金属積層造形の2025-2035年:技術、プレーヤー、市場展望Metal Additive Manufacturing 2025-2035: Technologies, Players, and Market Outlook 粉末床溶融、指向性エネルギー蒸着、バインダージェッティングなどを含む金属3Dプリンティング技術のベンチマークAMハードウェアと材料の10年間のきめ細かな市場予測。主要プレーヤー分析と市場展望。 ... もっと見る

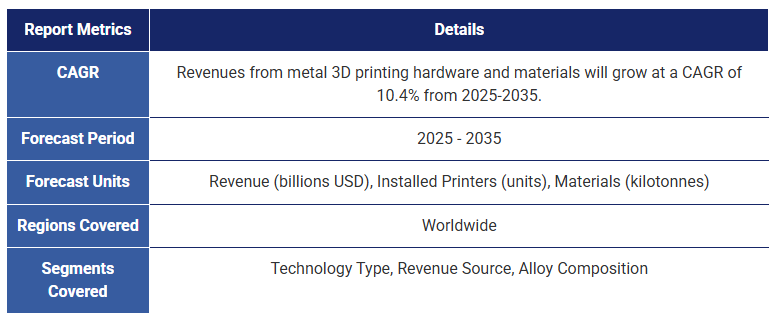

サマリー 粉末床溶融、指向性エネルギー蒸着、バインダージェッティングなどを含む金属3Dプリンティング技術のベンチマークAMハードウェアと材料の10年間のきめ細かな市場予測。主要プレーヤー分析と市場展望。 1990年代に商業化された金属積層造形(金属3Dプリンティングとも呼ばれる)は、過去10年間に大きな注目を集めました。この期間には、COVID-19の大流行から金属3Dプリンティング新興企業の盛衰、中国の積層造形市場の台頭、斬新な金属AM技術の継続的な出現に至るまで、業界を揺るがす数々の出来事があった。金属3Dプリンティング業界がダイナミックであることは間違いなく、マクロ経済環境が厳しくなっても監視する価値のある市場です。 IDTechExのこの包括的な技術レポートは、業界の詳細な現状と見通しを示している。市場におけるIDTechExの歴史と多数の一次インタビューに基づき、本レポートは市場の偏りのない予測を提供しています。 きめ細かな予測と詳細なプレイヤーのプロフィール 本レポートでは、業界の10年間のきめ細かな市場予測を提供しています。今後10年間の金属プリンティングハードウェアと金属3Dプリンティング材料の需要を定量化しています。プリンター技術と材料について、9つの技術セグメントと9つの材料セグメントに分けて、的を絞った定量分析を行っています。 IDTechExのアナリストが作成したこれらの予測は、一般に公開されているものをはるかに超え、広範な数の一次インタビューに基づいており、読者に最も重要な情報を提供している。このレポートには、主要OEM、破壊的新興企業、既存粉体プロバイダー、新興材料企業など、100社以上の企業プロフィールが含まれている。  競争力のあるプリンタープロセスのベンチマーク 金属積層造形に提案されている利点は、設計の自由度、局所的な多用途製造、潜在的なコスト削減、製造時間の短縮など、数多くある。 これを利用するために、多くの材料原料を使用するプリンタープロセス群が拡大し続けている。新規参入者の一般的な戦術は、競争相手と差別化するために、自社の技術に新しい用語を発明することである。これらの中にはユニークなものもあるが、ほとんどは既存のプロセスに沿ったもので、微妙なバリエーションを導入しているに過ぎない。 本レポートは、このようなマーケティングに切り込み、業界にとって利用しやすい公平な分類を提供する。現実には、どのプロセスも、速度、価格、精度、サイズ、材料適合性など、何かを妥協しなければならない。IDTechExは、これらのプロセスの重要なベンチマーク研究を提供しています。これは、市場と最終用途におけるギャップを特定するために不可欠なプロセスです。 考慮すべき学習曲線もある。大きな値札のついた(主に)B2Bの新技術と同様、エンドユーザーがそのプロセスと付加価値に自信を持ち、投資を正当化するには時間がかかる。粉末床溶融プロセス(DMLS/SLMとEBM)は、最も長い間商業化されており、その結果、この技術がほとんどの設備を支えている。しかし、次世代技術の牽引力が強まっているため、今後10年以内に、より多様な設置ベースが観察されるようになるだろう。 市場の隙間を見つけようとする新規参入企業には、いくつかの包括的な傾向がある。低コストのバリエーション、マイクロから超大型までの極端なサイズを押し進めるプリンター、より高速な速度、代替形態の原料を利用するプリンターなど、すべてが急速に台頭し、評価されている。 拡大する材料ポートフォリオ、生産能力、競争 IDTechExは、年間収益の大半はプリンターの販売や設置よりもむしろ材料需要からもたらされると予測している。プリンターのプロセスや用途ごとに、材料要件、スループット率、合金需要は異なる。 この業界では、注目すべき買収、生産能力の拡大、噴霧化プロセスの改善、新材料、コスト削減など、多くの動きがある。プレーヤーは、よく知られた構造用合金から、MMC、高エントロピー合金、アモルファス合金などの高度なオプションまで、積層造形用に特化した材料ポートフォリオを導入している。 この業界全体のばらつきを考慮すると、コストと量を考慮した場合の予測は大きく異なる。チタン粉が最も重要であることは、拡張、投資、垂直統合、スクラップ原料の使用などの新たな道を探るという市場力学からも明らかである。 航空宇宙やヘルスケアなど、金属積層造形の主要市場 金属積層造形は、プロトタイプ、ツーリング、交換部品、小規模から大規模の製造に使用されている。石油・ガス、宝飾品、建築・建設など、この新興技術が大きな支持を得ている分野は複数ある。成長と採用はすべて高価値産業で行われており、長期的な未来は非常に楽観的である。 しかし、より不透明な経済・貿易環境の中で、金属積層造形の将来についても疑問が投げかけられている。一方では、関税に関する絶え間ない議論により、国内の分散型製造事業への関心が一般的に高まっており、金属積層造形はサプライチェーンの問題を解決する重要なツールとして機能する可能性を秘めている。その一方で、積層造形のような新技術への投資に対する消極的な姿勢は、この急速に変化する経済情勢の中でエンドユーザーの採用に影響を与える可能性がある。本レポートでは、10年以内に金属積層造形に影響を与える多くのトレンドと世界市場要因について分析しています。 本レポートで回答する主な質問

本レポートでは、金属積層造形に関する以下の情報を提供しています: 技術動向&メーカー分析

市場予測&分析:

目次

1. エグゼクティブサマリー

1.1. 3Dプリンティングプロセスの概要

1.2. 3Dプリンティングの成長を促進する要因と制約

1.3. 金属積層造形:技術概要

1.4. 金属3Dプリンティング技術の概要

1.5. 業界のトレンド: 中国の金属積層造形市場の台頭

1.6. 業界のトレンド: 関税、貿易戦争、リショアリング

1.7. 金属積層造形における主要技術トレンド

1.8. 金属積層造形における主要技術トレンド(繰り返し)

1.9. 2024年における金属積層造形の投資概況

1.10. 金属3Dプリンティング市場におけるサービスの重要性

1.11. 金属積層造形予測 2025-2035

1.12. 予測で使用される技術セグメンテーションの説明

1.13. 金属積層造形 - 技術市場シェアの進化

1.14. 金属3Dプリンティングハードウェア予測 2025-2035:技術別

1.15. 金属3Dプリンティングハードウェア予測 2025-2035:技術別(II)

1.16. 金属積層造形材料予測 2025-2035:技術別

1.17. 金属積層造形材料予測 2025-2035:技術別(II)

1.18. 積層造形用金属 - 合金別市場シェアの進化

1.19. 金属積層造形材料予測 2025-2035:合金別

1.20. 金属積層造形材料予測 2025-2035:合金別(II)

1.21. 企業プロファイル

1.22. IDTechExサブスクリプションでさらに詳細にアクセス

2. はじめに

2.1. 用語集:一般的な略語

2.2. レポートの範囲

2.3. 3Dプリンティングプロセスの概要

2.4. 材料とプロセスの関係

2.5. なぜ3Dプリンティングを採用するのか?

2.6. 金属3Dプリンティングのタイムライン

2.7. ビジネスモデル: プリンター販売 vs 部品販売

2.8. 3Dプリンティングの成長を促進する要因と制約

3. 金属積層造形市場分析

3.1. 業界の財務状況と進化

3.1.1. 3Dプリンティング業界の最近の財務パフォーマンス

3.1.2. 2024年における金属3Dプリンティングに影響を与えたマクロ経済要因:金利

3.1.3. 2024年における金属3Dプリンティングに影響を与えたマクロ経済要因:ヨーロッパ経済

3.1.4. 金属3Dプリンティングに影響を与えるマクロ経済要因:関税、貿易戦争、リショアリング

3.1.5. レーザー粉末床溶融ハードウェア市場シェア:多様化の継続

3.1.6. 金属積層造形 - 技術市場シェアの進化

3.1.7. 積層造形用金属 - 合金別市場シェアの進化

3.2. 金属3Dプリンティングにおける財務とプレイヤーの活動

3.2.1. 2024年の金属積層造形投資概況

3.2.2. 金属AM関連企業へのプライベートファンディング:2021-2024年

3.2.3. 中国の金属AM企業へのプライベートファンディング:2024年

3.2.4. 金属3Dプリンティングへのプライベートファンディング:2023年 vs 2024年

3.2.5. 金属3Dプリンティングのプライベートファンディングの傾向:2023年 vs 2024年

3.2.6. 金属3Dプリンティングの最近の注目すべき買収

3.2.7. 買収スポットライト:Nano DimensionがDesktop MetalとMarkforgedを買収

3.2.8. 買収スポットライト:Nano DimensionがDesktop MetalとMarkforgedを買収(II)

3.2.9. 3Dプリンティング関連企業の上場:2021-2024年

3.2.10. 2024年における金属AMの参入および退出の概要

3.2.11. その他の金属3Dプリンティングプレイヤーの更新情報

3.3. 金属積層造形における業界のトレンドと議論

3.3.1. トレンド:手頃でコスト競争力のある金属3Dプリンター

3.3.2. トレンド:大型フォーマットLPBFプリンティング

3.3.3. トレンド:金属積層造形材料における持続可能性

3.3.4. トレンド:電子ビーム溶融(EBM)への関心の再燃

3.3.5. 中国の金属積層造形市場の台頭

3.3.6. 金属バインダージェッティングの進展

3.3.7. 金属3Dプリンティング市場におけるサービスの重要性

4. 金属プリンティングプロセス

4.1. 確立された金属プリンティング技術

4.1.1. 粉末床溶融:直接金属レーザー焼結(DMLS)または選択的レーザー溶融(SLM)

4.1.2. 粉末床溶融:電子ビーム溶融(EBM)

4.1.3. 指向エネルギー堆積:粉末(または吹き付け粉末)

4.1.4. 指向エネルギー堆積:ワイヤー

4.1.5. バインダージェッティング:金属バインダージェッティング

4.1.6. バインダージェッティング:砂バインダージェッティング

4.1.7. シートラミネーション:超音波積層造形(UAM)

4.2. 新興金属プリンティング技術

4.2.1. 新興3Dプリンティングプロセス:概要

4.2.2. 押出成形:金属-ポリマーフィラメント(MPFE)

4.2.3. 押出成形:金属-ポリマーペレット

4.2.4. 押出成形:金属ペースト

4.2.5. バット光重合:デジタルライトプロセッシング(DLP)

4.2.6. 材料ジェッティング:ナノ粒子ジェッティング(NPJ)

4.2.7. 材料ジェッティング:液体金属または磁気流体堆積

4.2.8. 材料ジェッティング:電気化学的堆積

4.2.9. 材料ジェッティング:冷間スプレー

4.2.10. バインダージェッティングの進展

4.2.11. PBFおよびDEDの開発:エネルギー源

4.2.12. PBFおよびDEDの開発:低コストプリンター

4.2.13. PBFおよびDEDの開発:新技術

4.2.14. 金属スラリー供給原料を使用するプロセス

4.2.15. DMLS/SLMの代替新興技術

5. 金属プリンター:比較とベンチマーク

5.1.1. 金属積層造形:技術概要

5.1.2. ベンチマーク:最大ビルドボリューム

5.1.3. ベンチマーク:ビルドレート

5.1.4. ベンチマーク:Z解像度

5.1.5. ベンチマーク:XY解像度

5.1.6. ベンチマーク:価格 vs ビルドボリューム

5.1.7. ベンチマーク:価格 vs ビルドレート

5.1.8. ベンチマーク:価格 vs Z解像度

5.1.9. ベンチマーク:ビルドレート vs ビルドボリューム

5.1.10. ベンチマーク:ビルドレート vs Z解像度

5.1.11. 金属3Dプリンティング技術の概要

5.1.12. 金属3Dプリンティング技術の最大値と最小値

6. 3Dプリンティング用金属材料

6.1. 金属粉末

6.1.1. 金属AMフィードストックオプションの概要

6.1.2. 粉末形態仕様

6.1.3. 確立された原子化技術:水、ガス、プラズマ原子化

6.1.4. 新興粉末製造技術:電解

6.1.5. 粉末形態は原子化プロセスに依存

6.1.6. 粉末製造技術の評価

6.1.7. プリント技術に対する金属の適合性

6.1.8. AM用金属粉末の供給者:金属別にセグメント化

6.1.9. AM用金属粉末の供給者:原子化プロセス別にセグメント化

6.1.10. チタン粉末 - 概要

6.1.11. チタン粉末 - 主なプレイヤー(I)

6.1.12. チタン粉末 - 主なプレイヤー(II)

6.1.13. 金属積層造形用主要素材のスタートアップ

6.1.14. リサイクルチタンフィードストック

6.1.15. 金属粉末床溶融後処理

6.1.16. 金属粉末使用における障壁と制約

6.2. その他の金属フィードストック

6.2.1. 金属ワイヤーフィードストック

6.2.2. 金属-ポリマーフィラメントおよびペレット

6.2.3. 商業例:Forward AMのUltrafuseフィラメント

6.2.4. 金属-光重合樹脂

7. 互換性のある金属材料

7.1.1. 合金および材料特性

7.1.2. アルミニウムおよびアルミニウム合金

7.1.3. アルミニウムAM材料ポートフォリオの拡大

7.1.4. 銅および青銅

7.1.5. 銅での3Dプリンティング:多くの機会を秘めた挑戦的な材料

7.1.6. 銅AM材料ポートフォリオの拡大

7.1.7. 銅3Dプリンティングの現在の用途

7.1.8. コバルトおよび合金

7.1.9. ニッケル合金:インコネル625

7.1.10. ニッケル合金:インコネル718

7.1.11. 貴金属および合金

7.1.12. マレージング鋼1.2709

7.1.13. 15-5PHステンレス鋼

7.1.14. 17-4PHステンレス鋼

7.1.15. 316Lステンレス鋼

7.1.16. チタンおよび合金

7.1.17. 高エントロピー合金(HEA)のAM

7.1.18. アモルファス合金のAM

7.1.19. 新興アルミニウム合金および金属マトリックス複合材料(MMC)

7.1.20. マルチマテリアルソリューション

7.1.21. 積層造形材料のためのマテリアルインフォマティクス

7.1.22. 積層造形材料のためのマテリアルインフォマティクス(II)

7.1.23. タングステン粉末およびナノ粒子

8. 金属3Dプリンティングの主な応用

8.1. 航空、宇宙、防衛における金属3Dプリンティング

8.1.1. GEアビエーション:LEAP燃料ノズル

8.1.2. GEアビエーション:次世代RISEエンジン

8.1.3. GEアビエーション:ブリードエア部品およびターボプロップエンジン

8.1.4. GEアビエーションおよびボーイング777X:GE9Xエンジン

8.1.5. ボーイング787ドリームライナー:Ti-6Al-4V構造

8.1.6. ボーイング:チヌークヘリコプターのギアボックス

8.1.7. ボーイングおよびMaxar Technologies:衛星

8.1.8. エアバスおよびEutelsat:衛星

8.1.9. オートデスクおよびエアバス:最適化された仕切壁

8.1.10. RUAG SpaceおよびAltair:アンテナマウント

8.1.11. ホフマン:酸素供給管

8.1.12. リラティビティ・スペース:ロケット

8.1.13. OEM AM戦略 - GEアエロスペースおよびColibrium Additive

8.1.14. OEM AM戦略 - エアバス

8.1.15. OEM AM戦略 - ボーイング

8.1.16. OEM AM戦略 - ロールス・ロイス

8.2. 医療および歯科における金属3Dプリンティング

8.2.1. 医療分野で最も一般的な3Dプリンティング技術

8.2.2. カスタムプレート、インプラント、バルブ、ステントの3Dプリンティング

8.2.3. 医療用金属材料:チタン合金粉末

8.2.4. ケーススタディ:股関節置換手術の再手術

8.2.5. ケーススタディ:犬の頭蓋骨プレート(チタン製)

8.2.6. ケーススタディ:歯科用インプラントデバイスと義歯

8.2.7. ケーススタディ:下顎再建手術

9. 金属3Dプリンティングの部品製造サービス

9.1. 3Dプリンティングサービスビューローとは?

9.2. サービスビューローの役割

9.3. サービスビューローの価値提案

9.4. 積層造形のためのデザイン(DfAM)

9.5. 金属AMに特化した注目すべきサービスビューロー

9.6. サービスビューローが直面する課題

9.7. 独自の金属3Dプリンティング技術を使用する部品製造業者

9.8. 社内部品製造のための金属AM企業

9.9. 社内部品製造のための金属AM企業(II)

9.10. 社内部品製造のための金属AM企業(III)

10. 金属積層造形の予測

10.1. 予測手法

10.2. 予測で使用される技術セグメンテーションの説明

10.3. 金属積層造形の予測 2025-2035

10.4. 金属3Dプリンターの設置台数予測 2025-2035:技術別

10.5. 金属3Dプリンティングハードウェア予測 2025-2035:技術別

10.6. 金属3Dプリンティングハードウェア予測 2025-2035:技術別(II)

10.7. 金属3Dプリンティング材料予測 2025-2035:原料別

10.8. 金属積層造形材料予測 2025-2035:技術別

10.9. 金属積層造形材料予測 2025-2035:技術別(II)

10.10. 金属積層造形材料予測 2025-2035:合金別

10.11. 金属積層造形材料予測 2025-2035:合金別(II)

11. 企業プロフィール

11.1.1. 3Dシステムズ

11.1.2. 3DEO

11.1.3. 3Tアディティブマニュファクチャリング

11.1.4. 6K

11.1.5. 6Kアディティブ(更新)

11.1.6. アコニティ3D

11.1.7. ADDere(MWES)

11.1.8. アディラン

11.1.9. アディティブ・インダストリーズ

11.1.10. アディティブ・インダストリーズb.v.

11.1.11. アドマテック・ヨーロッパBV

11.1.12. エアロシント

11.1.13. AIM3D

11.1.14. ATIパウダー・メタルズ

11.1.15. アビメタル・アディティブ

11.1.16. BeAMマシン

11.1.17. カーペンター

11.1.18. チロン

11.1.19. シトリン・インフォマティクス

11.1.20. クックソン・プレシャス・メタルズ

11.1.21. デスクトップ・メタル

11.1.22. デジタル・アロイズ(現在は閉鎖)

11.1.23. DMG森精機(アディティブマニュファクチャリング部門)

11.1.24. エレメンタム3D

11.1.25. EOS

11.1.26. エクイスポールズ

11.1.27. エクサドン

11.1.28. エクスワン

11.1.29. エクスポネンシャル・テクノロジーズ

11.1.30. フォームアロイ

11.1.31. ファウンドリ・ラボ

11.1.32. フラウンホーファーIKTS

11.1.33. ガンマ・アロイズ

11.1.34. GEアディティブ

11.1.35. ゲフェルテック

11.1.36. GHインダクション(3Dインダクター)

11.1.37. ギャランティード

11.1.38. H.C.スターク

11.1.39. ヘッドメイド・マテリアルズ

11.1.40. ホロ

11.1.41. ホーガナス(デジタル・メタルを含む)

11.1.42. インステック

11.1.43. マントル

11.1.44. マークフォージド

11.1.45. マークフォージド(更新)

11.1.46. マテリアライズ

11.1.47. MELDマニュファクチャリング

11.1.48. メルティオ

11.1.49. メルティオ(更新)

11.1.50. メタルム3D

11.1.51. メタリシス(更新)

11.1.52. メタリシス(完全プロフィール)

11.1.53. メットシェイプ

11.1.54. MX3D

11.1.55. ナノAL

11.1.56. ナノe

11.1.57. ノルスク・チタニウム

11.1.58. ワン・クリック・メタル

11.1.59. オプトメック

11.1.60. オプトメック(更新)

11.1.61. オプトメック(更新)

11.1.62. フェーズシフト・テクノロジーズ

11.1.63. プリマ・アディティブ

11.1.64. ラピディア

11.1.65. レニショー

11.1.66. リコー3D

11.1.67. サフィナ

11.1.68. サイアキー

11.1.69. セウラ・テクノロジーズ

11.1.70. SLMソリューションズ

11.1.71. SPEE3D(バックグラウンド)

11.1.72. SPEE3D(完全プロフィール)

11.1.73. タニオビス

11.1.74. ティトミック

11.1.75. トリトン・テクノロジーズ

11.1.76. トゥルンプ

11.1.77. ユニフォーミティ・ラボズ

11.1.78. ValCUN(完全プロフィール)

11.1.79. ValCUN(更新)

11.1.80. Velo3D(完全プロフィール)

11.1.81. Velo3D(更新)

11.1.82. Velo3D(更新)

11.1.83. WAAM3D(完全プロフィール)

11.1.84. WAAM3D(更新)

11.1.85. ゼロックス(完全プロフィール)

11.1.86. ゼロックス・エレメックス(ADDiTECに買収)

11.1.87. 西安ブライト・レーザー・テクノロジー

11.1.88. XJet

11.1.89. Z3DLAB

12. 付録

12.1. 金属積層造形の予測 2025-2035

12.2. 金属3Dプリンターの設置台数予測 2025-2035:技術別

12.3. 金属3Dプリンティングハードウェア予測 2025-2035:技術別

12.4. 金属3Dプリンティング材料予測 2025-2035:原料別

12.5. 金属積層造形材料予測 2025-2035:技術別(質量)

12.6. 金属積層造形材料予測 2025-2035:技術別(収益)

12.7. 金属積層造形材料予測 2025-2035:合金別(質量)

12.8. 金属積層造形材料予測 2025-2035:合金別(収益)

Summary

Metal 3D printing technology benchmarking including powder bed fusion, directed energy deposition, binder jetting, etc. 10-year granular market forecasts for AM hardware and materials. Key player analysis and market landscape.

After initial commercialization in the 1990s, metal additive manufacturing (also known as metal 3D printing) has witnessed a flurry of interest in the past decade. This time period has witnessed numerous industry-shifting events - from the COVID-19 pandemic to the rise and fall of hyped metal 3D printing startups, the ascent of the Chinese additive manufacturing market, and the continued emergence of novel metal AM technologies. There is no doubt that the metal 3D printing industry is dynamic - a market worth monitoring even in a more challenging macroeconomic environment.

This comprehensive technical report from IDTechEx gives a detailed status and outlook for the industry. Built upon IDTechEx's history in the market and large number of primary interviews, this report provides an unbiased forecast for the market.

Granular forecasts and detailed player profiles

This report provides granular 10-year market forecasts for the industry. The demand for metal printing hardware and metal 3D printing materials in the next decade is quantified. Targeted quantitative analysis is given for printer technologies and materials, broken down into 9 technology segments and 9 materials segments.

These forecasts, generated by IDTechEx analysts, go far beyond what is publicly available and is based upon an extensive number of primary interviews, providing the most important information to the reader. Over 100 company profiles are included as part of this report; this includes key OEMs, disruptive start-ups, incumbent powder providers, and emerging material companies.

Benchmarking the competitive printer processes

The proposed advantages to metal additive manufacturing are numerous with design freedom, local versatile manufacturing, potential cost savings, shortened manufacturing times, and much more.

To exploit this there is an ever-expanding family of printer processes using a wide number of material feedstocks. A common tactic for new entrants is to invent new terms for their technology to differentiate from the competition. Some of these are unique but most are aligned with existing processes, introducing only subtle variations.

This report cuts through this marketing and provides accessible impartial categorization for the industry. The reality is that every process must compromise on something, be it the rate, price, precision, size, material compatibility, or more. IDTechEx provides critical benchmarking studies of these processes: an essential process for identifying gaps in the market and end-use applications.

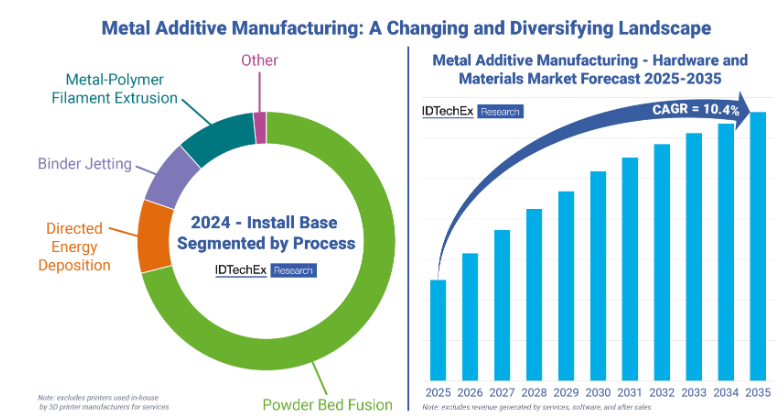

There is also the learning curve to be considered. As with any new (primarily) B2B technology with a large price tag, it will take time for end-users to have confidence in the process and value-add to warrant the investment. Powder bed fusion processes (DMLS/SLM and EBM) have been commercial for the longest time, which results in this technology underpinning most installations. However, the next generation of technologies are gaining more traction, so within the next decade, a more diverse installation base will be observed.

There are some overarching trends for new entrants as they try to find gaps in the market. Low-cost variants, printers pushing the size extremes from micro to very large scales, faster rates, and those exploiting alternative forms of feedstocks are all rapidly emerging and assessed.

Expanding material portfolio, capacity, and competition

IDTechEx forecast that the majority of annual revenue will come from material demand rather than printer sales and installation. Every printer process and application have different material requirements, throughput rates, and alloy demands.

There is a large amount of movement in this industry with notable acquisitions, capacity expansions, improved atomization processes, new materials, and cost reductions. Players are introducing material portfolios bespoke for additive manufacturing from well-known structural alloys to advanced options such as MMCs, high entropy alloys, and amorphous alloys.

Given the variation across this industry, there are very different forecasts when considering cost and volume; titanium powder will be the most significant which is again evident from the market dynamics of expansions, investments, vertical integration and exploring new avenues such as the use of scrap feedstocks.

Key markets for metal additive manufacturing, including aerospace and healthcare

Metal additive manufacturing has been used for prototypes, tooling, replacement parts, and small to large manufacturing. There are multiple sectors in which this emerging technology is gaining significant uptake, including oil & gas, jewelry, and building & construction. The growth and adoption have all been in high-value industry verticals, and the long-term future looks very optimistic.

However, in this more uncertain economic and trade environment, there are questions about the future of metal additive manufacturing. On the one hand, the constant discussion of tariffs has generally raised interest in domestic, distributed manufacturing operations, which metal additive manufacturing has the potential to serve as a key tool in solving supply chain issues. On the other hand, reluctance to invest in new technologies like additive manufacturing may impact end-user adoption during this rapidly changing economic landscape. This report analyzes the many trends and global market factors impacting metal additive manufacturing within the decade.

Key questions that are answered in this report

This report provides the following information on metal additive manufacturing:

Technology trends & manufacturer analysis

Market Forecasts & Analysis:

Table of Contents1. EXECUTIVE SUMMARY

1.1. Overview of 3D printing processes

1.2. Drivers and restraints of growth for 3D printing

1.3. Metal additive manufacturing: Technology overview

1.4. Overview of metal 3D printing technologies

1.5. Industry trend: The rise of the Chinese metal additive manufacturing market

1.6. Industry trend: Tariffs, trade wars, and reshoring

1.7. Key technology trends in metal additive manufacturing

1.8. Key technology trends in metal additive manufacturing

1.9. Metal additive manufacturing investment overview for 2024

1.10. The importance of services within the metal 3D printing market

1.11. Metal additive manufacturing forecast 2025-2035

1.12. Explanation of technology segmentation used in forecast

1.13. Metal additive manufacturing - evolution of technology market share

1.14. Metal 3D printing hardware forecast 2025-2035: Segmented by technology

1.15. Metal 3D printing hardware forecast 2025-2035: Segmented by technology (II)

1.16. Metal additive manufacturing materials forecast 2025-2035 split by technology

1.17. Metal additive manufacturing materials forecast 2025-2035 split by technology (II)

1.18. Additive manufacturing metals - evolution of market share by alloy

1.19. Metal additive manufacturing materials forecast 2025-2035 split by alloy

1.20. Metal additive manufacturing materials forecast 2025-2035 split by alloy (II)

1.21. Company profiles

1.22. Access More With an IDTechEx Subscription

2. INTRODUCTION

2.1. Glossary: Common acronyms for reference

2.2. Scope of report

2.3. Overview of 3D printing processes

2.4. Material-process relationships

2.5. Why adopt 3D printing?

2.6. Timeline of 3D printing metals

2.7. Business models: Selling printers vs parts

2.8. Drivers and restraints of growth for 3D printing

3. METAL ADDITIVE MANUFACTURING MARKET ANALYSIS

3.1. Industry financials and evolution

3.1.1. Recent financial performance in the 3D printing industry

3.1.2. Macro-economic factors that influenced metal 3D printing in 2024: Interest rates

3.1.3. Macro-economic factors that influenced metal 3D printing in 2024: The European economy

3.1.4. Macro-economic factors influencing metal 3D printing: Tariffs, trade wars, and reshoring

3.1.5. Market shares in laser powder bed fusion hardware: Continued diversification

3.1.6. Metal additive manufacturing - evolution of technology market share

3.1.7. Additive manufacturing metals - evolution of market share by alloy

3.2. Financial and player activity in metal 3D printing

3.2.1. Metal additive manufacturing investment overview for 2024

3.2.2. Private funding in metal AM-related companies: 2021-2024

3.2.3. Private funding in Chinese metal AM companies 2024

3.2.4. Metal 3D printing private funding: 2023 vs 2024

3.2.5. Metal 3D printing private funding trends: 2023 vs 2024

3.2.6. Recent notable acquisitions in metal 3D printing

3.2.7. Acquisition spotlight: Nano Dimension acquires Desktop Metal and Markforged

3.2.8. Acquisition spotlight: Nano Dimension acquires Desktop Metal and Markforged (II)

3.2.9. 3D printing related companies going public: 2021-2024

3.2.10. Summary of entrances and exits in metal AM in 2024

3.2.11. Other metal 3D printing player updates

3.3. Industry trends and discussion in metal additive manufacturing

3.3.1. Trend: Affordable, cost-competitive metal 3D printers

3.3.2. Trend: Large-format LPBF printing

3.3.3. Trend: Sustainability in metal additive manufacturing materials

3.3.4. Trend: A resurgence of interest in electron beam melting (EBM)

3.3.5. The rise of the Chinese metal additive manufacturing market

3.3.6. Progress on metal binder jetting

3.3.7. The importance of services within the metal 3D printing market

4. METAL PRINTING PROCESSES

4.1. Established metal printing technologies

4.1.1. Powder bed fusion: Direct metal laser sintering (DMLS) or selective laser melting (SLM)

4.1.2. Powder bed fusion: Electron beam melting (EBM)

4.1.3. Directed energy deposition: Powder (or blown powder)

4.1.4. Directed energy deposition: Wire

4.1.5. Binder jetting: Metal binder jetting

4.1.6. Binder jetting: Sand binder jetting

4.1.7. Sheet lamination: Ultrasonic additive manufacturing (UAM)

4.2. Emerging metal printing technologies

4.2.1. Emerging 3D printing processes: Overview

4.2.2. Extrusion: Metal-polymer filament (MPFE)

4.2.3. Extrusion: Metal-polymer pellet

4.2.4. Extrusion: Metal paste

4.2.5. Vat photopolymerization: Digital light processing (DLP)

4.2.6. Material jetting: Nanoparticle jetting (NPJ)

4.2.7. Material jetting: Liquid metal or magnetohydrodynamic deposition

4.2.8. Material jetting: Electrochemical deposition

4.2.9. Material jetting: Cold spray

4.2.10. Binder jetting advancements

4.2.11. Developments in PBF and DED: Energy sources

4.2.12. Developments in PBF and DED: Low-cost printers

4.2.13. Developments in PBF and DED: New technologies

4.2.14. Processes with a metal slurry feedstock

4.2.15. Alternative emerging DMLS/SLM variations

5. METAL PRINTERS: COMPARISON AND BENCHMARKING

5.1.1. Metal additive manufacturing: Technology overview

5.1.2. Benchmarking: Maximum build volume

5.1.3. Benchmarking: Build rate

5.1.4. Benchmarking: Z resolution

5.1.5. Benchmarking: XY Resolution

5.1.6. Benchmarking: Price vs build volume

5.1.7. Benchmarking: Price vs build rate

5.1.8. Benchmarking: Price vs Z resolution

5.1.9. Benchmarking: Build rate vs build volume

5.1.10. Benchmarking: Build rate vs Z resolution

5.1.11. Overview of metal 3D printing technologies

5.1.12. Maximums & minimums of metal 3D printing technologies

6. METAL MATERIALS FOR 3D PRINTING

6.1. Metal powders

6.1.1. Overview of metal AM feedstock options

6.1.2. Powder morphology specification

6.1.3. Established atomization technologies: Water, gas, and plasma atomization

6.1.4. Emerging powder production technology: Electrolysis

6.1.5. Powder morphology depends on atomization process

6.1.6. Evaluation of powder manufacturing techniques

6.1.7. Metal compatibility with printing technologies

6.1.8. Suppliers of metal powders for AM: Segmented by metal

6.1.9. Suppliers of metal powders for AM: Segmented by atomization process

6.1.10. Titanium powder - overview

6.1.11. Titanium powder - main players (I)

6.1.12. Titanium powder - main players (II)

6.1.13. Key material start-ups for metal additive manufacturing

6.1.14. Recycled titanium feedstocks

6.1.15. Metal powder bed fusion post processing

6.1.16. Barriers and limitations to using metal powders

6.2. Other metal feedstocks

6.2.1. Metal wire feedstocks

6.2.2. Metal-polymer filaments and pellets

6.2.3. Commercial example: Forward AM's Ultrafuse filaments

6.2.4. Metal-photopolymer resins

7. COMPATIBLE METAL MATERIALS

7.1.1. Alloys and material properties

7.1.2. Aluminum and aluminum alloys

7.1.3. Expanding the aluminum AM material portfolio

7.1.4. Copper and bronze

7.1.5. 3D printing with copper: A challenging material with many opportunities

7.1.6. Expanding the copper AM material portfolio

7.1.7. Current applications for copper 3D printing

7.1.8. Cobalt and alloys

7.1.9. Nickel alloy: Inconel 625

7.1.10. Nickel alloy: Inconel 718

7.1.11. Precious metals and alloys

7.1.12. Maraging steel 1.2709

7.1.13. 15-5PH stainless steel

7.1.14. 17-4PH stainless steel

7.1.15. 316L stainless steel

7.1.16. Titanium and alloys

7.1.17. AM of High Entropy Alloys

7.1.18. AM of amorphous alloys

7.1.19. Emerging aluminum alloys and metal-matrix composites (MMCs)

7.1.20. Multi-material solutions

7.1.21. Materials informatics for additive manufacturing materials

7.1.22. Materials informatics for additive manufacturing materials

7.1.23. Tungsten powder and nanoparticles

8. KEY APPLICATIONS OF METAL 3D PRINTING

8.1. Metal 3D printing in aviation, space, and defense

8.1.1. GE Aviation: LEAP fuel nozzles

8.1.2. GE Aviation: next-gen RISE engine

8.1.3. GE Aviation: Bleed air parts and turboprop engines

8.1.4. GE Aviation and Boeing 777X: GE9X engines

8.1.5. Boeing 787 dreamliner: Ti-6Al-4V structures

8.1.6. Boeing: gearboxes for Chinook helicopters

8.1.7. Boeing and Maxar Technologies: Satellites

8.1.8. Airbus and Eutelsat: Satellites

8.1.9. Autodesk and Airbus: Optimized partition wall

8.1.10. RUAG Space and Altair: Antenna mount

8.1.11. Hofmann: Oxygen supply tube

8.1.12. Relativity Space: Rockets

8.1.13. OEM AM Strategy - GE Aerospace and Colibrium Additive

8.1.14. OEM AM Strategy - Airbus

8.1.15. OEM AM Strategy - Boeing

8.1.16. OEM AM Strategy - Rolls-Royce

8.2. Metal 3D printing in medical and dental

8.2.1. Most popular 3D printing technologies in healthcare

8.2.2. 3D printing custom plates, implants, valves and stents

8.2.3. Metal materials for 3D printing in medical: Titanium alloy powders

8.2.4. Case study: Hip replacement revision surgery

8.2.5. Case study: Canine cranial plate in titanium

8.2.6. Case study: Implantable dental devices and prostheses

8.2.7. Case study: Mandibular reconstructive surgery

9. PART PRODUCTION SERVICES FOR METAL 3D PRINTING

9.1. What are 3D printing service bureaus?

9.2. What does a service bureau do?

9.3. Value proposition behind service bureaus

9.4. Design for additive manufacturing (DfAM)

9.5. Notable metal AM-focused service bureaus

9.6. Challenges facing service bureaus

9.7. Part manufacturers using proprietary metal 3D printing technology

9.8. Metal AM companies for in-house part production

9.9. Metal AM companies for in-house part production

9.10. Metal AM companies for in-house part production

10. METAL ADDITIVE MANUFACTURING FORECASTS

10.1. Forecast methodology

10.2. Explanation of technology segmentation used in forecast

10.3. Metal additive manufacturing forecast 2025-2035

10.4. Metal 3D printer installed base 2025-2035: Segmented by technology

10.5. Metal 3D printing hardware forecast 2025-2035: Segmented by technology

10.6. Metal 3D printing hardware forecast 2025-2035: Segmented by technology (II)

10.7. Metal 3D printing material forecast 2025-2035: Segmented by feedstock type

10.8. Metal additive manufacturing materials forecast 2025-2035 split by technology

10.9. Metal additive manufacturing materials forecast 2025-2035 split by technology (II)

10.10. Metal additive manufacturing materials forecast 2025-2035 split by alloy

10.11. Metal additive manufacturing materials forecast 2025-2035 split by alloy (II)

11. COMPANY PROFILES

11.1.1. 3D Systems

11.1.2. 3DEO

11.1.3. 3T Additive Manufacturing

11.1.4. 6K

11.1.5. 6K Additive (Update)

11.1.6. Aconity3D

11.1.7. ADDere (MWES)

11.1.8. Addilan

11.1.9. Additive Industries

11.1.10. Additive Industries b.v.

11.1.11. Admatec Europe BV

11.1.12. Aerosint

11.1.13. AIM3D

11.1.14. ATI Powder Metals

11.1.15. Avimetal Additive

11.1.16. BeAM Machines

11.1.17. Carpenter

11.1.18. Chiron

11.1.19. Citrine Informatics

11.1.20. Cookson Precious Metals

11.1.21. Desktop Metal

11.1.22. Digital Alloys (now defunct)

11.1.23. DMG Mori (Additive Manufacturing division)

11.1.24. Elementum 3D

11.1.25. EOS

11.1.26. Equispheres

11.1.27. Exaddon

11.1.28. ExOne

11.1.29. Exponential Technologies

11.1.30. FormAlloy

11.1.31. Foundry Lab

11.1.32. Fraunhofer IKTS

11.1.33. Gamma Alloys

11.1.34. GE Additive

11.1.35. Gefertec

11.1.36. GH Induction (3D Inductors)

11.1.37. Guaranteed

11.1.38. H. C. Starck

11.1.39. Headmade Materials

11.1.40. Holo

11.1.41. Höganäs (including Digital Metal)

11.1.42. InssTek

11.1.43. Mantle

11.1.44. Markforged

11.1.45. Markforged (Update)

11.1.46. Materialise

11.1.47. MELD Manufacturing

11.1.48. Meltio

11.1.49. Meltio (Update)

11.1.50. Metallum3D

11.1.51. Metalysis (Update)

11.1.52. Metalysis (Full Profile)

11.1.53. MetShape

11.1.54. MX3D

11.1.55. NanoAL

11.1.56. Nanoe

11.1.57. Norsk Titanium

11.1.58. One Click Metal

11.1.59. Optomec

11.1.60. Optomec (Update)

11.1.61. Optomec (Update)

11.1.62. Phaseshift Technologies

11.1.63. Prima Additive

11.1.64. Rapidia

11.1.65. Renishaw

11.1.66. Ricoh 3D

11.1.67. SAFINA

11.1.68. Sciaky

11.1.69. Seurat Technologies

11.1.70. SLM Solutions

11.1.71. SPEE3D (background)

11.1.72. SPEE3D (full profile)

11.1.73. TANIOBIS

11.1.74. Titomic

11.1.75. Tritone Technologies

11.1.76. TRUMPF

11.1.77. Uniformity Labs

11.1.78. ValCUN (full profile)

11.1.79. ValCUN (update)

11.1.80. Velo3D (full profile)

11.1.81. Velo3D (update)

11.1.82. Velo3D (update)

11.1.83. WAAM3D (full profile)

11.1.84. WAAM3D (update)

11.1.85. Xerox (Full profile)

11.1.86. Xerox ElemX Acquired by ADDiTEC (update)

11.1.87. Xi'an Bright Laser Technology

11.1.88. XJet

11.1.89. Z3DLAB

12. APPENDIX

12.1. Metal additive manufacturing forecast 2025-2035

12.2. Metal 3D printer installed base 2025-2035: Segmented by technology

12.3. Metal 3D printing hardware forecast 2025-2035: Segmented by technology

12.4. Metal 3D printing material forecast 2025-2035: Segmented by feedstock type

12.5. Metal additive manufacturing materials forecast 2025-2035 split by technology - mass

12.6. Metal additive manufacturing materials forecast 2025-2035 split by technology - revenue

12.7. Metal additive manufacturing materials forecast 2025-2035 split by alloy - mass

12.8. Metal additive manufacturing materials forecast 2025-2035 split by alloy - revenue

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(産業機械)の最新刊レポート

IDTechEx社の 3D印刷 - 3D Printing分野 での最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|