先進固体冷却の世界市場 2026-2036年The Global Advanced Solid-State Cooling Market 2026-2036 ソリッドステート冷却市場は、従来の機械式コンプレッサーや有害な冷媒を使用せずに動作する高度な冷却ソリューションの多様なポートフォリオを包含し、熱管理技術において最もダイナミック... もっと見る

サマリー

ソリッドステート冷却市場は、従来の機械式コンプレッサーや有害な冷媒を使用せずに動作する高度な冷却ソリューションの多様なポートフォリオを包含し、熱管理技術において最もダイナミックで急速に進化している分野の1つです。この市場は、量子コンピューティング、データセンター、半導体デバイス、医療機器、持続可能なHVACシステムなど、次世代アプリケーションを実現する重要な手段として浮上している。

世界の固体冷却市場は、エネルギー効率に優れ、環境的に持続可能な冷却ソリューションに対する需要の増加により、かつてない成長を遂げている。この分野で最も成熟した技術であるサーモエレクトリック冷却分野は、すでに大きな商業的浸透を達成している。より広範なソリッドステート冷却市場は、マグネトロリック、エレクトロカロリック、LEDベースの冷却システムなどの新技術が研究室での研究から商業用途に移行するにつれて、劇的に拡大すると予測される。

この市場には6つの主要技術カテゴリーがあり、それぞれが異なる物理現象を利用して冷却効果を実現している。熱電(ペルチェ)システムは現在の市場シェアを独占しており、電子部品の冷却から医療機器の熱管理まで、多様な用途に対応しています。磁気熱量冷却は、有害な冷媒を完全に排除しながら、従来のシステムに比べて30~50%のエネルギー効率向上を約束します。

エレクトロカロリック、バロカロリック、エラストカロリック、ツイストカロリックシステムを含む新しいカロリック冷却技術は、固体技術革新の次のフロンティアを象徴しています。これらの技術は、電界、圧力、機械的応力、ねじり力をそれぞれ操作して冷却効果を得るもので、特定の用途に独自の利点を提供する。一方、LEDベースのエレクトロルミネッセンス冷却は、極低温アプリケーションに革命をもたらす可能性のある光学的冷却メカニズムへのパラダイムシフトを意味する。

ソリッドステート冷却市場は、さまざまな産業でますます高度化するアプリケーションに対応している。データセンターと通信インフラは主要な成長ドライバーである。量子技術分野は特に有望な市場セグメントとして浮上している。自動車、航空宇宙、医療機器業界では、精密な温度制御、コンパクトなフォームファクター、高い信頼性を必要とする用途で固体冷却の採用が進んでいる。ポータブル冷蔵庫やHVACシステムなどの消費者向けアプリケーションは、コストの低下と性能の向上に伴い、長期的に大きな市場機会をもたらす。

ソリッドステート冷却市場は、複数の技術が同時に商用化に近づく変曲点に立っている。冷媒の段階的廃止、エネルギー効率の義務化、量子技術の展開を推進する環境規制は、前例のない市場機会を生み出している。材料科学の進歩、製造規模の経済性、用途に特化した性能要件の融合は、今後10年間で市場が大幅に拡大し多様化することを示唆している。

この市場で成功するには、深い技術的専門知識、特定のアプリケーション・ニッチ内での戦略的ポジショニング、研究開発から商業展開への移行を慎重に進めることが必要である。企業は、技術開発投資と市場参入のタイミングをバランスさせ、この急速に進化する環境における新たな機会をとらえなければならない。

先進固体冷却の世界市場 2026-2036」は、急速に発展する世界の先進固体冷却市場を詳細に分析し、量子コンピューティング、半導体デバイス、医療機器、自動車システム、データセンターなどの冷却アプリケーションに革命をもたらしている最先端の熱管理技術を調査しています。本レポートでは、2036年まで数十億ドル規模の世界冷却市場を変革すると予測される、磁気熱源、電気熱源、LEDベースのサーモフォトニック、量子クライオジェニック、その他の革新的なソリッドステート冷却ソリューションなど、新たな冷却技術に関する戦略的洞察をお届けします。

レポート内容

本レポートは、量子コンピューティング、半導体製造、自動車、航空宇宙、医療機器、民生用電子機器業界における次世代固体冷却ソリューションの市場機会を把握し、戦略的パートナーシップの機会を特定し、技術投資の意思決定を評価し、市場参入戦略を策定しようとする技術企業、投資家、研究機関、業界専門家にとって不可欠な資料となります。

目次1 要旨

1.1 市場機会と戦略概要

1.1.1 世界の冷却市場

1.1.2 世界の固体冷却市場規模および成長予測(2025-2036年)

1.1.3 新興技術の冷却市場機会評価および競合のポジショニング

1.2 ソリッドステート冷却の利点

1.3 技術展望技術展望

1.3.1 確立した対新興のソリッドステート冷却技術

1.3. 新興固体冷却技術

1.3.2 LEDベースの熱光冷却性能ベンチマークと利点

1.3.3 量子極低温冷却の要件と市場アプリケーション

1.4 全セグメントにおける技術成熟度と商用化のタイムライン

1.5 市場セグメンテーションとアプリケーション分析

1.5.1 主要ターゲット市場:半導体冷却、量子技術、極低温アプリケーション

1.5.2 セグメント別に$価値を定量化したアプリケーション別市場サイジング

1.6 顧客ニーズ評価および採用障壁分析

1.7 温度範囲のセグメンテーション(サブ100K~150K+)とアプリケーションマッピング

1.8 競争環境と産業構造

1.8.1 サーモエレクトリック、磁気誘導体、新興技術にわたる市場シェア分析

1.8.2 主要プレーヤーのポジショニング:既存メーカー対イノベーション主導の新興企業

1.8.3 技術差別化戦略と競争優位性

1.8.4 パートナーシップ・エコシステムとバリューチェーンのポジショニング機会

1.9 LEDベース冷却

1.9.1 従来のペルチェおよび極低温システムに対する技術性能の優位性

1.9.2 対応可能な市場機会と普及シナリオ

1.9.3 最初のアプリケーションの優先順位とビーチヘッド市場戦略

1.9.4 半導体センサー冷却および量子アプリケーションに対する独自の価値提案

1.10 資金調達と投資の状況

2 はじめに

2.1 冷却の必要性

2.2 固体冷却技術の基礎と分類

2.3 熱量冷却効果

2.4 市場の進化と技術年表

2.5 分析範囲:確立された技術対新興技術

2.6 技術横断的バリューチェーン分析

2.6.1 コンポーネントおよび材料サプライヤー

2.6.2 技術開発者およびIPホルダー

2.6.3 システム・インテグレーターおよびOEM

2.6.4 エンドユーザー顧客および市場チャネル

2.6.5 流通およびサービスネットワーク

3 ソリッドステート冷却技術

3.1 熱電(ペルチェ)冷却システム

3.1.1 技術の成熟度と市場への浸透

3.1.2 熱電材料

3.1.3 性能特性と限界

3.1.4 熱電冷却および温度制御アプリケーション

3.1.5 市場規模

3.1.6 SWOT分析

3.2 磁気熱電冷却

3.2.1 技術原理と開発状況

3.2.2 商業用途

3.2.3 性能上の利点と課題

3.2.4 SWOT分析

3.3 電熱冷却

3.3.1 技術の基礎と材料システム

3.3.2 現在の開発段階と商業化スケジュール

3.3.3 市場ポテンシャルと用途

3.3.4 SWOT分析

3.4 LEDベースの固体冷却技術

3.4.1 LEDベースのサーモフォトニック冷却原理

3.4.2 技術仕様および性能パラメーター

3.4.3 従来方式を超える利点

3.4.4 技術対応レベルと開発状況

3.4.5 製造コスト分析($/Wベース)

3.4.6 温度範囲能力(サブ100K~150K)

3.4.7 対応可能な市場規模および機会

3.4.8 ソリッドステート冷却における競争環境

3.4.9 市場参入障壁と利点

3.4.10 技術差別化と独自の価値提案

3.4.11 ペルチェシステムを上回る性能上の利点

3.4.12 コスト競争力分析 vs.磁気熱量式冷却システム

3.5 フォノニック冷却システム

3.5.1 固体フォノン操作原理

3.5.2 技術アプローチと開発状況

3.5.3 市場ポジショニングと商業的可能性

3.5.4 SWOT分析

3.6 量子ドット冷却技術

3.6.1 冷却応用における量子閉じ込め効果

3.6.2 研究開発と商業的展望

3.6.3 量子コンピューティングシステムとの統合

3.7 フォトニック結晶冷却 フォトニック結晶冷却

3.7.1 技術原理と波長選択性

3.7.2 市場対応と製造上の課題

3.8 アドバンスト・サーミオン冷却

3.8.1 はじめに

3.8.2 最近のブレークスルーと商業化のタイムライン

3.8.3 電子放出冷却メカニズム

3.9 電熱冷却システム

3.9.1 電界誘起温度変化

3.9.2 ポリマーおよびセラミックベース材料

3.9.3 スケーラビリティと商業的可能性

3.10 バロカロリック冷却システム

3.10.1 圧力誘起カロリック効果と材料

3.10.2 機械的圧力循環メカニズム

3.10.3 開発状況と研究の進展

3.10.4 他の熱量冷却技術との比較

3.11 弾性熱量冷却システム

3.11.1 応力-ひずみ誘起温度変化

3.11.2 形状記憶合金およびポリマーベース材料

3.11.3 機械的サイクルおよび疲労に関する考察

3.11.4 性能特性および応用

3.12 ツイストカロリー(Torsocaloric)冷却システム

3.12.1 材料におけるツイスト誘起カロリー効果

3.12.2 カーボンナノチューブヤーンと繊維ベースのシステム

3.12.3 回転メカニカルサイクリングメカニズム

3.12.4 研究開発と商業化の可能性

3.13 固体ヒートポンプおよびエンジン

3.13.1 技術収束の機会

3.13.2 ハイブリッド冷却システム・アーキテクチャ

3.14 量子極低温冷却技術

3.14.1 断熱減磁冷凍(ADR)

3.14.1.1 単段および連続ADR(cADR)システム

3.14.1.2 常磁性塩冷却媒体

3.14.1.3 量子コンピューティングおよびセンシングにおける応用

3.14.2 希釈冷凍の代替手段

3.14.2.1 ヘリウム-3フリー冷却ソリューション

3.14.2.2 ミリケルビン温度用磁気冷凍

3.14.2.3 量子デバイス動作要件

3.14.3 超伝導冷却技術

3.14.3.1 ジョセフソン接合冷却アプリケーション

3.14.3.2 トラップイオン量子コンピュータ冷却

3.14.3.3 超伝導量子ビットの熱管理

3.14.4 量子センシングと通信の冷却

3.14.4.1 単一光子検出器冷却要件

3.14.4.2 NVセンターおよび量子センサー熱管理

3.14.4.3 光量子デバイス冷却の課題

3.15 比較技術分析

3.15.1 全技術にわたる性能ベンチマークマトリックス

3.15.2 アプリケーション・セグメント別のコスト競争力分析

3.15.3 アプリケーション適合性マッピングと温度範囲

3.15.4 技術ロードマップと収束傾向

3.15.5 量子技術統合能力

4 世界固体冷却市場分析

4.1 市場全体のセグメンテーションとサイジング

4.1.1 世界の固体冷却市場の概要(金額)

4.1.2 技術セグメントの内訳と市場シェア

4.1.3 地域別市場分析と成長パターン

4.1.4 市場促進要因と成長触媒

4.2 アプリケーションベースの市場セグメンテーション

4.2.1 温度要件別の主要市場セグメント

4.2.1.1 極低温アプリケーション(100-100K未満)

4.2.1.2 超低温アプリケーション(100-150K)

4.2. アプリケーションベースの市場セグメンテーション

4.2.2 クロステクノロジー・アプリケーション分析

4.2.2.1 半導体センサー冷却

4.2.2.2 科学機器

4.2.2.3 医療機器および診断

4.2.2.4 防衛および航空宇宙

4.2.2.5 民生用電子機器の熱管理

4.2.2.6 データセンターおよびITの冷却

4.2.2.7 自動車の熱システム

4.2.3 成長予測および市場力学(5~10年の展望)

4.3 市場セグメントにわたる顧客ニーズ評価

4.3.1 用途別性能要件

4.3.2 コスト感度および価値推進要因

4.3.3 技術採用基準および決定要因

5 企業プロファイル (54社のプロファイル)6 付録

6.1 報告書の作成方法

7 参考文献図表リスト表の一覧

表1 世界のソリッドステート冷却市場規模(2025~2036年)

表2 確立したソリッドステート冷却技術と新興

表3 LEDベースのサーモフォトニック冷却の性能ベンチマークと優位性

表4 量子極低温冷却の要件と市場用途

表5 ソリッドステート冷却技術の準備レベル

表6 セグメント別に$価値を定量化した用途別市場サイジング

表7 温度範囲のセグメンテーション(サブ100K~150K+)

表8 技術の差別化戦略と競争上の優位性

表9 従来のペルチェおよび極低温システムに対する技術性能の優位性

表10 熱電(ペルチェ)冷却システム 性能特性と限界

表11 磁気熱電冷却 性能と従来システムとの比較

表12 磁気熱電冷却 商業用途

表13 磁気熱電冷却 性能の優位性と課題

表14 電気熱電材料と性能特性および性能特性

表15 材料タイプ別の電気熱量効果温度変化

表16 LED 冷却性能パラメータおよび仕様

表17 冷却用途の GaAs LED 性能特性

表18 LED 冷却と熱電冷却の性能比較

表19 LED 冷却技術の準備レベルと開発状況

表20 LED 冷却製造コスト分析 ($/W ベース)

表21 LED 冷却温度範囲能力 (100K~150K)

表22 アプリケーション別量子冷却要件

表23 量子デバイス動作温度要件

表24 ジョセフソン接合冷却アプリケーション

表25 光量子デバイス冷却の課題

表26 全技術にわたる性能ベンチマークマトリックス

表27 アプリケーションセグメント別コスト競争力分析

表28 世界の固体冷却市場規模 エンドユーザー市場別(2020~2036年)

表29 固体冷却の世界市場規模:技術別(2020-2036年)、百万米ドル

表30 技術タイプ別価格実績推移

表31 地域別市場分析-2022-2036年地域別収益、百万米ドル

表32 市場促進要因と成長触媒

表33 極低温アプリケーション(100K未満)

表34 超低温アプリケーション(100~150K)

表35 中温冷却アプリケーション(>150K)

表36 半導体センサー固体冷却

表37 民生用電子機器の熱管理における固体冷却

表38自動車熱システムにおける固体冷却

表39 アプリケーション別性能要件

図一覧

図1 世界のソリッドステート冷却市場規模(2025-2036年)

図2 ソリッドステート冷却の商業化スケジュール

図3 ソリッドステート冷却技術のスケジュール

図4 ソリッドステート冷却のバリューチェーン

図5 サーモエレクトロニクスにおけるソリッドステート冷却のバリューチェーン

図5 熱電冷却の動作

図6 熱電(ペルチェ)冷却システムのSWOT分析

図7 磁気熱効果

図8 磁気熱冷却のSWOT分析

図9 電気熱冷却

図10 電気熱冷却の現在の開発段階と商業化のタイムライン

図11 電気熱冷却のSWOT分析

図12 エレクトロルミネッセンス冷却の簡単なスケッチ

図13 フォノニック冷却の SWOT 分析

図14 アドバンスド・サーミオニック冷却の商業化スケジュール

図15 ADR (断熱消磁冷凍) プロセス

図16 連続 ADR (cADR) システム・アーキテクチャ

図17 アプリケーションの適合性マッピングと温度範囲

図18 ソリッドステート冷却技術のロードマップ

図19 ソリッドステート冷却の世界市場規模、エンドユーザー市場別(2020-2036 年)

図20 固体冷却の技術別世界市場規模(2020~2036 年)百万米ドル

図21 技術セグメントの内訳と市場シェア

図22 地域別市場分析-地域別収益、百万米ドル

図23 Pascal 固体冷媒プロトタイプ

図24 μ冷却ファン・オン・チップ

Summary

The solid-state cooling market represents one of the most dynamic and rapidly evolving sectors in thermal management technology, encompassing a diverse portfolio of advanced cooling solutions that operate without traditional mechanical compressors or harmful refrigerants. This market has emerged as a critical enabler for next-generation applications spanning quantum computing, data centers, semiconductor devices, medical equipment, and sustainable HVAC systems.

The global solid-state cooling market is experiencing unprecedented growth, driven by increasing demand for energy-efficient, environmentally sustainable cooling solutions. The thermoelectric cooling segment, representing the most mature technology within this space, has already achieved significant commercial penetration. The broader solid-state cooling market is projected to expand dramatically as emerging technologies like magnetocaloric, electrocaloric, and LED-based cooling systems transition from laboratory research to commercial applications.

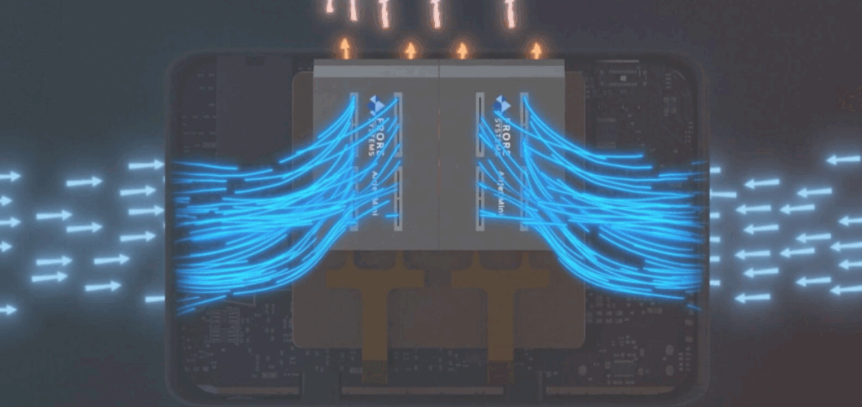

The market encompasses six major technology categories, each leveraging different physical phenomena to achieve cooling effects. Thermoelectric (Peltier) systems dominate current market share, serving diverse applications from electronic component cooling to medical device thermal management. Magnetocaloric cooling promises 30-50% energy efficiency improvements over conventional systems while eliminating harmful refrigerants entirely.

Emerging caloric cooling technologies—including electrocaloric, barocaloric, elastocaloric, and twistocaloric systems—represent the next frontier of solid-state innovation. These technologies manipulate electric fields, pressure, mechanical stress, and torsional forces respectively to achieve cooling effects, offering unique advantages for specific applications. Meanwhile, LED-based electroluminescent cooling represents a paradigm shift toward optical cooling mechanisms that could revolutionize cryogenic applications.

The solid-state cooling market serves increasingly sophisticated applications across multiple industries. Data centers and telecommunications infrastructure represent major growth drivers. The quantum technology sector has emerged as a particularly promising market segment. Automotive, aerospace, and medical device industries are increasingly adopting solid-state cooling for applications requiring precise temperature control, compact form factors, and high reliability. Consumer applications, including portable refrigeration and HVAC systems, represent significant long-term market opportunities as costs decrease and performance improves.

The solid-state cooling market stands at an inflection point where multiple technologies are approaching commercial viability simultaneously. Environmental regulations driving refrigerant phase-outs, energy efficiency mandates, and quantum technology deployment are creating unprecedented market opportunities. The convergence of materials science advances, manufacturing scale economies, and application-specific performance requirements suggests the market will experience substantial expansion and diversification over the next decade.

Success in this market requires deep technical expertise, strategic positioning within specific application niches, and careful navigation of the transition from research and development to commercial deployment. Companies must balance technology development investments with market timing to capture emerging opportunities in this rapidly evolving landscape.

The Global Advanced Solid-State Cooling Market 2026-2036 provides an in-depth analysis of the rapidly evolving global advanced solid-state cooling market, examining cutting-edge thermal management technologies that are revolutionizing cooling applications across quantum computing, semiconductor devices, medical equipment, automotive systems, and data centers. The report delivers strategic insights into emerging cooling technologies including magnetocaloric, electrocaloric, LED-based thermophotonic, quantum cryogenic, and other innovative solid-state cooling solutions projected to transform the multi-billion global cooling market through 2036.

Report contents include

This report serves as an essential resource for technology companies, investors, research institutions, and industry professionals seeking to understand market opportunities in advanced thermal management, identify strategic partnership opportunities, evaluate technology investment decisions, and develop go-to-market strategies for next-generation solid-state cooling solutions across quantum computing, semiconductor manufacturing, automotive, aerospace, medical device, and consumer electronics industries.

Table of Contents1 EXECUTIVE SUMMARY

1.1 Market Opportunity and Strategic Overview

1.1.1 The global cooling market

1.1.2 Global solid-state cooling market size and growth projections (2025-2036)

1.1.3 Emerging technologies cooling market opportunity assessment and competitive positioning

1.2 Advantages of Solid-state Cooling

1.3 Technology Landscape

1.3.1 Established vs. emerging solid-state cooling technologies

1.3.2 LED-based thermophotonic cooling performance benchmarks and advantages

1.3.3 Quantum cryogenic cooling requirements and market applications

1.4 Technology readiness levels and commercialization timelines across all segments

1.5 Market Segmentation and Application Analysis

1.5.1 Primary target markets: semiconductor cooling, quantum technologies, cryogenic applications

1.5.2 Application-specific market sizing with $-value quantification by segment

1.6 Customer needs assessment and adoption barriers analysis

1.7 Temperature range segmentation (sub-100K to 150K+) and application mapping

1.8 Competitive Landscape and Industry Structure

1.8.1 Market share analysis across thermoelectric, magnetocaloric, and emerging technologies

1.8.2 Key player positioning: established manufacturers vs. innovation-driven startups

1.8.3 Technology differentiation strategies and competitive advantages

1.8.4 Partnership ecosystems and value chain positioning opportunities

1.9 LED-Based Cooling

1.9.1 Technology performance advantages over conventional Peltier and cryogenic systems

1.9.2 Addressable market opportunity and penetration scenarios

1.9.3 First application priorities and beachhead market strategies

1.9.4 Unique value propositions for semiconductor sensor cooling and quantum applications

1.10 Funding and Investment Landscape

2 INTRODUCTION

2.1 Need for cooling

2.2 Solid state cooling technology fundamentals and classification

2.3 Caloric cooling effects

2.4 Market evolution and technology timeline

2.5 Scope of analysis: established vs. emerging technologies

2.6 Value Chain Analysis Across Technologies

2.6.1 Component and material suppliers

2.6.2 Technology developers and IP holders

2.6.3 System integrators and OEMs

2.6.4 End-user customers and market channels

2.6.5 Distribution and service networks

3 SOLID-STATE COOLING TECHNOLOGIES

3.1 Thermoelectric (Peltier) cooling systems

3.1.1 Technology maturity and market penetration

3.1.2 Thermoelectric materials

3.1.3 Performance characteristics and limitations

3.1.4 Thermoelectric cooling and temperature control applications

3.1.5 Market size

3.1.6 SWOT analysis

3.2 Magnetocaloric cooling

3.2.1 Technology principles and development status

3.2.2 Commercial applications

3.2.3 Performance advantages and challenges

3.2.4 SWOT analysis

3.3 Electrocaloric cooling

3.3.1 Technology fundamentals and material systems

3.3.2 Current development stage and commercialization timeline

3.3.3 Market potential and applications

3.3.4 SWOT analysis

3.4 LED-based Solid-state cooling technologies

3.4.1 LED-based thermophotonic cooling principles

3.4.2 Technical specifications and performance parameters

3.4.3 Advantages over conventional methods

3.4.4 Technology readiness level and development status

3.4.5 Manufacturing cost analysis ($/W basis)

3.4.6 Temperature range capabilities (sub-100K to 150K)

3.4.7 Addressable market size and opportunity

3.4.8 Competitive landscape within solid-state cooling

3.4.9 Market entry barriers and advantages

3.4.10 Technology differentiation and unique value propositions

3.4.11 Performance advantages over Peltier systems

3.4.12 Cost competitiveness analysis vs. magnetocaloric

3.5 Phononic cooling systems

3.5.1 Solid-state phonon manipulation principles

3.5.2 Technology approach and development status

3.5.3 Market positioning and commercial potential

3.5.4 SWOT analysis

3.6 Quantum dot cooling technologies

3.6.1 Quantum confinement effects in cooling applications

3.6.2 Research developments and commercial prospects

3.6.3 Integration with quantum computing systems

3.7 Photonic crystal cooling

3.7.1 Technology principles and wavelength selectivity

3.7.2 Market readiness and manufacturing challenges

3.8 Advanced thermionic cooling

3.8.1 Introduction

3.8.2 Recent breakthroughs and commercialization timeline

3.8.3 Electron emission cooling mechanisms

3.9 Electrocaloric cooling systems

3.9.1 Electric field-induced temperature changes

3.9.2 Polymer and ceramic-based materials

3.9.3 Scalability and commercial potential

3.10 Barocaloric cooling systems

3.10.1 Pressure-induced caloric effects and materials

3.10.2 Mechanical pressure cycling mechanisms

3.10.3 Development status and research progress

3.10.4 Comparison with other caloric cooling technologies

3.11 Elastocaloric cooling systems

3.11.1 Stress-strain induced temperature changes

3.11.2 Shape-memory alloy and polymer-based materials

3.11.3 Mechanical cycling and fatigue considerations

3.11.4 Performance characteristics and applications

3.12 Twistocaloric (Torsocaloric) cooling systems

3.12.1 Twist-induced caloric effects in materials

3.12.2 Carbon nanotube yarns and fiber-based systems

3.12.3 Rotational mechanical cycling mechanisms

3.12.4 Research developments and commercialization potential

3.13 Solid-state heat pumps and engines

3.13.1 Technology convergence opportunities

3.13.2 Hybrid cooling system architectures

3.14 Quantum cryogenic cooling technologies

3.14.1 Adiabatic Demagnetization Refrigeration (ADR)

3.14.1.1 Single-stage and continuous ADR (cADR) systems

3.14.1.2 Paramagnetic salt cooling media

3.14.1.3 Applications in quantum computing and sensing

3.14.2 Dilution refrigeration alternatives

3.14.2.1 Helium-3 free cooling solutions

3.14.2.2 Magnetic refrigeration for millikelvin temperatures

3.14.2.3 Quantum device operation requirements

3.14.3 Superconducting cooling technologies

3.14.3.1 Josephson junction cooling applications

3.14.3.2 Trapped-ion quantum computer cooling

3.14.3.3 Superconducting qubit thermal management

3.14.4 Quantum sensing and communication cooling

3.14.4.1 Single-photon detector cooling requirements

3.14.4.2 NV center and quantum sensor thermal management

3.14.4.3 Optical quantum device cooling challenges

3.15 Comparative Technology Analysis

3.15.1 Performance benchmarking matrix across all technologies

3.15.2 Cost competitiveness analysis by application segment

3.15.3 Application suitability mapping and temperature ranges

3.15.4 Technology roadmap and convergence trends

3.15.5 Quantum technology integration capabilities

4 GLOBAL SOLID STATE COOLING MARKET ANALYSIS

4.1 Overall Market Segmentation and Sizing

4.1.1 Global solid-state cooling market overview ($ values)

4.1.2 Technology segment breakdown and market share

4.1.3 Regional market analysis and growth patterns

4.1.4 Market drivers and growth catalysts

4.2 Application-Based Market Segmentation

4.2.1 Primary market segments by temperature requirements

4.2.1.1 Cryogenic applications (sub-100K)

4.2.1.2 Ultra-low temperature applications (100-150K)

4.2.1.3 Moderate cooling applications (>150K)

4.2.2 Cross-technology application analysis

4.2.2.1 Semiconductor sensor cooling

4.2.2.2 Scientific instrumentation

4.2.2.3 Medical devices and diagnostics

4.2.2.4 Defence and aerospace

4.2.2.5 Consumer electronics thermal management

4.2.2.6 Data center and IT cooling

4.2.2.7 Automotive thermal systems

4.2.3 Growth projections and market dynamics (5-10 year outlook)

4.3 Customer needs assessment across market segments

4.3.1 Performance requirements by application

4.3.2 Cost sensitivity and value drivers

4.3.3 Technology adoption criteria and decision factors

5 COMPANY PROFILES 165 (54 company profiles)6 APPENDIX

6.1 Report methodology

7 REFERENCESList of Tables/GraphsList of Tables

Table1 Global solid-state cooling market size (2025-2036)

Table2 Established vs. emerging solid-state cooling technologies

Table3 LED-based thermophotonic cooling performance benchmarks and advantages

Table4 Quantum cryogenic cooling requirements and market applications

Table5 Solid-state Cooling Technology readiness levels

Table6 Application-specific market sizing with $-value quantification by segment

Table7 Temperature range segmentation (sub-100K to 150K+)

Table8 Technology differentiation strategies and competitive advantages

Table9 Technology performance advantages over conventional Peltier and cryogenic systems

Table10 Thermoelectric (Peltier) cooling systems Performance characteristics and limitations

Table11 Magnetocaloric Cooling Performance vs Conventional Systems

Table12 Magnetocaloric cooling Commercial applications

Table13 Magnetocaloric cooling Performance advantages and challenges

Table14 Electrocaloric Materials and Performance Characteristics

Table15 Electrocaloric Effect Temperature Changes by Material Type

Table16 LED Cooling Performance Parameters and Specifications

Table17 GaAs LED Performance Characteristics for Cooling Applications

Table18 LED Cooling vs Thermoelectric Cooling Performance Comparison

Table19 LED Cooling Technology readiness level and development status

Table20 LED Cooling manufacturing cost analysis ($/W basis)

Table21 LED Cooling Temperature range capabilities (sub-100K to 150K)

Table22 Quantum Cooling Requirements by Application

Table23 Quantum Device Operating Temperature Requirements

Table24 Josephson junction cooling applications

Table25 Optical quantum device cooling challenges

Table26 Performance benchmarking matrix across all technologies

Table27 Cost competitiveness analysis by application segment

Table28 Global Solid State Cooling Market Size by End User Market (2020-2036), Millions USD

Table29 Global Solid State Cooling Market Size by Technology (2020-2036), Millions USD

Table30 Price Performance Evolution by Technology Type

Table31 Regional Market Analysis - Revenue by Geography 2022-2036, Millions USD

Table32 Market drivers and growth catalysts

Table33 Cryogenic applications (sub-100K)

Table34 Ultra-low temperature applications (100-150K)

Table35 Moderate cooling applications (>150K)

Table36 Semiconductor sensor Solid-state cooling

Table37 Solid-state cooling in Consumer electronics thermal management

Table38 Solid-state cooling in Automotive thermal systems

Table39 Performance requirements by application

List of Figures

Figure1 Global solid-state cooling market size (2025-2036)

Figure2 Solid-state Cooling commercialization timelines

Figure3 Solid-state cooling technology timeline

Figure4 Solid-state cooling value chain

Figure5 Thermoelectric cooling operation

Figure6 Thermoelectric (Peltier) cooling systems SWOT analysis

Figure7 Magnetocaloric Effect

Figure8 Magnetocaloric cooling SWOT analysis

Figure9 Electrocaloric cooling

Figure10 Electrocaloric cooling current development stage and commercialization timeline

Figure11 Electrocaloric cooling SWOT analysis

Figure12 Simple sketch of electroluminescent cooling

Figure13 Phonoic cooling SWOT analysis

Figure14 Advanced thermionic cooling commercialization timeline

Figure15 Adiabatic Demagnetization Refrigeration (ADR) Process

Figure16 Continuous ADR (cADR) System Architecture

Figure17 Application suitability mapping and temperature ranges

Figure18 Solid-state cooling technology roadmap

Figure19 Global Solid State Cooling Market Size by End User Market (2020-2036), Millions USD

Figure20 Global Solid State Cooling Market Size by Technology (2020-2036), Millions USD

Figure21 Technology segment breakdown and market share

Figure22 Regional Market Analysis - Revenue by Geography, Millions USD

Figure23 Pascal solid refrigerant prototype

Figure24 μCooling fan-on-a-chip

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(ケミカル)の最新刊レポート

Future Markets, inc.社の アドバンスドマテリアル分野 での最新刊レポートよくあるご質問Future Markets, inc.社はどのような調査会社ですか?Future Markets, inc.は先端技術に焦点をあてたスウェーデンの調査会社です。 2009年設立のFMi社は先端素材、バイオ由来の素材、ナノマテリアルの市場をトラッキングし、企業や学... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|