-year global rare earth magnet recycling forecast by feedstock source (tonnes), 2026-2036

6.4.3. 10-year forecast of rare earth magnet recycling feedstock composition, 2026-2036

6.4.4. 10-year global rare earth magnet recycling forecast by technology (tonnes), 2026-2036

6.4.5. 10-year global rare earth magnet production forecast, segmented by primary and secondary source, 2026-2036

6.4.6. 10-year global rare earth magnet recycling forecast by material recovered (tonnes), 2026-2036

6.4.7. 10-year global rare earth magnet recycling value forecast by material recovered (US$M), 2026-2036

7. COMPANY PROFILES

7.1. 1X Technologies

7.2. Advanced Electric Machines: Rare Earth Free Motors

7.3. Apptronik, Inc

7.4. Australian Strategic Materials Ltd (ASM)

7.5. Carester (Caremag)

7.6. Carester (Caremag)

7.7. Cyclic Materials

7.8. Cyclic Materials

7.9. EVR Motors

7.10. Garner Products

7.11. GeMMe (Georesources, Mineral Engineering and Extractive Metallurgy)

7.12. HyProMag

7.13. HyProMag Ltd

7.14. Ionic Rare Earths

7.15. Ionic Technologies

7.16. JL Mag

7.17. Metalysis

7.18. Modal Motors

7.19. Monumo: AI Motor Design

7.20. Niron Magnetics: Rare Earth Free Permanent Magnets

7.21. Noveon Magnetics

7.22. QuantumScape

7.23. Rare Earth Technologies Inc. (RETi)

7.24. ReElement Technologies

7.25. REETec

7.26. Seloxium

7.27. Tesla: We, Robot Optimus Reveal

7.28. Unitree Robotics: Humanoid Robotics

7.29. Victrex

7.30. ZF: SELECT Drive Unit

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

IDTechEx社の 先端材料 - Advanced Materials&Crisical Minerals分野 での最新刊レポート

関連レポート(キーワード「レアアース」)

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|